Recording Financial Transactions: Double Entry Bookkeeping Methods

VerifiedAdded on 2023/06/09

|18

|4145

|147

Report

AI Summary

This report details the process of recording financial transactions using double-entry bookkeeping, emphasizing accuracy and timeliness. It covers the chronological steps of recording transactions, defining key bookkeeping terms, and preparing ledger accounts and a trial balance. The report also demonstrates the application of double-entry bookkeeping to various business transactions, utilizing books of prime entry, journals, and ledgers. Additionally, it includes the preparation of a bank reconciliation statement to identify discrepancies and a discussion on the roles and differences between control and suspense accounts, along with control account reconciliation for accounts receivable and payable. The report aims to provide a comprehensive understanding of financial transaction recording and reconciliation processes.

Recording Financial

Transactions

Transactions

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1. How to record double entry bookkeeping transactions in a timely and accurate way?.........3

P2 Apply a range of business transactions using double entry bookkeeping, books of prime

entry, journals and ledgers...........................................................................................................4

P3 Using data provided, extract ledger balances into a trial balance for an organisation to

accurately record transactions....................................................................................................10

P4 Prepare a bank reconciliation statement from given data for an organisation......................11

P5 Explain the role and differences between control and suspense accounts............................13

P6. Perform control account reconciliation for accounts receivable and payable from given

data.............................................................................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

MAIN BODY...................................................................................................................................3

P1. How to record double entry bookkeeping transactions in a timely and accurate way?.........3

P2 Apply a range of business transactions using double entry bookkeeping, books of prime

entry, journals and ledgers...........................................................................................................4

P3 Using data provided, extract ledger balances into a trial balance for an organisation to

accurately record transactions....................................................................................................10

P4 Prepare a bank reconciliation statement from given data for an organisation......................11

P5 Explain the role and differences between control and suspense accounts............................13

P6. Perform control account reconciliation for accounts receivable and payable from given

data.............................................................................................................................................14

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Bookkeeping is the recording of all the financial transactions including purchases, sales,

receipts and payment (Burke, 2019). In this report, the chronological order of recording

transactions will be explained with defining some book keeping terms to understand better. A

trial balance and ledger accounts will be prepared to show the accurate way of recording entries.

Additionally, bank reconciliation statement to show the bank entries and identify errors and

omissions. Lastly, control and suspense account will be differentiated and performed for

accounts receivable and payable.

MAIN BODY

P1. How to record double entry bookkeeping transactions in a timely and accurate way?

Double entry book keeping is a place where each and every transaction is recorded twice

in the books of accounts.

The double entry book keeping is divided among several steps and that are:

1. Produce document: A document that is most common is the sales invoice, the document

might differ according to the activities of the business. A business deed can be selling,

buying or providing loan in cash or kind. It is referred to as a business transaction and

this document is called as accounting source document.

2. Recording: The business document contains some important information like date,

name, descriptive transaction and the amount. These details are used to record the entry

in the day book or book keeping journals. These journals describe the transaction in a

summary form so that it is easy for the reader to understand. A transaction without

quantitative value is not recorded in the accounts (Čegar, Poljašević and Šnjegota, 2019).

3. Update accounts: The amount or the value is recorded in the books. Each and every

account has a different ledger. Sometimes one account contains many transactions so that

account might exceed a page or two. A ledger is made in a T format. In this, the amount

will be entered either on the left side or the right side depending on the type of account

and type of transaction. In double entry system, each transaction affects two accounts to

balance.

4. Debit and Credit: The amount is entered using debit credit procedure. The entry is

recorded once in debit and other in credit always. A book keeper should be well versed

Bookkeeping is the recording of all the financial transactions including purchases, sales,

receipts and payment (Burke, 2019). In this report, the chronological order of recording

transactions will be explained with defining some book keeping terms to understand better. A

trial balance and ledger accounts will be prepared to show the accurate way of recording entries.

Additionally, bank reconciliation statement to show the bank entries and identify errors and

omissions. Lastly, control and suspense account will be differentiated and performed for

accounts receivable and payable.

MAIN BODY

P1. How to record double entry bookkeeping transactions in a timely and accurate way?

Double entry book keeping is a place where each and every transaction is recorded twice

in the books of accounts.

The double entry book keeping is divided among several steps and that are:

1. Produce document: A document that is most common is the sales invoice, the document

might differ according to the activities of the business. A business deed can be selling,

buying or providing loan in cash or kind. It is referred to as a business transaction and

this document is called as accounting source document.

2. Recording: The business document contains some important information like date,

name, descriptive transaction and the amount. These details are used to record the entry

in the day book or book keeping journals. These journals describe the transaction in a

summary form so that it is easy for the reader to understand. A transaction without

quantitative value is not recorded in the accounts (Čegar, Poljašević and Šnjegota, 2019).

3. Update accounts: The amount or the value is recorded in the books. Each and every

account has a different ledger. Sometimes one account contains many transactions so that

account might exceed a page or two. A ledger is made in a T format. In this, the amount

will be entered either on the left side or the right side depending on the type of account

and type of transaction. In double entry system, each transaction affects two accounts to

balance.

4. Debit and Credit: The amount is entered using debit credit procedure. The entry is

recorded once in debit and other in credit always. A book keeper should be well versed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

with the knowledge of transactions that come on debit side and transactions on the credit

side. For example, expenses are always debited and incomes are always credited.

5. Chart of accounts: The names and numbers of ledgers are found in the chart of

accounts. All the accounts made either go in the income statement or the balance sheet.

The balance sheet accounts are, assets, liabilities and equity. Income statement consists of

all the income and expenses of the business (Harris and Wonglimpiyarat, 2019).

6. Mathematical formula of double entry: It is called as the accounting equation which is

used to maintain the structure of the ledger.

7. Preparation of Trial Balance: It is prepared to ensure that the debit and credit matches.

If any corrections are to be made, the keeper can do it now because if doesn't match then

the financial statements will be faultily produced.

