Business Valuation Report: Duxton Broadacre Farm Ltd IPO Analysis

VerifiedAdded on 2021/06/14

|22

|5749

|33

Report

AI Summary

This business valuation report assesses the investment potential of Duxton Broadacre Farm Ltd's IPO. It begins with an executive summary outlining the purpose of the valuation, which is to determine whether the IPO presents a viable investment opportunity. The report then delves into an analysis of the company's background, industry, and competitive strategy. It examines accounting methods, earning management, and financial performance using ratio analysis and DuPont analysis. Furthermore, the report includes financial forecasting, cost of capital estimation, and the application of various equity valuation models such as the Dividend Discount Model, Residual Earning Model, Discounted Cash Flow Model, P/B Ratio, and Ohlson model. Risk analysis is also incorporated. The conclusion suggests that the IPO could be a short-term investment opportunity based on the valuation models, while acknowledging the importance of industry and market factors.

Business Valuation

Name of the Student

Name of the University

Author Note

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The purpose of this valuation report was to investigate whether the investor should

consider the IPO opportunity of Duxton Broadacre Farm Ltd as probable investment

option or not. In order to find out whether to invest or not, the analyst has performed a

list of analysis stating from financial performance over the last three years to valuation

of stock price basis the future projections. Additionally, the analyst has also used risk

assessment models to explain associate risk with such investment.

While, the financial performance of the organisation over the last two years has shown

a balanced performance; valuation models indicates that the investor can opt this IPO

as a short term investment opportunity.

The purpose of this valuation report was to investigate whether the investor should

consider the IPO opportunity of Duxton Broadacre Farm Ltd as probable investment

option or not. In order to find out whether to invest or not, the analyst has performed a

list of analysis stating from financial performance over the last three years to valuation

of stock price basis the future projections. Additionally, the analyst has also used risk

assessment models to explain associate risk with such investment.

While, the financial performance of the organisation over the last two years has shown

a balanced performance; valuation models indicates that the investor can opt this IPO

as a short term investment opportunity.

Table of Contents

1.0 Introduction:............................................................................................................4

1.1 IPO background...................................................................................................4

1.2 Analysis of Industry............................................................................................5

1.3 Firm Competitive strategy...................................................................................6

2.0 Analysis of accounting method and earning management.......................................7

3.0 Analysis of performance using financial ratio analysis...........................................8

3.1 Ratio Analysis.....................................................................................................8

3.2 DoPont Analysis..................................................................................................9

3.3 Risk Analysis.....................................................................................................10

4.0 Financial forecasting.............................................................................................11

5.0 Estimation of cost of capital..................................................................................12

6.0 Equity valuation Model.........................................................................................12

6.1 Dividend Discount Model.................................................................................12

6.2 Residual Earning Model....................................................................................13

6.3 Discounted Cash Flow Model...........................................................................13

6.4 P/B Ratio...........................................................................................................14

6.5 Ohlson model....................................................................................................15

7.0 Conclusion............................................................................................................15

8.0 References.............................................................................................................17

Appendix.....................................................................................................................18

1.0 Introduction:............................................................................................................4

1.1 IPO background...................................................................................................4

1.2 Analysis of Industry............................................................................................5

1.3 Firm Competitive strategy...................................................................................6

2.0 Analysis of accounting method and earning management.......................................7

3.0 Analysis of performance using financial ratio analysis...........................................8

3.1 Ratio Analysis.....................................................................................................8

3.2 DoPont Analysis..................................................................................................9

3.3 Risk Analysis.....................................................................................................10

4.0 Financial forecasting.............................................................................................11

5.0 Estimation of cost of capital..................................................................................12

6.0 Equity valuation Model.........................................................................................12

6.1 Dividend Discount Model.................................................................................12

6.2 Residual Earning Model....................................................................................13

6.3 Discounted Cash Flow Model...........................................................................13

6.4 P/B Ratio...........................................................................................................14

6.5 Ohlson model....................................................................................................15

7.0 Conclusion............................................................................................................15

8.0 References.............................................................................................................17

Appendix.....................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

