Advanced Corporate Reporting: Earning Management Report Analysis

VerifiedAdded on 2023/04/03

|16

|4032

|114

Report

AI Summary

This report delves into the multifaceted realm of earning management within corporate reporting, exploring its techniques, ethical implications, and consequences. It begins with an abstract that introduces the core concepts, including income smoothing and manipulation of accounting data, often employed to meet company objectives, particularly in the face of financial scandals. A comprehensive literature review is presented, built upon five key theories such as the signal theory, agency theory, and positive accounting theory, to understand how and why managers use these strategies to influence stakeholders. The report examines the incentives driving earning management, both for executives and investors, and investigates factors influencing managers' decisions regarding loss reporting. Key terms like 'window dressing,' 'income smoothing,' and 'the big bath' are defined to provide a clear understanding of the practices discussed. The research methodology relies on secondary data from online journals, offering a qualitative, descriptive analysis of the subject. The report then reviews selected journals, focusing on the incentive methodology and the role of executives and investors. The report concludes by summarizing the key findings and implications of earning management in corporate reporting. The assignment is a literature review of five academic journal papers.

0Report on role of Earning management in corporate dressing

Report on role of Earning management in corporate dressing

Name of the Student

Roll NO

Subject Code

Report on role of Earning management in corporate dressing

Name of the Student

Roll NO

Subject Code

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1Report on role of Earning management in corporate dressing

Abstract

The report talks about the issues, consequences and the meaning of terms related to the earning

management. It talks about the importance of having earning management the corporate

accounting world. The financial scandals are highly affected by the usage of the earning

management. It is one of the most widely used terms by the managers to hide or manipulate the

accounting data. They do this to fulfill many objective of the company. It is defines as the

fundamentals of influencing the income of the firm by using the discretionary accruals. Here the

evidence of earning management has been examined in many different context to understand it

better. There are many imperial literature on earning management and to explain the use of the

method to hypothesis of the end result of the financial statement. The report provides a literature

review on earning management based on five theories that exxaplains the use of the earning

management. Thus the aim of the report is to understand the relationship between the opportunist

and information theory as well. How and when the managers use the theory to gain the most out

of it and propose a result that give a positive influence on the stakeholder. The study also looks

at factors why a manager never reports a loss in the statement to the shareholders.

Abstract

The report talks about the issues, consequences and the meaning of terms related to the earning

management. It talks about the importance of having earning management the corporate

accounting world. The financial scandals are highly affected by the usage of the earning

management. It is one of the most widely used terms by the managers to hide or manipulate the

accounting data. They do this to fulfill many objective of the company. It is defines as the

fundamentals of influencing the income of the firm by using the discretionary accruals. Here the

evidence of earning management has been examined in many different context to understand it

better. There are many imperial literature on earning management and to explain the use of the

method to hypothesis of the end result of the financial statement. The report provides a literature

review on earning management based on five theories that exxaplains the use of the earning

management. Thus the aim of the report is to understand the relationship between the opportunist

and information theory as well. How and when the managers use the theory to gain the most out

of it and propose a result that give a positive influence on the stakeholder. The study also looks

at factors why a manager never reports a loss in the statement to the shareholders.

2Report on role of Earning management in corporate dressing

Table of Contents

Table of Contents........................................................................................................................................2

Introduction.................................................................................................................................................3

Literature review:........................................................................................................................................3

Background and Objective of the study:..................................................................................................3

Terms related to case study ....................................................................................................................4

Research Methodology............................................................................................................................6

Review of the Journals.................................................................................................................................6

1. Incentive Methodology....................................................................................................................6

1.1 Incentive related to Executives................................................................................................7

1.2 Incentives gain by investors.....................................................................................................7

2. Theoretical Approach to earning management...............................................................................7

2.1 Signal Theory...........................................................................................................................7

2.2 Agency Theory.........................................................................................................................8

3. The positive accounting theory........................................................................................................8

4. Monitoring mechanism...................................................................................................................9

5. The Threshold management theory................................................................................................9

Conclusion.................................................................................................................................................10

References.................................................................................................................................................11

Appendix...................................................................................................................................................14

Table of Contents

Table of Contents........................................................................................................................................2

Introduction.................................................................................................................................................3

Literature review:........................................................................................................................................3

Background and Objective of the study:..................................................................................................3

Terms related to case study ....................................................................................................................4

Research Methodology............................................................................................................................6

Review of the Journals.................................................................................................................................6

1. Incentive Methodology....................................................................................................................6

1.1 Incentive related to Executives................................................................................................7

1.2 Incentives gain by investors.....................................................................................................7

2. Theoretical Approach to earning management...............................................................................7

2.1 Signal Theory...........................................................................................................................7

2.2 Agency Theory.........................................................................................................................8

3. The positive accounting theory........................................................................................................8

4. Monitoring mechanism...................................................................................................................9

5. The Threshold management theory................................................................................................9

Conclusion.................................................................................................................................................10

References.................................................................................................................................................11

Appendix...................................................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3Report on role of Earning management in corporate dressing

Introduction

Earning is the profit made by the company in the end of the year. To invest in the

company or to buy the stock of company, investors checks the profit of the company. A company

with bad earning prospect will have bad review and investors may hesitate to invest into it. Thus

to make the company lucrative the management uses the earning strategies to manipulate the

profit of the company. It is done to match the numbers with the pre determined figures. Its also

called as income smoothing.

