Swinburne ECO10004 Economic Principles: Elasticity, Costs, & Strategy

VerifiedAdded on 2023/04/21

|11

|1678

|427

Homework Assignment

AI Summary

This assignment delves into key economic principles, focusing on elasticity, costs of production, market power, and business strategy. It examines the price elasticity of demand for luxury and necessary goods, as well as goods with many or few substitutes. The assignment also explores the impact of fixed and variable costs on production decisions, using the example of Airbus and Boeing to illustrate long-run average cost considerations. Furthermore, it analyzes market power in monopoly and competitive scenarios, and assesses dominant strategies and Nash equilibrium in game theory, using the example of Jim's Coffee and Stars and Coffee. Desklib offers a wide range of study tools and resources for students.

Running head: ECONOMIC PRINCIPLES

Economic Principles

Name of the Student

Name of the University

Course ID

Economic Principles

Name of the Student

Name of the University

Course ID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1ECONOMIC PRINCIPLES

Table of Contents

Task 2: Elasticity........................................................................................................................2

Question 1..............................................................................................................................2

Question 2..............................................................................................................................2

Question 3..............................................................................................................................2

Task 3: Costs of production.......................................................................................................3

Question 1..............................................................................................................................3

Question 2..............................................................................................................................3

Question 3..............................................................................................................................3

Task 4: Market power................................................................................................................4

Question 1..............................................................................................................................4

Question 2..............................................................................................................................5

Task 5: Business Strategy..........................................................................................................6

Question 1..............................................................................................................................6

Question 2..............................................................................................................................6

Question 3..............................................................................................................................6

Question 4..............................................................................................................................6

Question 5..............................................................................................................................7

References..................................................................................................................................8

Table of Contents

Task 2: Elasticity........................................................................................................................2

Question 1..............................................................................................................................2

Question 2..............................................................................................................................2

Question 3..............................................................................................................................2

Task 3: Costs of production.......................................................................................................3

Question 1..............................................................................................................................3

Question 2..............................................................................................................................3

Question 3..............................................................................................................................3

Task 4: Market power................................................................................................................4

Question 1..............................................................................................................................4

Question 2..............................................................................................................................5

Task 5: Business Strategy..........................................................................................................6

Question 1..............................................................................................................................6

Question 2..............................................................................................................................6

Question 3..............................................................................................................................6

Question 4..............................................................................................................................6

Question 5..............................................................................................................................7

References..................................................................................................................................8

2ECONOMIC PRINCIPLES

Task 2: Elasticity

Question 1

3D television is a luxury item. Therefore, quantity demanded changes largely for a

given change in price. This makes demand for 3D television highly price elastic that is having

absolute value of elasticity greater than 1. Prescription in contrast is a necessary items and

hence, people cannot change the demand much whenever price changes. The demand of

prescription is relatively price inelastic with absolute value less than 1.

Question 2

Coffee sold in café have a large number of substitutes. As people have alternative

choice to coffee they can change their demand to a relatively large extent given the change in

price. Electricity in contrast has only limited substitute and demand therefore can be adjusted

only to a limited extent in response to price change (Baumol and Blinder 2015). Coffee

therefore has a higher price elasticity of demand compared to electricity.

Question 3

Cross Price Elastcity= Percentage change∈quantity demanded of tyres

Percentage chnage ∈ price of tyres

¿

21000−25000

25000 ×100

35000−25000

25000 ×100

¿ −16

40

¿−0.4

The estimated cross price elasticity of demand between tyres and cars is -0.4. This

estimated value of cross price elasticity of demand implies that 10 percent increase in price of

Task 2: Elasticity

Question 1

3D television is a luxury item. Therefore, quantity demanded changes largely for a

given change in price. This makes demand for 3D television highly price elastic that is having

absolute value of elasticity greater than 1. Prescription in contrast is a necessary items and

hence, people cannot change the demand much whenever price changes. The demand of

prescription is relatively price inelastic with absolute value less than 1.

