Dysonica Plc: Cost Management, Budgeting, and Performance Evaluation

VerifiedAdded on 2023/06/11

|20

|4441

|362

Case Study

AI Summary

This case study examines Dysonica Plc's financial operations, focusing on cost analysis, budgeting, and performance evaluation. It begins by defining various cost types, including variable, fixed, and semi-variable costs, and explores costing methods like absorption, marginal, and activity-based costing. The study proposes cost-cutting strategies for the company and develops a 12-month budget plan until April 30, 2023. Finally, it evaluates Dysonica Plc's performance based on forecasts and budgets, considering its competitive landscape and the importance of effective financial management for sustainable success. The analysis emphasizes the need for strategic cost control and revenue optimization to maintain a competitive edge.

CASE STUDY

DYSONICA Plc LO1

LO2 LO3 LO4

DYSONICA Plc LO1

LO2 LO3 LO4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................4

Describes the cost regarding the nature of the business..............................................................4

TASK 2............................................................................................................................................6

Provide the company your ideas for a cost-cutting approach......................................................6

TASK 3............................................................................................................................................8

The creation of a 12-month plan and budget for the company until 30 April 2023....................8

TASK 4..........................................................................................................................................15

On the basis of the facts and figures in the forecasts and budgets, evaluate and analyze the

performance of Dysonica Plc.....................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION...........................................................................................................................3

Task 1...............................................................................................................................................4

Describes the cost regarding the nature of the business..............................................................4

TASK 2............................................................................................................................................6

Provide the company your ideas for a cost-cutting approach......................................................6

TASK 3............................................................................................................................................8

The creation of a 12-month plan and budget for the company until 30 April 2023....................8

TASK 4..........................................................................................................................................15

On the basis of the facts and figures in the forecasts and budgets, evaluate and analyze the

performance of Dysonica Plc.....................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................18

INTRODUCTION

The seamless operation of the company’s activities depends on finance. It aids a range of

enterprises in securing funding from various sources. It serves to get goods, property, and raw

resources for the business. A business that begins out with minimal capital will continually need

more money to run its activities. The foundation of any firm is finance. Without even a strong

financial base, success is all but unattainable. Financial management refers to the funds and

credits utilized by a company. Major corporations also oversee a wide range of procedures to

produce this income in order to satisfy these requirements. In order to build a financially sound

strategy for the efficient operation of an organisation, the analysis of the financial demands and

opportunities can be bridge on a daily basis. In this research, the research project of Dysonica Plc

is examined. It consists of four tasks, the first of which includes the cost divisions of a firm and

how it distinguishes them. The next duty focuses on management recommendations that will

assist managers in lowering expenditures and costs. The Dysonica Plc's cash flow predictions

through April 30, 2023 are covered in the third step. The last task examines the company's

successes and achievements as well as its performance within that particular sector (Sandra and

Kim, 2022). This decision will be made by considering the anticipated amounts of Dysonica

Plc's cash flow.

Each firm must choose the financing from its preferred sources. A firm like Dysonica Plc.

operates in several nations and contends with strong competition. Therefore, it needs to manage

all of its activities extremely effectively if it would like to compete including its rivals. These

businesses will employ a variety of methods for cost-cutting and several mechanisms to boost

sales operational income. The many cost elements, such as variable costs, overhead expenses,

and marginal costs, are also distinct in addition to this. This study has also provided a

comprehensive explanation of how to forecast a company concern's expected investment

capacity and potential to satisfy its impending wants and demands. The two most effective

methods for Dysonica Plc to reduce needless costs and keep track of costs related to various

types of tasks carried out in various divisions are marginal costing and activity-based costing.

The seamless operation of the company’s activities depends on finance. It aids a range of

enterprises in securing funding from various sources. It serves to get goods, property, and raw

resources for the business. A business that begins out with minimal capital will continually need

more money to run its activities. The foundation of any firm is finance. Without even a strong

financial base, success is all but unattainable. Financial management refers to the funds and

credits utilized by a company. Major corporations also oversee a wide range of procedures to

produce this income in order to satisfy these requirements. In order to build a financially sound

strategy for the efficient operation of an organisation, the analysis of the financial demands and

opportunities can be bridge on a daily basis. In this research, the research project of Dysonica Plc

is examined. It consists of four tasks, the first of which includes the cost divisions of a firm and

how it distinguishes them. The next duty focuses on management recommendations that will

assist managers in lowering expenditures and costs. The Dysonica Plc's cash flow predictions

through April 30, 2023 are covered in the third step. The last task examines the company's

successes and achievements as well as its performance within that particular sector (Sandra and

Kim, 2022). This decision will be made by considering the anticipated amounts of Dysonica

Plc's cash flow.

