North South University: Time Series Analysis of DBBL (Fin 464)

VerifiedAdded on 2022/11/21

|32

|6069

|301

Project

AI Summary

This project provides a comprehensive time series analysis of Dutch Bangla Bank Limited (DBBL), examining its financial performance from 2017 to 2021. The analysis focuses on key financial ratios across several categories, including liquidity, profitability, efficiency, financial risk, and market position. The methodology employed involves the calculation and interpretation of various ratios using data extracted from DBBL's annual reports and other sources. The report details the trends and fluctuations observed in these ratios over the five-year period, including the impact of the COVID-19 pandemic. Findings include insights into DBBL's cash position, liquid securities, capacity ratio, hot money ratio, and asset utilization, along with an overview of the bank's operations, mission, and vision. The project also acknowledges limitations, such as data availability and the influence of external factors. This project was conducted for a Bank Management course (Fin 464) at North South University.

1 | P a g e

Group Assignment: Time series analysis of “Dutch Bangla

Bank Limited”

Course: Bank Management

Course Code: Fin 464

Section: 3

Prepared By:

Name ID

Syeda Numaira Shehrin 2022400630

Tahmid Shahriyar 1931791630

Mayesha Nuzhat Khandkar 1911465630

Submitted To:

Mr. Mokhdum Morshed [MdM]

Senior Lecturer

Department of Accounting & Finance

School of Business & Economics

North South University

Date of Submission: 2nd September, 2022

Group Assignment: Time series analysis of “Dutch Bangla

Bank Limited”

Course: Bank Management

Course Code: Fin 464

Section: 3

Prepared By:

Name ID

Syeda Numaira Shehrin 2022400630

Tahmid Shahriyar 1931791630

Mayesha Nuzhat Khandkar 1911465630

Submitted To:

Mr. Mokhdum Morshed [MdM]

Senior Lecturer

Department of Accounting & Finance

School of Business & Economics

North South University

Date of Submission: 2nd September, 2022

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 | P a g e

Acknowledgment:

We are grateful to our respected faculty member and course instructor, Mr. Mokhdum Morshed

sir, for providing us with the opportunity to work as a group and complete this project with a

united effort and utmost efficiency, as well as for his guidance, sustained interest, constant

encouragement, motivating inspiration, directions, valuable suggestions, and advice. We are

grateful to North South University's Department of Accounting and Finance for providing such

a well-designed course and facilities, which greatly aided us in completing our project

methodically. Finally, we would like to express our gratitude to everyone who assisted us,

directly or indirectly, in the smooth execution and completion of this report.

Acknowledgment:

We are grateful to our respected faculty member and course instructor, Mr. Mokhdum Morshed

sir, for providing us with the opportunity to work as a group and complete this project with a

united effort and utmost efficiency, as well as for his guidance, sustained interest, constant

encouragement, motivating inspiration, directions, valuable suggestions, and advice. We are

grateful to North South University's Department of Accounting and Finance for providing such

a well-designed course and facilities, which greatly aided us in completing our project

methodically. Finally, we would like to express our gratitude to everyone who assisted us,

directly or indirectly, in the smooth execution and completion of this report.

3 | P a g e

Executive Summary:

For this following project, we conducted a performance analysis on our given bank which is

Dutch Bangla Bank Limited. We primarily conducted ratio analysis for this bank. For ratio

analysis, we used the historical data for the last five years, 2017-2021. We used time series

analysis and for ratio analysis, we focused on profitability, liquidity, efficiency, financial

risk, and market positions. Lastly, the following report contains two segments: excel and

word documents. The excel segment contains all the necessary assigned calculations

centering on the project and the word contains the written body of the report which will be

shown in the table of contents below which will further shed light on components we worked

with for the completion of our report.

Executive Summary:

For this following project, we conducted a performance analysis on our given bank which is

Dutch Bangla Bank Limited. We primarily conducted ratio analysis for this bank. For ratio

analysis, we used the historical data for the last five years, 2017-2021. We used time series

analysis and for ratio analysis, we focused on profitability, liquidity, efficiency, financial

risk, and market positions. Lastly, the following report contains two segments: excel and

word documents. The excel segment contains all the necessary assigned calculations

centering on the project and the word contains the written body of the report which will be

shown in the table of contents below which will further shed light on components we worked

with for the completion of our report.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 | P a g e

Table of Contents

Topic Page Number

Introduction 5

Methodology 5

Limitations 6

Overview of the Assigned Bank 7

Findings and Analysis 8-30

Recommendations and Conclusions 31

Appendix 31

References 32

Table of Contents

Topic Page Number

Introduction 5

Methodology 5

Limitations 6

Overview of the Assigned Bank 7

Findings and Analysis 8-30

Recommendations and Conclusions 31

Appendix 31

References 32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 | P a g e

Introduction:

In today’s world, banks are the heart of the economic system. If the banking industry fails, the

economy will collapse, demonstrating the importance of this industry in comparison to others.

