Business Finance: Cost Analysis, Forecasting and Budgeting at Dysonica

VerifiedAdded on 2023/06/11

|17

|5497

|85

Case Study

AI Summary

This case study provides a detailed examination of Dysonica Plc's financial operations, focusing on cost analysis, budgeting, and forecasting. Task 1 involves classifying costs as fixed, variable, or semi-variable, which includes raw materials, machinery, factory rent, direct labor, utilities, office staff, insurance, and logistics. Task 2 suggests plans to reduce organizational costs, emphasizing the use of activity-based costing (ABC) to identify and manage expenses effectively. Task 3 develops a 12-month forecasting budget for the business up to April 30, 2022. Finally, Task 4 evaluates Dysonica's performance against the budget. The report concludes by highlighting the importance of effective financial management in achieving organizational goals. Desklib offers a variety of resources, including past papers and solved assignments, to assist students in understanding and mastering business finance concepts.

BUSINESS FINANCE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

Find out expenses according to their nature. ..............................................................................3

TASK- 2 ..........................................................................................................................................7

Suggest some plans to reduce the cost of the organization.........................................................7

TASK 3..........................................................................................................................................9

Development of a 12 month forecasting/ budget being prepared for the business up to 30 April

2022.............................................................................................................................................9

TASK 4..........................................................................................................................................13

Forecast and budget evaluation of the Dysonica ......................................................................13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

Find out expenses according to their nature. ..............................................................................3

TASK- 2 ..........................................................................................................................................7

Suggest some plans to reduce the cost of the organization.........................................................7

TASK 3..........................................................................................................................................9

Development of a 12 month forecasting/ budget being prepared for the business up to 30 April

2022.............................................................................................................................................9

TASK 4..........................................................................................................................................13

Forecast and budget evaluation of the Dysonica ......................................................................13

CONCLUSION .............................................................................................................................14

REFERENCES..............................................................................................................................16

INTRODUCTION

The report prepared as under takes in account the funds that are being generated,

arranged and managed in a firm, company, enterprise or business for achieving and

accomplishing their goals and objectives as well. It can also be explained as the assets which are

being acquired by companies in relation to start a organisation. Credit subsidiaries and capital

assets which are being invested into a enterprise that are included in such assets(Battisti and

et.al., 2021). The money can be put for attracting resources, purchasing raw materials and

making commodities for the company related operative system. When a firm first begin with

operational work, the funds that are available are lesser not sufficient for finding solutions

related to problems which are rising. As a outcome, in relation to addressing their requirements

and meeting their needs as well. Business companies must be taking care of a larger number of

elements in order to generating income or profits. The examination of monetary related needs

and requirements and the results which must be cross checked in a standard based approach,

which would be allowing for the development of monetary based management plans, policies

and strategies as well. In context study of Dysonica Plc is the subject related research reports. It

carries and contains four exercises, at first place it covers the expense related element of a

company and how they have been bifurcated. The next project would be handling

recommendations for the management which will aid the chief in lessening their rates and

expenses as well(Chen and et.al., 2020). The third sector contains Dysonica PLc's revenue

forecasted till April 30, 2023. Hence, the final plan evaluates the company's achievements, and

triumphs as well as in what ways it would be operating in that certain industry. The decision can

be made would be based on the gauged values in Dysonica Plc's income.

TASK 1

Find out expenses according to their nature.

The term "expense" is useful when put together and would be supplying commodities and

services. Cost is very critical at such stages where the manufacturing and production related

cycle, by procurement of unprocessed material for completion an companies finished

commodities. Essentially expense is the quantity of monetary terms which would be used to help

in paying the price of production. There are various several kind of expenses which would be

The report prepared as under takes in account the funds that are being generated,

arranged and managed in a firm, company, enterprise or business for achieving and

accomplishing their goals and objectives as well. It can also be explained as the assets which are

being acquired by companies in relation to start a organisation. Credit subsidiaries and capital

assets which are being invested into a enterprise that are included in such assets(Battisti and

et.al., 2021). The money can be put for attracting resources, purchasing raw materials and

making commodities for the company related operative system. When a firm first begin with

operational work, the funds that are available are lesser not sufficient for finding solutions

related to problems which are rising. As a outcome, in relation to addressing their requirements

and meeting their needs as well. Business companies must be taking care of a larger number of

elements in order to generating income or profits. The examination of monetary related needs

and requirements and the results which must be cross checked in a standard based approach,

which would be allowing for the development of monetary based management plans, policies

and strategies as well. In context study of Dysonica Plc is the subject related research reports. It

carries and contains four exercises, at first place it covers the expense related element of a

company and how they have been bifurcated. The next project would be handling

recommendations for the management which will aid the chief in lessening their rates and

expenses as well(Chen and et.al., 2020). The third sector contains Dysonica PLc's revenue

forecasted till April 30, 2023. Hence, the final plan evaluates the company's achievements, and

triumphs as well as in what ways it would be operating in that certain industry. The decision can

be made would be based on the gauged values in Dysonica Plc's income.

TASK 1

Find out expenses according to their nature.

The term "expense" is useful when put together and would be supplying commodities and

services. Cost is very critical at such stages where the manufacturing and production related

cycle, by procurement of unprocessed material for completion an companies finished

commodities. Essentially expense is the quantity of monetary terms which would be used to help

in paying the price of production. There are various several kind of expenses which would be