Question 2

Coffee sold in café have a large number of substitutes. As people have alternative

choice to coffee they can change their demand to a relatively large extent given the change in

price. Electricity in contrast has only limited substitute and demand therefore can be adjusted

only to a limited extent in response to price change (Baumol and Blinder 2015). Coffee

therefore has a higher price elasticity of demand compared to electricity.

Question 3

Cross Price Elastcity= Percentage change∈quantity demanded of tyres

Percentage chnage ∈ price of tyres

¿

21000−25000

25000 ×100

35000−25000

25000 ×100

¿ −16

40

¿−0.4

The estimated cross price elasticity of demand between tyres and cars is -0.4. This

estimated value of cross price elasticity of demand implies that 10 percent increase in price of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3ECONOMIC PRINCIPLES

cars reduces demand of tyres by 4 percent. The negative value of cross price elasticity

indicates tyres and cars are complementary goods (Kreps 2019).

Task 3: Costs of production

Question 1

Licence fee does not depend on level of production and hence is considered as a fixed

cost. The application of license fee therefore affects the fixed cost of production.

Question 2

As power boards are used as an input in making TVs, the price of power boars form

variable cost of production. If Samsung signs a new contract that change price of power

board, it will affect the variable cost (Cowell 2018).

Question 3

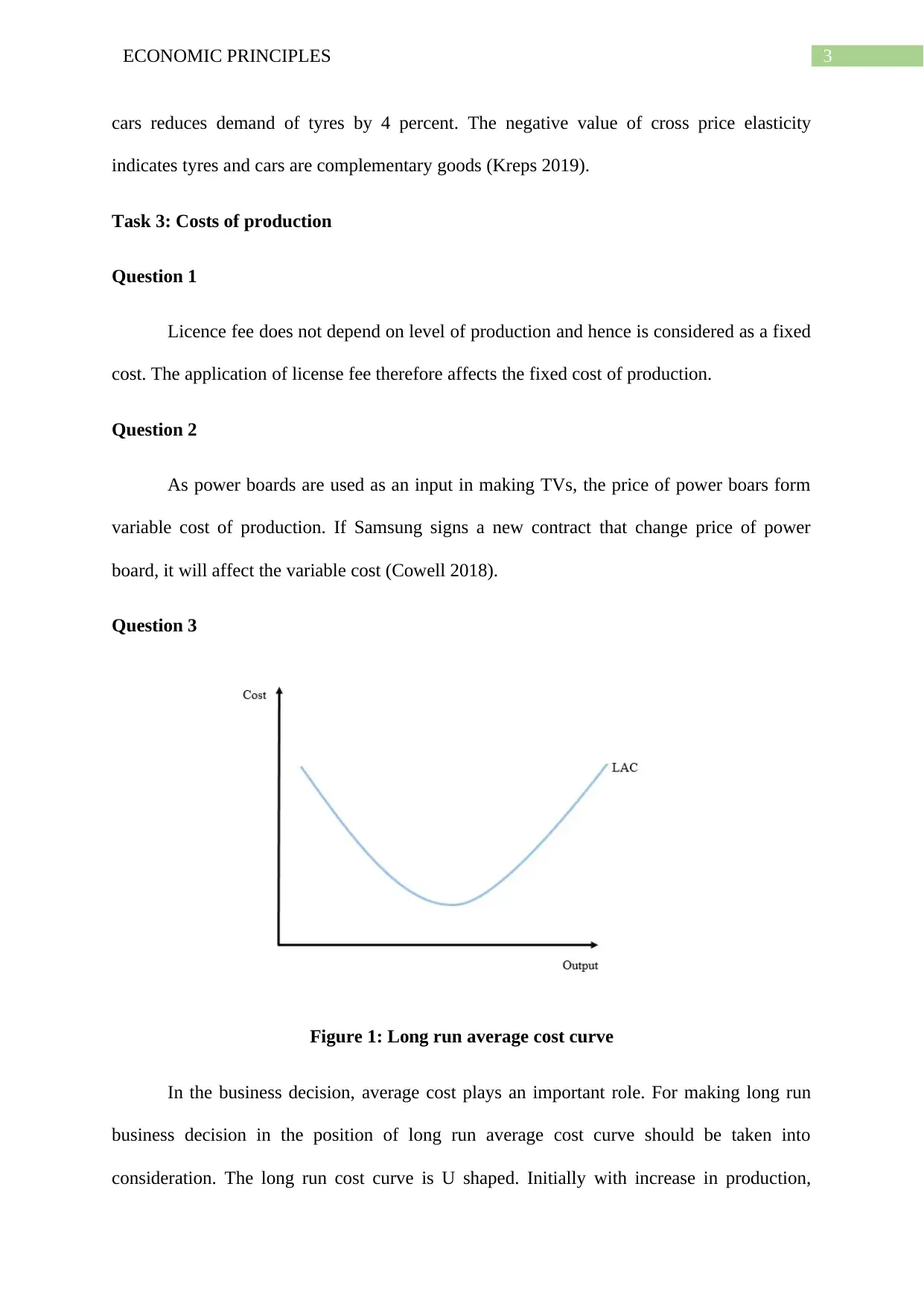

Figure 1: Long run average cost curve

In the business decision, average cost plays an important role. For making long run

business decision in the position of long run average cost curve should be taken into

consideration. The long run cost curve is U shaped. Initially with increase in production,

cars reduces demand of tyres by 4 percent. The negative value of cross price elasticity

indicates tyres and cars are complementary goods (Kreps 2019).

Task 3: Costs of production

Question 1

