Memorandum on Auditing Risks for Dudley Health Limited (DHL)

VerifiedAdded on 2022/10/19

|10

|2737

|200

Report

AI Summary

This memorandum, prepared by an audit manager at Samway Baker Fitzgerald (SBF), advises an audit senior on the audit risks associated with Dudley Health Limited (DHL). The memo addresses fraud at Pellegrino Shores, focusing on database access and completeness/accuracy assertions. It examines the new patient revenue system at St Neville’s, identifying detection and control risks. The report also covers Acuity Vison’s sales practices and associated account balances, emphasizing the importance of environment control and customer payment testing. Furthermore, the memo discusses account payable testing and the payroll system of Pellegrino Shores, including key assertions and internal control recommendations. The analysis provides a comprehensive overview of potential auditing issues and suggests strategies to mitigate risks and protect stakeholder interests.

Running head: AUDITING AND ASSURANCE

AUDITING AND ASSURANCE

Name of the Student:

Name of the University:

Author Note

AUDITING AND ASSURANCE

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1AUDITING AND ASSURANCE

MEMO

Date: 18th September, 2019

To: Jek Porkins

Audit Senior,

Dudley Health Limited (DHL)

From: Mr XYZ

Audit Manager

Samway Baker Fitzgerald (SBF)

Subject: Letter of Advice regarding the various auditing risks

This memorandum is prepared to advise you about the relevant audit risk associated with the

different units of DHL. This is prepared to advise you as well as provide you the brief insight

of the auditing related issues, risks and other concerns of the different units of DHL. This

memo mainly have the five sections while each section discuss about the separate audit

related issues of the DHL. The first section of the memo discuss about the Pellegrino Shoes

including the key business risks and those accounts which is utmost probable to be

pretentious by scam at Pellegrino Shoes. Second section deals with the transition of new

patient revenue system by St Neville’s including audit risks, key question to inquire internal

audit as well as justification for adopting the audit for the revenue of the firm. Next part of

memo covers sale of medical supplies of Acuity Vison including key account balance and

associated assertions at risk, consequences for governor environment as well as efficiency of

customer payments testing. Fourth section will discuss about undertaken account payable

MEMO

Date: 18th September, 2019

To: Jek Porkins

Audit Senior,

Dudley Health Limited (DHL)

From: Mr XYZ

Audit Manager

Samway Baker Fitzgerald (SBF)

Subject: Letter of Advice regarding the various auditing risks

This memorandum is prepared to advise you about the relevant audit risk associated with the

different units of DHL. This is prepared to advise you as well as provide you the brief insight

of the auditing related issues, risks and other concerns of the different units of DHL. This

memo mainly have the five sections while each section discuss about the separate audit

related issues of the DHL. The first section of the memo discuss about the Pellegrino Shoes

including the key business risks and those accounts which is utmost probable to be

pretentious by scam at Pellegrino Shoes. Second section deals with the transition of new

patient revenue system by St Neville’s including audit risks, key question to inquire internal

audit as well as justification for adopting the audit for the revenue of the firm. Next part of

memo covers sale of medical supplies of Acuity Vison including key account balance and

associated assertions at risk, consequences for governor environment as well as efficiency of

customer payments testing. Fourth section will discuss about undertaken account payable

2AUDITING AND ASSURANCE

test. While, the last section of the memo is all about the key assertion at risk in respect to

payment of overtime of Pellegrino Shores.

First case is that the fraud at Pellegrino Shores which is fully owned subsidiary of the DHL.

This is a retirement village located in Port Macquarie. It is observed that the firm dismissed a

senior staff member last month due to her involvement in the fraud. She used to reduce the

fees of number of resident and privately receive secrete payment from them. This fraud is

highlighted by her co – employees. Here, the key business of the Pellegrino Shores is present

in the authentication of accessing the resident data base. As she was only expected to apprise

room location but she also have the access to reduce the charges for the other services

provided to the residents. Hence, the biggest business risk of this fraud is associated with the

authentication of access to the resident data base. The need to develop such system in which

any staff member only be able to access as much as required as per his allocated job. While,

in this fraud case, mainly two audit assertions are involved those are completeness and

accuracy. As discussed above the senior staff member decreases the cost of the various

services provided to the residents, hence, there is high chances that the she must be omitted

various revenue related transaction to minimize the cost of the services for the resident.

