HI6026 Audit Case Study: Double Ink Printers Ltd - Risk and Audit

VerifiedAdded on 2023/05/23

|10

|2543

|457

Case Study

AI Summary

This audit assignment focuses on Double Ink Printers Ltd (DIPL), performing analytical procedures to assess risks and plan the audit. It examines inherent risks, such as those related to a new IT system and revenue recognition practices, and identifies fraud risk factors, including inadequate segregation of duties and a questionable investment in Nuclear Publishing Ltd. The analysis emphasizes the importance of thorough audit procedures to detect material misstatements and potential fraud, referencing Australian auditing standards throughout. The study concludes that auditors must exercise due care and increase substantive procedures for transactions showing risk factors to ensure accurate financial reporting. Desklib provides access to similar solved assignments and past papers for students.

Audit assignment

Student name:

Student ID:

Word count:

Professor name:

Date: August 16, 2017 Reference style: Harvard

Audit Assignment

1 | P a g e

Student name:

Student ID:

Word count:

Professor name:

Date: August 16, 2017 Reference style: Harvard

Audit Assignment

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit assignment

Table of Contents

Contents

Table of Contents.............................................................................................................................2

Introduction......................................................................................................................................3

Question 1........................................................................................................................................3

Effect of analytical procedures on audit planning.......................................................................5

Question 2........................................................................................................................................5

Risk assessment procedures.........................................................................................................5

Inherent risk.................................................................................................................................5

Inherent risk factors in DIPL.......................................................................................................6

Question 3........................................................................................................................................6

Risk of fraud.................................................................................................................................6

Fraud risk factors in DIPL and their effect..................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

2 | P a g e

Table of Contents

Contents

Table of Contents.............................................................................................................................2

Introduction......................................................................................................................................3

Question 1........................................................................................................................................3

Effect of analytical procedures on audit planning.......................................................................5

Question 2........................................................................................................................................5

Risk assessment procedures.........................................................................................................5

Inherent risk.................................................................................................................................5

Inherent risk factors in DIPL.......................................................................................................6

Question 3........................................................................................................................................6

Risk of fraud.................................................................................................................................6

Fraud risk factors in DIPL and their effect..................................................................................7

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

2 | P a g e

Audit assignment

Introduction

Purpose

The purpose behind this writeup is to perfom analytical procedures for Double ink printers

limited (DIPL), analysis results from analytical procedures and effects of results from analytical

procedures on audit planning. Moreover, this writeup will also explain regarding inherent risk in

the DIPL. At the end of the write up fraud risk factors of DIPL will also analyze.

Background

DIPL is printing company provides printing on demand i.e. company prints number of prints

require by the clients only not more not less. Previously this company was audited by Jay and

Associates and from the audit of the year ended 2015; new audit firm undertakes the audit of this

firm. The company makes purchases from Australian and Indian sources. The company also

provides electronically searchable books with publisher’s tile i.e. e-books.

Method of investigation

The write up will use Australian auditing standards for providing understanding as well as a

proof for performing analytical procedures, make decisions regarding inherent risk factors and

fraud risk factors.

Scope

Besides the audit procedures analysis for DIPL, this writes up will also present an explanation

about the Australian auditing standard 520 for analytical procedures, Australian auditing

standard 200 for inherent risk and Australian auditing standard 240 for fraud risk.

Question 1

Preliminary analytical procedures are those procedures which performed by the auditor to make

an estimate regarding the nature time and extent of substantive analytical procedures required by

the audit of the specific organization (Anon., 2016). Under preliminary analytical procedures,

auditor requires making an understanding regarding the business of organization for which audit

will perform (BIGGS et al., 1999). Background information of the company demonstrates that

company is in make revenues from two ways one is from printing books, magazines etc and

3 | P a g e

Introduction

Purpose

The purpose behind this writeup is to perfom analytical procedures for Double ink printers

limited (DIPL), analysis results from analytical procedures and effects of results from analytical

procedures on audit planning. Moreover, this writeup will also explain regarding inherent risk in

the DIPL. At the end of the write up fraud risk factors of DIPL will also analyze.

