Analysis of Financial Information and Risk Factors at DIPL: A Report

VerifiedAdded on 2020/03/13

|11

|2774

|79

Report

AI Summary

This report provides a comprehensive analysis of the financial information and risk factors associated with Double Ink Printers Limited (DIPL). It begins with an executive summary outlining the report's objectives, which include examining audit planning, identifying inherent and fraud risk factors, and assessing their impact on the financial statements. The report delves into audit planning, detailing the application of analytical procedures and their influence on audit decisions. It identifies inherent risk factors stemming from the company's inventory valuation methods and business acquisitions, emphasizing their potential for material misstatements. Furthermore, the report addresses fraud risk factors, highlighting areas susceptible to fraudulent financial reporting and asset misstatement. The analysis includes a review of financial ratios and their implications for the audit process, culminating in conclusions and recommendations for effective financial reporting and audit practices. This report aims to provide a thorough understanding of the financial health and risk landscape of DIPL, offering valuable insights for auditors and stakeholders alike.

ANALYSIS OF FINANCIAL INFORMATION AND RISK FACTORS OF DOUBLE INK PRINTERS LIMITED (DIPL)

Student Name Student ID

8/14/2017

Student Name Student ID

8/14/2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

With this report, the main area of the focus has been the auditing and its aspects. As the title of

the report states that the analysis has been done of the financial information of the company, the

main emphasis has been laid on the process that is being followed by the company since its

inception for both financial and non financial matters and how the same is required to be dealt by

the auditors while planning for the audit for the year ending as on that date. The main aim of the

report is to provide how the auditor will plan his audit while conducting the preliminary

analytical procedures. The second major aim for which the report is prepared is to identify the

inherent risk factors that has arisen from the nature of the business of the company and the

procedure that the company have followed from its incorporation for accounting of the incomes

and expenses and procedures adopted to maintain the internal control system. The third major

aim is to identify the areas where there are chances of having the possibilities of fraud is very

high and which may affect the true and fair view of the financial statements. With these aims, the

report has been prepared.

2

With this report, the main area of the focus has been the auditing and its aspects. As the title of

the report states that the analysis has been done of the financial information of the company, the

main emphasis has been laid on the process that is being followed by the company since its

inception for both financial and non financial matters and how the same is required to be dealt by

the auditors while planning for the audit for the year ending as on that date. The main aim of the

report is to provide how the auditor will plan his audit while conducting the preliminary

analytical procedures. The second major aim for which the report is prepared is to identify the

inherent risk factors that has arisen from the nature of the business of the company and the

procedure that the company have followed from its incorporation for accounting of the incomes

and expenses and procedures adopted to maintain the internal control system. The third major

aim is to identify the areas where there are chances of having the possibilities of fraud is very

high and which may affect the true and fair view of the financial statements. With these aims, the

report has been prepared.

2

Table of Contents

Executive Summary 2

Introduction 4

Audit Planning 5

Inherent Risk Factors 8

Fraud Risk Factors and Its Impact on Audit 9

Conclusion and Recommendation 10

References 11

3

Executive Summary 2

Introduction 4

Audit Planning 5

Inherent Risk Factors 8

Fraud Risk Factors and Its Impact on Audit 9

Conclusion and Recommendation 10

References 11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial statement plays a very vital role for assessing the financial position and financial

performance of the company. Financial position is displayed by the statement of affairs or the

balance sheet and the financial performance is given by the statement of profit and loss for the

period ending. These financial statements should be prepared and presented in such a manner

that the financial position and the financial performance of the company shall be displayed to the

users of the financial statements in the true and fair manner. If in any case the financial

statements are not prepared in that manner then the chances of having the bad reputation of the

company in the market increases and gradually the chances of having the fraud occurrence

within the company will increase. Thus, the financial statements are the backbone of the

company and it shall be prepared with utmost due care. Through this report, the financial

statements and its requirements have been better viewed from the angle of the auditors of the

company. Auditors are the persons who certify that the company’s financial statements reflect

the true and fair view of the financial position and performance of the company. Thus, while

conducting the audit, the auditors are required to plan the audit in such a way that no area shall

be left and escape without the proper scrutiny by the auditors.

The aforesaid duty of the auditor is the major underline objective of the report. For the purpose

of the analysis, the company – Double Ink Printers Limited has been made available with proper

background information and the last three years financial information. In the beginning the

executive summary has been detailed giving the aims of the report. Thereafter, introduction has

been given about the report. Then the main body of the report has been started with the layout of

the plan that the auditors have prepared using the analytical procedures and how the same have

affected the planning decision. Secondly, as part of the audit, the risk assessment has been done

and two inherent risk factors have been identified from the nature of the operation of the business

and it has been explained as to how the risk have affected the risk of material misstatement in the

financial statement. Thirdly, the risk factors have been identified which contributes to the

fraudulent reporting of the transactions and has been explained as to how the risk factors have

affected the audit.