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

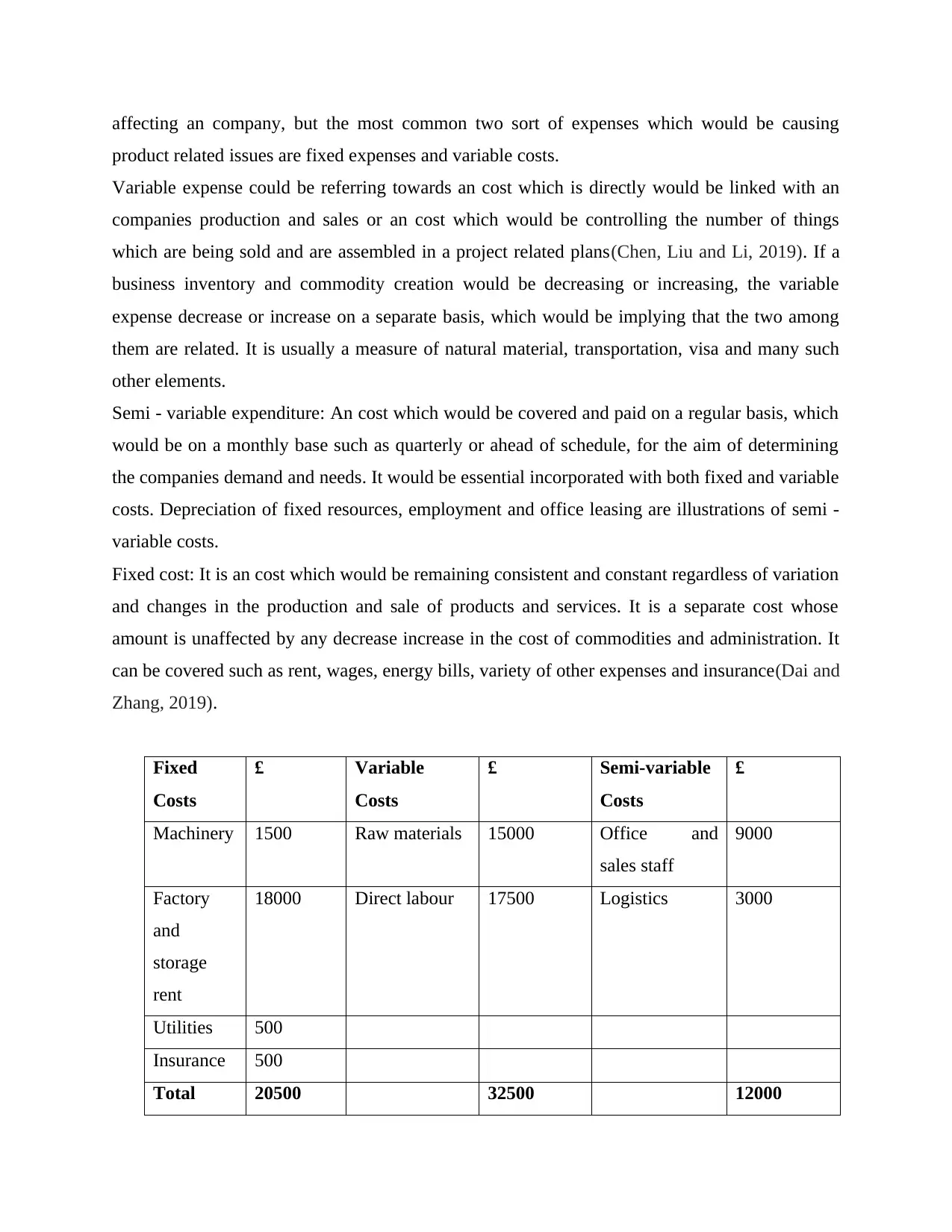

affecting an company, but the most common two sort of expenses which would be causing

product related issues are fixed expenses and variable costs.

Variable expense could be referring towards an cost which is directly would be linked with an

companies production and sales or an cost which would be controlling the number of things

which are being sold and are assembled in a project related plans(Chen, Liu and Li, 2019). If a

business inventory and commodity creation would be decreasing or increasing, the variable

expense decrease or increase on a separate basis, which would be implying that the two among

them are related. It is usually a measure of natural material, transportation, visa and many such

other elements.

Semi - variable expenditure: An cost which would be covered and paid on a regular basis, which

would be on a monthly base such as quarterly or ahead of schedule, for the aim of determining

the companies demand and needs. It would be essential incorporated with both fixed and variable

costs. Depreciation of fixed resources, employment and office leasing are illustrations of semi -

variable costs.

Fixed cost: It is an cost which would be remaining consistent and constant regardless of variation

and changes in the production and sale of products and services. It is a separate cost whose

amount is unaffected by any decrease increase in the cost of commodities and administration. It

can be covered such as rent, wages, energy bills, variety of other expenses and insurance(Dai and

Zhang, 2019).

Fixed

Costs

£ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory

and

storage

rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total 20500 32500 12000

product related issues are fixed expenses and variable costs.

Variable expense could be referring towards an cost which is directly would be linked with an

companies production and sales or an cost which would be controlling the number of things

which are being sold and are assembled in a project related plans(Chen, Liu and Li, 2019). If a

business inventory and commodity creation would be decreasing or increasing, the variable

expense decrease or increase on a separate basis, which would be implying that the two among

them are related. It is usually a measure of natural material, transportation, visa and many such

other elements.

Semi - variable expenditure: An cost which would be covered and paid on a regular basis, which

would be on a monthly base such as quarterly or ahead of schedule, for the aim of determining

the companies demand and needs. It would be essential incorporated with both fixed and variable

costs. Depreciation of fixed resources, employment and office leasing are illustrations of semi -

variable costs.

Fixed cost: It is an cost which would be remaining consistent and constant regardless of variation

and changes in the production and sale of products and services. It is a separate cost whose

amount is unaffected by any decrease increase in the cost of commodities and administration. It

can be covered such as rent, wages, energy bills, variety of other expenses and insurance(Dai and

Zhang, 2019).

Fixed

Costs

£ Variable

Costs

£ Semi-variable

Costs

£

Machinery 1500 Raw materials 15000 Office and

sales staff

9000

Factory

and

storage

rent

18000 Direct labour 17500 Logistics 3000

Utilities 500

Insurance 500

Total 20500 32500 12000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The cost which is related to production of a comparable thing in a larger volume on a regular

base is explained as unit expense. The cost can be referred such as assembled material of single

unit. It is also explained as the expense of item being supplied, cycle expense could be referred

to accounting which results in indistinguishable or identical unit of income. The following are

the variation between interaction expense and unit as well.

Absorption Costing: It is an cost which can be covered with the help of costing approach which

account and dissect for all assembly related costs(Hariyani, Ratnawati and Rahmiyati, 2021).

The majority of the time consumed, this element is used by companies to internalise the expense

of item. In simpler terms, the cost is at . times related to as 'full cost. Direct labour, direct

material, variable created upward and fixed assembly upward are four sort of retentment costing

elements. The expense counts both indirect and direct cost. The most necessary element of direct

expenses are the quantity of raw materials which are being adapted and used and the time which

is being spent constructing the good. Office plant rentals, expense, security charge and protection

as well which can be included in creation of indirect expense.

Calculation of Absorption costing:

Formula = (Direct work cost + Direct material expense + Variable assembling upward expense +

Fixed assembling upward) / No. of units created

It is mostly used in the section of assembled organisations in aiding the organisation in

computation of cost of commodities so that the business would be examining the best expense

approaches for the quantity as well as managing the expense of goods.