Background

DIPL is printing company provides printing on demand i.e. company prints number of prints

require by the clients only not more not less. Previously this company was audited by Jay and

Associates and from the audit of the year ended 2015; new audit firm undertakes the audit of this

firm. The company makes purchases from Australian and Indian sources. The company also

provides electronically searchable books with publisher’s tile i.e. e-books.

Method of investigation

The write up will use Australian auditing standards for providing understanding as well as a

proof for performing analytical procedures, make decisions regarding inherent risk factors and

fraud risk factors.

Scope

Besides the audit procedures analysis for DIPL, this writes up will also present an explanation

about the Australian auditing standard 520 for analytical procedures, Australian auditing

standard 200 for inherent risk and Australian auditing standard 240 for fraud risk.

Question 1

Preliminary analytical procedures are those procedures which performed by the auditor to make

an estimate regarding the nature time and extent of substantive analytical procedures required by

the audit of the specific organization (Anon., 2016). Under preliminary analytical procedures,

auditor requires making an understanding regarding the business of organization for which audit

will perform (BIGGS et al., 1999). Background information of the company demonstrates that

company is in make revenues from two ways one is from printing books, magazines etc and

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit assignment

another is from e-books. The company is having set order completion cycle i.e. two days from

small order and five days for big orders. But the company did not define small and big order; it

means this can be easily manipulated order processing by manipulating by order as small and

small order as big. One more area which requires taking into consideration is, in 2014 company

acquired a company Nuclear Publishing Limited for earning revenues from medical textbooks,

but as per an article in a medical journal, the company will become unable to generate revenue

from medical textbook data because of the new theory. Hence auditor of the company requires

making extensive procedures during the audit to know whether new theory explained in the

journal article is relevant or not and if the article is relevant the company requires to reduce the

value of its assets due to lower expected revenues from assets related to Nuclear Publishing

Limited book data.