8. Preparation of Financial Statements: After the trial balance matches and everything is

recorded, then financial statements like income statement and balance sheet is prepared.

These are prepared to know how the organisation is performing. A tax accountant will

prepare specialised accounts to calculate the income tax for the year. Certain steps that

are included for this process are:

Adjusting entries are to be prepared for accruals and deferred transactions.

Closing entries and preparing a modified trial balance.

P2 Apply a range of business transactions using double entry bookkeeping, books of prime entry,

journals and ledgers.

1. Double entry bookkeeping: It is a concept that is used in present day book keeping

which is defined as financial transaction that is recorded in two ledger accounts once in

credit side and once in debit side to satisfy the accounting equation.

Accounting equation: Assets = Liabilities + Equity

The double entry book keeping standardizes the accounting process and enhances the

accuracy of financial statements and minimizing the errors. For example, if a business takes a

loan from bank. The borrowed amount raises the liability as well as the asset of the company i.e.

there will be an increase in cash at bank and an increase in long term liabilities (Hou, Wang and

Luo, 2020).

side. For example, expenses are always debited and incomes are always credited.

5. Chart of accounts: The names and numbers of ledgers are found in the chart of

accounts. All the accounts made either go in the income statement or the balance sheet.

The balance sheet accounts are, assets, liabilities and equity. Income statement consists of

all the income and expenses of the business (Harris and Wonglimpiyarat, 2019).

6. Mathematical formula of double entry: It is called as the accounting equation which is

used to maintain the structure of the ledger.

7. Preparation of Trial Balance: It is prepared to ensure that the debit and credit matches.

If any corrections are to be made, the keeper can do it now because if doesn't match then

the financial statements will be faultily produced.

8. Preparation of Financial Statements: After the trial balance matches and everything is

recorded, then financial statements like income statement and balance sheet is prepared.

These are prepared to know how the organisation is performing. A tax accountant will

prepare specialised accounts to calculate the income tax for the year. Certain steps that

are included for this process are:

Adjusting entries are to be prepared for accruals and deferred transactions.

Closing entries and preparing a modified trial balance.

P2 Apply a range of business transactions using double entry bookkeeping, books of prime entry,

journals and ledgers.

1. Double entry bookkeeping: It is a concept that is used in present day book keeping

which is defined as financial transaction that is recorded in two ledger accounts once in

credit side and once in debit side to satisfy the accounting equation.

Accounting equation: Assets = Liabilities + Equity

The double entry book keeping standardizes the accounting process and enhances the

accuracy of financial statements and minimizing the errors. For example, if a business takes a

loan from bank. The borrowed amount raises the liability as well as the asset of the company i.e.

there will be an increase in cash at bank and an increase in long term liabilities (Hou, Wang and

Luo, 2020).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Books of prime entry: A book where the entries are recorded before entering into the

double entry system. These books include, daybook, cash-book and journal. To cross-

check the transactions, looking at the ledgers might be a tedious task so instead prime

books are used to find the information. It provides a chronological record and mistakes

can be easily identified. It can also be used for future reference and provide backup in

case anything goes wrong with books of accounts.

3. Journals: It is an account that contains all the financial transactions related top the

account which is used for future reconciling and transfer of information such as general

ledger. It consists of the date and the amount of transaction which a short description.

Main information that is included in journals are, sales, expenses, cash, inventory and

debts. These transactions should be recorded hand to hand because the guess work later

might cause errors.

4. Ledgers: It is an account or record used to store book keeping entries which will later be

used for balance sheet and income statements. Posting to a ledger is the process of

recording credit and debits (Jin, Shang and Ma, 2019). A ledger is a place where all the

accounting entries are entered.