Commercial banks play an important role in the development of the economy's financial structure

by making large investments in markets to bridge the gap between surplus and deficit units. Banks

are heavily regulated by the government because they deal with public deposits. Furthermore, as

banks control the circulation of money, a country's economic development is heavily reliant on

them. Thus, a bank's performance must be well organized because a strong banking sector is

critical for growth, job creation, wealth creation, poverty eradication, entrepreneurial activity, and

GDP growth. As a result, our course instructor assigned us the task of analyzing the performance

of Dutch Bangla Bank Limited. We will be using historical data from the last five years (2017-

2021). For these, we will primarily use ratio analysis to understand the liquidity position,

efficiency, financial risk, profitability, and market position.

Methodology:

For this report analyzing the profitability, risk exposure, liquidity position, and market analysis for

Dutch Bangla Bank Ltd we used Ratios as our main tool for analysis. We used Liquidity Indicator

Ratios, Profitability Ratios, Efficiency Ratios, and Market Ratios to analyze the different aspects

of this commercial bank. We did a time series analysis using the ratios we calculated. A time series

analysis is the comparison of different values of the same company for a selected period. The time

period provided to us is the last five years starting from 2017 to 2021. This includes the year when

covid-19 began and thus lets us find out the effects of the economic changes on the commercial

banks due to an ongoing pandemic. To calculate these ratios, we needed data about the bank. For

this, we went for the secondary source of data; which is their annual reports. Using their annual

reports for the past five years that we collected from their official website we calculated the ratios.

Along with that, any additional information that was needed for example the closing stock prices

of DBBL each year was obtained from another website called “amarstock.com”.

Introduction:

In today’s world, banks are the heart of the economic system. If the banking industry fails, the

economy will collapse, demonstrating the importance of this industry in comparison to others.

Commercial banks play an important role in the development of the economy's financial structure

by making large investments in markets to bridge the gap between surplus and deficit units. Banks

are heavily regulated by the government because they deal with public deposits. Furthermore, as

banks control the circulation of money, a country's economic development is heavily reliant on

them. Thus, a bank's performance must be well organized because a strong banking sector is

critical for growth, job creation, wealth creation, poverty eradication, entrepreneurial activity, and

GDP growth. As a result, our course instructor assigned us the task of analyzing the performance

of Dutch Bangla Bank Limited. We will be using historical data from the last five years (2017-

2021). For these, we will primarily use ratio analysis to understand the liquidity position,

efficiency, financial risk, profitability, and market position.

Methodology:

For this report analyzing the profitability, risk exposure, liquidity position, and market analysis for

Dutch Bangla Bank Ltd we used Ratios as our main tool for analysis. We used Liquidity Indicator

Ratios, Profitability Ratios, Efficiency Ratios, and Market Ratios to analyze the different aspects

of this commercial bank. We did a time series analysis using the ratios we calculated. A time series

analysis is the comparison of different values of the same company for a selected period. The time

period provided to us is the last five years starting from 2017 to 2021. This includes the year when

covid-19 began and thus lets us find out the effects of the economic changes on the commercial

banks due to an ongoing pandemic. To calculate these ratios, we needed data about the bank. For

this, we went for the secondary source of data; which is their annual reports. Using their annual

reports for the past five years that we collected from their official website we calculated the ratios.

Along with that, any additional information that was needed for example the closing stock prices

of DBBL each year was obtained from another website called “amarstock.com”.

6 | P a g e

Limitations:

One of the major issues we faced while conducting this research was obtaining accurate values

from the bank’s financial statements. Some ratios like the Hot Money Ratio and the Expense

Control Efficiency Ratio were difficult to collect. We had to email the bank and call them multiple

times to gather the information we needed but most of our attempts were unsuccessful. However,

we eventually found the accurate values we had been looking for. Moreover, the time frame from

which we had to derive our analysis and interpretation was subject to the Coronavirus Pandemic

and its aftermath. Hence, the outcome or pattern of majority of our analysis involved the

assumption of the pandemic causing an unexpected change in the usual pattern of the ratios. This

is especially problematic as this does not give the true overview or analysis of the bank but gives

the values for when an adverse situation or anomaly is present. This data might not be a useful tool

for forecasting or comparison with future or past conditions, as there is a good chance that another

outbreak is not going to happen for another generation or even a century.

Limitations:

One of the major issues we faced while conducting this research was obtaining accurate values

from the bank’s financial statements. Some ratios like the Hot Money Ratio and the Expense

Control Efficiency Ratio were difficult to collect. We had to email the bank and call them multiple

times to gather the information we needed but most of our attempts were unsuccessful. However,

we eventually found the accurate values we had been looking for. Moreover, the time frame from

which we had to derive our analysis and interpretation was subject to the Coronavirus Pandemic

and its aftermath. Hence, the outcome or pattern of majority of our analysis involved the

assumption of the pandemic causing an unexpected change in the usual pattern of the ratios. This

is especially problematic as this does not give the true overview or analysis of the bank but gives

the values for when an adverse situation or anomaly is present. This data might not be a useful tool

for forecasting or comparison with future or past conditions, as there is a good chance that another

outbreak is not going to happen for another generation or even a century.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7 | P a g e

Overview of the Assigned Bank:

Dutch Bangla Bank Limited (DBBL):

M Sahabuddin Ahmed (Founder & Chairman) and the Dutch company FMO launched Dutch-

Bangla Bank as Bangladesh's first joint venture private commercial bank. In Bangladesh, DBBL

was founded under the Bank Companies Act of 1991 and incorporated as a public limited company

under the Companies Act of 1994. Its formal operations began on June 3, 1996.