For example:

Accepting which the ABC corporation is a fan producer. One assembly step would be

accommodating the reliable data and information(Israel, Kelly and Moskowitz, 2020). The

retention expense tool and technique would be used in finding advantages. The number of unit

being produced would be equivalent to 10,000, 9000 units could be sold over a point of time = $

50 per unit rate

Direct labour = $ 5 Direct material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

base is explained as unit expense. The cost can be referred such as assembled material of single

unit. It is also explained as the expense of item being supplied, cycle expense could be referred

to accounting which results in indistinguishable or identical unit of income. The following are

the variation between interaction expense and unit as well.

Absorption Costing: It is an cost which can be covered with the help of costing approach which

account and dissect for all assembly related costs(Hariyani, Ratnawati and Rahmiyati, 2021).

The majority of the time consumed, this element is used by companies to internalise the expense

of item. In simpler terms, the cost is at . times related to as 'full cost. Direct labour, direct

material, variable created upward and fixed assembly upward are four sort of retentment costing

elements. The expense counts both indirect and direct cost. The most necessary element of direct

expenses are the quantity of raw materials which are being adapted and used and the time which

is being spent constructing the good. Office plant rentals, expense, security charge and protection

as well which can be included in creation of indirect expense.

Calculation of Absorption costing:

Formula = (Direct work cost + Direct material expense + Variable assembling upward expense +

Fixed assembling upward) / No. of units created

It is mostly used in the section of assembled organisations in aiding the organisation in

computation of cost of commodities so that the business would be examining the best expense

approaches for the quantity as well as managing the expense of goods.

For example:

Accepting which the ABC corporation is a fan producer. One assembly step would be

accommodating the reliable data and information(Israel, Kelly and Moskowitz, 2020). The

retention expense tool and technique would be used in finding advantages. The number of unit

being produced would be equivalent to 10,000, 9000 units could be sold over a point of time = $

50 per unit rate

Direct labour = $ 5 Direct material = $ 20

$ 5 in other variable costs

Overheads Fixed = $ 5

$ 30,000 in fixed costs

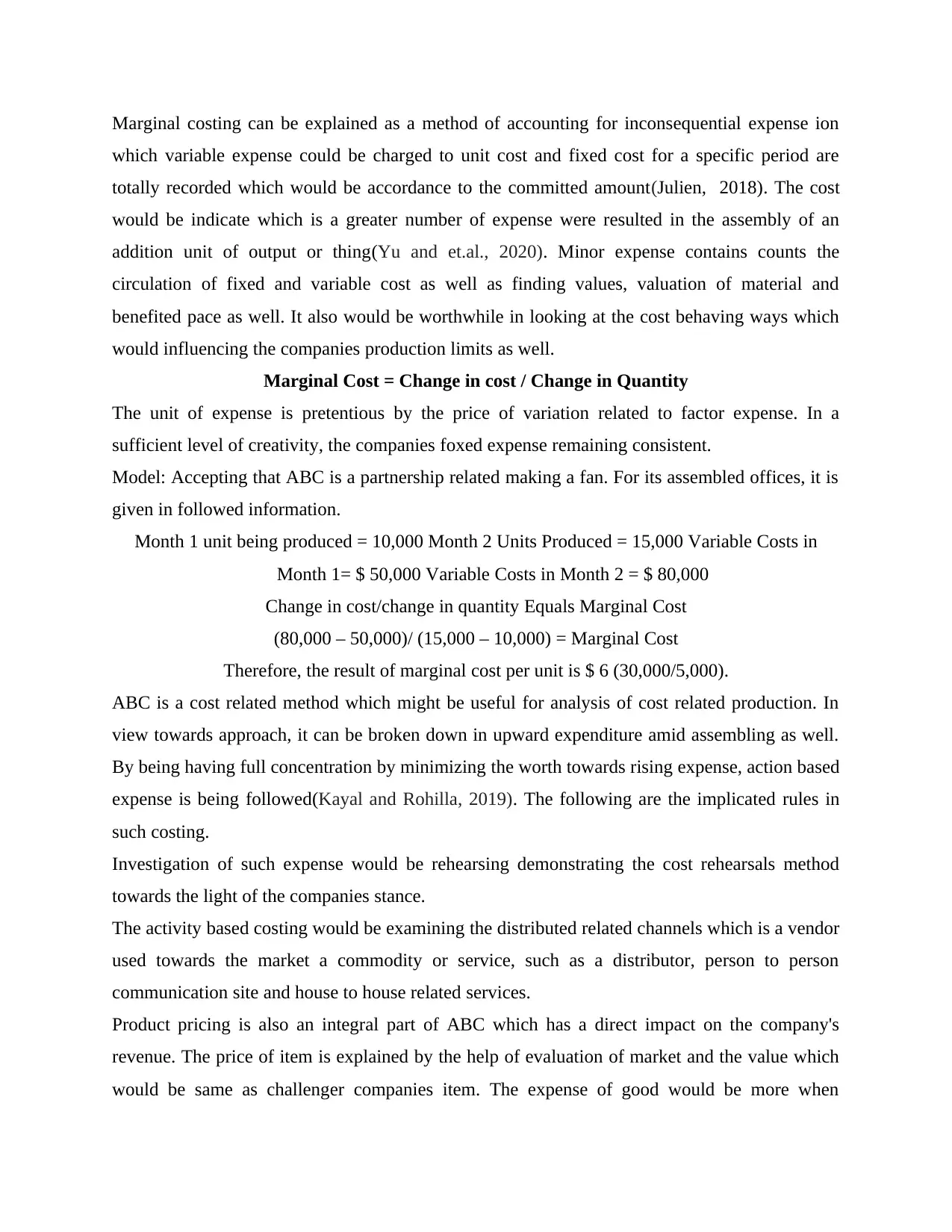

Marginal costing can be explained as a method of accounting for inconsequential expense ion

which variable expense could be charged to unit cost and fixed cost for a specific period are

totally recorded which would be accordance to the committed amount(Julien, 2018). The cost

would be indicate which is a greater number of expense were resulted in the assembly of an

addition unit of output or thing(Yu and et.al., 2020). Minor expense contains counts the

circulation of fixed and variable cost as well as finding values, valuation of material and

benefited pace as well. It also would be worthwhile in looking at the cost behaving ways which

would influencing the companies production limits as well.

Marginal Cost = Change in cost / Change in Quantity

The unit of expense is pretentious by the price of variation related to factor expense. In a

sufficient level of creativity, the companies foxed expense remaining consistent.

Model: Accepting that ABC is a partnership related making a fan. For its assembled offices, it is

given in followed information.

Month 1 unit being produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in

Month 1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

Therefore, the result of marginal cost per unit is $ 6 (30,000/5,000).

