HI5002 Finance Group Assignment: Domino's Pizza Company Analysis

VerifiedAdded on 2022/11/01

|23

|3916

|177

Report

AI Summary

This report presents a comprehensive financial analysis of Domino's Pizza Enterprises Limited, an ASX-listed company. It examines the company's financial performance using profitability ratios (Return on Total Assets, Net Profit Ratio, and Return on Equity) and operating efficiency ratios (Inventory Turnover Ratio, Account Receivable Turnover Ratio, and Asset Turnover Ratio) from 2015 to 2018. The analysis includes the use of marketable securities for cash management, application of sensitivity analysis in capital budgeting, and an assessment of systematic and unsystematic risks. Furthermore, the report calculates the dividend payout ratio and interprets the company's dividend policy, concluding with a recommendation letter to a potential institutional investor. The study highlights Domino's Pizza's strong financial position, sound cash management, and effective risk management, making it a potentially attractive investment opportunity. The report is designed to provide guidance to investors by providing a clear understanding of the company's financial health and future prospects.

1

HI5002

Finance for Business

Group Assignment

Company Performance Analysis

HI5002

Finance for Business

Group Assignment

Company Performance Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Abstract

The report is being developed for providing an understating of the financial analysis

carried out for a company to provide recommendation to an institutional investor aiming to

invest within a company. The overall financial analysis is based on an ASX listed entity, that is,

Dominos Pizza Enterprises Limited. It has been suggested to invest within the company on the

basis of iota good profitability and efficiency position, sound cash management, regular dividend

paid to shareholders and effective management of systematic and unsystematic risks.

Abstract

The report is being developed for providing an understating of the financial analysis

carried out for a company to provide recommendation to an institutional investor aiming to

invest within a company. The overall financial analysis is based on an ASX listed entity, that is,

Dominos Pizza Enterprises Limited. It has been suggested to invest within the company on the

basis of iota good profitability and efficiency position, sound cash management, regular dividend

paid to shareholders and effective management of systematic and unsystematic risks.

3

Contents

Abstract............................................................................................................................................2

I: Introduction..................................................................................................................................4

II: Detailed discussion on financial analysis of Dominos Pizza Enterprise Limited.......................4

2.1: Brief information of the selected company...........................................................................4

2.2: Use of performance ratios to depict the performance of the company.................................5

Profitability Ratios of Domino’s Pizza........................................................................................5

2.3: Use of marketable securities for cash management............................................................10

2.4: Application of sensitivity analysis in capital budgeting problem.......................................12

2.5: Systematic and Unsystematic Risks Associated with Dominos Pizza................................17

Systematic Risks........................................................................................................................18

Unsystematic Risks....................................................................................................................18

2.6: Calculation of dividend payout ratio and interpretation of dividend policy implemented by

the company...............................................................................................................................19

III: Recommendation Letter to client (As a potential investor).....................................................20

IV: Conclusion...............................................................................................................................21

References......................................................................................................................................22

Contents

Abstract............................................................................................................................................2

I: Introduction..................................................................................................................................4

II: Detailed discussion on financial analysis of Dominos Pizza Enterprise Limited.......................4

2.1: Brief information of the selected company...........................................................................4

2.2: Use of performance ratios to depict the performance of the company.................................5

Profitability Ratios of Domino’s Pizza........................................................................................5

2.3: Use of marketable securities for cash management............................................................10

2.4: Application of sensitivity analysis in capital budgeting problem.......................................12

2.5: Systematic and Unsystematic Risks Associated with Dominos Pizza................................17

Systematic Risks........................................................................................................................18

Unsystematic Risks....................................................................................................................18

2.6: Calculation of dividend payout ratio and interpretation of dividend policy implemented by

the company...............................................................................................................................19

III: Recommendation Letter to client (As a potential investor).....................................................20

IV: Conclusion...............................................................................................................................21

References......................................................................................................................................22

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

I: Introduction

The business entities tend to prepare and disclose their financial information through the

financial statements to facilitate the economic decision-making of its investors. The financial

statement assists the investors of an entity from across the world to take investment decisions by

analysis of its past, present and future financial performance. This report has been developed to

undertake an analysis of the financial performance of a selected listed company on the ASX for

the purpose for providing guidance to an institutional investor. The business entity selected for

the purpose is Domino’s Pizza Enterprise Limited, an ASX listed pizza chain in Australia.

The report undertakes an evaluation of the financial performance of the selected entity

through the use of ratio analysis, cash management, conducting sensitivity analysis and

discussing the systematic and unsystematic risks associated with the company operations. It also

calculates the dividend payout ratio for providing an assessment regarding the dividend policy of

the company. Lastly, the overall findings generated are presented within the recommendation

section to provide guidance to an institutional investor regarding investment within the company.

II: Detailed discussion on financial analysis of Dominos Pizza Enterprise Limited

2.1: Brief information of the selected company

Domino’s Pizza Enterprises Limited is regarded as largest pizza chain in Australia in

reference to the number of stores and its wide network. The company realizes high sales within

the Australian market as it is the largest franchise for Domino’s Pizza brand across the world. Its

pizza chain has extended to several countries across the world having about 2,500 stores and thus

largely contributing to the growth and expansion of Domino’s franchise on an international level.