Hence, the financial report prepared by the firm does not provide the complete information of

the financial transactions. Secondly, as her reduces the cost of the services and receive

privately other benefits, hence, transaction recorded in the accounting report does not

consider the actual balance of the firm as this is based on the tempered balances. Hence, the

completeness and accuracy are the two audit assertion which are present in the fraud case of

the Pellegrino Shores.

If we talk about the other subsidiary of DHL that is St Neville’s, then the main auditing

aspect of this subsidiary is patient revenue system of the this subsidiary. Here, St Neville’s

adopted new patient revenue system from ‘Home-grown’ to ‘Off the shelf’. The new patient

test. While, the last section of the memo is all about the key assertion at risk in respect to

payment of overtime of Pellegrino Shores.

First case is that the fraud at Pellegrino Shores which is fully owned subsidiary of the DHL.

This is a retirement village located in Port Macquarie. It is observed that the firm dismissed a

senior staff member last month due to her involvement in the fraud. She used to reduce the

fees of number of resident and privately receive secrete payment from them. This fraud is

highlighted by her co – employees. Here, the key business of the Pellegrino Shores is present

in the authentication of accessing the resident data base. As she was only expected to apprise

room location but she also have the access to reduce the charges for the other services

provided to the residents. Hence, the biggest business risk of this fraud is associated with the

authentication of access to the resident data base. The need to develop such system in which

any staff member only be able to access as much as required as per his allocated job. While,

in this fraud case, mainly two audit assertions are involved those are completeness and

accuracy. As discussed above the senior staff member decreases the cost of the various

services provided to the residents, hence, there is high chances that the she must be omitted

various revenue related transaction to minimize the cost of the services for the resident.

Hence, the financial report prepared by the firm does not provide the complete information of

the financial transactions. Secondly, as her reduces the cost of the services and receive

privately other benefits, hence, transaction recorded in the accounting report does not

consider the actual balance of the firm as this is based on the tempered balances. Hence, the

completeness and accuracy are the two audit assertion which are present in the fraud case of

the Pellegrino Shores.

If we talk about the other subsidiary of DHL that is St Neville’s, then the main auditing

aspect of this subsidiary is patient revenue system of the this subsidiary. Here, St Neville’s

adopted new patient revenue system from ‘Home-grown’ to ‘Off the shelf’. The new patient

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3AUDITING AND ASSURANCE

revenue system is system of DHL and DHL remained involved in the entire switchover

period. This system mainly perform the function related to the billing for the patients while

calculating all subsidies and all. While, analysing the impact of the switching the patient

revenue system, it has been noticed that the due to the power surge all the data related to the

billing of patient for last two weeks need to re – entered. Secondly, it is observed the fresh

structure is not capable to calculate fee statement as per decided medical fund as well as

pensioner grant tariffs. System also faces the issues with those patients who have same

surname. It is also observed that the system is billing lower room rate to the patient without

any reason. Hence, in this case the main two audit risks are detection risk and control risk. As

the entire system is based on the system hence there is high chances that the auditor will not

able to sense the material misstatement before audit. Hence, to avoid this the auditor needs to

prepare the proper audit planning to detect the audit risk. While, the control audit risk is also

associated with the case as the new system does not calculate the subsidies and all properly

and charge the lower rate to the patients without any reason, hence auditor need to identify

the actual number associated with related accounts. For this the auditor need to ask some

question to the internal auditors those are the accuracy in calculating the subsidies by the

system and the fairness of the re – entered revenue transaction of the last two weeks along

with the evidence. The main reason behind choosing the above audit strategy is that the main

area which need the proper audit in this case is the calculation of the subsidies and all the

transaction those are need to be re – entered because of the power surge.

