Report: Financial Analysis of Double Ink Printers Limited Case Study

VerifiedAdded on 2020/03/04

|10

|2250

|196

Case Study

AI Summary

This case study provides a financial analysis of Double Ink Printers Limited, focusing on the accounting system and internal control procedures from an auditor's perspective. The report begins with an executive summary and introduction, followed by an analysis of analytical procedures performed on the company's financial reports over three years. It identifies inherent risk factors, such as inventory valuation changes and the acquisition of assets, and assesses their potential impact on financial reporting. The study also examines potential fraud risk factors, including employee pressure and financial covenants, and their influence on the financial statements. The report concludes with recommendations, emphasizing the importance of a sound internal control system and the avoidance of manipulative practices, offering a comprehensive overview of the company's financial health and potential vulnerabilities.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

The report has been prepared with the consideration of having the accounting aspect as the

important in the functioning of the company. Without the accounting no business can run

effectively and efficiently. Second major focus that has been thrown through this report is on the

internal control system and procedures of the company. It covers all the accounting policies

including the documentations that have been prepared to keep the finance function and other

related functions of the company operative. The major part of the report is that it has been

designed and presented from the part of the auditor instead of the company. The first major aim

of the report is regarding the plan that the auditor will prepare keeping in consideration the first

step of conducting the preliminary analytical procedures. The next aim of the report is to

ascertain the inherent risk factors that has occur because of the nature and the complexity of the

business. The last aim is to ascertain the possible areas where the chances of having fraud is high

and thus affecting the presentation of the financial statements. Having these aims the report has

been divided into different sections and the headings so that the users can have better

understanding.

2

The report has been prepared with the consideration of having the accounting aspect as the

important in the functioning of the company. Without the accounting no business can run

effectively and efficiently. Second major focus that has been thrown through this report is on the

internal control system and procedures of the company. It covers all the accounting policies

including the documentations that have been prepared to keep the finance function and other

related functions of the company operative. The major part of the report is that it has been

designed and presented from the part of the auditor instead of the company. The first major aim

of the report is regarding the plan that the auditor will prepare keeping in consideration the first

step of conducting the preliminary analytical procedures. The next aim of the report is to

ascertain the inherent risk factors that has occur because of the nature and the complexity of the

business. The last aim is to ascertain the possible areas where the chances of having fraud is high

and thus affecting the presentation of the financial statements. Having these aims the report has

been divided into different sections and the headings so that the users can have better

understanding.

2

Table of Contents

Executive Summary 2

Introduction 4

Analytical Procedures to the Financial Report 5

Risk Factors and its Impact 8

Risk Factors leading to Fraud and its Impact 8

Conclusion and Recommendation 9

References 10

3

Executive Summary 2

Introduction 4

Analytical Procedures to the Financial Report 5

Risk Factors and its Impact 8

Risk Factors leading to Fraud and its Impact 8

Conclusion and Recommendation 9

References 10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Every company shall have the sound accounting system clubbed with the internal control system

so as to have the effective and efficient working of the company. Accounting system plays

crucial in assessing the financial position of the company as on date and the financial

performance of the company which the company has gained over the period. Both the financial

position and the financial performance are judged by the financial statements of the company.

These financial statements are prepared by the accounting system. On these financial statements

the auditors of the company gives their opinion and they give their opinion after having the true

and fair audit of the books of accounts of the company. These financial statements give the

company an image in the market and in case it is not prepared in accordance with the relevant

accounting standards then the reputation of the company gets deteriorated not only in the market

but also in the eyes of the different stakeholders. Having the need of the proper financial

statements, the report has been prepared with defined aims and mainly from the auditors view.

The auditors view has been chosen so as to provide the insights of the financial information of

the company that the company has presented to their stakeholders. For the purpose of this report

the background information and the financial information of the company – Double Ink Printers

Limited has been made available.

