Dysonica Plc: Cost Analysis, Reduction Strategies, and Budgeting 2023

VerifiedAdded on 2023/06/09

|14

|4312

|160

Report

AI Summary

This report assesses Dysonica Plc's cost management strategies, providing an in-depth analysis of various costing methods including variable, fixed, marginal, activity-based, and absorption costing. It recommends cost reduction policies, such as adopting activity-based costing and marginal costing, to improve efficiency and profitability. The report also develops a 12-month budget forecast up to April 30, 2023, and examines the company's financial presentation based on these forecasts. The analysis covers key areas like cost identification, expense reduction, and financial performance evaluation, offering insights into how Dysonica Plc can optimize its financial operations. Desklib provides access to similar solved assignments and resources for students.

FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION.......................................................................................................................3

TASK 1.....................................................................................................................................3

Establish the purpose of cost.............................................................................................................3

TASK 2.....................................................................................................................................7

Render the recommendations towards the business for the cost reduction policies and strategies...7

TASK 3.....................................................................................................................................8

Develop a 12-month budget/forecast the business activities up to 30th April 2023............................8

TASK 4...................................................................................................................................11

With the help of figures and facts in the budgets and forecast, examine and analyse the

presentation of Dysonica Plc............................................................................................................11

CONCLUSION.........................................................................................................................12

REFERENCES..........................................................................................................................13

INTRODUCTION.......................................................................................................................3

TASK 1.....................................................................................................................................3

Establish the purpose of cost.............................................................................................................3

TASK 2.....................................................................................................................................7

Render the recommendations towards the business for the cost reduction policies and strategies...7

TASK 3.....................................................................................................................................8

Develop a 12-month budget/forecast the business activities up to 30th April 2023............................8

TASK 4...................................................................................................................................11

With the help of figures and facts in the budgets and forecast, examine and analyse the

presentation of Dysonica Plc............................................................................................................11

CONCLUSION.........................................................................................................................12

REFERENCES..........................................................................................................................13

INTRODUCTION

The report prepared as under explains the quantity of amount, managed and arranged by the

business enterprises for the purpose to fulfil the demands and expectations of the firm in long

run. It can also be explained as the funds which are being utilised by the companies or businesses

for running a business in competitive environment. These funds would include the credit funds

and capital funds which are being invested in a industry. The enterprise further would be utilising

these funds in acquiring the assets, purchasing of raw materials and producing a good and other

operational function considering activities. When the business would be starting its firm after

that the capital being introduced is not enough for meeting and reaching each and every desire

related to business (Aldridge and Avellaneda, 2021). Hence, in relation to fulfil such needs,

business companies would be looking after so many mechanisms for generating revenues and

profits. The evaluation of possibilities and financial requirements and possibilities could be cross

checked on a daily basis such that the good financial management plan could be created,

developed and prepared for smoother functioning of a business. This report takes in account case

study based on Dysonica Plc. It consists of four operational activities where the first task would

be considering the expense related areas. And segments of a firm and in what ways it would be

differentiating among them. The second task would be highlighting the recommendations for the

management which would help the managers in reducing the expenses and cost as well. The third

task consists the projection and estimation of cash flow of Dysonica Plc till April 30, 2023. And

the last task states in what ways accomplishment and achievements can be examined of an

organisation and in what ways a specific industry is being observed to perform. This judgement

would be taking place in relation with forecasted values in the cash flow of Dysonica Plc.

TASK 1

Establish the purpose of cost.

Cost can be explained as a term which is helpful in supplying and manufacturing of

commodities and services. In production cycle, cost can explain as a very essential element at

every level from acquisition of raw materials to finished products of a company. Generally the

cost is stated as a amount of fund which is helpful in covering expenses related towards

production being carried out. There are various sort of costs which would be affecting the

The report prepared as under explains the quantity of amount, managed and arranged by the

business enterprises for the purpose to fulfil the demands and expectations of the firm in long

run. It can also be explained as the funds which are being utilised by the companies or businesses

for running a business in competitive environment. These funds would include the credit funds

and capital funds which are being invested in a industry. The enterprise further would be utilising

these funds in acquiring the assets, purchasing of raw materials and producing a good and other

operational function considering activities. When the business would be starting its firm after

that the capital being introduced is not enough for meeting and reaching each and every desire

related to business (Aldridge and Avellaneda, 2021). Hence, in relation to fulfil such needs,

business companies would be looking after so many mechanisms for generating revenues and

profits. The evaluation of possibilities and financial requirements and possibilities could be cross

checked on a daily basis such that the good financial management plan could be created,

developed and prepared for smoother functioning of a business. This report takes in account case

study based on Dysonica Plc. It consists of four operational activities where the first task would

be considering the expense related areas. And segments of a firm and in what ways it would be

differentiating among them. The second task would be highlighting the recommendations for the

management which would help the managers in reducing the expenses and cost as well. The third

task consists the projection and estimation of cash flow of Dysonica Plc till April 30, 2023. And

the last task states in what ways accomplishment and achievements can be examined of an

organisation and in what ways a specific industry is being observed to perform. This judgement

would be taking place in relation with forecasted values in the cash flow of Dysonica Plc.

TASK 1

Establish the purpose of cost.

Cost can be explained as a term which is helpful in supplying and manufacturing of

commodities and services. In production cycle, cost can explain as a very essential element at

every level from acquisition of raw materials to finished products of a company. Generally the

cost is stated as a amount of fund which is helpful in covering expenses related towards

production being carried out. There are various sort of costs which would be affecting the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

