Comprehensive Corporate Reporting Analysis: Domino's Pizza Enterprises

VerifiedAdded on 2023/06/05

|13

|3099

|243

Report

AI Summary

This report provides a detailed analysis of the corporate reporting practices of Domino's Pizza Enterprises. It begins with an executive summary and an introduction to the company, highlighting its position as a leading pizza chain and franchisee. The report then delves into key aspects of corporate reporting, including the auditor's independence declaration, the independent auditor's report, and non-audit services performed. It examines auditor remuneration, the role and composition of the audit committee, and the independent auditor's report to shareholders. The analysis further reviews key audit matters, such as the valuation of goodwill, put options, and guarantees, and discusses the responsibilities of directors and management. The report also includes ratio analysis, material subsequent events, and an assessment of the effectiveness of material information, concluding with a comprehensive overview of the company's financial reporting practices and related audit procedures. References are also provided.

CORPORATE REPORTING 1

CORPORATE

REPORTING

CORPORATE

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE REPORTING 2

Executive summary:

The company chosen for review is Domino’s Pizza enterprises.

The report talks about the company, the independence of the auditors, the opinion expressed

by the auditor on its financial statements, the remuneration of the auditors, the difference

between the managements and auditors responsibilities etc (ASX, 2018).

Executive summary:

The company chosen for review is Domino’s Pizza enterprises.

The report talks about the company, the independence of the auditors, the opinion expressed

by the auditor on its financial statements, the remuneration of the auditors, the difference

between the managements and auditors responsibilities etc (ASX, 2018).

CORPORATE REPORTING 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE REPORTING 4

Contents

Introduction:...............................................................................................................................5

Auditor’s Independence Declaration:........................................................................................5

Independent auditor’s report:.....................................................................................................5

Non-Audit services performed by the Auditor:.........................................................................5

Auditors’ remuneration:.............................................................................................................6

Role, functions and composition of the Audit Committee:........................................................7

Independent Auditors report to the members (shareholders):....................................................8

Review all Key Audit Matters noted and the associated audit procedures:...............................8

Directors’ and Management’s responsibilities:..........................................................................9

Material subsequent events:.....................................................................................................10

Assessment of effectiveness of material information:.............................................................10

Under reporting and questions to be asked to auditor:.............................................................10

Conclusion:..............................................................................................................................10

References:...............................................................................................................................12

Contents

Introduction:...............................................................................................................................5

Auditor’s Independence Declaration:........................................................................................5

Independent auditor’s report:.....................................................................................................5

Non-Audit services performed by the Auditor:.........................................................................5

Auditors’ remuneration:.............................................................................................................6

Role, functions and composition of the Audit Committee:........................................................7

Independent Auditors report to the members (shareholders):....................................................8

Review all Key Audit Matters noted and the associated audit procedures:...............................8

Directors’ and Management’s responsibilities:..........................................................................9

Material subsequent events:.....................................................................................................10

Assessment of effectiveness of material information:.............................................................10

Under reporting and questions to be asked to auditor:.............................................................10

Conclusion:..............................................................................................................................10

References:...............................................................................................................................12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE REPORTING 5