In respect of the Acuity Vison, the additional information is required about the sale of Acuity

Vison. Acuity Vison is another subsidiary of the DHL which directly sale its own range of

health materials. The sales crew of Acuity Vison is responsible for the all the sales and

receive bonus for sales founded on dollar value of the sale along with the fairly low salary.

The audit senior selected a sample of the customer payment for the medical supplies which is

revenue system is system of DHL and DHL remained involved in the entire switchover

period. This system mainly perform the function related to the billing for the patients while

calculating all subsidies and all. While, analysing the impact of the switching the patient

revenue system, it has been noticed that the due to the power surge all the data related to the

billing of patient for last two weeks need to re – entered. Secondly, it is observed the fresh

structure is not capable to calculate fee statement as per decided medical fund as well as

pensioner grant tariffs. System also faces the issues with those patients who have same

surname. It is also observed that the system is billing lower room rate to the patient without

any reason. Hence, in this case the main two audit risks are detection risk and control risk. As

the entire system is based on the system hence there is high chances that the auditor will not

able to sense the material misstatement before audit. Hence, to avoid this the auditor needs to

prepare the proper audit planning to detect the audit risk. While, the control audit risk is also

associated with the case as the new system does not calculate the subsidies and all properly

and charge the lower rate to the patients without any reason, hence auditor need to identify

the actual number associated with related accounts. For this the auditor need to ask some

question to the internal auditors those are the accuracy in calculating the subsidies by the

system and the fairness of the re – entered revenue transaction of the last two weeks along

with the evidence. The main reason behind choosing the above audit strategy is that the main

area which need the proper audit in this case is the calculation of the subsidies and all the

transaction those are need to be re – entered because of the power surge.

In respect of the Acuity Vison, the additional information is required about the sale of Acuity

Vison. Acuity Vison is another subsidiary of the DHL which directly sale its own range of

health materials. The sales crew of Acuity Vison is responsible for the all the sales and

receive bonus for sales founded on dollar value of the sale along with the fairly low salary.

The audit senior selected a sample of the customer payment for the medical supplies which is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4AUDITING AND ASSURANCE

received by the firm just after the year end and find that the entries regarding this sale is all

entered in the general ledger and customers account. Here, the key account balances which

are affected by this activity are the sale of the firm, value of the debtors, bonus of the sales

team, gross profit and net profit of the firm for the period. As this sales is not for the last year

but it was included in the last year financial statement. Hence, this sale which is for the next

year increases the profit of the firm for the last year as well as this also increases the bonus

amount of sales management as this is also based on the amount of sale. Further, it is

suggested to the management of the DHL to implement the environment control in the firm

the management of the DHL needs to consider various aspects like integrity, assurance to

examine inconsistencies, evaluating accountabilities and assiduousness in planning structures.

Lastly, it is also essential to recognise effectiveness of the payment structure testing. The

payment system testing identifies the area of risk within the payment system which improve

the cost effectiveness in the payment system, speed up market as well as confirms effective

payment centres, which justify the condition of the today’s differentiated world. Hence, it is

suggested to properly perform the customer payment testing to avoid the above discusses

auditing issues and to safe gaud the profit of the firm as well as the interest of the

stakeholders.

The test performed by the senior auditor in respect to the account payable revels in the first

test that the two out of the fifteen selected creditors the balance are inflated and in second test

stated that the three out of twenty suppliers was not approved and the improper discounts had

been applied to them. Following table shows the all related information of the stated case of