Each firm must choose the financing from its preferred sources. A firm like Dysonica Plc.

operates in several nations and contends with strong competition. Therefore, it needs to manage

all of its activities extremely effectively if it would like to compete including its rivals. These

businesses will employ a variety of methods for cost-cutting and several mechanisms to boost

sales operational income. The many cost elements, such as variable costs, overhead expenses,

and marginal costs, are also distinct in addition to this. This study has also provided a

comprehensive explanation of how to forecast a company concern's expected investment

capacity and potential to satisfy its impending wants and demands. The two most effective

methods for Dysonica Plc to reduce needless costs and keep track of costs related to various

types of tasks carried out in various divisions are marginal costing and activity-based costing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Task 1

Describes the cost regarding the nature of the business.

Cost is a concept used throughout the production and distribution of both goods and

services. Cost is crucial at every phase of the manufacturing process, from procuring raw

materials to producing a firm's final items. In essence, cost is the sum of money used to offset

production-related costs. The costs which are relevant for any type of organization need to be

characterised and defined, so as to effectively manage the costs related to various items used in

the course of business. The definition of cost may differ from the point of view of different

individuals, such as the seller may view the cost of producing and manufacturing a product as

costs to the company, however for the buyer, the amount which has been paid towards availing

the services or products is often called the price. This amount or the price, is the unified

monetary value of the activities which the seller executed to bring the product or service to its

current condition and not to mention, the cost of the commodity itself. Furthermore, the costs

should include the expenses which directly or indirectly form part of the overall amount of the

product or service sold or to be sold. There are numerous different sorts of costs that the business

must deal with, but the two that pose the most challenges to the creation of products are indirect

costs and fixed costs.

Variable costs: These costs are those that are significantly influenced by a firm's sales

and productivity, or they are those that gauge how many products a business is producing

and marketing. A company's variable costs will rise or fall in direct proportion to its sale

and manufacturing of commodities, therefore indicates that things are simultaneous to

one another. The cost of transportation, raw materials, plastic cards, and other expenses

are all variables. Also, there will be deviations in the variable costs of the products across

the profits and may need to be allocated among the products, if the same are incurred for

goods or services sold through multiple branches. The variable costs are not of one kind,

they may be related to different items and accordingly their nature may vary, such as the

raw material and labour costs, commissions provided to the salesperson, utilities directly

affecting the costs of goods and services, shipping or freight charges incurred at the time

of transportation of the commodity by way of cargo. All of such costs are expenses to the

company and need to be allocated systematically.

Describes the cost regarding the nature of the business.

Cost is a concept used throughout the production and distribution of both goods and

services. Cost is crucial at every phase of the manufacturing process, from procuring raw

materials to producing a firm's final items. In essence, cost is the sum of money used to offset

production-related costs. The costs which are relevant for any type of organization need to be

characterised and defined, so as to effectively manage the costs related to various items used in

the course of business. The definition of cost may differ from the point of view of different

individuals, such as the seller may view the cost of producing and manufacturing a product as

costs to the company, however for the buyer, the amount which has been paid towards availing

the services or products is often called the price. This amount or the price, is the unified

monetary value of the activities which the seller executed to bring the product or service to its

current condition and not to mention, the cost of the commodity itself. Furthermore, the costs

should include the expenses which directly or indirectly form part of the overall amount of the

product or service sold or to be sold. There are numerous different sorts of costs that the business

must deal with, but the two that pose the most challenges to the creation of products are indirect

costs and fixed costs.

Variable costs: These costs are those that are significantly influenced by a firm's sales

and productivity, or they are those that gauge how many products a business is producing

and marketing. A company's variable costs will rise or fall in direct proportion to its sale

and manufacturing of commodities, therefore indicates that things are simultaneous to

one another. The cost of transportation, raw materials, plastic cards, and other expenses

are all variables. Also, there will be deviations in the variable costs of the products across

the profits and may need to be allocated among the products, if the same are incurred for

goods or services sold through multiple branches. The variable costs are not of one kind,

they may be related to different items and accordingly their nature may vary, such as the

raw material and labour costs, commissions provided to the salesperson, utilities directly

affecting the costs of goods and services, shipping or freight charges incurred at the time

of transportation of the commodity by way of cargo. All of such costs are expenses to the

company and need to be allocated systematically.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed Costs: It is a cost that never changes, notwithstanding variations in the

manufacturing and sale of products and activities (Plaskova and et.al., 2020). It is a

separate expense whose amount is unaffected by any rises or falls in the price of goods or

activities. It involves paying bills, paying rental, paying healthcare, and paying a pay

check. Furthermore, the fixed costs are said to be the expenses incurred indirectly

towards bringing the product at its current location and condition. The management

should implement multiple methods to reduce such cost, which could be done through

application of shutdown points. The costs can be broken down into multiple types, such

as indirect and capital costs or those which are recorded in various financial statements. It

is to be noted that the fixed costs do not change over the course of the company’s life of

an agreement or cost schedule.