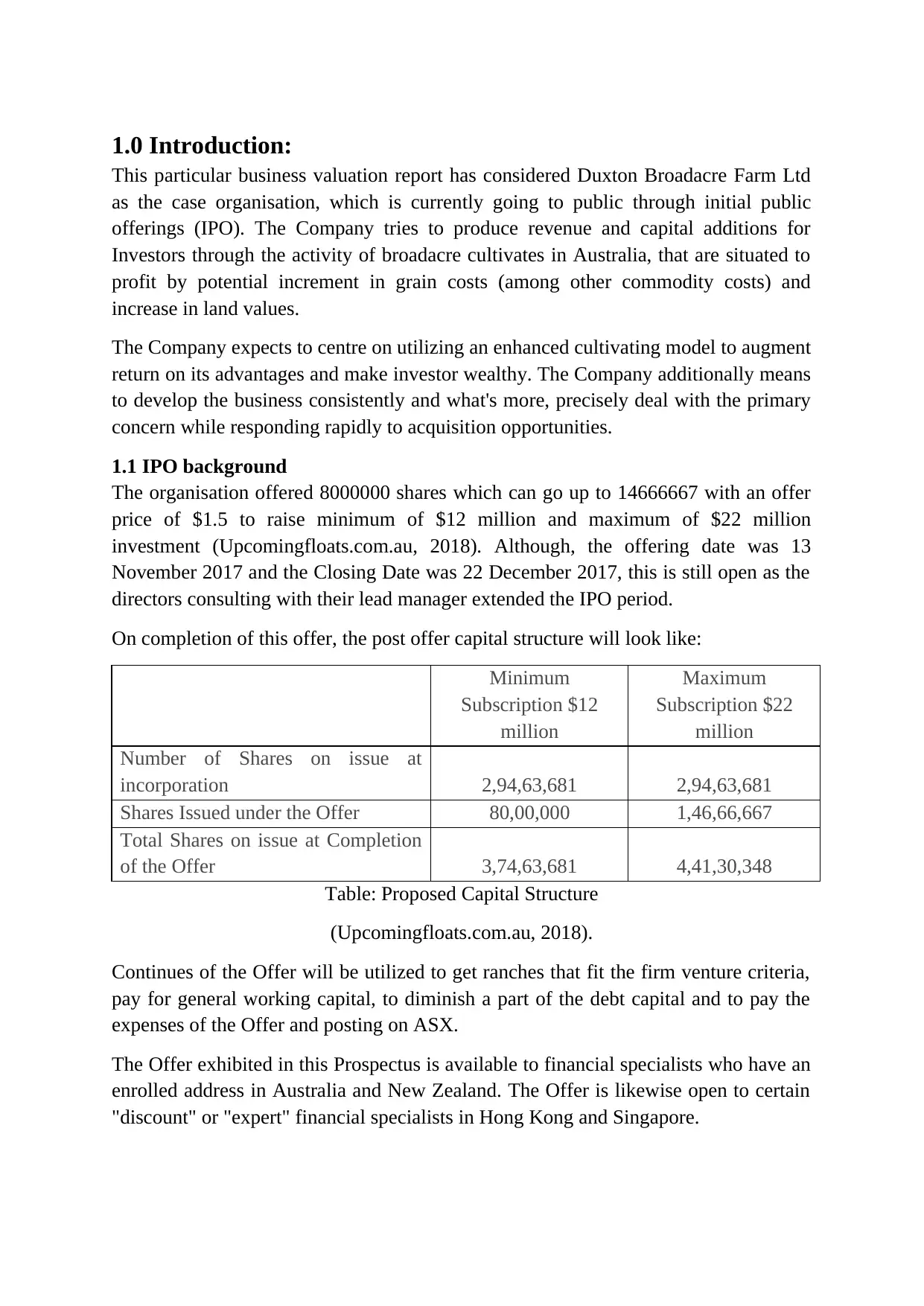

1.0 Introduction:

This particular business valuation report has considered Duxton Broadacre Farm Ltd

as the case organisation, which is currently going to public through initial public

offerings (IPO). The Company tries to produce revenue and capital additions for

Investors through the activity of broadacre cultivates in Australia, that are situated to

profit by potential increment in grain costs (among other commodity costs) and

increase in land values.

The Company expects to centre on utilizing an enhanced cultivating model to augment

return on its advantages and make investor wealthy. The Company additionally means

to develop the business consistently and what's more, precisely deal with the primary

concern while responding rapidly to acquisition opportunities.

1.1 IPO background

The organisation offered 8000000 shares which can go up to 14666667 with an offer

price of $1.5 to raise minimum of $12 million and maximum of $22 million

investment (Upcomingfloats.com.au, 2018). Although, the offering date was 13

November 2017 and the Closing Date was 22 December 2017, this is still open as the

directors consulting with their lead manager extended the IPO period.

On completion of this offer, the post offer capital structure will look like:

Minimum

Subscription $12

million

Maximum

Subscription $22

million

Number of Shares on issue at

incorporation 2,94,63,681 2,94,63,681

Shares Issued under the Offer 80,00,000 1,46,66,667

Total Shares on issue at Completion

of the Offer 3,74,63,681 4,41,30,348

Table: Proposed Capital Structure

(Upcomingfloats.com.au, 2018).

Continues of the Offer will be utilized to get ranches that fit the firm venture criteria,

pay for general working capital, to diminish a part of the debt capital and to pay the

expenses of the Offer and posting on ASX.

The Offer exhibited in this Prospectus is available to financial specialists who have an

enrolled address in Australia and New Zealand. The Offer is likewise open to certain

"discount" or "expert" financial specialists in Hong Kong and Singapore.

This particular business valuation report has considered Duxton Broadacre Farm Ltd

as the case organisation, which is currently going to public through initial public

offerings (IPO). The Company tries to produce revenue and capital additions for

Investors through the activity of broadacre cultivates in Australia, that are situated to

profit by potential increment in grain costs (among other commodity costs) and

increase in land values.

The Company expects to centre on utilizing an enhanced cultivating model to augment

return on its advantages and make investor wealthy. The Company additionally means

to develop the business consistently and what's more, precisely deal with the primary

concern while responding rapidly to acquisition opportunities.

1.1 IPO background

The organisation offered 8000000 shares which can go up to 14666667 with an offer

price of $1.5 to raise minimum of $12 million and maximum of $22 million

investment (Upcomingfloats.com.au, 2018). Although, the offering date was 13

November 2017 and the Closing Date was 22 December 2017, this is still open as the

directors consulting with their lead manager extended the IPO period.

On completion of this offer, the post offer capital structure will look like:

Minimum

Subscription $12

million

Maximum

Subscription $22

million

Number of Shares on issue at

incorporation 2,94,63,681 2,94,63,681

Shares Issued under the Offer 80,00,000 1,46,66,667

Total Shares on issue at Completion

of the Offer 3,74,63,681 4,41,30,348

Table: Proposed Capital Structure

(Upcomingfloats.com.au, 2018).

Continues of the Offer will be utilized to get ranches that fit the firm venture criteria,

pay for general working capital, to diminish a part of the debt capital and to pay the

expenses of the Offer and posting on ASX.

The Offer exhibited in this Prospectus is available to financial specialists who have an

enrolled address in Australia and New Zealand. The Offer is likewise open to certain

"discount" or "expert" financial specialists in Hong Kong and Singapore.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