Licence fee does not depend on level of production and hence is considered as a fixed

cost. The application of license fee therefore affects the fixed cost of production.

Question 2

As power boards are used as an input in making TVs, the price of power boars form

variable cost of production. If Samsung signs a new contract that change price of power

board, it will affect the variable cost (Cowell 2018).

Question 3

Figure 1: Long run average cost curve

In the business decision, average cost plays an important role. For making long run

business decision in the position of long run average cost curve should be taken into

consideration. The long run cost curve is U shaped. Initially with increase in production,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4ECONOMIC PRINCIPLES

average cost decreases, then reaches to the minimum and after reaching the minimum long

run average cost increases. Airbus’s A380 dominates the airline market in terms of flying

airline while Boeing’s 787 dominates the market for testing flights. Airbus’s A380 is the

most expensive civilian airplane. It is highly fuel-efficient having sound reduction technology

and control system. The targeted customers of using A380 is therefore high-income people

who can afford flight fare. The company therefore should choose to use A380 in the long run

if it targets the high income people forming the luxury market (Nicholson and Snyder 2014).

To afford the cost of A380, other costs should be lower. Therefore, when the firm is

operating at falling part of long run average cost and having customers demanding luxury

airplane then the company should choose A380. In contrast, Boeing’s 787 Dreamliner is of

small size, has the facility of quick flight turnaround time and has advantage of fuel

economy. Use of Dreamliner therefore gives the company cost advantage (Blad and Keiding

2014). When the company operates at the rising part of long run average cost, they should

focus on reducing cost and hence, should chose cost-efficient Boeing 787 Dreamliner.