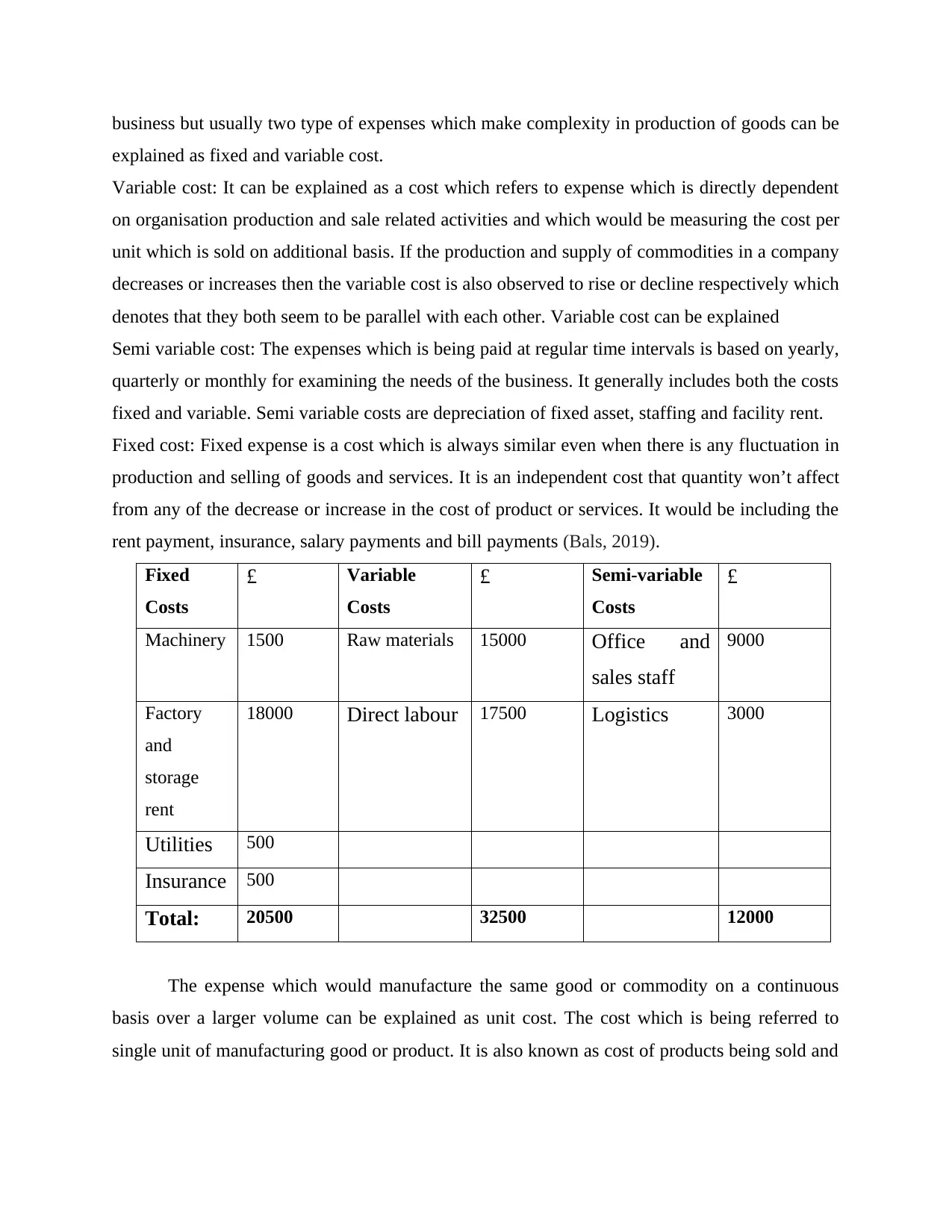

business but usually two type of expenses which make complexity in production of goods can be

explained as fixed and variable cost.

Variable cost: It can be explained as a cost which refers to expense which is directly dependent

on organisation production and sale related activities and which would be measuring the cost per

unit which is sold on additional basis. If the production and supply of commodities in a company

decreases or increases then the variable cost is also observed to rise or decline respectively which

denotes that they both seem to be parallel with each other. Variable cost can be explained

Semi variable cost: The expenses which is being paid at regular time intervals is based on yearly,

quarterly or monthly for examining the needs of the business. It generally includes both the costs

fixed and variable. Semi variable costs are depreciation of fixed asset, staffing and facility rent.

Fixed cost: Fixed expense is a cost which is always similar even when there is any fluctuation in

production and selling of goods and services. It is an independent cost that quantity won’t affect

from any of the decrease or increase in the cost of product or services. It would be including the

rent payment, insurance, salary payments and bill payments (Bals, 2019).

Fixed

Costs

£ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory

and

storage

rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

The expense which would manufacture the same good or commodity on a continuous

basis over a larger volume can be explained as unit cost. The cost which is being referred to

single unit of manufacturing good or product. It is also known as cost of products being sold and

explained as fixed and variable cost.

Variable cost: It can be explained as a cost which refers to expense which is directly dependent

on organisation production and sale related activities and which would be measuring the cost per

unit which is sold on additional basis. If the production and supply of commodities in a company

decreases or increases then the variable cost is also observed to rise or decline respectively which

denotes that they both seem to be parallel with each other. Variable cost can be explained

Semi variable cost: The expenses which is being paid at regular time intervals is based on yearly,

quarterly or monthly for examining the needs of the business. It generally includes both the costs

fixed and variable. Semi variable costs are depreciation of fixed asset, staffing and facility rent.

Fixed cost: Fixed expense is a cost which is always similar even when there is any fluctuation in

production and selling of goods and services. It is an independent cost that quantity won’t affect

from any of the decrease or increase in the cost of product or services. It would be including the

rent payment, insurance, salary payments and bill payments (Bals, 2019).

Fixed

Costs

£ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory

and

storage

rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

The expense which would manufacture the same good or commodity on a continuous

basis over a larger volume can be explained as unit cost. The cost which is being referred to

single unit of manufacturing good or product. It is also known as cost of products being sold and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