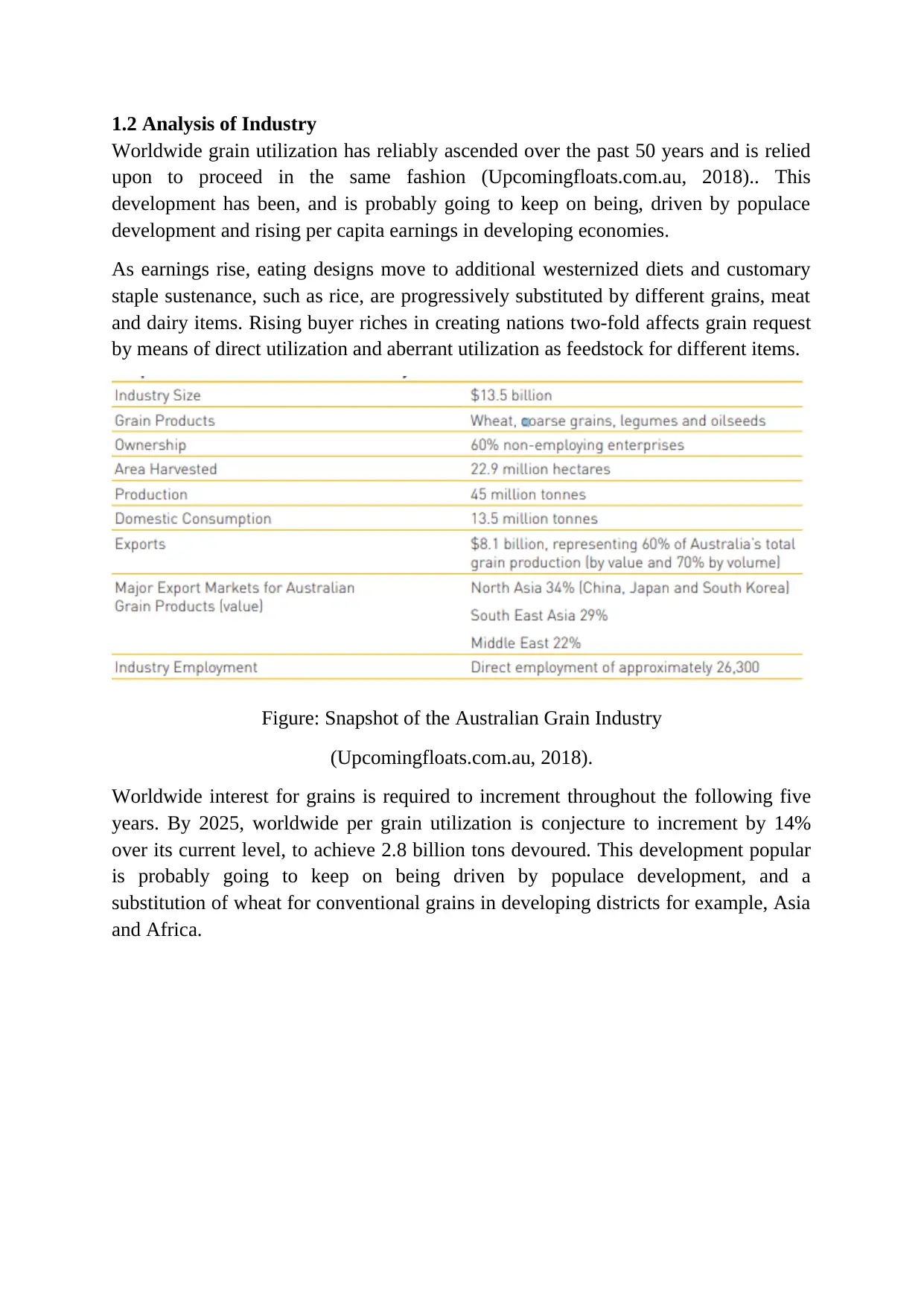

1.2 Analysis of Industry

Worldwide grain utilization has reliably ascended over the past 50 years and is relied

upon to proceed in the same fashion (Upcomingfloats.com.au, 2018).. This

development has been, and is probably going to keep on being, driven by populace

development and rising per capita earnings in developing economies.

As earnings rise, eating designs move to additional westernized diets and customary

staple sustenance, such as rice, are progressively substituted by different grains, meat

and dairy items. Rising buyer riches in creating nations two-fold affects grain request

by means of direct utilization and aberrant utilization as feedstock for different items.

Figure: Snapshot of the Australian Grain Industry

(Upcomingfloats.com.au, 2018).

Worldwide interest for grains is required to increment throughout the following five

years. By 2025, worldwide per grain utilization is conjecture to increment by 14%

over its current level, to achieve 2.8 billion tons devoured. This development popular

is probably going to keep on being driven by populace development, and a

substitution of wheat for conventional grains in developing districts for example, Asia

and Africa.

Worldwide grain utilization has reliably ascended over the past 50 years and is relied

upon to proceed in the same fashion (Upcomingfloats.com.au, 2018).. This

development has been, and is probably going to keep on being, driven by populace

development and rising per capita earnings in developing economies.

As earnings rise, eating designs move to additional westernized diets and customary

staple sustenance, such as rice, are progressively substituted by different grains, meat

and dairy items. Rising buyer riches in creating nations two-fold affects grain request

by means of direct utilization and aberrant utilization as feedstock for different items.

Figure: Snapshot of the Australian Grain Industry

(Upcomingfloats.com.au, 2018).

Worldwide interest for grains is required to increment throughout the following five

years. By 2025, worldwide per grain utilization is conjecture to increment by 14%

over its current level, to achieve 2.8 billion tons devoured. This development popular

is probably going to keep on being driven by populace development, and a

substitution of wheat for conventional grains in developing districts for example, Asia

and Africa.

