Comparative Economic Analysis: ECC and IPC Business Performance

VerifiedAdded on 2022/08/01

|23

|5848

|13

Report

AI Summary

This report provides a detailed economic analysis comparing two companies, ECC and IPC, focusing on the coal industry. It examines the domestic and global financial drivers impacting the companies, including changes in electricity generation, RBA interventions, and global economic growth, particularly in China and Southeast Asia. The report explores the impact of an appreciating USD on Forex and commodity markets and strategies for IPC to manage USD risk. Furthermore, it delves into asset allocation for personal investment and the role of monetary and fiscal policies in economic stabilization. The analysis covers various factors affecting coal demand and prices, such as supply interruptions, government policies, and the transition to renewable energy sources, offering insights into the future prospects of the industry and the strategic decisions of the companies involved.

Name of the student

Section

Date

Section

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents 1

Section -A 2

QUESTION - 1 2

Domestic and Global Financial Drivers 3

Changes in electricity generation 5

RBA Intervention 6

QUESTION - 2 7

Global Economic Growth 7

Chinese Economy10

Impact on ECC 11

QUESTION - 3 12

Impact of Appreciating USD 12

Impact of appreciating USD on Forex and commodity markets. 14

Strategies for IPC to manage the USD risk 14

Section - B 16

QUESTION - 1 16

Asset Allocation for Personal Investment16

QUESTION - 2 20

Stabilisation through Monetary Policies 20

Stabilisation Through Fiscal Policies 21

References 23

1

Table of Contents 1

Section -A 2

QUESTION - 1 2

Domestic and Global Financial Drivers 3

Changes in electricity generation 5

RBA Intervention 6

QUESTION - 2 7

Global Economic Growth 7

Chinese Economy10

Impact on ECC 11

QUESTION - 3 12

Impact of Appreciating USD 12

Impact of appreciating USD on Forex and commodity markets. 14

Strategies for IPC to manage the USD risk 14

Section - B 16

QUESTION - 1 16

Asset Allocation for Personal Investment16

QUESTION - 2 20

Stabilisation through Monetary Policies 20

Stabilisation Through Fiscal Policies 21

References 23

1

Section -A

QUESTION - 1

Coal stays a significant fuel in worldwide energy frameworks, representing practically 40% of

power age and over 40% of energy-related carbon dioxide emanations. According to

concentrates throughout the following five years, worldwide coal demand is estimated to stay

steady, bolstered by the flexible market, which represents half of the worldwide utilization.

Domestic and Global Financial Drivers

In our case study obviously, ECC is a constrained organization and is acquiring a significant

static benefit to remain suitable in the business. (Ali &Rahman, 2012) The development plans

are likewise very rewarding however everything accompanies an expense. It is significant for the

organization to comprehend the monetary drivers to take a savvy extension choice. Prices for

coal have expanded, from that point forward mirroring a scope of components including:

● changes in Government policies that have impacted worldwide supply and demand

elements

● restricted supply development in the seaborne market

● supply interruptions

● a few changes in demand for coal with various quality attributes.

2

QUESTION - 1

Coal stays a significant fuel in worldwide energy frameworks, representing practically 40% of

power age and over 40% of energy-related carbon dioxide emanations. According to

concentrates throughout the following five years, worldwide coal demand is estimated to stay

steady, bolstered by the flexible market, which represents half of the worldwide utilization.

Domestic and Global Financial Drivers

In our case study obviously, ECC is a constrained organization and is acquiring a significant

static benefit to remain suitable in the business. (Ali &Rahman, 2012) The development plans

are likewise very rewarding however everything accompanies an expense. It is significant for the

organization to comprehend the monetary drivers to take a savvy extension choice. Prices for

coal have expanded, from that point forward mirroring a scope of components including:

● changes in Government policies that have impacted worldwide supply and demand

elements

● restricted supply development in the seaborne market

● supply interruptions

● a few changes in demand for coal with various quality attributes.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A portion of the domestic factors that will influence the demand for coal is given underneath

with the idea of both the extension plans. (Chow, 2016)