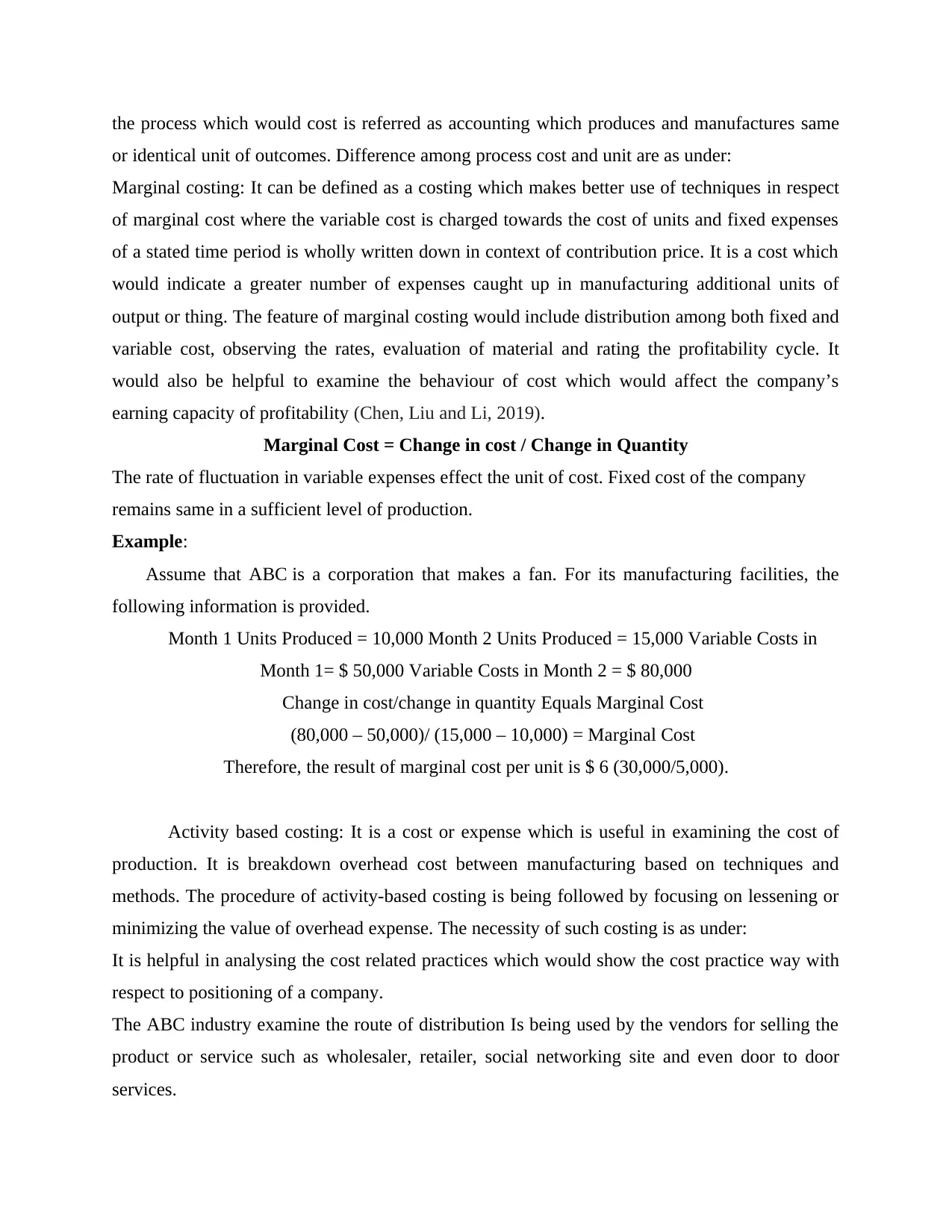

the process which would cost is referred as accounting which produces and manufactures same

or identical unit of outcomes. Difference among process cost and unit are as under:

Marginal costing: It can be defined as a costing which makes better use of techniques in respect

of marginal cost where the variable cost is charged towards the cost of units and fixed expenses

of a stated time period is wholly written down in context of contribution price. It is a cost which

would indicate a greater number of expenses caught up in manufacturing additional units of

output or thing. The feature of marginal costing would include distribution among both fixed and

variable cost, observing the rates, evaluation of material and rating the profitability cycle. It

would also be helpful to examine the behaviour of cost which would affect the company’s

earning capacity of profitability (Chen, Liu and Li, 2019).

Marginal Cost = Change in cost / Change in Quantity

The rate of fluctuation in variable expenses effect the unit of cost. Fixed cost of the company

remains same in a sufficient level of production.

Example:

Assume that ABC is a corporation that makes a fan. For its manufacturing facilities, the

following information is provided.

Month 1 Units Produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in

Month 1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

Therefore, the result of marginal cost per unit is $ 6 (30,000/5,000).

Activity based costing: It is a cost or expense which is useful in examining the cost of

production. It is breakdown overhead cost between manufacturing based on techniques and

methods. The procedure of activity-based costing is being followed by focusing on lessening or

minimizing the value of overhead expense. The necessity of such costing is as under:

It is helpful in analysing the cost related practices which would show the cost practice way with

respect to positioning of a company.

The ABC industry examine the route of distribution Is being used by the vendors for selling the

product or service such as wholesaler, retailer, social networking site and even door to door

services.

or identical unit of outcomes. Difference among process cost and unit are as under:

Marginal costing: It can be defined as a costing which makes better use of techniques in respect

of marginal cost where the variable cost is charged towards the cost of units and fixed expenses

of a stated time period is wholly written down in context of contribution price. It is a cost which

would indicate a greater number of expenses caught up in manufacturing additional units of

output or thing. The feature of marginal costing would include distribution among both fixed and

variable cost, observing the rates, evaluation of material and rating the profitability cycle. It

would also be helpful to examine the behaviour of cost which would affect the company’s

earning capacity of profitability (Chen, Liu and Li, 2019).

Marginal Cost = Change in cost / Change in Quantity

The rate of fluctuation in variable expenses effect the unit of cost. Fixed cost of the company

remains same in a sufficient level of production.

Example:

Assume that ABC is a corporation that makes a fan. For its manufacturing facilities, the

following information is provided.

Month 1 Units Produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in

Month 1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

Therefore, the result of marginal cost per unit is $ 6 (30,000/5,000).

Activity based costing: It is a cost or expense which is useful in examining the cost of

production. It is breakdown overhead cost between manufacturing based on techniques and

methods. The procedure of activity-based costing is being followed by focusing on lessening or

minimizing the value of overhead expense. The necessity of such costing is as under:

It is helpful in analysing the cost related practices which would show the cost practice way with

respect to positioning of a company.

The ABC industry examine the route of distribution Is being used by the vendors for selling the

product or service such as wholesaler, retailer, social networking site and even door to door

services.

The price scale of goods is also essential part of activity-based costing which would directly be

affecting the revenue of company. Price of good are fixed after examination of marketplace and

the value of same competitors company goods. If the price of goods is more than minimum

expense then it may lead to problem of loss so the minimum pricing would prove to be useful for

maintaining the postilion in market (Costello, 2019).

