EastJet Audit Project: Planning, Risk, and Materiality

VerifiedAdded on 2019/09/16

|7

|1549

|300

Project

AI Summary

This project provides a comprehensive audit of EastJet, a small airline, focusing on the fiscal year ending December 31, 2016. The project addresses several key aspects of the audit process, including performing a planning analytical review of the financial statements, identifying and explaining audit risks, and designing appropriate audit approaches. It involves calculating planning materiality, evaluating the work of a junior auditor on accounts receivable and property, plant, and equipment, and developing a PPE audit program. The project also discusses the importance of documentation in the audit file and concludes with the drafting of an audit report, considering a material but not pervasive misstatement related to capital leases. The solution covers all required elements, including analysis, risk assessment, procedure design, and reporting, providing a complete response to the assignment brief.

Nadu

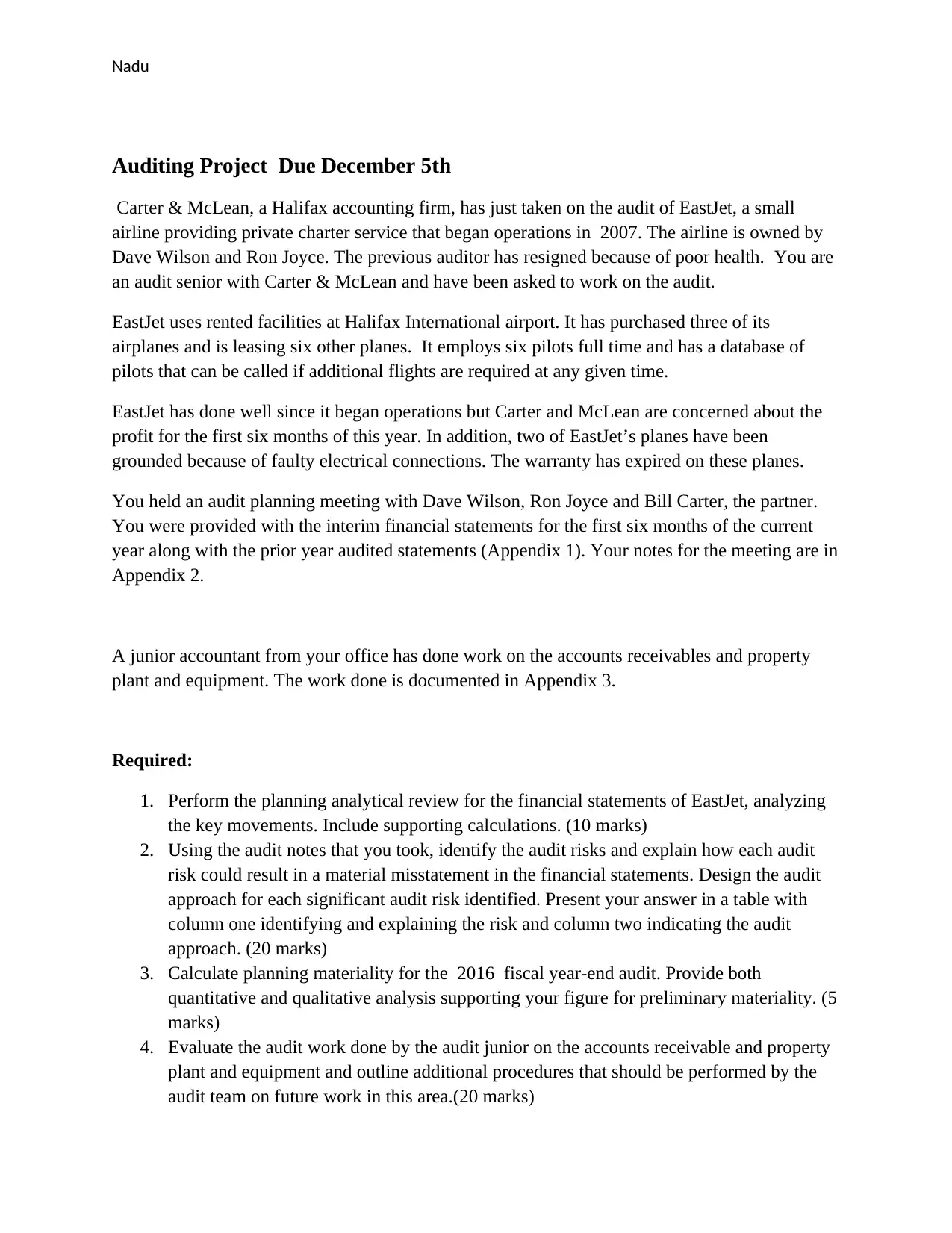

Auditing Project Due December 5th

Carter & McLean, a Halifax accounting firm, has just taken on the audit of EastJet, a small

airline providing private charter service that began operations in 2007. The airline is owned by

Dave Wilson and Ron Joyce. The previous auditor has resigned because of poor health. You are

an audit senior with Carter & McLean and have been asked to work on the audit.

EastJet uses rented facilities at Halifax International airport. It has purchased three of its

airplanes and is leasing six other planes. It employs six pilots full time and has a database of

pilots that can be called if additional flights are required at any given time.

EastJet has done well since it began operations but Carter and McLean are concerned about the

profit for the first six months of this year. In addition, two of EastJet’s planes have been

grounded because of faulty electrical connections. The warranty has expired on these planes.

You held an audit planning meeting with Dave Wilson, Ron Joyce and Bill Carter, the partner.

You were provided with the interim financial statements for the first six months of the current

year along with the prior year audited statements (Appendix 1). Your notes for the meeting are in

Appendix 2.

A junior accountant from your office has done work on the accounts receivables and property