Fixing of the worldwide supply-demand balance

One of the principal drivers of more grounded prices for coal since mid-2016 was the defence of

domestic coal creation around that time. Measures were actualized to lessen obsolete limits and

to improve gainfulness in Australian's domestic coal industry, and working days in coal mines

were decreased from 330 to 276 days out of each year (even though this strategy was switched in

late 2016). (Allaro, Kassa & Hundie, 2015) The decrease in Australian coal creation happened

close by recuperation in coal demand for use in both steel creation and power age. Accordingly,

there was an expanded demand for coal, which largely affected coal prices.

Supply interruptions

There have been various impermanent interruptions in the supply of coal in recent years,

especially for metallurgical coal. Since Australia represents over a portion of the metallurgical

coal seaborne market, and creation is amassed in the Bowen Basin area in Queensland, any

interruptions to Australian coal supply will in general largely affect the seaborne market for

metallurgical coal. In 2017, Australian metallurgical coal trades declined by around 50 per cent,

after Tropical Cyclone Debbie harmed key rail foundation adjusting the Bowen Basin area. The

decrease in Australian fares significantly affected worldwide supply and prices rose forcefully,

therefore. Prices kept on being upheld over the remainder of 2017 by continuous operational

issues and port postponements in Australia which marked down metallurgical coal trades. This

part additionally clarifies how utilizing IPC will be advantageous contrasted with ECC. (Clarke

& Waschik, 2012)

3

with the idea of both the extension plans. (Chow, 2016)

Fixing of the worldwide supply-demand balance

One of the principal drivers of more grounded prices for coal since mid-2016 was the defence of

domestic coal creation around that time. Measures were actualized to lessen obsolete limits and

to improve gainfulness in Australian's domestic coal industry, and working days in coal mines

were decreased from 330 to 276 days out of each year (even though this strategy was switched in

late 2016). (Allaro, Kassa & Hundie, 2015) The decrease in Australian coal creation happened

close by recuperation in coal demand for use in both steel creation and power age. Accordingly,

there was an expanded demand for coal, which largely affected coal prices.

Supply interruptions

There have been various impermanent interruptions in the supply of coal in recent years,

especially for metallurgical coal. Since Australia represents over a portion of the metallurgical

coal seaborne market, and creation is amassed in the Bowen Basin area in Queensland, any

interruptions to Australian coal supply will in general largely affect the seaborne market for

metallurgical coal. In 2017, Australian metallurgical coal trades declined by around 50 per cent,

after Tropical Cyclone Debbie harmed key rail foundation adjusting the Bowen Basin area. The

decrease in Australian fares significantly affected worldwide supply and prices rose forcefully,

therefore. Prices kept on being upheld over the remainder of 2017 by continuous operational

issues and port postponements in Australia which marked down metallurgical coal trades. This

part additionally clarifies how utilizing IPC will be advantageous contrasted with ECC. (Clarke

& Waschik, 2012)

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Over the long haul, there is impressive vulnerability around the standpoint for coal utilization.

Demand will rely upon numerous variables that are hard to conjecture, remembering the pace of

financial development for creating economies, changes in the expense and capacities of various

advancements (especially for sustainable power source and steel creation), and changes to

government policies. A portion of the worldwide elements with the amalgamation of domestic

components are featured underneath:

Changes in electricity generation

In the close to term, demand for coal is relied upon to stay bolstered by increments in coal-fueled

power age in India and South-East Asia just as proceeded with development in these economies.

The more drawn out run standpoint will emphatically rely upon the speed of progress to less

carbon-serious power age comparative with the pace at which total power demand develops.

Throughout the following five years or something like that, some proceeded with increment in

coal demand, especially from India and economies in South-East Asia, may incompletely

balance an increasingly broad decrease in demand as worldwide power age changes from coal to

other energy sources. Over the more drawn out term, notwithstanding, the equalization of

dangers for demand have all the earmarks of being to the drawback, as they progress from coal to

other energy sources in cutting edge economies proceeds – remembering for Europe, the United

States, South Korea and Japan.

