MBA Assignment 1: Cost Allocation, Profitability, and Investment

VerifiedAdded on 2023/04/22

|20

|3569

|342

Homework Assignment

AI Summary

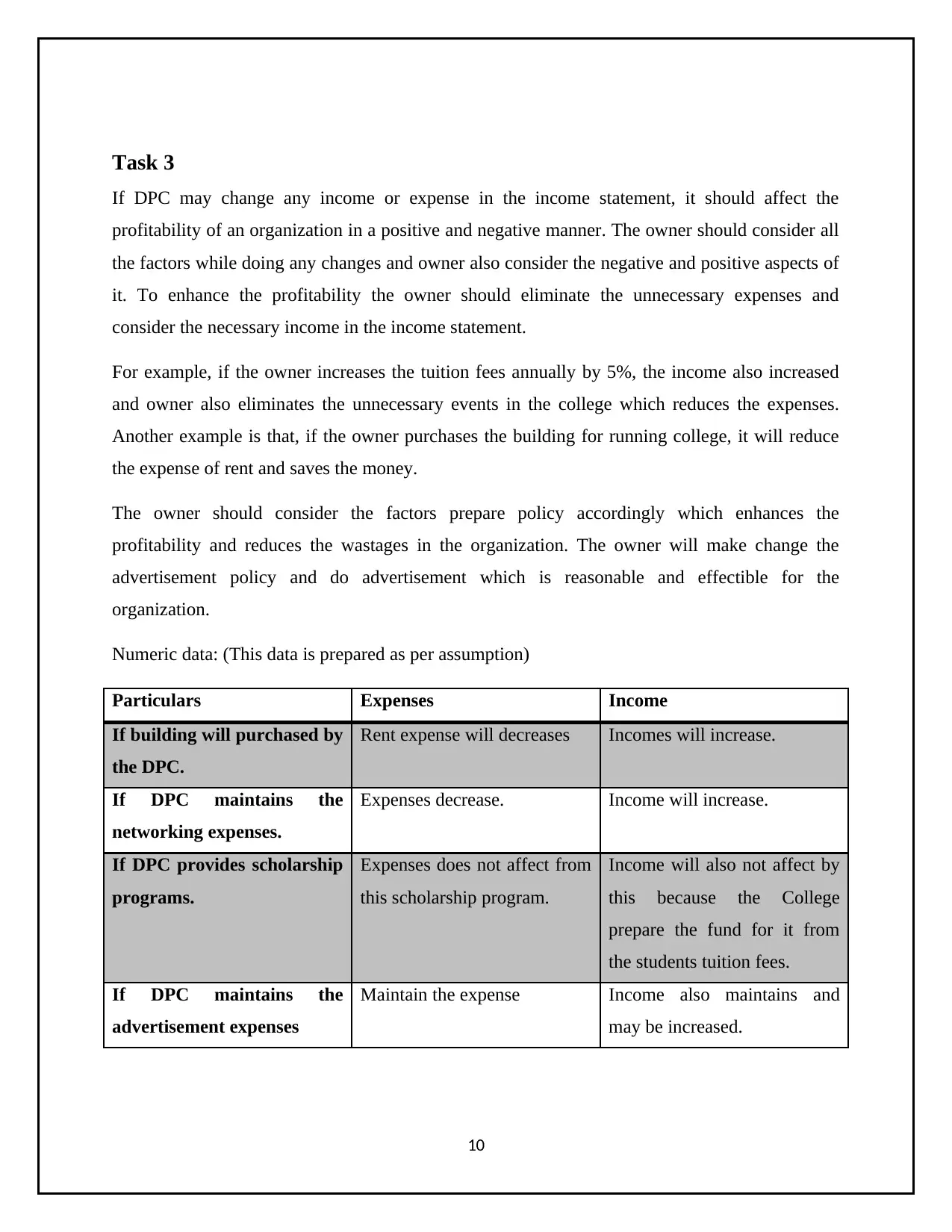

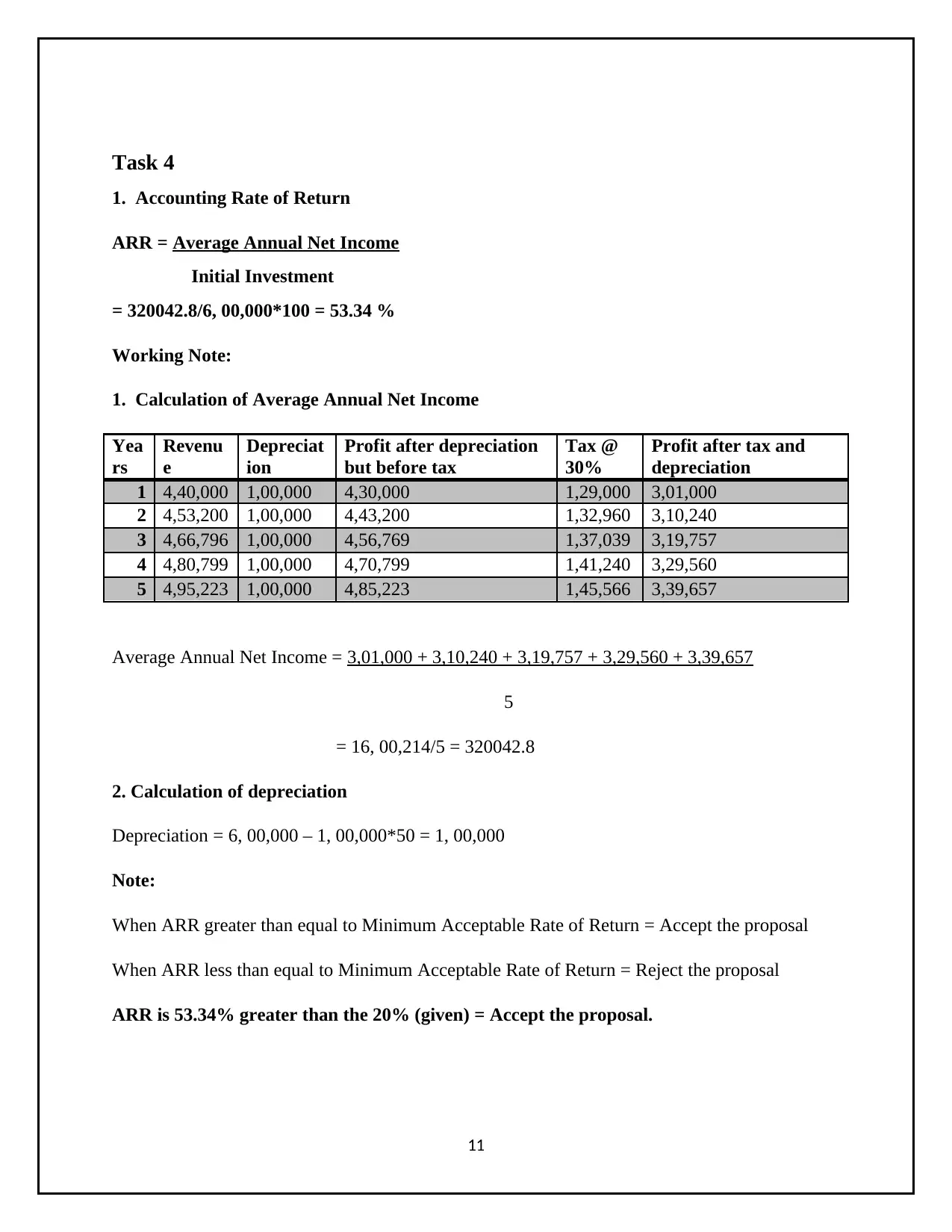

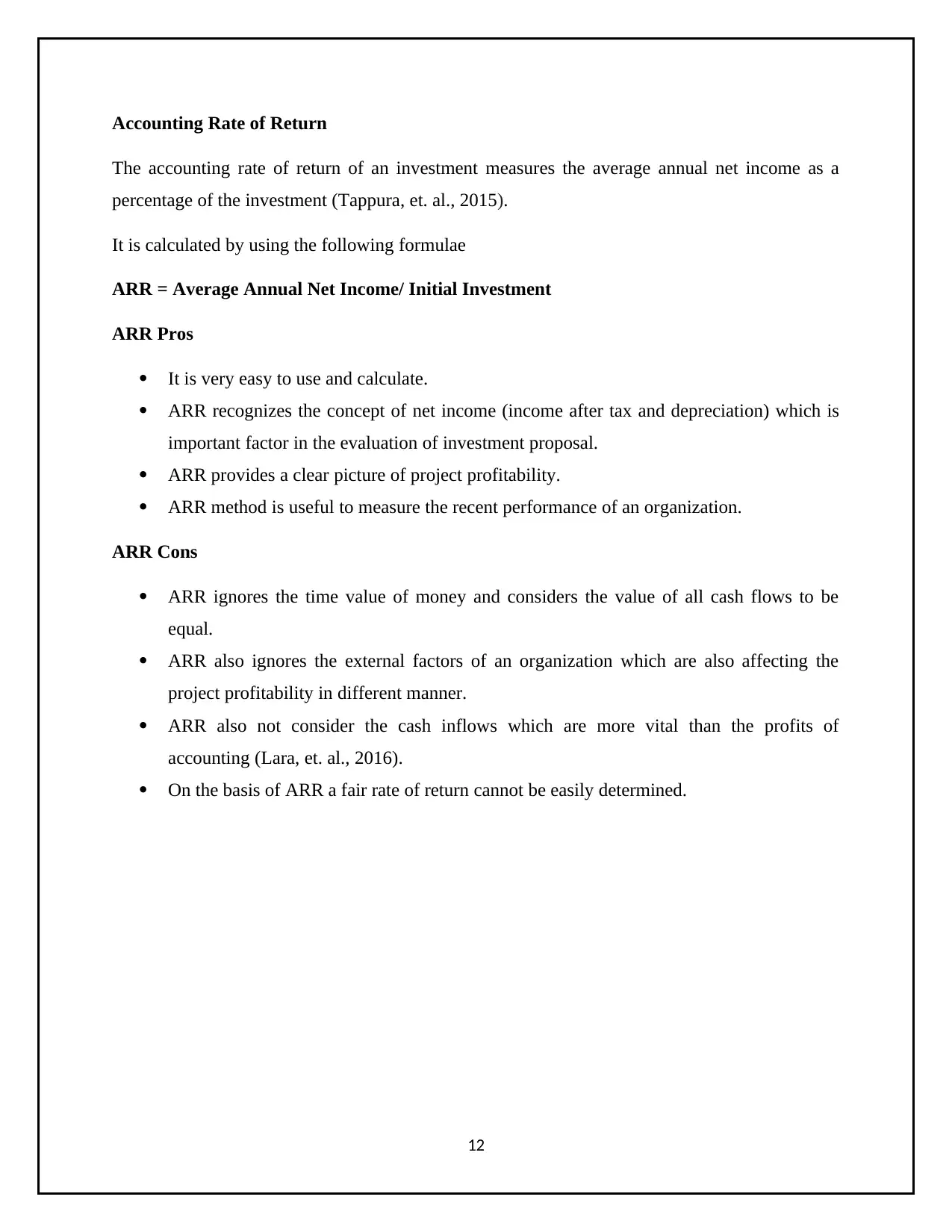

This MBA assignment analyzes the financial aspects of DPC College, a start-up institution offering Bachelor's and Master's programs. The assignment begins by comparing traditional and activity-based costing methods, highlighting their impact on program profitability and the allocation of indirect costs. It then delves into decision-making, recommending the most suitable costing method and outlining its pros and cons. Further, the assignment addresses potential changes to the income statement, considering their positive and negative impacts on profitability. Finally, it evaluates investment proposals using the accounting rate of return, payback period, and weighted average cost of capital, providing a comprehensive financial analysis of the college's operations and investment strategies.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.