It has been noticed in many cases that earning management is used extensively and

securities & exchange commission has deemed it to be intentional material misstatement practice

if used unethically. In many cases when the income smoothing increases and posses risk of mis

representation on large scale the SEC issues fines and penalties. To a certain point Earning

management is considered legal (Wu 2014).

The approach to manipulate the books of account to make the results looks more lucrative

has damaged the trust of the stakeholders. The incentive to the managers plays a very important

role in earning management miss conduct. Though it’s not illegal but over use has proved to be

fatal to the company itself. There are many examples where the company died due to extensive

use of earning management. The case has been studied how over the years this has been made

protective tool to hide the true reality of the performance of the firms form the stakeholders.

Literature review:

Background and Objective of the study:

The purpose of the study is to understand the ethical use of earning management in the

corporate world. How has it influenced the managers to create a whole new set of accounting for

the stakeholders. Financial scandals like Enron, Gowex, carrilian have shacked the economic

world when examined closely the earning management manipulation was the main reason for all

the fall. Aim of the paper is understand the impact of the fraud on the society, creditors and

shareholders. To investigate the cited paper on this topic why does the managers manipulate

what are the major cause of it. The term and theory used in this paper are reviewed externally.

Also to explore the papers that show the trade-off by managers by two techniques usually used in

Introduction

Earning is the profit made by the company in the end of the year. To invest in the

company or to buy the stock of company, investors checks the profit of the company. A company

with bad earning prospect will have bad review and investors may hesitate to invest into it. Thus

to make the company lucrative the management uses the earning strategies to manipulate the

profit of the company. It is done to match the numbers with the pre determined figures. Its also

called as income smoothing.

It has been noticed in many cases that earning management is used extensively and

securities & exchange commission has deemed it to be intentional material misstatement practice

if used unethically. In many cases when the income smoothing increases and posses risk of mis

representation on large scale the SEC issues fines and penalties. To a certain point Earning

management is considered legal (Wu 2014).

The approach to manipulate the books of account to make the results looks more lucrative

has damaged the trust of the stakeholders. The incentive to the managers plays a very important

role in earning management miss conduct. Though it’s not illegal but over use has proved to be

fatal to the company itself. There are many examples where the company died due to extensive

use of earning management. The case has been studied how over the years this has been made

protective tool to hide the true reality of the performance of the firms form the stakeholders.

Literature review:

Background and Objective of the study:

The purpose of the study is to understand the ethical use of earning management in the

corporate world. How has it influenced the managers to create a whole new set of accounting for

the stakeholders. Financial scandals like Enron, Gowex, carrilian have shacked the economic

world when examined closely the earning management manipulation was the main reason for all

the fall. Aim of the paper is understand the impact of the fraud on the society, creditors and

shareholders. To investigate the cited paper on this topic why does the managers manipulate

what are the major cause of it. The term and theory used in this paper are reviewed externally.

Also to explore the papers that show the trade-off by managers by two techniques usually used in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4Report on role of Earning management in corporate dressing

the earnings management literature, real activity and accrual manipulation. One of the major

impacts of earnings management is the degeneration of information quality in the financial

statements, which misleads stakeholders decisions (De Klerk Et al,. 2015).

Earning management is defined as purposeful intension to draw an external financial

reporting process with the intent to obtain private gain. It occurs through manipulation in the

accounting tools. The review of the journal revealed that there are many sides of the earning

management facets like the opportunist , informational, incentive oriented.

Terms related to case study .

1. Positive accounting management- It can be associated with tool of accounting

providing the nexus of the information about the performance and formation of the

contract. Under this the accounting mitigates the contracting cost s by agreement among

various parties. positive accounting postulates that conservatism in accounting has origins

in contract markets, including managerial compensation contracts and lender debt

contracts (Sun 2010).

2. Entrenchment theory- it is a situation when the manager are holding a very less equity

of the company and the shareholders are not strong to take action against it. Insiders

generally deploy corporate actions to gain person al benefits. In this case the agency cost

rise. Many entrenchment practice re there that are employs by the manager such as the

Poison pills, Golden parachutes and Anti-takeover devices (Roychowdhury 2019).

3. Agency Theory- it is a principle used to explain the issues of the relationship between

the business principle and the agent. The relationship of the shareholder, creditors, debtor

and executives of the company (Chen 2015).

4. Consequences of earnings management- The family firm have more control on the firm

and avoiding the information asymmetric . Thus sometime losses the reputation in the

market as the control can be manipulative. The negative impact is generally seen in the

highly concentrated ownership structure. The most influencing negative impact is on the

stakeholders as they face the most of the wraths. The consequences are studies well in the

following review (Bazrafshan 2016).