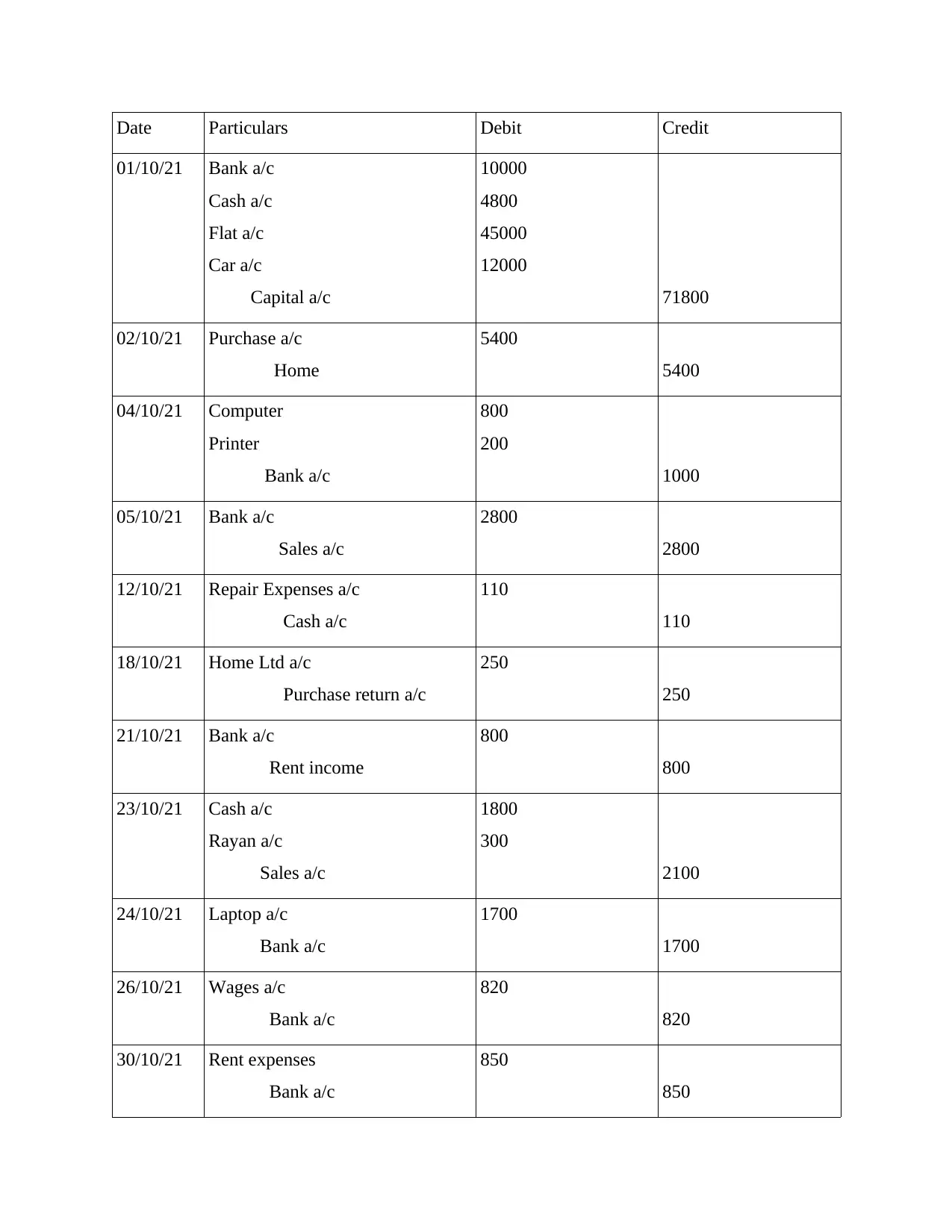

Following is the list of business transactions:

1. Capital invested in business £71800 divided among back, cash, flat and car with amounts

being 10000, 4800, 45000 and 12000 respectively on 1st October 2021.

2. Purchased a home for £5400 on 2nd October.

3. Purchased a computer and a printer fro £800 and £200 respectively on 4th October.

4. Sold goods worth £2800 on 5th October.

5. Paid £110 for repairs on 12th October.

6. Received rent of £800 on 21th October.

7. Sold goods worth £1800 to Rayan in cash and £300 in credit on 23rd October.

8. Purchased a laptop worth £1700 from bank on 24th October.

9. Paid wages £820 by bank on 26th October.

10. Paid rent £850 by bank on 30th October.

11. Drawings made of £1200 by bank on 31st October.

12. Received £150 cash from Rayan on 31st October.

double entry system. These books include, daybook, cash-book and journal. To cross-

check the transactions, looking at the ledgers might be a tedious task so instead prime

books are used to find the information. It provides a chronological record and mistakes

can be easily identified. It can also be used for future reference and provide backup in

case anything goes wrong with books of accounts.

3. Journals: It is an account that contains all the financial transactions related top the

account which is used for future reconciling and transfer of information such as general

ledger. It consists of the date and the amount of transaction which a short description.

Main information that is included in journals are, sales, expenses, cash, inventory and

debts. These transactions should be recorded hand to hand because the guess work later

might cause errors.

4. Ledgers: It is an account or record used to store book keeping entries which will later be

used for balance sheet and income statements. Posting to a ledger is the process of

recording credit and debits (Jin, Shang and Ma, 2019). A ledger is a place where all the

accounting entries are entered.

Following is the list of business transactions:

1. Capital invested in business £71800 divided among back, cash, flat and car with amounts

being 10000, 4800, 45000 and 12000 respectively on 1st October 2021.