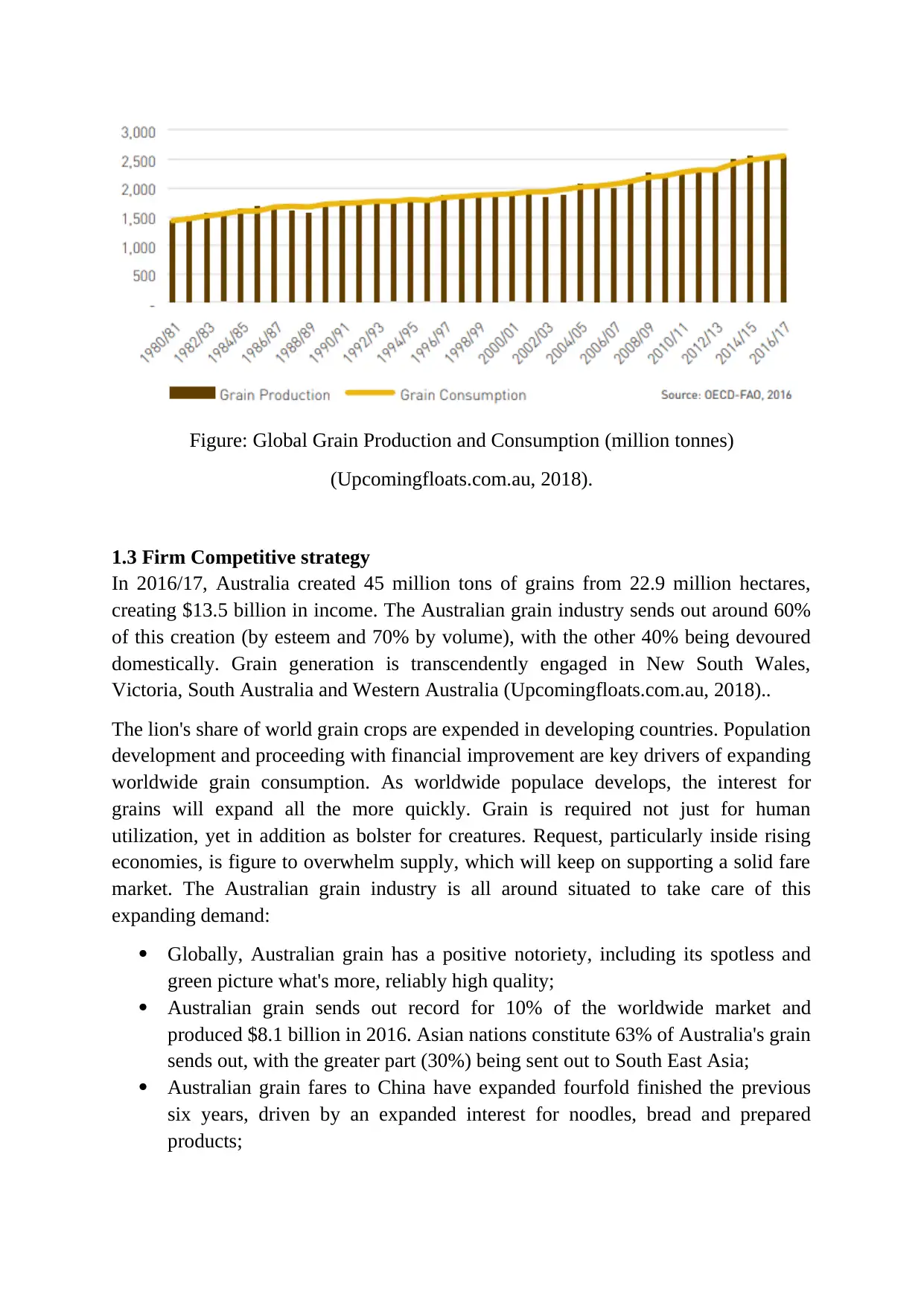

Figure: Global Grain Production and Consumption (million tonnes)

(Upcomingfloats.com.au, 2018).

1.3 Firm Competitive strategy

In 2016/17, Australia created 45 million tons of grains from 22.9 million hectares,

creating $13.5 billion in income. The Australian grain industry sends out around 60%

of this creation (by esteem and 70% by volume), with the other 40% being devoured

domestically. Grain generation is transcendently engaged in New South Wales,

Victoria, South Australia and Western Australia (Upcomingfloats.com.au, 2018)..

The lion's share of world grain crops are expended in developing countries. Population

development and proceeding with financial improvement are key drivers of expanding

worldwide grain consumption. As worldwide populace develops, the interest for

grains will expand all the more quickly. Grain is required not just for human

utilization, yet in addition as bolster for creatures. Request, particularly inside rising

economies, is figure to overwhelm supply, which will keep on supporting a solid fare

market. The Australian grain industry is all around situated to take care of this

expanding demand:

Globally, Australian grain has a positive notoriety, including its spotless and

green picture what's more, reliably high quality;

Australian grain sends out record for 10% of the worldwide market and

produced $8.1 billion in 2016. Asian nations constitute 63% of Australia's grain

sends out, with the greater part (30%) being sent out to South East Asia;

Australian grain fares to China have expanded fourfold finished the previous

six years, driven by an expanded interest for noodles, bread and prepared

products;

(Upcomingfloats.com.au, 2018).

1.3 Firm Competitive strategy

In 2016/17, Australia created 45 million tons of grains from 22.9 million hectares,

creating $13.5 billion in income. The Australian grain industry sends out around 60%

of this creation (by esteem and 70% by volume), with the other 40% being devoured

domestically. Grain generation is transcendently engaged in New South Wales,

Victoria, South Australia and Western Australia (Upcomingfloats.com.au, 2018)..

The lion's share of world grain crops are expended in developing countries. Population

development and proceeding with financial improvement are key drivers of expanding

worldwide grain consumption. As worldwide populace develops, the interest for

grains will expand all the more quickly. Grain is required not just for human

utilization, yet in addition as bolster for creatures. Request, particularly inside rising

economies, is figure to overwhelm supply, which will keep on supporting a solid fare

market. The Australian grain industry is all around situated to take care of this

expanding demand:

Globally, Australian grain has a positive notoriety, including its spotless and

green picture what's more, reliably high quality;

Australian grain sends out record for 10% of the worldwide market and

produced $8.1 billion in 2016. Asian nations constitute 63% of Australia's grain

sends out, with the greater part (30%) being sent out to South East Asia;

Australian grain fares to China have expanded fourfold finished the previous

six years, driven by an expanded interest for noodles, bread and prepared

products;

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Australian wheat makes up 58%, 26% and 56% of Indonesia, South Korea and

Vietnam's aggregate wheat imports, individually;

Over the previous decade, Australian grain sends out for domesticated animals

bolster and malting has more than multiplied from 3.1 Mt to 7 Mt.29 This

development in request has been driven overwhelmingly by the developing

Chinese sustenance and refreshment showcase, which expends 30% of

Australia's aggregate grain production (Upcomingfloats.com.au, 2018).

As the Asian area keeps on developing, interest for grains will keep on rise.

2.0 Analysis of accounting method and earning management

The Company is a revenue driven substance for money related detailing purposes

under Australian Accounting Standards. Material bookkeeping arrangements

embraced in the planning of these pro forma financial statements are exhibited

underneath and have been reliably connected unless expressed generally.

The money related data exhibited in the Plan is exhibited in a contracted shape

furthermore, does not contain the majority of the divulgences that are normally given

in a yearly report arranged as per the Corporations Act.

During the IPO, the organisation has made creation forecasts. However, any estimates

or forward looking explanations are expectations just and are liable to different natural

hazard variables and vulnerabilities that could make the Company's genuine outcomes

vary substantially from the outcomes communicated or foreseen in these figures or

proclamations (Reilly, 2017).

Such gauges or proclamations are not ensures of future execution and include known

and obscure dangers, vulnerabilities, presumptions what's more, other vital elements, a

large number of which are outside the ability to control of the Company, its Directors

what's more, administration (Trugman, 2016). Gauges and forward looking

articulations ought to along these lines be perused in conjunction with, and are

qualified by reference to, the discourse of the Pro Forma Historical Financial Data.

The Company presents financial specialists with the opportunity to get to the

Australian grain industry by means of an arrangement of expanded dry land and

watered broadacre ranches. Worldwide grain utilization has reliably ascended in the

course of recent years and is figure to increment 14% over its present level by 2025,

driven by populace development and rising per capita wages in developing economies

(Batkovskiy et al. 2016). As wages rise, eating designs move to more westernize eats

less, and customary staple nourishments, for example, rice, are progressively

substituted by different grains, meat and dairy items. Rising shopper riches in creating

nations twofoldly affects grain request by means of coordinate utilization and

backhanded utilization as feedstock for different items (Patel and Prajapati, 2018).

Vietnam's aggregate wheat imports, individually;

Over the previous decade, Australian grain sends out for domesticated animals

bolster and malting has more than multiplied from 3.1 Mt to 7 Mt.29 This

development in request has been driven overwhelmingly by the developing

Chinese sustenance and refreshment showcase, which expends 30% of

Australia's aggregate grain production (Upcomingfloats.com.au, 2018).

As the Asian area keeps on developing, interest for grains will keep on rise.

2.0 Analysis of accounting method and earning management

The Company is a revenue driven substance for money related detailing purposes

under Australian Accounting Standards. Material bookkeeping arrangements

embraced in the planning of these pro forma financial statements are exhibited

underneath and have been reliably connected unless expressed generally.

