Dysonica Plc: Cost Analysis, Budgeting, and Performance Review

VerifiedAdded on 2023/06/11

|12

|3505

|286

Report

AI Summary

This report provides a comprehensive financial analysis of Dysonica Plc, beginning with the classification of costs into fixed, variable, and semi-variable categories. It discusses various costing methods, including absorption, marginal, and activity-based costing, and recommends cost reduction strategies to improve operational efficiency. A 12-month cash flow forecast up to April 2023 is prepared to project the company's financial performance. Based on the forecast, the report evaluates Dysonica's performance, providing insights into its financial health and industry position. The analysis aims to assist Dysonica in making informed financial decisions and optimizing its business operations. Desklib provides solved assignments and past papers for students.

Constrained Project-

Business Finance

Business Finance

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Classify the costs according to their nature.................................................................................3

TASK 2............................................................................................................................................6

Provide recommendation and cost reduction strategy.................................................................6

TASK 3............................................................................................................................................7

Preparation a 12 - month forecast/budget for the business up to 30 April 2023.........................7

TASK 4..........................................................................................................................................10

Based on the facts in the forecast and budgets, evaluate Dysonica's performance...................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Classify the costs according to their nature.................................................................................3

TASK 2............................................................................................................................................6

Provide recommendation and cost reduction strategy.................................................................6

TASK 3............................................................................................................................................7

Preparation a 12 - month forecast/budget for the business up to 30 April 2023.........................7

TASK 4..........................................................................................................................................10

Based on the facts in the forecast and budgets, evaluate Dysonica's performance...................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Business finance refers to the money and credit that a company uses. The financial

foundation of a corporation is critical. Finance is necessary for the acquisition of assets,

products, and raw materials, as well as other economic activities. Let's look at the definition of

business finance in more detail. The capital invested by the entrepreneur to start the firm is

insufficient to meet the company's financial obligations (Connolly, and Bank, 2018). As an

outcome, the entrepreneur must find a strategy to generate revenue. To keep the company

running, a thorough examination of financial demands and options for meeting those needs must

be conducted with the express goal of achieving good financial management. The following

report highlights the case of Dysonica Plc. The report is divided into four tasks. Task one talks

about different costs of the business and how the business segregates these costs into heads like

fixed cost, variable cost and semi variable costs. It also talks about the case of absorption,

marginal and activity - based costing. Task two highlights the recommendation to the business in

the report on how they can reduce the cost and manage their operations efficiently. Task three

highlights the cash flow forecast of the business of Dysonica for 12 months upto 30th April 2023.

And task four gives a performance analysis of the business and how the business is working in

the industry with the help of these forecasted figures in the cash flow forecast of Dysonica.

TASK 1

Classify the costs according to their nature

Cost refers to any expense incurred by a company throughout the entire manufacturing

process for its services and goods. Simply described, it is the expenditure incurred by companies

on purchasing and selling things (Babones, Åberg, and Hodzi, 2020). When businesses

manufacture items, they suffer two sorts of expenses: variable and fixed costs.

Variable costs are any expenses that change based on how much a company produces and

sells. This implies that variable costs rise with rising output and fall with lower output. Some of

the most common types of variable expenses are labour, utility bills, commissions, and raw

materials.

Fixed expenses, on the other hand, are costs that remain constant regardless of how much

money a company makes. These expenses, such as rent, property tax, insurance, and

depreciation, are generally unrelated to a company's specific economic activity.

Business finance refers to the money and credit that a company uses. The financial

foundation of a corporation is critical. Finance is necessary for the acquisition of assets,

products, and raw materials, as well as other economic activities. Let's look at the definition of

business finance in more detail. The capital invested by the entrepreneur to start the firm is

insufficient to meet the company's financial obligations (Connolly, and Bank, 2018). As an

outcome, the entrepreneur must find a strategy to generate revenue. To keep the company

running, a thorough examination of financial demands and options for meeting those needs must

be conducted with the express goal of achieving good financial management. The following

report highlights the case of Dysonica Plc. The report is divided into four tasks. Task one talks

about different costs of the business and how the business segregates these costs into heads like

fixed cost, variable cost and semi variable costs. It also talks about the case of absorption,

marginal and activity - based costing. Task two highlights the recommendation to the business in

the report on how they can reduce the cost and manage their operations efficiently. Task three

highlights the cash flow forecast of the business of Dysonica for 12 months upto 30th April 2023.

And task four gives a performance analysis of the business and how the business is working in

the industry with the help of these forecasted figures in the cash flow forecast of Dysonica.

TASK 1

Classify the costs according to their nature

Cost refers to any expense incurred by a company throughout the entire manufacturing

process for its services and goods. Simply described, it is the expenditure incurred by companies

on purchasing and selling things (Babones, Åberg, and Hodzi, 2020). When businesses

manufacture items, they suffer two sorts of expenses: variable and fixed costs.

Variable costs are any expenses that change based on how much a company produces and

sells. This implies that variable costs rise with rising output and fall with lower output. Some of

the most common types of variable expenses are labour, utility bills, commissions, and raw

materials.

Fixed expenses, on the other hand, are costs that remain constant regardless of how much

money a company makes. These expenses, such as rent, property tax, insurance, and

depreciation, are generally unrelated to a company's specific economic activity.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