2. Purchased a home for £5400 on 2nd October.

3. Purchased a computer and a printer fro £800 and £200 respectively on 4th October.

4. Sold goods worth £2800 on 5th October.

5. Paid £110 for repairs on 12th October.

6. Received rent of £800 on 21th October.

7. Sold goods worth £1800 to Rayan in cash and £300 in credit on 23rd October.

8. Purchased a laptop worth £1700 from bank on 24th October.

9. Paid wages £820 by bank on 26th October.

10. Paid rent £850 by bank on 30th October.

11. Drawings made of £1200 by bank on 31st October.

12. Received £150 cash from Rayan on 31st October.

Date Particulars Debit Credit

01/10/21 Bank a/c

Cash a/c

Flat a/c

Car a/c

Capital a/c

10000

4800

45000

12000

71800

02/10/21 Purchase a/c

Home

5400

5400

04/10/21 Computer

Printer

Bank a/c

800

200

1000

05/10/21 Bank a/c

Sales a/c

2800

2800

12/10/21 Repair Expenses a/c

Cash a/c

110

110

18/10/21 Home Ltd a/c

Purchase return a/c

250

250

21/10/21 Bank a/c

Rent income

800

800

23/10/21 Cash a/c

Rayan a/c

Sales a/c

1800

300

2100

24/10/21 Laptop a/c

Bank a/c

1700

1700

26/10/21 Wages a/c

Bank a/c

820

820

30/10/21 Rent expenses

Bank a/c

850

850

01/10/21 Bank a/c

Cash a/c

Flat a/c

Car a/c

Capital a/c

10000

4800

45000

12000

71800

02/10/21 Purchase a/c

Home

5400

5400

04/10/21 Computer

Printer

Bank a/c

800

200

1000

05/10/21 Bank a/c

Sales a/c

2800

2800

12/10/21 Repair Expenses a/c

Cash a/c

110

110

18/10/21 Home Ltd a/c

Purchase return a/c

250

250

21/10/21 Bank a/c

Rent income

800

800

23/10/21 Cash a/c

Rayan a/c

Sales a/c

1800

300

2100

24/10/21 Laptop a/c

Bank a/c

1700

1700

26/10/21 Wages a/c

Bank a/c

820

820

30/10/21 Rent expenses

Bank a/c

850

850

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

31/10/21 Drawings a/c

Bank a/c

1200

1200

31/10/21 Cash a/c

Rayan a/c

150

150

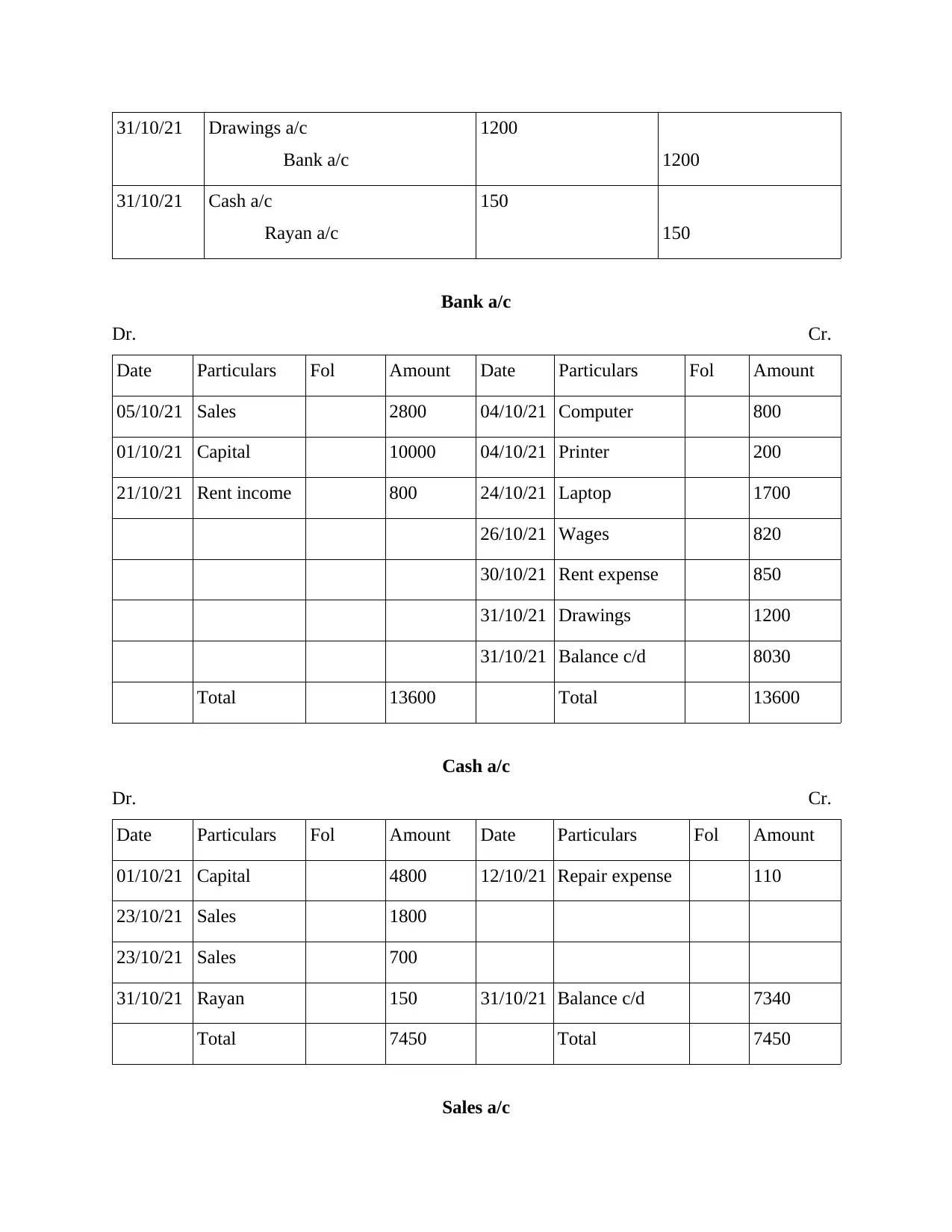

Bank a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

05/10/21 Sales 2800 04/10/21 Computer 800

01/10/21 Capital 10000 04/10/21 Printer 200

21/10/21 Rent income 800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent expense 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

Total 13600 Total 13600

Cash a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 4800 12/10/21 Repair expense 110

23/10/21 Sales 1800

23/10/21 Sales 700

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

Total 7450 Total 7450

Sales a/c

Bank a/c

1200

1200

31/10/21 Cash a/c

Rayan a/c

150

150

Bank a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

05/10/21 Sales 2800 04/10/21 Computer 800

01/10/21 Capital 10000 04/10/21 Printer 200

21/10/21 Rent income 800 24/10/21 Laptop 1700

26/10/21 Wages 820

30/10/21 Rent expense 850

31/10/21 Drawings 1200

31/10/21 Balance c/d 8030

Total 13600 Total 13600

Cash a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 4800 12/10/21 Repair expense 110