plant and equipment. The work done is documented in Appendix 3.

Required:

1. Perform the planning analytical review for the financial statements of EastJet, analyzing

the key movements. Include supporting calculations. (10 marks)

2. Using the audit notes that you took, identify the audit risks and explain how each audit

risk could result in a material misstatement in the financial statements. Design the audit

approach for each significant audit risk identified. Present your answer in a table with

column one identifying and explaining the risk and column two indicating the audit

approach. (20 marks)

3. Calculate planning materiality for the 2016 fiscal year-end audit. Provide both

quantitative and qualitative analysis supporting your figure for preliminary materiality. (5

marks)

4. Evaluate the audit work done by the audit junior on the accounts receivable and property

plant and equipment and outline additional procedures that should be performed by the

audit team on future work in this area.(20 marks)

Auditing Project Due December 5th

Carter & McLean, a Halifax accounting firm, has just taken on the audit of EastJet, a small

airline providing private charter service that began operations in 2007. The airline is owned by

Dave Wilson and Ron Joyce. The previous auditor has resigned because of poor health. You are

an audit senior with Carter & McLean and have been asked to work on the audit.

EastJet uses rented facilities at Halifax International airport. It has purchased three of its

airplanes and is leasing six other planes. It employs six pilots full time and has a database of

pilots that can be called if additional flights are required at any given time.

EastJet has done well since it began operations but Carter and McLean are concerned about the

profit for the first six months of this year. In addition, two of EastJet’s planes have been

grounded because of faulty electrical connections. The warranty has expired on these planes.

You held an audit planning meeting with Dave Wilson, Ron Joyce and Bill Carter, the partner.

You were provided with the interim financial statements for the first six months of the current

year along with the prior year audited statements (Appendix 1). Your notes for the meeting are in

Appendix 2.

A junior accountant from your office has done work on the accounts receivables and property

plant and equipment. The work done is documented in Appendix 3.