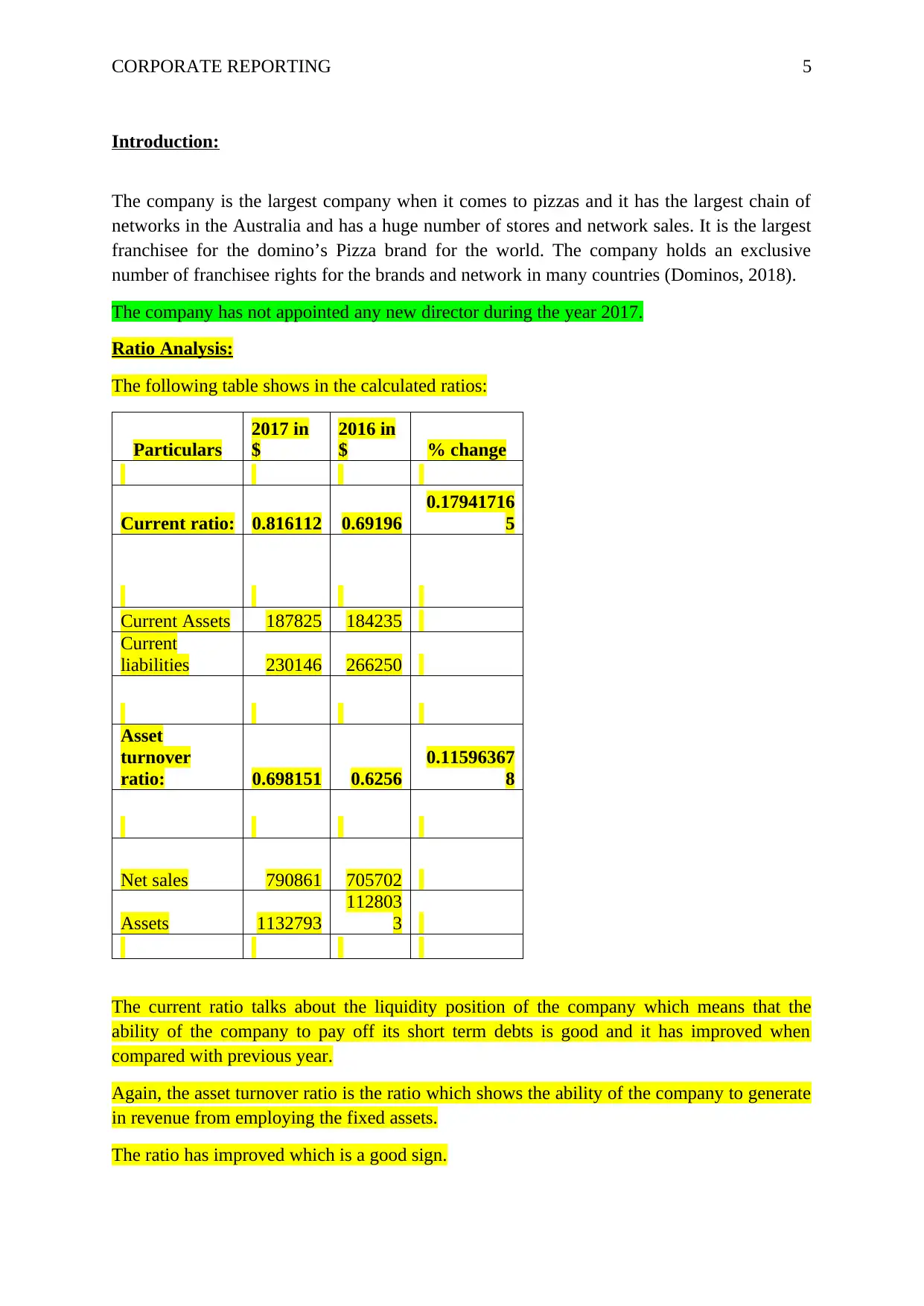

Introduction:

The company is the largest company when it comes to pizzas and it has the largest chain of

networks in the Australia and has a huge number of stores and network sales. It is the largest

franchisee for the domino’s Pizza brand for the world. The company holds an exclusive

number of franchisee rights for the brands and network in many countries (Dominos, 2018).

The company has not appointed any new director during the year 2017.

Ratio Analysis:

The following table shows in the calculated ratios:

Particulars

2017 in

$

2016 in

$ % change

Current ratio: 0.816112 0.69196

0.17941716

5

Current Assets 187825 184235

Current

liabilities 230146 266250

Asset

turnover

ratio: 0.698151 0.6256

0.11596367

8

Net sales 790861 705702

Assets 1132793

112803

3

The current ratio talks about the liquidity position of the company which means that the

ability of the company to pay off its short term debts is good and it has improved when

compared with previous year.

Again, the asset turnover ratio is the ratio which shows the ability of the company to generate

in revenue from employing the fixed assets.

The ratio has improved which is a good sign.

Introduction:

The company is the largest company when it comes to pizzas and it has the largest chain of

networks in the Australia and has a huge number of stores and network sales. It is the largest

franchisee for the domino’s Pizza brand for the world. The company holds an exclusive

number of franchisee rights for the brands and network in many countries (Dominos, 2018).

The company has not appointed any new director during the year 2017.

Ratio Analysis:

The following table shows in the calculated ratios:

Particulars

2017 in

$

2016 in

$ % change

Current ratio: 0.816112 0.69196

0.17941716

5

Current Assets 187825 184235

Current

liabilities 230146 266250

Asset

turnover

ratio: 0.698151 0.6256

0.11596367

8

Net sales 790861 705702

Assets 1132793

112803

3

The current ratio talks about the liquidity position of the company which means that the

ability of the company to pay off its short term debts is good and it has improved when

compared with previous year.

Again, the asset turnover ratio is the ratio which shows the ability of the company to generate

in revenue from employing the fixed assets.

The ratio has improved which is a good sign.

CORPORATE REPORTING 6

Auditor’s Independence Declaration:

As per the section 307C of the Corporations Act of the year 2001, the auditors specified the

following:

The various different requirements as have been laid down under the corporations Act

2001 has bene fulfilled

Also, any of the applicable code of the professional conduct has been duly complied

with.

Independent auditor’s report:

As per the section 307C of the Corporations Act of the year 2001, the auditors specified the

following:

The various different requirements as have been laid down under the corporations Act

2001 has bene fulfilled

Also, any of the applicable code of the professional conduct has been duly complied

with.

Non-Audit services performed by the Auditor:

In terms of the non-audit services, all of the services have been detailed down in the note 42

of the financial statements of the company. The directors that satisfied that all of the

provisions with relation with the non-audit services by the auditor are very much in line with

all of the general standards of the independence of the auditors that have been imposed in the

various different provisions of the Corporations Act, 2001. The directors are further of an

opinion that the following listed down services as contained in the financial statements are

not capable enough to compromise in the independence of the external auditor which is

somewhat based on the advice which has been received from the Audit Committee of the

company. And this is mainly due to the following listed reasons:

All of the non-audit services that are being provided by in by the auditors have been

duly reviewed and approved in order to make sure that none of it affects the integrity

and the objectivity of the auditor

The non-audit services being rendered are not capable enough to undermine in the

general principles of the independence of the auditor as have been laid down in the

ethics code. This includes in the reviewing or the auditing work of the auditor, acting

in the management or working as in the capacity of the decision making for the

company such as an advocate for the company or sharing in the economic risks and

rewards.