The bank's initial focus was on financing high-growth manufacturing industries in Bangladesh.

The reasoning is that the manufacturing sector exports Bangladeshi goods all over the world. By

financing and concentrating on this sector, Bangladesh can achieve the desired growth. Another

area of emphasis for Dutch Bangla Bank is Corporate Social Responsibility (CSR). Dutch Bangla

Bank has become one of Bangladesh's largest bank donors as a result of its investment in this

sector. Because of its unique approach as a socially conscious bank, the bank has received

numerous international awards.

Dutch Bangla Bank was Bangladesh's first fully automated bank. It is also known as the "most

innovative and technologically advanced bank in Bangladesh." The Electronic-Banking Division

was founded in 2002 with the goal of rapid automation and the introduction of modern banking

services into this field. In 2003, full automation was completed, introducing plastic money to the

Bangladeshi people. Dutch Bangla Bank also operates the nation's largest ATM fleet, cutting

consumer costs and fees by 80% in the process. Furthermore, the decision by Dutch Bangla Bank

to pursue a low-profitability strategy in this sector has surprised many critics. Because of this

mindset, the majority of local banks have joined the Dutch Bangla Bank banking infrastructure

rather than developing their own.

Mission: With a commitment to social responsibility, Dutch-Bangla Bank fosters enterprise and

creativity in business and industry. Profits are not the primary focus of the bank's operations

because "man does not live by bread and butter alone."

Vision: The Dutch-Bangla Bank envisions a better Bangladesh, where the arts and letters, sports

and athletics, music and entertainment, science and education, health and hygiene, a clean and

pollution-free environment, and, most importantly, a society based on morality and ethics make

all of our lives worthwhile. The essence and ethos of Dutch-Bangla Bank are based on a cosmos

of creativity and the marvel-magic of a charmed life that abounds with the spirit of life and

adventures that contribute to human development.

Overview of the Assigned Bank:

Dutch Bangla Bank Limited (DBBL):

M Sahabuddin Ahmed (Founder & Chairman) and the Dutch company FMO launched Dutch-

Bangla Bank as Bangladesh's first joint venture private commercial bank. In Bangladesh, DBBL

was founded under the Bank Companies Act of 1991 and incorporated as a public limited company

under the Companies Act of 1994. Its formal operations began on June 3, 1996.

The bank's initial focus was on financing high-growth manufacturing industries in Bangladesh.

The reasoning is that the manufacturing sector exports Bangladeshi goods all over the world. By

financing and concentrating on this sector, Bangladesh can achieve the desired growth. Another

area of emphasis for Dutch Bangla Bank is Corporate Social Responsibility (CSR). Dutch Bangla

Bank has become one of Bangladesh's largest bank donors as a result of its investment in this

sector. Because of its unique approach as a socially conscious bank, the bank has received

numerous international awards.

Dutch Bangla Bank was Bangladesh's first fully automated bank. It is also known as the "most

innovative and technologically advanced bank in Bangladesh." The Electronic-Banking Division

was founded in 2002 with the goal of rapid automation and the introduction of modern banking

services into this field. In 2003, full automation was completed, introducing plastic money to the

Bangladeshi people. Dutch Bangla Bank also operates the nation's largest ATM fleet, cutting

consumer costs and fees by 80% in the process. Furthermore, the decision by Dutch Bangla Bank

to pursue a low-profitability strategy in this sector has surprised many critics. Because of this

mindset, the majority of local banks have joined the Dutch Bangla Bank banking infrastructure

rather than developing their own.

Mission: With a commitment to social responsibility, Dutch-Bangla Bank fosters enterprise and

creativity in business and industry. Profits are not the primary focus of the bank's operations

because "man does not live by bread and butter alone."

Vision: The Dutch-Bangla Bank envisions a better Bangladesh, where the arts and letters, sports

and athletics, music and entertainment, science and education, health and hygiene, a clean and

pollution-free environment, and, most importantly, a society based on morality and ethics make

all of our lives worthwhile. The essence and ethos of Dutch-Bangla Bank are based on a cosmos

of creativity and the marvel-magic of a charmed life that abounds with the spirit of life and

adventures that contribute to human development.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8 | P a g e

Findings and Analysis:

Liquidity Indicator Ratios

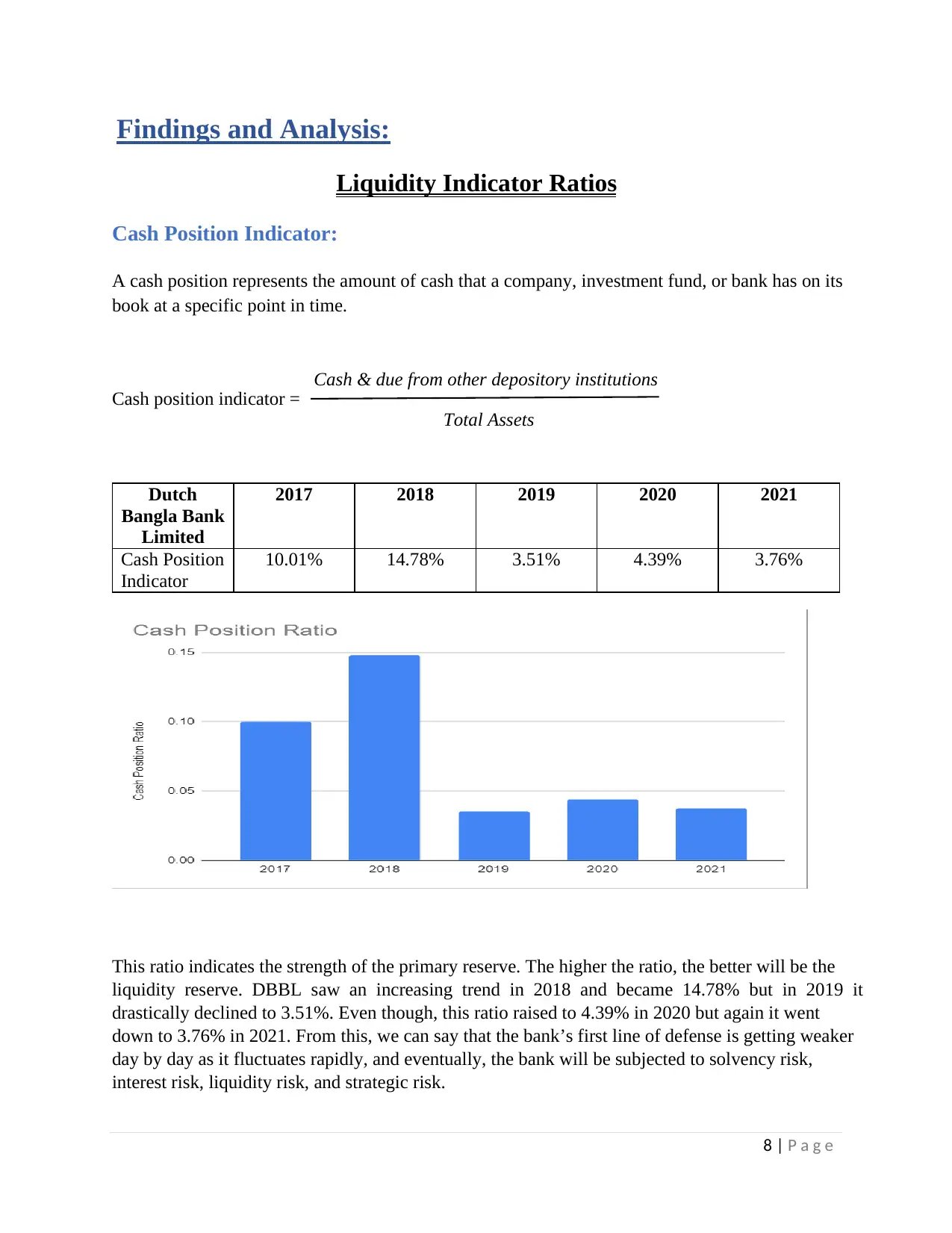

Cash Position Indicator:

A cash position represents the amount of cash that a company, investment fund, or bank has on its

book at a specific point in time.

Cash position indicator =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Cash Position

Indicator

10.01% 14.78% 3.51% 4.39% 3.76%

This ratio indicates the strength of the primary reserve. The higher the ratio, the better will be the

liquidity reserve. DBBL saw an increasing trend in 2018 and became 14.78% but in 2019 it

drastically declined to 3.51%. Even though, this ratio raised to 4.39% in 2020 but again it went

down to 3.76% in 2021. From this, we can say that the bank’s first line of defense is getting weaker

day by day as it fluctuates rapidly, and eventually, the bank will be subjected to solvency risk,

interest risk, liquidity risk, and strategic risk.

Cash & due from other depository institutions

Total Assets

Findings and Analysis:

Liquidity Indicator Ratios

Cash Position Indicator:

A cash position represents the amount of cash that a company, investment fund, or bank has on its

book at a specific point in time.

Cash position indicator =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Cash Position

Indicator

10.01% 14.78% 3.51% 4.39% 3.76%

This ratio indicates the strength of the primary reserve. The higher the ratio, the better will be the

liquidity reserve. DBBL saw an increasing trend in 2018 and became 14.78% but in 2019 it

drastically declined to 3.51%. Even though, this ratio raised to 4.39% in 2020 but again it went

down to 3.76% in 2021. From this, we can say that the bank’s first line of defense is getting weaker

day by day as it fluctuates rapidly, and eventually, the bank will be subjected to solvency risk,

interest risk, liquidity risk, and strategic risk.