Developments in steel production

Chinese yearly steel creation gives off an impression of being comprehensively around its

pinnacle and creation is required to continuously decay, even though there is significant

vulnerability around the viewpoint. Steel demand is relied upon to direct to a great extent since

4

Demand will rely upon numerous variables that are hard to conjecture, remembering the pace of

financial development for creating economies, changes in the expense and capacities of various

advancements (especially for sustainable power source and steel creation), and changes to

government policies. A portion of the worldwide elements with the amalgamation of domestic

components are featured underneath:

Changes in electricity generation

In the close to term, demand for coal is relied upon to stay bolstered by increments in coal-fueled

power age in India and South-East Asia just as proceeded with development in these economies.

The more drawn out run standpoint will emphatically rely upon the speed of progress to less

carbon-serious power age comparative with the pace at which total power demand develops.

Throughout the following five years or something like that, some proceeded with increment in

coal demand, especially from India and economies in South-East Asia, may incompletely

balance an increasingly broad decrease in demand as worldwide power age changes from coal to

other energy sources. Over the more drawn out term, notwithstanding, the equalization of

dangers for demand have all the earmarks of being to the drawback, as they progress from coal to

other energy sources in cutting edge economies proceeds – remembering for Europe, the United

States, South Korea and Japan.

Developments in steel production

Chinese yearly steel creation gives off an impression of being comprehensively around its

pinnacle and creation is required to continuously decay, even though there is significant

vulnerability around the viewpoint. Steel demand is relied upon to direct to a great extent since

4

populace development and the pace of urbanization are required to slow. This would lessen the

demand for private lodging and framework, for example, rail, interstates and open structures.

The continuous progress towards an additional administrations orientated economy may likewise

burden China's future steel demand.

RBA Intervention

Indonesia is a piece of the Southeast area so if the organization utilizes the area they will save

money on transport cost. Furthermore, will have the option to deliver more coal. Subsequently

universally and locally the demand for coal isn't getting influenced however the prices are

shooting up because of the less supply of coal. Regardless of whether RBA builds the rate,

throughout the following 20 years, the expansion in worldwide energy demand is relied upon to

be to a great extent met by sustainable power sources, and by 2040 renewables are required to

represent a bigger portion of power age than coal. The expanding take-up of renewables is relied

upon to be upheld by changes in advances that make inexhaustible power age progressively

feasible, for example, battery stockpiling and redesigned power matrix systems. Policies in

numerous locales are additionally liable to be aimed at decreasing the carbon force of power age,

incorporating through an expansion in the portion of renewables age. The Australian

Government has an objective of expanding the portion of scrap steel utilized in steel creation to

30 percent by 2025 (RBA 2017). Regardless, there is impressive vulnerability around how quick

and how much coal creation may be required to do the trick the demand. Warm coal prices

dramatically increased from the beginning of 2016 to their top in late 2016, while coking coal

prices quadrupled. The fares of coal will help the GDP development of Australia. Consequently,

the standards won't hamper the fares. On the off chance that the organization becomes IPC it

5

demand for private lodging and framework, for example, rail, interstates and open structures.

The continuous progress towards an additional administrations orientated economy may likewise

burden China's future steel demand.

RBA Intervention

Indonesia is a piece of the Southeast area so if the organization utilizes the area they will save

money on transport cost. Furthermore, will have the option to deliver more coal. Subsequently

universally and locally the demand for coal isn't getting influenced however the prices are

shooting up because of the less supply of coal. Regardless of whether RBA builds the rate,

throughout the following 20 years, the expansion in worldwide energy demand is relied upon to

be to a great extent met by sustainable power sources, and by 2040 renewables are required to

represent a bigger portion of power age than coal. The expanding take-up of renewables is relied

upon to be upheld by changes in advances that make inexhaustible power age progressively

feasible, for example, battery stockpiling and redesigned power matrix systems. Policies in

numerous locales are additionally liable to be aimed at decreasing the carbon force of power age,

incorporating through an expansion in the portion of renewables age. The Australian