Non-audit services being rendered by the auditors:

Investigating accountants

Auditor’s Independence Declaration:

As per the section 307C of the Corporations Act of the year 2001, the auditors specified the

following:

The various different requirements as have been laid down under the corporations Act

2001 has bene fulfilled

Also, any of the applicable code of the professional conduct has been duly complied

with.

Independent auditor’s report:

As per the section 307C of the Corporations Act of the year 2001, the auditors specified the

following:

The various different requirements as have been laid down under the corporations Act

2001 has bene fulfilled

Also, any of the applicable code of the professional conduct has been duly complied

with.

Non-Audit services performed by the Auditor:

In terms of the non-audit services, all of the services have been detailed down in the note 42

of the financial statements of the company. The directors that satisfied that all of the

provisions with relation with the non-audit services by the auditor are very much in line with

all of the general standards of the independence of the auditors that have been imposed in the

various different provisions of the Corporations Act, 2001. The directors are further of an

opinion that the following listed down services as contained in the financial statements are

not capable enough to compromise in the independence of the external auditor which is

somewhat based on the advice which has been received from the Audit Committee of the

company. And this is mainly due to the following listed reasons:

All of the non-audit services that are being provided by in by the auditors have been

duly reviewed and approved in order to make sure that none of it affects the integrity

and the objectivity of the auditor

The non-audit services being rendered are not capable enough to undermine in the

general principles of the independence of the auditor as have been laid down in the

ethics code. This includes in the reviewing or the auditing work of the auditor, acting

in the management or working as in the capacity of the decision making for the

company such as an advocate for the company or sharing in the economic risks and

rewards.

Non-audit services being rendered by the auditors:

Investigating accountants

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE REPORTING 7

Other assurance services

Other advisory services

Due diligence

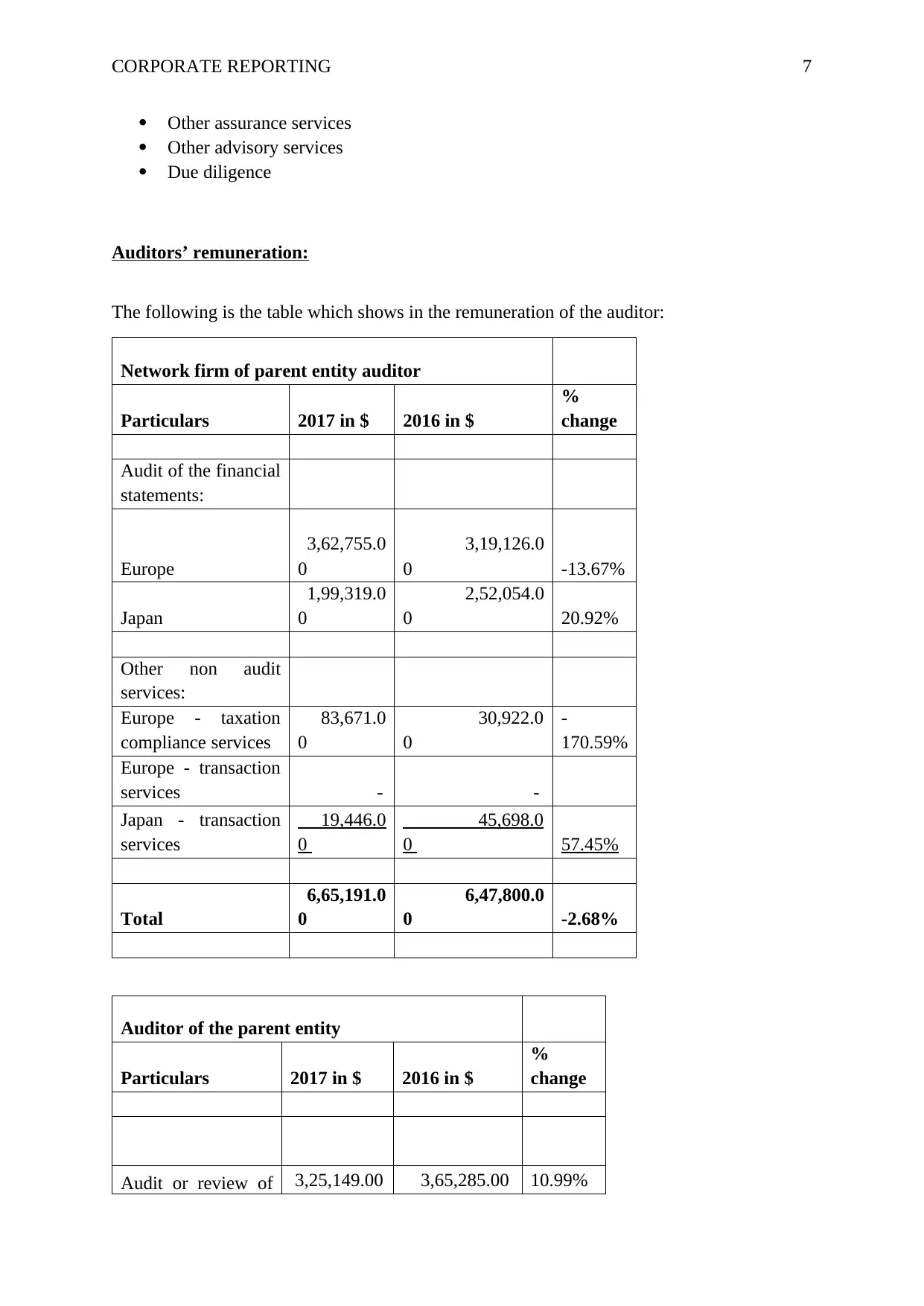

Auditors’ remuneration:

The following is the table which shows in the remuneration of the auditor:

Network firm of parent entity auditor

Particulars 2017 in $ 2016 in $

%

change

Audit of the financial

statements:

Europe

3,62,755.0

0

3,19,126.0

0 -13.67%

Japan

1,99,319.0

0

2,52,054.0

0 20.92%

Other non audit

services:

Europe - taxation

compliance services

83,671.0

0

30,922.0

0

-

170.59%

Europe - transaction

services - -

Japan - transaction

services

19,446.0

0

45,698.0

0 57.45%

Total

6,65,191.0

0

6,47,800.0

0 -2.68%

Auditor of the parent entity

Particulars 2017 in $ 2016 in $

%

change

Audit or review of 3,25,149.00 3,65,285.00 10.99%

Other assurance services

Other advisory services

Due diligence

Auditors’ remuneration:

The following is the table which shows in the remuneration of the auditor:

Network firm of parent entity auditor

Particulars 2017 in $ 2016 in $

%

change

Audit of the financial

statements:

Europe

3,62,755.0

0

3,19,126.0

0 -13.67%

Japan

1,99,319.0

0

2,52,054.0

0 20.92%

Other non audit

services:

Europe - taxation

compliance services

83,671.0

0

30,922.0

0

-

170.59%

Europe - transaction

services - -

Japan - transaction

services

19,446.0

0

45,698.0

0 57.45%

Total

6,65,191.0

0

6,47,800.0

0 -2.68%

Auditor of the parent entity

Particulars 2017 in $ 2016 in $

%

change

Audit or review of 3,25,149.00 3,65,285.00 10.99%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

