Metrics, Earned Value, and Project Performance: A Detailed Report

VerifiedAdded on 2023/01/23

|8

|2161

|92

Report

AI Summary

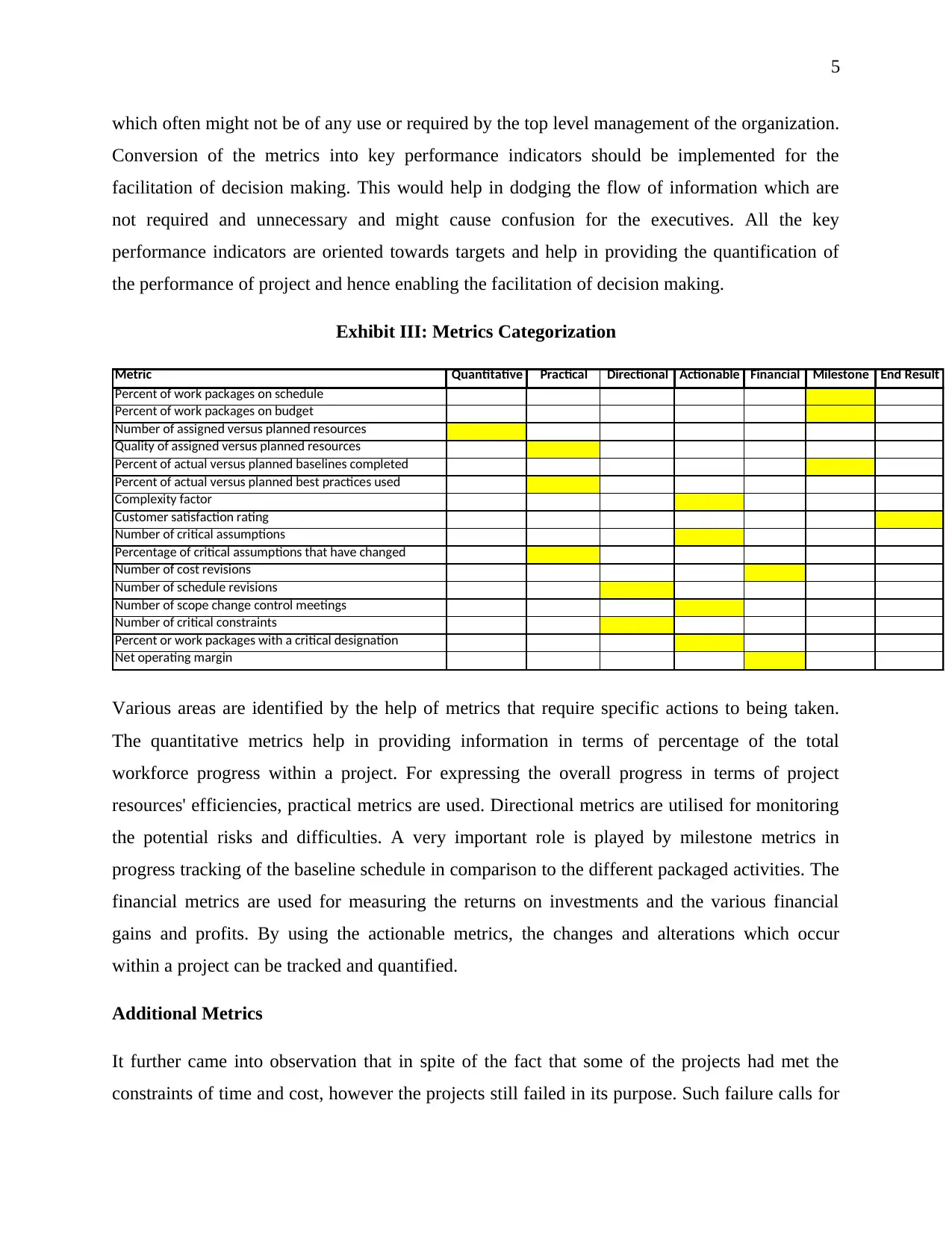

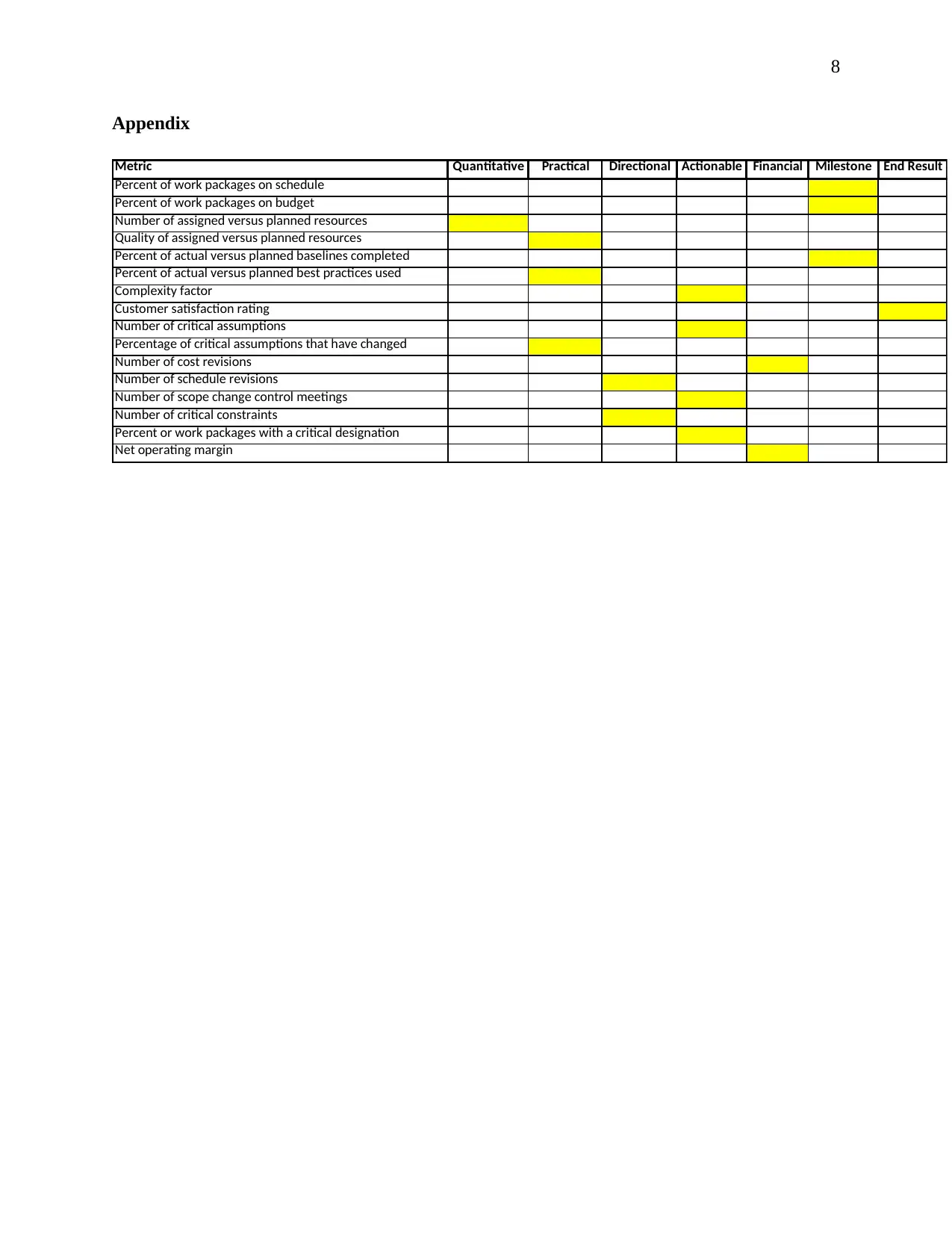

This report delves into the application of Earned Value Management (EVM) and project metrics within a research and development company facing financial losses due to ineffective project tracking. The analysis highlights the importance of incorporating comprehensive metrics beyond financial aspects, emphasizing the need for a committee-driven approach to define relevant Key Performance Indicators (KPIs). It discusses the challenges of balancing the number of metrics to avoid overwhelming employees while ensuring sufficient data for informed decision-making. The report categorizes metrics (quantitative, practical, directional, actionable, financial, milestone, and end result) and addresses the introduction of value-based and alert metrics, along with the significance of internal audits and executive training for proper interpretation. The report underscores the crucial role of metrics in anticipating risks, improving project outcomes, and aligning projects with client requirements, ultimately advocating for a strategic approach to project management measurement and evaluation.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.