Semi-variable costs: The expense that is incurred on a regular basis and is dependent on

annual, quarterly, or early payments in order to analyse the customer’s demands

Essentially, it includes both fixed costs and variable costs. Depreciation of capital assets,

building rent, and personnel are semi-variable expenditures. Along with the application

of the other costs which are discussed before, the semi-variable costs are also an integral

part of the financial statements of the company, where they are classified as an expense

account, such as the rent amount or similar utilities, which will later in be recorded in the

income statement. Moreover, the analysis of the semi variable costs are often considered

as the component of the managerial accounting system and can be used for internal

proceedings.

manufacturing and sale of products and activities (Plaskova and et.al., 2020). It is a

separate expense whose amount is unaffected by any rises or falls in the price of goods or

activities. It involves paying bills, paying rental, paying healthcare, and paying a pay

check. Furthermore, the fixed costs are said to be the expenses incurred indirectly

towards bringing the product at its current location and condition. The management

should implement multiple methods to reduce such cost, which could be done through

application of shutdown points. The costs can be broken down into multiple types, such

as indirect and capital costs or those which are recorded in various financial statements. It

is to be noted that the fixed costs do not change over the course of the company’s life of

an agreement or cost schedule.

Semi-variable costs: The expense that is incurred on a regular basis and is dependent on

annual, quarterly, or early payments in order to analyse the customer’s demands

Essentially, it includes both fixed costs and variable costs. Depreciation of capital assets,

building rent, and personnel are semi-variable expenditures. Along with the application

of the other costs which are discussed before, the semi-variable costs are also an integral

part of the financial statements of the company, where they are classified as an expense

account, such as the rent amount or similar utilities, which will later in be recorded in the

income statement. Moreover, the analysis of the semi variable costs are often considered

as the component of the managerial accounting system and can be used for internal

proceedings.