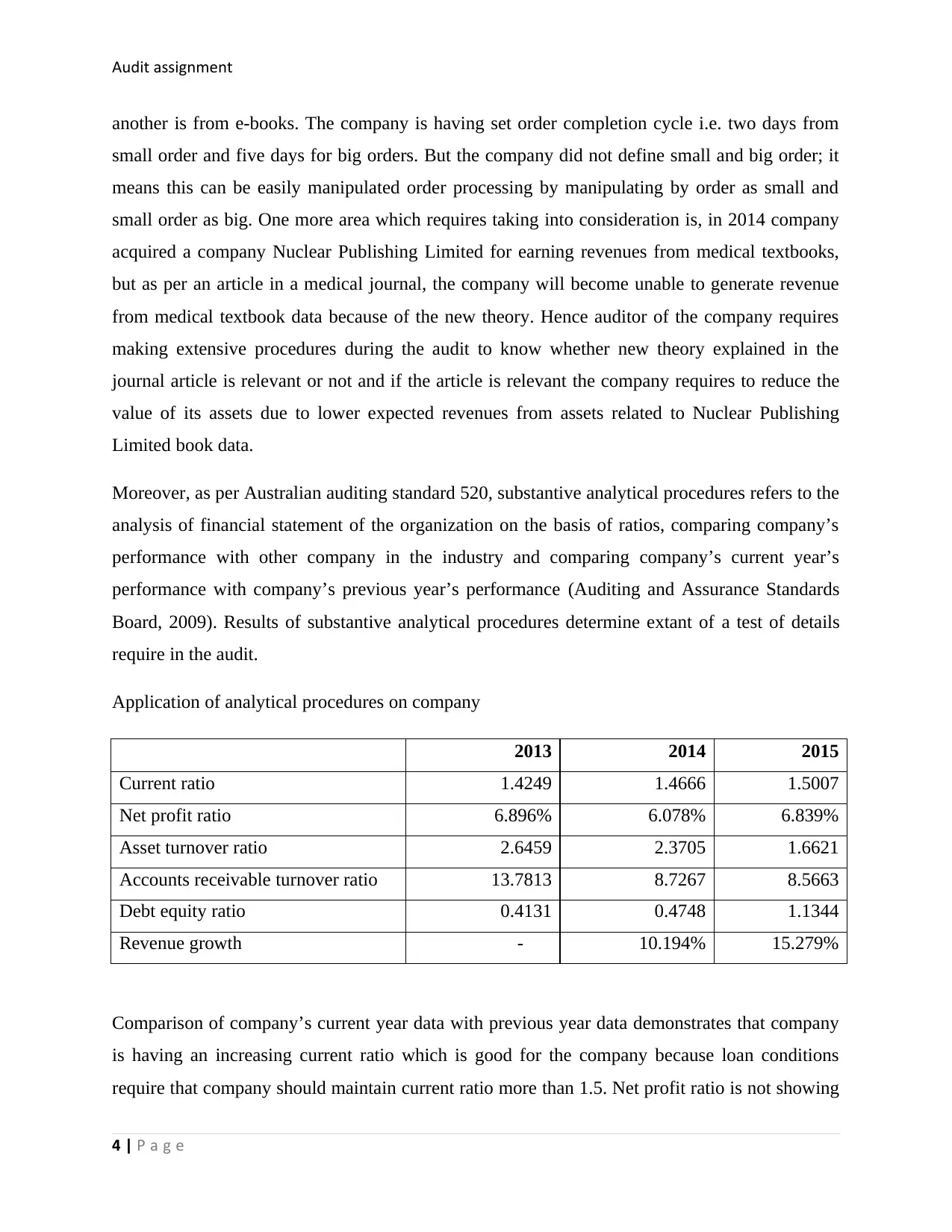

Moreover, as per Australian auditing standard 520, substantive analytical procedures refers to the

analysis of financial statement of the organization on the basis of ratios, comparing company’s

performance with other company in the industry and comparing company’s current year’s

performance with company’s previous year’s performance (Auditing and Assurance Standards

Board, 2009). Results of substantive analytical procedures determine extant of a test of details

require in the audit.

Application of analytical procedures on company

2013 2014 2015

Current ratio 1.4249 1.4666 1.5007

Net profit ratio 6.896% 6.078% 6.839%

Asset turnover ratio 2.6459 2.3705 1.6621

Accounts receivable turnover ratio 13.7813 8.7267 8.5663

Debt equity ratio 0.4131 0.4748 1.1344

Revenue growth - 10.194% 15.279%

Comparison of company’s current year data with previous year data demonstrates that company

is having an increasing current ratio which is good for the company because loan conditions

require that company should maintain current ratio more than 1.5. Net profit ratio is not showing

4 | P a g e

another is from e-books. The company is having set order completion cycle i.e. two days from

small order and five days for big orders. But the company did not define small and big order; it

means this can be easily manipulated order processing by manipulating by order as small and

small order as big. One more area which requires taking into consideration is, in 2014 company

acquired a company Nuclear Publishing Limited for earning revenues from medical textbooks,

but as per an article in a medical journal, the company will become unable to generate revenue

from medical textbook data because of the new theory. Hence auditor of the company requires

making extensive procedures during the audit to know whether new theory explained in the

journal article is relevant or not and if the article is relevant the company requires to reduce the

value of its assets due to lower expected revenues from assets related to Nuclear Publishing

Limited book data.

Moreover, as per Australian auditing standard 520, substantive analytical procedures refers to the

analysis of financial statement of the organization on the basis of ratios, comparing company’s

performance with other company in the industry and comparing company’s current year’s

performance with company’s previous year’s performance (Auditing and Assurance Standards

Board, 2009). Results of substantive analytical procedures determine extant of a test of details

require in the audit.

Application of analytical procedures on company

2013 2014 2015

Current ratio 1.4249 1.4666 1.5007

Net profit ratio 6.896% 6.078% 6.839%

Asset turnover ratio 2.6459 2.3705 1.6621

Accounts receivable turnover ratio 13.7813 8.7267 8.5663

Debt equity ratio 0.4131 0.4748 1.1344

Revenue growth - 10.194% 15.279%

Comparison of company’s current year data with previous year data demonstrates that company

is having an increasing current ratio which is good for the company because loan conditions

require that company should maintain current ratio more than 1.5. Net profit ratio is not showing

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit assignment

as much growth as shown by revenue in the company hence this assertion requires extensive

procedures for ascertaining whether the company is showing accurate revenue and expenditures

or not. As per loan condition, company’s debt equity ratio must be lower than one but in 2015

company’s debt equity ratio is more than which enhance the risk of recalling loan by BDO

finance limited. If the loan will recall by financing company then the company will face non

availability of funds. Hence it is also required extant procedures for this assertion that auditor

could make confirmation regarding the non presence of a risk of liquidation due to non

availability of funds.