Required:

1. Perform the planning analytical review for the financial statements of EastJet, analyzing

the key movements. Include supporting calculations. (10 marks)

2. Using the audit notes that you took, identify the audit risks and explain how each audit

risk could result in a material misstatement in the financial statements. Design the audit

approach for each significant audit risk identified. Present your answer in a table with

column one identifying and explaining the risk and column two indicating the audit

approach. (20 marks)

3. Calculate planning materiality for the 2016 fiscal year-end audit. Provide both

quantitative and qualitative analysis supporting your figure for preliminary materiality. (5

marks)

4. Evaluate the audit work done by the audit junior on the accounts receivable and property

plant and equipment and outline additional procedures that should be performed by the

audit team on future work in this area.(20 marks)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nadu

5. Prepare the property, plant and equipment (PPE) audit program that will be used by

Carter & McLean accounting for the December 31, 2016, fiscal year-end audit of EastJet.

(20 Marks)

6. Discuss the importance of documentation in the audit file and identify which parts of the

audit file require documentation.(10 marks)

7. Assume the 2016 fiscal year-end audit of EastJet is completed and that Carter and

McLean Accounting has determined that the financial statements of EastJet are presented

fairly, in all material respects, except for the area of capital leases. Capital leases are

material. Your audit work indicated the two capital leases should be accounted for as

capital leases; however, EastJet did not want to do this. The amount is material but not

pervasive to the financial statements. Draft the expected audit report that will be issued

by Carter and Mclean Accounting for this engagement. Assume that the financial

statements of EastJet are prepared under one of the two general purpose accounting

frameworks used in Canada.(15 marks)

5. Prepare the property, plant and equipment (PPE) audit program that will be used by

Carter & McLean accounting for the December 31, 2016, fiscal year-end audit of EastJet.

(20 Marks)

6. Discuss the importance of documentation in the audit file and identify which parts of the

audit file require documentation.(10 marks)

7. Assume the 2016 fiscal year-end audit of EastJet is completed and that Carter and

McLean Accounting has determined that the financial statements of EastJet are presented

fairly, in all material respects, except for the area of capital leases. Capital leases are

material. Your audit work indicated the two capital leases should be accounted for as

capital leases; however, EastJet did not want to do this. The amount is material but not

pervasive to the financial statements. Draft the expected audit report that will be issued

by Carter and Mclean Accounting for this engagement. Assume that the financial

statements of EastJet are prepared under one of the two general purpose accounting

frameworks used in Canada.(15 marks)