The major markets of the company include Australia, New Zealand, Germany, Denmark,

Luxemburg, Japan, France and the Netherlands. It has been established in the year 1983 and is

presently regarded as one of the biggest pizza franchised business across Australia. It is

headquartered within Queensland in Australia and is regarded as major player within the food

retail sector of the country. The distinctive advantage is acquired by the company in retail sector

of Australia owing to its capabilities of proving faster and fresh quality food to the people and

also has achieved a leadership in the use of innovative technologies in food sector. It is being

I: Introduction

The business entities tend to prepare and disclose their financial information through the

financial statements to facilitate the economic decision-making of its investors. The financial

statement assists the investors of an entity from across the world to take investment decisions by

analysis of its past, present and future financial performance. This report has been developed to

undertake an analysis of the financial performance of a selected listed company on the ASX for

the purpose for providing guidance to an institutional investor. The business entity selected for

the purpose is Domino’s Pizza Enterprise Limited, an ASX listed pizza chain in Australia.

The report undertakes an evaluation of the financial performance of the selected entity

through the use of ratio analysis, cash management, conducting sensitivity analysis and

discussing the systematic and unsystematic risks associated with the company operations. It also

calculates the dividend payout ratio for providing an assessment regarding the dividend policy of

the company. Lastly, the overall findings generated are presented within the recommendation

section to provide guidance to an institutional investor regarding investment within the company.

II: Detailed discussion on financial analysis of Dominos Pizza Enterprise Limited

2.1: Brief information of the selected company

Domino’s Pizza Enterprises Limited is regarded as largest pizza chain in Australia in

reference to the number of stores and its wide network. The company realizes high sales within

the Australian market as it is the largest franchise for Domino’s Pizza brand across the world. Its

pizza chain has extended to several countries across the world having about 2,500 stores and thus

largely contributing to the growth and expansion of Domino’s franchise on an international level.

The major markets of the company include Australia, New Zealand, Germany, Denmark,

Luxemburg, Japan, France and the Netherlands. It has been established in the year 1983 and is

presently regarded as one of the biggest pizza franchised business across Australia. It is

headquartered within Queensland in Australia and is regarded as major player within the food

retail sector of the country. The distinctive advantage is acquired by the company in retail sector

of Australia owing to its capabilities of proving faster and fresh quality food to the people and

also has achieved a leadership in the use of innovative technologies in food sector. It is being

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

recognized as first company to introduce drone-delivery pizza and also providing innovative

features such as ordering through app and using artificial intelligence in managing its operational

activities (About Dominos, 2019).

2.2: Use of performance ratios to depict the performance of the company

Profitability Ratios of Domino’s Pizza

Financial Data of Domino's Pizza for calculation of Profitability Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Earnings before

Interest and tax

$

93,085.00

$

130,603.00

$

164,202.00

$

182,407.00

Net profit after tax

$

68,421.00

$

86,592.00

$

105,804.00

$

121,693.00

Net Sales

$

539,138.00

$

705,702.00

$

790,861.00

$

794,072.00

Shareholder's equity

$

305,056.00

$

394,546.00

$

415,064.00

$

307,664.00

Average shareholder's

equity

$

349,801.00

$

404,805.00

$

361,364.00

Total Assets

$

630,600.00

$

1,125,728.0

0

$

1,132,793.0

0

$

1,302,411.0

0

Average total assets

$

878,164.00

$

1,129,260.5

0

$

1,217,602.0

0

Profitability Ratio of Domino's Pizza

recognized as first company to introduce drone-delivery pizza and also providing innovative

features such as ordering through app and using artificial intelligence in managing its operational

activities (About Dominos, 2019).

2.2: Use of performance ratios to depict the performance of the company

Profitability Ratios of Domino’s Pizza

Financial Data of Domino's Pizza for calculation of Profitability Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Earnings before

