AC4410 - Dixon's Carphone Financial Analysis Report 2014-2018

VerifiedAdded on 2023/04/21

|13

|2592

|331

Report

AI Summary

This assignment provides a financial analysis of Dixon's Carphone Plc. from 2014 to 2018, utilizing ratio analysis to assess the company's performance in terms of liquidity, profitability, and gearing. The analysis includes calculations and interpretations of key financial ratios such as gearing ratio, interest coverage ratio, return on capital employed, gross profit margin, operating margin ratio, current ratio, and quick ratio. The report reveals trends in the company's financial health, highlighting a decrease in gearing, an increase in interest coverage, fluctuations in return on capital employed and gross profit margin, a decline in operating margin, and inconsistent liquidity positions. The conclusion emphasizes the importance of maintaining a sound liquidity position and reducing operating expenses while acknowledging the company's efforts to reduce debt and leverage its product portfolio for revenue growth.

Running head: ACCOUNTS AND FINANCE

Dixon’s Carphone

Name of the Student:

Name of the University:

Author’s Note:

Dixon’s Carphone

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1DIXONS CARPHONE

Executive Summary

The aim of the assignment is to conduct a financial analysis on the Dixon’s Carphone

Company using the financial information presented by the company for the trend period

analysed for the company from the year 2014-2018. The application of ratio analysis was

applied in the analysis of the Dixons Carphone Limited Company and the relevant

performance of the company in terms of liquidity, profitability and gearing ratio for the

company was taken into consideration for the assignment.

Executive Summary

The aim of the assignment is to conduct a financial analysis on the Dixon’s Carphone

Company using the financial information presented by the company for the trend period

analysed for the company from the year 2014-2018. The application of ratio analysis was

applied in the analysis of the Dixons Carphone Limited Company and the relevant

performance of the company in terms of liquidity, profitability and gearing ratio for the

company was taken into consideration for the assignment.

2DIXONS CARPHONE

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Ratio Analysis........................................................................................................................3

Calculations............................................................................................................................4

Gearing/Capital Structure Ratio.........................................................................................4

Profitability Ratio...............................................................................................................5

Liquidity Ratio...................................................................................................................6

Conclusion..................................................................................................................................8

Bibliography...............................................................................................................................9

Appendix..................................................................................................................................11

Table of Contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Ratio Analysis........................................................................................................................3

Calculations............................................................................................................................4

Gearing/Capital Structure Ratio.........................................................................................4

Profitability Ratio...............................................................................................................5

Liquidity Ratio...................................................................................................................6

Conclusion..................................................................................................................................8

Bibliography...............................................................................................................................9

Appendix..................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3DIXONS CARPHONE

Introduction

The Dixon Carphone Plc. is a multinational electrical and telecommunication retailer

and services company which is headquartered in the London. The company primarily has its

operations in the Consumer Electronics Industry and has its presence globally. The company

has its presence in a variety of distinct marketplaces such as mobile phones, other types of

consumer electronic products and various other types of business services. The operations of

the company are usually carried on under various brands in the United Kingdom, Ireland and

mainland European region. Curry’s, PC World, Carphone Warehouse are some of the

common brands under which the company usually carries on their operating activities. The

company has a good employee base where around 43,000 employees directly work under the

company. The company is listed in the London Stock Exchange and is also a part of the

FTSE 250 Index. The future prospect of the company is dependent on the various brands

under which the operations of the company is performed and the profitability generated from

the same (Shouman, El Shenawy and Khattab 2016). There are various global business and

macro-economic factors, which plays a significant role in the development of the company

(Vogel 2014).

Discussion

Ratio Analysis

The ratio analysis of the company is performed in order to analyse the performance of

the company. The ratio analysis is quantitative analysis tool used for analysing the financial

performance of the company over the period of time. The application of the ratio analysis

help in understanding the trend of the financial performance of the company. The key benefit

of the ratio analysis is that it takes into account the financial data by indicating the financial

performance of the company and indicates the profitability, liquidity position and the capital

Introduction

The Dixon Carphone Plc. is a multinational electrical and telecommunication retailer

and services company which is headquartered in the London. The company primarily has its

operations in the Consumer Electronics Industry and has its presence globally. The company

has its presence in a variety of distinct marketplaces such as mobile phones, other types of

consumer electronic products and various other types of business services. The operations of

the company are usually carried on under various brands in the United Kingdom, Ireland and

mainland European region. Curry’s, PC World, Carphone Warehouse are some of the

common brands under which the company usually carries on their operating activities. The

company has a good employee base where around 43,000 employees directly work under the

company. The company is listed in the London Stock Exchange and is also a part of the

FTSE 250 Index. The future prospect of the company is dependent on the various brands

under which the operations of the company is performed and the profitability generated from

the same (Shouman, El Shenawy and Khattab 2016). There are various global business and

macro-economic factors, which plays a significant role in the development of the company

(Vogel 2014).

Discussion

Ratio Analysis

The ratio analysis of the company is performed in order to analyse the performance of

the company. The ratio analysis is quantitative analysis tool used for analysing the financial

performance of the company over the period of time. The application of the ratio analysis

help in understanding the trend of the financial performance of the company. The key benefit

of the ratio analysis is that it takes into account the financial data by indicating the financial

performance of the company and indicates the profitability, liquidity position and the capital

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4DIXONS CARPHONE

structure of the company (Cucchiella, D’Adamo and Gastaldi 2015). The inclusion of

financial data in the form of ratio helps the potential users of the data for the purpose of

understanding and comparison of various kinds of data by the company. The limitation of the

ratio analysis is that the same does not incorporate the various fundamental aspects of the

company during the financial analysis of the company. Companies may easily manipulate the

data at the year end to make the ratio more attractive for the potential investors and financial

information users (Nesticò and Pipolo 2015).