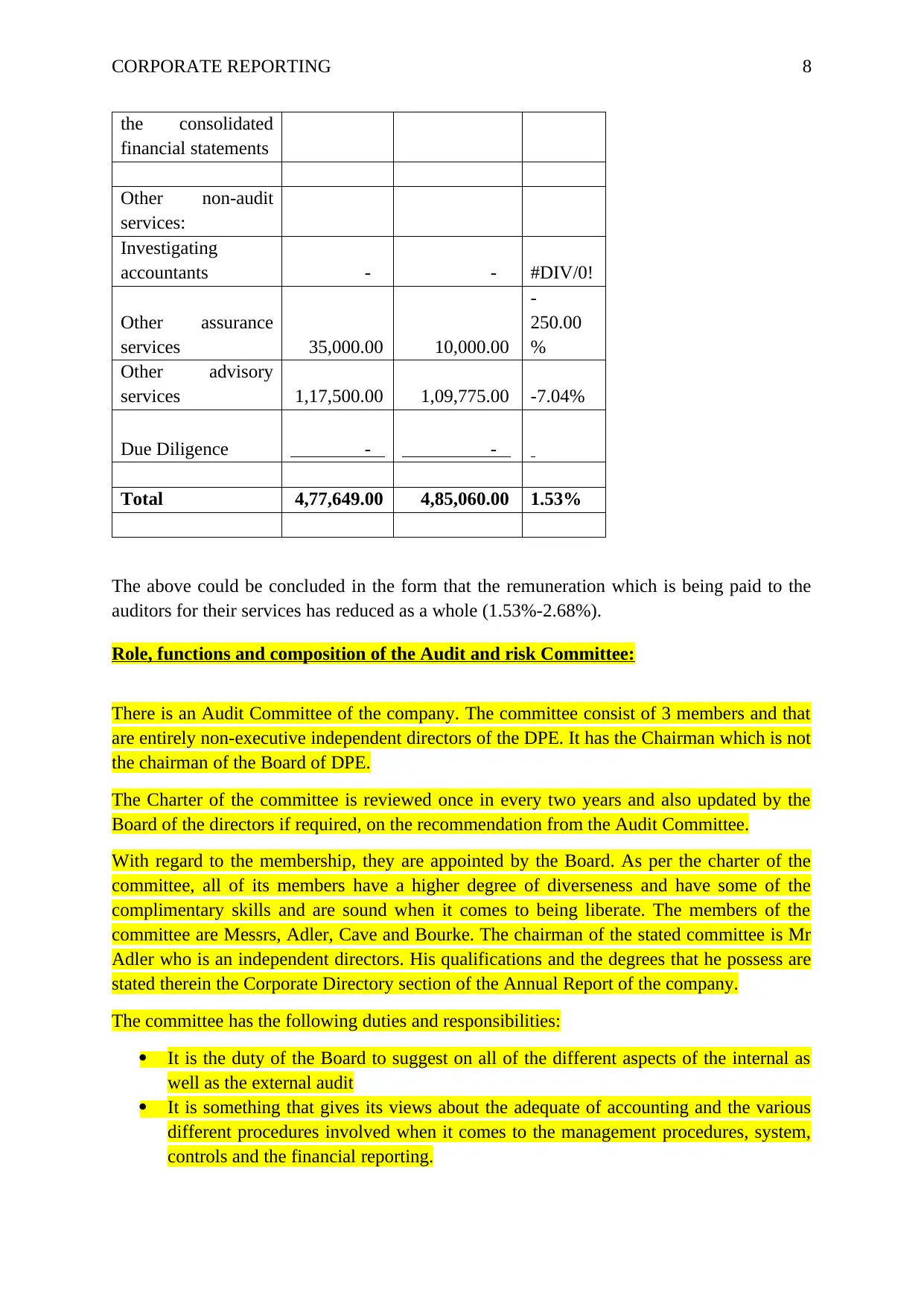

CORPORATE REPORTING 8

the consolidated

financial statements

Other non-audit

services:

Investigating

accountants - - #DIV/0!

Other assurance

services 35,000.00 10,000.00

-

250.00

%

Other advisory

services 1,17,500.00 1,09,775.00 -7.04%

Due Diligence - -

Total 4,77,649.00 4,85,060.00 1.53%

The above could be concluded in the form that the remuneration which is being paid to the

auditors for their services has reduced as a whole (1.53%-2.68%).

Role, functions and composition of the Audit and risk Committee:

There is an Audit Committee of the company. The committee consist of 3 members and that

are entirely non-executive independent directors of the DPE. It has the Chairman which is not

the chairman of the Board of DPE.

The Charter of the committee is reviewed once in every two years and also updated by the

Board of the directors if required, on the recommendation from the Audit Committee.

With regard to the membership, they are appointed by the Board. As per the charter of the

committee, all of its members have a higher degree of diverseness and have some of the

complimentary skills and are sound when it comes to being liberate. The members of the

committee are Messrs, Adler, Cave and Bourke. The chairman of the stated committee is Mr

Adler who is an independent directors. His qualifications and the degrees that he possess are

stated therein the Corporate Directory section of the Annual Report of the company.

The committee has the following duties and responsibilities:

It is the duty of the Board to suggest on all of the different aspects of the internal as

well as the external audit

It is something that gives its views about the adequate of accounting and the various

different procedures involved when it comes to the management procedures, system,

controls and the financial reporting.

the consolidated

financial statements

Other non-audit

services:

Investigating

accountants - - #DIV/0!

Other assurance

services 35,000.00 10,000.00

-

250.00

%

Other advisory

services 1,17,500.00 1,09,775.00 -7.04%

Due Diligence - -

Total 4,77,649.00 4,85,060.00 1.53%

The above could be concluded in the form that the remuneration which is being paid to the

auditors for their services has reduced as a whole (1.53%-2.68%).

Role, functions and composition of the Audit and risk Committee:

There is an Audit Committee of the company. The committee consist of 3 members and that

are entirely non-executive independent directors of the DPE. It has the Chairman which is not

the chairman of the Board of DPE.

The Charter of the committee is reviewed once in every two years and also updated by the

Board of the directors if required, on the recommendation from the Audit Committee.

With regard to the membership, they are appointed by the Board. As per the charter of the

committee, all of its members have a higher degree of diverseness and have some of the

complimentary skills and are sound when it comes to being liberate. The members of the

committee are Messrs, Adler, Cave and Bourke. The chairman of the stated committee is Mr

Adler who is an independent directors. His qualifications and the degrees that he possess are

stated therein the Corporate Directory section of the Annual Report of the company.

The committee has the following duties and responsibilities:

It is the duty of the Board to suggest on all of the different aspects of the internal as

well as the external audit

It is something that gives its views about the adequate of accounting and the various

different procedures involved when it comes to the management procedures, system,

controls and the financial reporting.