Nadu

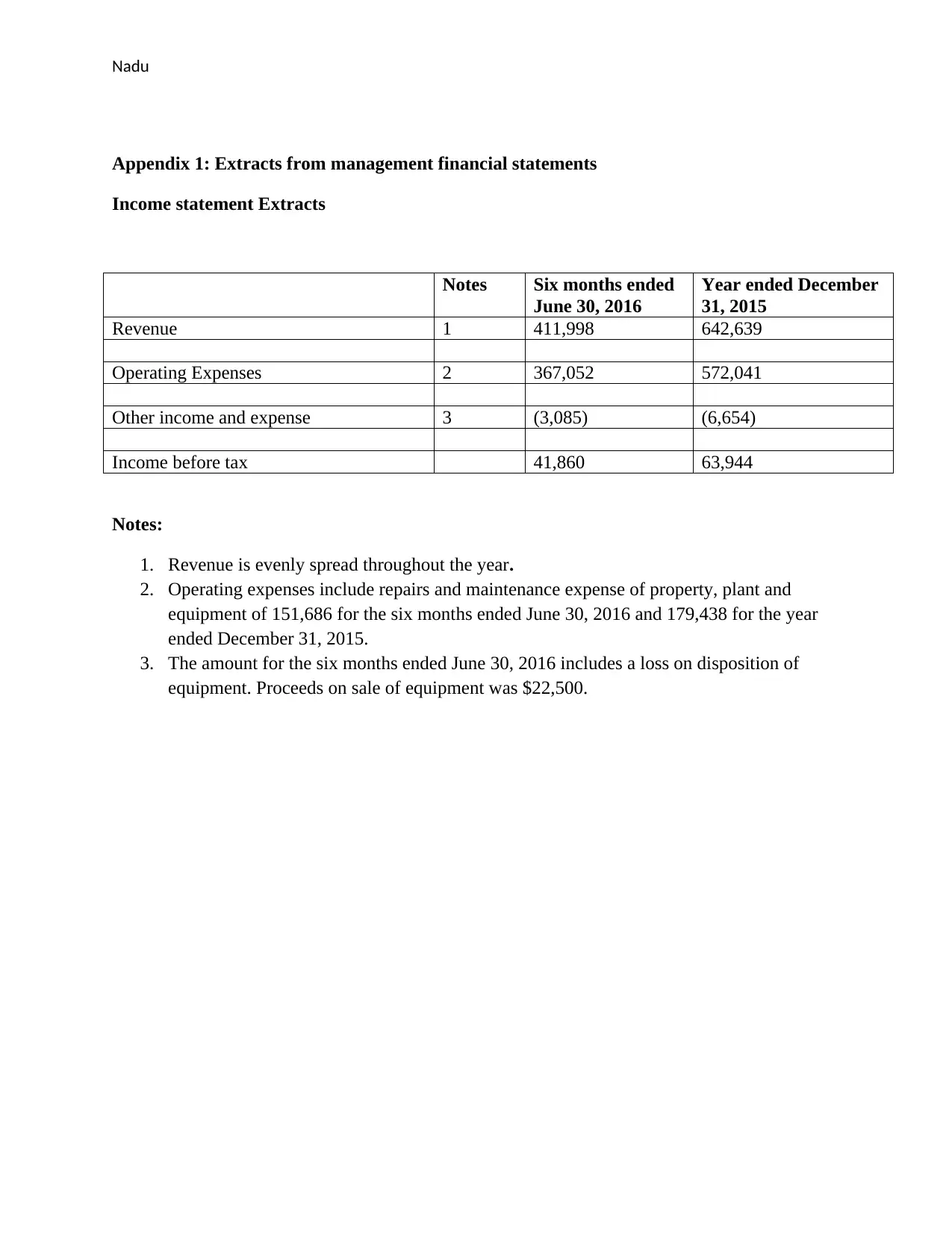

Appendix 1: Extracts from management financial statements

Income statement Extracts

Notes Six months ended

June 30, 2016

Year ended December

31, 2015

Revenue 1 411,998 642,639

Operating Expenses 2 367,052 572,041

Other income and expense 3 (3,085) (6,654)

Income before tax 41,860 63,944

Notes:

1. Revenue is evenly spread throughout the year.

2. Operating expenses include repairs and maintenance expense of property, plant and

equipment of 151,686 for the six months ended June 30, 2016 and 179,438 for the year

ended December 31, 2015.

3. The amount for the six months ended June 30, 2016 includes a loss on disposition of

equipment. Proceeds on sale of equipment was $22,500.

Appendix 1: Extracts from management financial statements

Income statement Extracts

Notes Six months ended

June 30, 2016

Year ended December

31, 2015

Revenue 1 411,998 642,639

Operating Expenses 2 367,052 572,041

Other income and expense 3 (3,085) (6,654)

Income before tax 41,860 63,944

Notes:

1. Revenue is evenly spread throughout the year.

2. Operating expenses include repairs and maintenance expense of property, plant and

equipment of 151,686 for the six months ended June 30, 2016 and 179,438 for the year

ended December 31, 2015.