Task 4: Market power

Question 1

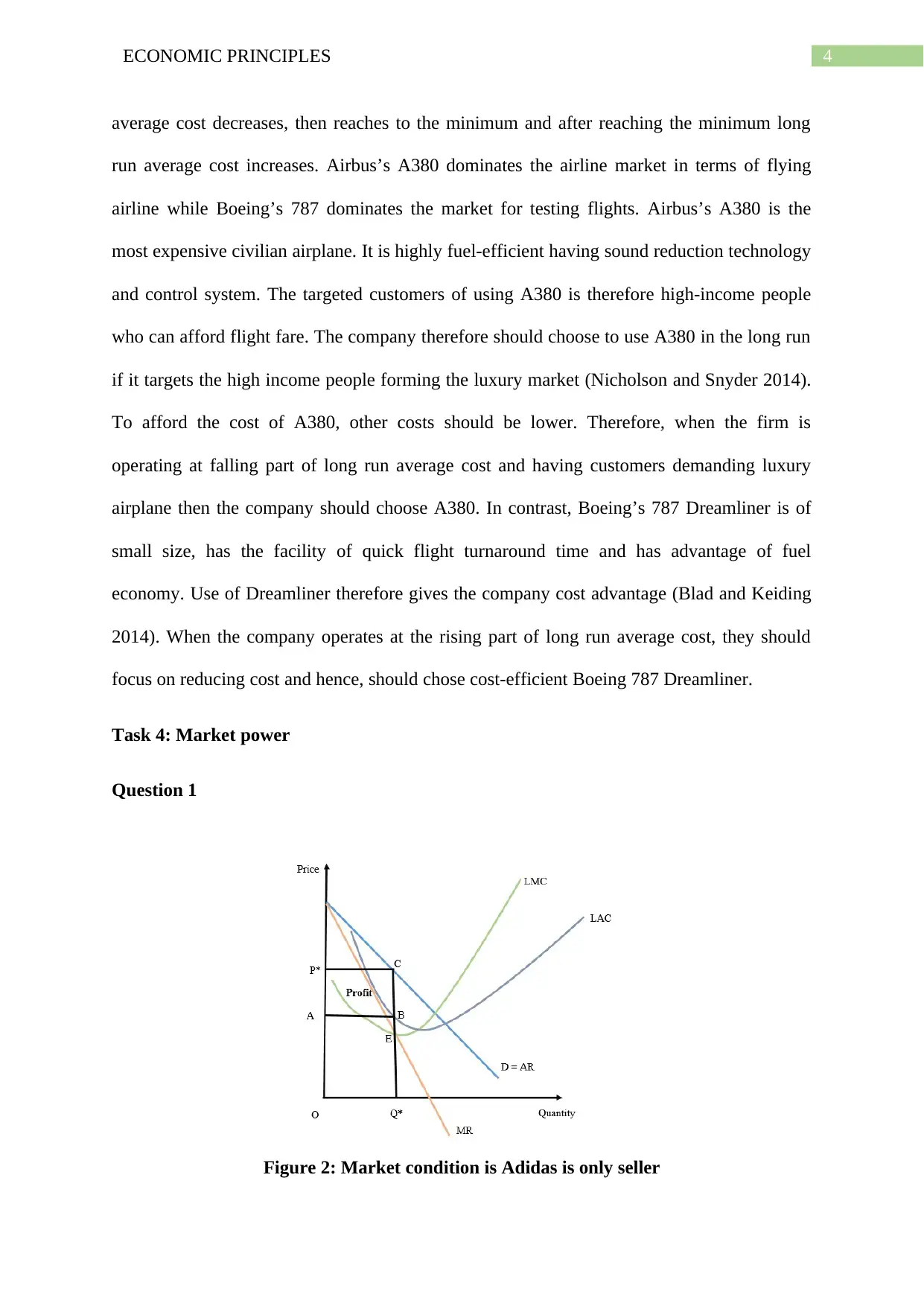

Figure 2: Market condition is Adidas is only seller

average cost decreases, then reaches to the minimum and after reaching the minimum long

run average cost increases. Airbus’s A380 dominates the airline market in terms of flying

airline while Boeing’s 787 dominates the market for testing flights. Airbus’s A380 is the

most expensive civilian airplane. It is highly fuel-efficient having sound reduction technology

and control system. The targeted customers of using A380 is therefore high-income people

who can afford flight fare. The company therefore should choose to use A380 in the long run

if it targets the high income people forming the luxury market (Nicholson and Snyder 2014).

To afford the cost of A380, other costs should be lower. Therefore, when the firm is

operating at falling part of long run average cost and having customers demanding luxury

airplane then the company should choose A380. In contrast, Boeing’s 787 Dreamliner is of

small size, has the facility of quick flight turnaround time and has advantage of fuel

economy. Use of Dreamliner therefore gives the company cost advantage (Blad and Keiding

2014). When the company operates at the rising part of long run average cost, they should

focus on reducing cost and hence, should chose cost-efficient Boeing 787 Dreamliner.