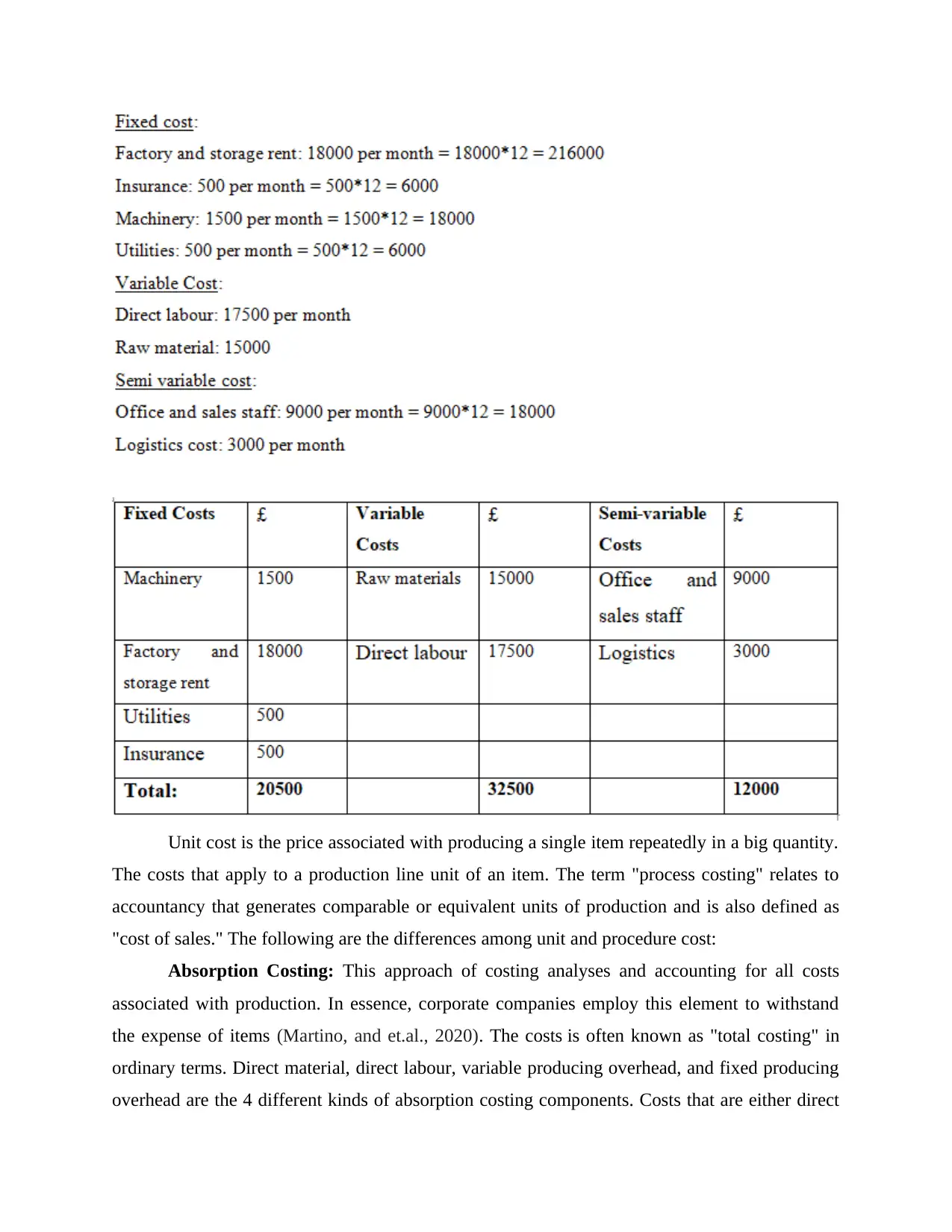

Unit cost is the price associated with producing a single item repeatedly in a big quantity.

The costs that apply to a production line unit of an item. The term "process costing" relates to

accountancy that generates comparable or equivalent units of production and is also defined as

"cost of sales." The following are the differences among unit and procedure cost:

Absorption Costing: This approach of costing analyses and accounting for all costs

associated with production. In essence, corporate companies employ this element to withstand

the expense of items (Martino, and et.al., 2020). The costs is often known as "total costing" in

ordinary terms. Direct material, direct labour, variable producing overhead, and fixed producing

overhead are the 4 different kinds of absorption costing components. Costs that are either direct

The costs that apply to a production line unit of an item. The term "process costing" relates to

accountancy that generates comparable or equivalent units of production and is also defined as

"cost of sales." The following are the differences among unit and procedure cost:

Absorption Costing: This approach of costing analyses and accounting for all costs

associated with production. In essence, corporate companies employ this element to withstand

the expense of items (Martino, and et.al., 2020). The costs is often known as "total costing" in

ordinary terms. Direct material, direct labour, variable producing overhead, and fixed producing

overhead are the 4 different kinds of absorption costing components. Costs that are either direct

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

or indirect are included in this. The primary components of direct costs are labour and the

quantity of materials used in producing the items. Included in the manufacturing's indirect costs

are administrative costs, facility rental, safety fees, and insuring. The absorption costing is

typically computed in the area of production sectors, which aids the business in calculating the

value of things in order to evaluate greater costs and amounts and therefore aids in pricing

management (Thi, Tran and Doan, 2021). For better understanding the concept of the fixed cost

and the way they impact the overall profitability of the company, the example of a company can

be examined, where the management proposes to produce 10000 units within the month. Here,

out of the 10000 units produced, 8000 units are sold to the consumers and the remaining 2000

are left as closing inventory. In this instance the management will incur multiple expenses such

as for the direct material and direct labour, whereas there will be certain indirect expenses which

could be related to the production facility where the products are manufactured and in this

instance, the company has incurred $20000 for the facility’s rent and the same will be identified

as the fixed overhead costs.

Marginal costing: It is the costing technique that charges variable costs to the pricing of

products and fully writes down fixed costs for a certain time in proportion to the contribution

price (Persson, 2019). The cost is what shows how many more expenses are involved in

producing an extra unit of something or output. The allocation of variable and fixed costs, price

observation, material value, and efficiency rate are all aspects of marginal costing. Analyzing the

cost factors that affects a firm's income ability and revenue is also helpful. There are multiple

factors which needs to be considered when the marginal costing method is applicable for

assessment of the company’s profit and overall market position in context to the manufacturing

and production process. Through administration of such factors or the revenue calculated from

the same, the organization can assess its revenue margin optimally for sustaining the sales and as

a result increase the profits. It can be witnessed that when the marginal cost per unit is high, then

an increase in the capacity of the production will lead to unnecessary expenses. For example, if a

tire manufacturing company manufactures 100 car tires and afterwards proposes to produce one

additional tire that would cost $80. Then such is considered as the marginal cost of the product

and will definitely make an impact over other related, whether direct or indirect business items.

Activity-based costing: To evaluate the manufacturing costs, cost is useful. The

distribution of production overhead costs manages according to methodologies (Liang, Ashuri

quantity of materials used in producing the items. Included in the manufacturing's indirect costs

are administrative costs, facility rental, safety fees, and insuring. The absorption costing is

typically computed in the area of production sectors, which aids the business in calculating the

value of things in order to evaluate greater costs and amounts and therefore aids in pricing

management (Thi, Tran and Doan, 2021). For better understanding the concept of the fixed cost

and the way they impact the overall profitability of the company, the example of a company can

be examined, where the management proposes to produce 10000 units within the month. Here,

out of the 10000 units produced, 8000 units are sold to the consumers and the remaining 2000

are left as closing inventory. In this instance the management will incur multiple expenses such

as for the direct material and direct labour, whereas there will be certain indirect expenses which

could be related to the production facility where the products are manufactured and in this

instance, the company has incurred $20000 for the facility’s rent and the same will be identified

as the fixed overhead costs.