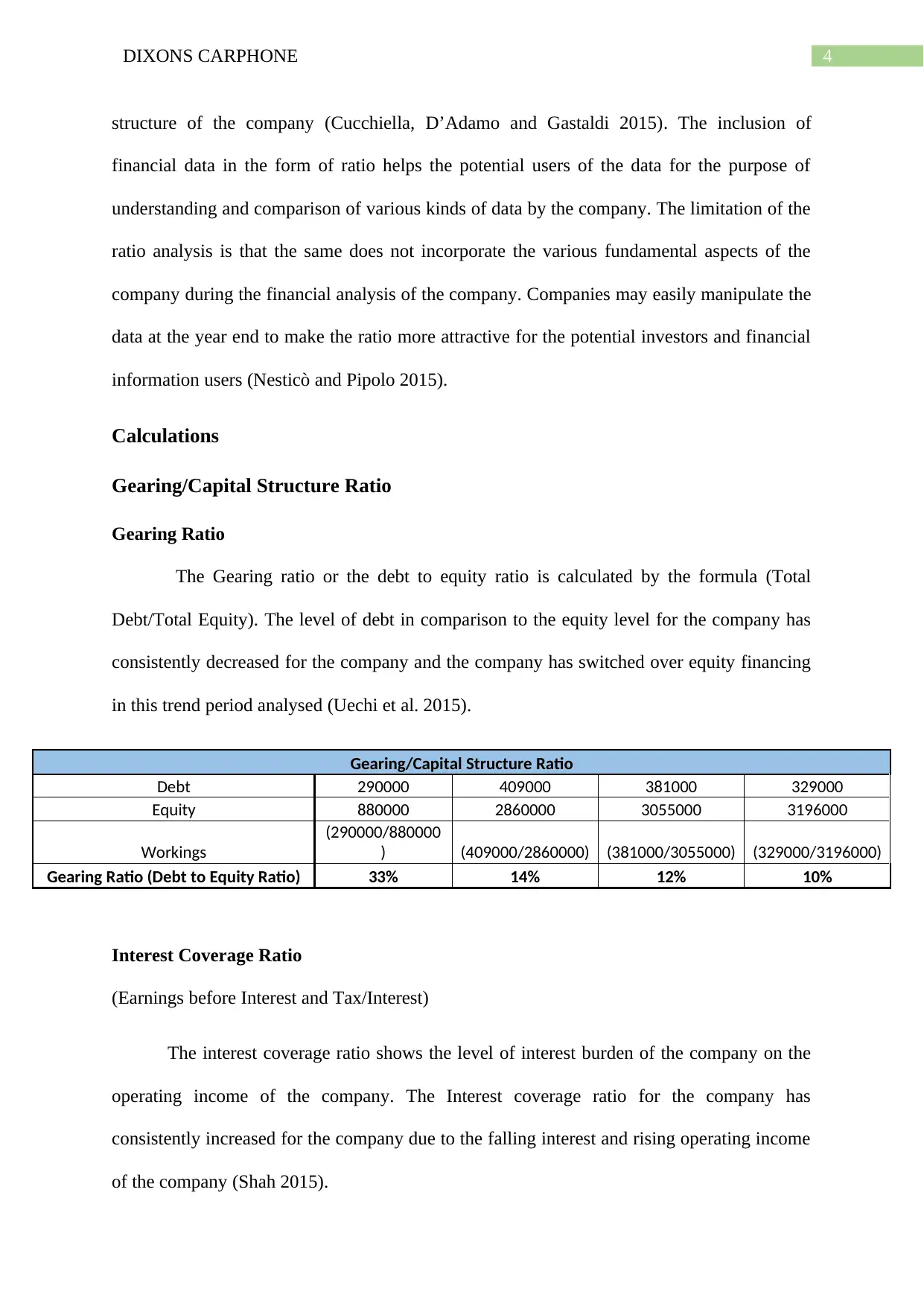

Calculations

Gearing/Capital Structure Ratio

Gearing Ratio

The Gearing ratio or the debt to equity ratio is calculated by the formula (Total

Debt/Total Equity). The level of debt in comparison to the equity level for the company has

consistently decreased for the company and the company has switched over equity financing

in this trend period analysed (Uechi et al. 2015).

Gearing/Capital Structure Ratio

Debt 290000 409000 381000 329000

Equity 880000 2860000 3055000 3196000

Workings

(290000/880000

) (409000/2860000) (381000/3055000) (329000/3196000)

Gearing Ratio (Debt to Equity Ratio) 33% 14% 12% 10%

Interest Coverage Ratio

(Earnings before Interest and Tax/Interest)

The interest coverage ratio shows the level of interest burden of the company on the

operating income of the company. The Interest coverage ratio for the company has

consistently increased for the company due to the falling interest and rising operating income

of the company (Shah 2015).

structure of the company (Cucchiella, D’Adamo and Gastaldi 2015). The inclusion of

financial data in the form of ratio helps the potential users of the data for the purpose of

understanding and comparison of various kinds of data by the company. The limitation of the

ratio analysis is that the same does not incorporate the various fundamental aspects of the

company during the financial analysis of the company. Companies may easily manipulate the

data at the year end to make the ratio more attractive for the potential investors and financial

information users (Nesticò and Pipolo 2015).

