Dubai Islamic Bank: Budget Analysis and Financial Options Report

VerifiedAdded on 2023/01/11

|9

|1441

|34

Report

AI Summary

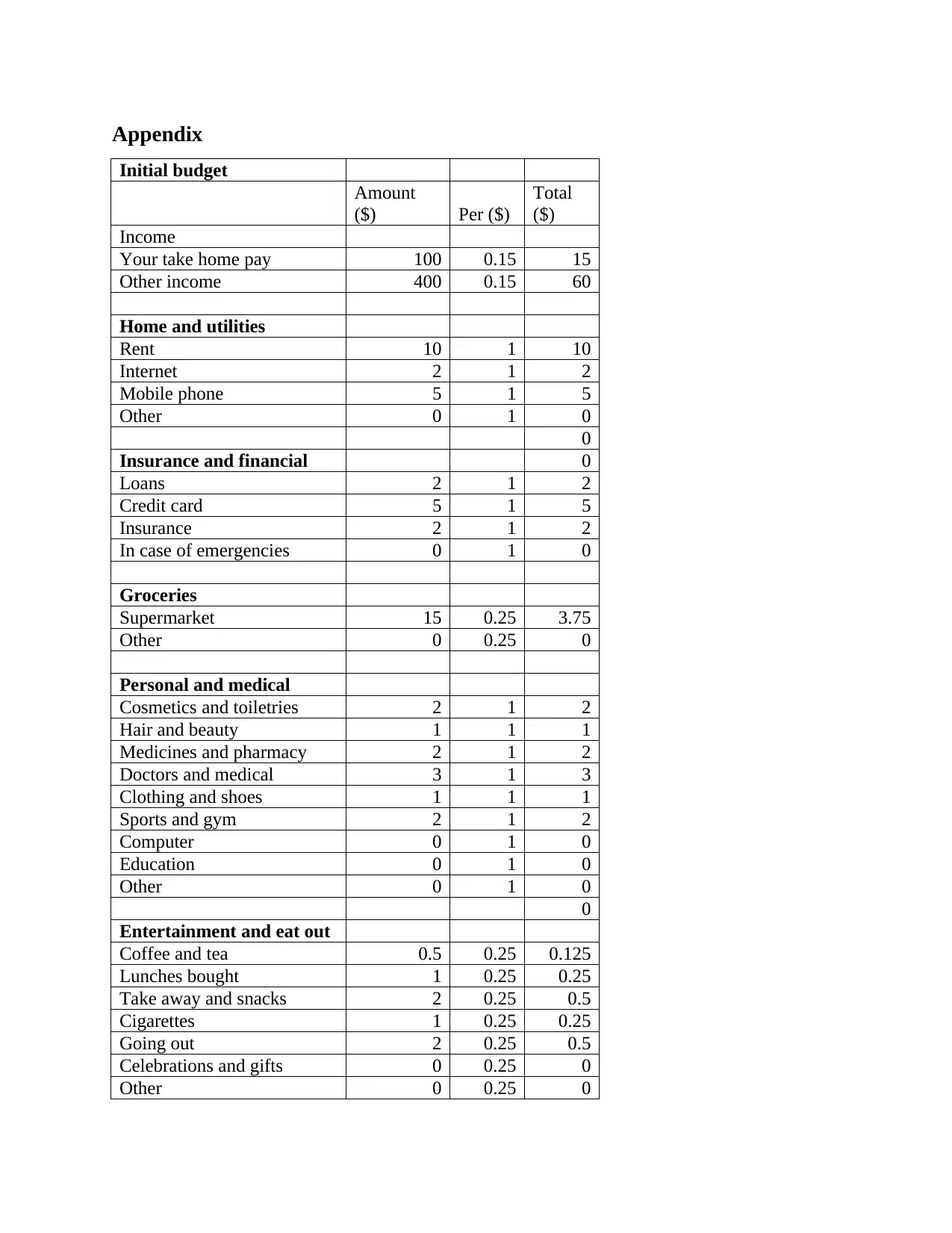

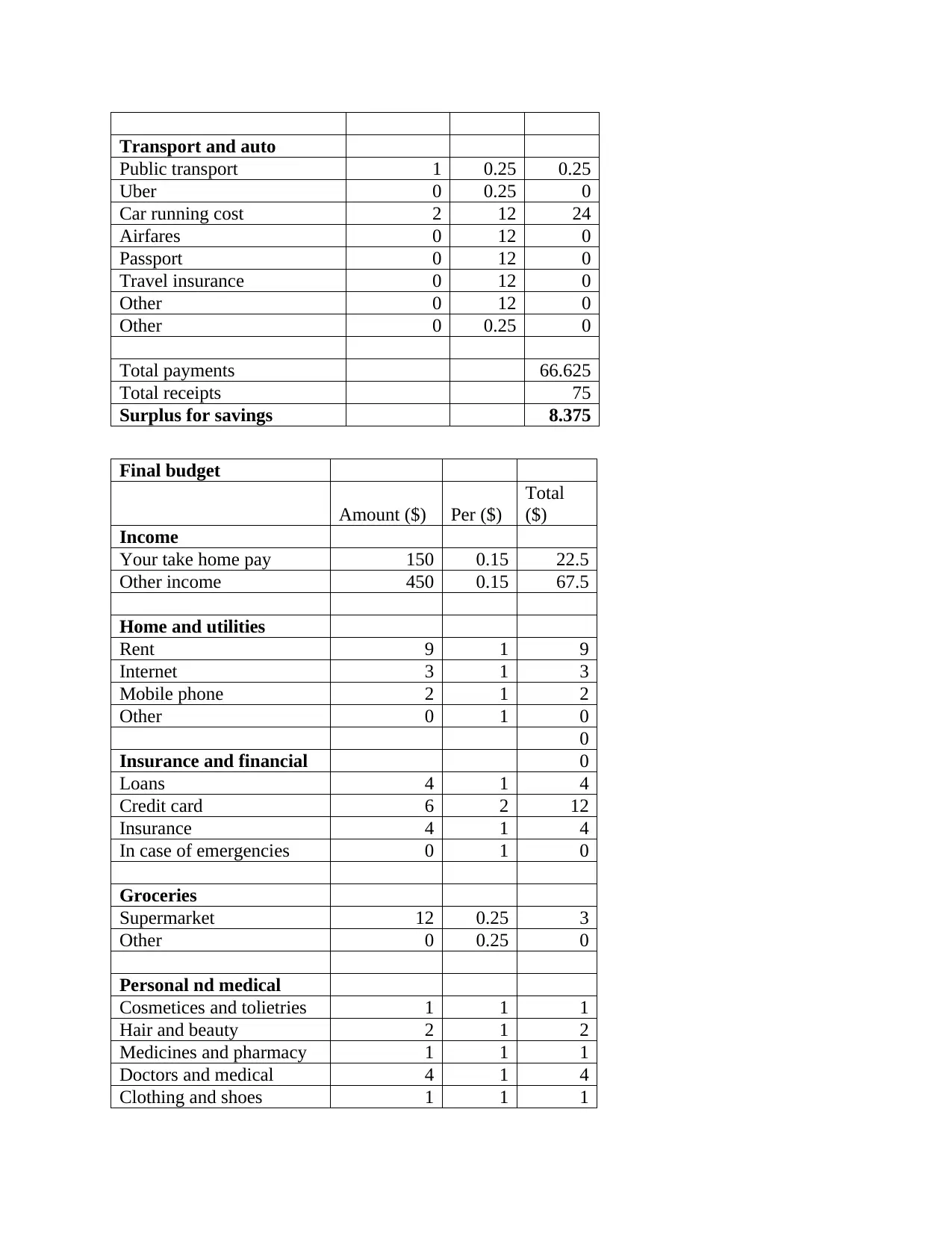

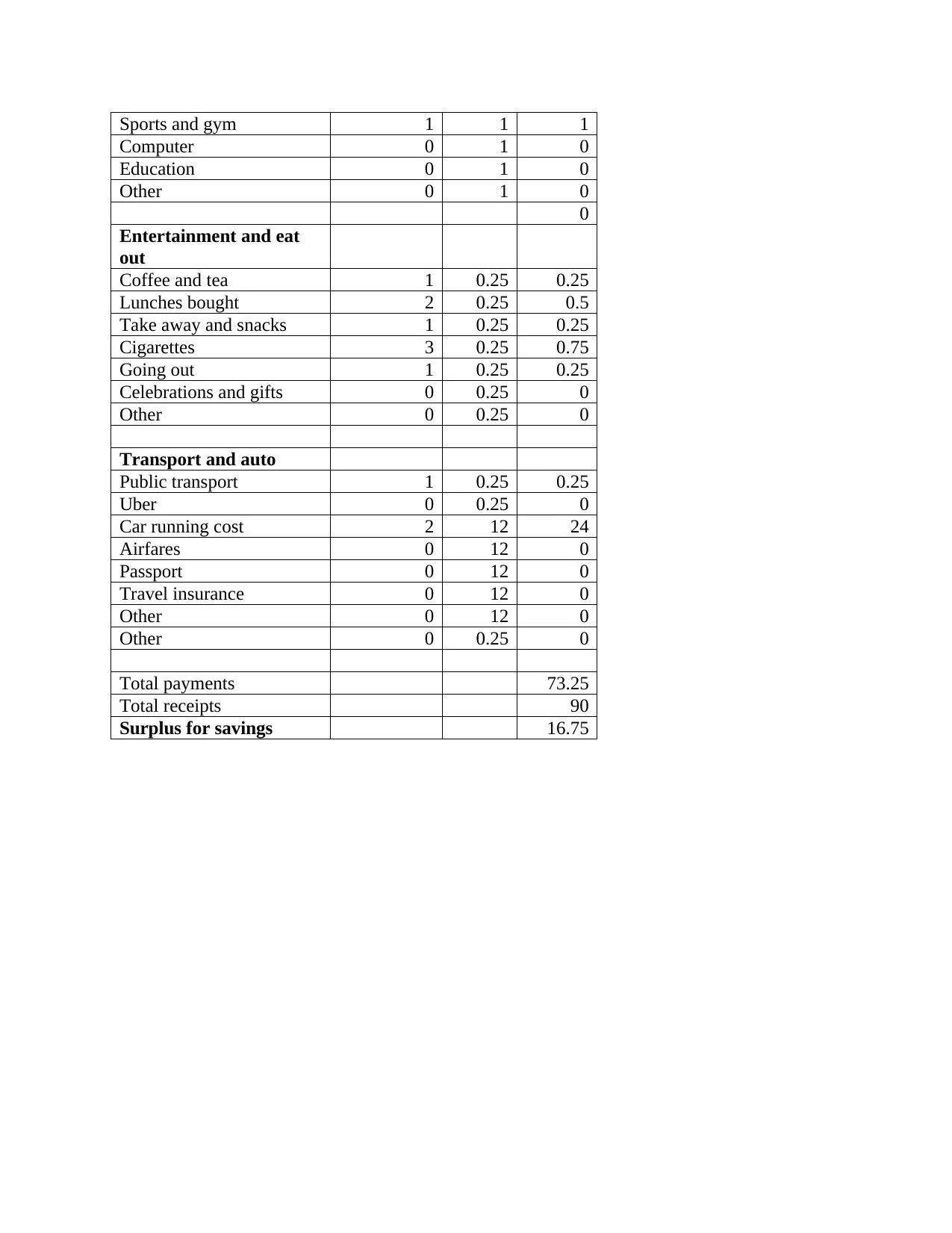

This report analyzes the budget planning, credit cards, and personal loan options. The report begins with an introduction to budgeting, followed by a discussion of two options: credit cards and personal loans offered by Dubai Islamic Bank. The analysis includes the pros and cons of each option, such as the convenience and rewards of credit cards versus the potentially lower interest rates of personal loans. The report then presents an initial and a final budget, demonstrating the allocation of funds and expense management. The conclusion emphasizes the effectiveness of budgeting in managing income and expenses and recommends the use of credit cards and personal loans when managed carefully. The report also includes references and an appendix with detailed budget breakdowns.

1 out of 9

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.