Cash & due from other depository institutions

Total Assets

9 | P a g e

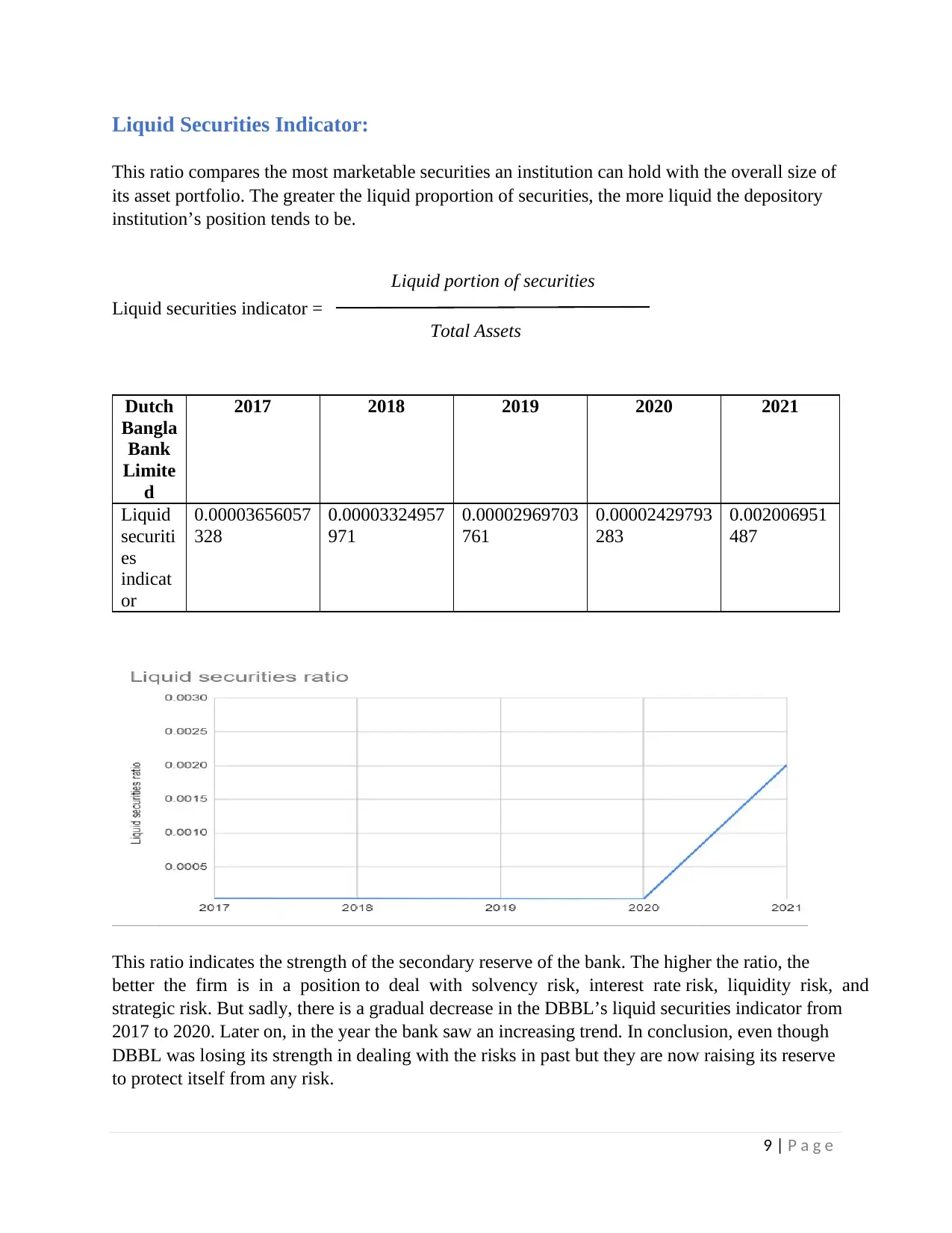

Liquid Securities Indicator:

This ratio compares the most marketable securities an institution can hold with the overall size of

its asset portfolio. The greater the liquid proportion of securities, the more liquid the depository

institution’s position tends to be.

Liquid securities indicator =

This ratio indicates the strength of the secondary reserve of the bank. The higher the ratio, the

better the firm is in a position to deal with solvency risk, interest rate risk, liquidity risk, and

strategic risk. But sadly, there is a gradual decrease in the DBBL’s liquid securities indicator from

2017 to 2020. Later on, in the year the bank saw an increasing trend. In conclusion, even though

DBBL was losing its strength in dealing with the risks in past but they are now raising its reserve

to protect itself from any risk.

Dutch

Bangla

Bank

Limite

d

2017 2018 2019 2020 2021

Liquid

securiti

es

indicat

or

0.00003656057

328

0.00003324957

971

0.00002969703

761

0.00002429793

283

0.002006951

487

Liquid portion of securities

Total Assets

Liquid Securities Indicator:

This ratio compares the most marketable securities an institution can hold with the overall size of

its asset portfolio. The greater the liquid proportion of securities, the more liquid the depository

institution’s position tends to be.

Liquid securities indicator =

This ratio indicates the strength of the secondary reserve of the bank. The higher the ratio, the

better the firm is in a position to deal with solvency risk, interest rate risk, liquidity risk, and

strategic risk. But sadly, there is a gradual decrease in the DBBL’s liquid securities indicator from

2017 to 2020. Later on, in the year the bank saw an increasing trend. In conclusion, even though

DBBL was losing its strength in dealing with the risks in past but they are now raising its reserve

to protect itself from any risk.