3. The amount for the six months ended June 30, 2016 includes a loss on disposition of

equipment. Proceeds on sale of equipment was $22,500.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Nadu

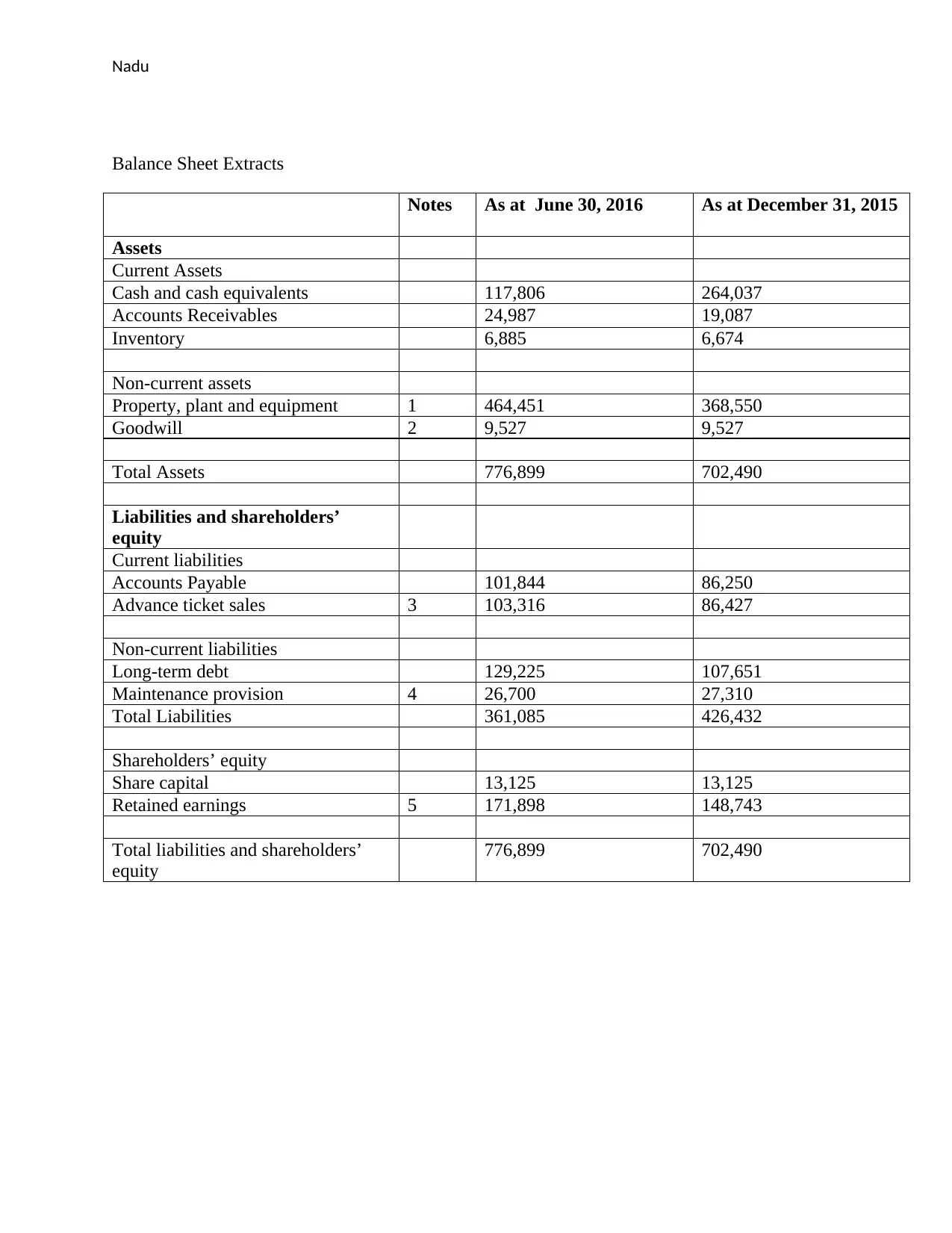

Balance Sheet Extracts

Notes As at June 30, 2016 As at December 31, 2015

Assets

Current Assets

Cash and cash equivalents 117,806 264,037

Accounts Receivables 24,987 19,087

Inventory 6,885 6,674

Non-current assets

Property, plant and equipment 1 464,451 368,550

Goodwill 2 9,527 9,527

Total Assets 776,899 702,490

Liabilities and shareholders’

