Management Accounting Report: Eastern Engineering Co Limited Analysis

VerifiedAdded on 2022/12/09

|18

|4646

|362

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within the context of Eastern Engineering Co Limited, a medium-sized manufacturing enterprise. The report begins by defining management accounting and its importance, emphasizing its role in financial decision-making, record-keeping, and performance evaluation. It explores various management accounting systems, including cost accounting, price optimization, inventory management, and job order costing, detailing their requirements and benefits. The report then delves into different methods of management accounting reporting, such as budgetary reports, performance reports, and accounts receivable reports. It presents income statements using both marginal and absorption costing techniques and interprets the resulting financial data. Furthermore, the report evaluates the pros and cons of budgetary control as a planning tool, analyzing its role in financial planning and forecasting. Finally, it assesses the adoption of management accounting systems in solving financial problems, concluding with an analysis of how organizations respond to financial challenges and achieve sustainable business success. The report includes an examination of cost accounting systems, marginal costing, and absorption costing, with practical applications and interpretations of data to improve financial performance and make informed business decisions.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and the necessity of management accounting system...................3

P2. Methods in management accounting reporting....................................................................5

M1. Evaluate the benefits of management accounting system....................................................5

D1. Management accounting system are critically evaluated with reports of management

accounting....................................................................................................................................6

TASK 2............................................................................................................................................6

P3. Different methods of cost in preparing the income statement...............................................6

M2. Application of range of techniques......................................................................................7

D2. Interpretation of data used in producing financial reports....................................................8

TASK 3............................................................................................................................................8

P4. Pros and Cons of budgetary control’s planning tool.............................................................8

M3. Analyze the different planning tool which helps in preparation as well as forecasting

budgets.........................................................................................................................................9

D3. Evaluation of planning tool in business.............................................................................10

TASK 4..........................................................................................................................................10

P5. Comparing adoption of management accounting system in order to solve financial

problems....................................................................................................................................10

M4. Analysation of respond of organisation towards financial problem of organisation which

helps in sustainable success of business....................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Books and Journals:...................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Management accounting and the necessity of management accounting system...................3

P2. Methods in management accounting reporting....................................................................5

M1. Evaluate the benefits of management accounting system....................................................5

D1. Management accounting system are critically evaluated with reports of management

accounting....................................................................................................................................6

TASK 2............................................................................................................................................6

P3. Different methods of cost in preparing the income statement...............................................6

M2. Application of range of techniques......................................................................................7

D2. Interpretation of data used in producing financial reports....................................................8

TASK 3............................................................................................................................................8

P4. Pros and Cons of budgetary control’s planning tool.............................................................8

M3. Analyze the different planning tool which helps in preparation as well as forecasting

budgets.........................................................................................................................................9

D3. Evaluation of planning tool in business.............................................................................10

TASK 4..........................................................................................................................................10

P5. Comparing adoption of management accounting system in order to solve financial

problems....................................................................................................................................10

M4. Analysation of respond of organisation towards financial problem of organisation which

helps in sustainable success of business....................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Books and Journals:...................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management Accounting is a term which performs business activities into a numerical

manner in the form of analysation, interpretation, keeping records and data. These Management

Accounting technique and records help in decision making criteria so that the organization will

perform business practices effectively and improve the quality of performance Taking financial

decisions keeping data and records, forecasting business activities are the main part of

management accounting through which the business organisations formulate their accounts plan

and financial funding to regulate for the business activities. Therefore Management Accounting

play a vital role in all the business sectors in order to compare past and present results in an

accurate manner and evaluate the strategies according to them (Drury, 2018). This report is going

to be about Eastern engineering co Limited it is a medium size Enterprise into manufacturing

sector. It is specialised in maintenance and repairing the motor vehicles into UK. This project is

going to evaluate the essential requirement of accounting system and different methods of

Management Accounting reporting by applying it to real business practice. Also the project is

going to apply a range of techniques to reduce financial problems by showing the advantages and

disadvantages of planning tool in relation to budgetary control. So the whole work will decide

the sustainable success of business through Management Accounting practices.