Task 4: Market power

Question 1

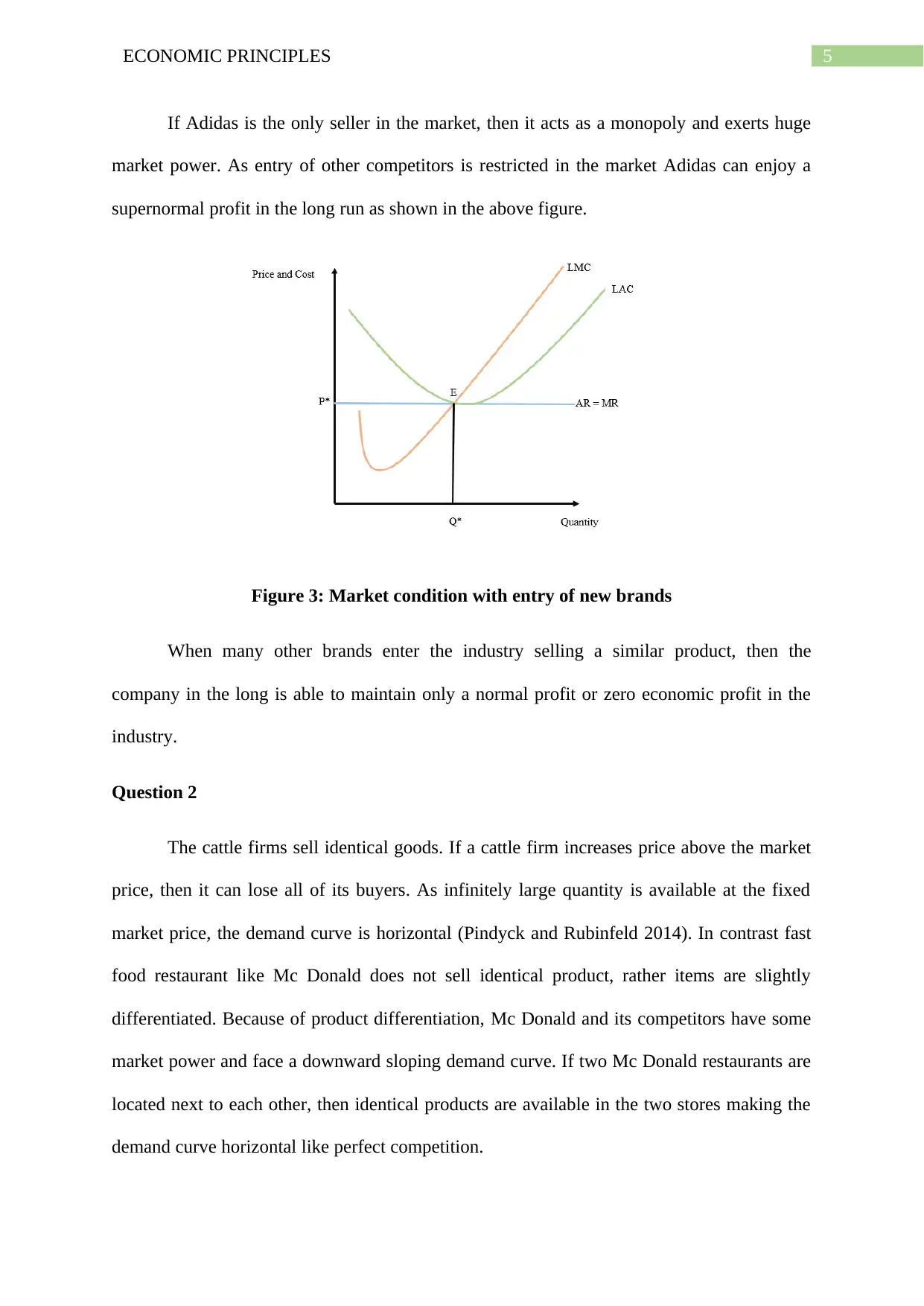

Figure 2: Market condition is Adidas is only seller

5ECONOMIC PRINCIPLES

If Adidas is the only seller in the market, then it acts as a monopoly and exerts huge

market power. As entry of other competitors is restricted in the market Adidas can enjoy a

supernormal profit in the long run as shown in the above figure.