Calculations

Gearing/Capital Structure Ratio

Gearing Ratio

The Gearing ratio or the debt to equity ratio is calculated by the formula (Total

Debt/Total Equity). The level of debt in comparison to the equity level for the company has

consistently decreased for the company and the company has switched over equity financing

in this trend period analysed (Uechi et al. 2015).

Gearing/Capital Structure Ratio

Debt 290000 409000 381000 329000

Equity 880000 2860000 3055000 3196000

Workings

(290000/880000

) (409000/2860000) (381000/3055000) (329000/3196000)

Gearing Ratio (Debt to Equity Ratio) 33% 14% 12% 10%

Interest Coverage Ratio

(Earnings before Interest and Tax/Interest)

The interest coverage ratio shows the level of interest burden of the company on the

operating income of the company. The Interest coverage ratio for the company has

consistently increased for the company due to the falling interest and rising operating income

of the company (Shah 2015).

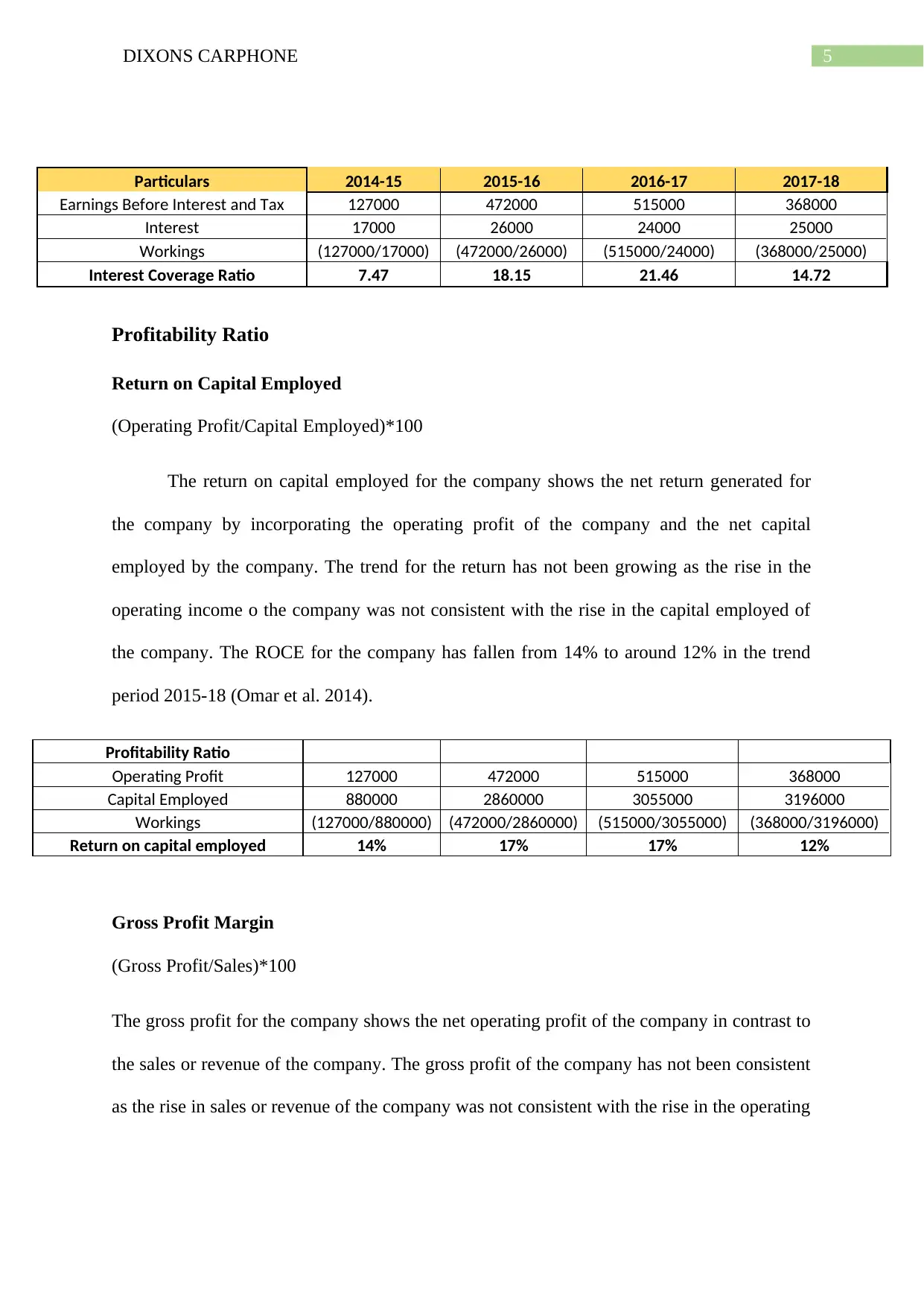

5DIXONS CARPHONE

Particulars 2014-15 2015-16 2016-17 2017-18

Earnings Before Interest and Tax 127000 472000 515000 368000

Interest 17000 26000 24000 25000

Workings (127000/17000) (472000/26000) (515000/24000) (368000/25000)

Interest Coverage Ratio 7.47 18.15 21.46 14.72

Profitability Ratio

Return on Capital Employed

(Operating Profit/Capital Employed)*100

The return on capital employed for the company shows the net return generated for

the company by incorporating the operating profit of the company and the net capital

employed by the company. The trend for the return has not been growing as the rise in the

operating income o the company was not consistent with the rise in the capital employed of

the company. The ROCE for the company has fallen from 14% to around 12% in the trend

period 2015-18 (Omar et al. 2014).