CORPORATE REPORTING 9

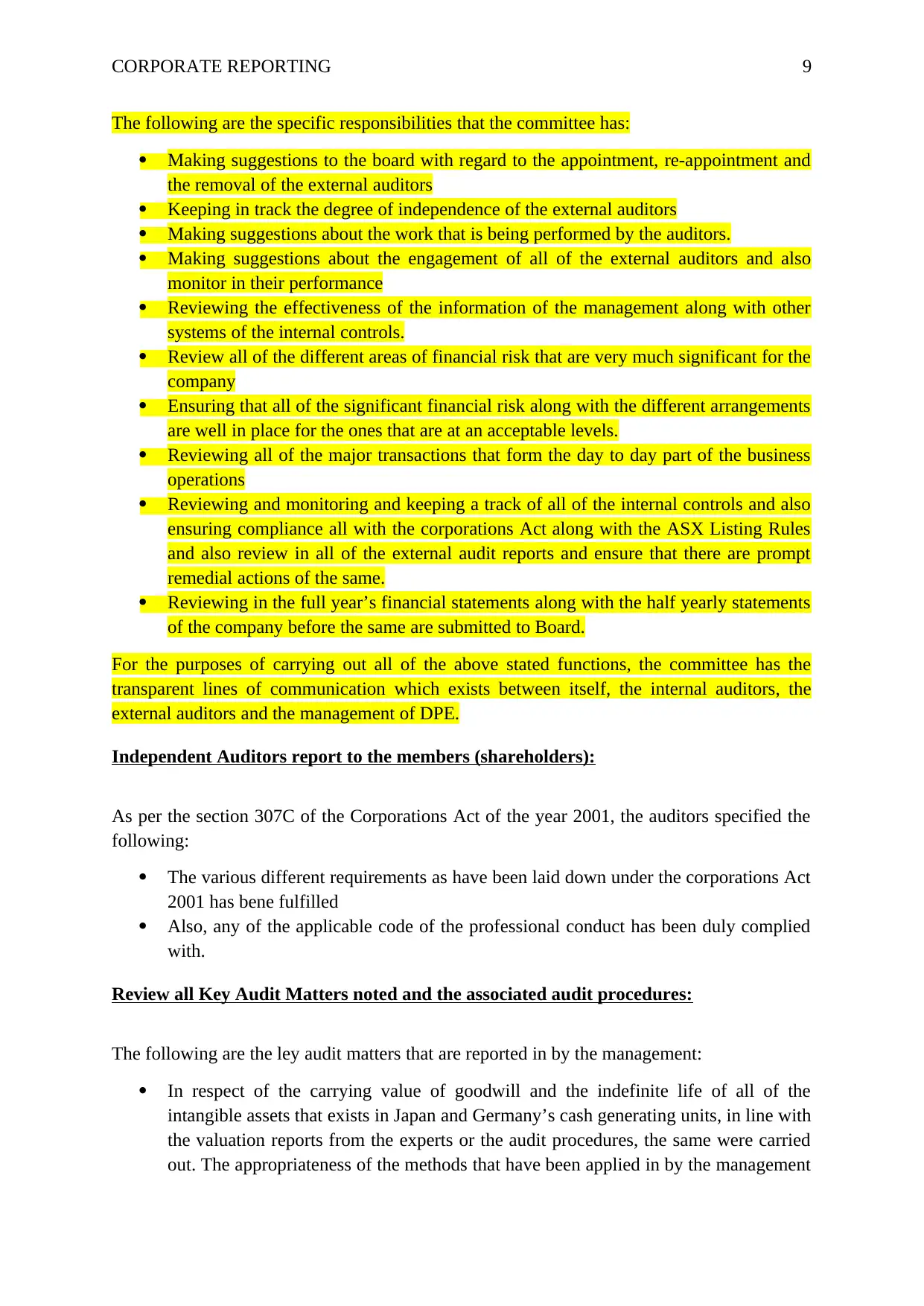

The following are the specific responsibilities that the committee has:

Making suggestions to the board with regard to the appointment, re-appointment and

the removal of the external auditors

Keeping in track the degree of independence of the external auditors

Making suggestions about the work that is being performed by the auditors.

Making suggestions about the engagement of all of the external auditors and also

monitor in their performance

Reviewing the effectiveness of the information of the management along with other

systems of the internal controls.

Review all of the different areas of financial risk that are very much significant for the

company

Ensuring that all of the significant financial risk along with the different arrangements

are well in place for the ones that are at an acceptable levels.

Reviewing all of the major transactions that form the day to day part of the business

operations

Reviewing and monitoring and keeping a track of all of the internal controls and also

ensuring compliance all with the corporations Act along with the ASX Listing Rules

and also review in all of the external audit reports and ensure that there are prompt

remedial actions of the same.

Reviewing in the full year’s financial statements along with the half yearly statements

of the company before the same are submitted to Board.

For the purposes of carrying out all of the above stated functions, the committee has the

transparent lines of communication which exists between itself, the internal auditors, the

external auditors and the management of DPE.

Independent Auditors report to the members (shareholders):

As per the section 307C of the Corporations Act of the year 2001, the auditors specified the

following:

The various different requirements as have been laid down under the corporations Act

2001 has bene fulfilled

Also, any of the applicable code of the professional conduct has been duly complied

with.

Review all Key Audit Matters noted and the associated audit procedures:

The following are the ley audit matters that are reported in by the management:

In respect of the carrying value of goodwill and the indefinite life of all of the

intangible assets that exists in Japan and Germany’s cash generating units, in line with

the valuation reports from the experts or the audit procedures, the same were carried

out. The appropriateness of the methods that have been applied in by the management

The following are the specific responsibilities that the committee has:

Making suggestions to the board with regard to the appointment, re-appointment and

the removal of the external auditors

Keeping in track the degree of independence of the external auditors

Making suggestions about the work that is being performed by the auditors.

Making suggestions about the engagement of all of the external auditors and also

monitor in their performance

Reviewing the effectiveness of the information of the management along with other

systems of the internal controls.

Review all of the different areas of financial risk that are very much significant for the

company

Ensuring that all of the significant financial risk along with the different arrangements

are well in place for the ones that are at an acceptable levels.

Reviewing all of the major transactions that form the day to day part of the business

operations

Reviewing and monitoring and keeping a track of all of the internal controls and also

ensuring compliance all with the corporations Act along with the ASX Listing Rules

and also review in all of the external audit reports and ensure that there are prompt

remedial actions of the same.

Reviewing in the full year’s financial statements along with the half yearly statements

of the company before the same are submitted to Board.