Figure 3: Market condition with entry of new brands

When many other brands enter the industry selling a similar product, then the

company in the long is able to maintain only a normal profit or zero economic profit in the

industry.

Question 2

The cattle firms sell identical goods. If a cattle firm increases price above the market

price, then it can lose all of its buyers. As infinitely large quantity is available at the fixed

market price, the demand curve is horizontal (Pindyck and Rubinfeld 2014). In contrast fast

food restaurant like Mc Donald does not sell identical product, rather items are slightly

differentiated. Because of product differentiation, Mc Donald and its competitors have some

market power and face a downward sloping demand curve. If two Mc Donald restaurants are

located next to each other, then identical products are available in the two stores making the

demand curve horizontal like perfect competition.

If Adidas is the only seller in the market, then it acts as a monopoly and exerts huge

market power. As entry of other competitors is restricted in the market Adidas can enjoy a

supernormal profit in the long run as shown in the above figure.

Figure 3: Market condition with entry of new brands

When many other brands enter the industry selling a similar product, then the

company in the long is able to maintain only a normal profit or zero economic profit in the

industry.

Question 2

The cattle firms sell identical goods. If a cattle firm increases price above the market

price, then it can lose all of its buyers. As infinitely large quantity is available at the fixed

market price, the demand curve is horizontal (Pindyck and Rubinfeld 2014). In contrast fast

food restaurant like Mc Donald does not sell identical product, rather items are slightly

differentiated. Because of product differentiation, Mc Donald and its competitors have some

market power and face a downward sloping demand curve. If two Mc Donald restaurants are

located next to each other, then identical products are available in the two stores making the

demand curve horizontal like perfect competition.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6ECONOMIC PRINCIPLES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ECONOMIC PRINCIPLES

Task 5: Business Strategy

Question 1

Dominant strategy

In game theory, dominant strategy refers to strategy of a player that always results in a

higher pay off to the player irrespective of the action taken by opponent (Mahanty 2014). A

strategy is said to be dominant when it yields a higher pay off compared to other strategy.

Question 2

Given the above information, Jim has two strategies – enter and do not enter. Stars

and Coffee also has two strategies – either to choose high price or to choose low price. If

Stars and Coffee chooses high price, then optimal strategy for Jim is to choose enter at it

yields a higher pay off (2 > 0). If Stars and Coffee chose low price, then again optimal

strategy for Jim is to enter (1>0). For Jim, therefore “enter” is the dominant strategy.

Question 3

For Stars and Coffee, the dominant strategy is to charge a high price. High price is the

dominant strategy for Stars and Coffee because irrespective of Jim’s strategy (enter or do not

enter), it always yields a higher profit compared to the strategy of low price (McMillan

2013).

Question 4

Nash equilibrium

Nash equilibrium is a concept of game theory stating that optimal outcome of a game

occurs where there is no incentive to either of the player to deviate from the chosen strategy

given the choice of strategy of the opponent (Tadelis 2013).

Task 5: Business Strategy

Question 1

Dominant strategy

In game theory, dominant strategy refers to strategy of a player that always results in a

higher pay off to the player irrespective of the action taken by opponent (Mahanty 2014). A

strategy is said to be dominant when it yields a higher pay off compared to other strategy.

Question 2

Given the above information, Jim has two strategies – enter and do not enter. Stars

and Coffee also has two strategies – either to choose high price or to choose low price. If

Stars and Coffee chooses high price, then optimal strategy for Jim is to choose enter at it

yields a higher pay off (2 > 0). If Stars and Coffee chose low price, then again optimal

strategy for Jim is to enter (1>0). For Jim, therefore “enter” is the dominant strategy.

Question 3

For Stars and Coffee, the dominant strategy is to charge a high price. High price is the

dominant strategy for Stars and Coffee because irrespective of Jim’s strategy (enter or do not

enter), it always yields a higher profit compared to the strategy of low price (McMillan

2013).

Question 4

Nash equilibrium

Nash equilibrium is a concept of game theory stating that optimal outcome of a game

occurs where there is no incentive to either of the player to deviate from the chosen strategy

given the choice of strategy of the opponent (Tadelis 2013).