5. Window Dressing: A method of dressing the financial statement for investors and

creditors to trust. Make the company look more profitable so that it gets support from the

the earnings management literature, real activity and accrual manipulation. One of the major

impacts of earnings management is the degeneration of information quality in the financial

statements, which misleads stakeholders decisions (De Klerk Et al,. 2015).

Earning management is defined as purposeful intension to draw an external financial

reporting process with the intent to obtain private gain. It occurs through manipulation in the

accounting tools. The review of the journal revealed that there are many sides of the earning

management facets like the opportunist , informational, incentive oriented.

Terms related to case study .

1. Positive accounting management- It can be associated with tool of accounting

providing the nexus of the information about the performance and formation of the

contract. Under this the accounting mitigates the contracting cost s by agreement among

various parties. positive accounting postulates that conservatism in accounting has origins

in contract markets, including managerial compensation contracts and lender debt

contracts (Sun 2010).

2. Entrenchment theory- it is a situation when the manager are holding a very less equity

of the company and the shareholders are not strong to take action against it. Insiders

generally deploy corporate actions to gain person al benefits. In this case the agency cost

rise. Many entrenchment practice re there that are employs by the manager such as the

Poison pills, Golden parachutes and Anti-takeover devices (Roychowdhury 2019).

3. Agency Theory- it is a principle used to explain the issues of the relationship between

the business principle and the agent. The relationship of the shareholder, creditors, debtor

and executives of the company (Chen 2015).

4. Consequences of earnings management- The family firm have more control on the firm

and avoiding the information asymmetric . Thus sometime losses the reputation in the

market as the control can be manipulative. The negative impact is generally seen in the

highly concentrated ownership structure. The most influencing negative impact is on the

stakeholders as they face the most of the wraths. The consequences are studies well in the

following review (Bazrafshan 2016).

5. Window Dressing: A method of dressing the financial statement for investors and

creditors to trust. Make the company look more profitable so that it gets support from the

5Report on role of Earning management in corporate dressing

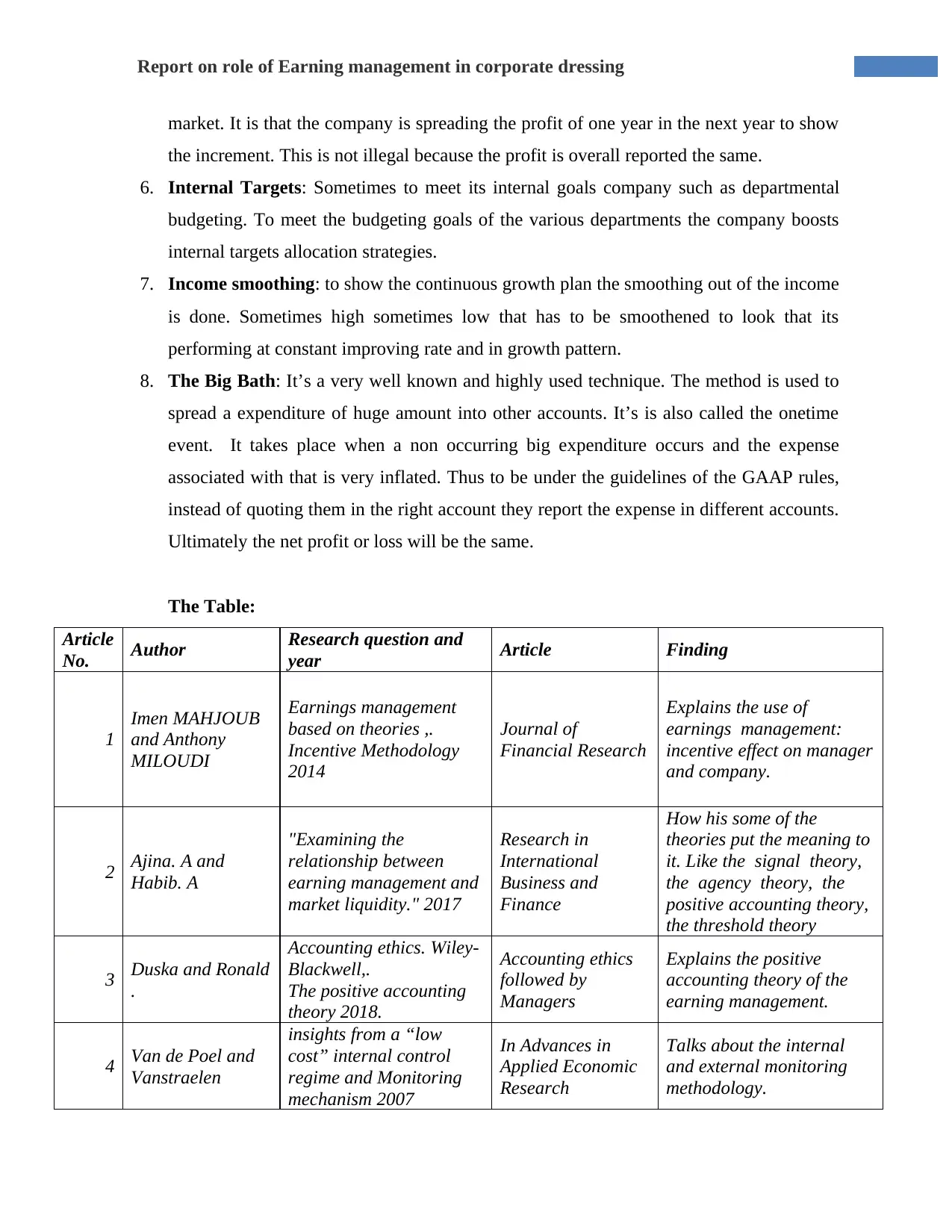

market. It is that the company is spreading the profit of one year in the next year to show

