Duolever: Financial Analysis of Plastic Packaging Recycling Options

VerifiedAdded on 2023/01/18

|6

|1516

|33

Report

AI Summary

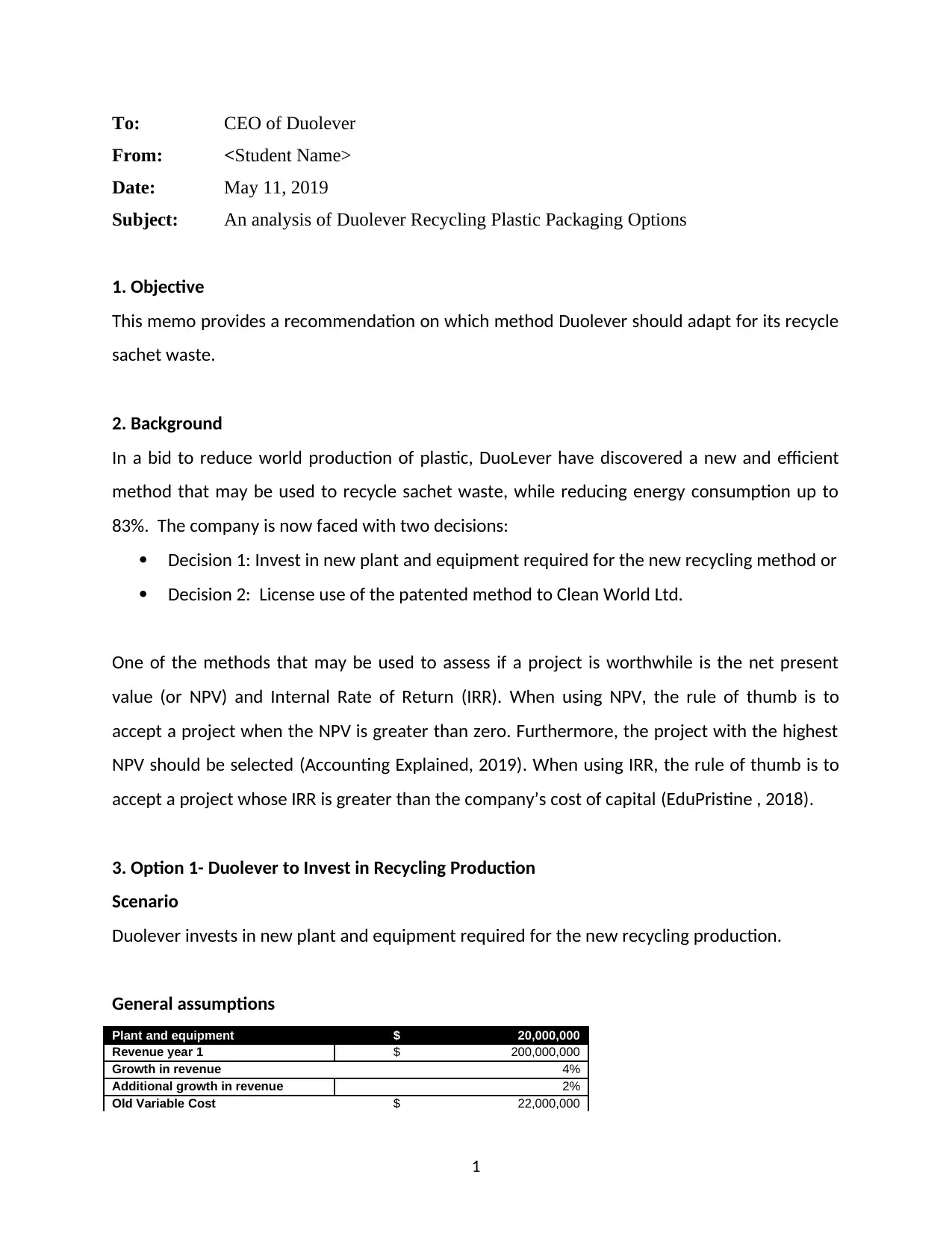

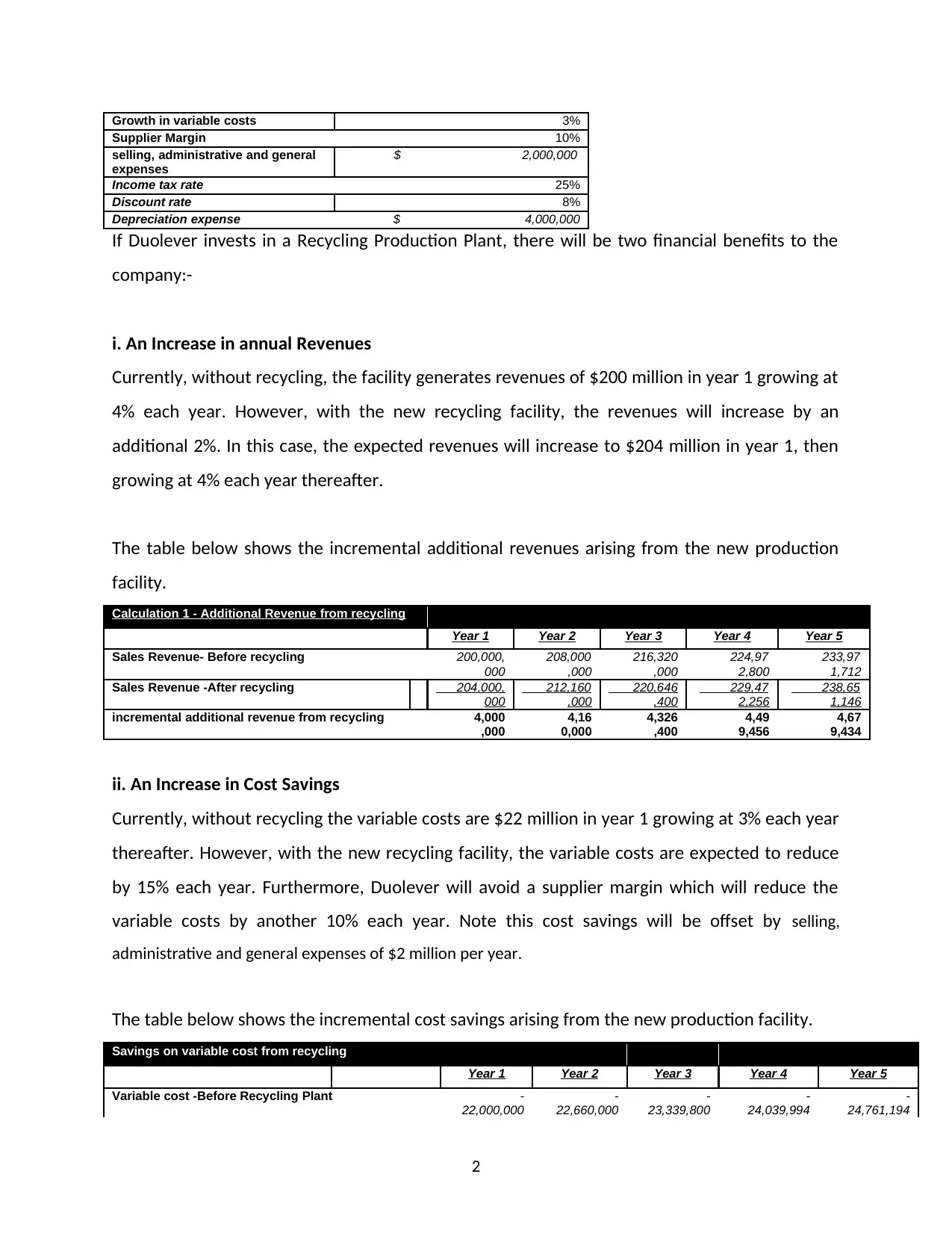

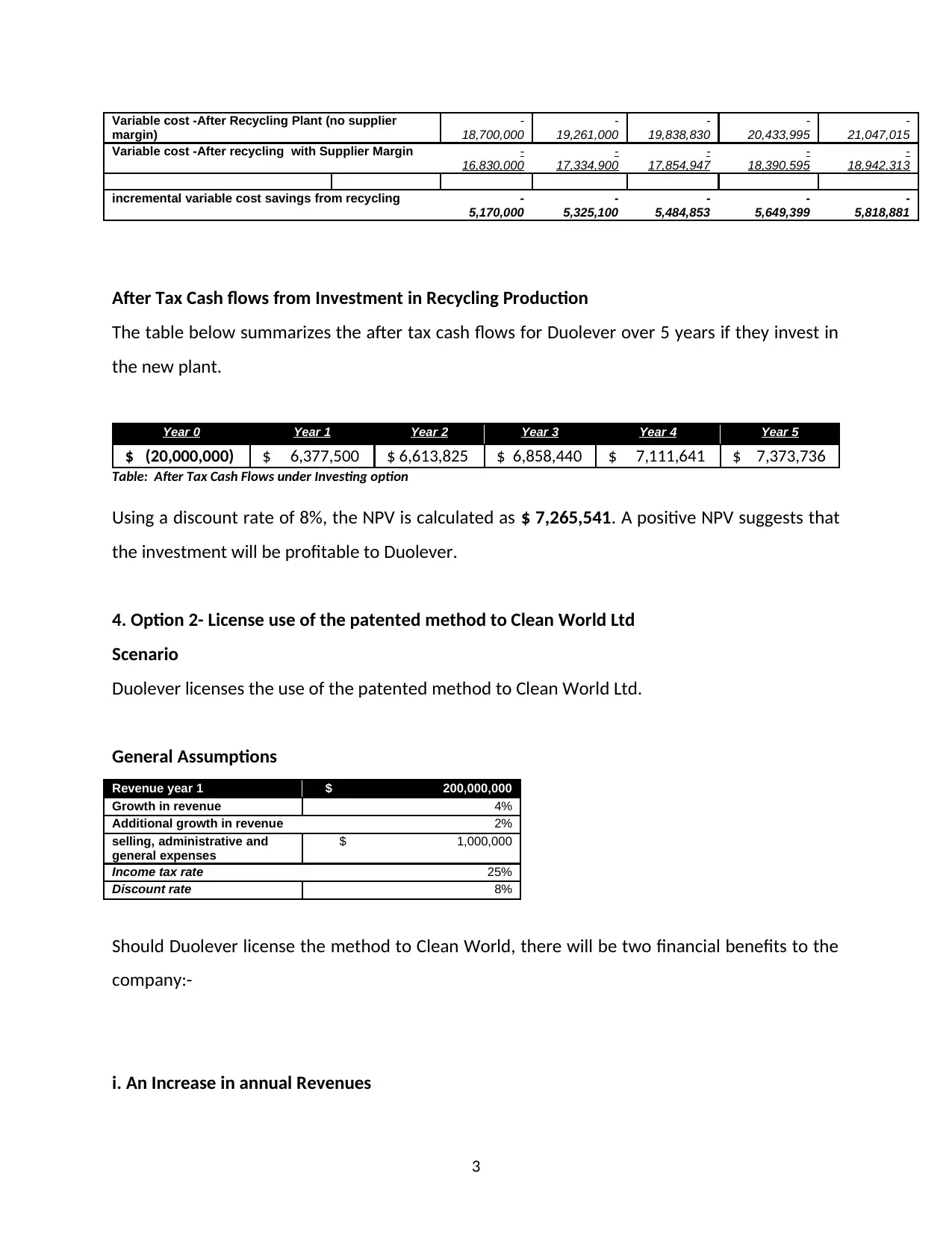

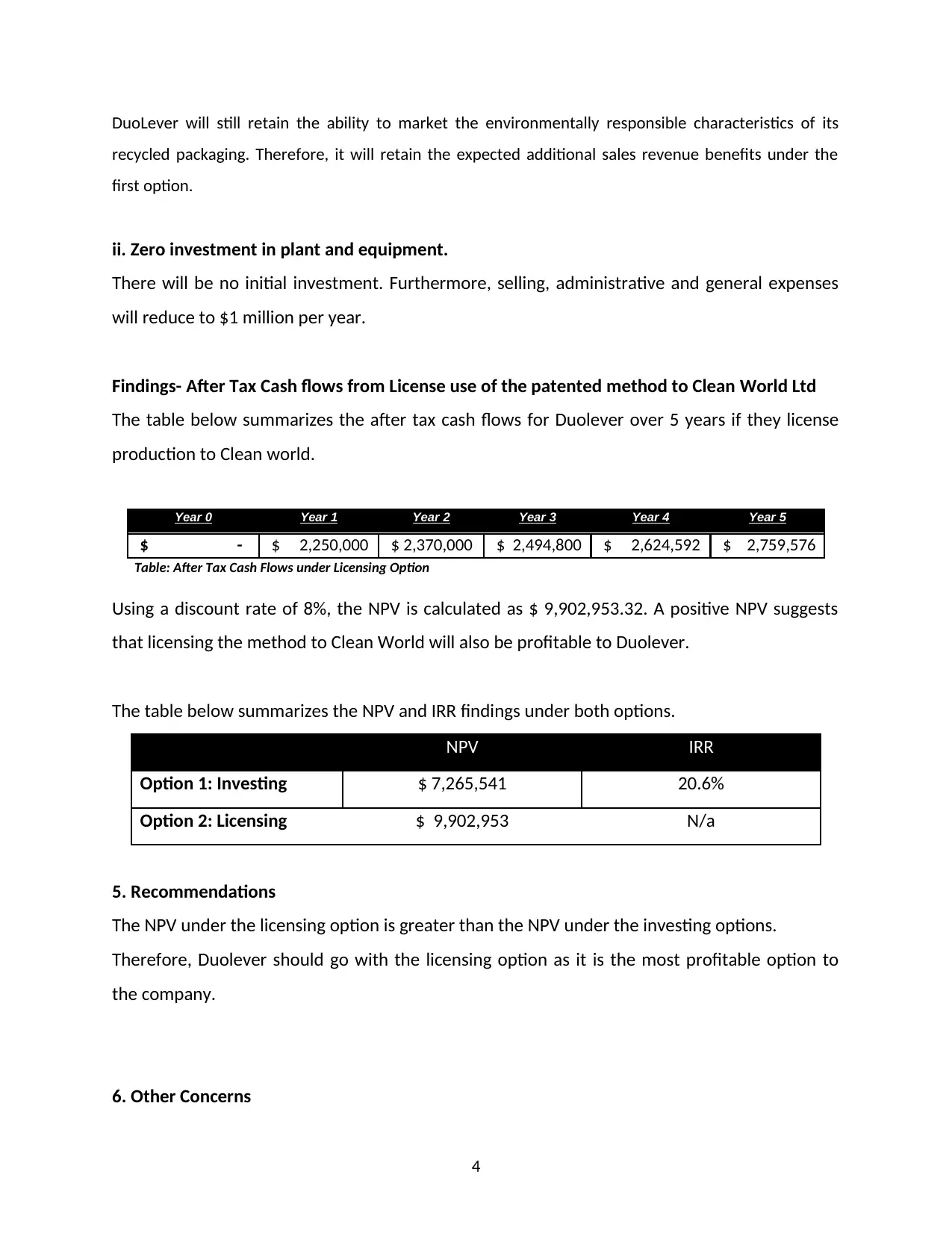

This memo presents a financial analysis of Duolever's plastic sachet waste recycling options. The company faces a decision between investing in a new recycling plant or licensing its patented method to Clean World Ltd. The analysis employs Net Present Value (NPV) and Internal Rate of Return (IRR) to evaluate the profitability of each option. The report details the assumptions, including revenue growth, variable costs, and tax rates, for both scenarios. The investment option involves increased revenues and cost savings due to recycling, while the licensing option offers revenue from the patented method with no initial investment. The NPV calculations indicate that the licensing option is more profitable, leading to the recommendation that Duolever should license its method. The memo also highlights the importance of understanding forecasting risks and the impact of key assumptions on the financial outcomes. The appendix provides detailed cash flow analyses for both options.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.