8ECONOMIC PRINCIPLES

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9ECONOMIC PRINCIPLES

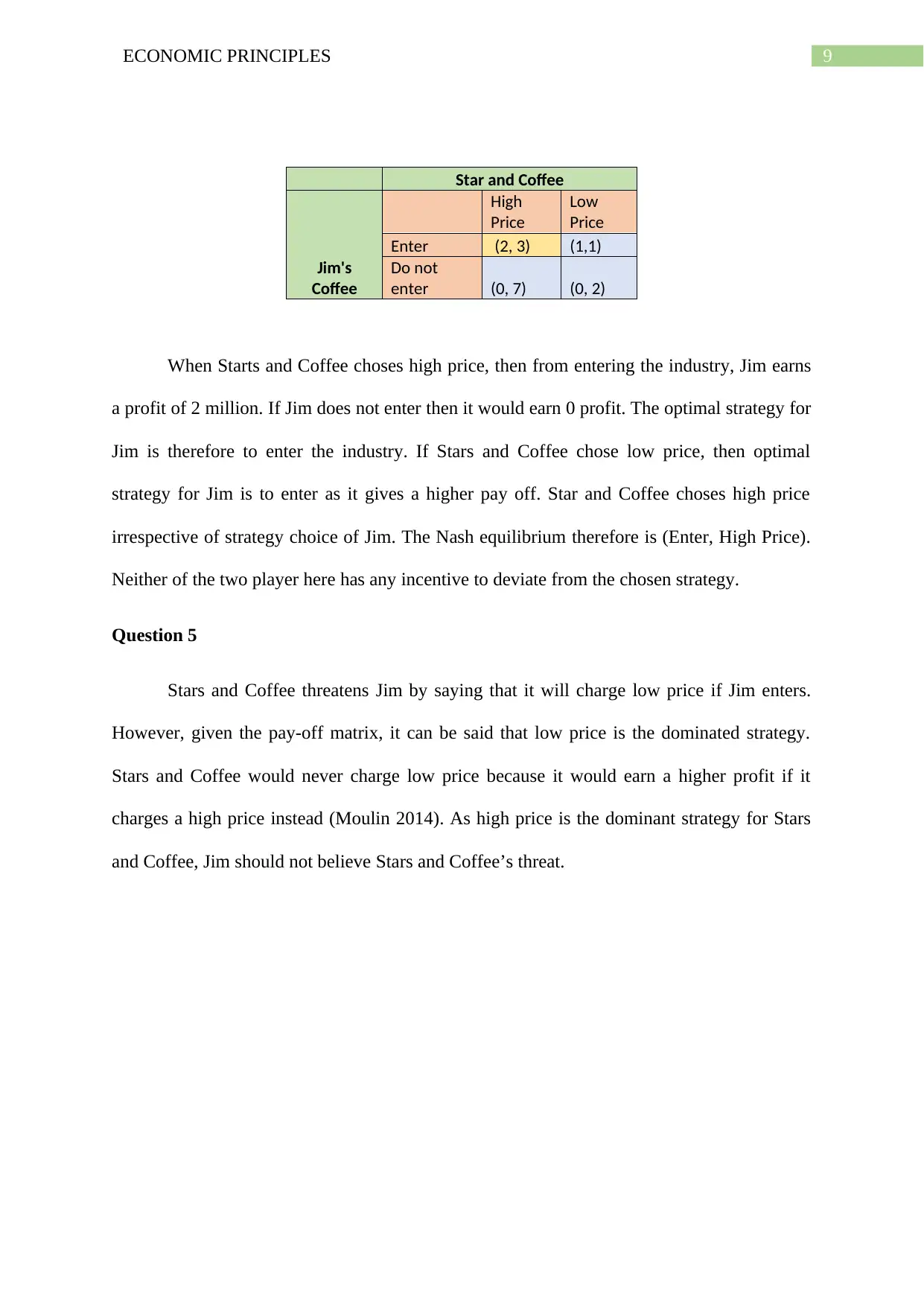

Star and Coffee

Jim's

Coffee

High

Price

Low

Price

Enter (2, 3) (1,1)

Do not

enter (0, 7) (0, 2)

When Starts and Coffee choses high price, then from entering the industry, Jim earns

a profit of 2 million. If Jim does not enter then it would earn 0 profit. The optimal strategy for

Jim is therefore to enter the industry. If Stars and Coffee chose low price, then optimal

strategy for Jim is to enter as it gives a higher pay off. Star and Coffee choses high price

irrespective of strategy choice of Jim. The Nash equilibrium therefore is (Enter, High Price).