the increment. This is not illegal because the profit is overall reported the same.

6. Internal Targets: Sometimes to meet its internal goals company such as departmental

budgeting. To meet the budgeting goals of the various departments the company boosts

internal targets allocation strategies.

7. Income smoothing: to show the continuous growth plan the smoothing out of the income

is done. Sometimes high sometimes low that has to be smoothened to look that its

performing at constant improving rate and in growth pattern.

8. The Big Bath: It’s a very well known and highly used technique. The method is used to

spread a expenditure of huge amount into other accounts. It’s is also called the onetime

event. It takes place when a non occurring big expenditure occurs and the expense

associated with that is very inflated. Thus to be under the guidelines of the GAAP rules,

instead of quoting them in the right account they report the expense in different accounts.

Ultimately the net profit or loss will be the same.

The Table:

Article

No. Author Research question and

year Article Finding

1

Imen MAHJOUB

and Anthony

MILOUDI

Earnings management

based on theories ,.

Incentive Methodology

2014

Journal of

Financial Research

Explains the use of

earnings management:

incentive effect on manager

and company.

2 Ajina. A and

Habib. A

"Examining the

relationship between

earning management and

market liquidity." 2017

Research in

International

Business and

Finance

How his some of the

theories put the meaning to

it. Like the signal theory,

the agency theory, the

positive accounting theory,

the threshold theory

3 Duska and Ronald

.

Accounting ethics. Wiley-

Blackwell,.

The positive accounting

theory 2018.

Accounting ethics

followed by

Managers

Explains the positive

accounting theory of the

earning management.

4 Van de Poel and

Vanstraelen

insights from a “low

cost” internal control

regime and Monitoring

mechanism 2007

In Advances in

Applied Economic

Research

Talks about the internal

and external monitoring

methodology.

market. It is that the company is spreading the profit of one year in the next year to show

the increment. This is not illegal because the profit is overall reported the same.

6. Internal Targets: Sometimes to meet its internal goals company such as departmental

budgeting. To meet the budgeting goals of the various departments the company boosts

internal targets allocation strategies.

7. Income smoothing: to show the continuous growth plan the smoothing out of the income

is done. Sometimes high sometimes low that has to be smoothened to look that its

performing at constant improving rate and in growth pattern.

8. The Big Bath: It’s a very well known and highly used technique. The method is used to

spread a expenditure of huge amount into other accounts. It’s is also called the onetime

event. It takes place when a non occurring big expenditure occurs and the expense

associated with that is very inflated. Thus to be under the guidelines of the GAAP rules,

instead of quoting them in the right account they report the expense in different accounts.

Ultimately the net profit or loss will be the same.

The Table:

Article

No. Author Research question and

year Article Finding

1

Imen MAHJOUB

and Anthony

MILOUDI

Earnings management

based on theories ,.

Incentive Methodology

2014

Journal of

Financial Research

Explains the use of

earnings management:

incentive effect on manager

and company.

2 Ajina. A and

Habib. A

"Examining the

relationship between

earning management and

market liquidity." 2017

Research in

International

Business and

Finance

How his some of the

theories put the meaning to

it. Like the signal theory,

the agency theory, the

positive accounting theory,

the threshold theory

3 Duska and Ronald

.

Accounting ethics. Wiley-

Blackwell,.

The positive accounting

theory 2018.

Accounting ethics

followed by

Managers

Explains the positive

accounting theory of the

earning management.

4 Van de Poel and

Vanstraelen

insights from a “low

cost” internal control

regime and Monitoring

mechanism 2007

In Advances in

Applied Economic

Research

Talks about the internal

and external monitoring

methodology.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6Report on role of Earning management in corporate dressing

5 Faisal Shahzad

earning management

strategies of leveraged

family and non-family

controlled firms: an

empirical evidence 2017

International

Journal of Business

& Society

On what context the

manger pushes the

threshold to meet the

requirements.

Research Methodology

As earning management is an important concept it has many research done in the past. It

is considered as one of the most important ethical financial reporting. Most of the report have

only focused on the positive side of the term and not investigating the misleading factors that it

can have to be prevented in the future. A huge rise was seen in the year 2007 when most of the

company became dependent on the earning management strategies affecting the capital market.

