Semester 2 ECO3018 Financial Economics Assignment Solution

VerifiedAdded on 2022/11/28

|12

|3219

|437

Homework Assignment

AI Summary

This document presents a comprehensive solution to an ECO3018 Financial Economics assignment. The solution addresses various financial concepts, including portfolio management, calculation of standard deviation, expected rate of return, and the application of the Capital Asset Pricing Model (CAPM). It analyzes bond valuation, including bond value at maturity, realized coupon yield, and yield to maturity. The assignment further delves into option pricing, exploring put-call parity, future pricing, and the binomial option pricing model. The solution also covers Sharpe ratios and investment strategies, providing a detailed breakdown of each question with relevant formulas, calculations, and explanations to facilitate a thorough understanding of the subject matter.

ECO3018 – FINANCIAL

ECONOMICS

ECONOMICS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................3

QUESTION 3...................................................................................................................................4

QUESTION 4...................................................................................................................................4

QUESTION 5...................................................................................................................................4

QUESTION 6...................................................................................................................................4

QUESTION 7...................................................................................................................................4

QUESTION 8...................................................................................................................................4

QUESTION 9...................................................................................................................................4

QUESTION 10.................................................................................................................................4

QUESTION 11.................................................................................................................................5

QUESTION 12.................................................................................................................................5

QUESTION 13.................................................................................................................................5

QUESTION 14.................................................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

QUESTION 2...................................................................................................................................3

QUESTION 3...................................................................................................................................4

QUESTION 4...................................................................................................................................4

QUESTION 5...................................................................................................................................4

QUESTION 6...................................................................................................................................4

QUESTION 7...................................................................................................................................4

QUESTION 8...................................................................................................................................4

QUESTION 9...................................................................................................................................4

QUESTION 10.................................................................................................................................4

QUESTION 11.................................................................................................................................5

QUESTION 12.................................................................................................................................5

QUESTION 13.................................................................................................................................5

QUESTION 14.................................................................................................................................6