Government has an objective of expanding the portion of scrap steel utilized in steel creation to

30 percent by 2025 (RBA 2017). Regardless, there is impressive vulnerability around how quick

and how much coal creation may be required to do the trick the demand. Warm coal prices

dramatically increased from the beginning of 2016 to their top in late 2016, while coking coal

prices quadrupled. The fares of coal will help the GDP development of Australia. Consequently,

the standards won't hamper the fares. On the off chance that the organization becomes IPC it

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

should follow the economy of Indonesia, and the government is very loose there. If they obtain

coal steam gas, at that point, the RBA policies will hurt the development of ECC.

QUESTION - 2

Global Economic Growth

Past the following, not many years, the viewpoint at coal costs and demand is progressively

questionable, especially for warm coal. The worldwide seaborne market for warm coal has

grown all together in recent years, and Australian warm coal exports are rivalling copious supply

from various other enormous ease makers. Huge numbers of Australia's key warm coal trade

goals, including China, Japan and South Korea, are progressing ceaselessly from the coal-fueled

power age. A continuation of this pattern would probably burden coal send out volumes and

prices. Then again, demand is relied upon to grow in different economies in the Asian locale, in

any event for a period. Specifically, India and South-East Asia are probably going to turn out to

be progressively significant goals for Australian coal exports throughout the following not many

decades as demand for energy grows and new coal-fueled activities are included in these

economies. It is hard to gauge whether proceeded with growth in exports to these business

sectors may for a period outpace the worldwide change to less carbon-concentrated power age.

(British Petroleum, 2012)

While numerous variables are viewed as joined in these cost fluctuations, more capable ones

than others are verified in this report. They incorporate (1) trade paces of the Australian dollar,

(2) vacillations in coal stocks (level of supply and demand snugness), (3) coal profitability

(creation cost), (4) the U.S. coal export patterns, and (5) the cost of oil as a matching fuel. The

6

coal steam gas, at that point, the RBA policies will hurt the development of ECC.

QUESTION - 2

Global Economic Growth

Past the following, not many years, the viewpoint at coal costs and demand is progressively

questionable, especially for warm coal. The worldwide seaborne market for warm coal has

grown all together in recent years, and Australian warm coal exports are rivalling copious supply

from various other enormous ease makers. Huge numbers of Australia's key warm coal trade

goals, including China, Japan and South Korea, are progressing ceaselessly from the coal-fueled

power age. A continuation of this pattern would probably burden coal send out volumes and

prices. Then again, demand is relied upon to grow in different economies in the Asian locale, in

any event for a period. Specifically, India and South-East Asia are probably going to turn out to

be progressively significant goals for Australian coal exports throughout the following not many

decades as demand for energy grows and new coal-fueled activities are included in these

economies. It is hard to gauge whether proceeded with growth in exports to these business

sectors may for a period outpace the worldwide change to less carbon-concentrated power age.

(British Petroleum, 2012)

While numerous variables are viewed as joined in these cost fluctuations, more capable ones

than others are verified in this report. They incorporate (1) trade paces of the Australian dollar,

(2) vacillations in coal stocks (level of supply and demand snugness), (3) coal profitability

(creation cost), (4) the U.S. coal export patterns, and (5) the cost of oil as a matching fuel. The

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Pound has neglected to make a critical recuperation since falling by 20 per cent after the Brexit

choice outcome in June 2018. The previous summer's snap general political race didn't improve

the situation as the estimation of Sterling dropped by two percent against the US dollar after the

outcome was affirmed. In the interim in the US, there are additionally various touchy issues

which could significantly affect the Dollar going ahead this year. President Trump's tax breaks

bundle can fuel expansion while the present acceleration of the war of words with North Korea's

authority could likewise compromise money steadiness. Progress in the examination over the

Trump battle and its connections to Russia is, nonetheless, liable to introduce the greatest hazard

for the time being. On the off chance that proof develops that straightforwardly involves the

President in this adventure, it would almost certainly negatively affect the estimation of the

Dollar. (Ivanova, Rolfe, Lockie & Timmer, 2017)

India intends to turn into an economy of USD 5 trillion by 2024, to some degree by putting

vigorously in the framework. This will support energy demand for industry and, particularly, for

power creation. Even though India has prevailed with regards to bringing some type of power

access to practically the entirety of its residents, the nation's per capita power utilization is still

low, giving it a critical extension to grow. Force age from renewables is estimated to extend

emphatically, with wind limit multiplying and sun-powered photovoltaics (PV) expanding

fourfold somewhere in the range of 2018 and 2024.