Absorption costing: It can be explained as a cost which cover the method of costing which

examine and make proper accounting of manufacturing related cost. Usually this element is used

by the businesses for absorbing the expense related to goods. In simple language the cost is also

denoted as full costing. There are four sort of absorption costing factors such as direct labour,

direct material, fixed manufacturing overhead and variable production overhead. It is the expense

which consider direct or indirect expense. The main aspects of direct cost is the number of labour

and material which are helpful in manufacturing of goods. Whereas in case of indirect cost of

production. It would be including security charges, insurance and factory rent as well.

Computation of absorption costing:

Absorption costing formula = (Direct labour cost + Direct material cost + Variable

manufacturing overhead cost + Fixed manufacturing overhead) / No. of units produced

The absorption costing is usually computed in the field of manufacturing industries helping the

firm in computation of cost of goods such that the business would be able to analyse the better

cost computed for the amount as well as it would also help in having better control over the price

of products.

For example:

Assuming that the ABC company is a manufacturer of fans. The following data is being provided

for manufacturing of one phase. The revenues will be computed with the help of absorption

costing method.

The number of units produced equals 10,000. 9,000 units sold over the time = $ 50 unit price

Direct Labour = $ 5 Direct Material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

affecting the revenue of company. Price of good are fixed after examination of marketplace and

the value of same competitors company goods. If the price of goods is more than minimum

expense then it may lead to problem of loss so the minimum pricing would prove to be useful for

maintaining the postilion in market (Costello, 2019).

Absorption costing: It can be explained as a cost which cover the method of costing which

examine and make proper accounting of manufacturing related cost. Usually this element is used

by the businesses for absorbing the expense related to goods. In simple language the cost is also

denoted as full costing. There are four sort of absorption costing factors such as direct labour,

direct material, fixed manufacturing overhead and variable production overhead. It is the expense

which consider direct or indirect expense. The main aspects of direct cost is the number of labour

and material which are helpful in manufacturing of goods. Whereas in case of indirect cost of

production. It would be including security charges, insurance and factory rent as well.

Computation of absorption costing:

Absorption costing formula = (Direct labour cost + Direct material cost + Variable

manufacturing overhead cost + Fixed manufacturing overhead) / No. of units produced

The absorption costing is usually computed in the field of manufacturing industries helping the

firm in computation of cost of goods such that the business would be able to analyse the better

cost computed for the amount as well as it would also help in having better control over the price

of products.

For example:

Assuming that the ABC company is a manufacturer of fans. The following data is being provided

for manufacturing of one phase. The revenues will be computed with the help of absorption

costing method.

The number of units produced equals 10,000. 9,000 units sold over the time = $ 50 unit price

Direct Labour = $ 5 Direct Material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

Render the recommendations towards the business for the cost reduction policies and strategies.

There are several methods which a business can adopt for reducing or cutting down its cost

and achieveing its desired or set objectives in methods which would reflect on the bottom line in

an efficient and effective manner.

On the basis of the outcomes which has been considered after implementation of the above tools

and techniques the conclusion which has been made is that they must incorporate Activity based

costing method as their tool to compute the cost (Dorfleitner and Braun, 2019). The main reason

after selection of such methodologies is that it is considered expense of each department of the

business separation and allocating the cost on the basis of drivers which has been computed. The

ABC costing would be helpful in enabling the cost in each of their business process and which

can be checked easily as which department is helpful for them in relation with cost allocation and

those departments which have been incurring more cost would be ensuring that their price shall

be managed and maintained under an acceptable bound. The main benefit of ABC costing is such

thst it facilitates grouping of cost according to the job work rather than allocating the same on the

department which are being operational. It is helpful in reducing the expense related to final

product as a whole which would be helpful in business enterprise for deciding the selling prices

of the goods and services to an acceptable level such that it won’t be creating burden on the

customers as well. Therefore, on the basis of above carried out discussion it is being

recommended to Dysonica Plc to adopt activity-based costing technique in their businesses so

that they are able to cut down cost of product in accordance.

Cost reduction strategy can be explained as a method which any company could adopt for

cutting down its expenses for bringing an increment in their bottom line. These methods are

observed to be different as they would be relying on the similar sort of goods and services which

is a company would be offering to its linked audience. The reason behind use of such strategies

and policies’ is to lower the expense which are being associated with every product without

bringing the transformation in its quality. From the above computations in accordance with the

cost Dysonica Plc must be choosing such strategies for lowering its expenses. The suggestions

given for Dysonica PLc takes in account the adoption of marginal costing as such cost of making

is the result with the variation in total production cost which arrives from manufacturing of one

extra unit (Gallagher, 2018). This will aid in cutting down expenses which are not important and

Render the recommendations towards the business for the cost reduction policies and strategies.

There are several methods which a business can adopt for reducing or cutting down its cost

and achieveing its desired or set objectives in methods which would reflect on the bottom line in

an efficient and effective manner.

On the basis of the outcomes which has been considered after implementation of the above tools

and techniques the conclusion which has been made is that they must incorporate Activity based

costing method as their tool to compute the cost (Dorfleitner and Braun, 2019). The main reason

after selection of such methodologies is that it is considered expense of each department of the

business separation and allocating the cost on the basis of drivers which has been computed. The

ABC costing would be helpful in enabling the cost in each of their business process and which

can be checked easily as which department is helpful for them in relation with cost allocation and

those departments which have been incurring more cost would be ensuring that their price shall

be managed and maintained under an acceptable bound. The main benefit of ABC costing is such

thst it facilitates grouping of cost according to the job work rather than allocating the same on the

department which are being operational. It is helpful in reducing the expense related to final

product as a whole which would be helpful in business enterprise for deciding the selling prices

of the goods and services to an acceptable level such that it won’t be creating burden on the

customers as well. Therefore, on the basis of above carried out discussion it is being

recommended to Dysonica Plc to adopt activity-based costing technique in their businesses so

that they are able to cut down cost of product in accordance.