ABC is a cost related method which might be useful for analysis of cost related production. In

view towards approach, it can be broken down in upward expenditure amid assembling as well.

By being having full concentration by minimizing the worth towards rising expense, action based

expense is being followed(Kayal and Rohilla, 2019). The following are the implicated rules in

such costing.

Investigation of such expense would be rehearsing demonstrating the cost rehearsals method

towards the light of the companies stance.

The activity based costing would be examining the distributed related channels which is a vendor

used towards the market a commodity or service, such as a distributor, person to person

communication site and house to house related services.

Product pricing is also an integral part of ABC which has a direct impact on the company's

revenue. The price of item is explained by the help of evaluation of market and the value which

would be same as challenger companies item. The expense of good would be more when

which variable expense could be charged to unit cost and fixed cost for a specific period are

totally recorded which would be accordance to the committed amount(Julien, 2018). The cost

would be indicate which is a greater number of expense were resulted in the assembly of an

addition unit of output or thing(Yu and et.al., 2020). Minor expense contains counts the

circulation of fixed and variable cost as well as finding values, valuation of material and

benefited pace as well. It also would be worthwhile in looking at the cost behaving ways which

would influencing the companies production limits as well.

Marginal Cost = Change in cost / Change in Quantity

The unit of expense is pretentious by the price of variation related to factor expense. In a

sufficient level of creativity, the companies foxed expense remaining consistent.

Model: Accepting that ABC is a partnership related making a fan. For its assembled offices, it is

given in followed information.

Month 1 unit being produced = 10,000 Month 2 Units Produced = 15,000 Variable Costs in

Month 1= $ 50,000 Variable Costs in Month 2 = $ 80,000

Change in cost/change in quantity Equals Marginal Cost

(80,000 – 50,000)/ (15,000 – 10,000) = Marginal Cost

Therefore, the result of marginal cost per unit is $ 6 (30,000/5,000).

ABC is a cost related method which might be useful for analysis of cost related production. In

view towards approach, it can be broken down in upward expenditure amid assembling as well.

By being having full concentration by minimizing the worth towards rising expense, action based

expense is being followed(Kayal and Rohilla, 2019). The following are the implicated rules in

such costing.

Investigation of such expense would be rehearsing demonstrating the cost rehearsals method

towards the light of the companies stance.

The activity based costing would be examining the distributed related channels which is a vendor

used towards the market a commodity or service, such as a distributor, person to person

communication site and house to house related services.

Product pricing is also an integral part of ABC which has a direct impact on the company's

revenue. The price of item is explained by the help of evaluation of market and the value which

would be same as challenger companies item. The expense of good would be more when

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compared to lower expenses it would be created problem related to misfortune, therefore the

base valuation is necessary for keeping a track of the condition over the watch.

TASK- 2

Suggest some plans to reduce the cost of the organization.

In this particular task on the bases of above used techniques. They already set up and

utilized the activity -based costing technique for calculating the expenses of the firm. The main

reason for selecting this method is that it measured and supplying charges to each and very

division within the firm which basically depends upon the definite drivers. Generally, ABC

costing will provide an assistance which already enable the cost in each and every company

projected task, and they will be capable to speedily identifying the benefits of cost involved in

which section of the entity for them. It also determine that in which division it incurred more

expenditures, which permit them to manage costs within a satisfactory range(Li and et.al., 2020).

The main benefits of ABC costing rather than the finding expenses for the projected task section

is that it removed them into the job work operations. It assist the organization to decline the

complete cost of the finished goods and services. Which allow them to determine a relevant

selling price for the goods and services that is not enormous to the consumer. For the

performance of the upward discussions, Dysonica plc. Is stimulate the company for using the

activity-based costing method in their business, so, that it helps the company to decline the cost

of product correspondingly.

This strategy of costing is numerous in nature and it suggest the method of costing that is activity

base costing or marginal costing. From past it continuously provides an assistance to the

company and determine that how organization control and direct the costs which includes in the

production of goods and services. Basically this also permit the companies for different

expenditure divisions which based on their systems and helps in identifying that which one is the

most costly method and it also assists them to break the cost and try to better the projected

activities in a same manner(Shiratori, 2019) . Firms mainly use the action-based costing

technique as a one- stop store and helps in reducing the cost of the business. It also includes

some businesses for tracing the expenses as it arise instead of merging them with another

expenditures. As a result that it misunderstood the basic source of cost, and the organization may

base valuation is necessary for keeping a track of the condition over the watch.

TASK- 2

Suggest some plans to reduce the cost of the organization.

In this particular task on the bases of above used techniques. They already set up and

utilized the activity -based costing technique for calculating the expenses of the firm. The main

reason for selecting this method is that it measured and supplying charges to each and very

division within the firm which basically depends upon the definite drivers. Generally, ABC

costing will provide an assistance which already enable the cost in each and every company

projected task, and they will be capable to speedily identifying the benefits of cost involved in

which section of the entity for them. It also determine that in which division it incurred more

expenditures, which permit them to manage costs within a satisfactory range(Li and et.al., 2020).

The main benefits of ABC costing rather than the finding expenses for the projected task section

is that it removed them into the job work operations. It assist the organization to decline the

complete cost of the finished goods and services. Which allow them to determine a relevant

selling price for the goods and services that is not enormous to the consumer. For the

performance of the upward discussions, Dysonica plc. Is stimulate the company for using the

activity-based costing method in their business, so, that it helps the company to decline the cost

of product correspondingly.

This strategy of costing is numerous in nature and it suggest the method of costing that is activity

base costing or marginal costing. From past it continuously provides an assistance to the

company and determine that how organization control and direct the costs which includes in the

production of goods and services. Basically this also permit the companies for different

expenditure divisions which based on their systems and helps in identifying that which one is the

most costly method and it also assists them to break the cost and try to better the projected

activities in a same manner(Shiratori, 2019) . Firms mainly use the action-based costing

technique as a one- stop store and helps in reducing the cost of the business. It also includes

some businesses for tracing the expenses as it arise instead of merging them with another

expenditures. As a result that it misunderstood the basic source of cost, and the organization may