Interest and tax

$

93,085.00

$

130,603.00

$

164,202.00

$

182,407.00

Net profit after tax

$

68,421.00

$

86,592.00

$

105,804.00

$

121,693.00

Net Sales

$

539,138.00

$

705,702.00

$

790,861.00

$

794,072.00

Shareholder's equity

$

305,056.00

$

394,546.00

$

415,064.00

$

307,664.00

Average shareholder's

equity

$

349,801.00

$

404,805.00

$

361,364.00

Total Assets

$

630,600.00

$

1,125,728.0

0

$

1,132,793.0

0

$

1,302,411.0

0

Average total assets

$

878,164.00

$

1,129,260.5

0

$

1,217,602.0

0

Profitability Ratio of Domino's Pizza

6

Ratios Formula 2016 2017 2018

Return on Total

Assets

Earnings before

Interest and

tax/Average

Total Assets

14.87% 14.54% 14.98%

Net profit ratio Net profit/Sales 12.27% 13.38% 15.33%

Return on equity

Net profit after

tax/Average

shareholder's

equity

24.75% 26.14% 33.68%

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

14.87% 14.54% 14.98%

12.27% 13.38%

15.33%

24.75% 26.14%

33.68%

Profitability Ratio of Domino's Pizza

Percentage

Ratios Formula 2016 2017 2018

Return on Total

Assets

Earnings before

Interest and

tax/Average

Total Assets

14.87% 14.54% 14.98%

Net profit ratio Net profit/Sales 12.27% 13.38% 15.33%

Return on equity

Net profit after

tax/Average

shareholder's

equity

24.75% 26.14% 33.68%

2016 2017 2018

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

14.87% 14.54% 14.98%

12.27% 13.38%

15.33%

24.75% 26.14%

33.68%

Profitability Ratio of Domino's Pizza

Percentage

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

(Source: Domino’s Pizza: Annual Report, 2016, Domino’s Pizza: Annual Report, 2017 &

Domino’s Pizza: Annual Report, 2018)

The profitability position of Domino’s Pizza can be analyzed by the use of following ratios:

Return on Total Assets (ROTA): The return on total assets is the ratio that measures an

entity’s earnings before interest and tax (EBIT) to its total assets. This ratio indicates that

how effectively a company is using its total assets to generate revenue before its finance

cost and tax expenses. The chart depicts a straight line which shows Domino’s Pizza has

a stable trend in respect of return on total assets. However from 2016 to 2017 return on

total assets have fallen from 14.87% to 14.54% and then it has increased in 2018 to

14.98%. Earnings before interest and taxes have increased over the selected financial

period which means that it is able to achieve control over its operational expenses thus

deriving higher profits (Moles and Kidwekk, 2011).

Net Profit Ratio: Net Profit Ratio measures the percentage of profitability in relation to

net sales. This Ratio indicates the profit earned per dollar of net sales. On analyzing the

past three years data it can be said that Domino’s Pizza has an upward trend in respect of

net profit ratio from 12.27 to 15. 33%. This is actually a good sign for the stakeholders as

well as prospective investors. The company is performing good in terms of deriving net

profits from its overall sales figure which supports its future growth prospects (Baker and

Powell, 2009).

Return on Equity: This ratio states the percentage of profit after taxes earned on total

equity of the company. In other words, return on equity measures the effectiveness of a

company is using its equity money to generate revenues after deducting the finance cost

and taxes. The chart depicts upward trend indicating the increase in the ratio in past three

years. This states that company is working very efficiently by using cheap source of

finance (debt) which needs low return to generate higher revenue that can be attributable

to equity investors. The company has attained highest return on its equity in the financial

year 2018 which means that it is bale to effectively generate returns on the shareholders

(Zimmerman and Yahya-Zadeh, 2011).

Operating Efficiency Ratios

(Source: Domino’s Pizza: Annual Report, 2016, Domino’s Pizza: Annual Report, 2017 &

Domino’s Pizza: Annual Report, 2018)

The profitability position of Domino’s Pizza can be analyzed by the use of following ratios:

Return on Total Assets (ROTA): The return on total assets is the ratio that measures an

entity’s earnings before interest and tax (EBIT) to its total assets. This ratio indicates that

how effectively a company is using its total assets to generate revenue before its finance

cost and tax expenses. The chart depicts a straight line which shows Domino’s Pizza has

a stable trend in respect of return on total assets. However from 2016 to 2017 return on

total assets have fallen from 14.87% to 14.54% and then it has increased in 2018 to

14.98%. Earnings before interest and taxes have increased over the selected financial

period which means that it is able to achieve control over its operational expenses thus

deriving higher profits (Moles and Kidwekk, 2011).

Net Profit Ratio: Net Profit Ratio measures the percentage of profitability in relation to

net sales. This Ratio indicates the profit earned per dollar of net sales. On analyzing the

past three years data it can be said that Domino’s Pizza has an upward trend in respect of

net profit ratio from 12.27 to 15. 33%. This is actually a good sign for the stakeholders as

well as prospective investors. The company is performing good in terms of deriving net

profits from its overall sales figure which supports its future growth prospects (Baker and

Powell, 2009).

Return on Equity: This ratio states the percentage of profit after taxes earned on total

equity of the company. In other words, return on equity measures the effectiveness of a

company is using its equity money to generate revenues after deducting the finance cost

and taxes. The chart depicts upward trend indicating the increase in the ratio in past three

years. This states that company is working very efficiently by using cheap source of

finance (debt) which needs low return to generate higher revenue that can be attributable

to equity investors. The company has attained highest return on its equity in the financial

year 2018 which means that it is bale to effectively generate returns on the shareholders

(Zimmerman and Yahya-Zadeh, 2011).