Cost reduction strategy can be explained as a method which any company could adopt for

cutting down its expenses for bringing an increment in their bottom line. These methods are

observed to be different as they would be relying on the similar sort of goods and services which

is a company would be offering to its linked audience. The reason behind use of such strategies

and policies’ is to lower the expense which are being associated with every product without

bringing the transformation in its quality. From the above computations in accordance with the

cost Dysonica Plc must be choosing such strategies for lowering its expenses. The suggestions

given for Dysonica PLc takes in account the adoption of marginal costing as such cost of making

is the result with the variation in total production cost which arrives from manufacturing of one

extra unit (Gallagher, 2018). This will aid in cutting down expenses which are not important and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

even linked with the production of other additional unit and would be useful in giving guidance

to the management for separating the cost and organizing its processes in a efficient and effective

way.

Another advice to Dysonica PLc is to opt the activity-based costing method as it is a very precise

approach towards projecting a cost of commodity or service which would be helpful in taking the

decision which are more accurate and reliable. Dysonica must use this method as this would help

the business firm in allocation of cost according to various activities which are being performed

in the manufacturing process. Dysonica PLc can get a better understanding of the expenses as it

would be giving a clear insight of those actions which are not able to add any value and even

involving more and more expenses.

Other methods which Dysonica PLc must go for is development of better payment

terminologies with the vendor such that they would be able to negotiate for the costing of raw

materials. But making sure that it won’t be affecting the quality rendered by raw materials. If this

cost is being reduced then it would prove to be very useful for the organisation to buy goods in

bulk without giving it a second thought. Dominos Plc shall be investing in the technology-based

solution it might also be an additional cost for the company and might incur higher expenses in

the beginning. But adoption of new technique advancement would be helpful for the business

enterprises to minimize or lower its operational cost for long term and the output would also rise.

Dysonica Plc Ltd must keep a track of expenses which are incurred in the performance of day to

day business actions and activities. It must be keeping a close eye on the cost related to utility,

storage, other cost and property as well. It must. Be making budgets according to the guidance

given to company for allocation of expenses which are according to the activities carried out in

various departments. Through such overheads cost can be minimized (Harvey, Liu and Saretto,

2020).

TASK 3

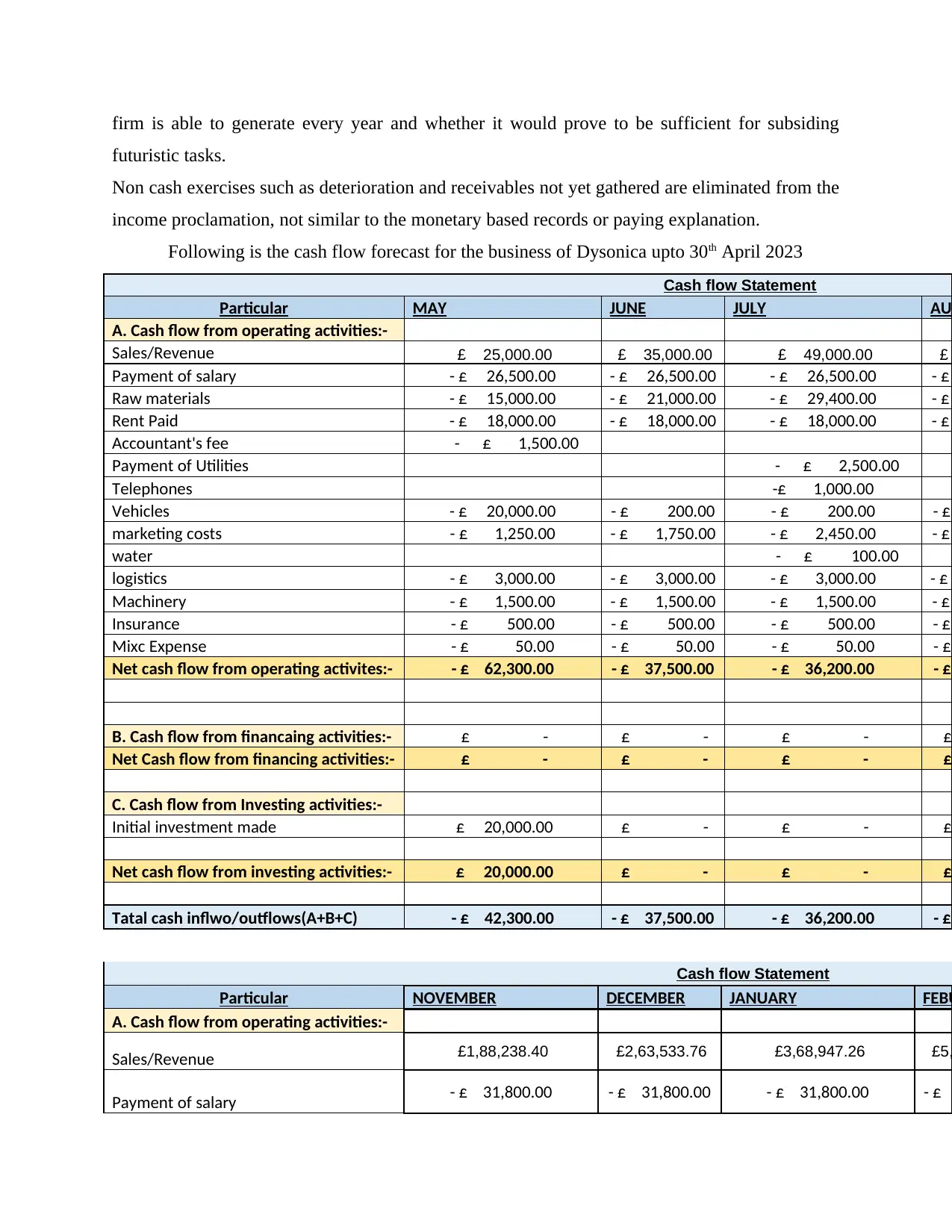

Develop a 12-month budget/forecast the business activities up to 30th April 2023.

An income articulation can be explained as a budget summary which shows the wellspring

of income for a enterprise. An income articulation is able to portray a company’s whole

monetary based status. Businesses are able to utilise the assertion for deciding how much cash a

to the management for separating the cost and organizing its processes in a efficient and effective

way.