There are more than 800 articles on earning management in 2008. This study focus on the

investigating the mis use of the earning management specially by the managers. If the data are

seen it can be found that the trend has doubled in last 10 years. There are now more than 10000

reference till 2014. That increase of 95% become the most enthusiast topic of finance. According

to the recent survey 20% of the firms manages to manipulate the economic performance of the

earning. They may manipulate the EPS by 10% or more and that will be coming in the

boundaries of the legal rules (Al-Thuneibat Et al. 2016).

The research methodology is secondary and the data is accumulated from the external

sources. The external sources can be attributed to the online journals spread across years. The

research methodology is qualitative where the data is collected based o the quality and not the

number. It is description based on the journals already present in the market. It is in-depth

understanding and more of subjective and informative thus it is sample based study. All the data

are linked with the topic of the research that can better explain why is there such earning

management discrepancies (Xiong 2006).

Review of the Journals

1. Incentive Methodology As per MAHJOUB and MILOUDI (2014) states earning and

management in terms of incentive of earning management. if there is an extensive use of

5 Faisal Shahzad

earning management

strategies of leveraged

family and non-family

controlled firms: an

empirical evidence 2017

International

Journal of Business

& Society

On what context the

manger pushes the

threshold to meet the

requirements.

Research Methodology

As earning management is an important concept it has many research done in the past. It

is considered as one of the most important ethical financial reporting. Most of the report have

only focused on the positive side of the term and not investigating the misleading factors that it

can have to be prevented in the future. A huge rise was seen in the year 2007 when most of the

company became dependent on the earning management strategies affecting the capital market.

There are more than 800 articles on earning management in 2008. This study focus on the

investigating the mis use of the earning management specially by the managers. If the data are

seen it can be found that the trend has doubled in last 10 years. There are now more than 10000

reference till 2014. That increase of 95% become the most enthusiast topic of finance. According

to the recent survey 20% of the firms manages to manipulate the economic performance of the

earning. They may manipulate the EPS by 10% or more and that will be coming in the

boundaries of the legal rules (Al-Thuneibat Et al. 2016).

The research methodology is secondary and the data is accumulated from the external

sources. The external sources can be attributed to the online journals spread across years. The

research methodology is qualitative where the data is collected based o the quality and not the

number. It is description based on the journals already present in the market. It is in-depth

understanding and more of subjective and informative thus it is sample based study. All the data

are linked with the topic of the research that can better explain why is there such earning

management discrepancies (Xiong 2006).

Review of the Journals

1. Incentive Methodology As per MAHJOUB and MILOUDI (2014) states earning and

management in terms of incentive of earning management. if there is an extensive use of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7Report on role of Earning management in corporate dressing

the earning management then there is a question what are the principle incentives for the

earning. The review focuses on the incentive benefits to the mangers and the investor.

1.1 Incentive related to Executives- To avoid losses, declines forecast or improving the

earning forecast it is used by mangers. Managers close to zero result use earning

management techniques to save the result output that is going to be added to the

annual report. To avoid any decline of the result that may be resulted due to loose

management. This is associated with premiums that are associated with the market.

Lastly to impact it psychologically. The price of any product close to 199$ is more

impactful than 201$. Thus the same reverse principles work for money market. The

bigger the result is the better it is thought to be (Sun et al. 2013).

1.2 Incentives gain by investors: To save and maintain the good reputation of the

company the executives manipulates the company’s result. By using the earning

management tools the executives hide the real value company so that the investors

gets influenced to invest more. This also helps to dress the company’s result in a

positive trend showing more future prospect for the shareholders and creditors

(Gordon 2016).

2. Theoretical Approach to earning management- According to Ajina and Habib (2017),

More than 33%of the companies around the world uses the earning management

techniques. It is no simple tool it is used influence the investment decision and also the

resource allocation of the different stakeholders. There are many theories explain the

motivation to earning management affecting the richness of the executive and the market

participants.

2.1 Signal Theory- There is no perfect information that is shared with the stakeholder.

The managers of the company has the most precious information of the company and

they allows them to signal it to the investors and the market participants. Thus to

impress the investor the managers has the true knowledge of the retained earning and

thus they also know the prospects of the investors. The deprivation of the result in the

market is makes it dependent on the behavior of the CEO and the published results.

Thus here the manager aligns them self by being the superior to have the real info

with the investors. There are two types of Signal one is the opportunist and the other

the earning management then there is a question what are the principle incentives for the

earning. The review focuses on the incentive benefits to the mangers and the investor.

1.1 Incentive related to Executives- To avoid losses, declines forecast or improving the

earning forecast it is used by mangers. Managers close to zero result use earning

management techniques to save the result output that is going to be added to the

annual report. To avoid any decline of the result that may be resulted due to loose

management. This is associated with premiums that are associated with the market.

Lastly to impact it psychologically. The price of any product close to 199$ is more

impactful than 201$. Thus the same reverse principles work for money market. The

bigger the result is the better it is thought to be (Sun et al. 2013).