The money related data exhibited in the Plan is exhibited in a contracted shape

furthermore, does not contain the majority of the divulgences that are normally given

in a yearly report arranged as per the Corporations Act.

During the IPO, the organisation has made creation forecasts. However, any estimates

or forward looking explanations are expectations just and are liable to different natural

hazard variables and vulnerabilities that could make the Company's genuine outcomes

vary substantially from the outcomes communicated or foreseen in these figures or

proclamations (Reilly, 2017).

Such gauges or proclamations are not ensures of future execution and include known

and obscure dangers, vulnerabilities, presumptions what's more, other vital elements, a

large number of which are outside the ability to control of the Company, its Directors

what's more, administration (Trugman, 2016). Gauges and forward looking

articulations ought to along these lines be perused in conjunction with, and are

qualified by reference to, the discourse of the Pro Forma Historical Financial Data.

The Company presents financial specialists with the opportunity to get to the

Australian grain industry by means of an arrangement of expanded dry land and

watered broadacre ranches. Worldwide grain utilization has reliably ascended in the

course of recent years and is figure to increment 14% over its present level by 2025,

driven by populace development and rising per capita wages in developing economies

(Batkovskiy et al. 2016). As wages rise, eating designs move to more westernize eats

less, and customary staple nourishments, for example, rice, are progressively

substituted by different grains, meat and dairy items. Rising shopper riches in creating

nations twofoldly affects grain request by means of coordinate utilization and

backhanded utilization as feedstock for different items (Patel and Prajapati, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Request, particularly inside rising economies, is gauge to overwhelm supply, which

will keep on supporting a solid send out market. The Australian grain industry is very

much situated to take care of this expanding demand.

The Company looks to gain by the expanding interest for grain as an imperative

contribution to a range of staple sustenance items and the domesticated animals

industry (Cong, 2017). The Company's goal is to grow its current interests into an

expanded arrangement of high caliber, productive broadacre ranches. The Company

expects to accomplish this target through the procurement and collection of land rich

packages of properties that have clear degree for advancement to enhance operational

efficiencies and deliver a various scope of items (counting as an aide domesticated

animals and cotton) to diminish chance. The Company's venture postulation is driven

by long haul development in worldwide grain request meaning critical working edges

and enhanced farmland esteems after some time, furnishing investors with both

progressing yearly operational yield and longer-term capital development.

3.0 Analysis of performance using financial ratio analysis

While analysing performance of any organisation, one have keep an eye over various

financial ratios in attempting to investigate an organization's general execution. The

proportions are helpful in various circumstances when the organization's money

related condition, gainfulness, and proficiency in utilizing its benefits should be

comprehended (Chiang, 2016).

Utilizing the ratio analysis can help to reveal insight into such imperative issues as the

organization's capacity to meet its commitments, its capital structure, how well it

utilizes its assets to produce pay, and how gainful it is (Manimala and Wasdani,

2015).

At the point when utilized appropriately, the budgetary proportions can be a helpful

device in chosen business valuation (Carter, Bizequity Llc, 2014). The undeniable

advantage is that they can enable the analyst to recognize the organization's qualities

and shortcomings and contrast it with its industry peers.

Surveying very much chosen proportions can enable in valuation to work in various

ways. Maybe the most valuable territory is the choice of fitting valuation products that

provide assistance in building up the organization's financial strategy in connection to

its money related execution measures (Titman et al. 2017). Valuation products are

generally gotten from equivalent business deals, influencing contender organizations.

Thus, it is necessary that one have a factual scope of products to look over.

3.1 Ratio Analysis

Considering the IPO of Duxton Broadacre Farm Ltd, when look into the average

collection periods, it has seen that it was 22.74 days during year end June 2015. It

will keep on supporting a solid send out market. The Australian grain industry is very

much situated to take care of this expanding demand.

The Company looks to gain by the expanding interest for grain as an imperative

contribution to a range of staple sustenance items and the domesticated animals

industry (Cong, 2017). The Company's goal is to grow its current interests into an

expanded arrangement of high caliber, productive broadacre ranches. The Company

expects to accomplish this target through the procurement and collection of land rich

packages of properties that have clear degree for advancement to enhance operational

efficiencies and deliver a various scope of items (counting as an aide domesticated

animals and cotton) to diminish chance. The Company's venture postulation is driven

by long haul development in worldwide grain request meaning critical working edges

and enhanced farmland esteems after some time, furnishing investors with both

progressing yearly operational yield and longer-term capital development.

3.0 Analysis of performance using financial ratio analysis

While analysing performance of any organisation, one have keep an eye over various

financial ratios in attempting to investigate an organization's general execution. The

proportions are helpful in various circumstances when the organization's money

related condition, gainfulness, and proficiency in utilizing its benefits should be

comprehended (Chiang, 2016).

Utilizing the ratio analysis can help to reveal insight into such imperative issues as the

organization's capacity to meet its commitments, its capital structure, how well it

utilizes its assets to produce pay, and how gainful it is (Manimala and Wasdani,

2015).

At the point when utilized appropriately, the budgetary proportions can be a helpful

device in chosen business valuation (Carter, Bizequity Llc, 2014). The undeniable

advantage is that they can enable the analyst to recognize the organization's qualities

and shortcomings and contrast it with its industry peers.

Surveying very much chosen proportions can enable in valuation to work in various

ways. Maybe the most valuable territory is the choice of fitting valuation products that

provide assistance in building up the organization's financial strategy in connection to

its money related execution measures (Titman et al. 2017). Valuation products are

generally gotten from equivalent business deals, influencing contender organizations.

Thus, it is necessary that one have a factual scope of products to look over.

3.1 Ratio Analysis

Considering the IPO of Duxton Broadacre Farm Ltd, when look into the average

collection periods, it has seen that it was 22.74 days during year end June 2015. It

reduced to 17.36 days in June 2016 and increased to 51.31 days in June 2017. It has

seen that average collection period is of noteworthy significance when utilized as a

part of conjunction with liquidity proportions.

A short collection period implies provoke gathering and better administration of

receivables. A more extended collection period may contrarily influence the transient

obligation paying capacity of the business according to investigators.

Regardless of whether a collection period is great or awful, relies upon the credit

terms permitted by the organization. In this case, as the normal collection time is 50

days and the organization's credit terms are 60 days; the normal collection time of 50

days would be viewed as great (Ahmed and Dina, 2018).

Similarly, the inventory turnover ratio, indicates how soon the organisation is able to

convert its inventory amount into dollar amount. The given case has shown that

Duxton Broadacre Farm Ltd took less than 100 days to convert their inventory

amount, which is a great sign for operation efficiency.