The report then has been ended with the proper conclusion and recommendation.

4

Financial statement plays a very vital role for assessing the financial position and financial

performance of the company. Financial position is displayed by the statement of affairs or the

balance sheet and the financial performance is given by the statement of profit and loss for the

period ending. These financial statements should be prepared and presented in such a manner

that the financial position and the financial performance of the company shall be displayed to the

users of the financial statements in the true and fair manner. If in any case the financial

statements are not prepared in that manner then the chances of having the bad reputation of the

company in the market increases and gradually the chances of having the fraud occurrence

within the company will increase. Thus, the financial statements are the backbone of the

company and it shall be prepared with utmost due care. Through this report, the financial

statements and its requirements have been better viewed from the angle of the auditors of the

company. Auditors are the persons who certify that the company’s financial statements reflect

the true and fair view of the financial position and performance of the company. Thus, while

conducting the audit, the auditors are required to plan the audit in such a way that no area shall

be left and escape without the proper scrutiny by the auditors.

The aforesaid duty of the auditor is the major underline objective of the report. For the purpose

of the analysis, the company – Double Ink Printers Limited has been made available with proper

background information and the last three years financial information. In the beginning the

executive summary has been detailed giving the aims of the report. Thereafter, introduction has

been given about the report. Then the main body of the report has been started with the layout of

the plan that the auditors have prepared using the analytical procedures and how the same have

affected the planning decision. Secondly, as part of the audit, the risk assessment has been done

and two inherent risk factors have been identified from the nature of the operation of the business

and it has been explained as to how the risk have affected the risk of material misstatement in the

financial statement. Thirdly, the risk factors have been identified which contributes to the

fraudulent reporting of the transactions and has been explained as to how the risk factors have

affected the audit.

The report then has been ended with the proper conclusion and recommendation.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