Neither of the two player here has any incentive to deviate from the chosen strategy.

Question 5

Stars and Coffee threatens Jim by saying that it will charge low price if Jim enters.

However, given the pay-off matrix, it can be said that low price is the dominated strategy.

Stars and Coffee would never charge low price because it would earn a higher profit if it

charges a high price instead (Moulin 2014). As high price is the dominant strategy for Stars

and Coffee, Jim should not believe Stars and Coffee’s threat.

Star and Coffee

Jim's

Coffee

High

Price

Low

Price

Enter (2, 3) (1,1)

Do not

enter (0, 7) (0, 2)

When Starts and Coffee choses high price, then from entering the industry, Jim earns

a profit of 2 million. If Jim does not enter then it would earn 0 profit. The optimal strategy for

Jim is therefore to enter the industry. If Stars and Coffee chose low price, then optimal

strategy for Jim is to enter as it gives a higher pay off. Star and Coffee choses high price

irrespective of strategy choice of Jim. The Nash equilibrium therefore is (Enter, High Price).

Neither of the two player here has any incentive to deviate from the chosen strategy.

Question 5

Stars and Coffee threatens Jim by saying that it will charge low price if Jim enters.

However, given the pay-off matrix, it can be said that low price is the dominated strategy.

Stars and Coffee would never charge low price because it would earn a higher profit if it

charges a high price instead (Moulin 2014). As high price is the dominant strategy for Stars

and Coffee, Jim should not believe Stars and Coffee’s threat.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10ECONOMIC PRINCIPLES

References

Baumol, W.J. and Blinder, A.S., 2015. Microeconomics: Principles and policy. Nelson

Education.

Blad, M.C. and Keiding, H., 2014. Microeconomics: Institutions, equilibrium and

optimality (Vol. 30). Elsevier.

Cowell, F., 2018. Microeconomics: principles and analysis. Oxford University Press.

Kreps, D.M., 2019. Microeconomics for managers. Princeton University Press.

Mahanty, A.K., 2014. Intermediate microeconomics with applications. Academic Press.

McMillan, J., 2013. Game theory in international economics. Taylor & francis.

Moulin, H., 2014. Cooperative microeconomics: a game-theoretic introduction (Vol. 313).

Princeton University Press.

Nicholson, W. and Snyder, C., 2014. Intermediate microeconomics and its application.

Nelson Education.

Pindyck, R. and Rubinfeld, D., 2014. Microeconomics GE. Pearson Australia Pty Limited.

Tadelis, S., 2013. Game theory: an introduction. Princeton University Press.

References

Baumol, W.J. and Blinder, A.S., 2015. Microeconomics: Principles and policy. Nelson

Education.

Blad, M.C. and Keiding, H., 2014. Microeconomics: Institutions, equilibrium and

optimality (Vol. 30). Elsevier.

Cowell, F., 2018. Microeconomics: principles and analysis. Oxford University Press.

Kreps, D.M., 2019. Microeconomics for managers. Princeton University Press.

Mahanty, A.K., 2014. Intermediate microeconomics with applications. Academic Press.

McMillan, J., 2013. Game theory in international economics. Taylor & francis.

Moulin, H., 2014. Cooperative microeconomics: a game-theoretic introduction (Vol. 313).

Princeton University Press.

Nicholson, W. and Snyder, C., 2014. Intermediate microeconomics and its application.

Nelson Education.

Pindyck, R. and Rubinfeld, D., 2014. Microeconomics GE. Pearson Australia Pty Limited.

Tadelis, S., 2013. Game theory: an introduction. Princeton University Press.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.