The report has been started with the Executive summary detailing the major aims of the report

and the outline view of the report. Thereafter the brief introduction has been given detailing the

flow of the report as to how different topics of the report have been dealt. At first the analytical

procedures that is performed by the auditor in the financial report level has been discussed and

that too for the last three consecutive years and thereafter the results of the analytical procedures

are analysed as to how the audit plan of the auditor will differ from the normal plan of audit. At

the second level, the risk assessment has been conducted and the inherent risk factors that are

prevailing has been identified and detailed as to how it can affect the risk of material

misstatement in the financial reporting level. At the last in the main body of the report, the

factors has been considered which can lead to fraud at the financial reporting level and how it

will affect the audit has been detailed. In the last the report has been concluded with the due

recommendation.

4

Every company shall have the sound accounting system clubbed with the internal control system

so as to have the effective and efficient working of the company. Accounting system plays

crucial in assessing the financial position of the company as on date and the financial

performance of the company which the company has gained over the period. Both the financial

position and the financial performance are judged by the financial statements of the company.

These financial statements are prepared by the accounting system. On these financial statements

the auditors of the company gives their opinion and they give their opinion after having the true

and fair audit of the books of accounts of the company. These financial statements give the

company an image in the market and in case it is not prepared in accordance with the relevant

accounting standards then the reputation of the company gets deteriorated not only in the market

but also in the eyes of the different stakeholders. Having the need of the proper financial

statements, the report has been prepared with defined aims and mainly from the auditors view.

The auditors view has been chosen so as to provide the insights of the financial information of

the company that the company has presented to their stakeholders. For the purpose of this report

the background information and the financial information of the company – Double Ink Printers

Limited has been made available.

The report has been started with the Executive summary detailing the major aims of the report

and the outline view of the report. Thereafter the brief introduction has been given detailing the

flow of the report as to how different topics of the report have been dealt. At first the analytical

procedures that is performed by the auditor in the financial report level has been discussed and

that too for the last three consecutive years and thereafter the results of the analytical procedures

are analysed as to how the audit plan of the auditor will differ from the normal plan of audit. At

the second level, the risk assessment has been conducted and the inherent risk factors that are

prevailing has been identified and detailed as to how it can affect the risk of material

misstatement in the financial reporting level. At the last in the main body of the report, the

factors has been considered which can lead to fraud at the financial reporting level and how it

will affect the audit has been detailed. In the last the report has been concluded with the due

recommendation.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ANALYTICAL PROCEDURES TO THE FINANCIAL REPORT

For the report, the company - Double Ink Printers Limited has been made available. The

company is in the business of books printing, magazines printing and other articles which is

required to be printed and bind. The company prints the books or magazines as and when the

demand and order comes. The company follows the due procedures for the documentation and

the accounting of the revenue or other incomes during the year.

Analytical procedures are the first stage of the audit planning which every auditor performs

before starting up of the audit. It applies to all the companies whether small, medium or large

and the analytical procedures provides the insights to the auditors as to which areas more focus

of the auditors is required and to which areas less focus is required. The analytical procedures are

conducted for both the financial as well as non financial information (Anastasia, 2015). In the

given case of Double Ink Printers Limited the analytical procedures have been performed

basically for the financial information. The International Standard on Auditing has provided as to

how the analytical procedures are performed and has been provided through the standard number

315. It defines that the analytical procedures are required to be conducted throughout the process

of the audit till the time it does not gets completed and in the given case the preliminary

analytical procedures has been performed which is defined as the identification of the

relationship between different items like revenue, net profit, gross profit, debt and equity, current

assets and current liabilities, etc. Through the preliminary analytical procedures the auditor will

be able to find whether there is any risk which can have the material effect in the financial

statements leading to material misstatements (ACCA, 2016). The 315 standard has defined three

different processes of analytical procedures which includes preliminary, substantive and lastly

the final. As per the given relevant financial information of the company for the last three

co0nsecutive years ending 2013, 2014 and 2015, the analytical procedures have been performed

and the same have been detailed below in the table.

5

For the report, the company - Double Ink Printers Limited has been made available. The

company is in the business of books printing, magazines printing and other articles which is

required to be printed and bind. The company prints the books or magazines as and when the

demand and order comes. The company follows the due procedures for the documentation and

the accounting of the revenue or other incomes during the year.