TASK 1

P1. Management accounting and thenecessity of management accounting system

Management accounting can be defined as a financial statement in which information are

recorded, measured and interpreted which helps to make decisions related to finance of

enterprise. It provides direction to the managers to make rational decision which make sure the

control over budget of the business. Financial statement are the basis of management accounting

which serves every data which are related to the business operations such as where are they

getting funds and what are the areas in which they are investing those funds. It includes planning,

budgeting, and other rational decisions which ensures by the account manager of eastern

engineering company (Tappura et al 2015).

Cost accounting system:

Management Accounting is a term which performs business activities into a numerical

manner in the form of analysation, interpretation, keeping records and data. These Management

Accounting technique and records help in decision making criteria so that the organization will

perform business practices effectively and improve the quality of performance Taking financial

decisions keeping data and records, forecasting business activities are the main part of

management accounting through which the business organisations formulate their accounts plan

and financial funding to regulate for the business activities. Therefore Management Accounting

play a vital role in all the business sectors in order to compare past and present results in an

accurate manner and evaluate the strategies according to them (Drury, 2018). This report is going

to be about Eastern engineering co Limited it is a medium size Enterprise into manufacturing

sector. It is specialised in maintenance and repairing the motor vehicles into UK. This project is

going to evaluate the essential requirement of accounting system and different methods of

Management Accounting reporting by applying it to real business practice. Also the project is

going to apply a range of techniques to reduce financial problems by showing the advantages and

disadvantages of planning tool in relation to budgetary control. So the whole work will decide

the sustainable success of business through Management Accounting practices.

TASK 1

P1. Management accounting and thenecessity of management accounting system

Management accounting can be defined as a financial statement in which information are

recorded, measured and interpreted which helps to make decisions related to finance of

enterprise. It provides direction to the managers to make rational decision which make sure the

control over budget of the business. Financial statement are the basis of management accounting

which serves every data which are related to the business operations such as where are they

getting funds and what are the areas in which they are investing those funds. It includes planning,

budgeting, and other rational decisions which ensures by the account manager of eastern

engineering company (Tappura et al 2015).

Cost accounting system:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting system is one of the system of management accounting which supports

managers to create estimation for the cost of production of goods and services that creates

turnover for the company. It supports in the valuation of inventory and control of budget of the

business.By estimating cost helps in examination of profitable product and non-profitable

product which offered by an organisation in the market. This system helps the manager to

identify total cost which includes product as well as service. It involves both fixed cost and

variable cost. Fixed cost is those costs which are fixed in the production process and life of the

form whereas variable cost is those cost which varies in the production process with one

addition. Cost is incurred by the purchase of raw material to the end selling of goods and services

of the business and its whole process is related with supply chain management (Van der Stede,

2015).

Requirement of Cost accounting system: Cost accounting system is used on the basis of the

size of the firm.It is the advantageous to the organisation as helps in achieving economy of scale

by reducing production cost of the Eastern Engineering Company (Abdusalomova, 2019).

Price Optimisation System:

Price optimisation system is one of those functions which are constructed on the

mathematical programs and which is used to calculate prices.This system supports in

reviewingdissimilarity in demand at different level of prices. Data which are related to cost as

well as inventory level can be done by this system. The main role of the system is to control the

prices of the product and services which help in generating the required amount of profit.This

system makes firm to use their prices as a competitive advantage. It could also help the account

manager in forecasting of demand, promotion of strategies, developing price in order to serve

best to their customers (Shields, 2015).

Requirement of Price optimisation System: This system helps manager in the estimation of

cost of product and services in the production process and decide on that price which generates

profit for the organisation. This method offers quick financial solution that helps in generating

more profit for the organization and also increases price differentiation according to the level of

demand (TRUHACHEV, KOSTYUKOVA and BOBRISHEV, 2017).

Inventory management System:

managers to create estimation for the cost of production of goods and services that creates

turnover for the company. It supports in the valuation of inventory and control of budget of the

business.By estimating cost helps in examination of profitable product and non-profitable

product which offered by an organisation in the market. This system helps the manager to

identify total cost which includes product as well as service. It involves both fixed cost and

variable cost. Fixed cost is those costs which are fixed in the production process and life of the

form whereas variable cost is those cost which varies in the production process with one

addition. Cost is incurred by the purchase of raw material to the end selling of goods and services

of the business and its whole process is related with supply chain management (Van der Stede,

2015).

Requirement of Cost accounting system: Cost accounting system is used on the basis of the

size of the firm.It is the advantageous to the organisation as helps in achieving economy of scale

by reducing production cost of the Eastern Engineering Company (Abdusalomova, 2019).