Coal demand in Southeast Asia is estimated to grow by over 5% every year through 2024, drove

by Indonesia and VietNam. The district's solid monetary growth will drive power and

mechanical utilization, which will both be fuelled to some degree by coal. South Asian nations

are additionally needing greater power supply for the growing populaces, and they are frequently

going to coal to give it. Pakistan has as of late dispatched more than 4 GW of new coal power

7

choice outcome in June 2018. The previous summer's snap general political race didn't improve

the situation as the estimation of Sterling dropped by two percent against the US dollar after the

outcome was affirmed. In the interim in the US, there are additionally various touchy issues

which could significantly affect the Dollar going ahead this year. President Trump's tax breaks

bundle can fuel expansion while the present acceleration of the war of words with North Korea's

authority could likewise compromise money steadiness. Progress in the examination over the

Trump battle and its connections to Russia is, nonetheless, liable to introduce the greatest hazard

for the time being. On the off chance that proof develops that straightforwardly involves the

President in this adventure, it would almost certainly negatively affect the estimation of the

Dollar. (Ivanova, Rolfe, Lockie & Timmer, 2017)

India intends to turn into an economy of USD 5 trillion by 2024, to some degree by putting

vigorously in the framework. This will support energy demand for industry and, particularly, for

power creation. Even though India has prevailed with regards to bringing some type of power

access to practically the entirety of its residents, the nation's per capita power utilization is still

low, giving it a critical extension to grow. Force age from renewables is estimated to extend

emphatically, with wind limit multiplying and sun-powered photovoltaics (PV) expanding

fourfold somewhere in the range of 2018 and 2024.

Coal demand in Southeast Asia is estimated to grow by over 5% every year through 2024, drove

by Indonesia and VietNam. The district's solid monetary growth will drive power and

mechanical utilization, which will both be fuelled to some degree by coal. South Asian nations

are additionally needing greater power supply for the growing populaces, and they are frequently

going to coal to give it. Pakistan has as of late dispatched more than 4 GW of new coal power

7

plants, with a comparative limit under development. Bangladesh is going to commission the

primary unit of the 10 GW it has in the pipeline.