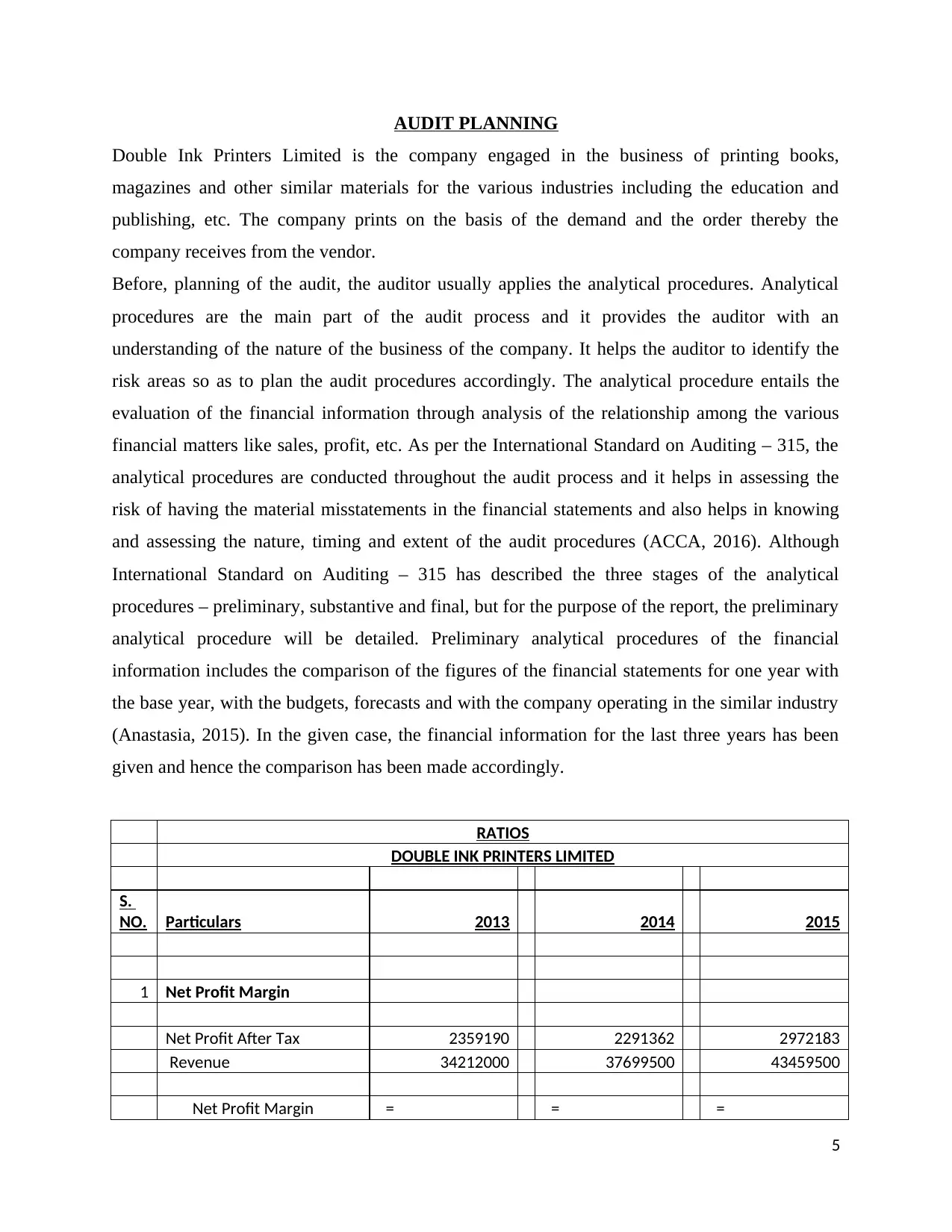

AUDIT PLANNING

Double Ink Printers Limited is the company engaged in the business of printing books,

magazines and other similar materials for the various industries including the education and

publishing, etc. The company prints on the basis of the demand and the order thereby the

company receives from the vendor.

Before, planning of the audit, the auditor usually applies the analytical procedures. Analytical

procedures are the main part of the audit process and it provides the auditor with an

understanding of the nature of the business of the company. It helps the auditor to identify the

risk areas so as to plan the audit procedures accordingly. The analytical procedure entails the

evaluation of the financial information through analysis of the relationship among the various

financial matters like sales, profit, etc. As per the International Standard on Auditing – 315, the

analytical procedures are conducted throughout the audit process and it helps in assessing the

risk of having the material misstatements in the financial statements and also helps in knowing

and assessing the nature, timing and extent of the audit procedures (ACCA, 2016). Although

International Standard on Auditing – 315 has described the three stages of the analytical

procedures – preliminary, substantive and final, but for the purpose of the report, the preliminary

analytical procedure will be detailed. Preliminary analytical procedures of the financial

information includes the comparison of the figures of the financial statements for one year with

the base year, with the budgets, forecasts and with the company operating in the similar industry

(Anastasia, 2015). In the given case, the financial information for the last three years has been

given and hence the comparison has been made accordingly.

RATIOS

DOUBLE INK PRINTERS LIMITED

S.

NO. Particulars 2013 2014 2015

1 Net Profit Margin

Net Profit After Tax 2359190 2291362 2972183

Revenue 34212000 37699500 43459500

Net Profit Margin = = =

5

Double Ink Printers Limited is the company engaged in the business of printing books,

magazines and other similar materials for the various industries including the education and

publishing, etc. The company prints on the basis of the demand and the order thereby the

company receives from the vendor.

Before, planning of the audit, the auditor usually applies the analytical procedures. Analytical

procedures are the main part of the audit process and it provides the auditor with an

understanding of the nature of the business of the company. It helps the auditor to identify the

risk areas so as to plan the audit procedures accordingly. The analytical procedure entails the

evaluation of the financial information through analysis of the relationship among the various

financial matters like sales, profit, etc. As per the International Standard on Auditing – 315, the

analytical procedures are conducted throughout the audit process and it helps in assessing the

risk of having the material misstatements in the financial statements and also helps in knowing

and assessing the nature, timing and extent of the audit procedures (ACCA, 2016). Although

International Standard on Auditing – 315 has described the three stages of the analytical

procedures – preliminary, substantive and final, but for the purpose of the report, the preliminary

analytical procedure will be detailed. Preliminary analytical procedures of the financial

information includes the comparison of the figures of the financial statements for one year with

the base year, with the budgets, forecasts and with the company operating in the similar industry

(Anastasia, 2015). In the given case, the financial information for the last three years has been

given and hence the comparison has been made accordingly.

RATIOS

DOUBLE INK PRINTERS LIMITED

S.