Price Optimisation System:

Price optimisation system is one of those functions which are constructed on the

mathematical programs and which is used to calculate prices.This system supports in

reviewingdissimilarity in demand at different level of prices. Data which are related to cost as

well as inventory level can be done by this system. The main role of the system is to control the

prices of the product and services which help in generating the required amount of profit.This

system makes firm to use their prices as a competitive advantage. It could also help the account

manager in forecasting of demand, promotion of strategies, developing price in order to serve

best to their customers (Shields, 2015).

Requirement of Price optimisation System: This system helps manager in the estimation of

cost of product and services in the production process and decide on that price which generates

profit for the organisation. This method offers quick financial solution that helps in generating

more profit for the organization and also increases price differentiation according to the level of

demand (TRUHACHEV, KOSTYUKOVA and BOBRISHEV, 2017).

Inventory management System:

To track inventory in the process of supply chain management as a whole that is from

purchase of raw material to the end result is understand as an inventory management system.

This system benefits managers in the activities such as preparing bill for materials, preparing

work order, products which are related business materials (Modell, 2014). This system functions

in minimizing state of under stock or over stock. This data is also used to collect data which

relates to inventory level in organization to avoid wastage. There is no difficulty to understand

this system and permits managers to make coordination between various activities.

Requirement of Inventory management system: This system help the business to reduce cost

of managing inventory. It also supports manager of connect catering service in the inventory

management according to the capacity of warehouse which provides stock details, satisfaction of

product and history of the product. It also helps manager to track inventory to avoid any waste of

material and inventory level (Hopper and Bui, 2016). It makes sure to control additional

purchase of raw material because it can increase the cost of warehouse.

Job order costing system:

Job order costing system can be understand as a system through which organisations take

support when they produces varieties of products and in range of units. By the use of this system

managers can identify the price of each and every product which are dissimilar and help them to

earn revenue for the enterprise. It involves information such as invoices of supplier, prices of

material, allocation of overhead to various activities as well as records of payroll. This is the

tracking in records of job which might be used in the production process of products and

services.

Requirement of Job order costing system: It helps manager to determine the cost of each and

every activities and job in the organisation. It also helps to know the profit of each and every

activity to take appropriate decisions. This supports manager to look out how companies have

fixing their assets anddifferent cost are produced for different jobs (Malmi, 2016).

P2. Methods in management accounting reporting

Budgetary report: Budget report is the report which has been used to compare the actual

performance by the planned budget.By budgeting, this report supports the manager to find out

those expenses which are high so that they take appropriate decisions to reduce the level of

purchase of raw material to the end result is understand as an inventory management system.

This system benefits managers in the activities such as preparing bill for materials, preparing

work order, products which are related business materials (Modell, 2014). This system functions

in minimizing state of under stock or over stock. This data is also used to collect data which

relates to inventory level in organization to avoid wastage. There is no difficulty to understand

this system and permits managers to make coordination between various activities.

Requirement of Inventory management system: This system help the business to reduce cost

of managing inventory. It also supports manager of connect catering service in the inventory

management according to the capacity of warehouse which provides stock details, satisfaction of

product and history of the product. It also helps manager to track inventory to avoid any waste of

material and inventory level (Hopper and Bui, 2016). It makes sure to control additional

purchase of raw material because it can increase the cost of warehouse.

Job order costing system:

Job order costing system can be understand as a system through which organisations take

support when they produces varieties of products and in range of units. By the use of this system

managers can identify the price of each and every product which are dissimilar and help them to

earn revenue for the enterprise. It involves information such as invoices of supplier, prices of

material, allocation of overhead to various activities as well as records of payroll. This is the

tracking in records of job which might be used in the production process of products and

services.

Requirement of Job order costing system: It helps manager to determine the cost of each and

every activities and job in the organisation. It also helps to know the profit of each and every

activity to take appropriate decisions. This supports manager to look out how companies have

fixing their assets anddifferent cost are produced for different jobs (Malmi, 2016).

P2. Methods in management accounting reporting

Budgetary report: Budget report is the report which has been used to compare the actual

performance by the planned budget.By budgeting, this report supports the manager to find out

those expenses which are high so that they take appropriate decisions to reduce the level of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenses as per the amount of budget.Basically, this report can be defined as a tool that controls

financial budget of a company.