Profitability Ratio

Operating Profit 127000 472000 515000 368000

Capital Employed 880000 2860000 3055000 3196000

Workings (127000/880000) (472000/2860000) (515000/3055000) (368000/3196000)

Return on capital employed 14% 17% 17% 12%

Gross Profit Margin

(Gross Profit/Sales)*100

The gross profit for the company shows the net operating profit of the company in contrast to

the sales or revenue of the company. The gross profit of the company has not been consistent

as the rise in sales or revenue of the company was not consistent with the rise in the operating

Particulars 2014-15 2015-16 2016-17 2017-18

Earnings Before Interest and Tax 127000 472000 515000 368000

Interest 17000 26000 24000 25000

Workings (127000/17000) (472000/26000) (515000/24000) (368000/25000)

Interest Coverage Ratio 7.47 18.15 21.46 14.72

Profitability Ratio

Return on Capital Employed

(Operating Profit/Capital Employed)*100

The return on capital employed for the company shows the net return generated for

the company by incorporating the operating profit of the company and the net capital

employed by the company. The trend for the return has not been growing as the rise in the

operating income o the company was not consistent with the rise in the capital employed of

the company. The ROCE for the company has fallen from 14% to around 12% in the trend

period 2015-18 (Omar et al. 2014).

Profitability Ratio

Operating Profit 127000 472000 515000 368000

Capital Employed 880000 2860000 3055000 3196000

Workings (127000/880000) (472000/2860000) (515000/3055000) (368000/3196000)

Return on capital employed 14% 17% 17% 12%

Gross Profit Margin

(Gross Profit/Sales)*100

The gross profit for the company shows the net operating profit of the company in contrast to

the sales or revenue of the company. The gross profit of the company has not been consistent

as the rise in sales or revenue of the company was not consistent with the rise in the operating

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

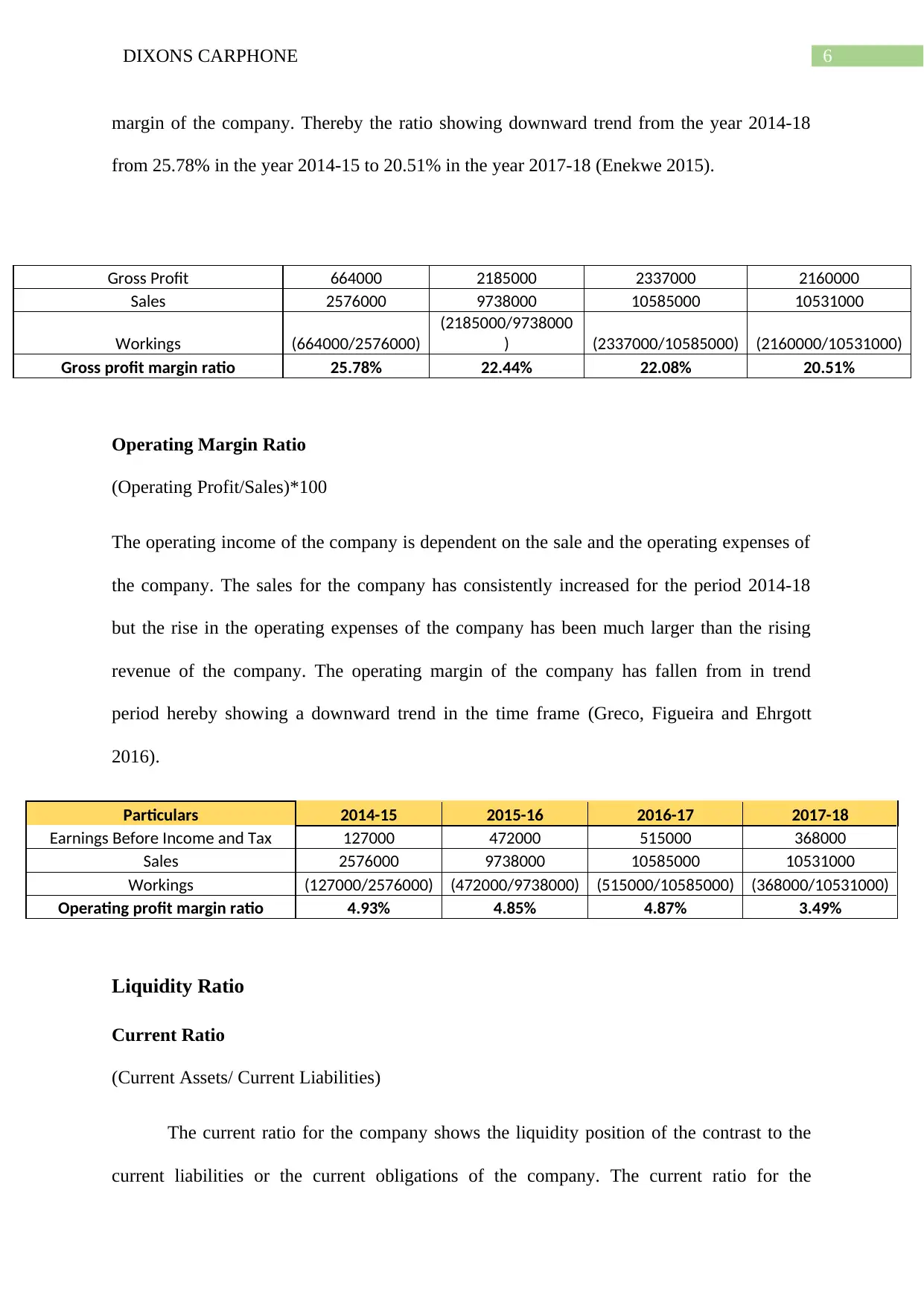

6DIXONS CARPHONE

margin of the company. Thereby the ratio showing downward trend from the year 2014-18

from 25.78% in the year 2014-15 to 20.51% in the year 2017-18 (Enekwe 2015).