NO. Particulars 2013 2014 2015

1 Net Profit Margin

Net Profit After Tax 2359190 2291362 2972183

Revenue 34212000 37699500 43459500

Net Profit Margin = = =

5

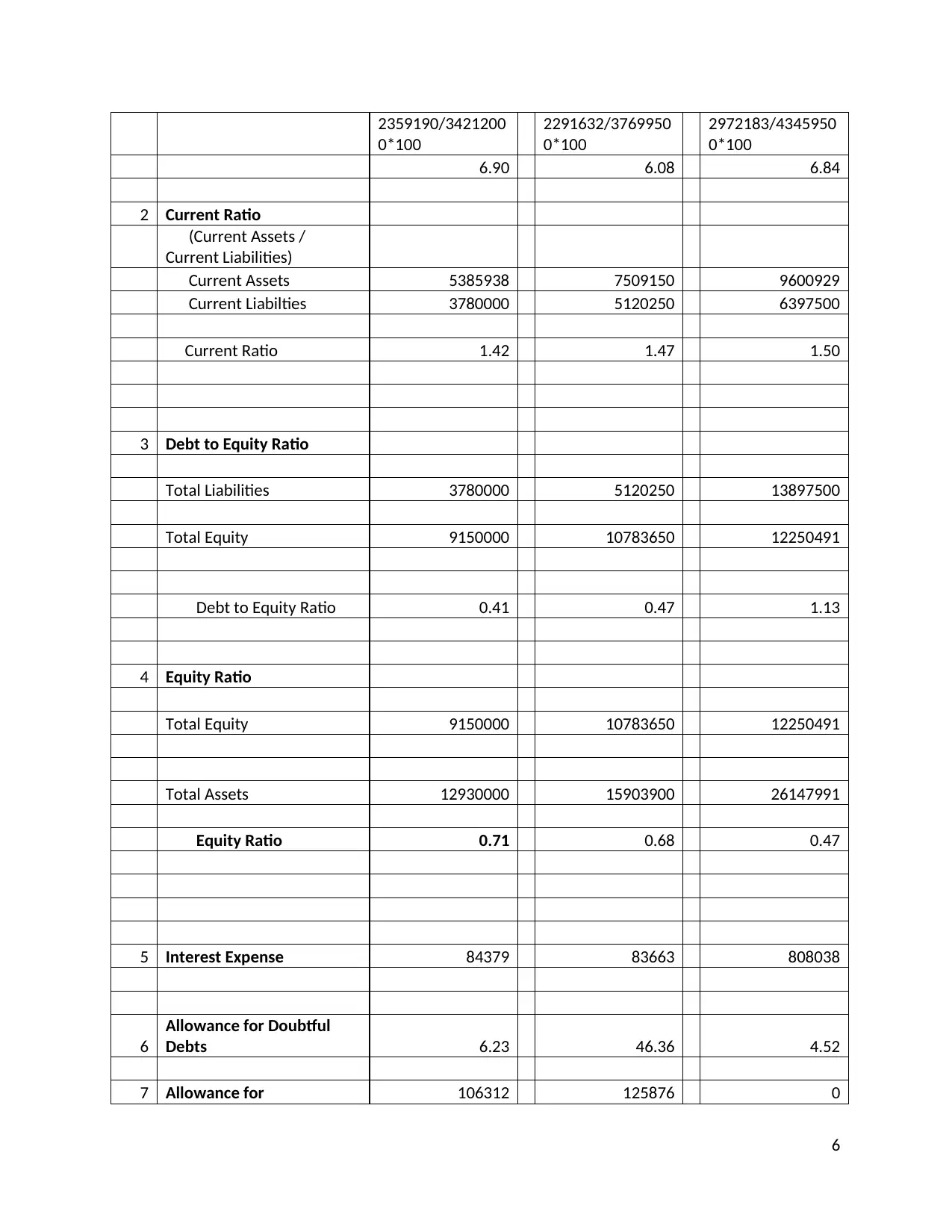

2359190/3421200

0*100

2291632/3769950

0*100

2972183/4345950

0*100

6.90 6.08 6.84

2 Current Ratio

(Current Assets /

Current Liabilities)

Current Assets 5385938 7509150 9600929

Current Liabilties 3780000 5120250 6397500

Current Ratio 1.42 1.47 1.50

3 Debt to Equity Ratio

Total Liabilities 3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to Equity Ratio 0.41 0.47 1.13

4 Equity Ratio

Total Equity 9150000 10783650 12250491

Total Assets 12930000 15903900 26147991

Equity Ratio 0.71 0.68 0.47

5 Interest Expense 84379 83663 808038

6

Allowance for Doubtful

Debts 6.23 46.36 4.52

7 Allowance for 106312 125876 0

6

0*100

2291632/3769950

0*100

2972183/4345950

0*100

6.90 6.08 6.84

2 Current Ratio

(Current Assets /

Current Liabilities)

Current Assets 5385938 7509150 9600929

Current Liabilties 3780000 5120250 6397500

Current Ratio 1.42 1.47 1.50

3 Debt to Equity Ratio

Total Liabilities 3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to Equity Ratio 0.41 0.47 1.13