Performance report: This report is the report which has been used to measure

performance of the employee, department, or an organisation. This report supports manager to

recognising the employees who is working hard and in efficient manner and who are inefficient

and underperformance.With the help of this report, they offer performance appraisal to the

efficient employees and on the other hand; they can terminate or punish the employees who are

underperformance.

Account receivable report: Account receivable reports are the reports which support to

identify the clients whose payment is outstanding. If the report is showing the amount which

have to be received increases then employers need to make modifications in their policy of

collection as it led to lack of funds in the company.

M1. Evaluate the benefits of management accounting system

Management accounting

System

Benefit and application of management accounting system

Cost accounting system Cost accounting provides benefits to manager of connect

catering services as it supports in reducing the overall cost of

production and improve the profitability level of the company.

Inventory Management

System

Inventory management system assist the manager in order to

track inventory management to identify the requirements of raw

material and to avoid any wastage as excess purchasing of raw

materials can lead to increase the cost of warehouse to keeping

the raw material at the workplace (Bobryshev et al 2015).

Job order costing System In order to reduce the cost per job it is one of the useful method

in the management accounting system.

Price optimisation System In order to identify the best price for the proposing product that

can be a support in producing demand and generates the more

financial budget of a company.

Performance report: This report is the report which has been used to measure

performance of the employee, department, or an organisation. This report supports manager to

recognising the employees who is working hard and in efficient manner and who are inefficient

and underperformance.With the help of this report, they offer performance appraisal to the

efficient employees and on the other hand; they can terminate or punish the employees who are

underperformance.

Account receivable report: Account receivable reports are the reports which support to

identify the clients whose payment is outstanding. If the report is showing the amount which

have to be received increases then employers need to make modifications in their policy of

collection as it led to lack of funds in the company.

M1. Evaluate the benefits of management accounting system

Management accounting

System

Benefit and application of management accounting system

Cost accounting system Cost accounting provides benefits to manager of connect

catering services as it supports in reducing the overall cost of

production and improve the profitability level of the company.

Inventory Management

System

Inventory management system assist the manager in order to

track inventory management to identify the requirements of raw

material and to avoid any wastage as excess purchasing of raw

materials can lead to increase the cost of warehouse to keeping

the raw material at the workplace (Bobryshev et al 2015).

Job order costing System In order to reduce the cost per job it is one of the useful method

in the management accounting system.

Price optimisation System In order to identify the best price for the proposing product that

can be a support in producing demand and generates the more

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit for the organisation, this method can be very beneficial.

D1. Management accounting system are critically evaluated with reportsof management

accounting

In order to reduce the extra price of the company and increased level of productivity and

profitability, the management accounting system and Management accounting reports are

integrated in the respective organisation. This method assists the organisation to bring up the

close results which are actual with the amounts of budget and it provides guarantee to control

more over the operational activities. This method also supports manager to monitor each and

every activity of the company and improve their overall performance (Alborov et al 2017).

TASK 2

P3. Different methods of cost in preparing the income statement.

income statement

quarter 1

particulars

amount

in $

sales 66000

less: cost of sales

opening inventory 0

production cost ( 78000*0.65)

5070

0

less: closing stock (1200*0.65) 7800

4290

0 42900

contribution 23100

less

fixed overhead

1600

0

D1. Management accounting system are critically evaluated with reportsof management

accounting

In order to reduce the extra price of the company and increased level of productivity and

profitability, the management accounting system and Management accounting reports are

integrated in the respective organisation. This method assists the organisation to bring up the

close results which are actual with the amounts of budget and it provides guarantee to control

more over the operational activities. This method also supports manager to monitor each and

every activity of the company and improve their overall performance (Alborov et al 2017).