Marginal costing: It is the costing technique that charges variable costs to the pricing of

products and fully writes down fixed costs for a certain time in proportion to the contribution

price (Persson, 2019). The cost is what shows how many more expenses are involved in

producing an extra unit of something or output. The allocation of variable and fixed costs, price

observation, material value, and efficiency rate are all aspects of marginal costing. Analyzing the

cost factors that affects a firm's income ability and revenue is also helpful. There are multiple

factors which needs to be considered when the marginal costing method is applicable for

assessment of the company’s profit and overall market position in context to the manufacturing

and production process. Through administration of such factors or the revenue calculated from

the same, the organization can assess its revenue margin optimally for sustaining the sales and as

a result increase the profits. It can be witnessed that when the marginal cost per unit is high, then

an increase in the capacity of the production will lead to unnecessary expenses. For example, if a

tire manufacturing company manufactures 100 car tires and afterwards proposes to produce one

additional tire that would cost $80. Then such is considered as the marginal cost of the product

and will definitely make an impact over other related, whether direct or indirect business items.

Activity-based costing: To evaluate the manufacturing costs, cost is useful. The

distribution of production overhead costs manages according to methodologies (Liang, Ashuri

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and Li, 2021). Concentrating on reducing overhead expenses is the next step in the activity-based

costing method. This costing significance is as follows:

Analyzing cost practises that indicate the cost practises route in relation to corporate

standing is helpful. Another crucial component of activity-based pricing that ultimately affects

business income is the item price (Lundberg and et.al, 2018). By considering the marketplace

and the worth of a similar rival's offering, the cost of the items is set. As an activity based costing

method, it is necessary to implement and execute procedures which can positively impact the

profit of the company, which has been calculated on the basis of the activity based costing

methods. For understanding the same, consider the example of ABC Ltd., a fabric manufacturing

company, specialised in selling different kinds of fabric to produce finished clothing items. Here

the company has incurred an electric bill of $50000 per year and the labour hours which have

been applied towards the same are 2500 hours. This figure of 2500 related to the actual labour

hours incurred, can be identified as the cost driver for such activity or the electricity bill expense.

Furthermore, the coast driver rate can be calculated by dividing the expense of $50000 from the

2500 hours, which will yield a cost of $20 and it simply implies the rate which the company will

incur in relation to the electric bill for each unit produced.

TASK 2

Provide the company your ideas for a cost-cutting approach.

There are several strategies which a company may use to decrease costs and accomplish its

declared or intended goals in ways which are beneficial to the bottom column. The opinion

which has been reached is that they must use the activity-based costing approach as their way of

cost calculation depending on the outcome which has been reached after using the

aforementioned methods (Liang, Ashuri and Li, 2021). The key justification for choosing this

strategy is that it separates the costs of each department of the firm and allocates the costs in

accordance with the determined drivers.

The ABC costing would aid them in enabling the costs associated with each of their

company operations, allowing them to quickly determine which departments are most beneficial

in terms of costing system. Departments that are operating at a loss increased expenses will be

certain that that their costs are kept within an appropriate range. The primary benefit of ABC

costing would be that it organizes costs as per task activity rather than assigning these to

costing method. This costing significance is as follows:

Analyzing cost practises that indicate the cost practises route in relation to corporate

standing is helpful. Another crucial component of activity-based pricing that ultimately affects

business income is the item price (Lundberg and et.al, 2018). By considering the marketplace

and the worth of a similar rival's offering, the cost of the items is set. As an activity based costing

method, it is necessary to implement and execute procedures which can positively impact the

profit of the company, which has been calculated on the basis of the activity based costing

methods. For understanding the same, consider the example of ABC Ltd., a fabric manufacturing

company, specialised in selling different kinds of fabric to produce finished clothing items. Here

the company has incurred an electric bill of $50000 per year and the labour hours which have

been applied towards the same are 2500 hours. This figure of 2500 related to the actual labour

hours incurred, can be identified as the cost driver for such activity or the electricity bill expense.

Furthermore, the coast driver rate can be calculated by dividing the expense of $50000 from the

2500 hours, which will yield a cost of $20 and it simply implies the rate which the company will

incur in relation to the electric bill for each unit produced.

TASK 2

Provide the company your ideas for a cost-cutting approach.