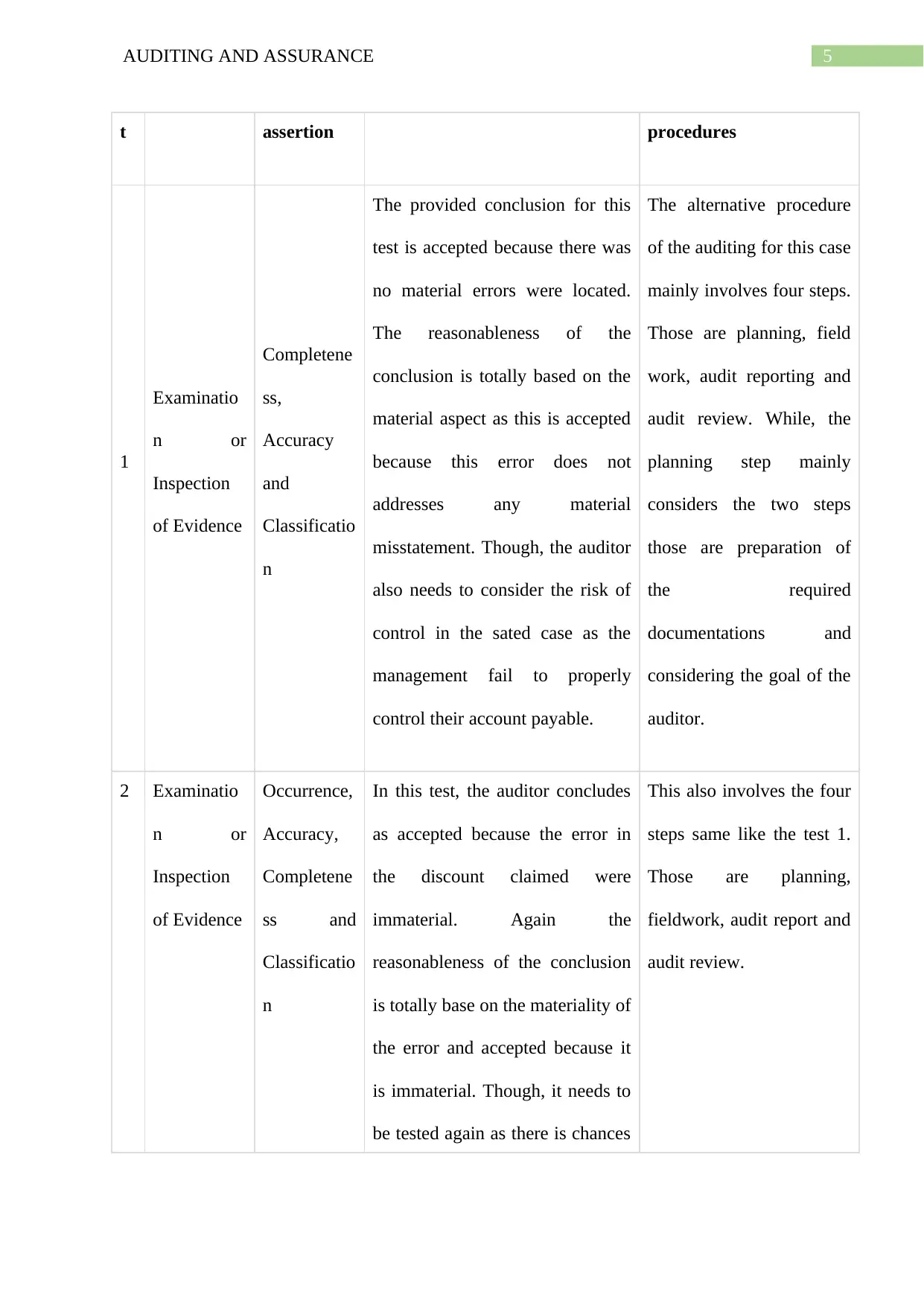

DHL accounts payables: -

T

es

type of test key reasonableness of conclusion additional audit

received by the firm just after the year end and find that the entries regarding this sale is all

entered in the general ledger and customers account. Here, the key account balances which

are affected by this activity are the sale of the firm, value of the debtors, bonus of the sales

team, gross profit and net profit of the firm for the period. As this sales is not for the last year

but it was included in the last year financial statement. Hence, this sale which is for the next

year increases the profit of the firm for the last year as well as this also increases the bonus

amount of sales management as this is also based on the amount of sale. Further, it is

suggested to the management of the DHL to implement the environment control in the firm

the management of the DHL needs to consider various aspects like integrity, assurance to

examine inconsistencies, evaluating accountabilities and assiduousness in planning structures.

