Financial Accounting: Double Entry, Trial Balance & Final Accounts

VerifiedAdded on 2024/06/04

|14

|970

|71

Report

AI Summary

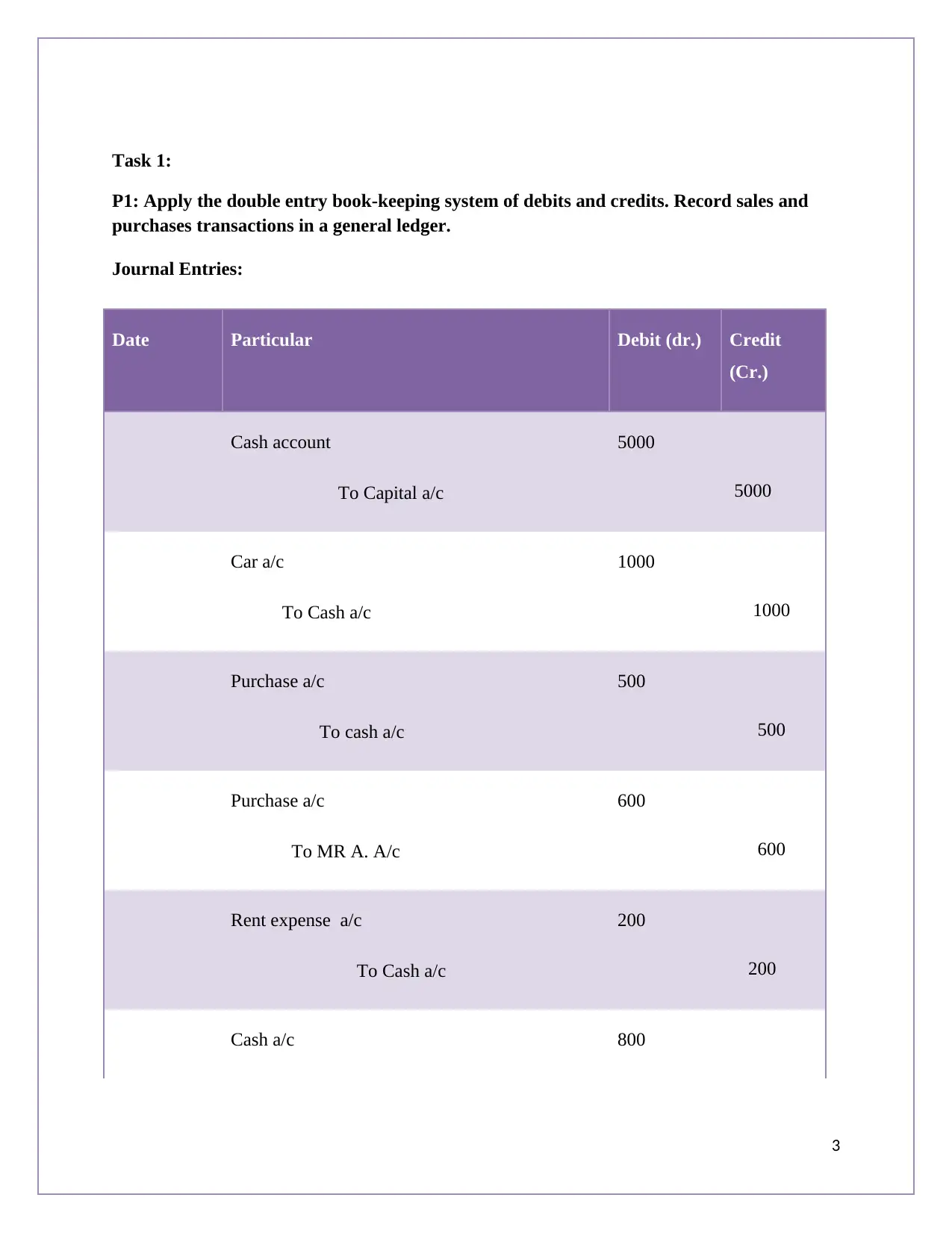