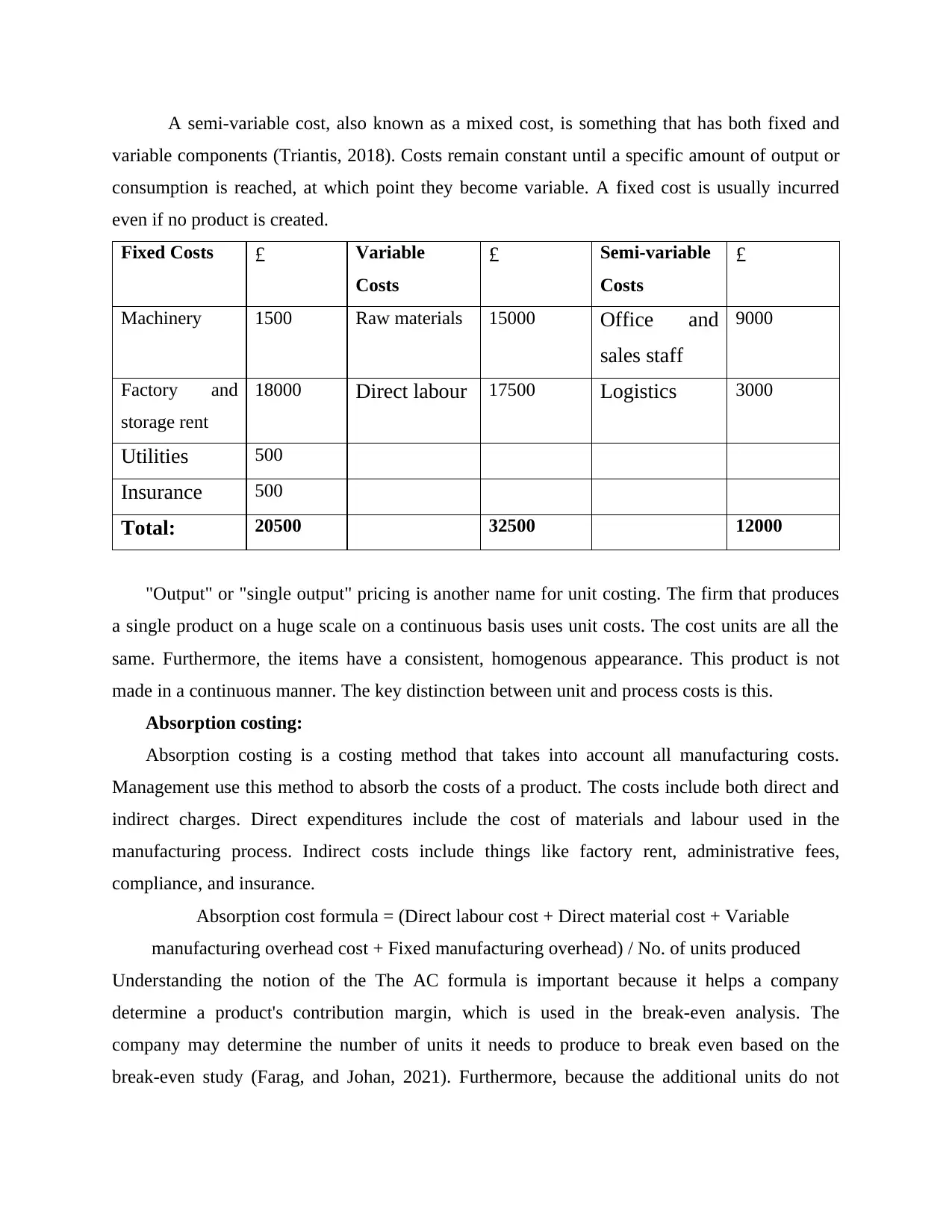

A semi-variable cost, also known as a mixed cost, is something that has both fixed and

variable components (Triantis, 2018). Costs remain constant until a specific amount of output or

consumption is reached, at which point they become variable. A fixed cost is usually incurred

even if no product is created.

Fixed Costs £ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

"Output" or "single output" pricing is another name for unit costing. The firm that produces

a single product on a huge scale on a continuous basis uses unit costs. The cost units are all the

same. Furthermore, the items have a consistent, homogenous appearance. This product is not

made in a continuous manner. The key distinction between unit and process costs is this.

Absorption costing:

Absorption costing is a costing method that takes into account all manufacturing costs.

Management use this method to absorb the costs of a product. The costs include both direct and

indirect charges. Direct expenditures include the cost of materials and labour used in the

manufacturing process. Indirect costs include things like factory rent, administrative fees,

compliance, and insurance.

Absorption cost formula = (Direct labour cost + Direct material cost + Variable

manufacturing overhead cost + Fixed manufacturing overhead) / No. of units produced

Understanding the notion of the The AC formula is important because it helps a company

determine a product's contribution margin, which is used in the break-even analysis. The

company may determine the number of units it needs to produce to break even based on the

break-even study (Farag, and Johan, 2021). Furthermore, because the additional units do not

variable components (Triantis, 2018). Costs remain constant until a specific amount of output or

consumption is reached, at which point they become variable. A fixed cost is usually incurred

even if no product is created.

Fixed Costs £ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory and

storage rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total: 20500 32500 12000

"Output" or "single output" pricing is another name for unit costing. The firm that produces

a single product on a huge scale on a continuous basis uses unit costs. The cost units are all the

same. Furthermore, the items have a consistent, homogenous appearance. This product is not

made in a continuous manner. The key distinction between unit and process costs is this.

Absorption costing:

Absorption costing is a costing method that takes into account all manufacturing costs.

Management use this method to absorb the costs of a product. The costs include both direct and

indirect charges. Direct expenditures include the cost of materials and labour used in the

manufacturing process. Indirect costs include things like factory rent, administrative fees,

compliance, and insurance.

Absorption cost formula = (Direct labour cost + Direct material cost + Variable

manufacturing overhead cost + Fixed manufacturing overhead) / No. of units produced

Understanding the notion of the The AC formula is important because it helps a company

determine a product's contribution margin, which is used in the break-even analysis. The

company may determine the number of units it needs to produce to break even based on the

break-even study (Farag, and Johan, 2021). Furthermore, because the additional units do not

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

incur an additional fixed cost, the use of AC in the manufacture of extra units boosts the

company's bottom line in terms of profit. Another advantage of AC is that it follows GAAP.

For example:

Assume XYZ Company is a bottle manufacturer. The following data is provided for one

manufacturing phase. The profits will be calculated using the absorption costing method.

The number of units produced equals 10,000. 9,000 units sold over the time = $ 50 unit price

Direct Labour = $ 5 Direct Material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

Marginal costing:

Marginal costing is the process of assigning variable production costs to goods. It's the

proportion of the change in cost to the change in output (Fodor, 2020).

There are two sorts of costs associated with a product: fixed and variable costs. Regardless

of industrial output, fixed expenses remain constant. Variable costs, on the other hand, fluctuate

in response to changes in manufacturing output.

Direct material, direct labour, and direct equipment expenses are all examples of variable

production costs. Some overheads, such as production utilities, can be classified as variable costs

of production.

Change in Cost/Change in Quantity = Marginal Cost

The changing level of variable expenses causes a cost change. Fixed costs will stay constant until

a particular level of production is reached (Schoenmaker, and Schramade, 2018).