Analytical procedures are the first stage of the audit planning which every auditor performs

before starting up of the audit. It applies to all the companies whether small, medium or large

and the analytical procedures provides the insights to the auditors as to which areas more focus

of the auditors is required and to which areas less focus is required. The analytical procedures are

conducted for both the financial as well as non financial information (Anastasia, 2015). In the

given case of Double Ink Printers Limited the analytical procedures have been performed

basically for the financial information. The International Standard on Auditing has provided as to

how the analytical procedures are performed and has been provided through the standard number

315. It defines that the analytical procedures are required to be conducted throughout the process

of the audit till the time it does not gets completed and in the given case the preliminary

analytical procedures has been performed which is defined as the identification of the

relationship between different items like revenue, net profit, gross profit, debt and equity, current

assets and current liabilities, etc. Through the preliminary analytical procedures the auditor will

be able to find whether there is any risk which can have the material effect in the financial

statements leading to material misstatements (ACCA, 2016). The 315 standard has defined three

different processes of analytical procedures which includes preliminary, substantive and lastly

the final. As per the given relevant financial information of the company for the last three

co0nsecutive years ending 2013, 2014 and 2015, the analytical procedures have been performed

and the same have been detailed below in the table.

5

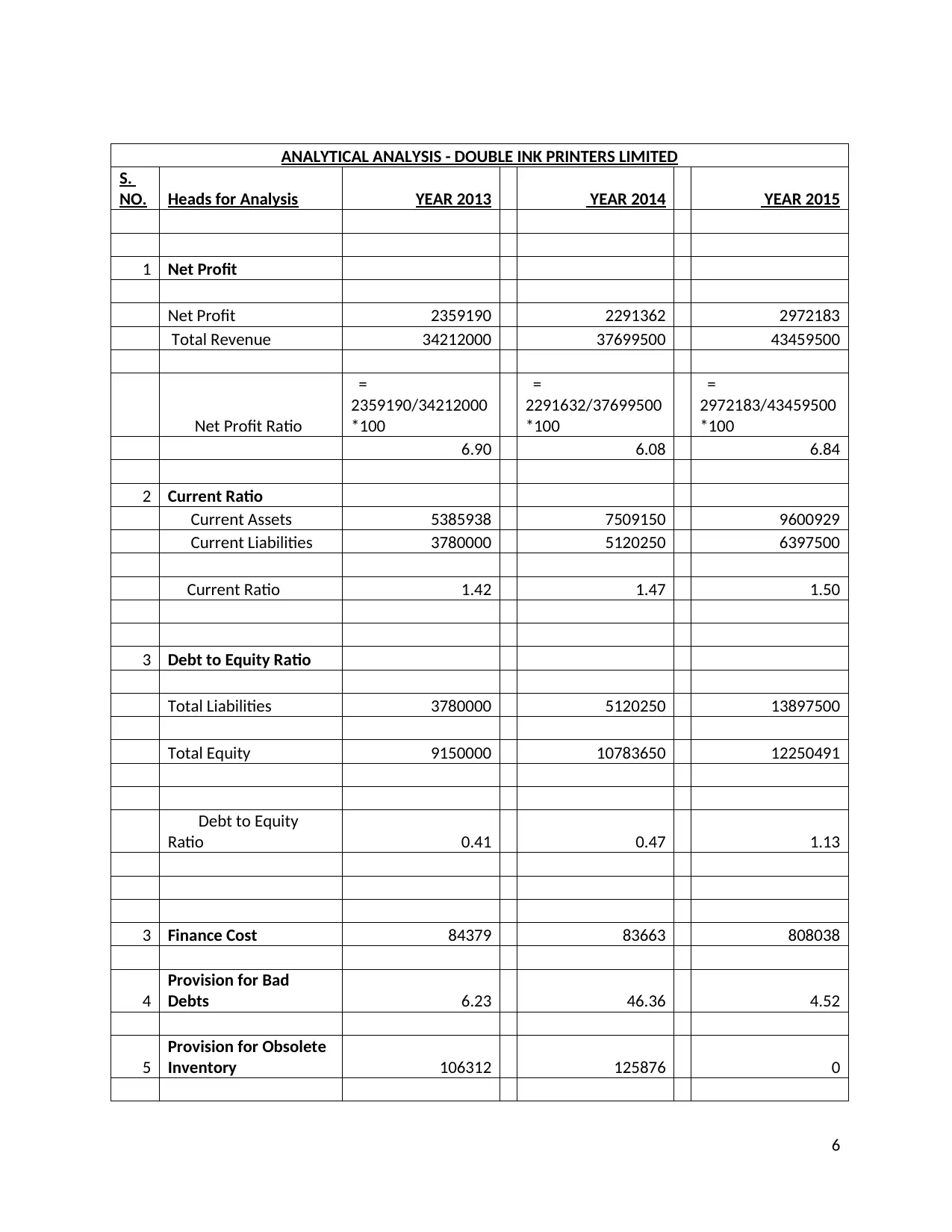

ANALYTICAL ANALYSIS - DOUBLE INK PRINTERS LIMITED

S.

NO. Heads for Analysis YEAR 2013 YEAR 2014 YEAR 2015

1 Net Profit

Net Profit 2359190 2291362 2972183

Total Revenue 34212000 37699500 43459500

Net Profit Ratio

=

2359190/34212000

*100

=

2291632/37699500

*100

=

2972183/43459500

*100

6.90 6.08 6.84

2 Current Ratio

Current Assets 5385938 7509150 9600929

Current Liabilities 3780000 5120250 6397500

Current Ratio 1.42 1.47 1.50

3 Debt to Equity Ratio

Total Liabilities 3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to Equity

Ratio 0.41 0.47 1.13

3 Finance Cost 84379 83663 808038

4

Provision for Bad

Debts 6.23 46.36 4.52

5

Provision for Obsolete

Inventory 106312 125876 0

6

S.

NO. Heads for Analysis YEAR 2013 YEAR 2014 YEAR 2015

1 Net Profit

Net Profit 2359190 2291362 2972183