equity

Current liabilities

Accounts Payable 101,844 86,250

Advance ticket sales 3 103,316 86,427

Non-current liabilities

Long-term debt 129,225 107,651

Maintenance provision 4 26,700 27,310

Total Liabilities 361,085 426,432

Shareholders’ equity

Share capital 13,125 13,125

Retained earnings 5 171,898 148,743

Total liabilities and shareholders’

equity

776,899 702,490

Balance Sheet Extracts

Notes As at June 30, 2016 As at December 31, 2015

Assets

Current Assets

Cash and cash equivalents 117,806 264,037

Accounts Receivables 24,987 19,087

Inventory 6,885 6,674

Non-current assets

Property, plant and equipment 1 464,451 368,550

Goodwill 2 9,527 9,527

Total Assets 776,899 702,490

Liabilities and shareholders’

equity

Current liabilities

Accounts Payable 101,844 86,250

Advance ticket sales 3 103,316 86,427

Non-current liabilities

Long-term debt 129,225 107,651

Maintenance provision 4 26,700 27,310

Total Liabilities 361,085 426,432

Shareholders’ equity

Share capital 13,125 13,125

Retained earnings 5 171,898 148,743

Total liabilities and shareholders’

equity

776,899 702,490

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Nadu

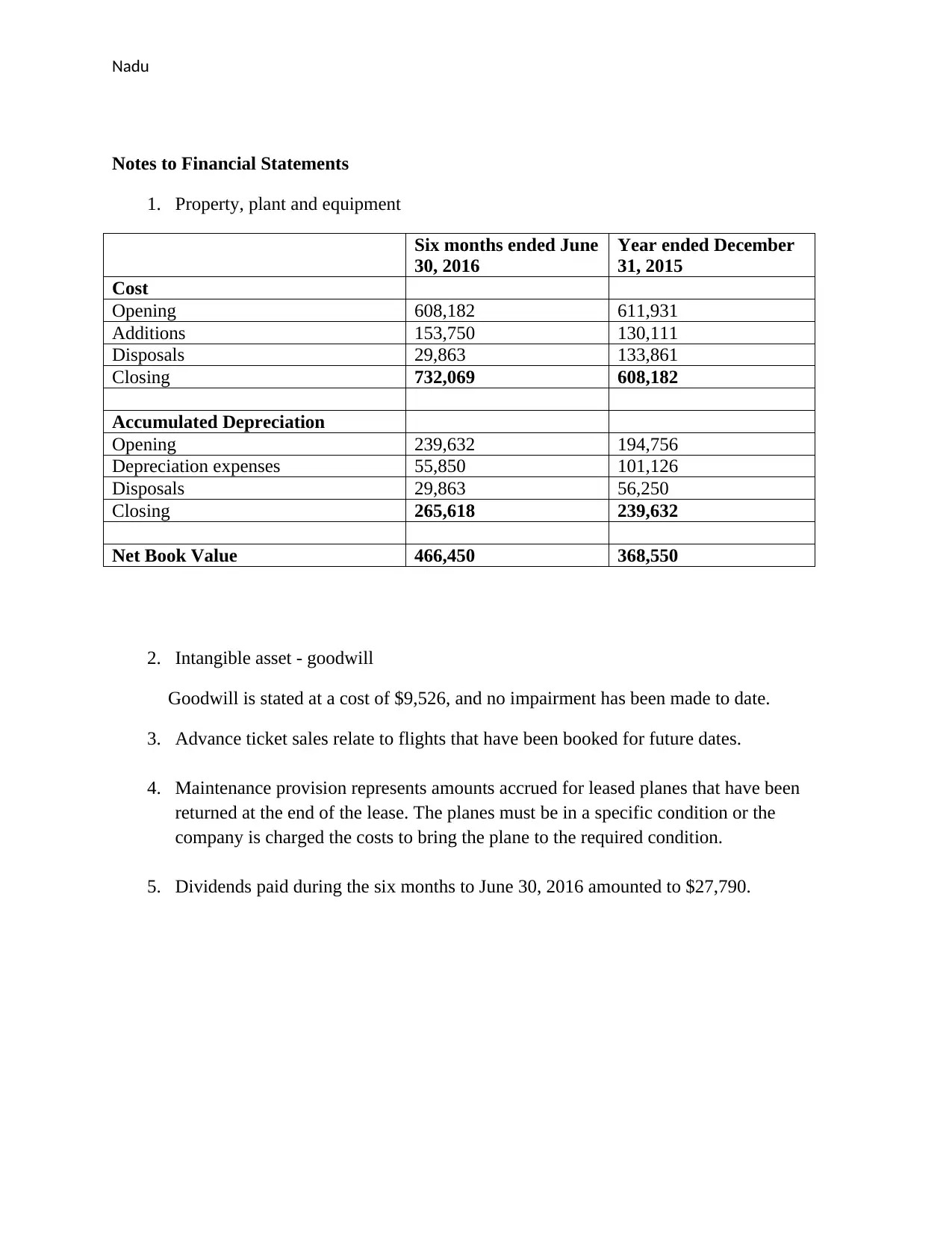

Notes to Financial Statements

1. Property, plant and equipment

Six months ended June

30, 2016

Year ended December

31, 2015

Cost

Opening 608,182 611,931

Additions 153,750 130,111

Disposals 29,863 133,861

Closing 732,069 608,182

Accumulated Depreciation

Opening 239,632 194,756

Depreciation expenses 55,850 101,126

Disposals 29,863 56,250

Closing 265,618 239,632

Net Book Value 466,450 368,550

2. Intangible asset - goodwill

Goodwill is stated at a cost of $9,526, and no impairment has been made to date.

3. Advance ticket sales relate to flights that have been booked for future dates.

4. Maintenance provision represents amounts accrued for leased planes that have been

returned at the end of the lease. The planes must be in a specific condition or the

company is charged the costs to bring the plane to the required condition.

5. Dividends paid during the six months to June 30, 2016 amounted to $27,790.

Notes to Financial Statements

1. Property, plant and equipment

Six months ended June

30, 2016

Year ended December

31, 2015

Cost

Opening 608,182 611,931