Effect of analytical procedures on audit planning

Analytical procedures of the company influence the planning of audit extensively. Main aim to

perform the substantive analytical procedure is to determine areas related to company’s financial

and non financial data which require extensive procedures. The second aim of this analytical

procedure is to plan audit (Glover et al., 2000). Substantive analytical procedures and

preliminary analytical procedures effect the planning decision for an audit of the company in this

way, these procedures concluded that company needs to plan audit procedures extensively for

higher debt equity ratio and its effects, the value of assets acquired from Nuclear Publishing

Limited and relevance of journal article. In addition to this company needs to plan audit

procedure regarding reasons behind variations in revenue and net profit growth.

Question 2

Risk assessment procedures

Risk assessment procedures are the procedures those are performed by auditors for making an

understanding regarding internal controls of the organization and making an understanding

regarding the organization for assessing the risk of material misstatement in the financial

statements and notes to accounts of the organization. Such risk can arise due to fraud or error

(Auditing and Assurance Standards Board, 2011). In performing risk assessment procedures

auditor needs to perform analytical procedures, enquiry, observation, and inspection.

Inherent risk

Inherent risk refers to the risk of material misstatement in any assertion due to nature of that

assertion or transactions related to that assertion. This risk assessment does not need the

5 | P a g e

as much growth as shown by revenue in the company hence this assertion requires extensive

procedures for ascertaining whether the company is showing accurate revenue and expenditures

or not. As per loan condition, company’s debt equity ratio must be lower than one but in 2015

company’s debt equity ratio is more than which enhance the risk of recalling loan by BDO

finance limited. If the loan will recall by financing company then the company will face non

availability of funds. Hence it is also required extant procedures for this assertion that auditor

could make confirmation regarding the non presence of a risk of liquidation due to non

availability of funds.

Effect of analytical procedures on audit planning

Analytical procedures of the company influence the planning of audit extensively. Main aim to

perform the substantive analytical procedure is to determine areas related to company’s financial

and non financial data which require extensive procedures. The second aim of this analytical

procedure is to plan audit (Glover et al., 2000). Substantive analytical procedures and

preliminary analytical procedures effect the planning decision for an audit of the company in this

way, these procedures concluded that company needs to plan audit procedures extensively for

higher debt equity ratio and its effects, the value of assets acquired from Nuclear Publishing

Limited and relevance of journal article. In addition to this company needs to plan audit

procedure regarding reasons behind variations in revenue and net profit growth.

Question 2

Risk assessment procedures

Risk assessment procedures are the procedures those are performed by auditors for making an

understanding regarding internal controls of the organization and making an understanding

regarding the organization for assessing the risk of material misstatement in the financial

statements and notes to accounts of the organization. Such risk can arise due to fraud or error

(Auditing and Assurance Standards Board, 2011). In performing risk assessment procedures

auditor needs to perform analytical procedures, enquiry, observation, and inspection.

Inherent risk

Inherent risk refers to the risk of material misstatement in any assertion due to nature of that

assertion or transactions related to that assertion. This risk assessment does not need the

5 | P a g e

Audit assignment

consideration regarding the controls applied by the organization regarding that assertion or not.

The materiality of misstatement can be on an individual basis or on an aggregate basis (Auditing

and Assurance Standards Board, 2009).

Inherent risk factors in DIPL

Inherent risks present in the DIPL for the year ended 2015 are,

1. The company invests in a new fully computerized IT system for integrating all

accounting process of the company. The company installed new procedure in June

without having appropriate staff for reconciliation. Preliminary testing of such new

system shows that some transactions which were performed in the year end of the current

year were not shown in the accounts of the current year.

This is a risk factor because due to new IT system company made a material

misstatement and made the inappropriate allocation of year end transaction to another

year.