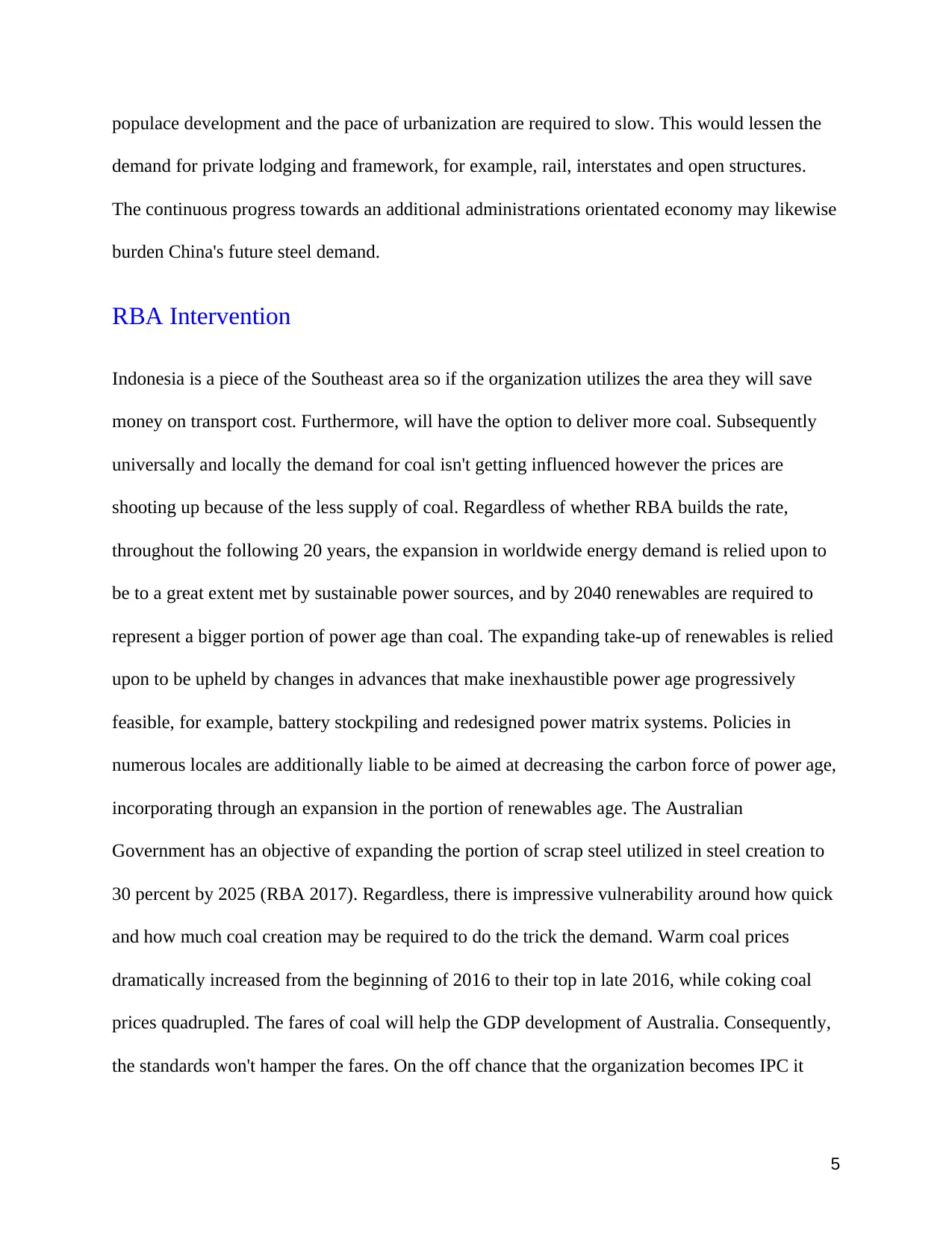

Chinese Economy

In China, the world's greatest coal maker and buyer, utilization will level around 2022. More

grounded than-anticipated power utilization and foundation advancement have pushed coal to go

through over the most recent couple of years. In our conjecture, the decrease of coal use in the

8

primary unit of the 10 GW it has in the pipeline.

Chinese Economy

In China, the world's greatest coal maker and buyer, utilization will level around 2022. More

grounded than-anticipated power utilization and foundation advancement have pushed coal to go

through over the most recent couple of years. In our conjecture, the decrease of coal use in the

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

private and little mechanical parts proceeds on account of air contamination concerns. Coal use

in overwhelming industry likewise drops, driven by auxiliary changes in the economy just as

macroeconomic conditions in the coming years. Our estimate sees the coal power age growing,

even at an easing back rate. A lot of the force age blend is required to tumble from 67% in 2018

to 59% in 2024. By and large, coal demand in China levels by 2022 and afterwards begins to

decrease gradually.

The five-year-plan factor. The direction delineated above stays subject to the policies and

focuses on that will be remembered for the Chinese government's fourteenth five-year plan

(which will be discharged in 2020). Future coal demand will possibly be influenced by the

government's financial growth targets just as its policies on the atomic force, wind and sun

oriented, and coal change ventures. While decreasing air contamination and CO2 discharges will

be an approach needed for China, coal is relied upon to keep on assuming a significant job in

continuing monetary growth and ensuring energy security.