The profitability position of the company has shown negative figure during most

recent audited time frame. However, previous two years have experienced a

significant profitability position. Even though, this negative figure is a cause of

concern, it can be said that the organisation has the sufficient capability to control this

shortcoming. The liquidity position of the organisation, over the last three years are

supporting this view. It has also seen that such negative figure is there may be because

of the review for the IPO purpose.

Now, if the solvency ratios are taken into account, then it can be said that the

organisation till date maintained a balanced capital structure and thus the solvency

aspect remained in a good position.

[Ratio analyses are shown in appendix section]

3.2 DoPont Analysis

In addition to ratio analysis, the analyst has also performed DoPont Analysis. This

model was produced to examine ROE and the impacts distinctive business execution

measures have on this proportion. So financial specialists are not searching for huge or

little yield numbers from this model. Rather, they are hoping to break down what is

causing the present ROE. For instance, the speculators will be unsatisfied with a low

ROE [shown in appendix section]]. Therefore, the administration can utilize this

equation to pinpoint the issue territory whether it is a lower overall revenue, resource

turnover, or poor money related utilizing (Herawati et al. 2017).

Once the issue zone is discovered, administration can endeavour to redress it or

address it with investors. Some typical activities bring down ROE normally and are

seen that average collection period is of noteworthy significance when utilized as a

part of conjunction with liquidity proportions.

A short collection period implies provoke gathering and better administration of

receivables. A more extended collection period may contrarily influence the transient

obligation paying capacity of the business according to investigators.

Regardless of whether a collection period is great or awful, relies upon the credit

terms permitted by the organization. In this case, as the normal collection time is 50

days and the organization's credit terms are 60 days; the normal collection time of 50

days would be viewed as great (Ahmed and Dina, 2018).

Similarly, the inventory turnover ratio, indicates how soon the organisation is able to

convert its inventory amount into dollar amount. The given case has shown that

Duxton Broadacre Farm Ltd took less than 100 days to convert their inventory

amount, which is a great sign for operation efficiency.

The profitability position of the company has shown negative figure during most

recent audited time frame. However, previous two years have experienced a

significant profitability position. Even though, this negative figure is a cause of

concern, it can be said that the organisation has the sufficient capability to control this

shortcoming. The liquidity position of the organisation, over the last three years are

supporting this view. It has also seen that such negative figure is there may be because

of the review for the IPO purpose.

Now, if the solvency ratios are taken into account, then it can be said that the

organisation till date maintained a balanced capital structure and thus the solvency

aspect remained in a good position.

[Ratio analyses are shown in appendix section]

3.2 DoPont Analysis

In addition to ratio analysis, the analyst has also performed DoPont Analysis. This

model was produced to examine ROE and the impacts distinctive business execution

measures have on this proportion. So financial specialists are not searching for huge or

little yield numbers from this model. Rather, they are hoping to break down what is

causing the present ROE. For instance, the speculators will be unsatisfied with a low

ROE [shown in appendix section]]. Therefore, the administration can utilize this

equation to pinpoint the issue territory whether it is a lower overall revenue, resource

turnover, or poor money related utilizing (Herawati et al. 2017).

Once the issue zone is discovered, administration can endeavour to redress it or

address it with investors. Some typical activities bring down ROE normally and are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

not an explanation behind financial specialists to be frightened. For example,

quickened deterioration misleadingly brings down ROE in the first place time frames.

This paper passage can be called attention to with the Dupont examination and

shouldn't influence a financial specialist's sentiment of the organization.

3.3 Risk Analysis

The Altman Z Score is utilized to foresee the probability that a business will go

bankrupt inside the following two years. The equation depends on data found in the

wage explanation and monetary record of an association; thusly, it can be promptly

gotten from normally accessible data (Chiang, 2016). Given the simplicity with which

the required data can be discovered, the Z Score is a valuable metric for an outcast

who approaches an organization's budgetary explanations. In its unique frame, the Z

score recipe is as per the following:

Z = 1.2A x 1.4B x 3.3C x 0.6D x 0.99E

The letters in the recipe assign the accompanying measures:

A = Working capital/Total resources

B = Retained income/Total resources

C = Earnings before premium and duties/Total resources

D = Market estimation of value/Book estimation of aggregate liabilities

E = Sales/Total resources

A Z score of more prominent than 2.99 implies that the element being estimated is

sheltered from liquidation. A score of under 1.81 implies that a business is at

impressive danger of going into insolvency, while scores in the middle of ought to be

viewed as a warning for conceivable issues (Cong, 2017). The model has ended up

being sensibly precise in anticipating the future of elements under examination. Here,

the value of z is above 3, which indicates that there is no immediate risk involve in

operation of the organisation.

quickened deterioration misleadingly brings down ROE in the first place time frames.

This paper passage can be called attention to with the Dupont examination and

shouldn't influence a financial specialist's sentiment of the organization.

3.3 Risk Analysis

The Altman Z Score is utilized to foresee the probability that a business will go

bankrupt inside the following two years. The equation depends on data found in the

wage explanation and monetary record of an association; thusly, it can be promptly

gotten from normally accessible data (Chiang, 2016). Given the simplicity with which

the required data can be discovered, the Z Score is a valuable metric for an outcast

who approaches an organization's budgetary explanations. In its unique frame, the Z

score recipe is as per the following:

Z = 1.2A x 1.4B x 3.3C x 0.6D x 0.99E

The letters in the recipe assign the accompanying measures:

A = Working capital/Total resources

B = Retained income/Total resources

C = Earnings before premium and duties/Total resources

D = Market estimation of value/Book estimation of aggregate liabilities

E = Sales/Total resources

A Z score of more prominent than 2.99 implies that the element being estimated is

sheltered from liquidation. A score of under 1.81 implies that a business is at

impressive danger of going into insolvency, while scores in the middle of ought to be

viewed as a warning for conceivable issues (Cong, 2017). The model has ended up

being sensibly precise in anticipating the future of elements under examination. Here,

the value of z is above 3, which indicates that there is no immediate risk involve in

operation of the organisation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