This shows that reason behind the installation of new IT system could be for execution of

fraud and for making misstatement regarding year end transactions and make

manipulations in the financial statements of the company for the year ending 2015. Due

to new system profits and assets of the company may be overestimated.

2. The company charges storage fees from the publishers for keeping the books of

publishers in the e-book services of the company. Company charge such fees in advance

for 12 months but company recognize such fees in the month in which books

downloaded. This may make variations between fees recognized and charged.

This is a risk factor because due to this type of practice company may make a material

misstatement and make the inappropriate allocation of storage fees revenue.

Due to this practice company may manipulate revenue from storage fees and in turn net

profits of the company hence this assertion can impact financial statements materially.

Question 3

Risk of fraud

Fraud means a deliberate misstatement. Fraud is an act which done by fraudster intentionally for

taking unfair or illegal advantages (Singleton et al., 2006). Such fraud can be conduct be

6 | P a g e

consideration regarding the controls applied by the organization regarding that assertion or not.

The materiality of misstatement can be on an individual basis or on an aggregate basis (Auditing

and Assurance Standards Board, 2009).

Inherent risk factors in DIPL

Inherent risks present in the DIPL for the year ended 2015 are,

1. The company invests in a new fully computerized IT system for integrating all

accounting process of the company. The company installed new procedure in June

without having appropriate staff for reconciliation. Preliminary testing of such new

system shows that some transactions which were performed in the year end of the current

year were not shown in the accounts of the current year.

This is a risk factor because due to new IT system company made a material

misstatement and made the inappropriate allocation of year end transaction to another

year.

This shows that reason behind the installation of new IT system could be for execution of

fraud and for making misstatement regarding year end transactions and make

manipulations in the financial statements of the company for the year ending 2015. Due

to new system profits and assets of the company may be overestimated.

2. The company charges storage fees from the publishers for keeping the books of

publishers in the e-book services of the company. Company charge such fees in advance

for 12 months but company recognize such fees in the month in which books

downloaded. This may make variations between fees recognized and charged.

This is a risk factor because due to this type of practice company may make a material

misstatement and make the inappropriate allocation of storage fees revenue.

Due to this practice company may manipulate revenue from storage fees and in turn net

profits of the company hence this assertion can impact financial statements materially.

Question 3

Risk of fraud

Fraud means a deliberate misstatement. Fraud is an act which done by fraudster intentionally for

taking unfair or illegal advantages (Singleton et al., 2006). Such fraud can be conduct be

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit assignment

employees, management, those charged with governance or any other individual of the

organization.

Fraud risk factors refer to the risk factors present which show any pressure like extensive losses

or opportunity of doing fraud like extensive rights to a single person or group of person those can

commit fraud (Zimbelman, 1997).

As per Australian auditing standard 240, for an auditor detection of fraud risk factor is trickier

then misstatement arise from error because in the case of deliberate misstatement fraudster use

some procedures to deceive that fraud (Auditing and Assurance Standards Board, 2013).

Fraud risk factors in DIPL and their effect

In the company DIPL, there are many fraud risk factors which indicate risk of fraud; two major

fraud risk factors are,

1. Whenever company receives inventory at warehouse then accounts payable clerk of

company records the arrival of the inventory, as well as records, accounts payables. This

indicates the fraud risk factor due to excessive rights to the accounts payable clerk.

Accounts payable clerk may make misstatement in inventory value as well as accounts

payable value during the recording of both and can embezzle money of company. This

risk factor effects the audit procedures and the auditor will make extensively procures for

reconciling amount due on behalf of accounts payable and value of inventory. For a

reconciliation of amount of accounts payable auditor may send a confirmation to

accounts payable for confirming their due balance and for reconciling inventory, the

auditor may attend physical count of inventory.

2. In September 2014, the company made an investment in net assets of Nuclear Publishing

Ltd by stating reasons that Nuclear Publishing Ltd is having large data of medical text

books which can be helpful for the company in generating revenues. But as per a journal

article medical universities are going to apply new technology due to which this data

become useless and assets of Nuclear Publishing Ltd become nil value. This transaction

arises fraud risk factor of money transfer of company from the company to another

company whose assets will have no value in near future. This fraud risk factor enhances

a number of the audit procedures applied by the auditors of the company. After

7 | P a g e

employees, management, those charged with governance or any other individual of the

organization.