Additions 153,750 130,111

Disposals 29,863 133,861

Closing 732,069 608,182

Accumulated Depreciation

Opening 239,632 194,756

Depreciation expenses 55,850 101,126

Disposals 29,863 56,250

Closing 265,618 239,632

Net Book Value 466,450 368,550

2. Intangible asset - goodwill

Goodwill is stated at a cost of $9,526, and no impairment has been made to date.

3. Advance ticket sales relate to flights that have been booked for future dates.

4. Maintenance provision represents amounts accrued for leased planes that have been

returned at the end of the lease. The planes must be in a specific condition or the

company is charged the costs to bring the plane to the required condition.

5. Dividends paid during the six months to June 30, 2016 amounted to $27,790.

Nadu

Appendix 2: Notes from meeting

Dave Wilson and Ron Joyce explained that EastJet operates in a very competitive environment.

The economic downturn has resulted in fewer charter flights and airlines have been offering

reduced rates to remain competitive. EastJet has been paying strict attention to cost controls and

have introduced a bonus for management that is based on the company’s profitability.

Recently two of EastJet’s major customers have gone into bankruptcy. There is $41,250 in

advanced ticket sales related to these customers.

EastJet held a manager’s retreat last month to think of ways to boost the business. The company

intends on offering an exclusive business class service for business customers such that they can

fly to and from a major city in the same day. This service will begin in the new year. EastJet is

optimistic that there will be an 80% uptake of seats on these flights that will be offered from

Monday through Friday.

One of EastJet’s planes was damaged as a result of a fire in the cockpit. Although the plane was

insured the insurance company is disputing the claim because the company did not meet safety

standards that were required in the industry. The cost of the damage is estimated at $105,000.

Because EastJet is anticipating additional flights in the new year, it will need to lease or purchase

additional planes. EastJet has begun discussions with a leasing company in regards to leasing the

planes. They expect the leasing agreements to be in place by year end.