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

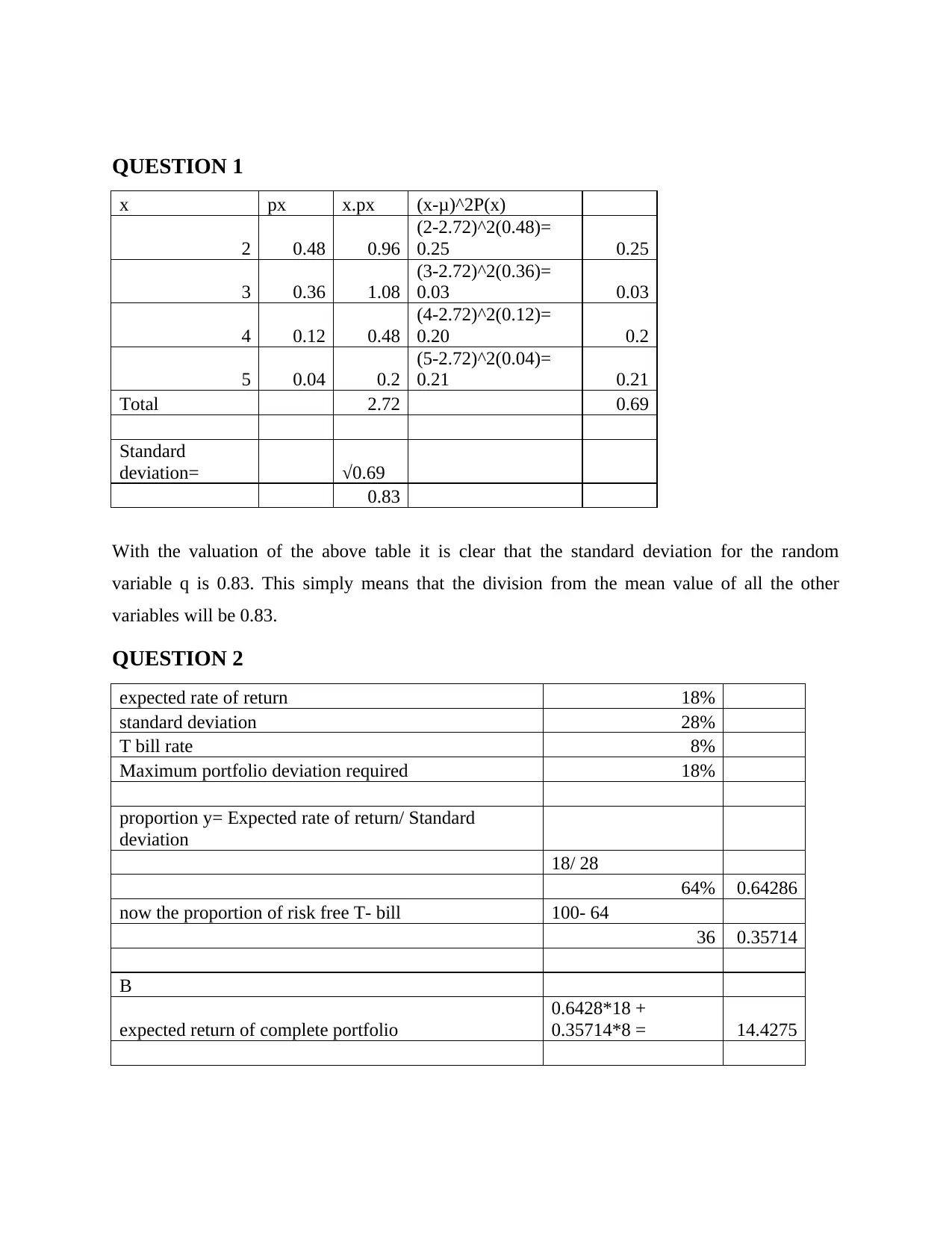

QUESTION 1

x px x.px (x-μ)^2P(x)

2 0.48 0.96

(2-2.72)^2(0.48)=

0.25 0.25

3 0.36 1.08

(3-2.72)^2(0.36)=

0.03 0.03

4 0.12 0.48

(4-2.72)^2(0.12)=

0.20 0.2

5 0.04 0.2

(5-2.72)^2(0.04)=

0.21 0.21

Total 2.72 0.69

Standard

deviation= √0.69

0.83

With the valuation of the above table it is clear that the standard deviation for the random

variable q is 0.83. This simply means that the division from the mean value of all the other

variables will be 0.83.

QUESTION 2

expected rate of return 18%

standard deviation 28%

T bill rate 8%

Maximum portfolio deviation required 18%

proportion y= Expected rate of return/ Standard

deviation

18/ 28

64% 0.64286

now the proportion of risk free T- bill 100- 64

36 0.35714

B

expected return of complete portfolio

0.6428*18 +

0.35714*8 = 14.4275

x px x.px (x-μ)^2P(x)

2 0.48 0.96

(2-2.72)^2(0.48)=

0.25 0.25

3 0.36 1.08

(3-2.72)^2(0.36)=

0.03 0.03

4 0.12 0.48

(4-2.72)^2(0.12)=

0.20 0.2

5 0.04 0.2

(5-2.72)^2(0.04)=

0.21 0.21

Total 2.72 0.69

Standard

deviation= √0.69

0.83

With the valuation of the above table it is clear that the standard deviation for the random

variable q is 0.83. This simply means that the division from the mean value of all the other

variables will be 0.83.

QUESTION 2

expected rate of return 18%

standard deviation 28%

T bill rate 8%

Maximum portfolio deviation required 18%

proportion y= Expected rate of return/ Standard

deviation

18/ 28

64% 0.64286

now the proportion of risk free T- bill 100- 64

36 0.35714

B

expected return of complete portfolio

0.6428*18 +

0.35714*8 = 14.4275

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With the above calculation it is pretty much clear that the proportion y invested in the

risky portfolio is 64%. In addition to this the expected rate of return over the complete portfolio

is 14.4 275. This is the combination of proportion by and the proportion of risk-free T bill.

QUESTION 3

On the basis of the statement about the minimum variance portfolio of all risky securities

is valid assuming the short sales are allowed the correct answer is (a). The reason underlying

this fact is that the option that is its variance must be lower than those of all other securities and

portfolios correct because it satisfies the definition of the minimum variance portfolio. This is

pertaining to the fact that the definition of the minimum variance portfolio indicates a well

diversified portfolio which involves individually risky assets that has to went read it together

which result in lowest possible risk of the rate of expected return.