Fraud risk factors refer to the risk factors present which show any pressure like extensive losses

or opportunity of doing fraud like extensive rights to a single person or group of person those can

commit fraud (Zimbelman, 1997).

As per Australian auditing standard 240, for an auditor detection of fraud risk factor is trickier

then misstatement arise from error because in the case of deliberate misstatement fraudster use

some procedures to deceive that fraud (Auditing and Assurance Standards Board, 2013).

Fraud risk factors in DIPL and their effect

In the company DIPL, there are many fraud risk factors which indicate risk of fraud; two major

fraud risk factors are,

1. Whenever company receives inventory at warehouse then accounts payable clerk of

company records the arrival of the inventory, as well as records, accounts payables. This

indicates the fraud risk factor due to excessive rights to the accounts payable clerk.

Accounts payable clerk may make misstatement in inventory value as well as accounts

payable value during the recording of both and can embezzle money of company. This

risk factor effects the audit procedures and the auditor will make extensively procures for

reconciling amount due on behalf of accounts payable and value of inventory. For a

reconciliation of amount of accounts payable auditor may send a confirmation to

accounts payable for confirming their due balance and for reconciling inventory, the

auditor may attend physical count of inventory.

2. In September 2014, the company made an investment in net assets of Nuclear Publishing

Ltd by stating reasons that Nuclear Publishing Ltd is having large data of medical text

books which can be helpful for the company in generating revenues. But as per a journal

article medical universities are going to apply new technology due to which this data

become useless and assets of Nuclear Publishing Ltd become nil value. This transaction

arises fraud risk factor of money transfer of company from the company to another

company whose assets will have no value in near future. This fraud risk factor enhances

a number of the audit procedures applied by the auditors of the company. After

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit assignment

identification of such fraud risk factor auditor should make some procedure to know

whether this transaction was a deliberate misappropriation of shareholder’s wealth of

company or was an innocent transaction for making the investment and increasing

company’s revenue.

Conclusion

This write up concludes that audit is a procedure which must be done by the auditor with due

care so that auditor must reach to the true material misstatement and fraud. Risk can arise due to

organization’s environment or nature of business such risk is known as inherent risk and this risk

can only be reduced by the company making substantive procedures. DIPL Company made

various transactions during the year some of those transactions or procedures of the company

shows inherent risk those transactions includes a recording of revenue from storage fees and new

IT procedure applied by the company. In addition to this, some transactions showing fraud risk

factors hence those transactions require extensive procedure because fraud conceals by the

person making fraud through means to deceive that fraud. Transactions showing fraud risk

factors are, purchase of net assets of Nuclear Publishing Ltd by company and non-availability of

segregation of duty for recording inventory and accounts payable. The conclusion of this write

up is, for each transaction which shows any type of risk factor during the audit or planning of the

audit, the auditor must increase the number of substantive procedures.

References

8 | P a g e

identification of such fraud risk factor auditor should make some procedure to know

whether this transaction was a deliberate misappropriation of shareholder’s wealth of

company or was an innocent transaction for making the investment and increasing

company’s revenue.

Conclusion

This write up concludes that audit is a procedure which must be done by the auditor with due

care so that auditor must reach to the true material misstatement and fraud. Risk can arise due to

organization’s environment or nature of business such risk is known as inherent risk and this risk

can only be reduced by the company making substantive procedures. DIPL Company made

various transactions during the year some of those transactions or procedures of the company

shows inherent risk those transactions includes a recording of revenue from storage fees and new

IT procedure applied by the company. In addition to this, some transactions showing fraud risk

factors hence those transactions require extensive procedure because fraud conceals by the

person making fraud through means to deceive that fraud. Transactions showing fraud risk

factors are, purchase of net assets of Nuclear Publishing Ltd by company and non-availability of

segregation of duty for recording inventory and accounts payable. The conclusion of this write

up is, for each transaction which shows any type of risk factor during the audit or planning of the

audit, the auditor must increase the number of substantive procedures.