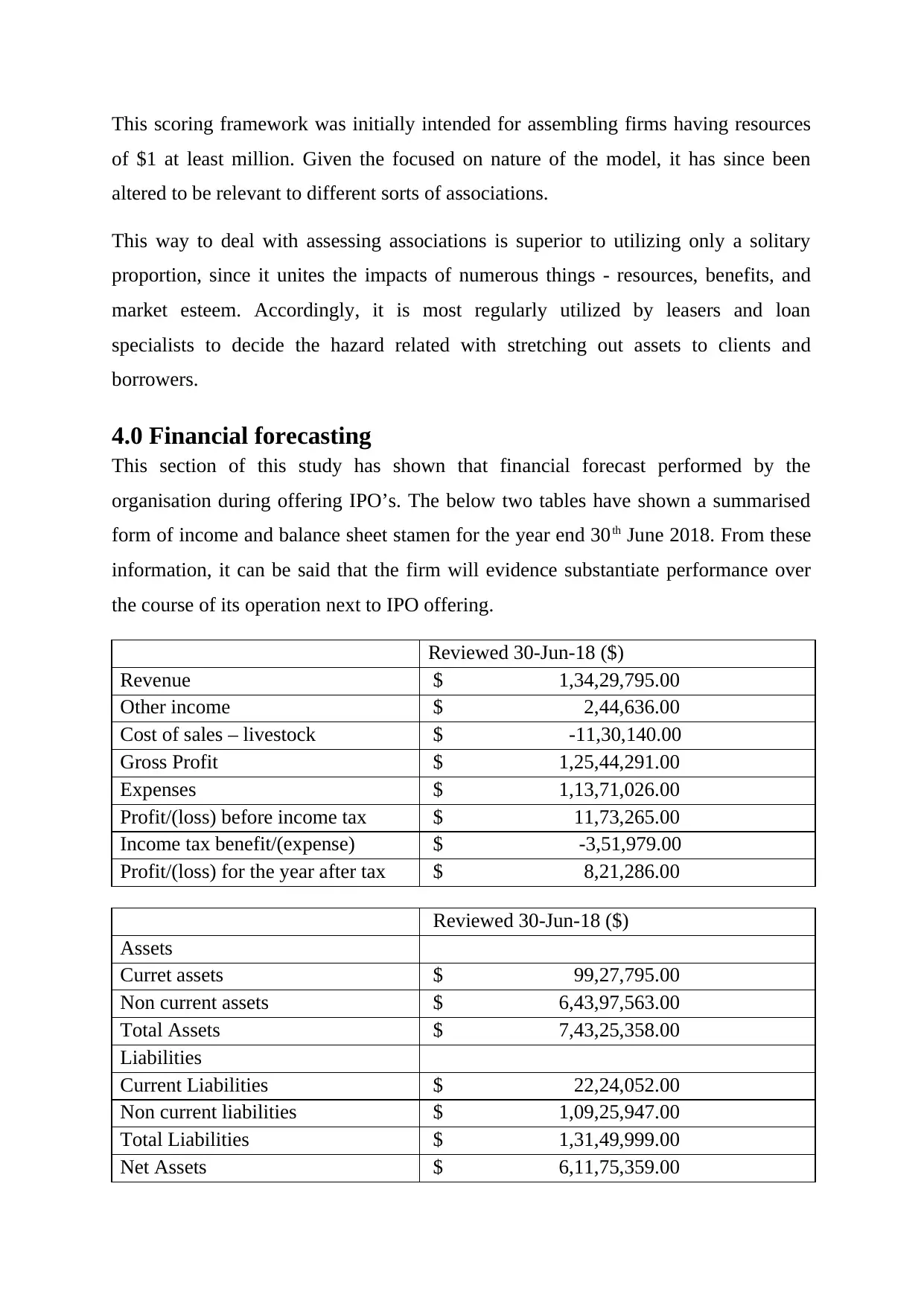

This scoring framework was initially intended for assembling firms having resources

of $1 at least million. Given the focused on nature of the model, it has since been

altered to be relevant to different sorts of associations.

This way to deal with assessing associations is superior to utilizing only a solitary

proportion, since it unites the impacts of numerous things - resources, benefits, and

market esteem. Accordingly, it is most regularly utilized by leasers and loan

specialists to decide the hazard related with stretching out assets to clients and

borrowers.

4.0 Financial forecasting

This section of this study has shown that financial forecast performed by the

organisation during offering IPO’s. The below two tables have shown a summarised

form of income and balance sheet stamen for the year end 30th June 2018. From these

information, it can be said that the firm will evidence substantiate performance over

the course of its operation next to IPO offering.

Reviewed 30-Jun-18 ($)

Revenue $ 1,34,29,795.00

Other income $ 2,44,636.00

Cost of sales – livestock $ -11,30,140.00

Gross Profit $ 1,25,44,291.00

Expenses $ 1,13,71,026.00

Profit/(loss) before income tax $ 11,73,265.00

Income tax benefit/(expense) $ -3,51,979.00

Profit/(loss) for the year after tax $ 8,21,286.00

Reviewed 30-Jun-18 ($)

Assets

Curret assets $ 99,27,795.00

Non current assets $ 6,43,97,563.00

Total Assets $ 7,43,25,358.00

Liabilities

Current Liabilities $ 22,24,052.00

Non current liabilities $ 1,09,25,947.00

Total Liabilities $ 1,31,49,999.00

Net Assets $ 6,11,75,359.00

of $1 at least million. Given the focused on nature of the model, it has since been

altered to be relevant to different sorts of associations.

This way to deal with assessing associations is superior to utilizing only a solitary

proportion, since it unites the impacts of numerous things - resources, benefits, and

market esteem. Accordingly, it is most regularly utilized by leasers and loan

specialists to decide the hazard related with stretching out assets to clients and

borrowers.

4.0 Financial forecasting

This section of this study has shown that financial forecast performed by the

organisation during offering IPO’s. The below two tables have shown a summarised

form of income and balance sheet stamen for the year end 30th June 2018. From these

information, it can be said that the firm will evidence substantiate performance over

the course of its operation next to IPO offering.

Reviewed 30-Jun-18 ($)

Revenue $ 1,34,29,795.00

Other income $ 2,44,636.00

Cost of sales – livestock $ -11,30,140.00

Gross Profit $ 1,25,44,291.00

Expenses $ 1,13,71,026.00

Profit/(loss) before income tax $ 11,73,265.00

Income tax benefit/(expense) $ -3,51,979.00

Profit/(loss) for the year after tax $ 8,21,286.00

Reviewed 30-Jun-18 ($)