For example:

Assume XYZ is a corporation that makes Bottles. For its manufacturing facilities, the

following information is provided.

Month 1 Units Produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in

Month 1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

As a result, the marginal cost per unit is $ 6 (30,000/5,000).

Activity-based costing:

company's bottom line in terms of profit. Another advantage of AC is that it follows GAAP.

For example:

Assume XYZ Company is a bottle manufacturer. The following data is provided for one

manufacturing phase. The profits will be calculated using the absorption costing method.

The number of units produced equals 10,000. 9,000 units sold over the time = $ 50 unit price

Direct Labour = $ 5 Direct Material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

Marginal costing:

Marginal costing is the process of assigning variable production costs to goods. It's the

proportion of the change in cost to the change in output (Fodor, 2020).

There are two sorts of costs associated with a product: fixed and variable costs. Regardless

of industrial output, fixed expenses remain constant. Variable costs, on the other hand, fluctuate

in response to changes in manufacturing output.

Direct material, direct labour, and direct equipment expenses are all examples of variable

production costs. Some overheads, such as production utilities, can be classified as variable costs

of production.

Change in Cost/Change in Quantity = Marginal Cost

The changing level of variable expenses causes a cost change. Fixed costs will stay constant until

a particular level of production is reached (Schoenmaker, and Schramade, 2018).

For example:

Assume XYZ is a corporation that makes Bottles. For its manufacturing facilities, the

following information is provided.

Month 1 Units Produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in

Month 1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

As a result, the marginal cost per unit is $ 6 (30,000/5,000).

Activity-based costing:

Activity-based costing is a more exact method of calculating a product's or service's cost,

resulting in more precise price decisions. It raises managers' knowledge of overheads and cost

drivers by revealing inefficient and non-value-adding procedures that may be decreased or

eliminated (Anglemark, and John, 2018). ABC enables a more thorough evaluation of

operational costs in order to find more efficient ways to distribute and minimise overheads. It

also enables for more precise product and customer profitability measurement. It promotes the

use of performance management tools like as scorecards and the pursuit of continual

improvement.

It is a form of cost allocation method in which all types of corporate costs are identified and

allocated to costs for products based on real consumption.

In three ways, it will enhance the costing process. It will initially expand the number of cost

pools, which will then be used to allocate those overhead charges (Xu, Cheng, Wang, and Yang,

2020). As a result, rather than aggregating these costs into a single pool for the entire business,

they are pooled per activity. Second, rather of depending on volume metrics like direct labour

costs or machine hours, it will develop new bases to allocate these overhead costs to products

based on these activities, which will produce expenses. Finally, these operations are assigned a

cost.

TASK 2

Provide recommendation and cost reduction strategy

From the above different costing techniques, it is recommended to the Dysonica Plc to use

activity based costing or marginal costing as it would help the business to manage their costs

which might arise from different processes (Ziegler, and et.al., 2021). This helps the business to

segregate the costs according to their process and check which one is incurring most of the costs

and guide the management to reduce the cost and manage its processes accordingly. Activity

based costing is one stop solution for the business to control its costs and it will help the business

to define costs as they are being incurred and not combine them with other costs. Actual cost

head is known in such way and businesses can focus on effectively managing that particular cost

head other than focusing on other rigid forces. Because overhead expenses are segregated and

organised into pools based on the number of activities, the allocation of overhead costs is more

resulting in more precise price decisions. It raises managers' knowledge of overheads and cost

drivers by revealing inefficient and non-value-adding procedures that may be decreased or

eliminated (Anglemark, and John, 2018). ABC enables a more thorough evaluation of

operational costs in order to find more efficient ways to distribute and minimise overheads. It

also enables for more precise product and customer profitability measurement. It promotes the

use of performance management tools like as scorecards and the pursuit of continual

improvement.

It is a form of cost allocation method in which all types of corporate costs are identified and

allocated to costs for products based on real consumption.

In three ways, it will enhance the costing process. It will initially expand the number of cost

pools, which will then be used to allocate those overhead charges (Xu, Cheng, Wang, and Yang,

2020). As a result, rather than aggregating these costs into a single pool for the entire business,

they are pooled per activity. Second, rather of depending on volume metrics like direct labour

costs or machine hours, it will develop new bases to allocate these overhead costs to products

based on these activities, which will produce expenses. Finally, these operations are assigned a

cost.

TASK 2

Provide recommendation and cost reduction strategy

From the above different costing techniques, it is recommended to the Dysonica Plc to use

activity based costing or marginal costing as it would help the business to manage their costs

which might arise from different processes (Ziegler, and et.al., 2021). This helps the business to

segregate the costs according to their process and check which one is incurring most of the costs

and guide the management to reduce the cost and manage its processes accordingly. Activity

based costing is one stop solution for the business to control its costs and it will help the business

to define costs as they are being incurred and not combine them with other costs. Actual cost

head is known in such way and businesses can focus on effectively managing that particular cost

head other than focusing on other rigid forces. Because overhead expenses are segregated and

organised into pools based on the number of activities, the allocation of overhead costs is more

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

exact and precise. To make things easier, rather than estimating the company's indirect

expenditures by adding all costs together, ABC groups costs by activity.

Previously untraceable expenses, like as depreciation, are traced to specific activities using

activity-based costing.

By moving overhead expenses from high-volume items to low-volume products, the ABC

technique can affect the unit cost of low-volume products.