References

8 | P a g e

Audit assignment

Anon., 2016. Analytical procedures. [Online] Available at:

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html [Accessed 16 August 2017].

Auditing and Assurance Standards Board, 2009. ASA 520 Analytical Procedures. [Online]

Available at: file:///C:/Users/DELL/Downloads/F2009L04090ES.pdf [Accessed August 16

2017].

Auditing and Assurance Standards Board, 2009. Auditing Standard ASA 200 Overall Objectives

of the Independent Auditor and the Conduct of an Audit in Accordance with Australian Auditing

Standards. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_200_27-10-09.pdf [Accessed 16 august

2017].

Auditing and Assurance Standards Board, 2011. Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment. [Online] Available at: file:///F:/GS%20Solution%20(60%20paise)/Aug/16/risk

%20assement%20procedure.pdf [Accessed 16 august 2017].

Auditing and Assurance Standards Board, 2013. Auditing Standard ASA 240 The Auditor's

Responsibilities Relating to Fraud in an Audit of a Financial Report. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA_

240.pdf [Accessed 2017 August 16].

BIGGS, S.F., MOCK, T.J. & SIMNETT, R., 1999. Analytical Procedures: Promise, Problems,

and Implications for Practice. Australian Accounting Review, 9(17), pp.42-52. 10.1111/j.1835-

2561.1999.tb00098.x.

Glover, S.M., Jiambalvo, J. & Kennedy, J., 2000. Analytical Procedures and Audit‐Planning

Decisions. AUDITING: A Journal of Practice & Theory, 19(2), pp.27-45.

Singleton, T.W., Singleton, A.J., Bologna, G.J. & Lindquist, R.J., 2006. Fraud Auditing and

Forensic Accounting. 3rd ed. New Jersey: John Wily & Sons, Inc.

9 | P a g e

Anon., 2016. Analytical procedures. [Online] Available at:

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-study-

resources/p7/technical-articles/analytical-procedures.html [Accessed 16 August 2017].

Auditing and Assurance Standards Board, 2009. ASA 520 Analytical Procedures. [Online]

Available at: file:///C:/Users/DELL/Downloads/F2009L04090ES.pdf [Accessed August 16

2017].

Auditing and Assurance Standards Board, 2009. Auditing Standard ASA 200 Overall Objectives

of the Independent Auditor and the Conduct of an Audit in Accordance with Australian Auditing

Standards. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/ASA_200_27-10-09.pdf [Accessed 16 august

2017].

Auditing and Assurance Standards Board, 2011. Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment. [Online] Available at: file:///F:/GS%20Solution%20(60%20paise)/Aug/16/risk

%20assement%20procedure.pdf [Accessed 16 august 2017].

Auditing and Assurance Standards Board, 2013. Auditing Standard ASA 240 The Auditor's

Responsibilities Relating to Fraud in an Audit of a Financial Report. [Online] Available at:

http://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA_

240.pdf [Accessed 2017 August 16].

BIGGS, S.F., MOCK, T.J. & SIMNETT, R., 1999. Analytical Procedures: Promise, Problems,

and Implications for Practice. Australian Accounting Review, 9(17), pp.42-52. 10.1111/j.1835-

2561.1999.tb00098.x.

Glover, S.M., Jiambalvo, J. & Kennedy, J., 2000. Analytical Procedures and Audit‐Planning

Decisions. AUDITING: A Journal of Practice & Theory, 19(2), pp.27-45.

Singleton, T.W., Singleton, A.J., Bologna, G.J. & Lindquist, R.J., 2006. Fraud Auditing and

Forensic Accounting. 3rd ed. New Jersey: John Wily & Sons, Inc.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Audit assignment

Zimbelman, M.F., 1997. The Effects of SAS No. 82 on Auditors' Attention to Fraud Risk Factors

and Audit Planning Decisions. Journal of Accounting Research, 35, pp.75-97. DOI:

10.2307/2491454.

10 | P a g e

Zimbelman, M.F., 1997. The Effects of SAS No. 82 on Auditors' Attention to Fraud Risk Factors

and Audit Planning Decisions. Journal of Accounting Research, 35, pp.75-97. DOI:

10.2307/2491454.

10 | P a g e

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.