Another advice to Dysonica PLc is to opt the activity-based costing method as it is a very precise

approach towards projecting a cost of commodity or service which would be helpful in taking the

decision which are more accurate and reliable. Dysonica must use this method as this would help

the business firm in allocation of cost according to various activities which are being performed

in the manufacturing process. Dysonica PLc can get a better understanding of the expenses as it

would be giving a clear insight of those actions which are not able to add any value and even

involving more and more expenses.

Other methods which Dysonica PLc must go for is development of better payment

terminologies with the vendor such that they would be able to negotiate for the costing of raw

materials. But making sure that it won’t be affecting the quality rendered by raw materials. If this

cost is being reduced then it would prove to be very useful for the organisation to buy goods in

bulk without giving it a second thought. Dominos Plc shall be investing in the technology-based

solution it might also be an additional cost for the company and might incur higher expenses in

the beginning. But adoption of new technique advancement would be helpful for the business

enterprises to minimize or lower its operational cost for long term and the output would also rise.

Dysonica Plc Ltd must keep a track of expenses which are incurred in the performance of day to

day business actions and activities. It must be keeping a close eye on the cost related to utility,

storage, other cost and property as well. It must. Be making budgets according to the guidance

given to company for allocation of expenses which are according to the activities carried out in

various departments. Through such overheads cost can be minimized (Harvey, Liu and Saretto,

2020).

TASK 3

Develop a 12-month budget/forecast the business activities up to 30th April 2023.

An income articulation can be explained as a budget summary which shows the wellspring

of income for a enterprise. An income articulation is able to portray a company’s whole

monetary based status. Businesses are able to utilise the assertion for deciding how much cash a

firm is able to generate every year and whether it would prove to be sufficient for subsiding

futuristic tasks.

Non cash exercises such as deterioration and receivables not yet gathered are eliminated from the

income proclamation, not similar to the monetary based records or paying explanation.

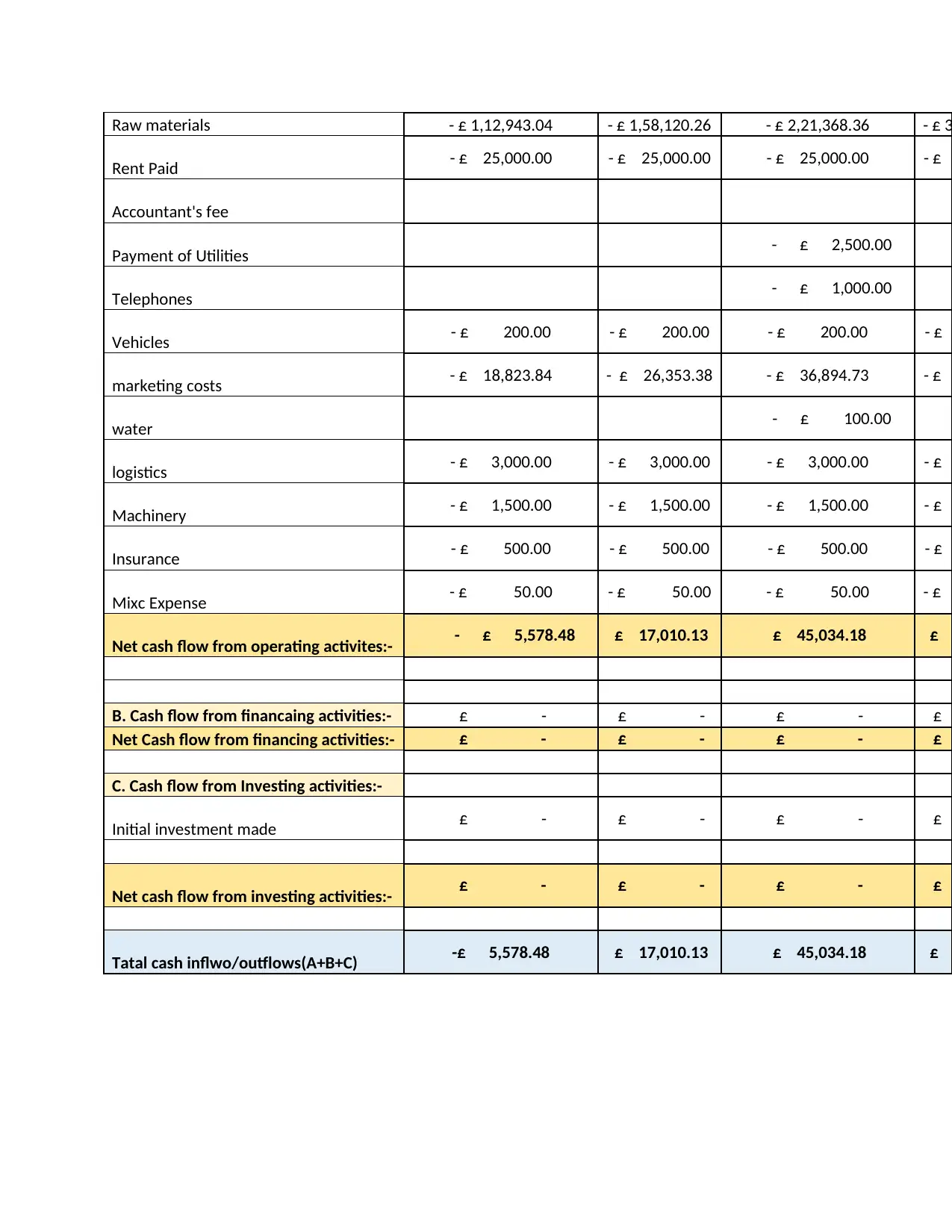

Following is the cash flow forecast for the business of Dysonica upto 30th April 2023

Cash flow Statement

Particular MAY JUNE JULY AUG

A. Cash flow from operating activities:-

Sales/Revenue £ 25,000.00 £ 35,000.00 £ 49,000.00 £

Payment of salary - £ 26,500.00 - £ 26,500.00 - £ 26,500.00 - £

Raw materials - £ 15,000.00 - £ 21,000.00 - £ 29,400.00 - £

Rent Paid - £ 18,000.00 - £ 18,000.00 - £ 18,000.00 - £

Accountant's fee - £ 1,500.00

Payment of Utilities - £ 2,500.00

Telephones -£ 1,000.00

Vehicles - £ 20,000.00 - £ 200.00 - £ 200.00 - £

marketing costs - £ 1,250.00 - £ 1,750.00 - £ 2,450.00 - £

water - £ 100.00

logistics - £ 3,000.00 - £ 3,000.00 - £ 3,000.00 - £

Machinery - £ 1,500.00 - £ 1,500.00 - £ 1,500.00 - £

Insurance - £ 500.00 - £ 500.00 - £ 500.00 - £

Mixc Expense - £ 50.00 - £ 50.00 - £ 50.00 - £

Net cash flow from operating activites:- - £ 62,300.00 - £ 37,500.00 - £ 36,200.00 - £