TASK 2

P3. Different methods of cost in preparing the income statement.

income statement

quarter 1

particulars

amount

in $

sales 66000

less: cost of sales

opening inventory 0

production cost ( 78000*0.65)

5070

0

less: closing stock (1200*0.65) 7800

4290

0 42900

contribution 23100

less

fixed overhead

1600

0

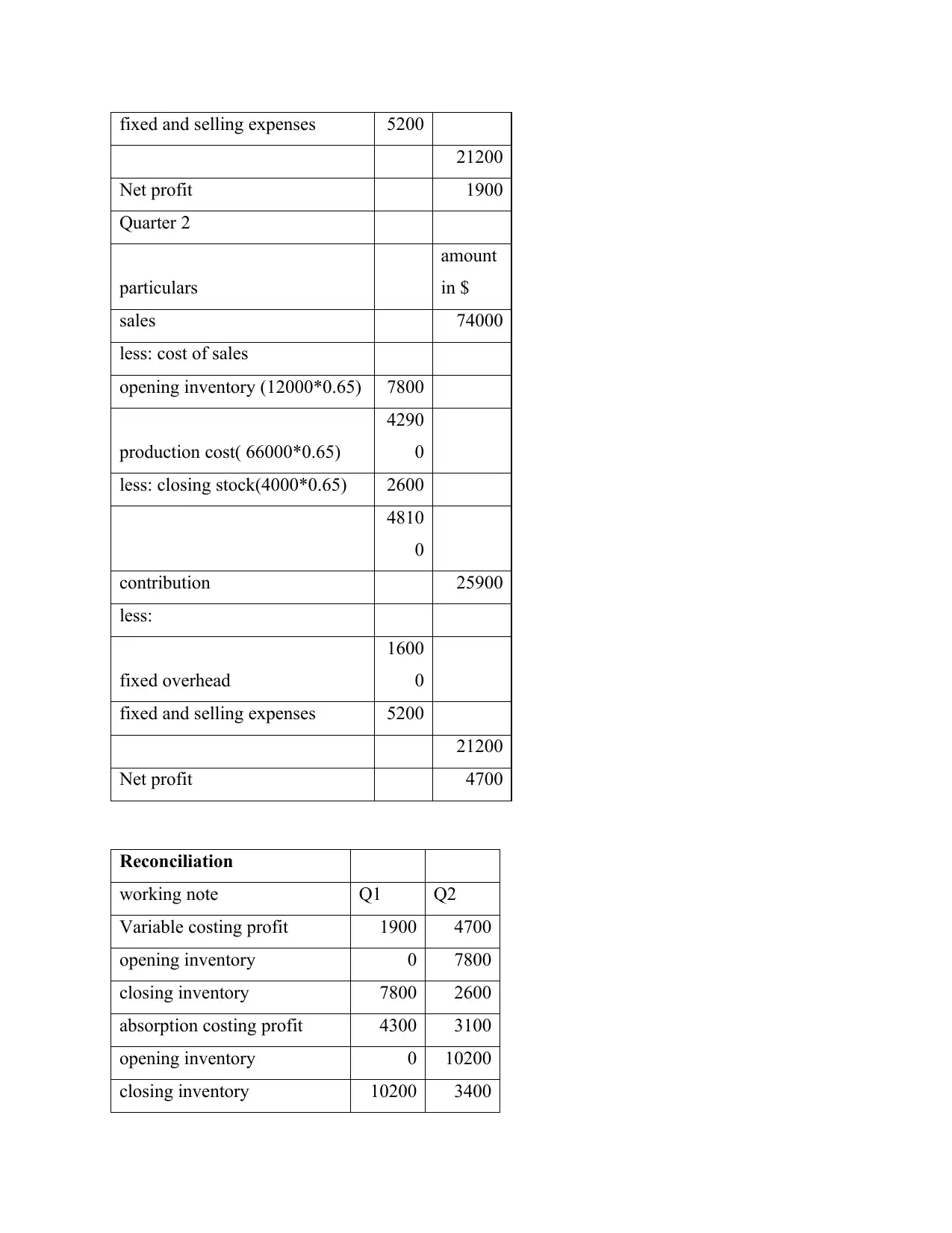

fixed and selling expenses 5200

21200

Net profit 1900

Quarter 2

particulars

amount

in $

sales 74000

less: cost of sales

opening inventory (12000*0.65) 7800

production cost( 66000*0.65)

4290

0

less: closing stock(4000*0.65) 2600

4810

0

contribution 25900

less:

fixed overhead

1600

0

fixed and selling expenses 5200

21200

Net profit 4700

Reconciliation

working note Q1 Q2

Variable costing profit 1900 4700

opening inventory 0 7800

closing inventory 7800 2600

absorption costing profit 4300 3100

opening inventory 0 10200

closing inventory 10200 3400

21200

Net profit 1900

Quarter 2

particulars

amount

in $

sales 74000

less: cost of sales

opening inventory (12000*0.65) 7800

production cost( 66000*0.65)

4290

0

less: closing stock(4000*0.65) 2600

4810

0

contribution 25900

less:

fixed overhead

1600

0

fixed and selling expenses 5200

21200

Net profit 4700

Reconciliation

working note Q1 Q2

Variable costing profit 1900 4700

opening inventory 0 7800

closing inventory 7800 2600

absorption costing profit 4300 3100

opening inventory 0 10200

closing inventory 10200 3400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2. Application of range of techniques.