Total Revenue 34212000 37699500 43459500

Net Profit Ratio

=

2359190/34212000

*100

=

2291632/37699500

*100

=

2972183/43459500

*100

6.90 6.08 6.84

2 Current Ratio

Current Assets 5385938 7509150 9600929

Current Liabilities 3780000 5120250 6397500

Current Ratio 1.42 1.47 1.50

3 Debt to Equity Ratio

Total Liabilities 3780000 5120250 13897500

Total Equity 9150000 10783650 12250491

Debt to Equity

Ratio 0.41 0.47 1.13

3 Finance Cost 84379 83663 808038

4

Provision for Bad

Debts 6.23 46.36 4.52

5

Provision for Obsolete

Inventory 106312 125876 0

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

Loss in Foreign

Currency 38500 49750 0

7 Loan 0 0 7500000

The above analysis depicts that if the analytical procedures has not been carried out then the

auditor would have been facing much difficulty and thereby giving the wrong picture of state of

affairs of the company and also the financial performance of the company. In order to have

further deep analysis of the analysis, following has been detailed one by one (Capital Markets

Advisory Committee Meeting, 2013).

The net profit of the company has been at the rate of 6.90 in the year 2013, 6.08 in the

year 2014 and again 6.84 in the year of 2015. It depicts that the company has the

fluctuating revenue on year on year basis or the company in order to maintain the revenue

figure due to the pressure of the stakeholders.

Current ratio has been sudden increased from 1.47 to 1.50. As per the background

information the company is required to keep the current ratio to the minimum to 1.50 so

as to enjoy the financing facility obtained from the BDO finance limited. Therefore, in

this case, there may be the chances that the company might have increased the debtors or

reduced the creditors so as to maintain the current ratio or also have modified the

inventory valuation.

Interest has been gradually increased from the year 2013 to the year 2015. Despite of

increasing the interest the company has been able to earn the same net profit after tax

which the company has been earning before obtaining the loan facility from the BDO

Finance.

The company has it made provision for doubtful debts with the very less amount detailing

that the company has overvalued its debtors so as to have the better current ratio. Also the

company has written back the provision for doubtful debts which again shows that the

company has manipulated its debtors.

The company has not made the provision for obsolete inventory which again shows that

the company has manipulated with the inventory so as to have the better current ratio of

1.50 as stipulated by the BDO Finance Limited.