23/10/21 Sales 1800

23/10/21 Sales 700

31/10/21 Rayan 150 31/10/21 Balance c/d 7340

Total 7450 Total 7450

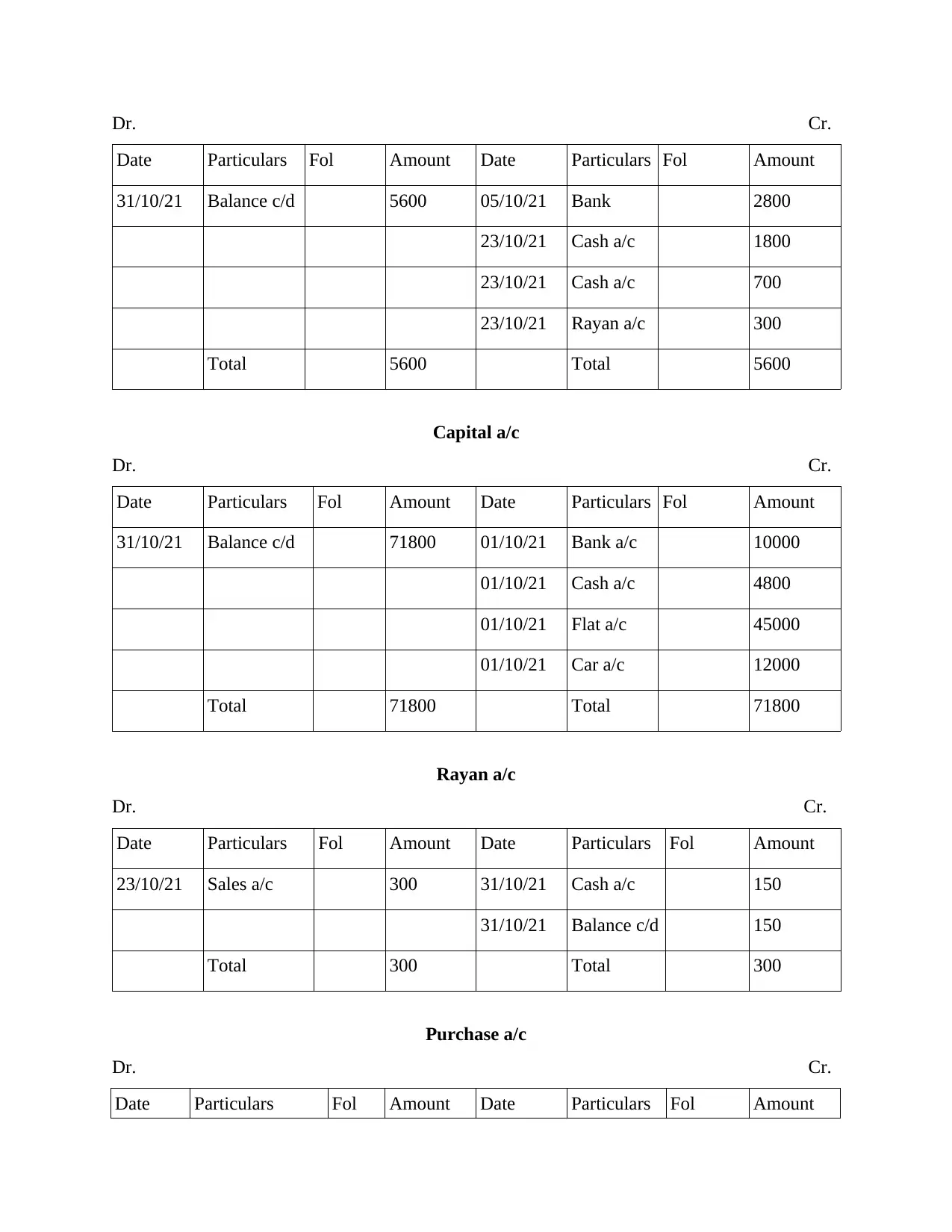

Sales a/c

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 5600 05/10/21 Bank 2800

23/10/21 Cash a/c 1800

23/10/21 Cash a/c 700

23/10/21 Rayan a/c 300

Total 5600 Total 5600

Capital a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 71800 01/10/21 Bank a/c 10000

01/10/21 Cash a/c 4800

01/10/21 Flat a/c 45000

01/10/21 Car a/c 12000

Total 71800 Total 71800

Rayan a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

23/10/21 Sales a/c 300 31/10/21 Cash a/c 150

31/10/21 Balance c/d 150

Total 300 Total 300

Purchase a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 5600 05/10/21 Bank 2800

23/10/21 Cash a/c 1800

23/10/21 Cash a/c 700

23/10/21 Rayan a/c 300

Total 5600 Total 5600

Capital a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Balance c/d 71800 01/10/21 Bank a/c 10000