For metallurgical coal exports, the balance in Chinese steel creation, just as a rising portion of

scrap underway, may burden demand throughout the following hardly any years. All the more,

for the most part, Chinese policies could largely affect Australian coal demand, given that China

represents near a fourth of Australian metallurgical coal exports. These policies may incorporate

financial improvement planned for boosting framework spending, natural measures or changes to

coal import policies. In any case, regardless of whether Chinese demand was to slow, this is

probably going to be to some degree counterbalanced by more grounded demand from different

goals. India, which is as of now Australia's biggest goal for metallurgical coal exports, ought to

stay a key wellspring of demand given anticipated growth in its steel part. Mirroring this,

9

in overwhelming industry likewise drops, driven by auxiliary changes in the economy just as

macroeconomic conditions in the coming years. Our estimate sees the coal power age growing,

even at an easing back rate. A lot of the force age blend is required to tumble from 67% in 2018

to 59% in 2024. By and large, coal demand in China levels by 2022 and afterwards begins to

decrease gradually.

The five-year-plan factor. The direction delineated above stays subject to the policies and

focuses on that will be remembered for the Chinese government's fourteenth five-year plan

(which will be discharged in 2020). Future coal demand will possibly be influenced by the

government's financial growth targets just as its policies on the atomic force, wind and sun

oriented, and coal change ventures. While decreasing air contamination and CO2 discharges will

be an approach needed for China, coal is relied upon to keep on assuming a significant job in

continuing monetary growth and ensuring energy security.

For metallurgical coal exports, the balance in Chinese steel creation, just as a rising portion of

scrap underway, may burden demand throughout the following hardly any years. All the more,

for the most part, Chinese policies could largely affect Australian coal demand, given that China

represents near a fourth of Australian metallurgical coal exports. These policies may incorporate

financial improvement planned for boosting framework spending, natural measures or changes to

coal import policies. In any case, regardless of whether Chinese demand was to slow, this is

probably going to be to some degree counterbalanced by more grounded demand from different

goals. India, which is as of now Australia's biggest goal for metallurgical coal exports, ought to

stay a key wellspring of demand given anticipated growth in its steel part. Mirroring this,

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Australian metallurgical coal exports are probably going to stay an enormous piece of the

worldwide seaborne market.

Impact on ECC

Australia had occurred under a fixed swapping scale system. All things considered, the auxiliary

macroeconomic acclimations to the ascent in exports happened through expanded domestic

swelling, which had troublesome effects all through the more extensive economy. The latest

mining blast has been anticipated, which has taken into account smoother basic modifications as

the energy about the conversion scale has helped with keeping expansion moderately low. As

indicated by the Productivity Commission, the coasting conversion scale has given the

Australian economy an "outside 'safeguard', the Reserve Bank has had the option to keep

swelling inside its objective band on normal since the blast started, and we have not seen the fast

economy-wide pay increments experienced in past blasts Hence, this stun will incidentally upset

the market yet over the long haul this area is profoundly congenial and gainful. (Lean & Smyth,

2019)

QUESTION - 3

Impact of Appreciating USD

Australian dollar volatility is a significant issue for Australian exporters, shippers, just as the

Australian government. A tremendous measure of writing has been created on the impact of

exchange rate on sending out, or on the worldwide exchange, or macroeconomic markers; yet

10

worldwide seaborne market.

Impact on ECC

Australia had occurred under a fixed swapping scale system. All things considered, the auxiliary

macroeconomic acclimations to the ascent in exports happened through expanded domestic

swelling, which had troublesome effects all through the more extensive economy. The latest

mining blast has been anticipated, which has taken into account smoother basic modifications as

the energy about the conversion scale has helped with keeping expansion moderately low. As

indicated by the Productivity Commission, the coasting conversion scale has given the

Australian economy an "outside 'safeguard', the Reserve Bank has had the option to keep

swelling inside its objective band on normal since the blast started, and we have not seen the fast

economy-wide pay increments experienced in past blasts Hence, this stun will incidentally upset

the market yet over the long haul this area is profoundly congenial and gainful. (Lean & Smyth,