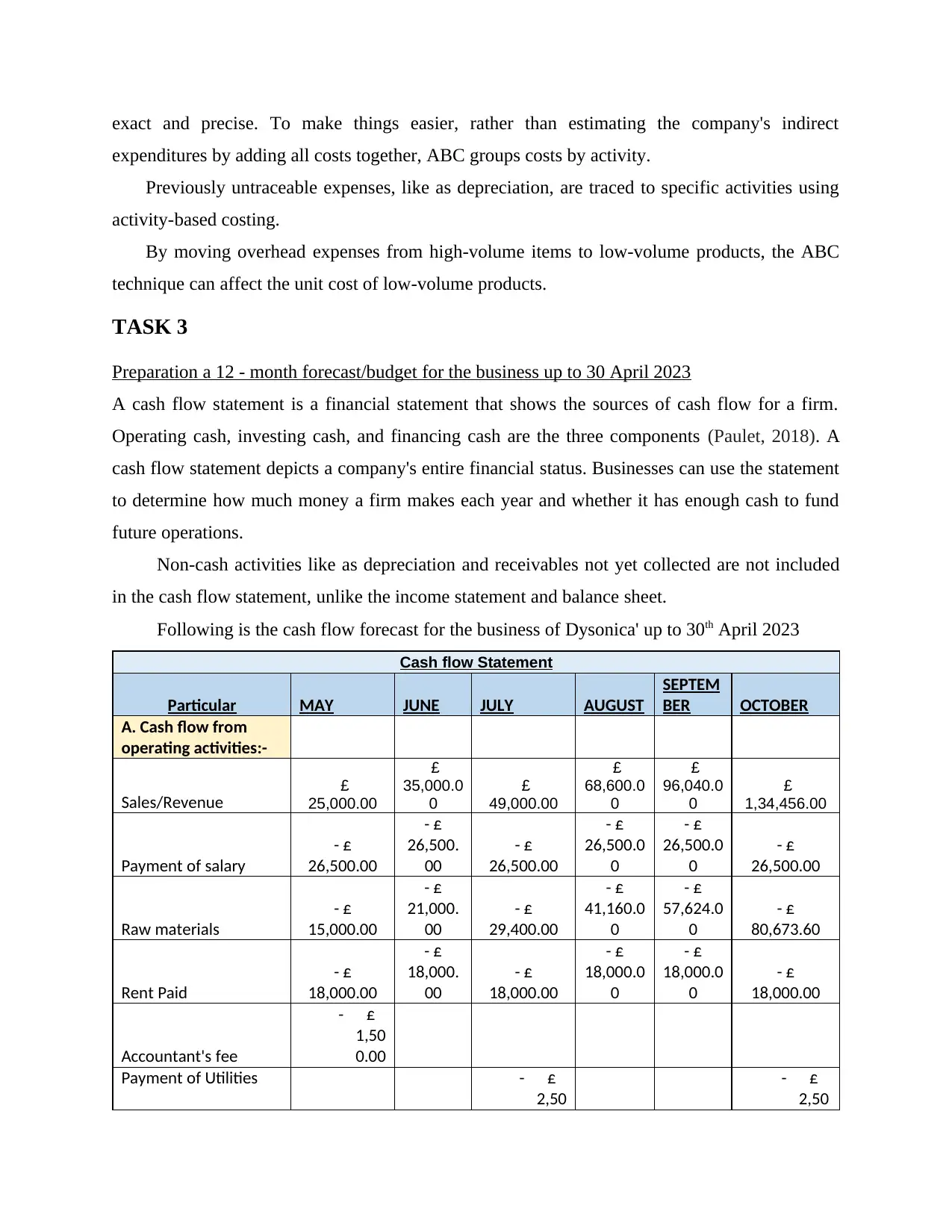

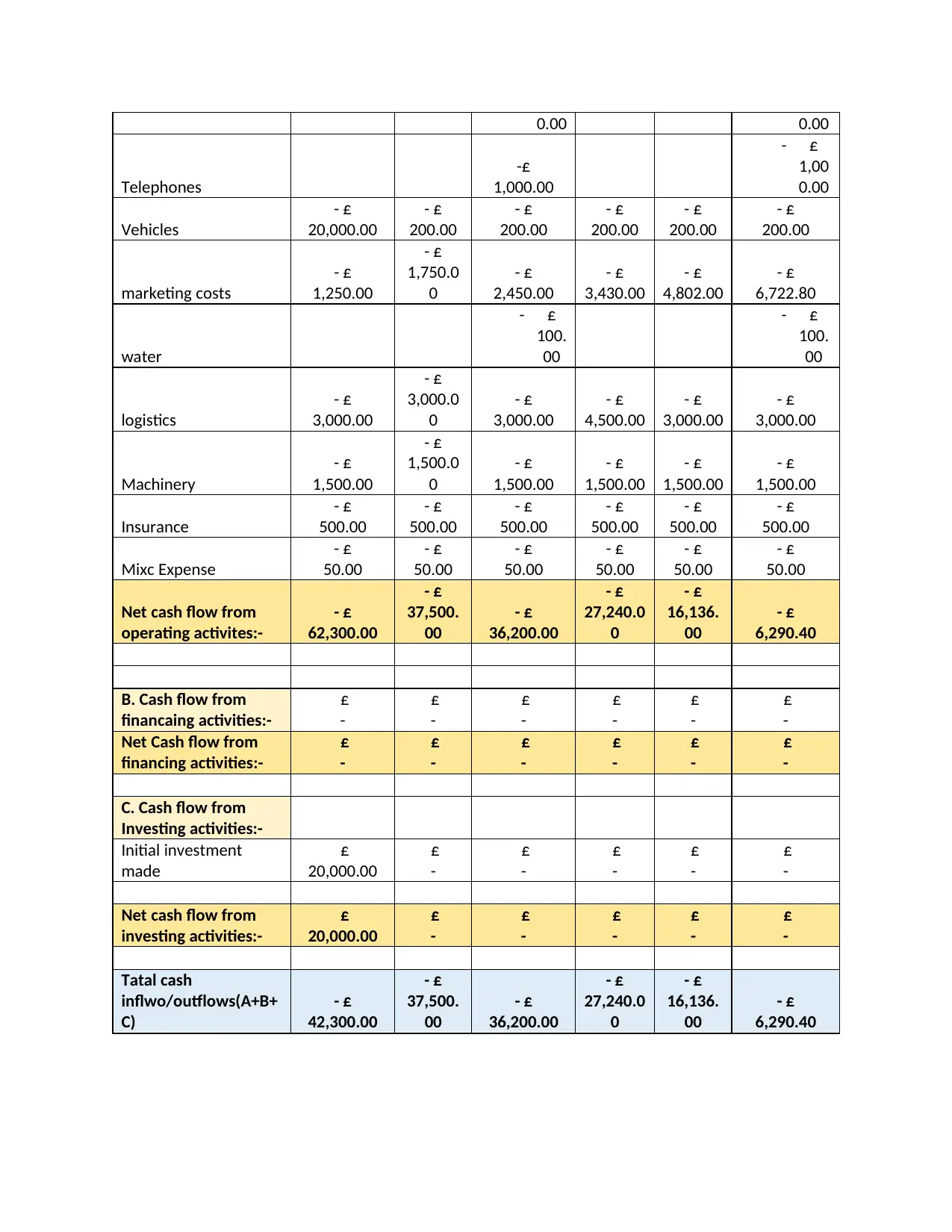

TASK 3

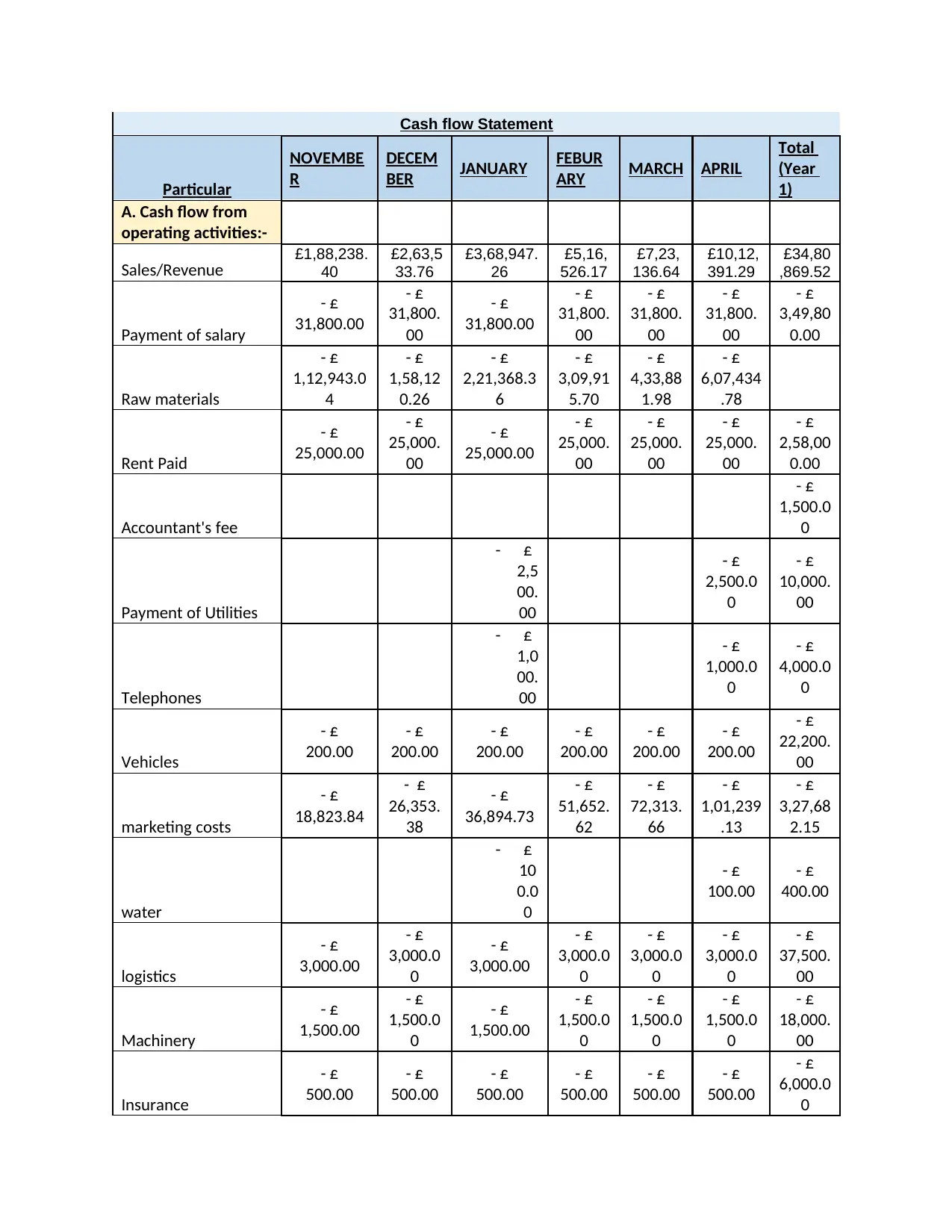

Preparation a 12 - month forecast/budget for the business up to 30 April 2023

A cash flow statement is a financial statement that shows the sources of cash flow for a firm.

Operating cash, investing cash, and financing cash are the three components (Paulet, 2018). A

cash flow statement depicts a company's entire financial status. Businesses can use the statement

to determine how much money a firm makes each year and whether it has enough cash to fund

future operations.

Non-cash activities like as depreciation and receivables not yet collected are not included

in the cash flow statement, unlike the income statement and balance sheet.

Following is the cash flow forecast for the business of Dysonica' up to 30th April 2023

Cash flow Statement

Particular MAY JUNE JULY AUGUST

SEPTEM

BER OCTOBER

A. Cash flow from

operating activities:-

Sales/Revenue £

25,000.00

£

35,000.0

0

£

49,000.00

£

68,600.0

0

£

96,040.0

0

£

1,34,456.00

Payment of salary

- £

26,500.00

- £

26,500.

00

- £

26,500.00

- £

26,500.0

0

- £

26,500.0

0

- £

26,500.00

Raw materials

- £

15,000.00

- £

21,000.

00

- £

29,400.00

- £

41,160.0

0

- £

57,624.0

0

- £

80,673.60

Rent Paid

- £

18,000.00

- £

18,000.

00

- £

18,000.00

- £

18,000.0

0

- £

18,000.0

0

- £

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities - £

2,50

- £

2,50

expenditures by adding all costs together, ABC groups costs by activity.

Previously untraceable expenses, like as depreciation, are traced to specific activities using

activity-based costing.

By moving overhead expenses from high-volume items to low-volume products, the ABC

technique can affect the unit cost of low-volume products.

TASK 3

Preparation a 12 - month forecast/budget for the business up to 30 April 2023

A cash flow statement is a financial statement that shows the sources of cash flow for a firm.

Operating cash, investing cash, and financing cash are the three components (Paulet, 2018). A

cash flow statement depicts a company's entire financial status. Businesses can use the statement

to determine how much money a firm makes each year and whether it has enough cash to fund

future operations.