Dutch

Bangla

Bank

Limite

d

2017 2018 2019 2020 2021

Liquid

securiti

es

indicat

or

0.00003656057

328

0.00003324957

971

0.00002969703

761

0.00002429793

283

0.002006951

487

Liquid portion of securities

Total Assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10 | P a g e

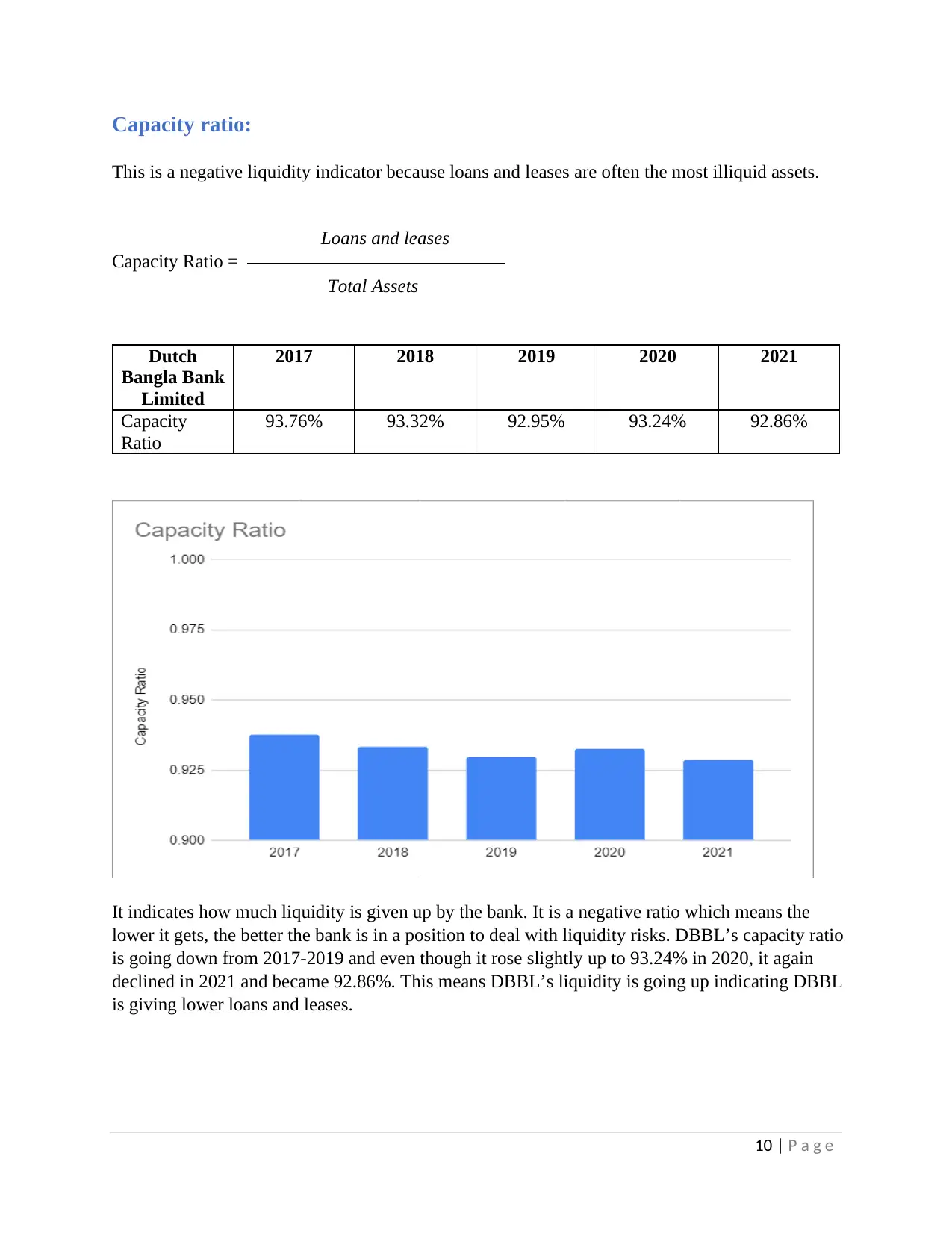

Capacity ratio:

This is a negative liquidity indicator because loans and leases are often the most illiquid assets.

Capacity Ratio =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Capacity

Ratio

93.76% 93.32% 92.95% 93.24% 92.86%

It indicates how much liquidity is given up by the bank. It is a negative ratio which means the

lower it gets, the better the bank is in a position to deal with liquidity risks. DBBL’s capacity ratio

is going down from 2017-2019 and even though it rose slightly up to 93.24% in 2020, it again

declined in 2021 and became 92.86%. This means DBBL’s liquidity is going up indicating DBBL

is giving lower loans and leases.

Total Assets

Loans and leases

Capacity ratio:

This is a negative liquidity indicator because loans and leases are often the most illiquid assets.

Capacity Ratio =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Capacity

Ratio

93.76% 93.32% 92.95% 93.24% 92.86%

It indicates how much liquidity is given up by the bank. It is a negative ratio which means the

lower it gets, the better the bank is in a position to deal with liquidity risks. DBBL’s capacity ratio

is going down from 2017-2019 and even though it rose slightly up to 93.24% in 2020, it again

declined in 2021 and became 92.86%. This means DBBL’s liquidity is going up indicating DBBL

is giving lower loans and leases.