QUESTION 4

CAPM:

= 8% + 1.25 (15% - 8%)

= 16.75%

On the basis of the above projection the return is expected as 16.75%. This certainly

demonstrates that XYZ alpha is -.25% (16.75% - 17%). The CAPM model has demonstrated the

value of the stock and that is 16.75%. The market value is denoted as 17% that is more than this.

This is clearly indicating the difference between both the prices. It can ascertain that the prices

are fluctuating in the market that can demonstrate the best projection of the stock value in the

market. This model is well sufficient to deal with the all different requirements associated with

the business entity.

QUESTION 5

In case the market become more fruitful the investors are always look for the long term

options. This can project in case the market become more fruitful the investment are made in

more long term funds that can generate the healthy return against the investment (Raza, 2020).

This can certainly allow the investor as the market is effective that allow the investor to put its

money in stable and long term funds or stocks. The statement is fair enough in respect to the

portfolio investment.

risky portfolio is 64%. In addition to this the expected rate of return over the complete portfolio

is 14.4 275. This is the combination of proportion by and the proportion of risk-free T bill.

QUESTION 3

On the basis of the statement about the minimum variance portfolio of all risky securities

is valid assuming the short sales are allowed the correct answer is (a). The reason underlying

this fact is that the option that is its variance must be lower than those of all other securities and

portfolios correct because it satisfies the definition of the minimum variance portfolio. This is

pertaining to the fact that the definition of the minimum variance portfolio indicates a well

diversified portfolio which involves individually risky assets that has to went read it together

which result in lowest possible risk of the rate of expected return.

QUESTION 4

CAPM:

= 8% + 1.25 (15% - 8%)

= 16.75%

On the basis of the above projection the return is expected as 16.75%. This certainly

demonstrates that XYZ alpha is -.25% (16.75% - 17%). The CAPM model has demonstrated the

value of the stock and that is 16.75%. The market value is denoted as 17% that is more than this.

This is clearly indicating the difference between both the prices. It can ascertain that the prices

are fluctuating in the market that can demonstrate the best projection of the stock value in the

market. This model is well sufficient to deal with the all different requirements associated with

the business entity.

QUESTION 5

In case the market become more fruitful the investors are always look for the long term

options. This can project in case the market become more fruitful the investment are made in

more long term funds that can generate the healthy return against the investment (Raza, 2020).

This can certainly allow the investor as the market is effective that allow the investor to put its

money in stable and long term funds or stocks. The statement is fair enough in respect to the

portfolio investment.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 6

Bond value of maturity

= n√ Face value / current price – 1

= 3√ 1000 / 953.1 – 1

= .02

This indicates that the bond value of maturity will equate to the .02. This is the value of

the bid at the time of maturity. This is essential to identify the value of bond at the time of the

maturity. This can project that the bond will lose all its values once the maturity period has

aroused. This has been ascertain that the bond will certainly loose all its value as the market

demand of the respective bind will be less that could further allow the bond to lose all its value at

the time of maturity. The bonds are the commodity that would certainly entitles the entity to sale

at a price that show up the value of the respective bond in market.

Bond realised coupon yield

= 1000 * 112%

= 1120

The bond realised coupon yield demonstrate the potential value of the bond at the time of

the maturity. This is clearly demonstrating about the price of the bond at the time of the maturity.

This clearly indicates or demonstrates about the price of the bind that can achieve at the time of

the maturity. The rate clearly demonstrates the growth of the bend that is 12% in the end of the

three financial years. This can clearly demonstrate about the potential growth rate of the bond in

the market. This can indicate that the above stated price is an expected value of the bond at the

end of the three years maturity value (Caine, Dardonville and Popelier, 2018). This is an

expected level of value of the bond that is received at the end of the three years. The value is that

can be stated that the organisation should address at the end of the three financial years.