B. Cash flow from financaing activities:- £ - £ - £ - £

Net Cash flow from financing activities:- £ - £ - £ - £

C. Cash flow from Investing activities:-

Initial investment made £ 20,000.00 £ - £ - £

Net cash flow from investing activities:- £ 20,000.00 £ - £ - £

Tatal cash inflwo/outflows(A+B+C) - £ 42,300.00 - £ 37,500.00 - £ 36,200.00 - £

Cash flow Statement

Particular NOVEMBER DECEMBER JANUARY FEBU

A. Cash flow from operating activities:-

Sales/Revenue £1,88,238.40 £2,63,533.76 £3,68,947.26 £5,

Payment of salary - £ 31,800.00 - £ 31,800.00 - £ 31,800.00 - £

futuristic tasks.

Non cash exercises such as deterioration and receivables not yet gathered are eliminated from the

income proclamation, not similar to the monetary based records or paying explanation.

Following is the cash flow forecast for the business of Dysonica upto 30th April 2023

Cash flow Statement

Particular MAY JUNE JULY AUG

A. Cash flow from operating activities:-

Sales/Revenue £ 25,000.00 £ 35,000.00 £ 49,000.00 £

Payment of salary - £ 26,500.00 - £ 26,500.00 - £ 26,500.00 - £

Raw materials - £ 15,000.00 - £ 21,000.00 - £ 29,400.00 - £

Rent Paid - £ 18,000.00 - £ 18,000.00 - £ 18,000.00 - £

Accountant's fee - £ 1,500.00

Payment of Utilities - £ 2,500.00

Telephones -£ 1,000.00

Vehicles - £ 20,000.00 - £ 200.00 - £ 200.00 - £

marketing costs - £ 1,250.00 - £ 1,750.00 - £ 2,450.00 - £

water - £ 100.00

logistics - £ 3,000.00 - £ 3,000.00 - £ 3,000.00 - £

Machinery - £ 1,500.00 - £ 1,500.00 - £ 1,500.00 - £

Insurance - £ 500.00 - £ 500.00 - £ 500.00 - £

Mixc Expense - £ 50.00 - £ 50.00 - £ 50.00 - £

Net cash flow from operating activites:- - £ 62,300.00 - £ 37,500.00 - £ 36,200.00 - £

B. Cash flow from financaing activities:- £ - £ - £ - £

Net Cash flow from financing activities:- £ - £ - £ - £

C. Cash flow from Investing activities:-

Initial investment made £ 20,000.00 £ - £ - £

Net cash flow from investing activities:- £ 20,000.00 £ - £ - £

Tatal cash inflwo/outflows(A+B+C) - £ 42,300.00 - £ 37,500.00 - £ 36,200.00 - £

Cash flow Statement

Particular NOVEMBER DECEMBER JANUARY FEBU

A. Cash flow from operating activities:-

Sales/Revenue £1,88,238.40 £2,63,533.76 £3,68,947.26 £5,

Payment of salary - £ 31,800.00 - £ 31,800.00 - £ 31,800.00 - £

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Raw materials - £ 1,12,943.04 - £ 1,58,120.26 - £ 2,21,368.36 - £ 3

Rent Paid - £ 25,000.00 - £ 25,000.00 - £ 25,000.00 - £

Accountant's fee

Payment of Utilities - £ 2,500.00

Telephones - £ 1,000.00

Vehicles - £ 200.00 - £ 200.00 - £ 200.00 - £

marketing costs - £ 18,823.84 - £ 26,353.38 - £ 36,894.73 - £

water - £ 100.00

logistics - £ 3,000.00 - £ 3,000.00 - £ 3,000.00 - £

Machinery - £ 1,500.00 - £ 1,500.00 - £ 1,500.00 - £

Insurance - £ 500.00 - £ 500.00 - £ 500.00 - £

Mixc Expense - £ 50.00 - £ 50.00 - £ 50.00 - £

Net cash flow from operating activites:- - £ 5,578.48 £ 17,010.13 £ 45,034.18 £

B. Cash flow from financaing activities:- £ - £ - £ - £

Net Cash flow from financing activities:- £ - £ - £ - £

C. Cash flow from Investing activities:-

Initial investment made £ - £ - £ - £

Net cash flow from investing activities:- £ - £ - £ - £

Tatal cash inflwo/outflows(A+B+C) -£ 5,578.48 £ 17,010.13 £ 45,034.18 £

Rent Paid - £ 25,000.00 - £ 25,000.00 - £ 25,000.00 - £

Accountant's fee

Payment of Utilities - £ 2,500.00

Telephones - £ 1,000.00

Vehicles - £ 200.00 - £ 200.00 - £ 200.00 - £

marketing costs - £ 18,823.84 - £ 26,353.38 - £ 36,894.73 - £

water - £ 100.00

logistics - £ 3,000.00 - £ 3,000.00 - £ 3,000.00 - £

Machinery - £ 1,500.00 - £ 1,500.00 - £ 1,500.00 - £

Insurance - £ 500.00 - £ 500.00 - £ 500.00 - £

Mixc Expense - £ 50.00 - £ 50.00 - £ 50.00 - £

Net cash flow from operating activites:- - £ 5,578.48 £ 17,010.13 £ 45,034.18 £

B. Cash flow from financaing activities:- £ - £ - £ - £

Net Cash flow from financing activities:- £ - £ - £ - £

C. Cash flow from Investing activities:-

Initial investment made £ - £ - £ - £

Net cash flow from investing activities:- £ - £ - £ - £

Tatal cash inflwo/outflows(A+B+C) -£ 5,578.48 £ 17,010.13 £ 45,034.18 £

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

With the help of figures and facts in the budgets and forecast, examine and analyse the

presentation of Dysonica Plc.