Gross Profit 664000 2185000 2337000 2160000

Sales 2576000 9738000 10585000 10531000

Workings (664000/2576000)

(2185000/9738000

) (2337000/10585000) (2160000/10531000)

Gross profit margin ratio 25.78% 22.44% 22.08% 20.51%

Operating Margin Ratio

(Operating Profit/Sales)*100

The operating income of the company is dependent on the sale and the operating expenses of

the company. The sales for the company has consistently increased for the period 2014-18

but the rise in the operating expenses of the company has been much larger than the rising

revenue of the company. The operating margin of the company has fallen from in trend

period hereby showing a downward trend in the time frame (Greco, Figueira and Ehrgott

2016).

Particulars 2014-15 2015-16 2016-17 2017-18

Earnings Before Income and Tax 127000 472000 515000 368000

Sales 2576000 9738000 10585000 10531000

Workings (127000/2576000) (472000/9738000) (515000/10585000) (368000/10531000)

Operating profit margin ratio 4.93% 4.85% 4.87% 3.49%

Liquidity Ratio

Current Ratio

(Current Assets/ Current Liabilities)

The current ratio for the company shows the liquidity position of the contrast to the

current liabilities or the current obligations of the company. The current ratio for the

margin of the company. Thereby the ratio showing downward trend from the year 2014-18

from 25.78% in the year 2014-15 to 20.51% in the year 2017-18 (Enekwe 2015).

Gross Profit 664000 2185000 2337000 2160000

Sales 2576000 9738000 10585000 10531000

Workings (664000/2576000)

(2185000/9738000

) (2337000/10585000) (2160000/10531000)

Gross profit margin ratio 25.78% 22.44% 22.08% 20.51%

Operating Margin Ratio

(Operating Profit/Sales)*100

The operating income of the company is dependent on the sale and the operating expenses of

the company. The sales for the company has consistently increased for the period 2014-18

but the rise in the operating expenses of the company has been much larger than the rising

revenue of the company. The operating margin of the company has fallen from in trend

period hereby showing a downward trend in the time frame (Greco, Figueira and Ehrgott

2016).

Particulars 2014-15 2015-16 2016-17 2017-18

Earnings Before Income and Tax 127000 472000 515000 368000

Sales 2576000 9738000 10585000 10531000

Workings (127000/2576000) (472000/9738000) (515000/10585000) (368000/10531000)

Operating profit margin ratio 4.93% 4.85% 4.87% 3.49%

Liquidity Ratio

Current Ratio

(Current Assets/ Current Liabilities)

The current ratio for the company shows the liquidity position of the contrast to the

current liabilities or the current obligations of the company. The current ratio for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