01/10/21 Cash a/c 4800

01/10/21 Flat a/c 45000

01/10/21 Car a/c 12000

Total 71800 Total 71800

Rayan a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

23/10/21 Sales a/c 300 31/10/21 Cash a/c 150

31/10/21 Balance c/d 150

Total 300 Total 300

Purchase a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

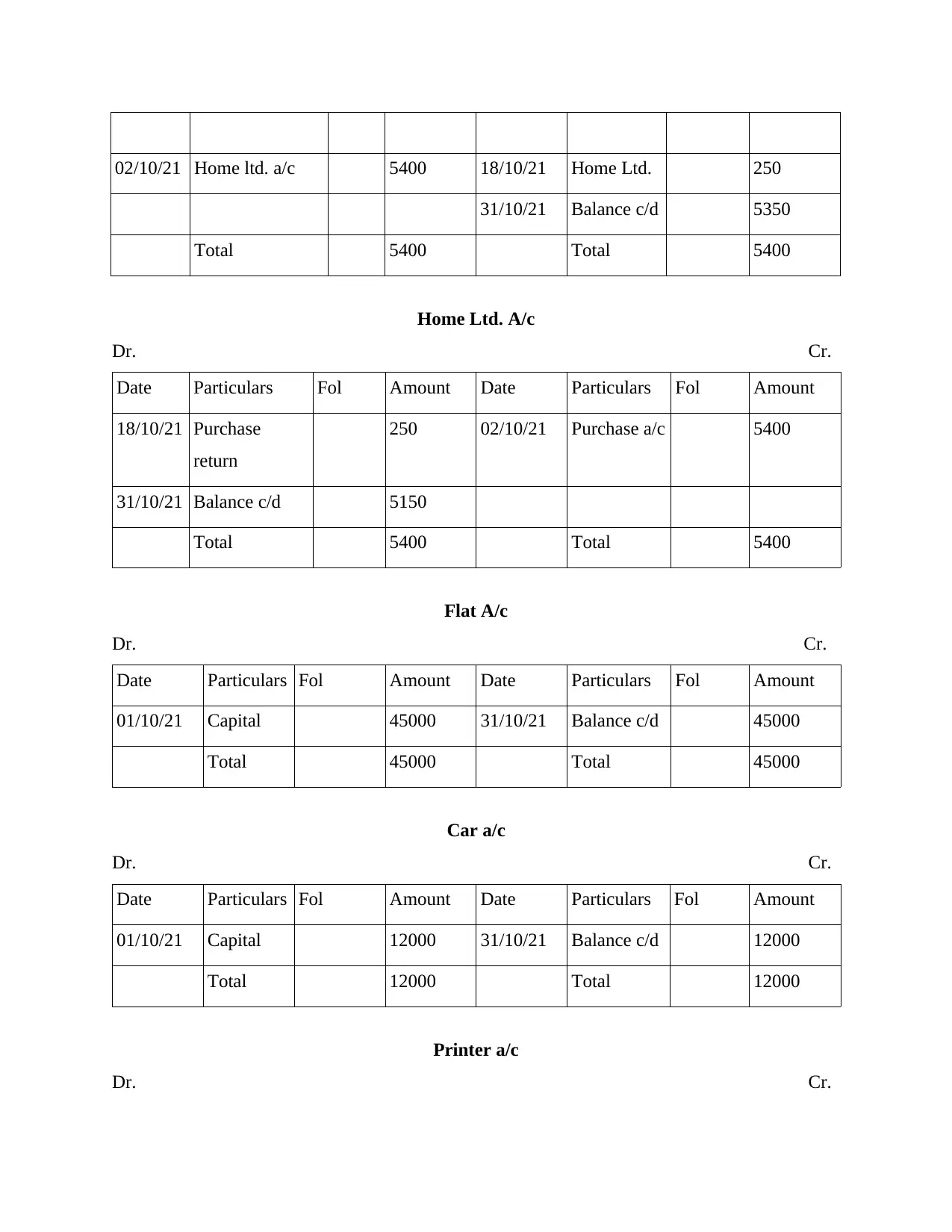

02/10/21 Home ltd. a/c 5400 18/10/21 Home Ltd. 250

31/10/21 Balance c/d 5350

Total 5400 Total 5400

Home Ltd. A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

18/10/21 Purchase

return

250 02/10/21 Purchase a/c 5400

31/10/21 Balance c/d 5150

Total 5400 Total 5400

Flat A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

Total 45000 Total 45000

Car a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

Total 12000 Total 12000

Printer a/c

Dr. Cr.

31/10/21 Balance c/d 5350

Total 5400 Total 5400

Home Ltd. A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

18/10/21 Purchase

return

250 02/10/21 Purchase a/c 5400

31/10/21 Balance c/d 5150

Total 5400 Total 5400

Flat A/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 45000 31/10/21 Balance c/d 45000

Total 45000 Total 45000

Car a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

01/10/21 Capital 12000 31/10/21 Balance c/d 12000

Total 12000 Total 12000

Printer a/c

Dr. Cr.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Date Particulars Fol Amount Date Particulars Fol Amount

04/10/21 Bank a/c 200 31/10/21 Balance c/d 200

Total 200 Total 200

Drawings a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Bank a/c 1200 31/10/21 Balance c/d 1200