4 Equity Ratio

Total Equity 9150000 10783650 12250491

Total Assets 12930000 15903900 26147991

Equity Ratio 0.71 0.68 0.47

5 Interest Expense 84379 83663 808038

6

Allowance for Doubtful

Debts 6.23 46.36 4.52

7 Allowance for 106312 125876 0

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

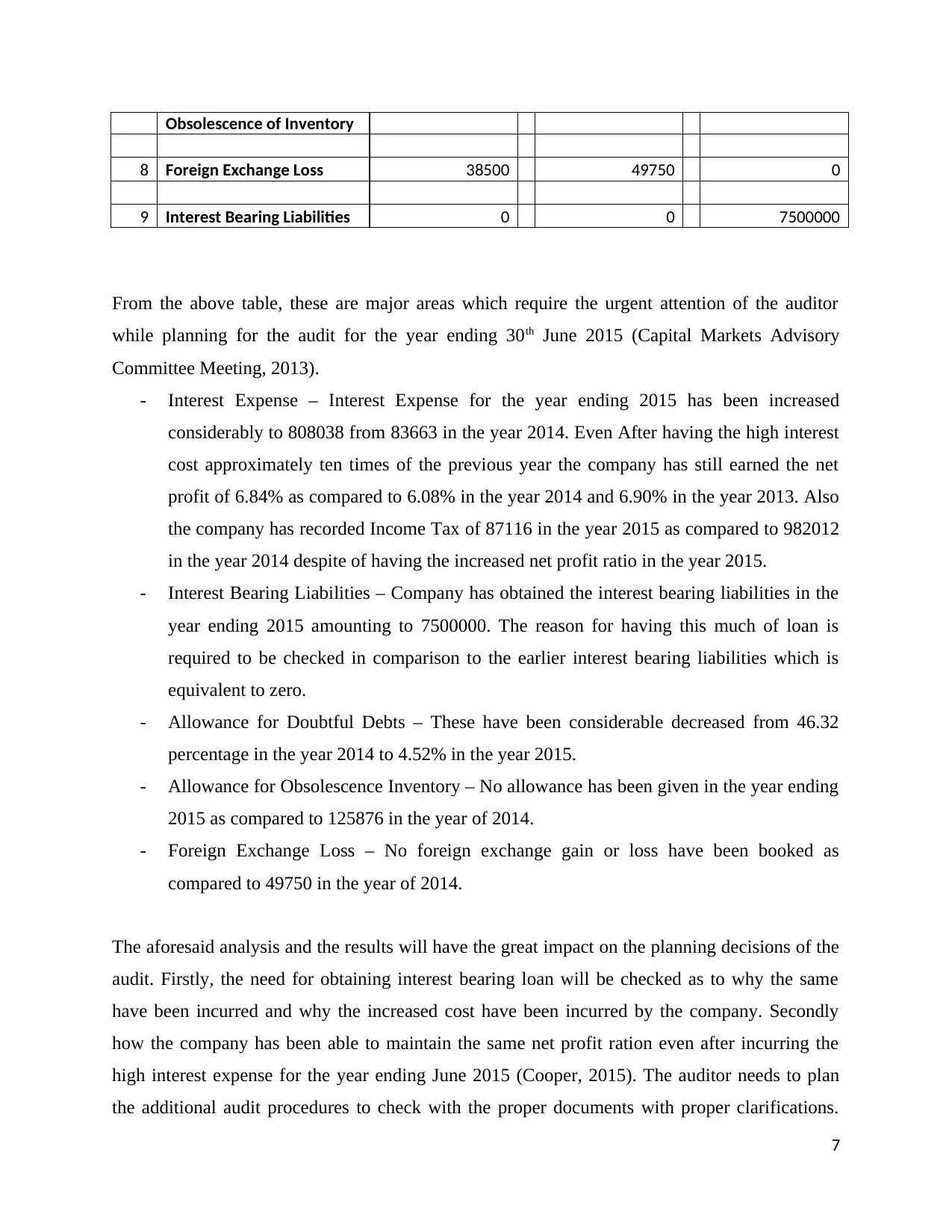

Obsolescence of Inventory

8 Foreign Exchange Loss 38500 49750 0

9 Interest Bearing Liabilities 0 0 7500000

From the above table, these are major areas which require the urgent attention of the auditor

while planning for the audit for the year ending 30th June 2015 (Capital Markets Advisory

Committee Meeting, 2013).

- Interest Expense – Interest Expense for the year ending 2015 has been increased

considerably to 808038 from 83663 in the year 2014. Even After having the high interest

cost approximately ten times of the previous year the company has still earned the net

profit of 6.84% as compared to 6.08% in the year 2014 and 6.90% in the year 2013. Also

the company has recorded Income Tax of 87116 in the year 2015 as compared to 982012

in the year 2014 despite of having the increased net profit ratio in the year 2015.