Total Assets

Loans and leases

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11 | P a g e

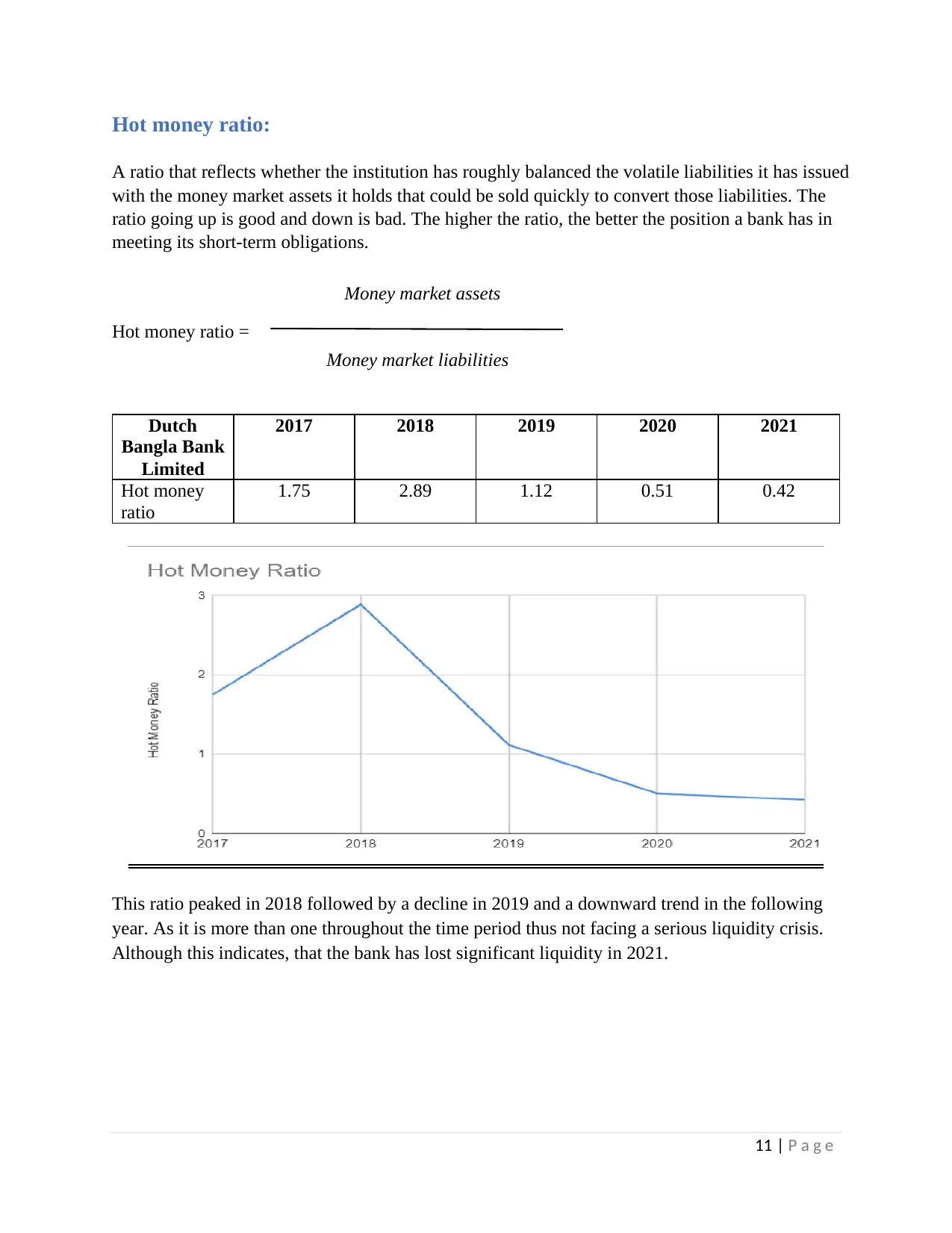

Hot money ratio:

A ratio that reflects whether the institution has roughly balanced the volatile liabilities it has issued

with the money market assets it holds that could be sold quickly to convert those liabilities. The

ratio going up is good and down is bad. The higher the ratio, the better the position a bank has in

meeting its short-term obligations.

Hot money ratio =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Hot money

ratio

1.75 2.89 1.12 0.51 0.42

This ratio peaked in 2018 followed by a decline in 2019 and a downward trend in the following

year. As it is more than one throughout the time period thus not facing a serious liquidity crisis.

Although this indicates, that the bank has lost significant liquidity in 2021.

Money market assets

Money market liabilities

Hot money ratio:

A ratio that reflects whether the institution has roughly balanced the volatile liabilities it has issued

with the money market assets it holds that could be sold quickly to convert those liabilities. The

ratio going up is good and down is bad. The higher the ratio, the better the position a bank has in

meeting its short-term obligations.

Hot money ratio =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Hot money

ratio

1.75 2.89 1.12 0.51 0.42

This ratio peaked in 2018 followed by a decline in 2019 and a downward trend in the following

year. As it is more than one throughout the time period thus not facing a serious liquidity crisis.

Although this indicates, that the bank has lost significant liquidity in 2021.