Total 1200 Total 1200

Wages a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

26/10/21 Bank a/c 820 31/10/21 Balance c/d 820

Total 820 Total 820

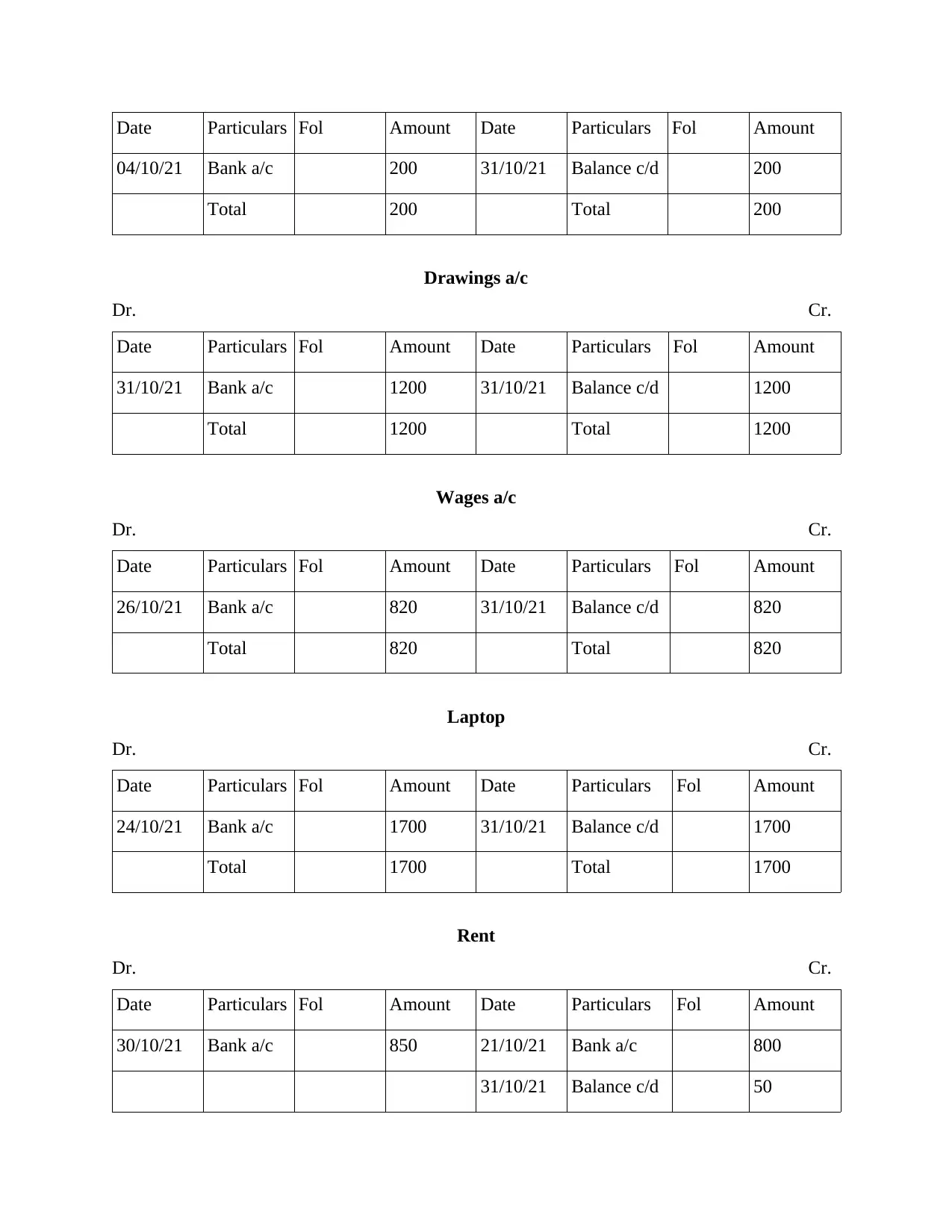

Laptop

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

24/10/21 Bank a/c 1700 31/10/21 Balance c/d 1700

Total 1700 Total 1700

Rent

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

30/10/21 Bank a/c 850 21/10/21 Bank a/c 800

31/10/21 Balance c/d 50

04/10/21 Bank a/c 200 31/10/21 Balance c/d 200

Total 200 Total 200

Drawings a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

31/10/21 Bank a/c 1200 31/10/21 Balance c/d 1200

Total 1200 Total 1200

Wages a/c

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

26/10/21 Bank a/c 820 31/10/21 Balance c/d 820

Total 820 Total 820

Laptop

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

24/10/21 Bank a/c 1700 31/10/21 Balance c/d 1700

Total 1700 Total 1700

Rent

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

30/10/21 Bank a/c 850 21/10/21 Bank a/c 800

31/10/21 Balance c/d 50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

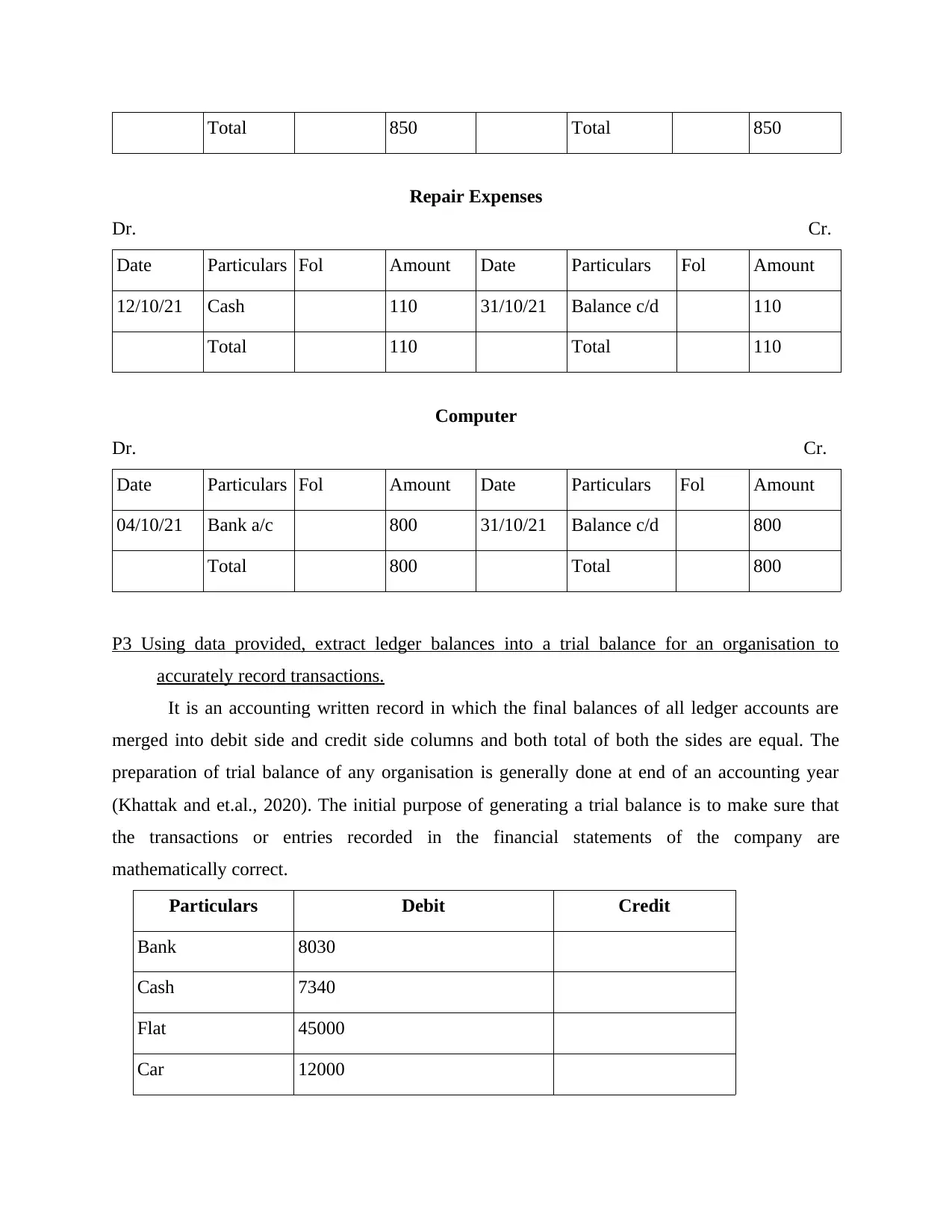

Total 850 Total 850

Repair Expenses

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

Total 110 Total 110

Computer

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

04/10/21 Bank a/c 800 31/10/21 Balance c/d 800

Total 800 Total 800

P3 Using data provided, extract ledger balances into a trial balance for an organisation to

accurately record transactions.

It is an accounting written record in which the final balances of all ledger accounts are

merged into debit side and credit side columns and both total of both the sides are equal. The

preparation of trial balance of any organisation is generally done at end of an accounting year

(Khattak and et.al., 2020). The initial purpose of generating a trial balance is to make sure that

the transactions or entries recorded in the financial statements of the company are

mathematically correct.