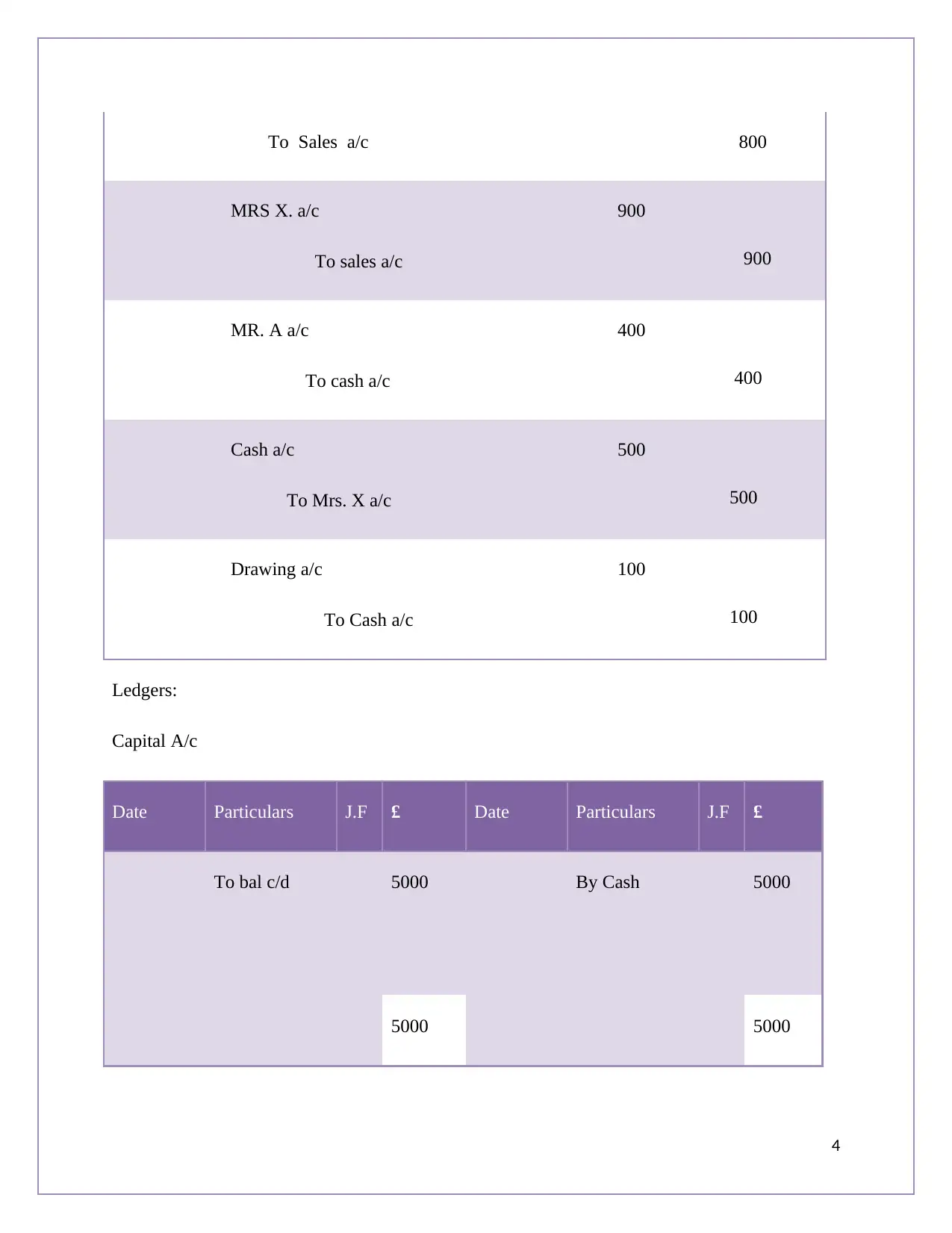

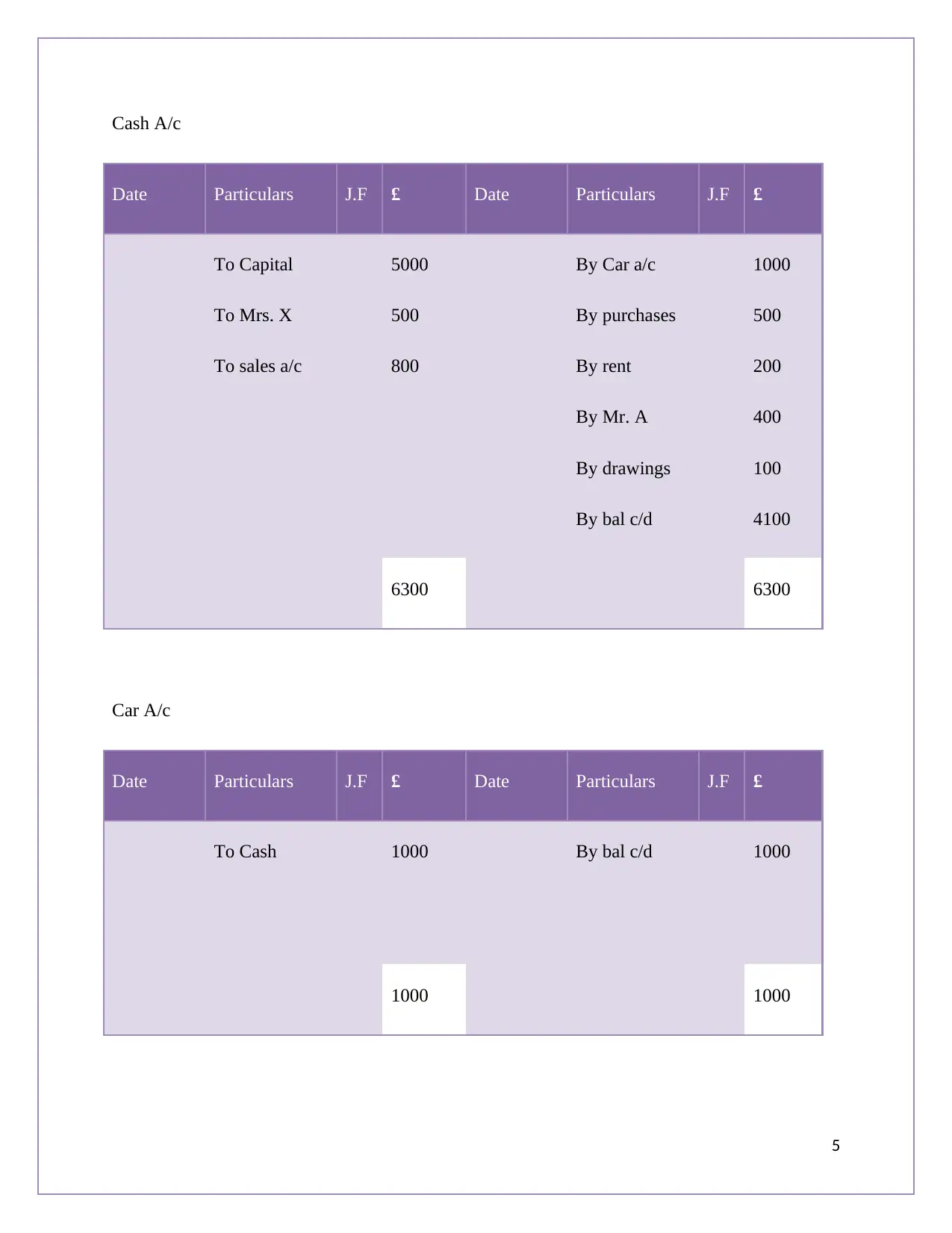

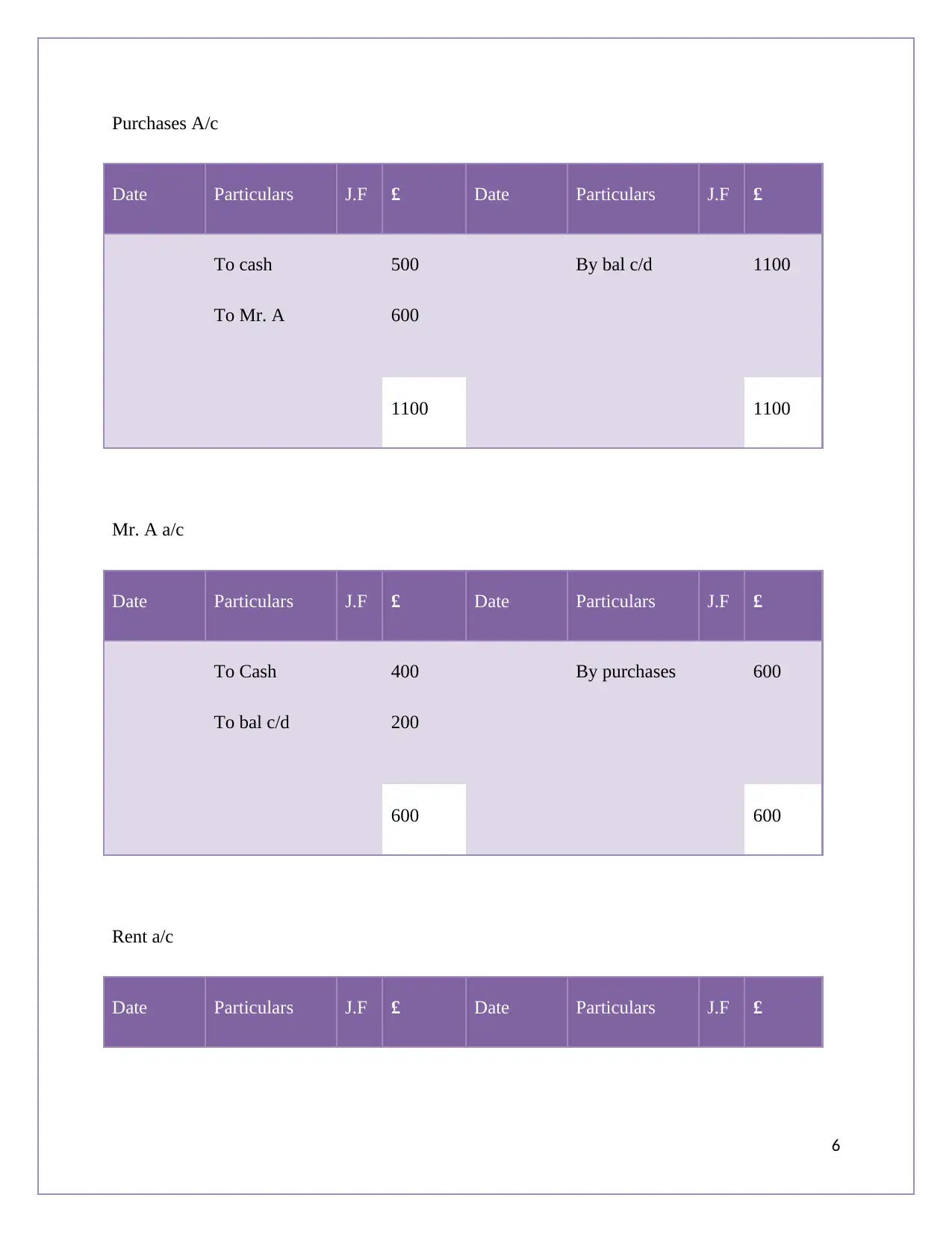

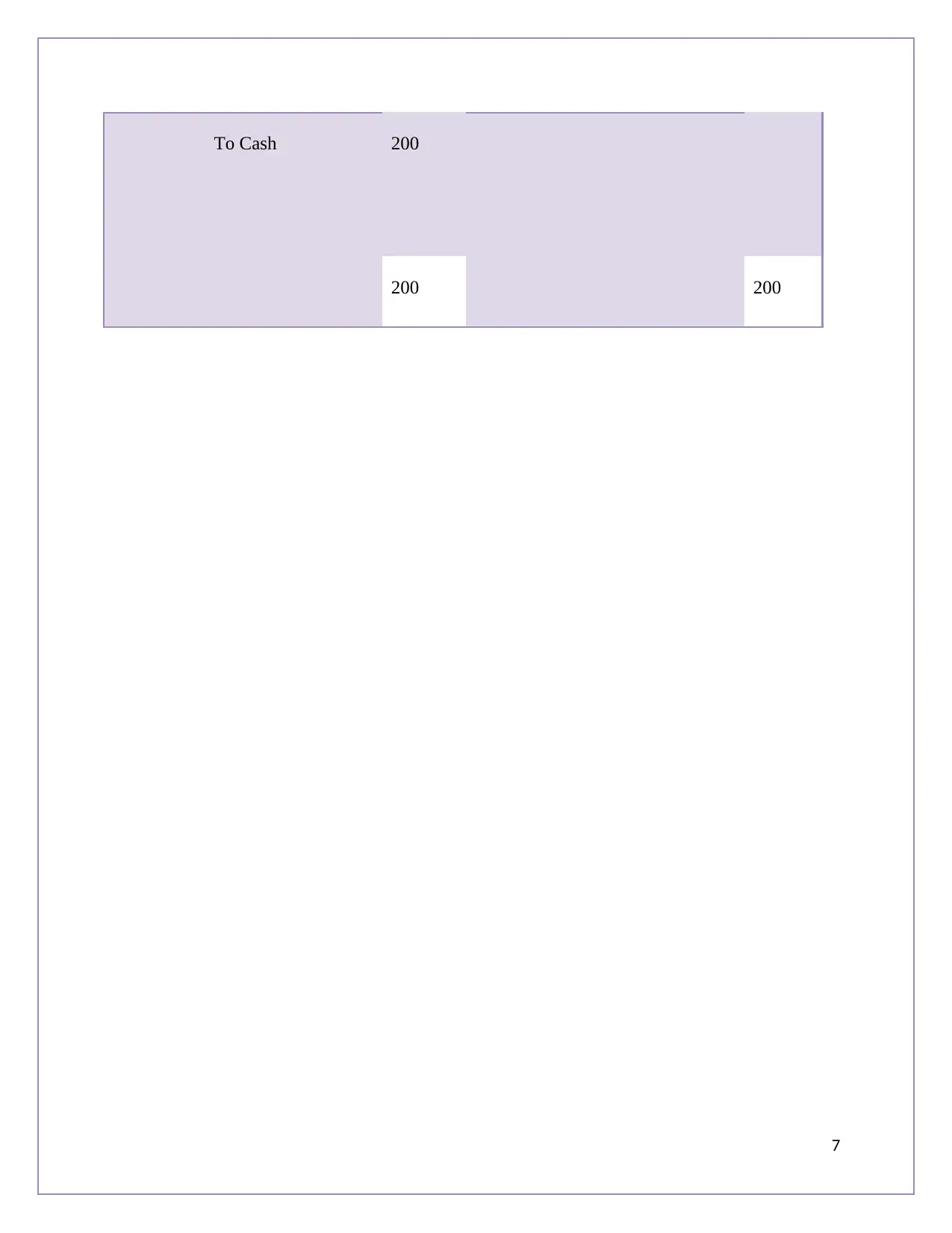

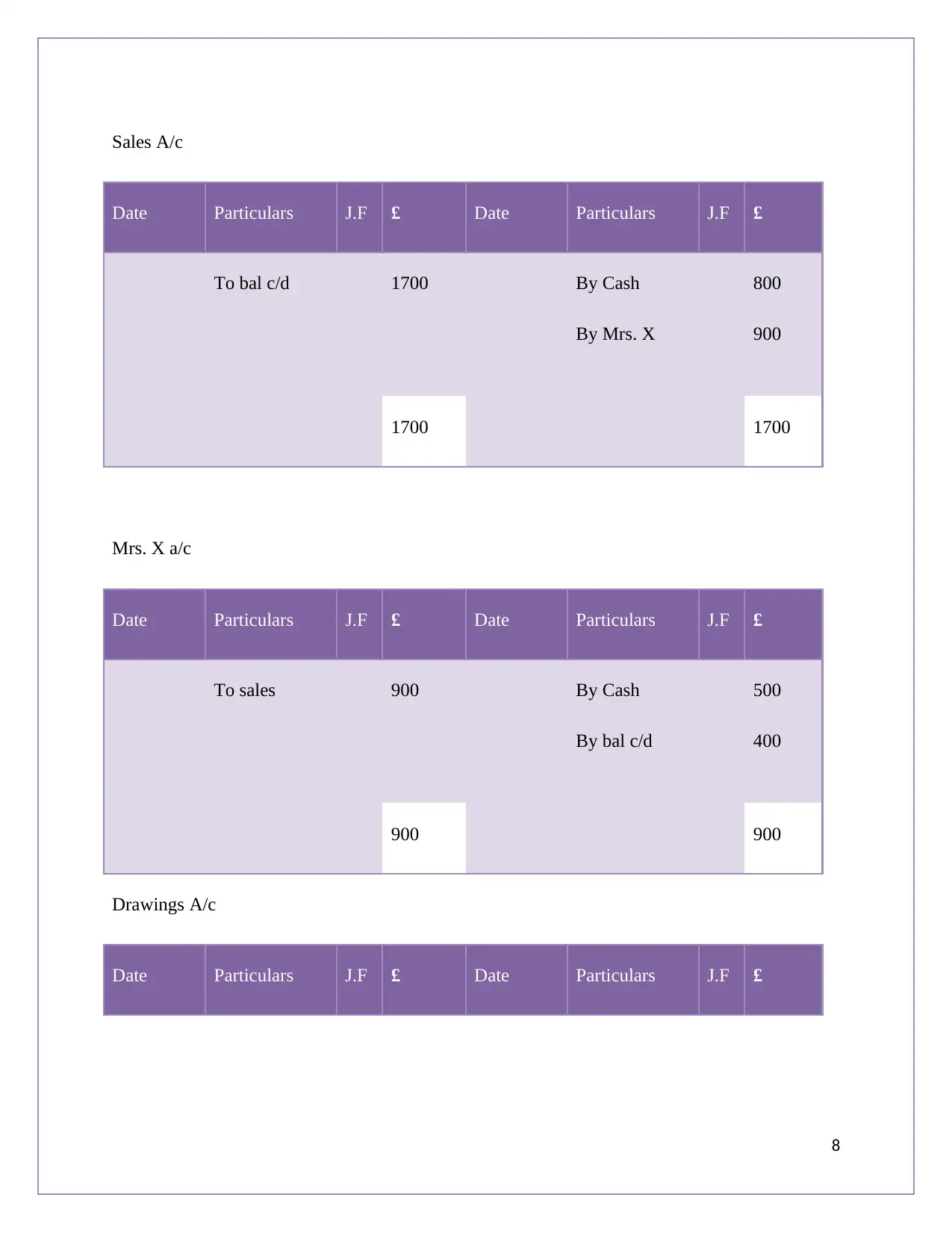