Assets

Curret assets $ 99,27,795.00

Non current assets $ 6,43,97,563.00

Total Assets $ 7,43,25,358.00

Liabilities

Current Liabilities $ 22,24,052.00

Non current liabilities $ 1,09,25,947.00

Total Liabilities $ 1,31,49,999.00

Net Assets $ 6,11,75,359.00

Equity $ 6,11,75,359.00

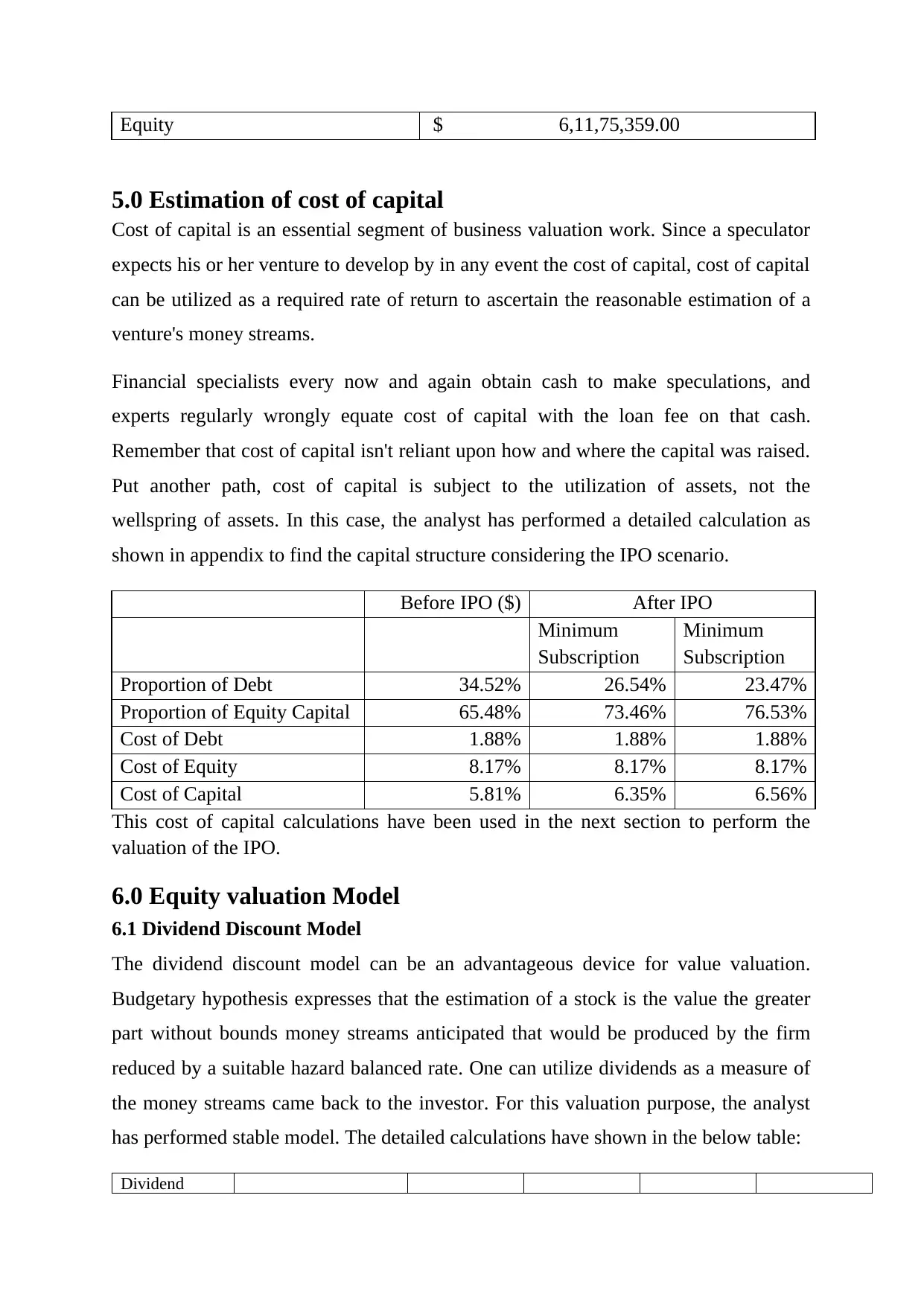

5.0 Estimation of cost of capital

Cost of capital is an essential segment of business valuation work. Since a speculator

expects his or her venture to develop by in any event the cost of capital, cost of capital

can be utilized as a required rate of return to ascertain the reasonable estimation of a

venture's money streams.

Financial specialists every now and again obtain cash to make speculations, and

experts regularly wrongly equate cost of capital with the loan fee on that cash.

Remember that cost of capital isn't reliant upon how and where the capital was raised.

Put another path, cost of capital is subject to the utilization of assets, not the

wellspring of assets. In this case, the analyst has performed a detailed calculation as

shown in appendix to find the capital structure considering the IPO scenario.

Before IPO ($) After IPO

Minimum

Subscription

Minimum

Subscription

Proportion of Debt 34.52% 26.54% 23.47%

Proportion of Equity Capital 65.48% 73.46% 76.53%

Cost of Debt 1.88% 1.88% 1.88%

Cost of Equity 8.17% 8.17% 8.17%

Cost of Capital 5.81% 6.35% 6.56%

This cost of capital calculations have been used in the next section to perform the

valuation of the IPO.

6.0 Equity valuation Model

6.1 Dividend Discount Model

The dividend discount model can be an advantageous device for value valuation.

Budgetary hypothesis expresses that the estimation of a stock is the value the greater

part without bounds money streams anticipated that would be produced by the firm

reduced by a suitable hazard balanced rate. One can utilize dividends as a measure of

the money streams came back to the investor. For this valuation purpose, the analyst

has performed stable model. The detailed calculations have shown in the below table:

Dividend

5.0 Estimation of cost of capital

Cost of capital is an essential segment of business valuation work. Since a speculator

expects his or her venture to develop by in any event the cost of capital, cost of capital

can be utilized as a required rate of return to ascertain the reasonable estimation of a

venture's money streams.

Financial specialists every now and again obtain cash to make speculations, and

experts regularly wrongly equate cost of capital with the loan fee on that cash.

Remember that cost of capital isn't reliant upon how and where the capital was raised.

Put another path, cost of capital is subject to the utilization of assets, not the

wellspring of assets. In this case, the analyst has performed a detailed calculation as

shown in appendix to find the capital structure considering the IPO scenario.

Before IPO ($) After IPO

Minimum

Subscription

Minimum

Subscription

Proportion of Debt 34.52% 26.54% 23.47%

Proportion of Equity Capital 65.48% 73.46% 76.53%

Cost of Debt 1.88% 1.88% 1.88%

Cost of Equity 8.17% 8.17% 8.17%

Cost of Capital 5.81% 6.35% 6.56%

This cost of capital calculations have been used in the next section to perform the

valuation of the IPO.

6.0 Equity valuation Model

6.1 Dividend Discount Model

The dividend discount model can be an advantageous device for value valuation.

Budgetary hypothesis expresses that the estimation of a stock is the value the greater

part without bounds money streams anticipated that would be produced by the firm

reduced by a suitable hazard balanced rate. One can utilize dividends as a measure of

the money streams came back to the investor. For this valuation purpose, the analyst

has performed stable model. The detailed calculations have shown in the below table:

Dividend

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.