- Interest Bearing Liabilities – Company has obtained the interest bearing liabilities in the

year ending 2015 amounting to 7500000. The reason for having this much of loan is

required to be checked in comparison to the earlier interest bearing liabilities which is

equivalent to zero.

- Allowance for Doubtful Debts – These have been considerable decreased from 46.32

percentage in the year 2014 to 4.52% in the year 2015.

- Allowance for Obsolescence Inventory – No allowance has been given in the year ending

2015 as compared to 125876 in the year of 2014.

- Foreign Exchange Loss – No foreign exchange gain or loss have been booked as

compared to 49750 in the year of 2014.

The aforesaid analysis and the results will have the great impact on the planning decisions of the

audit. Firstly, the need for obtaining interest bearing loan will be checked as to why the same

have been incurred and why the increased cost have been incurred by the company. Secondly

how the company has been able to maintain the same net profit ration even after incurring the

high interest expense for the year ending June 2015 (Cooper, 2015). The auditor needs to plan

the additional audit procedures to check with the proper documents with proper clarifications.

7

8 Foreign Exchange Loss 38500 49750 0

9 Interest Bearing Liabilities 0 0 7500000

From the above table, these are major areas which require the urgent attention of the auditor

while planning for the audit for the year ending 30th June 2015 (Capital Markets Advisory

Committee Meeting, 2013).

- Interest Expense – Interest Expense for the year ending 2015 has been increased

considerably to 808038 from 83663 in the year 2014. Even After having the high interest

cost approximately ten times of the previous year the company has still earned the net

profit of 6.84% as compared to 6.08% in the year 2014 and 6.90% in the year 2013. Also

the company has recorded Income Tax of 87116 in the year 2015 as compared to 982012

in the year 2014 despite of having the increased net profit ratio in the year 2015.

- Interest Bearing Liabilities – Company has obtained the interest bearing liabilities in the

year ending 2015 amounting to 7500000. The reason for having this much of loan is

required to be checked in comparison to the earlier interest bearing liabilities which is

equivalent to zero.

- Allowance for Doubtful Debts – These have been considerable decreased from 46.32

percentage in the year 2014 to 4.52% in the year 2015.

- Allowance for Obsolescence Inventory – No allowance has been given in the year ending

2015 as compared to 125876 in the year of 2014.

- Foreign Exchange Loss – No foreign exchange gain or loss have been booked as

compared to 49750 in the year of 2014.

The aforesaid analysis and the results will have the great impact on the planning decisions of the

audit. Firstly, the need for obtaining interest bearing loan will be checked as to why the same

have been incurred and why the increased cost have been incurred by the company. Secondly

how the company has been able to maintain the same net profit ration even after incurring the

high interest expense for the year ending June 2015 (Cooper, 2015). The auditor needs to plan

the additional audit procedures to check with the proper documents with proper clarifications.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Thirdly, the company made the less allowance for the doubtful debts and some doubtful debts

have been written back in the year ending June 2015. The reasons for writing back is required to

be checked as to what circumstances have led to wrong interpretation of the doubtful debts last

year and how the same have been undervalued this current year. Fourthly, why the company has

not made any allowance for the obsolete inventory despite of having the high turnover as

compared to the last year of the 2014. Lastly, as per the Accounting Standards, the company is

required to account for gain or loss on foreign exchange. In the current year 2015, it depicts that

the company has not entered into any foreign currency transactions.

Thus, in this manner the results of the preliminary analytical procedures have greatly influenced

the planning decision of the auditor.

INHERENT RISK FACTORS

Audit risk plays very important role in the process of audit and without considering the same

audit cannot be effectively completed. There are three types of audit risk – Control Risk,

Detection risk and the Inherent Risk. In the given case study, the inherent risk is required to be

considered and discussed as to how the risk will affect the material misstatement in the financial

reporting level. Company - Double Ink Printers Limited since its inception has been following

the defined internal control processes and procedures and has the following inherent risk factor

that has been arisen from the operations of the company.

The company has been valuing its inventory on the average cost basis. Average cost

method averages the prices and value the inventory on that basis. In this case even if the

purchase price of the item is high, the value of that item will be less because it has been

valued on average cost basis (Gary, 2017). Through this the company have been

disclosing the inventory at lower of the cost and thus reducing the profit and the current

ratio. But with the stipulation made by the BDO Finance from whom the company has

obtained the loan, Board of the company decides to value the inventory at the FIFO basis

rather than the average cost basis. This depicts that this inherent risk factor will always

contributes towards the risk of having material misstatement in the financial reporting

level.