Lastly, it is also essential to recognise effectiveness of the payment structure testing. The

payment system testing identifies the area of risk within the payment system which improve

the cost effectiveness in the payment system, speed up market as well as confirms effective

payment centres, which justify the condition of the today’s differentiated world. Hence, it is

suggested to properly perform the customer payment testing to avoid the above discusses

auditing issues and to safe gaud the profit of the firm as well as the interest of the

stakeholders.

The test performed by the senior auditor in respect to the account payable revels in the first

test that the two out of the fifteen selected creditors the balance are inflated and in second test

stated that the three out of twenty suppliers was not approved and the improper discounts had

been applied to them. Following table shows the all related information of the stated case of

DHL accounts payables: -

T

es

type of test key reasonableness of conclusion additional audit

5AUDITING AND ASSURANCE

t assertion procedures

1

Examinatio

n or

Inspection

of Evidence

Completene

ss,

Accuracy

and

Classificatio

n

The provided conclusion for this

test is accepted because there was

no material errors were located.

The reasonableness of the

conclusion is totally based on the

material aspect as this is accepted

because this error does not

addresses any material

misstatement. Though, the auditor

also needs to consider the risk of

control in the sated case as the

management fail to properly

control their account payable.

The alternative procedure

of the auditing for this case

mainly involves four steps.

Those are planning, field

work, audit reporting and

audit review. While, the

planning step mainly

considers the two steps

those are preparation of

the required

documentations and

considering the goal of the

auditor.

2 Examinatio

n or

Inspection

of Evidence

Occurrence,

Accuracy,

Completene

ss and

Classificatio

n

In this test, the auditor concludes

as accepted because the error in

the discount claimed were

immaterial. Again the

reasonableness of the conclusion

is totally base on the materiality of

the error and accepted because it

is immaterial. Though, it needs to

be tested again as there is chances

This also involves the four

steps same like the test 1.

Those are planning,

fieldwork, audit report and

audit review.

t assertion procedures

1

Examinatio

n or

Inspection

of Evidence

Completene

ss,

Accuracy

and

Classificatio

n

The provided conclusion for this

test is accepted because there was

no material errors were located.

The reasonableness of the

conclusion is totally based on the

material aspect as this is accepted

because this error does not

addresses any material

misstatement. Though, the auditor

also needs to consider the risk of

control in the sated case as the

management fail to properly

control their account payable.

The alternative procedure

of the auditing for this case

mainly involves four steps.

Those are planning, field

work, audit reporting and

audit review. While, the

planning step mainly

considers the two steps

those are preparation of

the required

documentations and

considering the goal of the

auditor.

2 Examinatio

n or

Inspection

of Evidence

Occurrence,

Accuracy,

Completene

ss and

Classificatio

n

In this test, the auditor concludes

as accepted because the error in

the discount claimed were

immaterial. Again the

reasonableness of the conclusion

is totally base on the materiality of

the error and accepted because it

is immaterial. Though, it needs to

be tested again as there is chances

This also involves the four

steps same like the test 1.

Those are planning,

fieldwork, audit report and

audit review.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6AUDITING AND ASSURANCE

of involvement of material.

Lastly, this will discuss about the auditing issues in the payroll system of Pellegrino Shores,

as discussed above that the along with the full – time staffs, Pellegrino Shores also have a

significant total of spontaneous nursing, housework as well as administrative staff. They

often need to labour overtime on weekends as well as in night shifts as there is lack of the

sufficient staffs. Hence, the payment for the overtime rate and standards weekend and night

shifts commonly happened in the firm. Hence, the key auditing assertions in the above case

are the Accuracy, Classification, Completeness and Occurrence. The accuracy is about to

analyse that the amount of the overtime time and night shift allowanced to the staffs is

accurately consider in the books of account or not. The classification is about the over - time

as well as night allowances are properly classified and entered under the appropriate account

or not. Completeness assurance that all the relevant information of the payroll of firm is

completely reported by the firm in their financial report in the correct manner. While

occurrence assertions assures that the all payroll related accounting information reported by

the firm in financial report are truly happened or not. The suggested preventive internal

control for this case is segregation of duties. As the preventive internal control activities are

those activities which are performed by the management of the firm to prevent the assets of

the firm. Hence, the suggested preventive control for the above case is the segregation of

duties, in this all the related responsibilities will be perform by the separate individual and

expected that this will minimize the material misstatement in the payroll system of the firm.