1.2 Incentives gain by investors: To save and maintain the good reputation of the

company the executives manipulates the company’s result. By using the earning

management tools the executives hide the real value company so that the investors

gets influenced to invest more. This also helps to dress the company’s result in a

positive trend showing more future prospect for the shareholders and creditors

(Gordon 2016).

2. Theoretical Approach to earning management- According to Ajina and Habib (2017),

More than 33%of the companies around the world uses the earning management

techniques. It is no simple tool it is used influence the investment decision and also the

resource allocation of the different stakeholders. There are many theories explain the

motivation to earning management affecting the richness of the executive and the market

participants.

2.1 Signal Theory- There is no perfect information that is shared with the stakeholder.

The managers of the company has the most precious information of the company and

they allows them to signal it to the investors and the market participants. Thus to

impress the investor the managers has the true knowledge of the retained earning and

thus they also know the prospects of the investors. The deprivation of the result in the

market is makes it dependent on the behavior of the CEO and the published results.

Thus here the manager aligns them self by being the superior to have the real info

with the investors. There are two types of Signal one is the opportunist and the other

8Report on role of Earning management in corporate dressing

is informational. The first type of signal is used by managers to camouflage the

unprofiting results and mislead the investor to investing risky business (Aerts, Cheng

and Tarca 2013). This is done to have a per4sonal gain of job security and their

responsibility towards their company. The second type of the signal is informational.

Mangers have the privilege to most of the important info of the company. Thus they

communicate the info to the market adjusting the values of the securities and by

reflecting the real value of the company. This minimizes the informational gap

between the different players of the market (Utomo, and Imang 2018).

2.2 Agency Theory- It was developed way back in 1976 by Jensen and Meckling. It talks

about the relationship between the executive and the shareholder. The diverge of

interest for one to profit and other to lose. If the egocentric manner increases in the

executive to maximize the wealth of the shareholder. The company pays profit to the

managers to meet the right company management needs. By motivating their

stakeholder they get incentives paid which maximizes their earning on the cost of the

investors. This was supported by the researcher that the greater the incentive the

greater is the deviation from the true and real results. They are focusing on their

interest and performing the consequence well. The difference in the interest of the

investor and the manager create a compensation contract based on the income of the

company. This contractual charges create pressure on the managers to reduce their

cost and be more realistic in the market (Jensen and Meckling 2009).

3. The positive accounting theory – as per Duska and Ronald (2018) It contains many

accounting policy to affect the result of the company. There are two types of behavior:

opportunistic behavior by favoring their interest at the expense of other stakeholders, and

behavior intended to apply accounting standards efficiently to maximize the company’s

value. According to the compensation that the manager gets, they work for their

incentives on the account of the stakeholders. Other criteria is Debt through the

knowledge of compensation of the managers the shareholders tries to alien their interest.

Generally harming the creditors due to transfer of wealth to the shareholder. To protect

they can by limitation clause in debt. That means to limit the dividend as per the debt

ratio permissible. It is sometimes termed to be to constrained for making free choices

from all the perspective. To avoid violating anti trust law the managers are advised and

is informational. The first type of signal is used by managers to camouflage the

unprofiting results and mislead the investor to investing risky business (Aerts, Cheng

and Tarca 2013). This is done to have a per4sonal gain of job security and their

responsibility towards their company. The second type of the signal is informational.

Mangers have the privilege to most of the important info of the company. Thus they

communicate the info to the market adjusting the values of the securities and by

reflecting the real value of the company. This minimizes the informational gap

between the different players of the market (Utomo, and Imang 2018).

2.2 Agency Theory- It was developed way back in 1976 by Jensen and Meckling. It talks

about the relationship between the executive and the shareholder. The diverge of

interest for one to profit and other to lose. If the egocentric manner increases in the

executive to maximize the wealth of the shareholder. The company pays profit to the

managers to meet the right company management needs. By motivating their

stakeholder they get incentives paid which maximizes their earning on the cost of the

investors. This was supported by the researcher that the greater the incentive the

greater is the deviation from the true and real results. They are focusing on their

interest and performing the consequence well. The difference in the interest of the

investor and the manager create a compensation contract based on the income of the

company. This contractual charges create pressure on the managers to reduce their

cost and be more realistic in the market (Jensen and Meckling 2009).

3. The positive accounting theory – as per Duska and Ronald (2018) It contains many

accounting policy to affect the result of the company. There are two types of behavior:

opportunistic behavior by favoring their interest at the expense of other stakeholders, and

behavior intended to apply accounting standards efficiently to maximize the company’s

value. According to the compensation that the manager gets, they work for their

incentives on the account of the stakeholders. Other criteria is Debt through the

knowledge of compensation of the managers the shareholders tries to alien their interest.

Generally harming the creditors due to transfer of wealth to the shareholder. To protect

they can by limitation clause in debt. That means to limit the dividend as per the debt

ratio permissible. It is sometimes termed to be to constrained for making free choices

from all the perspective. To avoid violating anti trust law the managers are advised and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9Report on role of Earning management in corporate dressing

supervised to lower the earning by earning management theory. By reducing the results

they get some of the sanctioned benefits in some of the countries (Azibi 2017).