8

have been written back in the year ending June 2015. The reasons for writing back is required to

be checked as to what circumstances have led to wrong interpretation of the doubtful debts last

year and how the same have been undervalued this current year. Fourthly, why the company has

not made any allowance for the obsolete inventory despite of having the high turnover as

compared to the last year of the 2014. Lastly, as per the Accounting Standards, the company is

required to account for gain or loss on foreign exchange. In the current year 2015, it depicts that

the company has not entered into any foreign currency transactions.

Thus, in this manner the results of the preliminary analytical procedures have greatly influenced

the planning decision of the auditor.

INHERENT RISK FACTORS

Audit risk plays very important role in the process of audit and without considering the same

audit cannot be effectively completed. There are three types of audit risk – Control Risk,

Detection risk and the Inherent Risk. In the given case study, the inherent risk is required to be

considered and discussed as to how the risk will affect the material misstatement in the financial

reporting level. Company - Double Ink Printers Limited since its inception has been following

the defined internal control processes and procedures and has the following inherent risk factor

that has been arisen from the operations of the company.

The company has been valuing its inventory on the average cost basis. Average cost

method averages the prices and value the inventory on that basis. In this case even if the

purchase price of the item is high, the value of that item will be less because it has been

valued on average cost basis (Gary, 2017). Through this the company have been

disclosing the inventory at lower of the cost and thus reducing the profit and the current

ratio. But with the stipulation made by the BDO Finance from whom the company has

obtained the loan, Board of the company decides to value the inventory at the FIFO basis

rather than the average cost basis. This depicts that this inherent risk factor will always

contributes towards the risk of having material misstatement in the financial reporting

level.

8

Second major risk is that the company has acquired the business of the company –

Nuclear Publishing Limited and also the copyright of having the medical text books.

With the introduction of the new theory, the text books of the Nuclear Publishing Limited

will become futile and hence there will be the high chances of having the high obsolete

inventory.

Therefore, the above two factors have pure chances of having the material misstatements at the

financial reporting level.

FRAUD RISK FACTORS AND ITS IMPACT ON AUDIT

The management is held responsible for prevention and control of Fraud Risk factors in the

organization and its financial reporting. The auditor should consider the presence of risk factors

if exist at the time of planning of the audit so that the auditor can give fair opinion and his

opinion is not deceptive. Auditor has to take into consideration about two types of fraud risk

factors which are present in the organization like fraud factors by fraudulent financial reporting

and fraud by misstatement of Assets (Weiss, 2014).

In the given case of DIPL, the fraud factors that arising from fraudulent financial reporting which

an auditor should consider are as follows:-

Excessive Pressure on Employees :- With the implementation of new IT Software in

DIPL without proper testing and reconciliations, the situation of fraudulent financial

reporting increases. The IT Manager, Any Rogers was under extreme pressure to

implement and go live with new accounting system and this pressure and high

expectation from Board of the company can lead to high changes to frauds and wrong

reporting with new accounting system.

High Expectation from Outside Party:- In the year 2015, DIPL has taken a loan financing

from BDO Finance of $ 7.5 million with a condition that the DIPL will maintain the

Current ratio of more than 1.5.:1 and Debt Equity Ratio will not reach and exceed from

1:1 otherwise the DBO Finance will rolled back the funds ploughed in. This particular

situation creates the high chances of Frauds at the level of Financial Reporting in DIPL.

9

Nuclear Publishing Limited and also the copyright of having the medical text books.

With the introduction of the new theory, the text books of the Nuclear Publishing Limited

will become futile and hence there will be the high chances of having the high obsolete

inventory.

Therefore, the above two factors have pure chances of having the material misstatements at the

financial reporting level.

FRAUD RISK FACTORS AND ITS IMPACT ON AUDIT

The management is held responsible for prevention and control of Fraud Risk factors in the

organization and its financial reporting. The auditor should consider the presence of risk factors

if exist at the time of planning of the audit so that the auditor can give fair opinion and his

opinion is not deceptive. Auditor has to take into consideration about two types of fraud risk

factors which are present in the organization like fraud factors by fraudulent financial reporting

and fraud by misstatement of Assets (Weiss, 2014).

In the given case of DIPL, the fraud factors that arising from fraudulent financial reporting which

an auditor should consider are as follows:-

Excessive Pressure on Employees :- With the implementation of new IT Software in

DIPL without proper testing and reconciliations, the situation of fraudulent financial

reporting increases. The IT Manager, Any Rogers was under extreme pressure to

implement and go live with new accounting system and this pressure and high

expectation from Board of the company can lead to high changes to frauds and wrong

reporting with new accounting system.