Further, the suggested detective controls for this is control total. In this management used to

analyse the register of the employee attendance with the register of the visiting log register to

verify the actual working hour of the employee with the attendance of staffs.

of involvement of material.

Lastly, this will discuss about the auditing issues in the payroll system of Pellegrino Shores,

as discussed above that the along with the full – time staffs, Pellegrino Shores also have a

significant total of spontaneous nursing, housework as well as administrative staff. They

often need to labour overtime on weekends as well as in night shifts as there is lack of the

sufficient staffs. Hence, the payment for the overtime rate and standards weekend and night

shifts commonly happened in the firm. Hence, the key auditing assertions in the above case

are the Accuracy, Classification, Completeness and Occurrence. The accuracy is about to

analyse that the amount of the overtime time and night shift allowanced to the staffs is

accurately consider in the books of account or not. The classification is about the over - time

as well as night allowances are properly classified and entered under the appropriate account

or not. Completeness assurance that all the relevant information of the payroll of firm is

completely reported by the firm in their financial report in the correct manner. While

occurrence assertions assures that the all payroll related accounting information reported by

the firm in financial report are truly happened or not. The suggested preventive internal

control for this case is segregation of duties. As the preventive internal control activities are

those activities which are performed by the management of the firm to prevent the assets of

the firm. Hence, the suggested preventive control for the above case is the segregation of

duties, in this all the related responsibilities will be perform by the separate individual and

expected that this will minimize the material misstatement in the payroll system of the firm.

Further, the suggested detective controls for this is control total. In this management used to

analyse the register of the employee attendance with the register of the visiting log register to

verify the actual working hour of the employee with the attendance of staffs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7AUDITING AND ASSURANCE

Hence, the fraud at Pellegrino Shoes mostly affect the revenue of the firm and the key

business of for the firm is associated with the authentication of the access of data. While the

audit assertions associated with the fraud in the accuracy and completes. The new billing

system adopted by St Neville also have several audit risk and issues. Acuity Vison have the

issues with the arrangements for paying its sales team as they try to maximize the sale to get

the bonus. While, the account payable testing of senior auditor and conclusion provided for

the test is appropriate but need some further considerations. Lastly, the payroll system of

Pellegrino Shores involves the preventative internal control as well as detective internal

control to straight report associated business risk.

Hence, the fraud at Pellegrino Shoes mostly affect the revenue of the firm and the key

business of for the firm is associated with the authentication of the access of data. While the

audit assertions associated with the fraud in the accuracy and completes. The new billing

system adopted by St Neville also have several audit risk and issues. Acuity Vison have the

issues with the arrangements for paying its sales team as they try to maximize the sale to get

the bonus. While, the account payable testing of senior auditor and conclusion provided for

the test is appropriate but need some further considerations. Lastly, the payroll system of

Pellegrino Shores involves the preventative internal control as well as detective internal

control to straight report associated business risk.

8AUDITING AND ASSURANCE

Bibliography

Basu, S. K. (2016). Auditing & Assurance. Pearson Education India.

Bentley-Goode, K. A., Newton, N. J., & Thompson, A. M. (2017). Business strategy, internal

control over financial reporting, and audit reporting quality. Auditing: A Journal of

Practice & Theory, 36(4), 49-69.

Bentley-Goode, K. A., Newton, N. J., & Thompson, A. M. (2017). Business strategy, internal

control over financial reporting, and audit reporting quality. Auditing: A Journal of

Practice & Theory, 36(4), 49-69.

Brink, W. D., Grenier, J. H., Pyzoha, J. S., & Reffett, A. (2019). The effects of clawbacks on

Auditors’ propensity to propose restatements and risk assessments. Journal of

Business Ethics, 158(2), 313-332.

Bumgarner, N., & Vasarhelyi, M. A. (2018). Continuous auditing—A new view.

In Continuous Auditing: Theory and Application (pp. 7-51). Emerald Publishing

Limited.