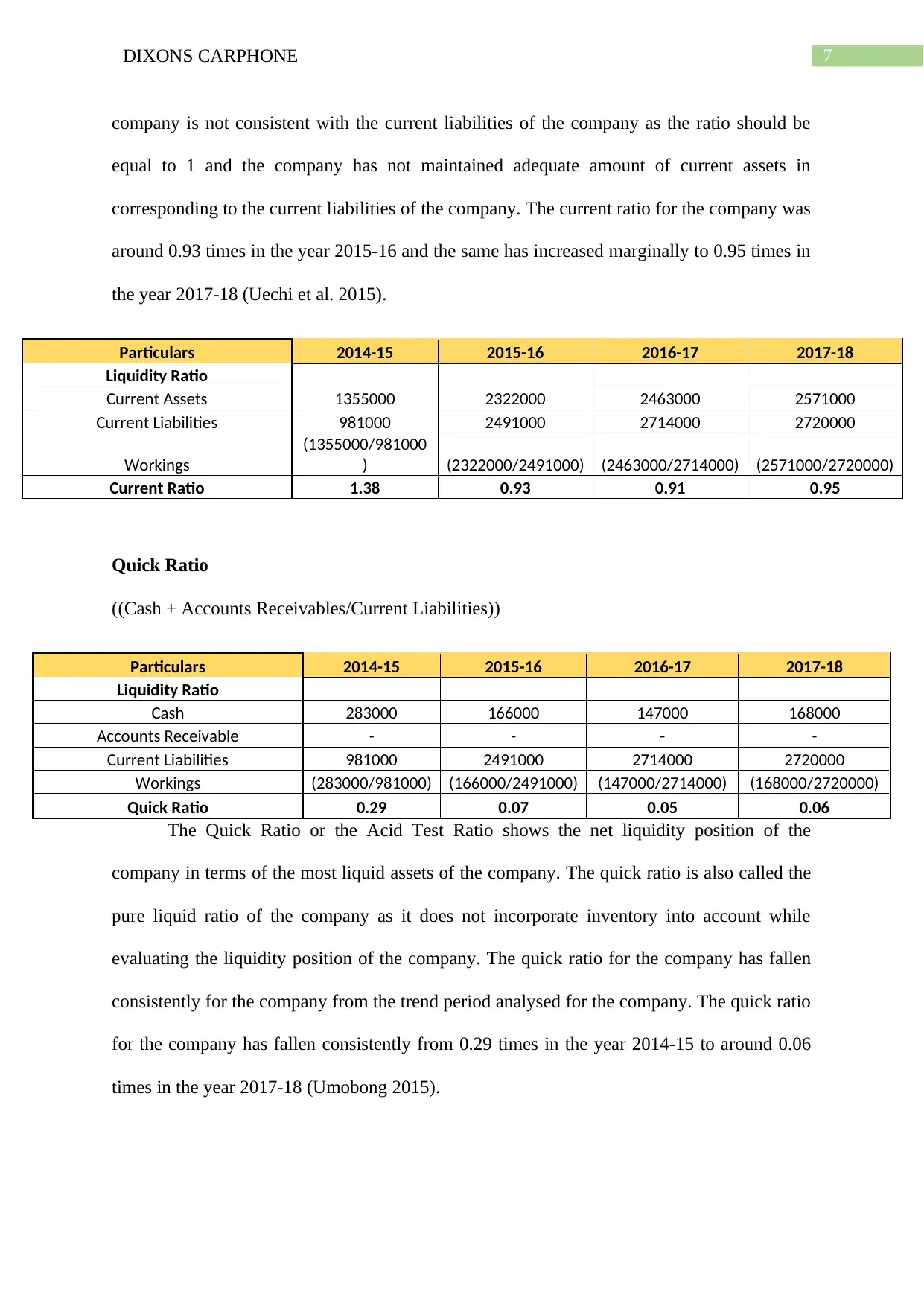

7DIXONS CARPHONE

company is not consistent with the current liabilities of the company as the ratio should be

equal to 1 and the company has not maintained adequate amount of current assets in

corresponding to the current liabilities of the company. The current ratio for the company was

around 0.93 times in the year 2015-16 and the same has increased marginally to 0.95 times in

the year 2017-18 (Uechi et al. 2015).

Particulars 2014-15 2015-16 2016-17 2017-18

Liquidity Ratio

Current Assets 1355000 2322000 2463000 2571000

Current Liabilities 981000 2491000 2714000 2720000

Workings

(1355000/981000

) (2322000/2491000) (2463000/2714000) (2571000/2720000)

Current Ratio 1.38 0.93 0.91 0.95

Quick Ratio

((Cash + Accounts Receivables/Current Liabilities))

Particulars 2014-15 2015-16 2016-17 2017-18

Liquidity Ratio

Cash 283000 166000 147000 168000

Accounts Receivable - - - -

Current Liabilities 981000 2491000 2714000 2720000

Workings (283000/981000) (166000/2491000) (147000/2714000) (168000/2720000)

Quick Ratio 0.29 0.07 0.05 0.06

The Quick Ratio or the Acid Test Ratio shows the net liquidity position of the

company in terms of the most liquid assets of the company. The quick ratio is also called the

pure liquid ratio of the company as it does not incorporate inventory into account while

evaluating the liquidity position of the company. The quick ratio for the company has fallen

consistently for the company from the trend period analysed for the company. The quick ratio

for the company has fallen consistently from 0.29 times in the year 2014-15 to around 0.06

times in the year 2017-18 (Umobong 2015).

company is not consistent with the current liabilities of the company as the ratio should be

equal to 1 and the company has not maintained adequate amount of current assets in

corresponding to the current liabilities of the company. The current ratio for the company was

around 0.93 times in the year 2015-16 and the same has increased marginally to 0.95 times in

the year 2017-18 (Uechi et al. 2015).

Particulars 2014-15 2015-16 2016-17 2017-18

Liquidity Ratio

Current Assets 1355000 2322000 2463000 2571000

Current Liabilities 981000 2491000 2714000 2720000

Workings

(1355000/981000

) (2322000/2491000) (2463000/2714000) (2571000/2720000)

Current Ratio 1.38 0.93 0.91 0.95

Quick Ratio

((Cash + Accounts Receivables/Current Liabilities))

Particulars 2014-15 2015-16 2016-17 2017-18

Liquidity Ratio

Cash 283000 166000 147000 168000

Accounts Receivable - - - -

Current Liabilities 981000 2491000 2714000 2720000

Workings (283000/981000) (166000/2491000) (147000/2714000) (168000/2720000)

Quick Ratio 0.29 0.07 0.05 0.06

The Quick Ratio or the Acid Test Ratio shows the net liquidity position of the

company in terms of the most liquid assets of the company. The quick ratio is also called the

pure liquid ratio of the company as it does not incorporate inventory into account while

evaluating the liquidity position of the company. The quick ratio for the company has fallen

consistently for the company from the trend period analysed for the company. The quick ratio

for the company has fallen consistently from 0.29 times in the year 2014-15 to around 0.06

times in the year 2017-18 (Umobong 2015).

8DIXONS CARPHONE

Conclusion

The financial analysis of the Dixon Carphone was evaluated for the trend period

2014-18 and the relevant financial data and the performance of the company was taken into

account for the trend period. The analysis of the company in the field of operating margin,

liquidity position of the company and the gearing or the debt structure of the company was

evaluated. The profitability ratio for the company has fallen consistently for the company and

the company should recognize various areas where it can reduce the operating expense so the

company thereby increasing the net gross margin of the company. It is also essential for the

company to maintain a sound liquidity position in the business so that the operations of the

company does not get hampered. However it is crucial to note that the company on the other

hand has also tried to reduce the debt of the company thereby reducing the financial risk of

the company. Dixons Carphone overall has a wide range of portfolio of products from where

the company can increase the revenue base for the company and examine the possibility of

reducing the operating costs for the company.