QUESTION 7

This is a true statement as the expectation of the hypothesis clearly indicates about the

market situation. In case the hypothesis demonstrates the upward flow of the curve than it clearly

means that the demand will certainly go rise. To take the advantage of the increased demand the

interest rate get an increase (Wu And et.al., 2020). This is a convenient or a feasible fact that can

favour the stakeholder to take the competitive advantage in the market. This can indicate that the

respective statement indicate about the market position or situation that state the true or right

Bond value of maturity

= n√ Face value / current price – 1

= 3√ 1000 / 953.1 – 1

= .02

This indicates that the bond value of maturity will equate to the .02. This is the value of

the bid at the time of maturity. This is essential to identify the value of bond at the time of the

maturity. This can project that the bond will lose all its values once the maturity period has

aroused. This has been ascertain that the bond will certainly loose all its value as the market

demand of the respective bind will be less that could further allow the bond to lose all its value at

the time of maturity. The bonds are the commodity that would certainly entitles the entity to sale

at a price that show up the value of the respective bond in market.

Bond realised coupon yield

= 1000 * 112%

= 1120

The bond realised coupon yield demonstrate the potential value of the bond at the time of

the maturity. This is clearly demonstrating about the price of the bond at the time of the maturity.

This clearly indicates or demonstrates about the price of the bind that can achieve at the time of

the maturity. The rate clearly demonstrates the growth of the bend that is 12% in the end of the

three financial years. This can clearly demonstrate about the potential growth rate of the bond in

the market. This can indicate that the above stated price is an expected value of the bond at the

end of the three years maturity value (Caine, Dardonville and Popelier, 2018). This is an

expected level of value of the bond that is received at the end of the three years. The value is that

can be stated that the organisation should address at the end of the three financial years.

QUESTION 7

This is a true statement as the expectation of the hypothesis clearly indicates about the

market situation. In case the hypothesis demonstrates the upward flow of the curve than it clearly

means that the demand will certainly go rise. To take the advantage of the increased demand the

interest rate get an increase (Wu And et.al., 2020). This is a convenient or a feasible fact that can

favour the stakeholder to take the competitive advantage in the market. This can indicate that the

respective statement indicate about the market position or situation that state the true or right

position or the behaviour of the market. This is a basic nature of the market as the demand

increases the prices go high as all stakeholder groups try to take the competitive advantage of the

respective market situation.