For the purposes of carrying out all of the above stated functions, the committee has the

transparent lines of communication which exists between itself, the internal auditors, the

external auditors and the management of DPE.

Independent Auditors report to the members (shareholders):

As per the section 307C of the Corporations Act of the year 2001, the auditors specified the

following:

The various different requirements as have been laid down under the corporations Act

2001 has bene fulfilled

Also, any of the applicable code of the professional conduct has been duly complied

with.

Review all Key Audit Matters noted and the associated audit procedures:

The following are the ley audit matters that are reported in by the management:

In respect of the carrying value of goodwill and the indefinite life of all of the

intangible assets that exists in Japan and Germany’s cash generating units, in line with

the valuation reports from the experts or the audit procedures, the same were carried

out. The appropriateness of the methods that have been applied in by the management

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CORPORATE REPORTING 10

when it comes to calculating the recoverable amounts of the cash generating units.

The various assumptions were also challenged when it came to the calculation of the

discount rates and the recalculating of these rates. The various different projected cash

flows along with the various assumptions which relates in with the expected rates of

growth and the operating margins as against the historical performance, the

projections of the management and the data of the observed industries, were duly

tested for adequacy and effectiveness. The categorisation of the cash generating units

of the company. The allocation of the goodwill to the carrying value of the cash

generating units was also considered and tested for adequacy. The mathematical

accuracy of these cash generating units was also cheeked. Sensitivity analysis was

conducted on the recoverable amounts of these cash generating units in and around

the key drivers of the growth rates that were being used in the forecasting of the cash

flows and the discount rates.

In terms of valuation of the various put options, in line with the valuation of the

experts, many of the audit procedures included the assessment of the appropriateness

of the methods that have been applied in by the management when it comes valuing in

the option and the assessment of the various key assumptions which includes in the

expected future earnings of each one of the components. The expected timing of these

exercises of the put options and the discount rates was also done. The assessment of

these assumptions that were used in the model of valuation for the purposes of

ensuring that these are in as per the terms of the put options that have been prescribed

in the agreement of the shareholder. The independence, competence, objectivity of the

expert of the management was also evaluated. A sensitivity analysis of the various

key assumptions of the valuation model was also done. The mathematical accuracy of

these calculations of the put options was also tested in,

In terms of valuation of the various put options, the assessment of the methods that

were applied in the group was tested along with the calculation of the liability of the

put option. The various inputs used in by the management was challenged and also,

the calculation which was done for the purposes of arrive in at the liability of the put

option as per the terms that have been prescribed n by the agreement of the

shareholders were checked. The correspondence with the counterparty as being the

part of the completion of the exercise of the put option was inspected. The

appropriateness of the various related disclosures required was also checked.

In terms of the accounting for the guarantees contingencies and the claims that were

related with the group, the process of the management for the purposes of valuating in

the different guarantees was evaluated. The status of any new and the existing claims

along with the contingencies were assessed. This was done through the inquiry pf the

management and the legal advisors of the group. The confirmation form the legal

visors was sought. The minutes of the board meetings along with all of the relevant

information were inspected thoroughly which was presented to the directors. The

appropriateness of the various disclosures was also checked in the financial

statements.

when it comes to calculating the recoverable amounts of the cash generating units.

The various assumptions were also challenged when it came to the calculation of the

discount rates and the recalculating of these rates. The various different projected cash

flows along with the various assumptions which relates in with the expected rates of

growth and the operating margins as against the historical performance, the

projections of the management and the data of the observed industries, were duly

tested for adequacy and effectiveness. The categorisation of the cash generating units

of the company. The allocation of the goodwill to the carrying value of the cash

generating units was also considered and tested for adequacy. The mathematical

accuracy of these cash generating units was also cheeked. Sensitivity analysis was

conducted on the recoverable amounts of these cash generating units in and around

the key drivers of the growth rates that were being used in the forecasting of the cash

flows and the discount rates.

In terms of valuation of the various put options, in line with the valuation of the

experts, many of the audit procedures included the assessment of the appropriateness

of the methods that have been applied in by the management when it comes valuing in

the option and the assessment of the various key assumptions which includes in the

expected future earnings of each one of the components. The expected timing of these

exercises of the put options and the discount rates was also done. The assessment of

these assumptions that were used in the model of valuation for the purposes of

ensuring that these are in as per the terms of the put options that have been prescribed

in the agreement of the shareholder. The independence, competence, objectivity of the

expert of the management was also evaluated. A sensitivity analysis of the various

key assumptions of the valuation model was also done. The mathematical accuracy of

these calculations of the put options was also tested in,

In terms of valuation of the various put options, the assessment of the methods that

were applied in the group was tested along with the calculation of the liability of the

put option. The various inputs used in by the management was challenged and also,

the calculation which was done for the purposes of arrive in at the liability of the put

option as per the terms that have been prescribed n by the agreement of the

shareholders were checked. The correspondence with the counterparty as being the

part of the completion of the exercise of the put option was inspected. The

appropriateness of the various related disclosures required was also checked.