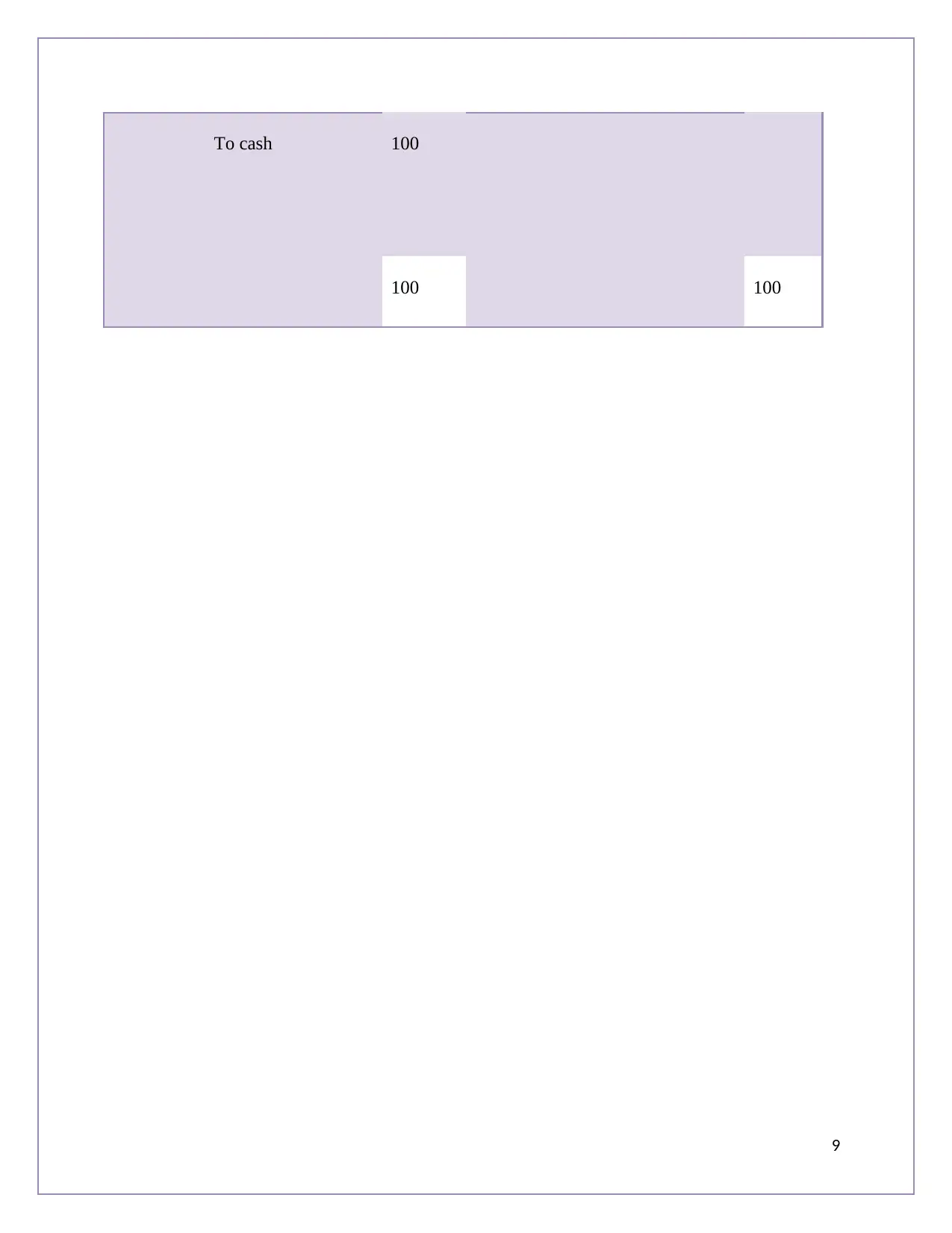

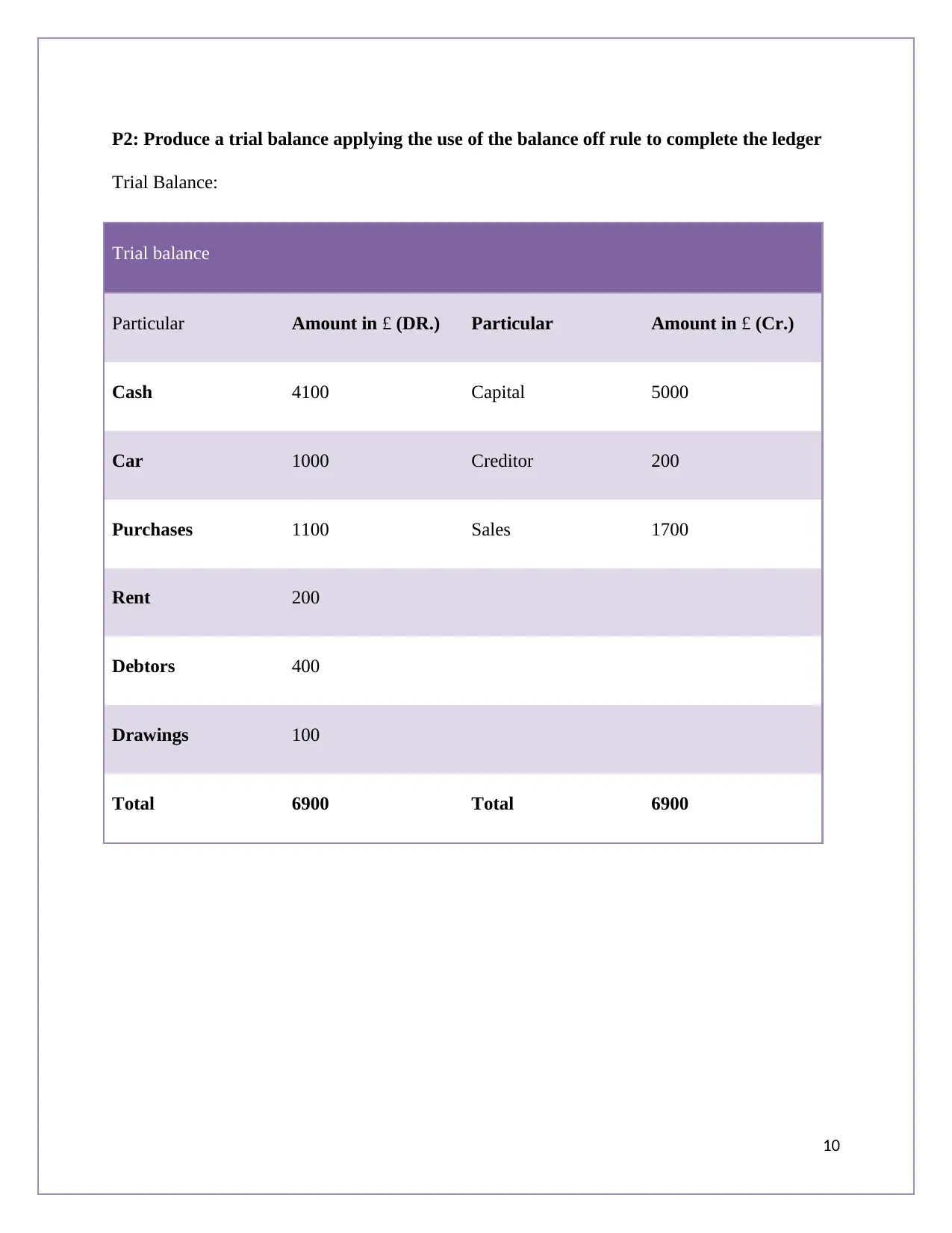

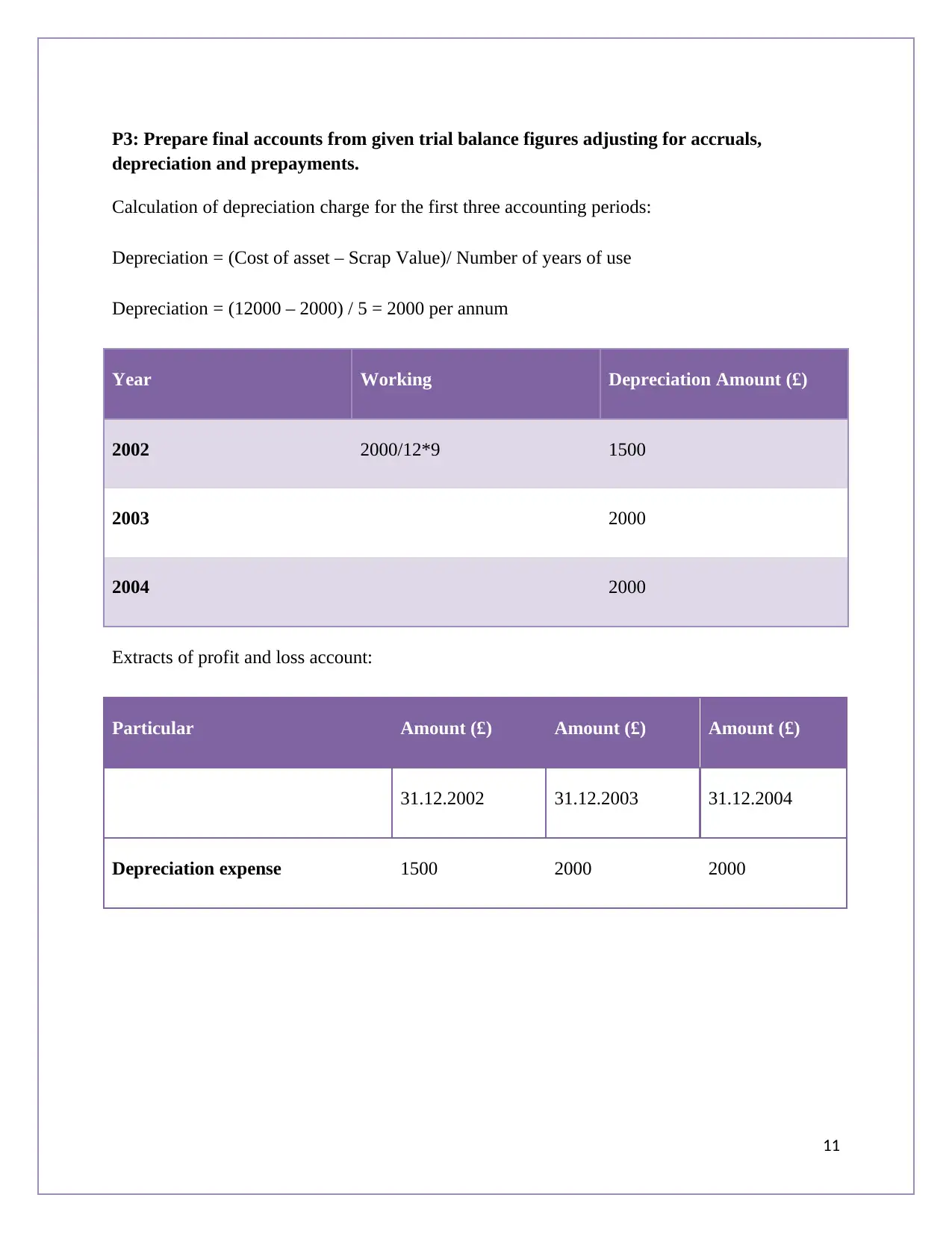

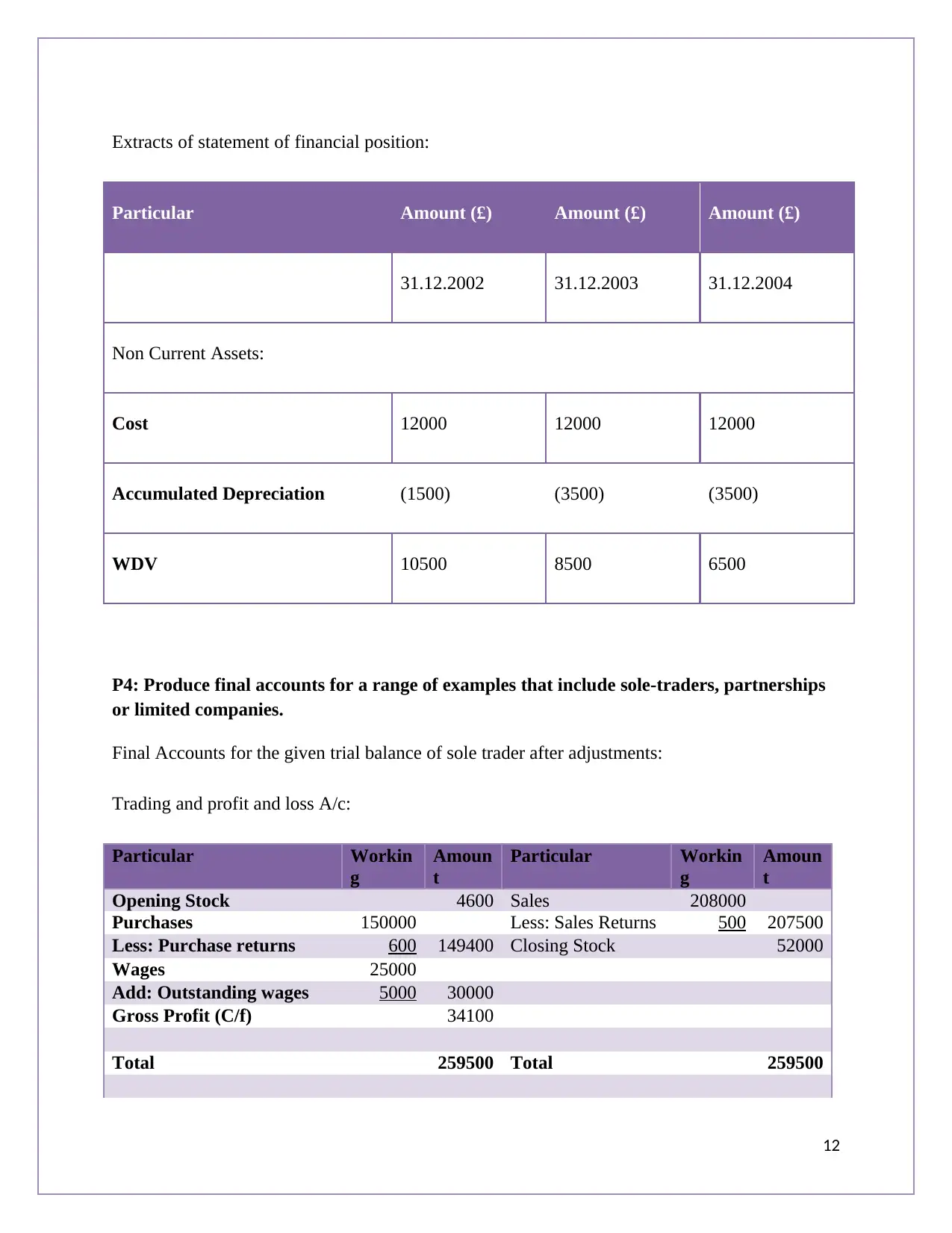

This financial accounting report provides a comprehensive overview of key accounting principles and techniques. It begins with an application of the double-entry bookkeeping system, recording sales and purchase transactions in a general ledger and extracting a trial balance. The report then progresses to preparing final accounts for sole proprietorships, partnerships, and limited companies, incorporating adjustments for accruals, depreciation, and prepayments. Furthermore, the report includes the preparation of a bank reconciliation statement and demonstrates the use of suspense accounts for reconciling discrepancies. The report showcases the application of these principles with journal entries, ledgers, trial balance, and final accounts preparation, providing a practical understanding of financial accounting concepts. Desklib offers a wealth of similar solved assignments and past papers for students seeking additional resources.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.