Marginal costing: Marginal cost is the cost of one extra unit of production. This method

is used to consider the quantity of production for organisation where cost are considered as the

least price to produce extra.

Absorption techniques:Absorption technique can be understand as a method which adds

extra proportion of the direct cost and production overhead to the cost of production. This

includes the cost of inventory which involves the full price of production for a product

manufacturing (Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, M.S.K., 2021).

D2. Interpretation of data used in producing financial reports

It has been analysed from the above calculation that quarters of opening inventory from

marginal costing is not more than an absorption inventory. There is also difference between net

profits of the company. 1900 pounds are the net profits from abortion costing while 4700 pounds

are derived from marginal costing.

TASK 3

P4. Pros and Cons of budgetary control’s planning tool.

Budgetary control:Budgetary control is a financial terminology for dealing revenue and

expenses. In order to identify the actions are required or not in managing income and expenditure

is means of budgetary control;some of them are as follows:

Zero based budgeting: Zero based budgeting is one of those approach with supports in

the preparation of budget that starts from zero. This budget is prepared for every New Year not

on the basis of previous year. It is vital for managers to validate several expenses before this can

be applied in official budget. Preparing zero based budgeting is a process which includes

recognition of objectives to prepare budget.It may also include the recognition of several ways to

accomplish those goals.It helps employers to access several ways to get financial funds for the

company and support in prioritising funds on the basis of cost and availability (Maas, K.,

Schaltegger and Crutzen, 2016).

Marginal costing: Marginal cost is the cost of one extra unit of production. This method

is used to consider the quantity of production for organisation where cost are considered as the

least price to produce extra.

Absorption techniques:Absorption technique can be understand as a method which adds

extra proportion of the direct cost and production overhead to the cost of production. This

includes the cost of inventory which involves the full price of production for a product

manufacturing (Maheshwari, S.N., Maheshwari, S.K. and Maheshwari, M.S.K., 2021).

D2. Interpretation of data used in producing financial reports

It has been analysed from the above calculation that quarters of opening inventory from

marginal costing is not more than an absorption inventory. There is also difference between net

profits of the company. 1900 pounds are the net profits from abortion costing while 4700 pounds

are derived from marginal costing.

TASK 3

P4. Pros and Cons of budgetary control’s planning tool.

Budgetary control:Budgetary control is a financial terminology for dealing revenue and

expenses. In order to identify the actions are required or not in managing income and expenditure

is means of budgetary control;some of them are as follows:

Zero based budgeting: Zero based budgeting is one of those approach with supports in

the preparation of budget that starts from zero. This budget is prepared for every New Year not

on the basis of previous year. It is vital for managers to validate several expenses before this can

be applied in official budget. Preparing zero based budgeting is a process which includes

recognition of objectives to prepare budget.It may also include the recognition of several ways to

accomplish those goals.It helps employers to access several ways to get financial funds for the

company and support in prioritising funds on the basis of cost and availability (Maas, K.,

Schaltegger and Crutzen, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage of zero-based budgeting:

It helps an organisation in preparing budget which help them to control access cost of the

company.

It is intended to reduce cost of the company with improved profitability level of the

organisation.

It supports employees by serving information that relates to use of funds in the business.

Managers of connect catering service supports and organisation to create budget and

reducing the cost of operation.

Disadvantage of zero-based budgeting:

It is an expensive tool that managers need to invest their time and efforts.

As it is not connected with intangibility it delivers information relates to all department of

the organisation but there are some information that should be bound to expose in front of

managers of the company.

It is a complex tool that manager required preparing zero based budget for every New

Year as it is not based on the performance of the last year (Nielsen, Mitchell and

Nørreklit, 2015).