Non-cash activities like as depreciation and receivables not yet collected are not included

in the cash flow statement, unlike the income statement and balance sheet.

Following is the cash flow forecast for the business of Dysonica' up to 30th April 2023

Cash flow Statement

Particular MAY JUNE JULY AUGUST

SEPTEM

BER OCTOBER

A. Cash flow from

operating activities:-

Sales/Revenue £

25,000.00

£

35,000.0

0

£

49,000.00

£

68,600.0

0

£

96,040.0

0

£

1,34,456.00

Payment of salary

- £

26,500.00

- £

26,500.

00

- £

26,500.00

- £

26,500.0

0

- £

26,500.0

0

- £

26,500.00

Raw materials

- £

15,000.00

- £

21,000.

00

- £

29,400.00

- £

41,160.0

0

- £

57,624.0

0

- £

80,673.60

Rent Paid

- £

18,000.00

- £

18,000.

00

- £

18,000.00

- £

18,000.0

0

- £

18,000.0

0

- £

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities - £

2,50

- £

2,50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

0.00 0.00

Telephones

-£

1,000.00

- £

1,00

0.00

Vehicles

- £

20,000.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

marketing costs

- £

1,250.00

- £

1,750.0

0

- £

2,450.00

- £

3,430.00

- £

4,802.00

- £

6,722.80

water

- £

100.

00

- £

100.

00

logistics

- £

3,000.00

- £

3,000.0

0

- £

3,000.00

- £

4,500.00

- £

3,000.00

- £

3,000.00

Machinery

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

Mixc Expense

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

Net cash flow from

operating activites:-

- £

62,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

B. Cash flow from

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Net cash flow from

investing activities:-

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Tatal cash

inflwo/outflows(A+B+

C)

- £

42,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

Telephones

-£

1,000.00

- £

1,00

0.00

Vehicles

- £

20,000.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

marketing costs

- £

1,250.00

- £

1,750.0

0

- £

2,450.00

- £

3,430.00

- £

4,802.00

- £

6,722.80

water

- £

100.

00

- £

100.

00

logistics

- £

3,000.00

- £

3,000.0

0

- £

3,000.00

- £

4,500.00

- £

3,000.00

- £

3,000.00

Machinery

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

- £

1,500.00

- £

1,500.00

- £

1,500.00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

Mixc Expense

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

Net cash flow from

operating activites:-

- £

62,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

B. Cash flow from

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Net cash flow from

investing activities:-

£

20,000.00

£

-

£

-

£

-

£

-

£

-

Tatal cash

inflwo/outflows(A+B+

C)

- £

42,300.00

- £

37,500.

00

- £

36,200.00

- £

27,240.0

0

- £

16,136.

00

- £

6,290.40

Cash flow Statement

Particular

NOVEMBE

R

DECEM

BER JANUARY FEBUR

ARY MARCH APRIL

Total

(Year

1)

A. Cash flow from

operating activities:-

Sales/Revenue £1,88,238.

40

£2,63,5

33.76

£3,68,947.

26

£5,16,

526.17

£7,23,

136.64

£10,12,

391.29

£34,80

,869.52

Payment of salary

- £

31,800.00

- £

31,800.

00

- £

31,800.00

- £

31,800.

00

- £

31,800.

00

- £

31,800.

00

- £

3,49,80

0.00

Raw materials

- £

1,12,943.0

4

- £

1,58,12

0.26

- £

2,21,368.3

6

- £

3,09,91

5.70

- £

4,33,88

1.98

- £

6,07,434

.78

Rent Paid

- £

25,000.00

- £

25,000.

00

- £

25,000.00

- £

25,000.

00

- £

25,000.

00

- £

25,000.

00

- £

2,58,00

0.00

Accountant's fee

- £

1,500.0

0

Payment of Utilities

- £

2,5

00.

00

- £

2,500.0

0

- £

10,000.

00

Telephones

- £

1,0

00.

00

- £

1,000.0

0

- £

4,000.0

0

Vehicles

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

22,200.

00

marketing costs

- £

18,823.84

- £

26,353.

38

- £

36,894.73

- £

51,652.

62

- £

72,313.

66

- £

1,01,239

.13

- £

3,27,68

2.15

water

- £

10

0.0

0

- £

100.00

- £

400.00

logistics

- £

3,000.00

- £

3,000.0

0

- £

3,000.00

- £

3,000.0

0

- £

3,000.0

0

- £

3,000.0

0

- £

37,500.

00

Machinery

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

- £

1,500.0

0

- £

1,500.0

0

- £

1,500.0

0

- £

18,000.

00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

6,000.0

0

Particular

NOVEMBE

R

DECEM

BER JANUARY FEBUR

ARY MARCH APRIL

Total

(Year

1)

A. Cash flow from

operating activities:-

Sales/Revenue £1,88,238.

40

£2,63,5

33.76

£3,68,947.

26

£5,16,

526.17

£7,23,

136.64

£10,12,

391.29

£34,80

,869.52

Payment of salary

- £

31,800.00

- £

31,800.

00

- £

31,800.00

- £

31,800.

00

- £

31,800.

00

- £

31,800.

00

- £

3,49,80

0.00

Raw materials

- £

1,12,943.0

4

- £

1,58,12

0.26

- £

2,21,368.3

6

- £

3,09,91

5.70

- £

4,33,88

1.98

- £

6,07,434

.78

Rent Paid

- £

25,000.00

- £

25,000.

00

- £

25,000.00

- £

25,000.

00

- £

25,000.

00

- £

25,000.

00

- £

2,58,00

0.00

Accountant's fee

- £

1,500.0

0

Payment of Utilities

- £

2,5

00.

00

- £

2,500.0

0

- £

10,000.

00

Telephones

- £

1,0

00.

00

- £

1,000.0

0

- £

4,000.0

0

Vehicles

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

200.00

- £

22,200.

00

marketing costs

- £

18,823.84

- £

26,353.

38

- £

36,894.73

- £

51,652.

62

- £

72,313.

66

- £

1,01,239

.13

- £

3,27,68

2.15

water

- £

10

0.0

0

- £

100.00

- £

400.00

logistics

- £

3,000.00

- £

3,000.0

0

- £

3,000.00

- £

3,000.0

0

- £

3,000.0

0

- £

3,000.0

0

- £

37,500.