In terms of the accounting for the guarantees contingencies and the claims that were

related with the group, the process of the management for the purposes of valuating in

the different guarantees was evaluated. The status of any new and the existing claims

along with the contingencies were assessed. This was done through the inquiry pf the

management and the legal advisors of the group. The confirmation form the legal

visors was sought. The minutes of the board meetings along with all of the relevant

information were inspected thoroughly which was presented to the directors. The

appropriateness of the various disclosures was also checked in the financial

statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CORPORATE REPORTING 11

Directors’ and Management’s responsibilities:

The main responsibility of the auditor is to plan in and also perform the audit in order to

obtain a reasonable assurance of the fact that the financial statements are free from any

material misstatements whatsoever and that there is no error or any fraud in them. This is

mainly due to the fact that the nature of the audit evidence and the characteristics of the fraud,

the auditor would not be able to obtain an exact assurance that there is no falsified business in

the financial statements (PACOBUS, 2018). The financial statements is the primary

responsibility of the management. The responsibility of the auditor is just to express an

opinion on the truthfulness and the fairness of these prepared financial statements (University

network, 2018). The management is the one that is responsible for the purposes of adopting

in the sound and correct accounting policies. It is the management which is responsible for

the intiation, recording, processing and preparing these financial statements.

Material subsequent events:

The Annual report of the company states that there is as such no matter or circumstance by

the end of the accounting year that could have affected in or could significant affect the

operations of the consolidated entity. There are material subsequent events that could affect

in the results from those operations or the stated of the affairs of the consolidated entity in the

future financial years.

But there is an event after the reporting date which is that on August 14, 2017, the directors

had declared in the final dividend for the financial year which ended on July 2, 2017.

Assessment of effectiveness of material information:

The information as has been contained in the annual report of the company is sufficient

enough to assess the reporting adequacy of the company.

Under reporting and questions to be asked to auditor:

The following questions could be posed in to the auditor:

Any fraud detection program that the company has?

The company’s policies to make sure that there is no insider trading?

Adequacy of the internal controls

The appropriateness and the adequacy of the internal controls (PWC, 2006).

Conclusion:

The company does have the Audit committee which has the roles and responsibilities of

overlooking all of the business functions of the company and to make sure that the company

is performing properly and that it is disclosing all of the relevant facts correctly and as per the

relevant accounting regulations.

The responsibility of the management sis to prepare in the financial statements.

Directors’ and Management’s responsibilities:

The main responsibility of the auditor is to plan in and also perform the audit in order to

obtain a reasonable assurance of the fact that the financial statements are free from any

material misstatements whatsoever and that there is no error or any fraud in them. This is

mainly due to the fact that the nature of the audit evidence and the characteristics of the fraud,

the auditor would not be able to obtain an exact assurance that there is no falsified business in

the financial statements (PACOBUS, 2018). The financial statements is the primary

responsibility of the management. The responsibility of the auditor is just to express an

opinion on the truthfulness and the fairness of these prepared financial statements (University

network, 2018). The management is the one that is responsible for the purposes of adopting

in the sound and correct accounting policies. It is the management which is responsible for

the intiation, recording, processing and preparing these financial statements.

Material subsequent events:

The Annual report of the company states that there is as such no matter or circumstance by

the end of the accounting year that could have affected in or could significant affect the

operations of the consolidated entity. There are material subsequent events that could affect

in the results from those operations or the stated of the affairs of the consolidated entity in the

future financial years.

But there is an event after the reporting date which is that on August 14, 2017, the directors

had declared in the final dividend for the financial year which ended on July 2, 2017.

Assessment of effectiveness of material information:

The information as has been contained in the annual report of the company is sufficient

enough to assess the reporting adequacy of the company.

Under reporting and questions to be asked to auditor:

The following questions could be posed in to the auditor:

Any fraud detection program that the company has?

The company’s policies to make sure that there is no insider trading?

Adequacy of the internal controls

The appropriateness and the adequacy of the internal controls (PWC, 2006).

Conclusion:

The company does have the Audit committee which has the roles and responsibilities of

overlooking all of the business functions of the company and to make sure that the company

is performing properly and that it is disclosing all of the relevant facts correctly and as per the

relevant accounting regulations.

The responsibility of the management sis to prepare in the financial statements.

CORPORATE REPORTING 12

As per the Statements of Auditing Standards, the transactions that are entered into during the

course of the events of the company are within the scope and within the knowledge of the

management of the company and hence, they are the right people to prepare the financial

statements. Their knowledge is all about the business that they have been indulging

themselves in. the main responsibility of the auditor is the expression of their opinion on the

truthfulness an fairness of the financial statements. The auditor could give suggestions to the

management with regard to the preparation of the financial statements but the sole

responsibility is still of the company.

Though the facts contained in the annual report are all relevant but then an investor could

pose some questions such as the programs that could test the adequacy of the internal

controls.

As per the Statements of Auditing Standards, the transactions that are entered into during the

course of the events of the company are within the scope and within the knowledge of the

management of the company and hence, they are the right people to prepare the financial

statements. Their knowledge is all about the business that they have been indulging

themselves in. the main responsibility of the auditor is the expression of their opinion on the

truthfulness an fairness of the financial statements. The auditor could give suggestions to the

management with regard to the preparation of the financial statements but the sole

responsibility is still of the company.

Though the facts contained in the annual report are all relevant but then an investor could

pose some questions such as the programs that could test the adequacy of the internal

controls.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.