For foreign exchange loss the auditor is required to check the transactions and the related

liability according to the relevant accounting standard (Cooper, 2015).

7

Loss in Foreign

Currency 38500 49750 0

7 Loan 0 0 7500000

The above analysis depicts that if the analytical procedures has not been carried out then the

auditor would have been facing much difficulty and thereby giving the wrong picture of state of

affairs of the company and also the financial performance of the company. In order to have

further deep analysis of the analysis, following has been detailed one by one (Capital Markets

Advisory Committee Meeting, 2013).

The net profit of the company has been at the rate of 6.90 in the year 2013, 6.08 in the

year 2014 and again 6.84 in the year of 2015. It depicts that the company has the

fluctuating revenue on year on year basis or the company in order to maintain the revenue

figure due to the pressure of the stakeholders.

Current ratio has been sudden increased from 1.47 to 1.50. As per the background

information the company is required to keep the current ratio to the minimum to 1.50 so

as to enjoy the financing facility obtained from the BDO finance limited. Therefore, in

this case, there may be the chances that the company might have increased the debtors or

reduced the creditors so as to maintain the current ratio or also have modified the

inventory valuation.

Interest has been gradually increased from the year 2013 to the year 2015. Despite of

increasing the interest the company has been able to earn the same net profit after tax

which the company has been earning before obtaining the loan facility from the BDO

Finance.

The company has it made provision for doubtful debts with the very less amount detailing

that the company has overvalued its debtors so as to have the better current ratio. Also the

company has written back the provision for doubtful debts which again shows that the

company has manipulated its debtors.

The company has not made the provision for obsolete inventory which again shows that

the company has manipulated with the inventory so as to have the better current ratio of

1.50 as stipulated by the BDO Finance Limited.

For foreign exchange loss the auditor is required to check the transactions and the related

liability according to the relevant accounting standard (Cooper, 2015).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above analysis depicts that the planning decision of the auditor will automatically gets

affected and is required to consider the same while planning for the audit.

RISK FACTORS AND ITS IMPACT

Following are the two inherent risk factors that have been identified during the risk assessment

process:

First inherent risk is of the valuation of the inventory. The company has been valuing the

inventory at the Average cost basis. As per the board meeting, the company decides to

change the inventory valuation on the basis of the First in First Out method. Due to this,

the value of inventory which has been coming with lower amount earlier will now come

with higher amount and thus, it is the inherent risk factors and may affect the risk of

material misstatements at the financial reporting level (Gary, 2017).

Second inherent risk is of the acquisition of the Nuclear Publishing Limited along with

the patent and the copyright of medical books. As per the news article the same will

become redundant after sometime due to the introduction of new theory. Thus, it may

adversely affect the financial statements as the assets of the company will get deteriorated

suddenly.

RISK FACTORS LEADING FRAUD AND ITS IMPACT

Following are the two fraud risk factors which have been identified using the background

information and the financial information (Weiss, 2014).

With the introduction of the new software, the employees of the company are under the

great pressure to get the new software implemented and made available to the company.

Due to this pressure there are high chances of having the mistakes and frauds being

committed at the end of the employees only.

Second major risk factor that will lead to the fraud is the covenant made by the BDO

Finance Limited. The company has obtained 75 millions from the BDO Finance limited

with the stipulation that the company is required to maintain the current ratio of 1.50 and

in case it falls below than that then the facility given to the company will be withdrawn

from the immediate effect and thus the company will be at the liberty to commit the fraud

8

affected and is required to consider the same while planning for the audit.

RISK FACTORS AND ITS IMPACT

Following are the two inherent risk factors that have been identified during the risk assessment

process:

First inherent risk is of the valuation of the inventory. The company has been valuing the

inventory at the Average cost basis. As per the board meeting, the company decides to

change the inventory valuation on the basis of the First in First Out method. Due to this,

the value of inventory which has been coming with lower amount earlier will now come

with higher amount and thus, it is the inherent risk factors and may affect the risk of

material misstatements at the financial reporting level (Gary, 2017).

Second inherent risk is of the acquisition of the Nuclear Publishing Limited along with

the patent and the copyright of medical books. As per the news article the same will

become redundant after sometime due to the introduction of new theory. Thus, it may

adversely affect the financial statements as the assets of the company will get deteriorated

suddenly.