Cohen, J., Krishnamoorthy, G., & Wright, A. (2017). Enterprise Risk Management and the

Financial Reporting Process: The Experiences of Audit Committee Members, CFO s,

and External Auditors. Contemporary Accounting Research, 34(2), 1178-1209.

Graham, L. (2015). Internal control audit and compliance: documentation and testing under

the new coso framework. John Wiley & Sons.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Khlif, H., & Samaha, K. (2016). Audit committee activity and internal control quality in

Egypt: does external auditor’s size matter?. Managerial Auditing Journal, 31(3), 269-

289.

Bibliography

Basu, S. K. (2016). Auditing & Assurance. Pearson Education India.

Bentley-Goode, K. A., Newton, N. J., & Thompson, A. M. (2017). Business strategy, internal

control over financial reporting, and audit reporting quality. Auditing: A Journal of

Practice & Theory, 36(4), 49-69.

Bentley-Goode, K. A., Newton, N. J., & Thompson, A. M. (2017). Business strategy, internal

control over financial reporting, and audit reporting quality. Auditing: A Journal of

Practice & Theory, 36(4), 49-69.

Brink, W. D., Grenier, J. H., Pyzoha, J. S., & Reffett, A. (2019). The effects of clawbacks on

Auditors’ propensity to propose restatements and risk assessments. Journal of

Business Ethics, 158(2), 313-332.

Bumgarner, N., & Vasarhelyi, M. A. (2018). Continuous auditing—A new view.

In Continuous Auditing: Theory and Application (pp. 7-51). Emerald Publishing

Limited.

Cohen, J., Krishnamoorthy, G., & Wright, A. (2017). Enterprise Risk Management and the

Financial Reporting Process: The Experiences of Audit Committee Members, CFO s,

and External Auditors. Contemporary Accounting Research, 34(2), 1178-1209.

Graham, L. (2015). Internal control audit and compliance: documentation and testing under

the new coso framework. John Wiley & Sons.

Griffiths, P. (2016). Risk-based auditing. Routledge.

Khlif, H., & Samaha, K. (2016). Audit committee activity and internal control quality in

Egypt: does external auditor’s size matter?. Managerial Auditing Journal, 31(3), 269-

289.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9AUDITING AND ASSURANCE

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Mock, T. J., & Fukukawa, H. (2015). Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in Accounting, 28(2), 75-84.

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism:

Unintended consequences on evidence evaluation. International Journal of

Auditing, 22(1), 55-64.

Newton, Nathan J., Julie S. Persellin, Dechun Wang, & Michael S. Wilkins (2016). "Internal

control opinion shopping and audit market competition." The Accounting Review 91,

no. 2 (2015): 603-623.

Sadgrove, K. (2016). The complete guide to business risk management. Routledge.

Simnett, R., & Huggins, A. L. (2015). Integrated reporting and assurance: where can research

add value?. Sustainability Accounting, Management and Policy Journal, 6(1), 29-53.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

Knechel, W. R., & Salterio, S. E. (2016). Auditing: Assurance and risk. Routledge.

Mock, T. J., & Fukukawa, H. (2015). Auditors' risk assessments: The effects of elicitation

approach and assertion framing. Behavioral Research in Accounting, 28(2), 75-84.

Mubako, G., & O'Donnell, E. (2018). Effect of fraud risk assessments on auditor skepticism:

Unintended consequences on evidence evaluation. International Journal of

Auditing, 22(1), 55-64.

Newton, Nathan J., Julie S. Persellin, Dechun Wang, & Michael S. Wilkins (2016). "Internal

control opinion shopping and audit market competition." The Accounting Review 91,

no. 2 (2015): 603-623.

Sadgrove, K. (2016). The complete guide to business risk management. Routledge.

Simnett, R., & Huggins, A. L. (2015). Integrated reporting and assurance: where can research

add value?. Sustainability Accounting, Management and Policy Journal, 6(1), 29-53.

William Jr, M., Glover, S., & Prawitt, D. (2016). Auditing and assurance services: A

systematic approach. McGraw-Hill Education.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.