Conclusion

The financial analysis of the Dixon Carphone was evaluated for the trend period

2014-18 and the relevant financial data and the performance of the company was taken into

account for the trend period. The analysis of the company in the field of operating margin,

liquidity position of the company and the gearing or the debt structure of the company was

evaluated. The profitability ratio for the company has fallen consistently for the company and

the company should recognize various areas where it can reduce the operating expense so the

company thereby increasing the net gross margin of the company. It is also essential for the

company to maintain a sound liquidity position in the business so that the operations of the

company does not get hampered. However it is crucial to note that the company on the other

hand has also tried to reduce the debt of the company thereby reducing the financial risk of

the company. Dixons Carphone overall has a wide range of portfolio of products from where

the company can increase the revenue base for the company and examine the possibility of

reducing the operating costs for the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9DIXONS CARPHONE

Bibliography

Cucchiella, F., D’Adamo, I. and Gastaldi, M., 2015. Financial analysis for investment and

policy decisions in the renewable energy sector. Clean Technologies and Environmental

Policy, 17(4), pp.887-904.

Enekwe, C.I., 2015. The relationship between financial ratio analysis and corporate

profitability: a study of selected quoted oil and gas companies in Nigeria. European Journal

of Accounting, Auditing and Finance Research, 3(2), pp.17-34.

Greco, S., Figueira, J. and Ehrgott, M., 2016. Multiple criteria decision analysis. New York:

Springer.

Nesticò, A. and Pipolo, O., 2015. A protocol for sustainable building interventions: financial

analysis and environmental effects. International Journal of Business Intelligence and Data

Mining, 10(3), pp.199-212.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A

case examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), p.184.

Shah, M.B., 2015. A financial ratio analysis of Hindustan Unilever Limited

(HUL). RESEARCH HUB-International Multidisciplinary Research Journal (RHIMRJ), 2(5),

pp.1-5.

Shouman, E.R., El Shenawy, E.T. and Khattab, N.M., 2016. Market financial analysis and

cost performance for photovoltaic technology through international and national perspective

with case study for Egypt. Renewable and Sustainable Energy Reviews, 57, pp.540-549.

Bibliography

Cucchiella, F., D’Adamo, I. and Gastaldi, M., 2015. Financial analysis for investment and

policy decisions in the renewable energy sector. Clean Technologies and Environmental

Policy, 17(4), pp.887-904.

Enekwe, C.I., 2015. The relationship between financial ratio analysis and corporate

profitability: a study of selected quoted oil and gas companies in Nigeria. European Journal

of Accounting, Auditing and Finance Research, 3(2), pp.17-34.

Greco, S., Figueira, J. and Ehrgott, M., 2016. Multiple criteria decision analysis. New York:

Springer.

Nesticò, A. and Pipolo, O., 2015. A protocol for sustainable building interventions: financial

analysis and environmental effects. International Journal of Business Intelligence and Data

Mining, 10(3), pp.199-212.

Omar, N., Koya, R.K., Sanusi, Z.M. and Shafie, N.A., 2014. Financial statement fraud: A

case examination using Beneish Model and ratio analysis. International Journal of Trade,

Economics and Finance, 5(2), p.184.

Shah, M.B., 2015. A financial ratio analysis of Hindustan Unilever Limited

(HUL). RESEARCH HUB-International Multidisciplinary Research Journal (RHIMRJ), 2(5),

pp.1-5.

Shouman, E.R., El Shenawy, E.T. and Khattab, N.M., 2016. Market financial analysis and

cost performance for photovoltaic technology through international and national perspective

with case study for Egypt. Renewable and Sustainable Energy Reviews, 57, pp.540-549.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10DIXONS CARPHONE

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Umobong, A.A., 2015. Assessing the impact of liquidity and profitability ratios on growth of

profits in pharmaceutical firms in Nigeria. European Journal of Accounting, Auditing and

Finance Research, 3(10), pp.97-114.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Uechi, L., Akutsu, T., Stanley, H.E., Marcus, A.J. and Kenett, D.Y., 2015. Sector dominance

ratio analysis of financial markets. Physica A: Statistical Mechanics and its

Applications, 421, pp.488-509.

Umobong, A.A., 2015. Assessing the impact of liquidity and profitability ratios on growth of

profits in pharmaceutical firms in Nigeria. European Journal of Accounting, Auditing and

Finance Research, 3(10), pp.97-114.

Vogel, H.L., 2014. Entertainment industry economics: A guide for financial analysis.

Cambridge University Press.