00

Machinery

- £

1,500.00

- £

1,500.0

0

- £

1,500.00

- £

1,500.0

0

- £

1,500.0

0

- £

1,500.0

0

- £

18,000.

00

Insurance

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

500.00

- £

6,000.0

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Mixc Expense

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

600.00

Net cash flow from

operating activites:-

- £

5,5

78.

48

£

17,010.

13

£

45,034.18

£

92,907.

85

£

1,54,89

0.99

£

2,38,06

7.39

£

24,45,1

87.37

B. Cash flow from

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.

00

Net cash flow from

investing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.

00

Tatal cash

inflwo/outflows(A+B

+C)

-£

5,578.48

£

17,010.

13

£

45,034.18

£

92,907.

85

£

1,54,89

0.99

£

2,38,06

7.39

£

24,65,1

87.37

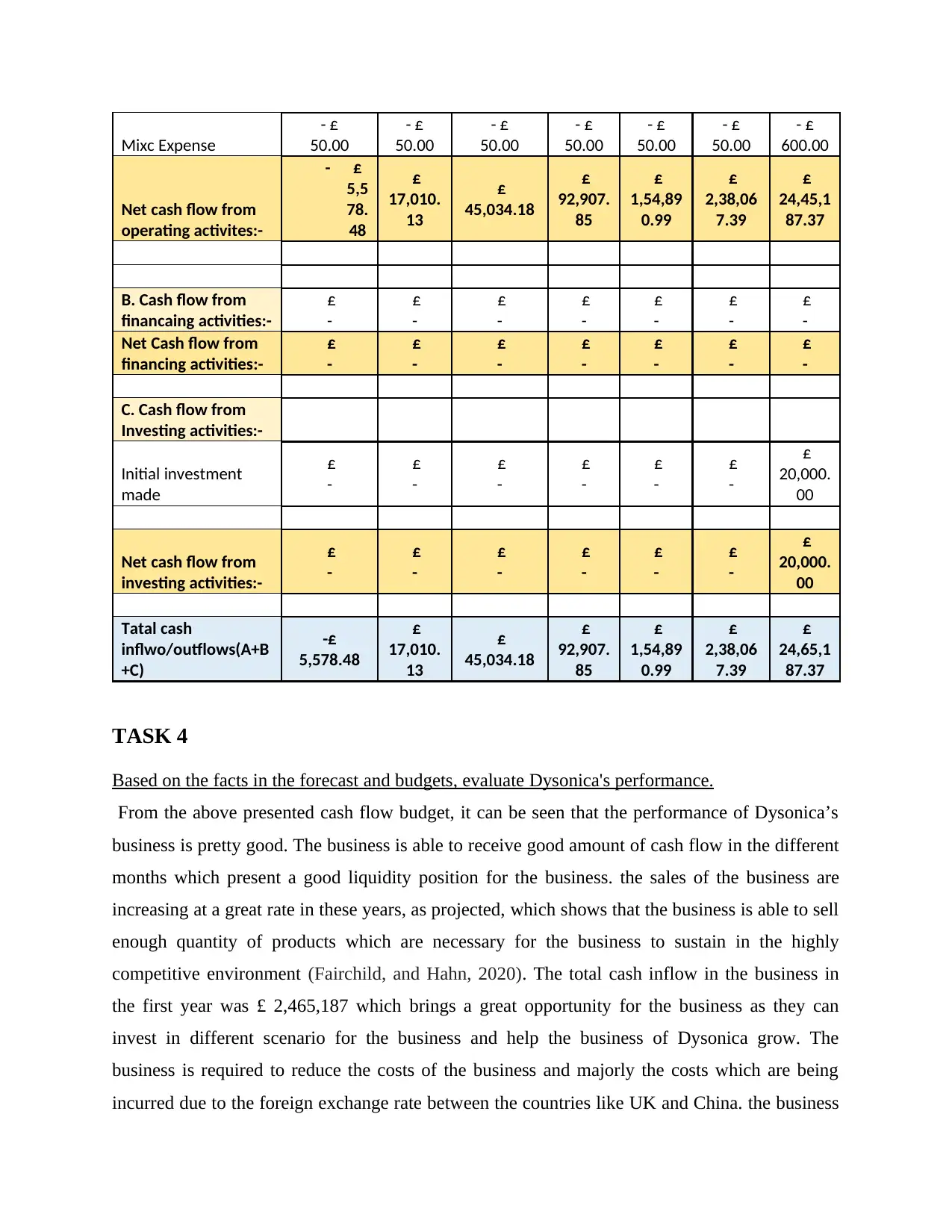

TASK 4

Based on the facts in the forecast and budgets, evaluate Dysonica's performance.

From the above presented cash flow budget, it can be seen that the performance of Dysonica’s

business is pretty good. The business is able to receive good amount of cash flow in the different

months which present a good liquidity position for the business. the sales of the business are

increasing at a great rate in these years, as projected, which shows that the business is able to sell

enough quantity of products which are necessary for the business to sustain in the highly

competitive environment (Fairchild, and Hahn, 2020). The total cash inflow in the business in

the first year was £ 2,465,187 which brings a great opportunity for the business as they can

invest in different scenario for the business and help the business of Dysonica grow. The

business is required to reduce the costs of the business and majorly the costs which are being

incurred due to the foreign exchange rate between the countries like UK and China. the business

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

50.00

- £

600.00

Net cash flow from

operating activites:-

- £

5,5

78.

48

£

17,010.

13

£

45,034.18

£

92,907.

85

£

1,54,89

0.99

£

2,38,06

7.39

£

24,45,1

87.37

B. Cash flow from

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.

00

Net cash flow from

investing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.

00

Tatal cash

inflwo/outflows(A+B

+C)

-£

5,578.48

£

17,010.

13

£

45,034.18

£

92,907.

85

£

1,54,89

0.99

£

2,38,06

7.39

£

24,65,1

87.37

TASK 4

Based on the facts in the forecast and budgets, evaluate Dysonica's performance.