Appendix 2: Notes from meeting

Dave Wilson and Ron Joyce explained that EastJet operates in a very competitive environment.

The economic downturn has resulted in fewer charter flights and airlines have been offering

reduced rates to remain competitive. EastJet has been paying strict attention to cost controls and

have introduced a bonus for management that is based on the company’s profitability.

Recently two of EastJet’s major customers have gone into bankruptcy. There is $41,250 in

advanced ticket sales related to these customers.

EastJet held a manager’s retreat last month to think of ways to boost the business. The company

intends on offering an exclusive business class service for business customers such that they can

fly to and from a major city in the same day. This service will begin in the new year. EastJet is

optimistic that there will be an 80% uptake of seats on these flights that will be offered from

Monday through Friday.

One of EastJet’s planes was damaged as a result of a fire in the cockpit. Although the plane was

insured the insurance company is disputing the claim because the company did not meet safety

standards that were required in the industry. The cost of the damage is estimated at $105,000.

Because EastJet is anticipating additional flights in the new year, it will need to lease or purchase

additional planes. EastJet has begun discussions with a leasing company in regards to leasing the

planes. They expect the leasing agreements to be in place by year end.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Nadu

Appendix 3: Notes regarding the accounts receivable and property, plant and equipment

work performed by the junior auditor.

Accounts Receivables / Unearned Revenue

When clients book charter flights, the flight is prepaid and the amounts are recorded in unearned

revenue. Once the service has been provided (the client takes the flight) the unearned revenue

related to the flight is transferred to revenue.

Large well established clients do not have to prepay and are invoiced for the amounts of the

flights. These represent the accounts receivable amounts on the balance sheet. The prior year

audit file indicates there were issues with accounts receivables in prior years - Eastjet had

accounted for unearned revenue as accounts receivable.

The junior accountant performed analytical review on the accounts receivable noting that

percentage of accounts receivable as a percentage of total assets was consistent with the prior

year. There were several credit balances in accounts receivable which the junior ignored. No

confirmations of accounts receivable were performed. The junior auditor concluded the accounts

receivable were fairly stated for the interim period.

Property Plant and Equipment

Property plant and equipment represents the largest item on the balance sheet and represents the

planes that Eastjet owns as well as leased planes. They are separated in the general ledger

accounts. The junior auditor traced each item on the subsidiary ledger to the original invoice,

added the subsidiary ledger and agreed the total to the general ledger. Then the junior auditor

signed the working paper concluding that property plant and equipment was fairly stated for the

interim period.

Appendix 3: Notes regarding the accounts receivable and property, plant and equipment

work performed by the junior auditor.

Accounts Receivables / Unearned Revenue

When clients book charter flights, the flight is prepaid and the amounts are recorded in unearned

revenue. Once the service has been provided (the client takes the flight) the unearned revenue

related to the flight is transferred to revenue.

Large well established clients do not have to prepay and are invoiced for the amounts of the

flights. These represent the accounts receivable amounts on the balance sheet. The prior year

audit file indicates there were issues with accounts receivables in prior years - Eastjet had

accounted for unearned revenue as accounts receivable.

The junior accountant performed analytical review on the accounts receivable noting that

percentage of accounts receivable as a percentage of total assets was consistent with the prior

year. There were several credit balances in accounts receivable which the junior ignored. No

confirmations of accounts receivable were performed. The junior auditor concluded the accounts

receivable were fairly stated for the interim period.

Property Plant and Equipment

Property plant and equipment represents the largest item on the balance sheet and represents the

planes that Eastjet owns as well as leased planes. They are separated in the general ledger

accounts. The junior auditor traced each item on the subsidiary ledger to the original invoice,

added the subsidiary ledger and agreed the total to the general ledger. Then the junior auditor

signed the working paper concluding that property plant and equipment was fairly stated for the

interim period.

1 out of 7

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.