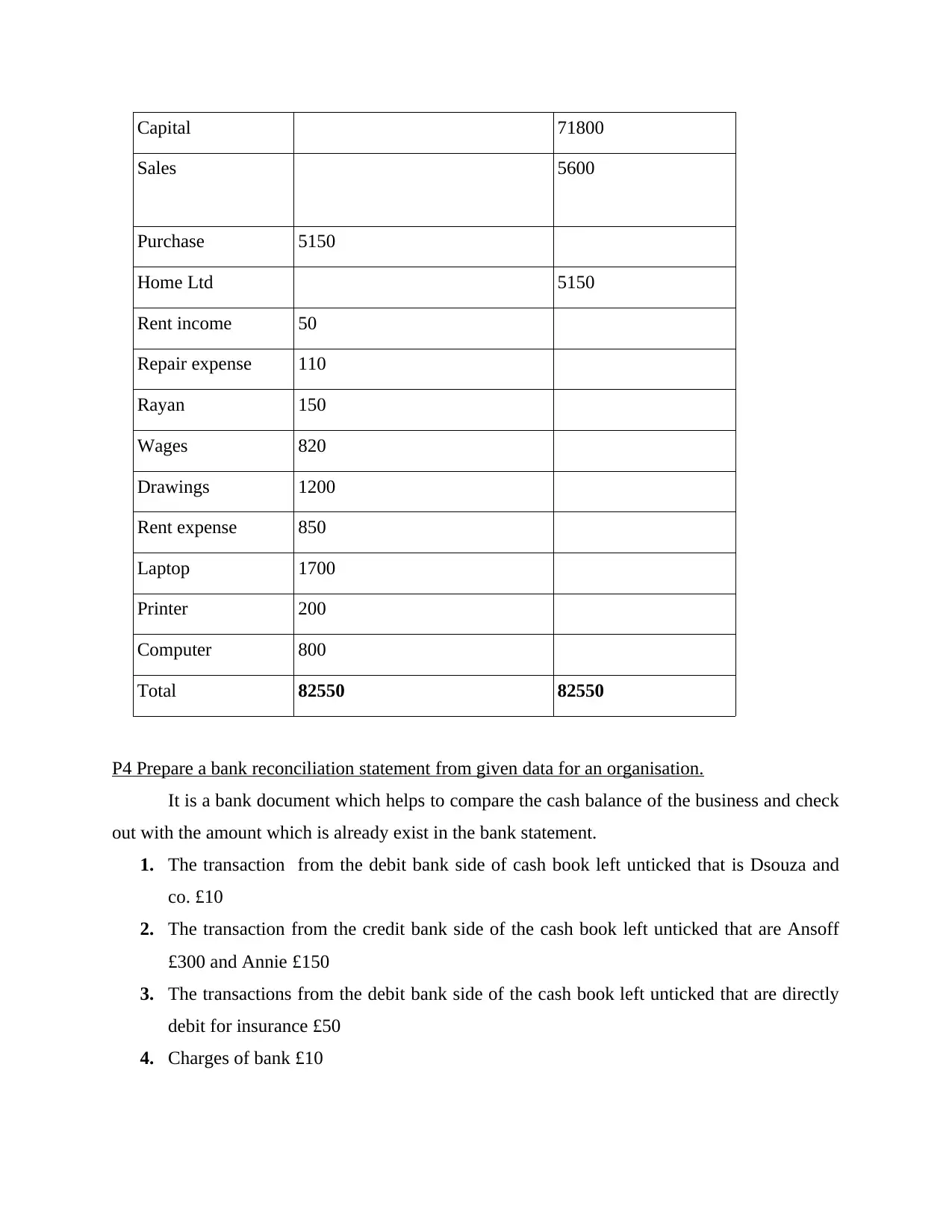

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Repair Expenses

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

12/10/21 Cash 110 31/10/21 Balance c/d 110

Total 110 Total 110

Computer

Dr. Cr.

Date Particulars Fol Amount Date Particulars Fol Amount

04/10/21 Bank a/c 800 31/10/21 Balance c/d 800

Total 800 Total 800

P3 Using data provided, extract ledger balances into a trial balance for an organisation to

accurately record transactions.

It is an accounting written record in which the final balances of all ledger accounts are

merged into debit side and credit side columns and both total of both the sides are equal. The

preparation of trial balance of any organisation is generally done at end of an accounting year

(Khattak and et.al., 2020). The initial purpose of generating a trial balance is to make sure that

the transactions or entries recorded in the financial statements of the company are

mathematically correct.

Particulars Debit Credit

Bank 8030

Cash 7340

Flat 45000

Car 12000

Capital 71800

Sales 5600

Purchase 5150

Home Ltd 5150

Rent income 50

Repair expense 110

Rayan 150

Wages 820

Drawings 1200

Rent expense 850

Laptop 1700

Printer 200

Computer 800

Total 82550 82550

P4 Prepare a bank reconciliation statement from given data for an organisation.

It is a bank document which helps to compare the cash balance of the business and check

out with the amount which is already exist in the bank statement.

1. The transaction from the debit bank side of cash book left unticked that is Dsouza and

co. £10

2. The transaction from the credit bank side of the cash book left unticked that are Ansoff

£300 and Annie £150

3. The transactions from the debit bank side of the cash book left unticked that are directly

debit for insurance £50

4. Charges of bank £10

Sales 5600

Purchase 5150

Home Ltd 5150

Rent income 50

Repair expense 110

Rayan 150

Wages 820

Drawings 1200

Rent expense 850

Laptop 1700

Printer 200

Computer 800

Total 82550 82550

P4 Prepare a bank reconciliation statement from given data for an organisation.

It is a bank document which helps to compare the cash balance of the business and check

out with the amount which is already exist in the bank statement.

1. The transaction from the debit bank side of cash book left unticked that is Dsouza and

co. £10

2. The transaction from the credit bank side of the cash book left unticked that are Ansoff

£300 and Annie £150

3. The transactions from the debit bank side of the cash book left unticked that are directly

debit for insurance £50

4. Charges of bank £10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.