From the above presented cash flow budget, it can be seen that the performance of Dysonica’s

business is pretty good. The business is able to receive good amount of cash flow in the different

months which present a good liquidity position for the business. the sales of the business are

increasing at a great rate in these years, as projected, which shows that the business is able to sell

enough quantity of products which are necessary for the business to sustain in the highly

competitive environment (Fairchild, and Hahn, 2020). The total cash inflow in the business in

the first year was £ 2,465,187 which brings a great opportunity for the business as they can

invest in different scenario for the business and help the business of Dysonica grow. The

business is required to reduce the costs of the business and majorly the costs which are being

incurred due to the foreign exchange rate between the countries like UK and China. the business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

may make use of hedging techniques which measure the trade at a predetermined rate and this

would help the business to control the cost which is related to this very aspect of the business. it

can be seen that the business is having negative cash inflows which means business saw a cash

outflow in the first six to seven months of the business which shows that the business is required

to either rise their sales or reduce the costs (Motta, 2020). The cash outflow is indirectly

affecting the liquidity position of the business which is a major condition to be held by any

business working in a competitive industry and globally. The reduction in costs can be seen by

using a better source of inputs and evaluating different projects in hand and which one is

providing losses in the hands of business.

CONCLUSION

From the above - mentioned report, it can be concluded that, business finance and management

of these finances is a major and critical factor in the success of the business. Business like

Dysonica, which are working internationally face tremendous competition. They need to reduce

the different costs that are being faced by the business to hold the competitive advantage in the

highly competitive industry. The cash flow forecasts are a great tool to measure the inflow or

outflow of cash in or from the business at the end of a specified period and the business can

create its own budget with that. Marginal and activity based costing are two of the best costing

technique which can be used by the business of Dysonica to reduce the chances of error and

count every cost which is required to be taken. It also helps the business to reduce the costs using

the cost pool and cost head which are not adding to the major profits of the business.

would help the business to control the cost which is related to this very aspect of the business. it

can be seen that the business is having negative cash inflows which means business saw a cash

outflow in the first six to seven months of the business which shows that the business is required

to either rise their sales or reduce the costs (Motta, 2020). The cash outflow is indirectly

affecting the liquidity position of the business which is a major condition to be held by any

business working in a competitive industry and globally. The reduction in costs can be seen by

using a better source of inputs and evaluating different projects in hand and which one is

providing losses in the hands of business.

CONCLUSION

From the above - mentioned report, it can be concluded that, business finance and management

of these finances is a major and critical factor in the success of the business. Business like

Dysonica, which are working internationally face tremendous competition. They need to reduce

the different costs that are being faced by the business to hold the competitive advantage in the

highly competitive industry. The cash flow forecasts are a great tool to measure the inflow or

outflow of cash in or from the business at the end of a specified period and the business can

create its own budget with that. Marginal and activity based costing are two of the best costing

technique which can be used by the business of Dysonica to reduce the chances of error and

count every cost which is required to be taken. It also helps the business to reduce the costs using

the cost pool and cost head which are not adding to the major profits of the business.

REFERENCES

Books and Journals

Connolly, E. and Bank, J., 2018. Access to small business finance. RBA Bulletin, September,

pp.1-14.

Babones, S., Åberg, J.H. and Hodzi, O., 2020. China's role in global development finance: China

challenge or business as usual?. Global Policy, 11(3), pp.326-335.

Triantis, J.E., 2018. Project finance for business development. John Wiley & Sons.

Farag, H. and Johan, S., 2021. How alternative finance informs central themes in corporate

finance. Journal of Corporate Finance, 67, p.101879.

Fodor, P., 2020. The Business of State: Ottoman Finance Administration and Ruling Elites in

Transition (1580s–1615) (Vol. 28). Walter de Gruyter GmbH & Co KG.

Anglemark, L. and John, A., 2018. The use of English-language business and finance terms in

European languages. International Journal of Business Communication, 55(3), pp.406-

440.

Paulet, E., 2018. Banking liquidity regulation: Impact on their business model and on

entrepreneurial finance in Europe. Strategic Change, 27(4), pp.339-350.

Fairchild, C. and Hahn, W., 2020. Accounting and finance majors outperform other majors on

the major field test in business and the Comprehensive Business Exam: An analysis of

exam performance drivers. Journal of Education for Business, 95(6), pp.345-350.

Motta, V., 2020. Lack of access to external finance and SME labor productivity: does project

quality matter?. Small Business Economics, 54(1), pp.119-134.

Ziegler, T., and et.al., 2021. The global alternative finance market benchmarking

report. Available at SSRN 3771509.

Xu, Z., Cheng, X., Wang, K. and Yang, S., 2020. Analysis of the environmental trend of network

finance and its influence on tradition

Schoenmaker, D. and Schramade, W., 2018. Principles of sustainable finance. Oxford University

Press.

Books and Journals

Connolly, E. and Bank, J., 2018. Access to small business finance. RBA Bulletin, September,

pp.1-14.

Babones, S., Åberg, J.H. and Hodzi, O., 2020. China's role in global development finance: China

challenge or business as usual?. Global Policy, 11(3), pp.326-335.

Triantis, J.E., 2018. Project finance for business development. John Wiley & Sons.

Farag, H. and Johan, S., 2021. How alternative finance informs central themes in corporate

finance. Journal of Corporate Finance, 67, p.101879.

Fodor, P., 2020. The Business of State: Ottoman Finance Administration and Ruling Elites in

Transition (1580s–1615) (Vol. 28). Walter de Gruyter GmbH & Co KG.

Anglemark, L. and John, A., 2018. The use of English-language business and finance terms in

European languages. International Journal of Business Communication, 55(3), pp.406-

440.

Paulet, E., 2018. Banking liquidity regulation: Impact on their business model and on

entrepreneurial finance in Europe. Strategic Change, 27(4), pp.339-350.

Fairchild, C. and Hahn, W., 2020. Accounting and finance majors outperform other majors on

the major field test in business and the Comprehensive Business Exam: An analysis of

exam performance drivers. Journal of Education for Business, 95(6), pp.345-350.

Motta, V., 2020. Lack of access to external finance and SME labor productivity: does project

quality matter?. Small Business Economics, 54(1), pp.119-134.

Ziegler, T., and et.al., 2021. The global alternative finance market benchmarking

report. Available at SSRN 3771509.

Xu, Z., Cheng, X., Wang, K. and Yang, S., 2020. Analysis of the environmental trend of network

finance and its influence on tradition

Schoenmaker, D. and Schramade, W., 2018. Principles of sustainable finance. Oxford University

Press.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.