Operating Efficiency Ratios

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

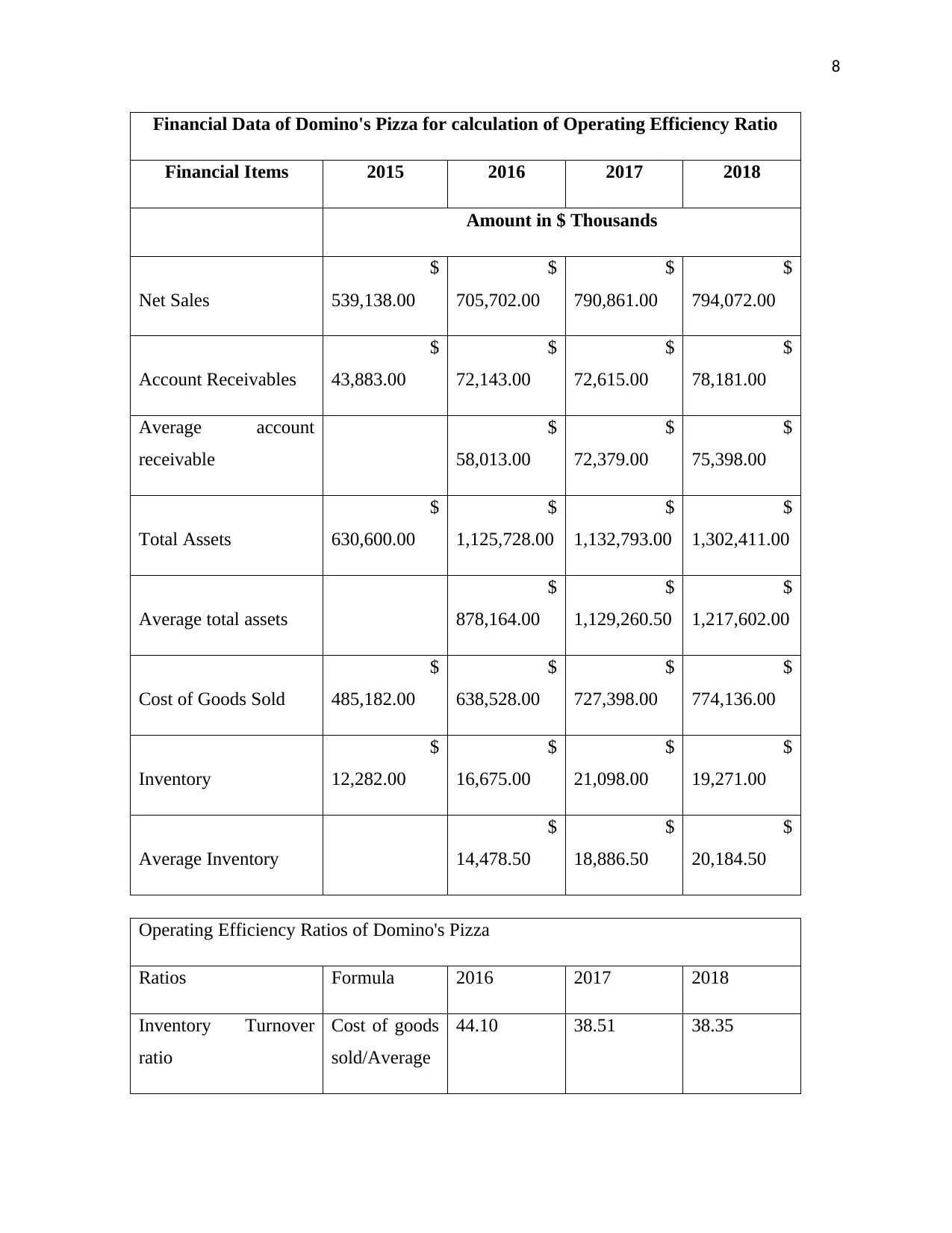

Financial Data of Domino's Pizza for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales

$

539,138.00

$

705,702.00

$

790,861.00

$

794,072.00

Account Receivables

$

43,883.00

$

72,143.00

$

72,615.00

$

78,181.00

Average account

receivable

$

58,013.00

$

72,379.00

$

75,398.00

Total Assets

$

630,600.00

$

1,125,728.00

$

1,132,793.00

$

1,302,411.00

Average total assets

$

878,164.00

$

1,129,260.50

$

1,217,602.00

Cost of Goods Sold

$

485,182.00

$

638,528.00

$

727,398.00

$

774,136.00

Inventory

$

12,282.00

$

16,675.00

$

21,098.00

$

19,271.00

Average Inventory

$

14,478.50

$

18,886.50

$

20,184.50

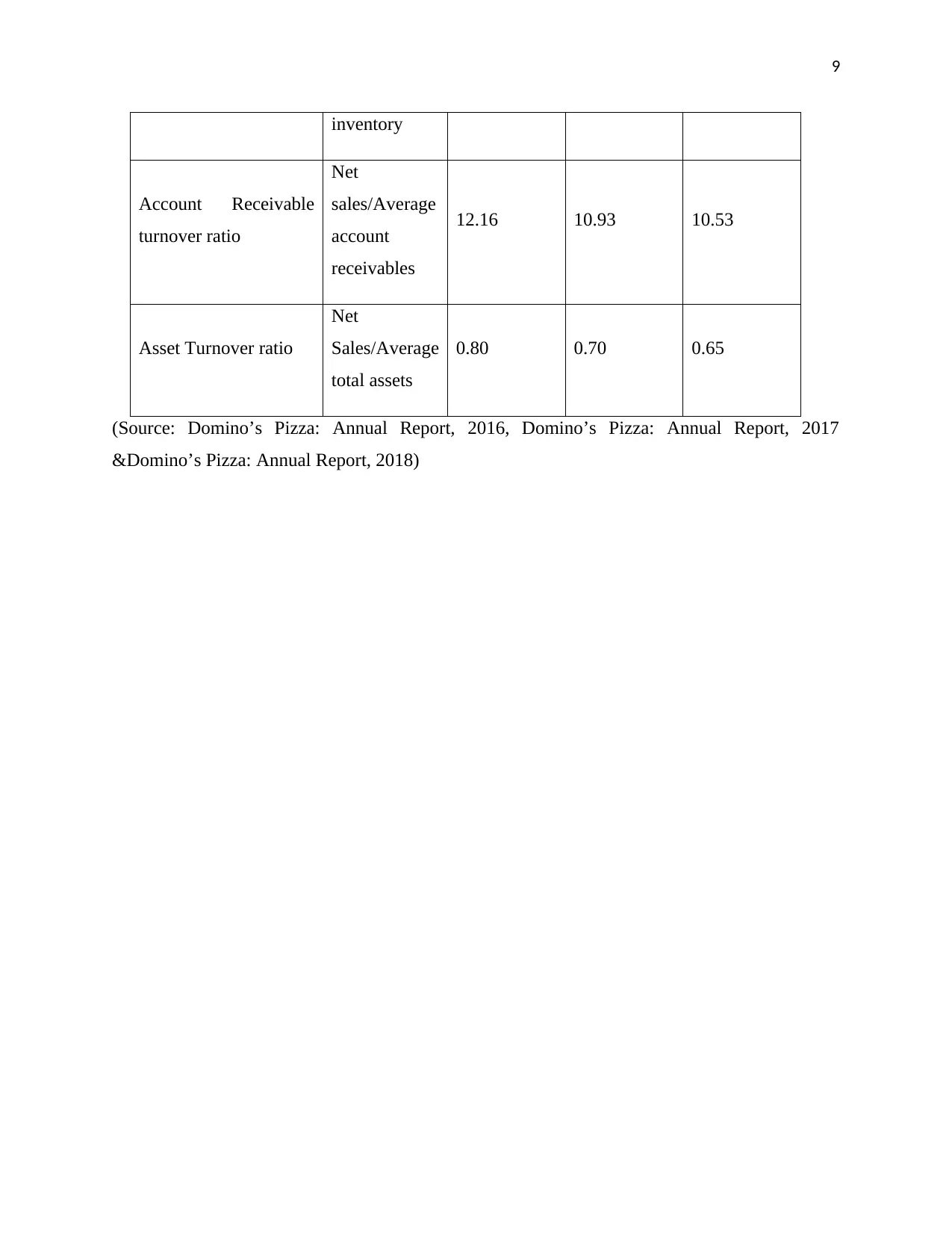

Operating Efficiency Ratios of Domino's Pizza

Ratios Formula 2016 2017 2018

Inventory Turnover

ratio

Cost of goods

sold/Average

44.10 38.51 38.35

Financial Data of Domino's Pizza for calculation of Operating Efficiency Ratio

Financial Items 2015 2016 2017 2018

Amount in $ Thousands

Net Sales

$

539,138.00

$

705,702.00

$

790,861.00

$

794,072.00

Account Receivables

$

43,883.00

$

72,143.00

$

72,615.00

$

78,181.00

Average account

receivable

$

58,013.00

$

72,379.00

$

75,398.00

Total Assets

$

630,600.00

$

1,125,728.00

$

1,132,793.00

$

1,302,411.00

Average total assets

$

878,164.00

$

1,129,260.50

$

1,217,602.00

Cost of Goods Sold

$

485,182.00

$

638,528.00

$

727,398.00

$

774,136.00

Inventory

$

12,282.00

$

16,675.00

$

21,098.00

$

19,271.00

Average Inventory

$

14,478.50

$

18,886.50

$

20,184.50

Operating Efficiency Ratios of Domino's Pizza

Ratios Formula 2016 2017 2018

Inventory Turnover

ratio

Cost of goods

sold/Average

44.10 38.51 38.35

9

inventory

Account Receivable

turnover ratio

Net

sales/Average

account

receivables

12.16 10.93 10.53

Asset Turnover ratio

Net

Sales/Average

total assets

0.80 0.70 0.65

(Source: Domino’s Pizza: Annual Report, 2016, Domino’s Pizza: Annual Report, 2017

&Domino’s Pizza: Annual Report, 2018)

inventory

Account Receivable

turnover ratio

Net

sales/Average

account

receivables

12.16 10.93 10.53

Asset Turnover ratio

Net

Sales/Average

total assets

0.80 0.70 0.65

(Source: Domino’s Pizza: Annual Report, 2016, Domino’s Pizza: Annual Report, 2017