RISK FACTORS LEADING FRAUD AND ITS IMPACT

Following are the two fraud risk factors which have been identified using the background

information and the financial information (Weiss, 2014).

With the introduction of the new software, the employees of the company are under the

great pressure to get the new software implemented and made available to the company.

Due to this pressure there are high chances of having the mistakes and frauds being

committed at the end of the employees only.

Second major risk factor that will lead to the fraud is the covenant made by the BDO

Finance Limited. The company has obtained 75 millions from the BDO Finance limited

with the stipulation that the company is required to maintain the current ratio of 1.50 and

in case it falls below than that then the facility given to the company will be withdrawn

from the immediate effect and thus the company will be at the liberty to commit the fraud

8

and manipulate the financial statements so as to avail the facility from the BDO Finance

Limited at the best possible extent.

CONCLUSION AND RECOMMENDATION

The company has been in the business of printing since its inception and has been growing since

its incorporation. The financial information and the background information has been analysed

by the auditors by performing the analytical procedures and with the identification of the

inherent risk factors and the fraud risk factors and the same have been detailed. In order to end

the report the company has the sound internal control system subject to the audit observations

that has been noted separately at each stage.

It is recommended for the company to avoid such manipulative and fraud practices.

REFERENCES

9

Limited at the best possible extent.

CONCLUSION AND RECOMMENDATION

The company has been in the business of printing since its inception and has been growing since

its incorporation. The financial information and the background information has been analysed

by the auditors by performing the analytical procedures and with the identification of the

inherent risk factors and the fraud risk factors and the same have been detailed. In order to end

the report the company has the sound internal control system subject to the audit observations

that has been noted separately at each stage.

It is recommended for the company to avoid such manipulative and fraud practices.

REFERENCES

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ACCA, (2016), “Analytical Procedures”, available on

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-

study-resources/p7/technical-articles/analytical-procedures.html accessed on 15-08-

2017.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 16-

08-2017.

Capital Markets Advisory Committee Meeting, (2013), “Conceptual Framework”

available on

http://www.ifrs.org/Meetings/MeetingDocs/Other%20Meeting/2013/March/AP

%203%20conceptual%20framework.pdf accessed on 16-08-2017.

Cooper S, (2015), “A Tale of Prudence”, available on http://www.ifrs.org/Investor-

resources/Investor-perspectives-2/Documents/Prudence_Investor-

Perspective_Conceptual-FW.PDF accessed on 16-08-2017.

Gary S., (2017), “The Importance of Inherent Risk Factors: Auditor’s Perceptions”,

Australian Accounting Review, Vol 3, Pp 38-44.

Weiss D, (2014), “Faithful Representation” available on

http://bschool.huji.ac.il/.upload/Seminars/Faithful%20Representation%20October

%202014.pdf accessed on 16-08-2017..

10

http://www.accaglobal.com/vn/en/student/exam-support-resources/professional-exams-

study-resources/p7/technical-articles/analytical-procedures.html accessed on 15-08-

2017.

Anastasia, (2015), “Financial Statement Analysis : An Introduction” available on

https://www.cleverism.com/financial-statement-analysis-introduction/ accessed on 16-

08-2017.

Capital Markets Advisory Committee Meeting, (2013), “Conceptual Framework”

available on

http://www.ifrs.org/Meetings/MeetingDocs/Other%20Meeting/2013/March/AP

%203%20conceptual%20framework.pdf accessed on 16-08-2017.

Cooper S, (2015), “A Tale of Prudence”, available on http://www.ifrs.org/Investor-

resources/Investor-perspectives-2/Documents/Prudence_Investor-

Perspective_Conceptual-FW.PDF accessed on 16-08-2017.

Gary S., (2017), “The Importance of Inherent Risk Factors: Auditor’s Perceptions”,

Australian Accounting Review, Vol 3, Pp 38-44.

Weiss D, (2014), “Faithful Representation” available on

http://bschool.huji.ac.il/.upload/Seminars/Faithful%20Representation%20October

%202014.pdf accessed on 16-08-2017..

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.