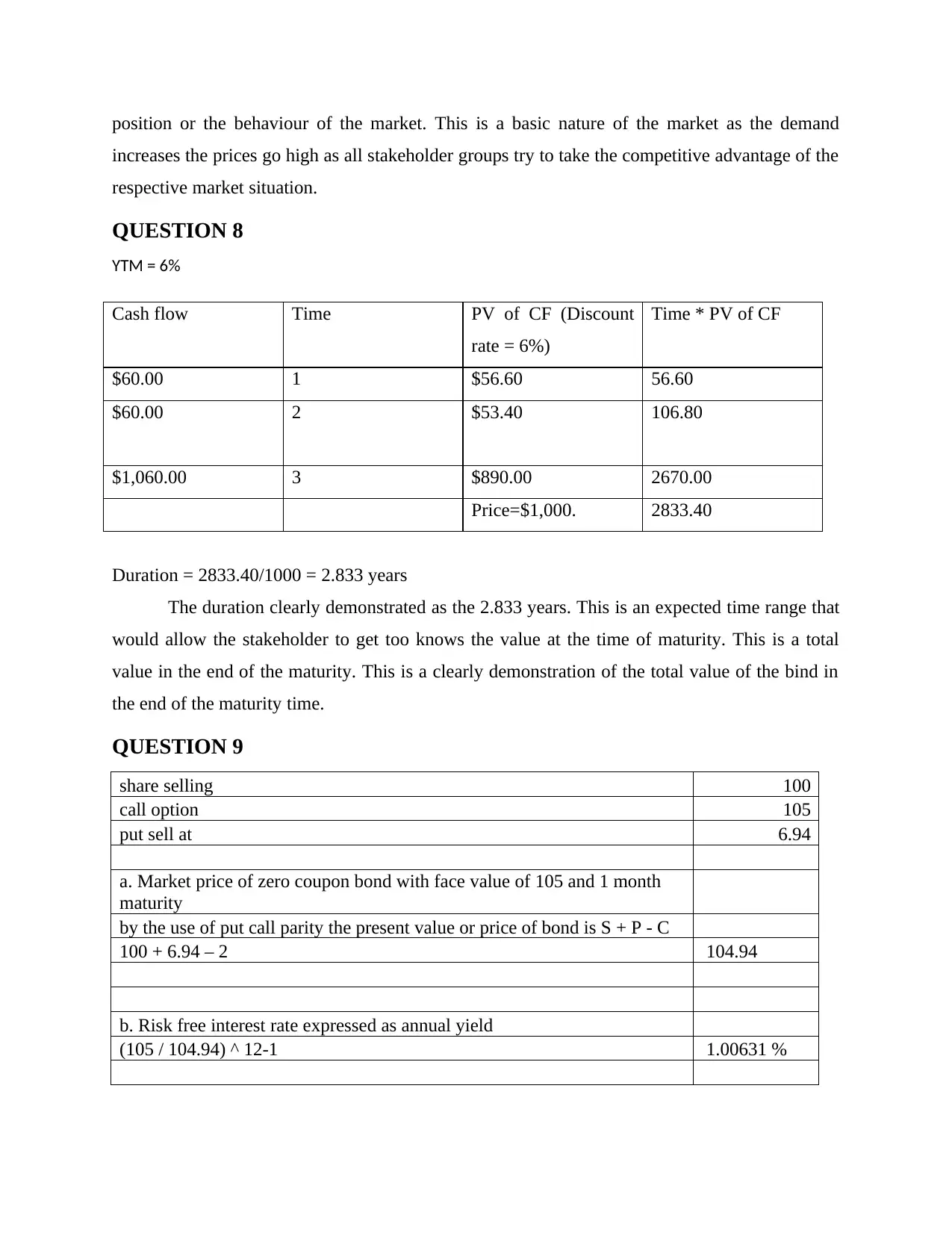

QUESTION 8

YTM = 6%

Cash flow Time PV of CF (Discount

rate = 6%)

Time * PV of CF

$60.00 1 $56.60 56.60

$60.00 2 $53.40 106.80

$1,060.00 3 $890.00 2670.00

Price=$1,000. 2833.40

Duration = 2833.40/1000 = 2.833 years

The duration clearly demonstrated as the 2.833 years. This is an expected time range that

would allow the stakeholder to get too knows the value at the time of maturity. This is a total

value in the end of the maturity. This is a clearly demonstration of the total value of the bind in

the end of the maturity time.

QUESTION 9

share selling 100

call option 105

put sell at 6.94

a. Market price of zero coupon bond with face value of 105 and 1 month

maturity

by the use of put call parity the present value or price of bond is S + P - C

100 + 6.94 – 2 104.94

b. Risk free interest rate expressed as annual yield

(105 / 104.94) ^ 12-1 1.00631 %

increases the prices go high as all stakeholder groups try to take the competitive advantage of the

respective market situation.

QUESTION 8

YTM = 6%

Cash flow Time PV of CF (Discount

rate = 6%)

Time * PV of CF

$60.00 1 $56.60 56.60

$60.00 2 $53.40 106.80

$1,060.00 3 $890.00 2670.00

Price=$1,000. 2833.40

Duration = 2833.40/1000 = 2.833 years

The duration clearly demonstrated as the 2.833 years. This is an expected time range that

would allow the stakeholder to get too knows the value at the time of maturity. This is a total

value in the end of the maturity. This is a clearly demonstration of the total value of the bind in

the end of the maturity time.

QUESTION 9

share selling 100

call option 105

put sell at 6.94

a. Market price of zero coupon bond with face value of 105 and 1 month

maturity

by the use of put call parity the present value or price of bond is S + P - C

100 + 6.94 – 2 104.94

b. Risk free interest rate expressed as annual yield

(105 / 104.94) ^ 12-1 1.00631 %

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

With the valuation of the above calculation it is clear that the market price of the zero

coupon bond having face value of 105 and 1 month maturity is 10 4.94. Further with the

evaluation of risk free rate calculation it was analysed that the risk-free interest rate is 1.00631 %

QUESTION 10

future price= Spot price * (1 + rf - D)

wherein,

rf is the risk free rate

d is the dividend

1 year maturity future price is

2000 * (1 + 0.03 - 0.020) = 2000.01

QUESTION 11

rA = 5%

rB = 10%

σA= 20%

σB = 35%

ρAB = 0.3

a) In the absence of risk free assets, the proportion will be calculated as follows:

Wa =σB2 - σAσB ρAB/ σA2 + σB2– 2ρABσAσB

Wa = (0.35)2 – 0.2 * 0.35 * 0.3 / (0.2)2 + (0.35)2 – 2(0.3) * 0.2 * 0.35

Wa = 0.1225 – 0.021 / 0.04 + 0.1225 – 0.042 = 0.1015 / 0.1205 = 0.84

So, the proportion of the industrial equity index in the portfolio = 0.84 or 84%

b) Proportion of the African sovereign bond index = 1 - Wa= 1 – 0.84 = 0.16 or 16%.

c) There is a possibility of investing in two assets only whose proportion are stated above. No

information regarding risk free rate and correlation coefficient, the proportion of the risk free

asset can’t be determined. Also, Matilda has a risk aversion coefficient of three, which means she

is a risk averse investor, so if there would be any proportion of risk free assets in the portfolio,

then it must be quite higher than the above two risky assets.

coupon bond having face value of 105 and 1 month maturity is 10 4.94. Further with the

evaluation of risk free rate calculation it was analysed that the risk-free interest rate is 1.00631 %

QUESTION 10

future price= Spot price * (1 + rf - D)

wherein,

rf is the risk free rate

d is the dividend

1 year maturity future price is

2000 * (1 + 0.03 - 0.020) = 2000.01

QUESTION 11

rA = 5%

rB = 10%

σA= 20%

σB = 35%

ρAB = 0.3

a) In the absence of risk free assets, the proportion will be calculated as follows:

Wa =σB2 - σAσB ρAB/ σA2 + σB2– 2ρABσAσB

Wa = (0.35)2 – 0.2 * 0.35 * 0.3 / (0.2)2 + (0.35)2 – 2(0.3) * 0.2 * 0.35

Wa = 0.1225 – 0.021 / 0.04 + 0.1225 – 0.042 = 0.1015 / 0.1205 = 0.84

So, the proportion of the industrial equity index in the portfolio = 0.84 or 84%

b) Proportion of the African sovereign bond index = 1 - Wa= 1 – 0.84 = 0.16 or 16%.

c) There is a possibility of investing in two assets only whose proportion are stated above. No

information regarding risk free rate and correlation coefficient, the proportion of the risk free

asset can’t be determined. Also, Matilda has a risk aversion coefficient of three, which means she

is a risk averse investor, so if there would be any proportion of risk free assets in the portfolio,

then it must be quite higher than the above two risky assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