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

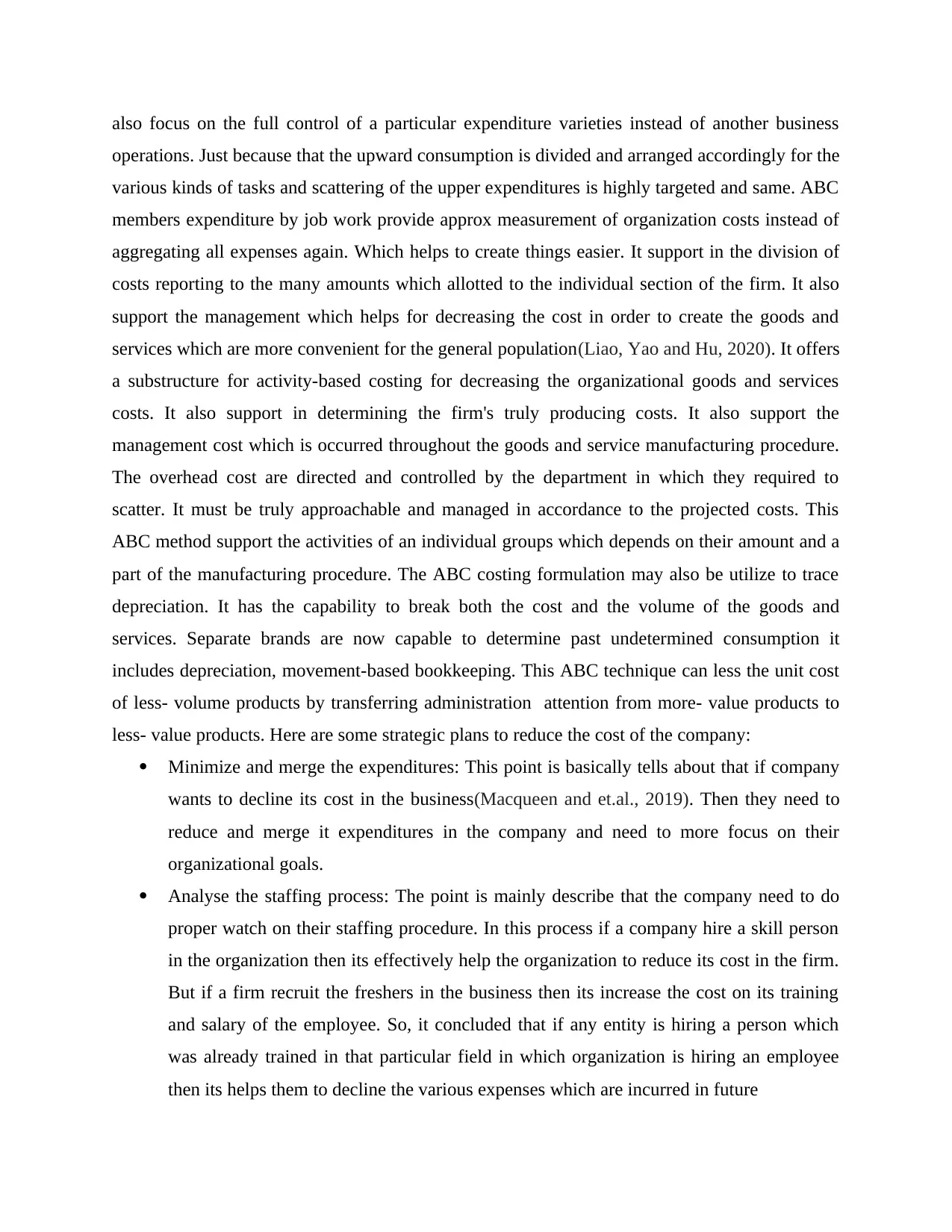

also focus on the full control of a particular expenditure varieties instead of another business

operations. Just because that the upward consumption is divided and arranged accordingly for the

various kinds of tasks and scattering of the upper expenditures is highly targeted and same. ABC

members expenditure by job work provide approx measurement of organization costs instead of

aggregating all expenses again. Which helps to create things easier. It support in the division of

costs reporting to the many amounts which allotted to the individual section of the firm. It also

support the management which helps for decreasing the cost in order to create the goods and

services which are more convenient for the general population(Liao, Yao and Hu, 2020). It offers

a substructure for activity-based costing for decreasing the organizational goods and services

costs. It also support in determining the firm's truly producing costs. It also support the

management cost which is occurred throughout the goods and service manufacturing procedure.

The overhead cost are directed and controlled by the department in which they required to

scatter. It must be truly approachable and managed in accordance to the projected costs. This

ABC method support the activities of an individual groups which depends on their amount and a

part of the manufacturing procedure. The ABC costing formulation may also be utilize to trace

depreciation. It has the capability to break both the cost and the volume of the goods and

services. Separate brands are now capable to determine past undetermined consumption it

includes depreciation, movement-based bookkeeping. This ABC technique can less the unit cost

of less- volume products by transferring administration attention from more- value products to

less- value products. Here are some strategic plans to reduce the cost of the company:

Minimize and merge the expenditures: This point is basically tells about that if company

wants to decline its cost in the business(Macqueen and et.al., 2019). Then they need to

reduce and merge it expenditures in the company and need to more focus on their

organizational goals.

Analyse the staffing process: The point is mainly describe that the company need to do

proper watch on their staffing procedure. In this process if a company hire a skill person

in the organization then its effectively help the organization to reduce its cost in the firm.

But if a firm recruit the freshers in the business then its increase the cost on its training

and salary of the employee. So, it concluded that if any entity is hiring a person which

was already trained in that particular field in which organization is hiring an employee

then its helps them to decline the various expenses which are incurred in future

operations. Just because that the upward consumption is divided and arranged accordingly for the

various kinds of tasks and scattering of the upper expenditures is highly targeted and same. ABC

members expenditure by job work provide approx measurement of organization costs instead of

aggregating all expenses again. Which helps to create things easier. It support in the division of

costs reporting to the many amounts which allotted to the individual section of the firm. It also

support the management which helps for decreasing the cost in order to create the goods and

services which are more convenient for the general population(Liao, Yao and Hu, 2020). It offers

a substructure for activity-based costing for decreasing the organizational goods and services

costs. It also support in determining the firm's truly producing costs. It also support the

management cost which is occurred throughout the goods and service manufacturing procedure.

The overhead cost are directed and controlled by the department in which they required to

scatter. It must be truly approachable and managed in accordance to the projected costs. This

ABC method support the activities of an individual groups which depends on their amount and a

part of the manufacturing procedure. The ABC costing formulation may also be utilize to trace

depreciation. It has the capability to break both the cost and the volume of the goods and

services. Separate brands are now capable to determine past undetermined consumption it

includes depreciation, movement-based bookkeeping. This ABC technique can less the unit cost

of less- volume products by transferring administration attention from more- value products to

less- value products. Here are some strategic plans to reduce the cost of the company:

Minimize and merge the expenditures: This point is basically tells about that if company

wants to decline its cost in the business(Macqueen and et.al., 2019). Then they need to

reduce and merge it expenditures in the company and need to more focus on their

organizational goals.