High Expectation from Outside Party:- In the year 2015, DIPL has taken a loan financing

from BDO Finance of $ 7.5 million with a condition that the DIPL will maintain the

Current ratio of more than 1.5.:1 and Debt Equity Ratio will not reach and exceed from

1:1 otherwise the DBO Finance will rolled back the funds ploughed in. This particular

situation creates the high chances of Frauds at the level of Financial Reporting in DIPL.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

EFFECTS OF FRAUDS RISK FACTORS ON AUDIT

The above factors impact the conduct of audit and the auditor has to remain cautious while doing

audit about the above factors identified as fraud factors. The factors will enhance the working of

the Audit team in the following manner:-

The audit has to take big sample size for collecting accurate date and results from their

audit.

The auditor has to consider the high chances of instances of collision of the employees in

presentation of financial reports.

CONCLUSION AND RECOMMENDATION

Double Ink Printers is the company engaged in the business of printing books, magazines and

other similar articles. Although the company has the sound internal control systems and

procedures but still there are many risk factors which have contributed towards the material

misstatement in the financial statements of the company. Through the analytical procedures, the

auditor has been able to find out the areas where his planning decision may be affected and

therefore he has to look considerably on the financial statements of the company. Secondly, the

inherent risk factors that have been listed and detailed will definitely lead to the risk of having

material misstatement of the financial statements of the company and lastly the risk of having the

fraud and its underlying factors are so material that the risk factors will affect the audit. To

conclude, the company has the inherent risk and has major deviations in the financial

information which requires the urgent attention of the management.

To recommend, the company shall install such a system in place so as to avoid the factors which

have contributed to the inherent risk and fraud and which in turn will affect the financial

statements. Company shall install the best software where the intervention of the personal bias

may be deleted.

10

The above factors impact the conduct of audit and the auditor has to remain cautious while doing

audit about the above factors identified as fraud factors. The factors will enhance the working of

the Audit team in the following manner:-

The audit has to take big sample size for collecting accurate date and results from their

audit.

The auditor has to consider the high chances of instances of collision of the employees in

presentation of financial reports.

CONCLUSION AND RECOMMENDATION

Double Ink Printers is the company engaged in the business of printing books, magazines and

other similar articles. Although the company has the sound internal control systems and

procedures but still there are many risk factors which have contributed towards the material

misstatement in the financial statements of the company. Through the analytical procedures, the

auditor has been able to find out the areas where his planning decision may be affected and

therefore he has to look considerably on the financial statements of the company. Secondly, the

inherent risk factors that have been listed and detailed will definitely lead to the risk of having

material misstatement of the financial statements of the company and lastly the risk of having the

fraud and its underlying factors are so material that the risk factors will affect the audit. To

conclude, the company has the inherent risk and has major deviations in the financial

information which requires the urgent attention of the management.

To recommend, the company shall install such a system in place so as to avoid the factors which

have contributed to the inherent risk and fraud and which in turn will affect the financial

statements. Company shall install the best software where the intervention of the personal bias

may be deleted.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-

study-resources/p7/technical-articles/analytical-procedures.html accessed on 15-08-

2017.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 16-

08-2017.

Capital Markets Advisory Committee Meeting, (2013), “Conceptual Framework”

available on

http://www.ifrs.org/Meetings/MeetingDocs/Other%20Meeting/2013/March/AP

%203%20conceptual%20framework.pdf accessed on 16-08-2017.

Cooper S, (2015), “A Tale of Prudence”, available on http://www.ifrs.org/Investor-

resources/Investor-perspectives-2/Documents/Prudence_Investor-

Perspective_Conceptual-FW.PDF accessed on 16-08-2017.

Gary S., (2017), “The Importance of Inherent Risk Factors: Auditor’s Perceptions”,

Australian Accounting Review, Vol 3, Pp 38-44.

Weiss D, (2014), “Faithful Representation” available on

http://bschool.huji.ac.il/.upload/Seminars/Faithful%20Representation%20October

%202014.pdf accessed on 16-08-2017..

11

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-

study-resources/p7/technical-articles/analytical-procedures.html accessed on 15-08-

2017.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 16-

08-2017.

Capital Markets Advisory Committee Meeting, (2013), “Conceptual Framework”

available on

http://www.ifrs.org/Meetings/MeetingDocs/Other%20Meeting/2013/March/AP

%203%20conceptual%20framework.pdf accessed on 16-08-2017.

Cooper S, (2015), “A Tale of Prudence”, available on http://www.ifrs.org/Investor-

resources/Investor-perspectives-2/Documents/Prudence_Investor-

Perspective_Conceptual-FW.PDF accessed on 16-08-2017.

Gary S., (2017), “The Importance of Inherent Risk Factors: Auditor’s Perceptions”,

Australian Accounting Review, Vol 3, Pp 38-44.

Weiss D, (2014), “Faithful Representation” available on

http://bschool.huji.ac.il/.upload/Seminars/Faithful%20Representation%20October

%202014.pdf accessed on 16-08-2017..

11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.