Variance analysis: Variance analysis is a process of analysis of difference between actual result

and the estimated performance of the organisation.It supports manager to assist the planning

whether the company is getting over performance or underperformance. The variance analysis

can be acknowledged in making differences between actual cost of business as well as the

standard cost of business. This method is used to calculate both quantity of labour, material,

overhead and prices of thecompany. It will also help manager to identify the issue in the

operations of the company and make them to prepare strategies that can improve the overall

performance.

Advantage of Variance analysis:

It provide competitive advantage to the company that helps to capture the market.

Helps employees to accomplish the desired objective and it also helps in managing the

strategies for business.

It helps an organisation in preparing budget which help them to control access cost of the

company.

It is intended to reduce cost of the company with improved profitability level of the

organisation.

It supports employees by serving information that relates to use of funds in the business.

Managers of connect catering service supports and organisation to create budget and

reducing the cost of operation.

Disadvantage of zero-based budgeting:

It is an expensive tool that managers need to invest their time and efforts.

As it is not connected with intangibility it delivers information relates to all department of

the organisation but there are some information that should be bound to expose in front of

managers of the company.

It is a complex tool that manager required preparing zero based budget for every New

Year as it is not based on the performance of the last year (Nielsen, Mitchell and

Nørreklit, 2015).

Variance analysis: Variance analysis is a process of analysis of difference between actual result

and the estimated performance of the organisation.It supports manager to assist the planning

whether the company is getting over performance or underperformance. The variance analysis

can be acknowledged in making differences between actual cost of business as well as the

standard cost of business. This method is used to calculate both quantity of labour, material,

overhead and prices of thecompany. It will also help manager to identify the issue in the

operations of the company and make them to prepare strategies that can improve the overall

performance.

Advantage of Variance analysis:

It provide competitive advantage to the company that helps to capture the market.

Helps employees to accomplish the desired objective and it also helps in managing the

strategies for business.

It helps in identification of risk which supports managers to solve problems for the

business.

Disadvantage of Variance analysis:

It can be the reason for delaying in completion of task.

Sometimes it may be difficult to identify the cause behind variance to company.

This method is not suitable of managers of connect catering service as it gives the reason

of delaying and in getting result of the task (Weetman, 2019).

Operating budget: Operating budget is one of those budgets which involve both expenses and

profit which are generated by the company. This budget is mainly focus on the expenses of

operation of the business which includes cost of goods sold which is directly linked with the

production process and also it include cost of direct material and labour. Operating budget

involves all the cost and administration overhead which is related with the production process of

the company.

Advantage of operating budget:

It helps in the requirements of long term planning which assist them to allocate funds in

several activities which has to be conducted in the business.

It allows flexibility in budget preparation.

It is helpful for managers of connect catering services as it offers right information.

Disadvantage of Operating budget:

Operating budget is difficult for business as it does not facilitate changes and flexibility.

Operating budget discourage information which is not right for the development of the

company

M3. Analyze the different planning tool which helps in preparation as well as forecasting

budgets

There are various tools and methods for planning that can be used to control actual result

of the organizational activities. The company may use various tools and techniques such as zero

based budgeting, operating budgeting and variance analysis. Variance analysis is a method which

business.

Disadvantage of Variance analysis:

It can be the reason for delaying in completion of task.

Sometimes it may be difficult to identify the cause behind variance to company.

This method is not suitable of managers of connect catering service as it gives the reason

of delaying and in getting result of the task (Weetman, 2019).

Operating budget: Operating budget is one of those budgets which involve both expenses and

profit which are generated by the company. This budget is mainly focus on the expenses of

operation of the business which includes cost of goods sold which is directly linked with the

production process and also it include cost of direct material and labour. Operating budget

involves all the cost and administration overhead which is related with the production process of

the company.

Advantage of operating budget:

It helps in the requirements of long term planning which assist them to allocate funds in

several activities which has to be conducted in the business.

It allows flexibility in budget preparation.

It is helpful for managers of connect catering services as it offers right information.

Disadvantage of Operating budget:

Operating budget is difficult for business as it does not facilitate changes and flexibility.

Operating budget discourage information which is not right for the development of the

company

M3. Analyze the different planning tool which helps in preparation as well as forecasting

budgets

There are various tools and methods for planning that can be used to control actual result

of the organizational activities. The company may use various tools and techniques such as zero

based budgeting, operating budgeting and variance analysis. Variance analysis is a method which

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.