Analyse the staffing process: The point is mainly describe that the company need to do

proper watch on their staffing procedure. In this process if a company hire a skill person

in the organization then its effectively help the organization to reduce its cost in the firm.

But if a firm recruit the freshers in the business then its increase the cost on its training

and salary of the employee. So, it concluded that if any entity is hiring a person which

was already trained in that particular field in which organization is hiring an employee

then its helps them to decline the various expenses which are incurred in future

Recreate departments: if a manger of the organization try to increase the productivity in

the organization then the firm invest more money to perform that specific activity. It only

happens when company is mainly involve the task in which they reorganize the

departments(Mali, Fallah Shams and Saeedi, 2021). Company play a hit and trial

technique to transfer most efficient employees to that department in which the

productivity of any department is very low and superior reorganize the department and

encourage the employees of each and every department to work more efficiently but its

create huge cost because if a firm need a person to perform some specific task then they

hire more employees and reorganize the department into the corporation.

Brainstorming with your staff members: This technique is also helps provide some

various kinds of plans for reducing the cost in the organization. This method mainly helps

the manager of the firm. It only works when supervisor of the company discuss the ideas

for reducing the cost of operational activities with their employees. Because each and

every employee in the firm is having it own innovative approach(Sandberg, 2018). So,

on that basis with the help of brainstorming technique manager take an innovative and

different ideas of each and every employee for reducing the cost of the firm.

Restructure services: In this point company need to restructure those services which are

unused in business. Basically every organization need to eliminate those unused activity

which is not provide any productivity to the firm and completely wasteful for the entity

for example: if any company provide 24 hours service facility to the customer and

company having more calls during working not in night shift then firm need to remove

the night shift from the company otherwise it will create more cost in the corporation and

reduce the efficiency of the employee also(Novak and Leslie, 2020).

Examine the facilities in the organization: In this particular point it also provide an

assistance to the company and firstly they need to determine the type of facility which

assist to reduce the cost of the entity and execute the facility into the firm(Zhang and

Toffanin, 2018). So, that firm invest on those facilities which helps the organization to

reduce the cost of operational task.

the organization then the firm invest more money to perform that specific activity. It only

happens when company is mainly involve the task in which they reorganize the

departments(Mali, Fallah Shams and Saeedi, 2021). Company play a hit and trial

technique to transfer most efficient employees to that department in which the

productivity of any department is very low and superior reorganize the department and

encourage the employees of each and every department to work more efficiently but its

create huge cost because if a firm need a person to perform some specific task then they

hire more employees and reorganize the department into the corporation.

Brainstorming with your staff members: This technique is also helps provide some

various kinds of plans for reducing the cost in the organization. This method mainly helps

the manager of the firm. It only works when supervisor of the company discuss the ideas

for reducing the cost of operational activities with their employees. Because each and

every employee in the firm is having it own innovative approach(Sandberg, 2018). So,

on that basis with the help of brainstorming technique manager take an innovative and

different ideas of each and every employee for reducing the cost of the firm.

Restructure services: In this point company need to restructure those services which are

unused in business. Basically every organization need to eliminate those unused activity

which is not provide any productivity to the firm and completely wasteful for the entity

for example: if any company provide 24 hours service facility to the customer and

company having more calls during working not in night shift then firm need to remove

the night shift from the company otherwise it will create more cost in the corporation and

reduce the efficiency of the employee also(Novak and Leslie, 2020).

Examine the facilities in the organization: In this particular point it also provide an

assistance to the company and firstly they need to determine the type of facility which

assist to reduce the cost of the entity and execute the facility into the firm(Zhang and

Toffanin, 2018). So, that firm invest on those facilities which helps the organization to

reduce the cost of operational task.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