2019)

QUESTION - 3

Impact of Appreciating USD

Australian dollar volatility is a significant issue for Australian exporters, shippers, just as the

Australian government. A tremendous measure of writing has been created on the impact of

exchange rate on sending out, or on the worldwide exchange, or macroeconomic markers; yet

10

shockingly little consideration has been paid to gauge the converse impact of fare on the

exchange rate of a nation. Scientists, for example, Sheen and Kim (2002), Aruman and Dungey

(2003), Edison (2002) and the Reserve Bank of Australia (RBA), have been endeavouring to

clarify the reasons for the volatility of the Australian dollar (AUD). Simpson and Evans (2003)

guarantee that Australia is a commodity-rich nation; along these lines, developments in

commodity prices are reflected in the volatility of the exchange rate most of the world's coal

exchange markets are making exchanges in the U.S. cash (US$). It implies the Australian coal

makers have their business incomes influenced extensively by the exchange rate of their nearby

money, the Australian dollar, against the U.S. dollar. By and large, the exchange rate is relied

upon to con-skirt into buying power equality over the long haul.

For IPC, a powerless Australian dollar guarantees more noteworthy incomes in neighbourhood

mongrels and, in the opposite, a solid Australian dollar less-ens their incomes. Consequently, it's

anything but difficult to envision the impressive size of effects created by the Australian dollar's

rate on not just the Australian coal industry's misfortunes and gains yet additionally coal pricing,

the last as a response to the previous. The buying power equality of Australian dollars against the

U.S. dollar relies upon the inflation rates in Australia and the U.S. If the Australian inflation rate

remains higher than in the U.S., it produces weights to debilitate the Australian dollar, while a

lower inflation rate than in the U.S. quality ensues Australian dollars. Consequently, in the long

haul, the Australian dollar's rate against the U.S. dollar can be represented by the Australian and

American inflation rates. Australia's inflation has been lower than in the U.S., which helped its

buying power equality remain high. All things considered, Australian dollars have remained

rather underestimated. (Pindyck, 2019) Since the mid-1990s, when the coal digging division was

revived for outside speculation, Indonesia saw a strong increment in coal creation, coal exports

11

exchange rate of a nation. Scientists, for example, Sheen and Kim (2002), Aruman and Dungey

(2003), Edison (2002) and the Reserve Bank of Australia (RBA), have been endeavouring to

clarify the reasons for the volatility of the Australian dollar (AUD). Simpson and Evans (2003)

guarantee that Australia is a commodity-rich nation; along these lines, developments in

commodity prices are reflected in the volatility of the exchange rate most of the world's coal

exchange markets are making exchanges in the U.S. cash (US$). It implies the Australian coal

makers have their business incomes influenced extensively by the exchange rate of their nearby

money, the Australian dollar, against the U.S. dollar. By and large, the exchange rate is relied

upon to con-skirt into buying power equality over the long haul.

For IPC, a powerless Australian dollar guarantees more noteworthy incomes in neighbourhood

mongrels and, in the opposite, a solid Australian dollar less-ens their incomes. Consequently, it's

anything but difficult to envision the impressive size of effects created by the Australian dollar's

rate on not just the Australian coal industry's misfortunes and gains yet additionally coal pricing,

the last as a response to the previous. The buying power equality of Australian dollars against the

U.S. dollar relies upon the inflation rates in Australia and the U.S. If the Australian inflation rate

remains higher than in the U.S., it produces weights to debilitate the Australian dollar, while a

lower inflation rate than in the U.S. quality ensues Australian dollars. Consequently, in the long

haul, the Australian dollar's rate against the U.S. dollar can be represented by the Australian and

American inflation rates. Australia's inflation has been lower than in the U.S., which helped its

buying power equality remain high. All things considered, Australian dollars have remained

rather underestimated. (Pindyck, 2019) Since the mid-1990s, when the coal digging division was

revived for outside speculation, Indonesia saw a strong increment in coal creation, coal exports

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.