&Domino’s Pizza: Annual Report, 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

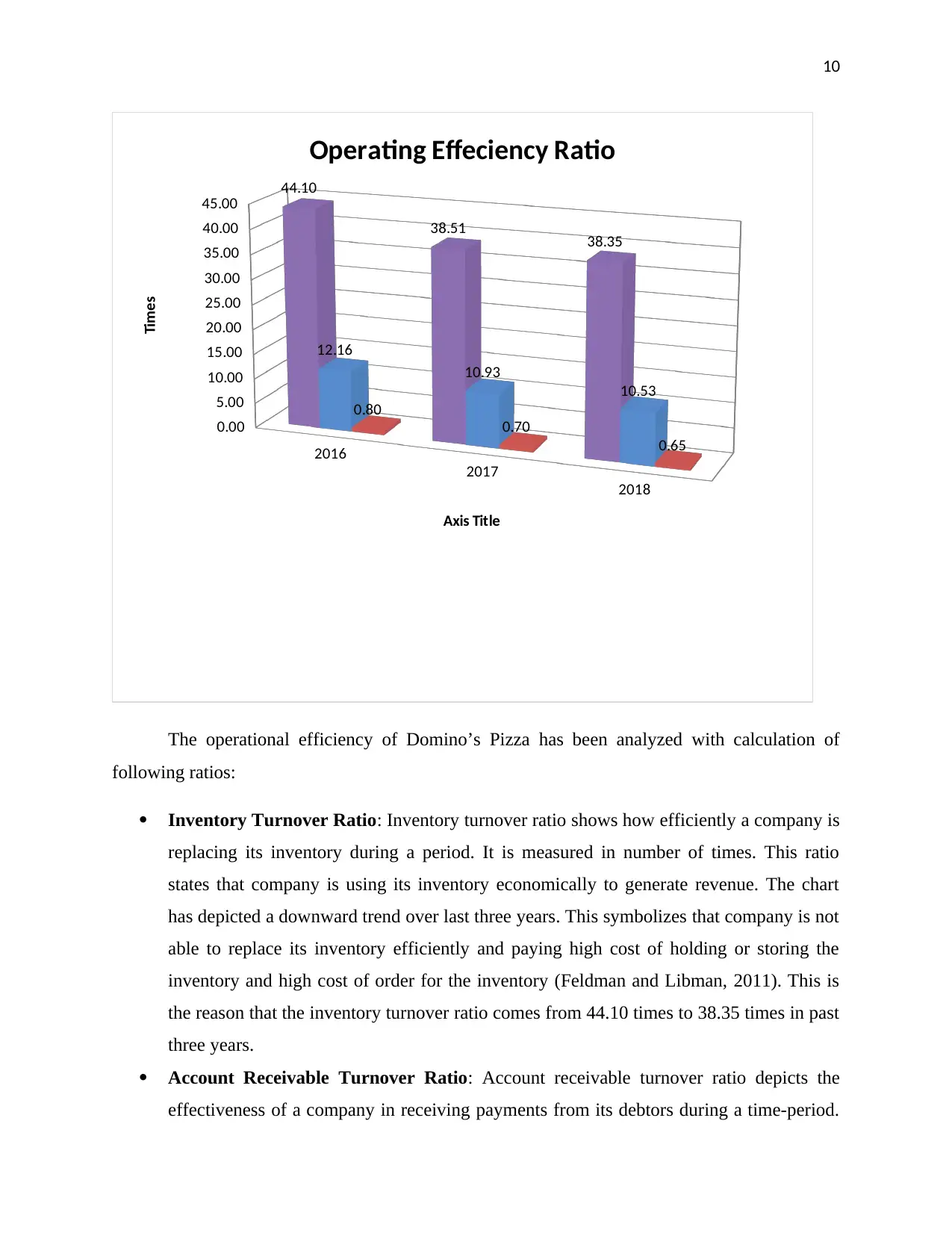

2016

2017

2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

44.10

38.51 38.35

12.16

10.93

10.53

0.80

0.70

0.65

Operating Effeciency Ratio

Axis Title

Times

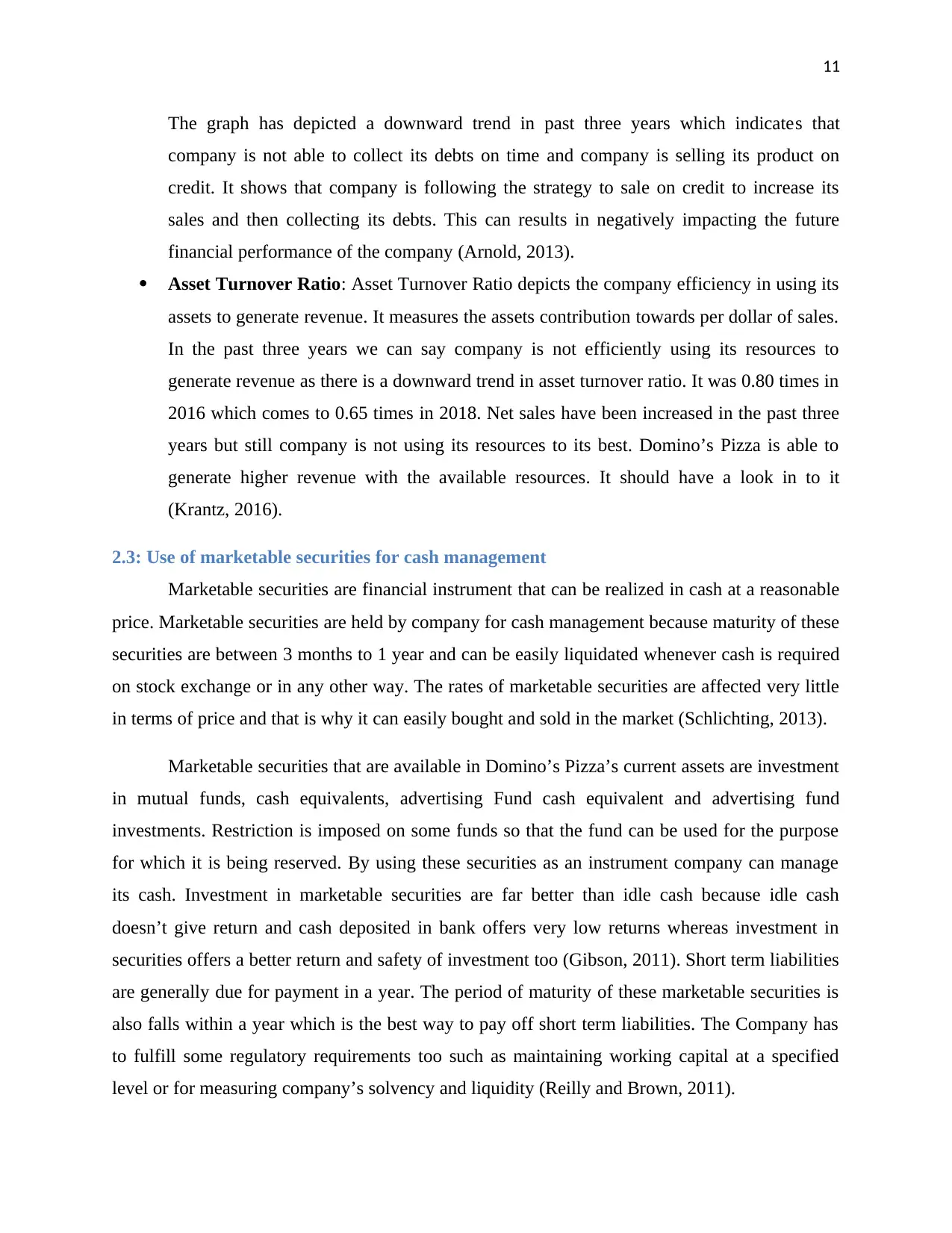

The operational efficiency of Domino’s Pizza has been analyzed with calculation of

following ratios:

Inventory Turnover Ratio: Inventory turnover ratio shows how efficiently a company is

replacing its inventory during a period. It is measured in number of times. This ratio

states that company is using its inventory economically to generate revenue. The chart

has depicted a downward trend over last three years. This symbolizes that company is not

able to replace its inventory efficiently and paying high cost of holding or storing the

inventory and high cost of order for the inventory (Feldman and Libman, 2011). This is

the reason that the inventory turnover ratio comes from 44.10 times to 38.35 times in past

three years.

Account Receivable Turnover Ratio: Account receivable turnover ratio depicts the

effectiveness of a company in receiving payments from its debtors during a time-period.

2016

2017

2018

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

40.00

45.00

44.10

38.51 38.35

12.16

10.93

10.53

0.80

0.70

0.65

Operating Effeciency Ratio

Axis Title

Times

The operational efficiency of Domino’s Pizza has been analyzed with calculation of

following ratios:

Inventory Turnover Ratio: Inventory turnover ratio shows how efficiently a company is

replacing its inventory during a period. It is measured in number of times. This ratio

states that company is using its inventory economically to generate revenue. The chart

has depicted a downward trend over last three years. This symbolizes that company is not

able to replace its inventory efficiently and paying high cost of holding or storing the

inventory and high cost of order for the inventory (Feldman and Libman, 2011). This is

the reason that the inventory turnover ratio comes from 44.10 times to 38.35 times in past

three years.

Account Receivable Turnover Ratio: Account receivable turnover ratio depicts the

effectiveness of a company in receiving payments from its debtors during a time-period.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

The graph has depicted a downward trend in past three years which indicates that

company is not able to collect its debts on time and company is selling its product on

credit. It shows that company is following the strategy to sale on credit to increase its

sales and then collecting its debts. This can results in negatively impacting the future

financial performance of the company (Arnold, 2013).

Asset Turnover Ratio: Asset Turnover Ratio depicts the company efficiency in using its

assets to generate revenue. It measures the assets contribution towards per dollar of sales.