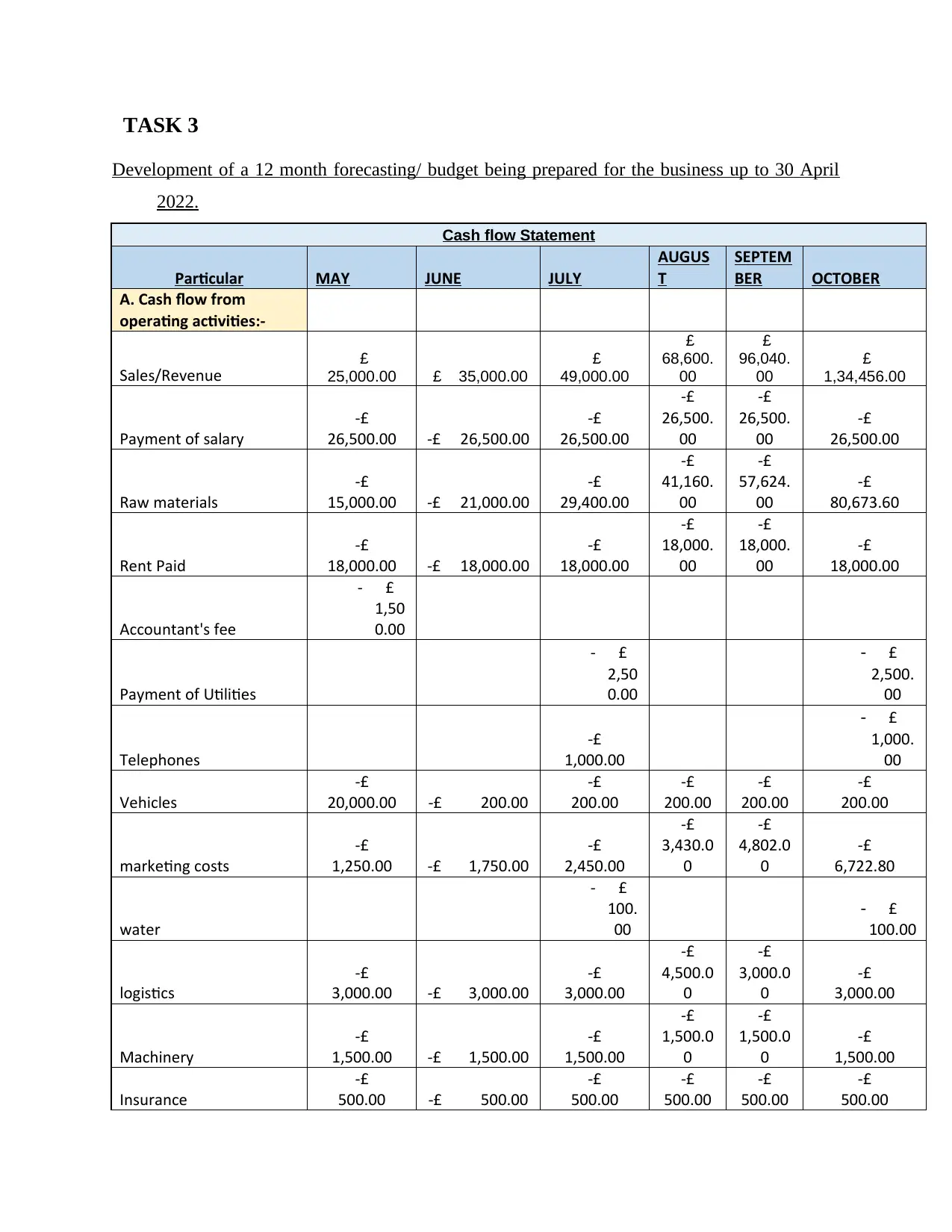

TASK 3

Development of a 12 month forecasting/ budget being prepared for the business up to 30 April

2022.

Cash flow Statement

Particular MAY JUNE JULY

AUGUS

T

SEPTEM

BER OCTOBER

A. Cash flow from

operating activities:-

Sales/Revenue £

25,000.00 £ 35,000.00

£

49,000.00

£

68,600.

00

£

96,040.

00

£

1,34,456.00

Payment of salary

-£

26,500.00 -£ 26,500.00

-£

26,500.00

-£

26,500.

00

-£

26,500.

00

-£

26,500.00

Raw materials

-£

15,000.00 -£ 21,000.00

-£

29,400.00

-£

41,160.

00

-£

57,624.

00

-£

80,673.60

Rent Paid

-£

18,000.00 -£ 18,000.00

-£

18,000.00

-£

18,000.

00

-£

18,000.

00

-£

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities

- £

2,50

0.00

- £

2,500.

00

Telephones

-£

1,000.00

- £

1,000.

00

Vehicles

-£

20,000.00 -£ 200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

marketing costs

-£

1,250.00 -£ 1,750.00

-£

2,450.00

-£

3,430.0

0

-£

4,802.0

0

-£

6,722.80

water

- £

100.

00

- £

100.00

logistics

-£

3,000.00 -£ 3,000.00

-£

3,000.00

-£

4,500.0

0

-£

3,000.0

0

-£

3,000.00

Machinery

-£

1,500.00 -£ 1,500.00

-£

1,500.00

-£

1,500.0

0

-£

1,500.0

0

-£

1,500.00

Insurance

-£

500.00 -£ 500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

Development of a 12 month forecasting/ budget being prepared for the business up to 30 April

2022.

Cash flow Statement

Particular MAY JUNE JULY

AUGUS

T

SEPTEM

BER OCTOBER

A. Cash flow from

operating activities:-

Sales/Revenue £

25,000.00 £ 35,000.00

£

49,000.00

£

68,600.

00

£

96,040.

00

£

1,34,456.00

Payment of salary

-£

26,500.00 -£ 26,500.00

-£

26,500.00

-£

26,500.

00

-£

26,500.

00

-£

26,500.00

Raw materials

-£

15,000.00 -£ 21,000.00

-£

29,400.00

-£

41,160.

00

-£

57,624.

00

-£

80,673.60

Rent Paid

-£

18,000.00 -£ 18,000.00

-£

18,000.00

-£

18,000.

00

-£

18,000.

00

-£

18,000.00

Accountant's fee

- £

1,50

0.00

Payment of Utilities

- £

2,50

0.00

- £

2,500.

00

Telephones

-£

1,000.00

- £

1,000.

00

Vehicles

-£

20,000.00 -£ 200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

marketing costs

-£

1,250.00 -£ 1,750.00

-£

2,450.00

-£

3,430.0

0

-£

4,802.0

0

-£

6,722.80

water

- £

100.

00

- £

100.00

logistics

-£

3,000.00 -£ 3,000.00

-£

3,000.00

-£

4,500.0

0

-£

3,000.0

0

-£

3,000.00

Machinery

-£

1,500.00 -£ 1,500.00

-£

1,500.00

-£

1,500.0

0

-£

1,500.0

0

-£

1,500.00

Insurance

-£

500.00 -£ 500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Mixc Expense

-£

50.00 -£ 50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

Net cash flow from

operating activites:-

-£

62,300.00 -£ 37,500.00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

B. Cash flow from

financaing activities:- £ - £ - £ -

£

-

£

- £ -

Net Cash flow from

financing activities:- £ - £ - £ -

£

-

£

- £ -

C. Cash flow from

Investing activities:-

Initial investment made

£

20,000.00 £ - £ -

£

-

£

- £ -

Net cash flow from

investing activities:-

£

20,000.00 £ - £ -

£

-

£

- £ -

Tatal cash

inflwo/outflows(A+B+C)

-£

42,300.00 -£ 37,500.00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

Cash flow Statement

Particular

NOVEMBE

R

DECEMBE

R JANUARY FEBURAR

Y MARCH APRIL Total(Year

1)

A. Cash flow from

operating activities:-

Sales/Revenue £1,88,238.

40

£2,63,53

3.76

£3,68,947.

26

£5,16,52

6.17

£7,23,136.

64

£10,12,3

91.29

£34,80,86

9.52

Payment of salary

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

3,49,800.0

0

Raw materials

-£

1,12,943.04

-£

1,58,120.

26

-£

2,21,368.36

-£

3,09,915.

70

-£

4,33,881.98

-£

6,07,434.

78

Rent Paid

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

2,58,000.0

0

Accountant's fee

-£

1,500.00

Payment of Utilities

- £

2,5

00.

00

-£

2,500.00

-£

10,000.00

-£

50.00 -£ 50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

Net cash flow from

operating activites:-

-£

62,300.00 -£ 37,500.00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

B. Cash flow from

financaing activities:- £ - £ - £ -

£

-

£

- £ -

Net Cash flow from

financing activities:- £ - £ - £ -

£

-

£

- £ -

C. Cash flow from

Investing activities:-

Initial investment made

£

20,000.00 £ - £ -

£

-

£

- £ -

Net cash flow from

investing activities:-

£

20,000.00 £ - £ -

£

-

£

- £ -

Tatal cash

inflwo/outflows(A+B+C)

-£

42,300.00 -£ 37,500.00

-£

36,200.00

-£

27,240.

00

-£

16,136.