4. Monitoring mechanism- According to Van de Poel and Vanstraelen (2007), It is divided

into two major parts the internal monitoring is the members with the corporation, like the

board of director, internal audit, managers. They are there to control the internal factors

to reduce the management’s opportunist behaviors. The external monitoring is a

mechanism that works from outside the corporation like the lenders, creditor,

stakeholders. The other control mechanism is leverage. It helps in avoiding the use of

excessive earning management harming the company. It is simplified that a high leverage

company has higher financial risk. Like the financial distress, bankruptcy, payment

defaulting. The is the debt ratio then the interest paid by the company is also higher

signaling the optimum utilization of the leverage factor (Abbadi Et al. 2016). Now the

external factors that are monitoring the working of the company will be concerned about

the debt repayment. The management has to ensure that they are available with enough to

rescue the situation. thus if the lenders are monitoring then there is less room for higher

incentives to the managements. Ultimately monitoring contributes to the profit and

growth of the company. It has been observed that the companies that default makes more

changes in their books of account than the stable companies (Marco, and Pompili 2017).

5. The Threshold management theory- as per Faisal (2017). The managers of the

company use the earning management to reach the expected earning. Which is the

threshold where they are expected to bring the result. There comes many irregularities in

the distribution of the results of accounting. The threshold of zero result that meant that

the company has to avoid loss at any cost. the threshold of no variation. The company has

to monitor that there is no decrease in the income. Market analyst uses the tool to analysis

and evaluate the performance of the company. To understand the manipulation in the

accounting result there was found some irregularities sin the thresholds. By a survey it

was found that company would rather cross the threshold instead of showing a loss in the

financial statement. As per the studies it has been seen that the managers not only

maximize their compensation but also tries to give a good image of their company in

order to exceed the objectives. This helps giving a good image to the job market. It has

supervised to lower the earning by earning management theory. By reducing the results

they get some of the sanctioned benefits in some of the countries (Azibi 2017).

4. Monitoring mechanism- According to Van de Poel and Vanstraelen (2007), It is divided

into two major parts the internal monitoring is the members with the corporation, like the

board of director, internal audit, managers. They are there to control the internal factors

to reduce the management’s opportunist behaviors. The external monitoring is a

mechanism that works from outside the corporation like the lenders, creditor,

stakeholders. The other control mechanism is leverage. It helps in avoiding the use of

excessive earning management harming the company. It is simplified that a high leverage

company has higher financial risk. Like the financial distress, bankruptcy, payment

defaulting. The is the debt ratio then the interest paid by the company is also higher

signaling the optimum utilization of the leverage factor (Abbadi Et al. 2016). Now the

external factors that are monitoring the working of the company will be concerned about

the debt repayment. The management has to ensure that they are available with enough to

rescue the situation. thus if the lenders are monitoring then there is less room for higher

incentives to the managements. Ultimately monitoring contributes to the profit and

growth of the company. It has been observed that the companies that default makes more

changes in their books of account than the stable companies (Marco, and Pompili 2017).

5. The Threshold management theory- as per Faisal (2017). The managers of the

company use the earning management to reach the expected earning. Which is the

threshold where they are expected to bring the result. There comes many irregularities in

the distribution of the results of accounting. The threshold of zero result that meant that

the company has to avoid loss at any cost. the threshold of no variation. The company has

to monitor that there is no decrease in the income. Market analyst uses the tool to analysis

and evaluate the performance of the company. To understand the manipulation in the

accounting result there was found some irregularities sin the thresholds. By a survey it

was found that company would rather cross the threshold instead of showing a loss in the

financial statement. As per the studies it has been seen that the managers not only

maximize their compensation but also tries to give a good image of their company in

order to exceed the objectives. This helps giving a good image to the job market. It has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10Report on role of Earning management in corporate dressing

been studied that psychologically human get aversion by the negative result and they

future don’t try to understand the benefits of it (Mard 2003) . Thus it becomes easier for

the manager to convince the higher management to send a positive sign in the market

even thou when the company is not doing well

Conclusion

Through the theoretical foundation the purpose of the paper was to study the earning

management through the literature review. The research has reviewed the papers of researcher

who did analysis on the role of the executives in the earning management. Why they adopt such

behaviors and what pressurizes them to follow those methods which leads to fall under the

ethical guidelines of the GAAP. The theory that studied the signal theory , as there are two types

of signal the opportunist and informative. It used to explain the use of the earning theory. Other

theory was about the agency theory that talks about the development of the contract agencies of

the corporate involved in it. The review is done on the incentive developed by the management

to lure the executives to follow the demand of the company even when it’s not true. how and

when do these executives uses their skills to hide or execrate the situations pertaining to the total

earring of the company. The third theory talked about is the positive accounting theory. That is

first study suggesting the use of the accounting terms to take decision affecting the income often

company¸ and there is threshold theory to give a better understanding of the issue .