In the past three years we can say company is not efficiently using its resources to

generate revenue as there is a downward trend in asset turnover ratio. It was 0.80 times in

2016 which comes to 0.65 times in 2018. Net sales have been increased in the past three

years but still company is not using its resources to its best. Domino’s Pizza is able to

generate higher revenue with the available resources. It should have a look in to it

(Krantz, 2016).

2.3: Use of marketable securities for cash management

Marketable securities are financial instrument that can be realized in cash at a reasonable

price. Marketable securities are held by company for cash management because maturity of these

securities are between 3 months to 1 year and can be easily liquidated whenever cash is required

on stock exchange or in any other way. The rates of marketable securities are affected very little

in terms of price and that is why it can easily bought and sold in the market (Schlichting, 2013).

Marketable securities that are available in Domino’s Pizza’s current assets are investment

in mutual funds, cash equivalents, advertising Fund cash equivalent and advertising fund

investments. Restriction is imposed on some funds so that the fund can be used for the purpose

for which it is being reserved. By using these securities as an instrument company can manage

its cash. Investment in marketable securities are far better than idle cash because idle cash

doesn’t give return and cash deposited in bank offers very low returns whereas investment in

securities offers a better return and safety of investment too (Gibson, 2011). Short term liabilities

are generally due for payment in a year. The period of maturity of these marketable securities is

also falls within a year which is the best way to pay off short term liabilities. The Company has

to fulfill some regulatory requirements too such as maintaining working capital at a specified

level or for measuring company’s solvency and liquidity (Reilly and Brown, 2011).

The graph has depicted a downward trend in past three years which indicates that

company is not able to collect its debts on time and company is selling its product on

credit. It shows that company is following the strategy to sale on credit to increase its

sales and then collecting its debts. This can results in negatively impacting the future

financial performance of the company (Arnold, 2013).

Asset Turnover Ratio: Asset Turnover Ratio depicts the company efficiency in using its

assets to generate revenue. It measures the assets contribution towards per dollar of sales.

In the past three years we can say company is not efficiently using its resources to

generate revenue as there is a downward trend in asset turnover ratio. It was 0.80 times in

2016 which comes to 0.65 times in 2018. Net sales have been increased in the past three

years but still company is not using its resources to its best. Domino’s Pizza is able to

generate higher revenue with the available resources. It should have a look in to it

(Krantz, 2016).

2.3: Use of marketable securities for cash management

Marketable securities are financial instrument that can be realized in cash at a reasonable

price. Marketable securities are held by company for cash management because maturity of these

securities are between 3 months to 1 year and can be easily liquidated whenever cash is required

on stock exchange or in any other way. The rates of marketable securities are affected very little

in terms of price and that is why it can easily bought and sold in the market (Schlichting, 2013).

Marketable securities that are available in Domino’s Pizza’s current assets are investment

in mutual funds, cash equivalents, advertising Fund cash equivalent and advertising fund

investments. Restriction is imposed on some funds so that the fund can be used for the purpose

for which it is being reserved. By using these securities as an instrument company can manage

its cash. Investment in marketable securities are far better than idle cash because idle cash

doesn’t give return and cash deposited in bank offers very low returns whereas investment in

securities offers a better return and safety of investment too (Gibson, 2011). Short term liabilities

are generally due for payment in a year. The period of maturity of these marketable securities is

also falls within a year which is the best way to pay off short term liabilities. The Company has

to fulfill some regulatory requirements too such as maintaining working capital at a specified

level or for measuring company’s solvency and liquidity (Reilly and Brown, 2011).

12

Domino’s Pizza is investing in mutual funds and cash equivalents so that it can pay off its

short term liabilities. Company’s investment in marketable securities such as advertisement fund

and advertisement fund investment which are restricted is for advertisement and promotion of

domino’s brand in future. By investing in such securities company is also complying with its

regulatory requirements and attaining faith of bankers and creditors by maintaining liquidity and

solvency.

2.4: Application of sensitivity analysis in capital budgeting problem

Project Life 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per

year 450,000.00$

Initial Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Information Provided

Domino’s Pizza is investing in mutual funds and cash equivalents so that it can pay off its

short term liabilities. Company’s investment in marketable securities such as advertisement fund

and advertisement fund investment which are restricted is for advertisement and promotion of

domino’s brand in future. By investing in such securities company is also complying with its

regulatory requirements and attaining faith of bankers and creditors by maintaining liquidity and

solvency.

2.4: Application of sensitivity analysis in capital budgeting problem

Project Life 4 Years

Cost of Equipment 2,000,000.00$

Reisdual Value 200,000.00$

Depreciation Method Straight Line

Life of Equipment 4 years

Depreciation of Equipment per

year 450,000.00$

Initial Working Capital 600,000.00$

Recovery of working capital 600,000.00$

Selling Units per year 300000 per year

Selling Price 20.00$

Variable Cost 12.00$

Fixed Cost 300,000.00$

Discount Rate 10%

Tax Rate 30%

Information Provided

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.