00

-£

6,290.40

Cash flow Statement

Particular

NOVEMBE

R

DECEMBE

R JANUARY FEBURAR

Y MARCH APRIL Total(Year

1)

A. Cash flow from

operating activities:-

Sales/Revenue £1,88,238.

40

£2,63,53

3.76

£3,68,947.

26

£5,16,52

6.17

£7,23,136.

64

£10,12,3

91.29

£34,80,86

9.52

Payment of salary

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

31,800.00

-£

3,49,800.0

0

Raw materials

-£

1,12,943.04

-£

1,58,120.

26

-£

2,21,368.36

-£

3,09,915.

70

-£

4,33,881.98

-£

6,07,434.

78

Rent Paid

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

25,000.00

-£

2,58,000.0

0

Accountant's fee

-£

1,500.00

Payment of Utilities

- £

2,5

00.

00

-£

2,500.00

-£

10,000.00

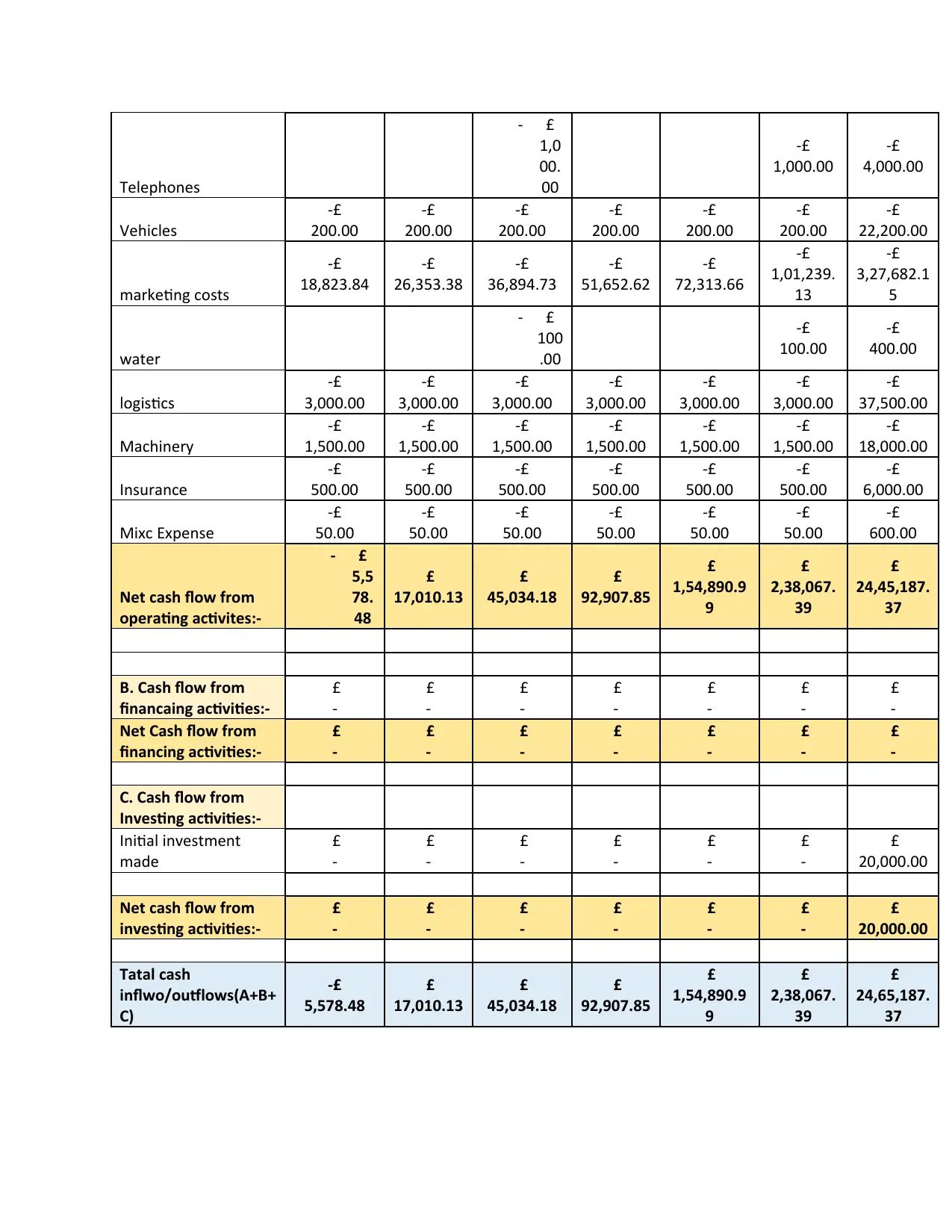

Telephones

- £

1,0

00.

00

-£

1,000.00

-£

4,000.00

Vehicles

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

22,200.00

marketing costs

-£

18,823.84

-£

26,353.38

-£

36,894.73

-£

51,652.62

-£

72,313.66

-£

1,01,239.

13

-£

3,27,682.1

5

water

- £

100

.00

-£

100.00

-£

400.00

logistics

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

37,500.00

Machinery

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

18,000.00

Insurance

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

6,000.00

Mixc Expense

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

600.00

Net cash flow from

operating activites:-

- £

5,5

78.

48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,45,187.

37

B. Cash flow from

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Net cash flow from

investing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Tatal cash

inflwo/outflows(A+B+

C)

-£

5,578.48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,65,187.

37

- £

1,0

00.

00

-£

1,000.00

-£

4,000.00

Vehicles

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

200.00

-£

22,200.00

marketing costs

-£

18,823.84

-£

26,353.38

-£

36,894.73

-£

51,652.62

-£

72,313.66

-£

1,01,239.

13

-£

3,27,682.1

5

water

- £

100

.00

-£

100.00

-£

400.00

logistics

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

3,000.00

-£

37,500.00

Machinery

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

1,500.00

-£

18,000.00

Insurance

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

500.00

-£

6,000.00

Mixc Expense

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

50.00

-£

600.00

Net cash flow from

operating activites:-

- £

5,5

78.

48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,45,187.

37

B. Cash flow from

financaing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

Net Cash flow from

financing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

-

C. Cash flow from

Investing activities:-

Initial investment

made

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Net cash flow from

investing activities:-

£

-

£

-

£

-

£

-

£

-

£

-

£

20,000.00

Tatal cash

inflwo/outflows(A+B+

C)

-£

5,578.48

£

17,010.13

£

45,034.18

£

92,907.85

£

1,54,890.9

9

£

2,38,067.

39

£

24,65,187.

37

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.