been studied that psychologically human get aversion by the negative result and they

future don’t try to understand the benefits of it (Mard 2003) . Thus it becomes easier for

the manager to convince the higher management to send a positive sign in the market

even thou when the company is not doing well

Conclusion

Through the theoretical foundation the purpose of the paper was to study the earning

management through the literature review. The research has reviewed the papers of researcher

who did analysis on the role of the executives in the earning management. Why they adopt such

behaviors and what pressurizes them to follow those methods which leads to fall under the

ethical guidelines of the GAAP. The theory that studied the signal theory , as there are two types

of signal the opportunist and informative. It used to explain the use of the earning theory. Other

theory was about the agency theory that talks about the development of the contract agencies of

the corporate involved in it. The review is done on the incentive developed by the management

to lure the executives to follow the demand of the company even when it’s not true. how and

when do these executives uses their skills to hide or execrate the situations pertaining to the total

earring of the company. The third theory talked about is the positive accounting theory. That is

first study suggesting the use of the accounting terms to take decision affecting the income often

company¸ and there is threshold theory to give a better understanding of the issue .

11Report on role of Earning management in corporate dressing

References

Abbadi, Sinan S., Qutaiba F. Hijazi, and Ayat S. Al-Rahahleh. "Corporate governance quality

and earnings management: Evidence from Jordan." Australasian Accounting, Business and

Finance Journal 10, no. 2 (2016): 54-75.

Aerts, W., Cheng, P. and Tarca, A. “Management's Earnings Justification and Earnings

Management under Different Institutional Regimes. Corporate Governance”: An International

Review, 21(1) (2013): pp.93-115.

Ajina, Aymen, and Aymen Habib. "Examining the relationship between earning management

and market liquidity." Research in International Business and Finance 42 (2017): 1164-1172.

Al-Thuneibat, Ali Abedalqader, Hussam Abdulmohsen Al-Angari, and Saleh Abdulrahman Al-

Saad. "The effect of corporate governance mechanisms on earnings management: Evidence from

Saudi Arabia." Review of International Business and Strategy 26, no. 1 (2016): 2-32.

Azibi, Jamel, Hamza Azibi, and Hubert Tondeur. "Institutional Activism, Auditor’s Choice and

Earning Management after the Enron Collapse: Evidence from France." International Business

Research 10, no. 2 (2017): 154-168.

Bazrafshan, Ebrahim, Amene S. Kandelousi, and Chee-Wooi Hooy. "The impact of earnings

management on the extent of disclosure and true financial performance: Evidence from listed

firms in Hong Kong." The British Accounting Review 48, no. 2 (2016): 206-219.

Chen, Ching-Lung, and Pin-Yu Lin. "Real Earnings Management and Subsequent Accounting

Performance: The moderating role of corporate governance." 61 (2015): 1-36.

De Klerk, Marna, Charl de Villiers, and Chris van Staden. "The influence of corporate social

responsibility disclosure on share prices: evidence from the United Kingdom." Pacific

Accounting Review 27, no. 2 (2015): 208-228.

Duska, Ronald F., Brenda Shay Duska, and Kenneth Wm Kury. Accounting ethics. Wiley-

Blackwell, 2018.

References

Abbadi, Sinan S., Qutaiba F. Hijazi, and Ayat S. Al-Rahahleh. "Corporate governance quality

and earnings management: Evidence from Jordan." Australasian Accounting, Business and

Finance Journal 10, no. 2 (2016): 54-75.

Aerts, W., Cheng, P. and Tarca, A. “Management's Earnings Justification and Earnings

Management under Different Institutional Regimes. Corporate Governance”: An International

Review, 21(1) (2013): pp.93-115.

Ajina, Aymen, and Aymen Habib. "Examining the relationship between earning management

and market liquidity." Research in International Business and Finance 42 (2017): 1164-1172.

Al-Thuneibat, Ali Abedalqader, Hussam Abdulmohsen Al-Angari, and Saleh Abdulrahman Al-

Saad. "The effect of corporate governance mechanisms on earnings management: Evidence from

Saudi Arabia." Review of International Business and Strategy 26, no. 1 (2016): 2-32.

Azibi, Jamel, Hamza Azibi, and Hubert Tondeur. "Institutional Activism, Auditor’s Choice and

Earning Management after the Enron Collapse: Evidence from France." International Business

Research 10, no. 2 (2017): 154-168.

Bazrafshan, Ebrahim, Amene S. Kandelousi, and Chee-Wooi Hooy. "The impact of earnings

management on the extent of disclosure and true financial performance: Evidence from listed

firms in Hong Kong." The British Accounting Review 48, no. 2 (2016): 206-219.

Chen, Ching-Lung, and Pin-Yu Lin. "Real Earnings Management and Subsequent Accounting

Performance: The moderating role of corporate governance." 61 (2015): 1-36.

De Klerk, Marna, Charl de Villiers, and Chris van Staden. "The influence of corporate social

responsibility disclosure on share prices: evidence from the United Kingdom." Pacific

Accounting Review 27, no. 2 (2015): 208-228.

Duska, Ronald F., Brenda Shay Duska, and Kenneth Wm Kury. Accounting ethics. Wiley-

Blackwell, 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.