11DIXONS CARPHONE

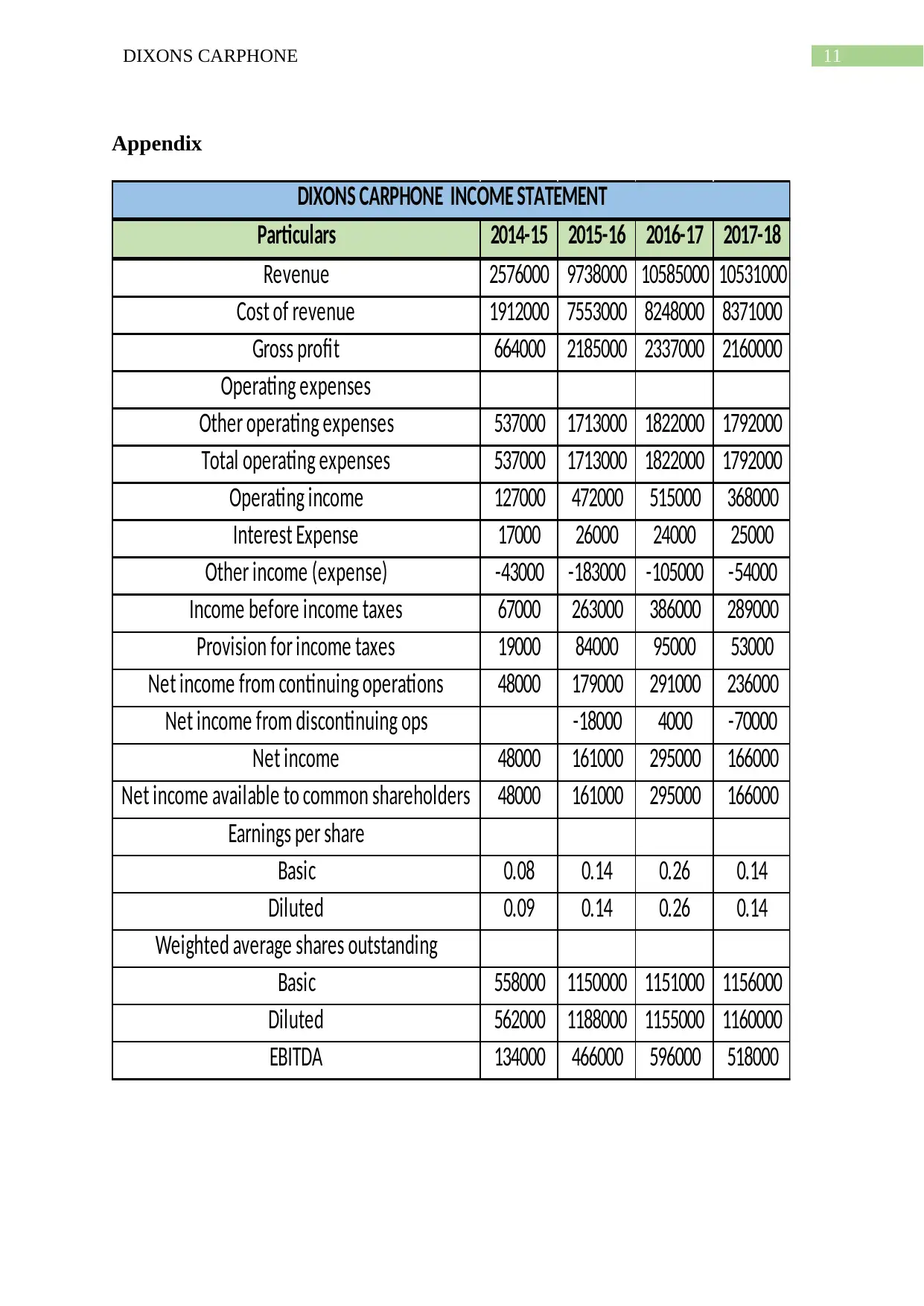

Appendix

Particulars 2014-15 2015-16 2016-17 2017-18

Revenue 2576000 9738000 10585000 10531000

Cost of revenue 1912000 7553000 8248000 8371000

Gross profit 664000 2185000 2337000 2160000

Operating expenses

Other operating expenses 537000 1713000 1822000 1792000

Total operating expenses 537000 1713000 1822000 1792000

Operating income 127000 472000 515000 368000

Interest Expense 17000 26000 24000 25000

Other income (expense) -43000 -183000 -105000 -54000

Income before income taxes 67000 263000 386000 289000

Provision for income taxes 19000 84000 95000 53000

Net income from continuing operations 48000 179000 291000 236000

Net income from discontinuing ops -18000 4000 -70000

Net income 48000 161000 295000 166000

Net income available to common shareholders 48000 161000 295000 166000

Earnings per share

Basic 0.08 0.14 0.26 0.14

Diluted 0.09 0.14 0.26 0.14

Weighted average shares outstanding

Basic 558000 1150000 1151000 1156000

Diluted 562000 1188000 1155000 1160000

EBITDA 134000 466000 596000 518000

DIXONS CARPHONE INCOME STATEMENT

Appendix

Particulars 2014-15 2015-16 2016-17 2017-18

Revenue 2576000 9738000 10585000 10531000

Cost of revenue 1912000 7553000 8248000 8371000

Gross profit 664000 2185000 2337000 2160000

Operating expenses

Other operating expenses 537000 1713000 1822000 1792000

Total operating expenses 537000 1713000 1822000 1792000

Operating income 127000 472000 515000 368000

Interest Expense 17000 26000 24000 25000

Other income (expense) -43000 -183000 -105000 -54000

Income before income taxes 67000 263000 386000 289000

Provision for income taxes 19000 84000 95000 53000

Net income from continuing operations 48000 179000 291000 236000

Net income from discontinuing ops -18000 4000 -70000

Net income 48000 161000 295000 166000

Net income available to common shareholders 48000 161000 295000 166000

Earnings per share

Basic 0.08 0.14 0.26 0.14

Diluted 0.09 0.14 0.26 0.14

Weighted average shares outstanding

Basic 558000 1150000 1151000 1156000

Diluted 562000 1188000 1155000 1160000

EBITDA 134000 466000 596000 518000

DIXONS CARPHONE INCOME STATEMENT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.