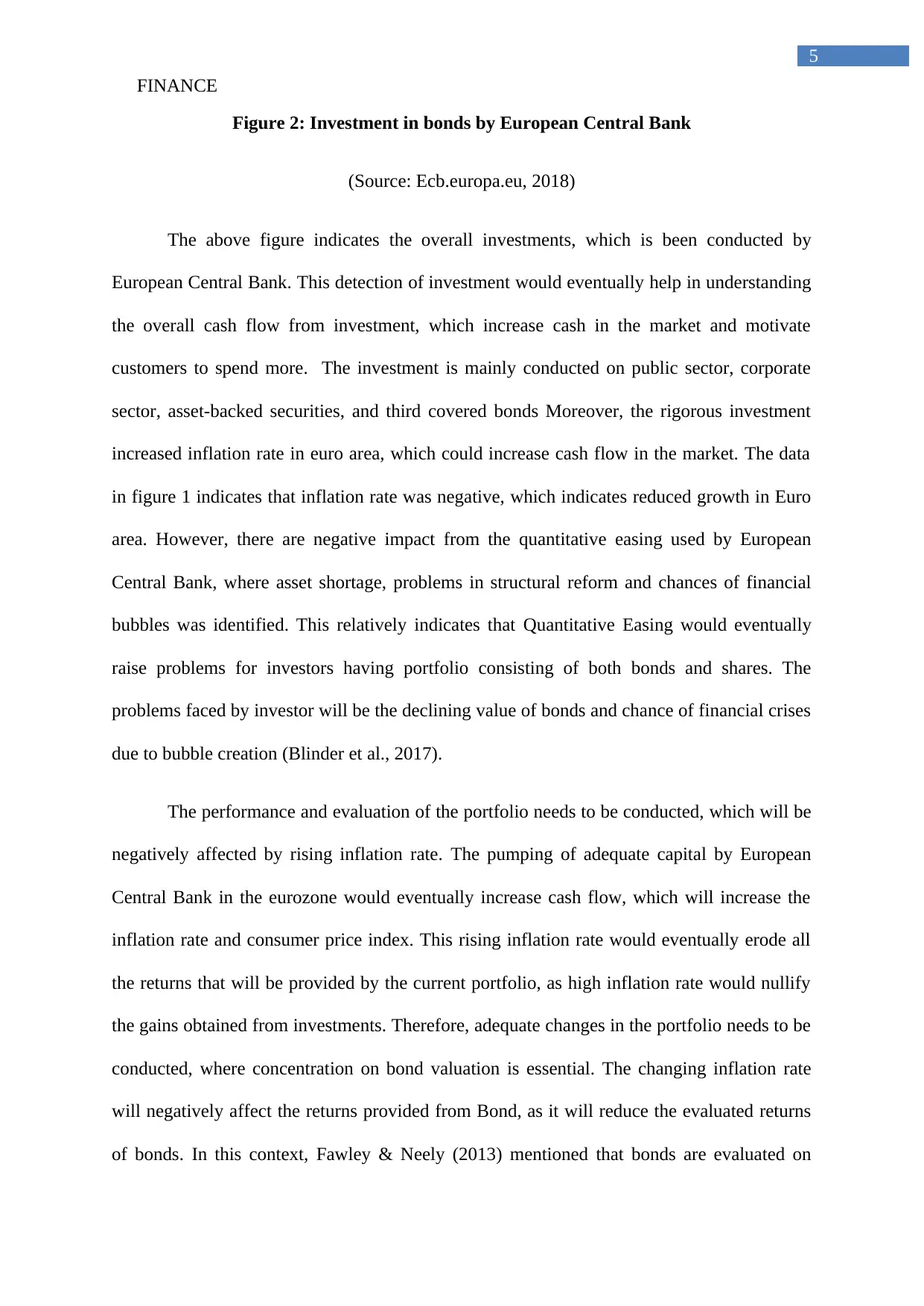

Analysis of ECB's Quantitative Easing and its Effects on Inflation

VerifiedAdded on 2021/04/17

|10

|2153

|19

Report

AI Summary

This finance report examines the European Central Bank's (ECB) Quantitative Easing (QE) program, implemented to combat low inflation in the Eurozone. The report analyzes the impact of QE on inflation rates, highlighting how the ECB's actions, such as buying investment-grade debt securities, aimed to increase the money supply and lower market interest rates. It discusses the effects of rising inflation on bond prices and values, emphasizing the concerns for portfolio managers. The analysis covers the use of QE during the 2008 economic crisis and its reapplication in 2015 to address deflation risks. The report evaluates the impact of QE on bond investments, the potential for financial bubbles, and the devaluation of the Euro against the USD. It concludes with recommendations for portfolio adjustments, suggesting a shift towards European shares to capitalize on increased cash flow and improved financial positions of companies. The report emphasizes the need for careful evaluation of investments in bonds due to the rising inflation and associated risks.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.