Money market assets

Money market liabilities

12 | P a g e

Efficiency Ratios

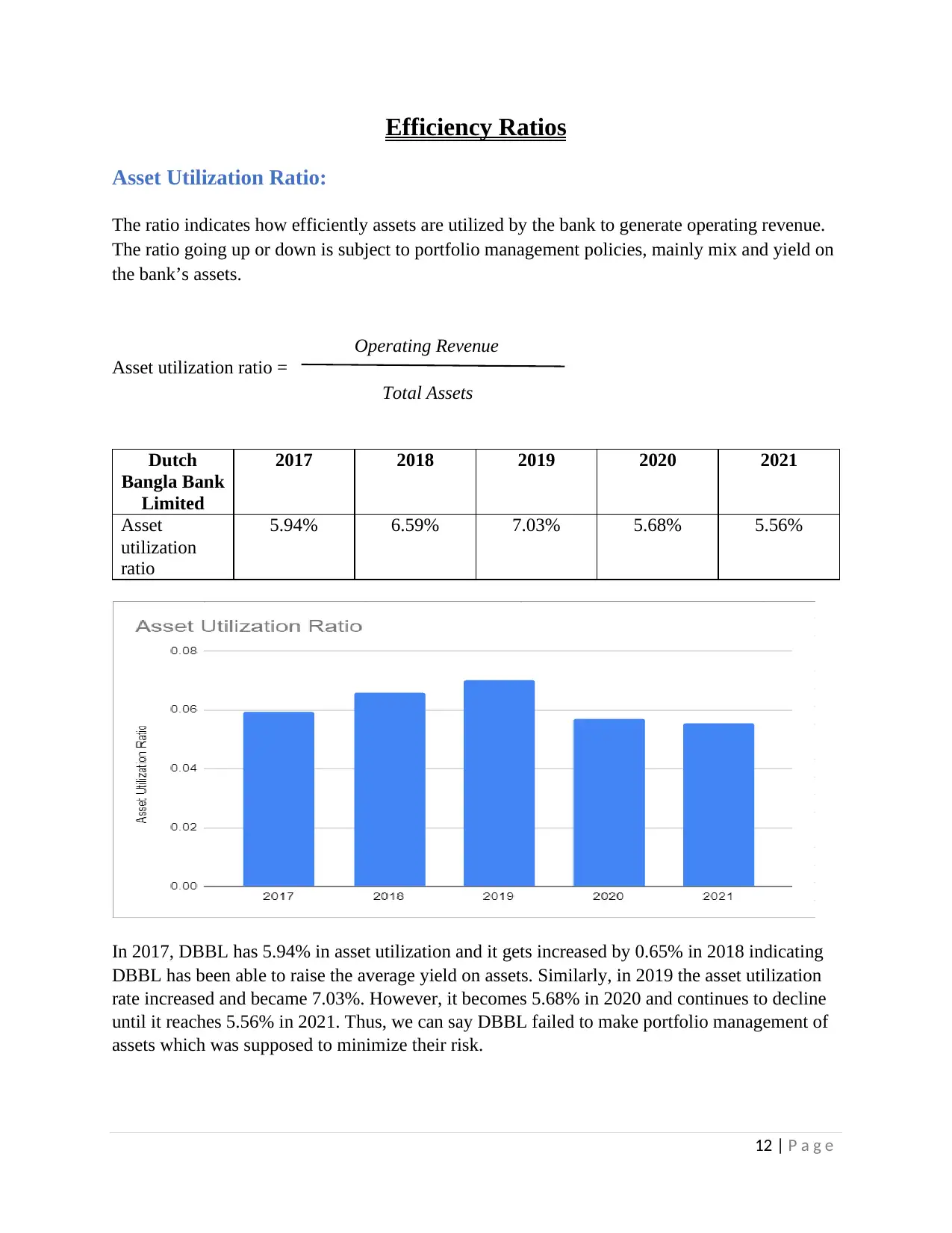

Asset Utilization Ratio:

The ratio indicates how efficiently assets are utilized by the bank to generate operating revenue.

The ratio going up or down is subject to portfolio management policies, mainly mix and yield on

the bank’s assets.

Asset utilization ratio =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Asset

utilization

ratio

5.94% 6.59% 7.03% 5.68% 5.56%

In 2017, DBBL has 5.94% in asset utilization and it gets increased by 0.65% in 2018 indicating

DBBL has been able to raise the average yield on assets. Similarly, in 2019 the asset utilization

rate increased and became 7.03%. However, it becomes 5.68% in 2020 and continues to decline

until it reaches 5.56% in 2021. Thus, we can say DBBL failed to make portfolio management of

assets which was supposed to minimize their risk.

Total Assets

Operating Revenue

Efficiency Ratios

Asset Utilization Ratio:

The ratio indicates how efficiently assets are utilized by the bank to generate operating revenue.

The ratio going up or down is subject to portfolio management policies, mainly mix and yield on

the bank’s assets.

Asset utilization ratio =

Dutch

Bangla Bank

Limited

2017 2018 2019 2020 2021

Asset

utilization

ratio

5.94% 6.59% 7.03% 5.68% 5.56%

In 2017, DBBL has 5.94% in asset utilization and it gets increased by 0.65% in 2018 indicating

DBBL has been able to raise the average yield on assets. Similarly, in 2019 the asset utilization

rate increased and became 7.03%. However, it becomes 5.68% in 2020 and continues to decline

until it reaches 5.56% in 2021. Thus, we can say DBBL failed to make portfolio management of

assets which was supposed to minimize their risk.

Total Assets

Operating Revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 32

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.