From the above prepared cash flow oit can be interpreted that the business has good

accomplishment and achievements. Dysonica’s company appears to be performing pretty well as

observed by the cash flow forecasting plan as above. Companies can generate significant profit

and income throughout various time intervals, which would result in a large influx of resources.

In a season such as this, the group would be dealing in developing quickly, implying that the

group is having enough for offering to keep up with itself in a significant commercial hub. The

whole infusion of £2,465,187 into the business in the primary year is a good opportunity for

companies because they can be activated in several conditions for the company and could help

Dysonica expand. The corporation must cut down cost, especially which are related to currency

exchange rates among countries such as China and United Kingdom. Currency subsidiaries can

be utilised by firms to analyse the trade at predetermined exchange rates which would allow

them to have better control over the cost which are linked with such elements in a business.

Unfavourable inflow are common which indicates that the business has revenue in its first six to

eight years of operation, implying what the company wants for expanding trading or cutting

down usage. The company’s funding position is observed to be affected by the cyclical rise in

investment, which is a mandatory prerequisite for any company to win in deep marketplaces and

around the world as well. Costs can be cut by usage of alternative supply connection and

determining which drives shall be blamed and which would cost the organisation’s money. It is

necessary for them to generate operational functions over a constant basis such that their

operational cash flow would be remaining positive over a longer period of time.

The very first element of cash flow from operating activities for an accounting periof reflects

sale which start from the month of May and end in April and an rise can also be observed in the

twelve months. The forecasted cash flow statement would reflect that the business is able to

maintain its financial position good and sound. The Dysonica Plc can cover its short-term

liabilities without facing any issues and it has enough of current asset for dealing with the current

liabilities. Also, the sales projections can also be observed, which would represent that the

business is able to play to the point and carry out selling of products and services and even

generate good quantity of profit. The total cash inflow for the first year is being assessed at £

With the help of figures and facts in the budgets and forecast, examine and analyse the

presentation of Dysonica Plc.

From the above prepared cash flow oit can be interpreted that the business has good

accomplishment and achievements. Dysonica’s company appears to be performing pretty well as

observed by the cash flow forecasting plan as above. Companies can generate significant profit

and income throughout various time intervals, which would result in a large influx of resources.

In a season such as this, the group would be dealing in developing quickly, implying that the

group is having enough for offering to keep up with itself in a significant commercial hub. The

whole infusion of £2,465,187 into the business in the primary year is a good opportunity for

companies because they can be activated in several conditions for the company and could help

Dysonica expand. The corporation must cut down cost, especially which are related to currency

exchange rates among countries such as China and United Kingdom. Currency subsidiaries can

be utilised by firms to analyse the trade at predetermined exchange rates which would allow

them to have better control over the cost which are linked with such elements in a business.

Unfavourable inflow are common which indicates that the business has revenue in its first six to

eight years of operation, implying what the company wants for expanding trading or cutting

down usage. The company’s funding position is observed to be affected by the cyclical rise in

investment, which is a mandatory prerequisite for any company to win in deep marketplaces and

around the world as well. Costs can be cut by usage of alternative supply connection and

determining which drives shall be blamed and which would cost the organisation’s money. It is

necessary for them to generate operational functions over a constant basis such that their

operational cash flow would be remaining positive over a longer period of time.

The very first element of cash flow from operating activities for an accounting periof reflects

sale which start from the month of May and end in April and an rise can also be observed in the

twelve months. The forecasted cash flow statement would reflect that the business is able to

maintain its financial position good and sound. The Dysonica Plc can cover its short-term

liabilities without facing any issues and it has enough of current asset for dealing with the current

liabilities. Also, the sales projections can also be observed, which would represent that the

business is able to play to the point and carry out selling of products and services and even

generate good quantity of profit. The total cash inflow for the first year is being assessed at £

2,465,187 which states the best thing and also give an origin and scope towards the Dysonica Plc

for making new investment-based opportunities. Investment in new asset will actually serve as

an helping hand to Dysonica Plc for growing its business and attracting larger number of

stakeholders group. It is also being observed from the projected cash flow statements that the

Dysonica Plc is involved in the foreign exchange rates with the territories such as United

Kingdom and China. Some the cost which is incurred is the exchange which result in high level

amount which must be controlled and monitored by the businesses by using the techniques as it

would assist in the estimation of trade at the pre decided rates. All this would be useful for the

business in that very field for monitoring the direct expenses. For another six months a negative

inflow in cash is being examined which means that the business must focus or concentrate on

increasing its sales and cut down costs.

CONCLUSION

So, from the above asserted report it can be concluded that funds are necessary for

maintaining the stand in market for long run. Every business must be opting for finance from

various sources. In relation to compete with rivalries it must be handling operational activities in

a precise and efficient manner. Such companies must be using various tools and techniques for

reducing the cost and adopting number of mechanisms which would increase the profit scale and

revenue from sale operations. This report also gives a clear presentation on how you could

predict future financial potential and the capability of a business concern for meeting its

upcoming needs and requirements.

for making new investment-based opportunities. Investment in new asset will actually serve as

an helping hand to Dysonica Plc for growing its business and attracting larger number of

stakeholders group. It is also being observed from the projected cash flow statements that the

Dysonica Plc is involved in the foreign exchange rates with the territories such as United

Kingdom and China. Some the cost which is incurred is the exchange which result in high level

amount which must be controlled and monitored by the businesses by using the techniques as it

would assist in the estimation of trade at the pre decided rates. All this would be useful for the

business in that very field for monitoring the direct expenses. For another six months a negative

inflow in cash is being examined which means that the business must focus or concentrate on

increasing its sales and cut down costs.

CONCLUSION

So, from the above asserted report it can be concluded that funds are necessary for

maintaining the stand in market for long run. Every business must be opting for finance from

various sources. In relation to compete with rivalries it must be handling operational activities in

a precise and efficient manner. Such companies must be using various tools and techniques for

reducing the cost and adopting number of mechanisms which would increase the profit scale and

revenue from sale operations. This report also gives a clear presentation on how you could

predict future financial potential and the capability of a business concern for meeting its

upcoming needs and requirements.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.