There are several strategies which a company may use to decrease costs and accomplish its

declared or intended goals in ways which are beneficial to the bottom column. The opinion

which has been reached is that they must use the activity-based costing approach as their way of

cost calculation depending on the outcome which has been reached after using the

aforementioned methods (Liang, Ashuri and Li, 2021). The key justification for choosing this

strategy is that it separates the costs of each department of the firm and allocates the costs in

accordance with the determined drivers.

The ABC costing would aid them in enabling the costs associated with each of their

company operations, allowing them to quickly determine which departments are most beneficial

in terms of costing system. Departments that are operating at a loss increased expenses will be

certain that that their costs are kept within an appropriate range. The primary benefit of ABC

costing would be that it organizes costs as per task activity rather than assigning these to

operating departments. It helps the firm reduce the total value of the final piece that helps with

company decisions on how much to charge for the goods at the point of sale in order not to

annoy the client. It is suggested that Dysonica Plc employ activity-based costing approaches in

their activities in addition to proportionately reduce manufacturing prices in consideration of the

preceding debate.

Any business that wants to increase its bottom line should implement a cost cutting plan

to reduce its costs. Such approaches are distinctive since they depend on the kinds of goods and

activities a business is providing to its target market. The goal of this method is to reduce the

price that is linked with every item sans compromising the excellence of that item. According to

the aforementioned figures and expenditures, Dysonica Plc should implement this method to cut

prices. The use of marginal costing is among the suggestions made by Dysonica Plc since it

results in a price of producing which is different from the overall output price when one more

item is produced (Li and Gu, 2020). This would help in reducing the wasteful costs associated

with the manufacturing of additional add-on units and furthermore help and direct administration

in decoupling the costs and streamlining its operations.

Another suggestion for Dysonica Plc is to choose the activity-based costing technique as

it is the suitable technique for projecting the price of a good or services and aids in making

choices which are more exact and trustworthy. This approach will be used by Dysonica since it

makes it easier for the company to divide expenses among the many tasks carried out during the

production procedure. As a result of having a comprehensive grasp of the tasks that bring no

benefit and incur additional costs, Dysonica Plc could better comprehend its spending.

Other strategies Dysonica Plc. will pursue include improving payments conditions with

vendors in order to bargain over the price of basic components. by ensuring that the supply

chains' value is unaffected. If this expense is reduced, the business would benefit greatly from

being able to purchase products in quantity sans providing it a further consideration.

Dysonica Plc will engage in digital alternatives, which could add to a business' expenses and

initially come at a significant costs (Kuzey, Uyar and Delen, 2019). However, implementing new

technology innovations would aid businesses in lowering their long-term operating costs while

simultaneously increasing their productivity. Dysonica Plc. Ltd is required to maintain account

of all costs spent throughout regular company operations. It will monitor the price of utilities,

land, warehousing, as well as other expenses. They will create estimates appropriately such that

company decisions on how much to charge for the goods at the point of sale in order not to

annoy the client. It is suggested that Dysonica Plc employ activity-based costing approaches in

their activities in addition to proportionately reduce manufacturing prices in consideration of the

preceding debate.

Any business that wants to increase its bottom line should implement a cost cutting plan

to reduce its costs. Such approaches are distinctive since they depend on the kinds of goods and

activities a business is providing to its target market. The goal of this method is to reduce the

price that is linked with every item sans compromising the excellence of that item. According to

the aforementioned figures and expenditures, Dysonica Plc should implement this method to cut

prices. The use of marginal costing is among the suggestions made by Dysonica Plc since it

results in a price of producing which is different from the overall output price when one more

item is produced (Li and Gu, 2020). This would help in reducing the wasteful costs associated

with the manufacturing of additional add-on units and furthermore help and direct administration

in decoupling the costs and streamlining its operations.

Another suggestion for Dysonica Plc is to choose the activity-based costing technique as

it is the suitable technique for projecting the price of a good or services and aids in making

choices which are more exact and trustworthy. This approach will be used by Dysonica since it

makes it easier for the company to divide expenses among the many tasks carried out during the

production procedure. As a result of having a comprehensive grasp of the tasks that bring no

benefit and incur additional costs, Dysonica Plc could better comprehend its spending.

Other strategies Dysonica Plc. will pursue include improving payments conditions with

vendors in order to bargain over the price of basic components. by ensuring that the supply

chains' value is unaffected. If this expense is reduced, the business would benefit greatly from

being able to purchase products in quantity sans providing it a further consideration.

Dysonica Plc will engage in digital alternatives, which could add to a business' expenses and

initially come at a significant costs (Kuzey, Uyar and Delen, 2019). However, implementing new

technology innovations would aid businesses in lowering their long-term operating costs while

simultaneously increasing their productivity. Dysonica Plc. Ltd is required to maintain account

of all costs spent throughout regular company operations. It will monitor the price of utilities,

land, warehousing, as well as other expenses. They will create estimates appropriately such that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

they may advise the business on how to allocate costs based on the activity in the various

divisions. Such administrative expenses could be reduced (Knezevic, 2019).

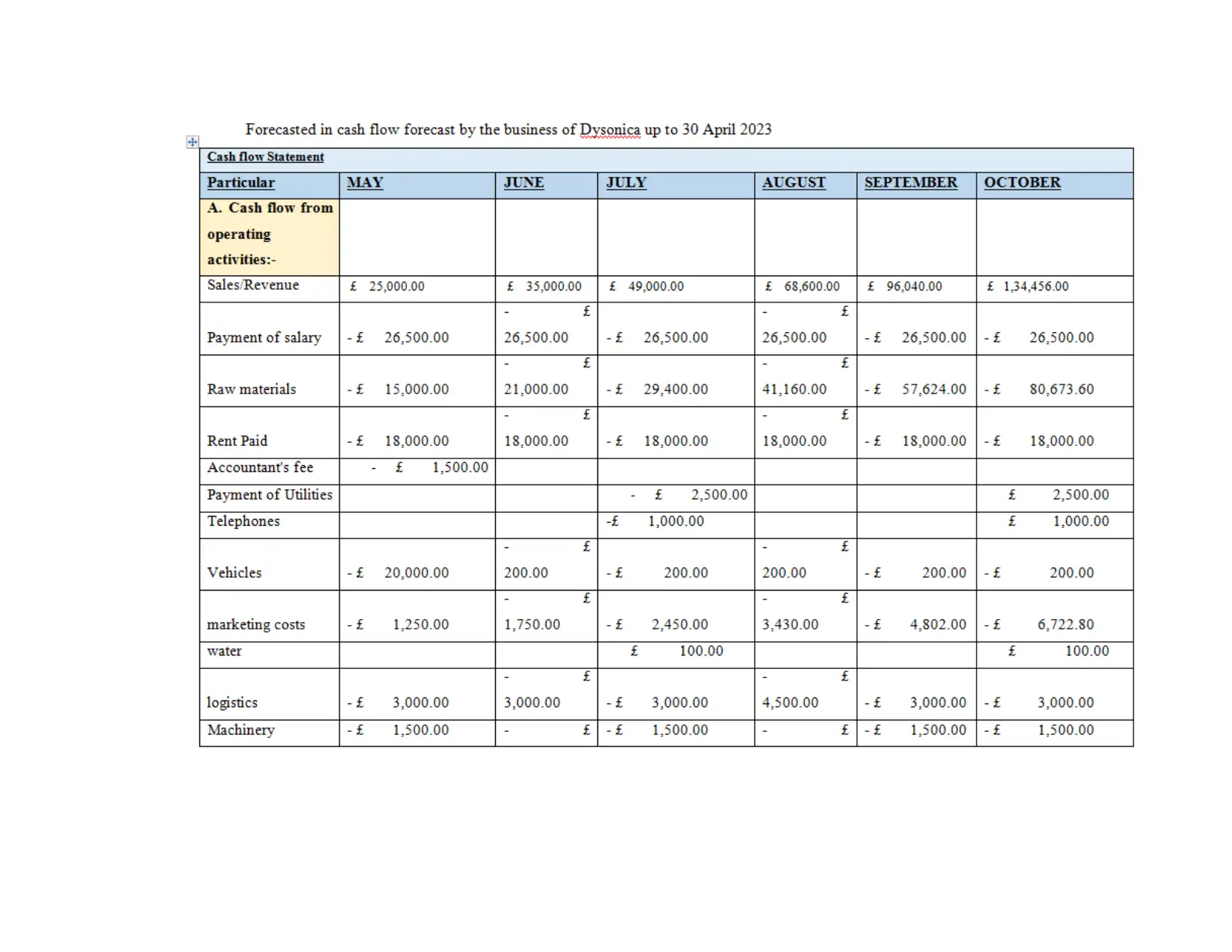

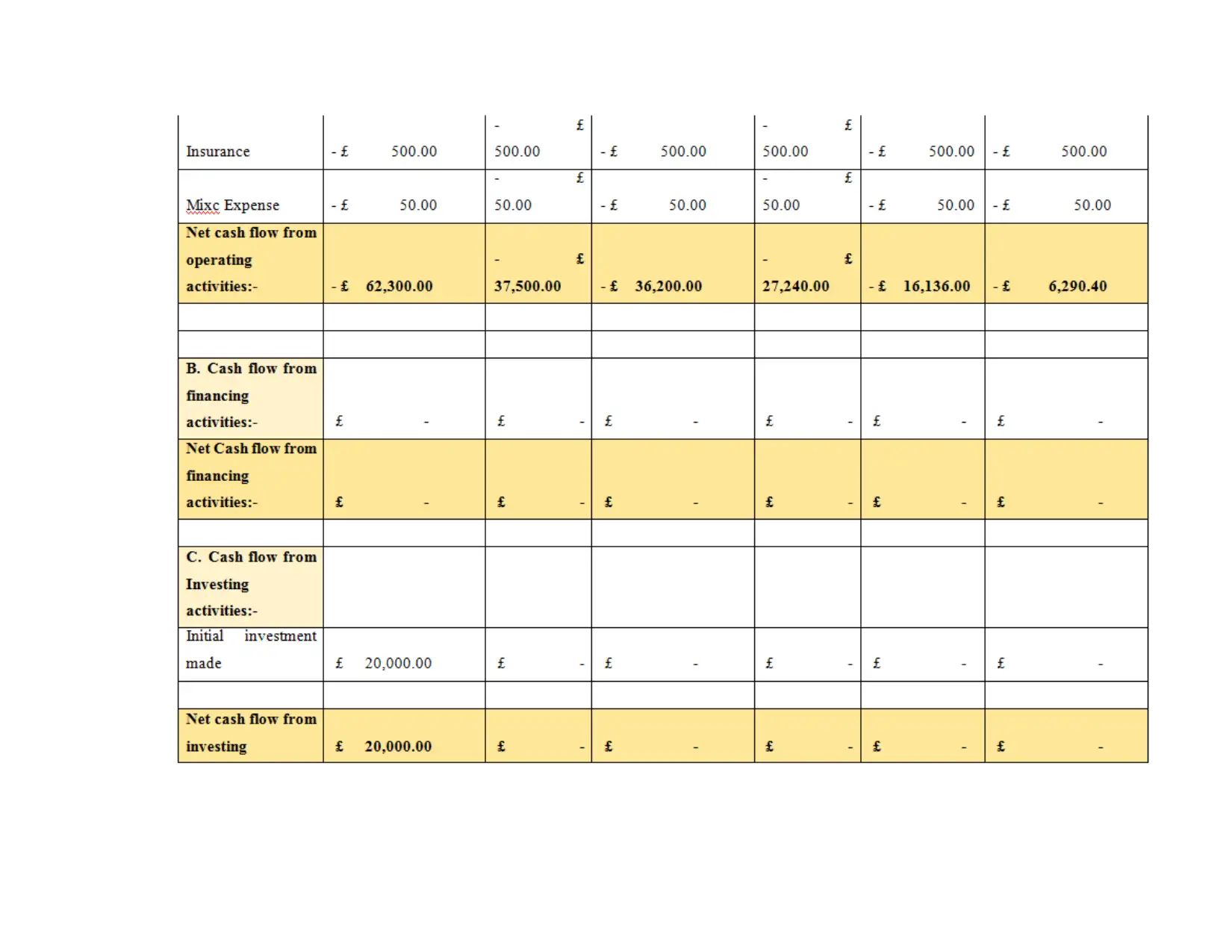

TASK 3

The creation of a 12-month plan and budget for the company until 30 April 2023

The budget of a company is defined as the systematic and clear representation of all the

expenses and incomes which are incurred in course of the business. This signifies the relevant

and sanctioned limit which needs to followed and should not be exceeded, if the company wants

effective and efficient results without risking the valuable resources which are available to the

company in a specific period of time. A budget overview that displays the sources of money for

a company is known as a "income articulation." The three components are earning money,

cutting costs, and investing money (Paulet, 2018). A revenue statement depicts a company's core

financial situation (Janzen, Carter and Ikegami, 2021). The assertion may be used by

organisations to determine how much money a company produces annually and if it has enough

cash on hand to fund future projects.

In contrast to the payment rationale and financial details, non-cash activities such as

depreciation and uncollected collections are not included in the revenue declaration.

divisions. Such administrative expenses could be reduced (Knezevic, 2019).

TASK 3

The creation of a 12-month plan and budget for the company until 30 April 2023

The budget of a company is defined as the systematic and clear representation of all the

expenses and incomes which are incurred in course of the business. This signifies the relevant

and sanctioned limit which needs to followed and should not be exceeded, if the company wants

effective and efficient results without risking the valuable resources which are available to the

company in a specific period of time. A budget overview that displays the sources of money for

a company is known as a "income articulation." The three components are earning money,

cutting costs, and investing money (Paulet, 2018). A revenue statement depicts a company's core

financial situation (Janzen, Carter and Ikegami, 2021). The assertion may be used by

organisations to determine how much money a company produces annually and if it has enough

cash on hand to fund future projects.

In contrast to the payment rationale and financial details, non-cash activities such as

depreciation and uncollected collections are not included in the revenue declaration.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.