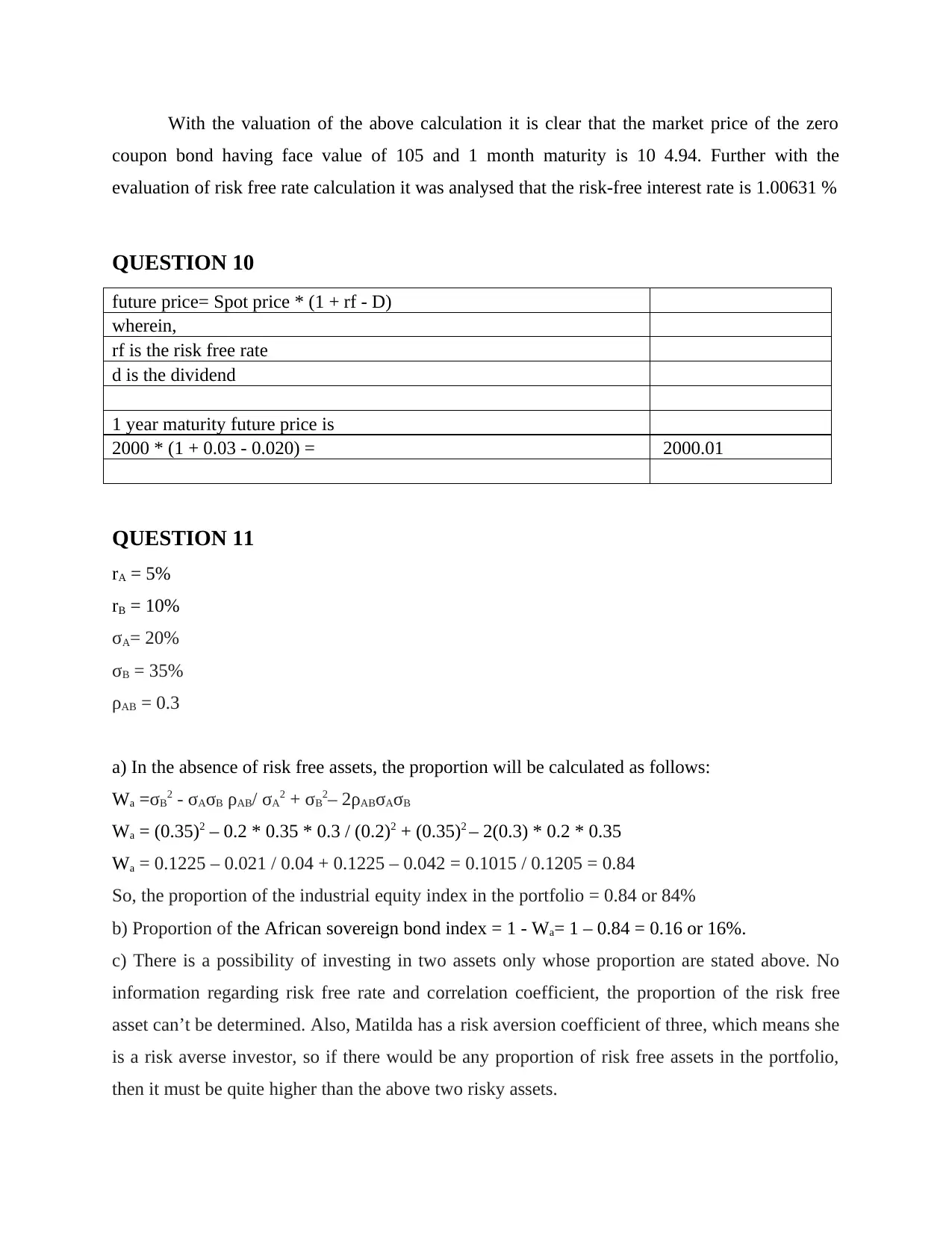

QUESTION 12

a. Bond price

N 2

PMT

9 % *100 =

9

FV

100, I/Y = 8

%

with help of PV function the bond value of 101.78

b. Yield to maturity (YTM)

the YTM is same as that on the 2 year zero coupon which is equal to 8

%

c. Market expectation of the price for which bonds will sell in next

year

(1 + s2)^2 = (1+s1) * (1 + 1f1)

(1 + 8 %) ^ 2 = (1 + 7 %) * (1 + 1f1)

1f1 = 9.01 % which is one year rate that is one year later

Hence, price of bond a year later will be-

(PMT + FV ) / (1 + 1f1)

(9 + 100)/ 1.0901 = 100

QUESTION 13

Current price 100

Increased price 110

Decreased price 90

Change in price 10

Change in new price 20

using the binomial option pricing model firstly the probability of both possibility need

to be found out

the probability of increased stock can be found with help of following formula

((1 + r) - d) / (u - d))

wherein, r is the risk free rate of return and u is the rate at which stock may increase

and d is the rate at which it will decrease

in the present case, 1 + 10 % that is 1.10 and d that is rate at which it will decrease is

1 - 10 % = 0.9

a. Bond price

N 2

PMT

9 % *100 =

9

FV

100, I/Y = 8

%

with help of PV function the bond value of 101.78

b. Yield to maturity (YTM)

the YTM is same as that on the 2 year zero coupon which is equal to 8

%

c. Market expectation of the price for which bonds will sell in next

year

(1 + s2)^2 = (1+s1) * (1 + 1f1)

(1 + 8 %) ^ 2 = (1 + 7 %) * (1 + 1f1)

1f1 = 9.01 % which is one year rate that is one year later

Hence, price of bond a year later will be-

(PMT + FV ) / (1 + 1f1)

(9 + 100)/ 1.0901 = 100

QUESTION 13

Current price 100

Increased price 110

Decreased price 90

Change in price 10

Change in new price 20

using the binomial option pricing model firstly the probability of both possibility need

to be found out

the probability of increased stock can be found with help of following formula

((1 + r) - d) / (u - d))

wherein, r is the risk free rate of return and u is the rate at which stock may increase

and d is the rate at which it will decrease

in the present case, 1 + 10 % that is 1.10 and d that is rate at which it will decrease is

1 - 10 % = 0.9

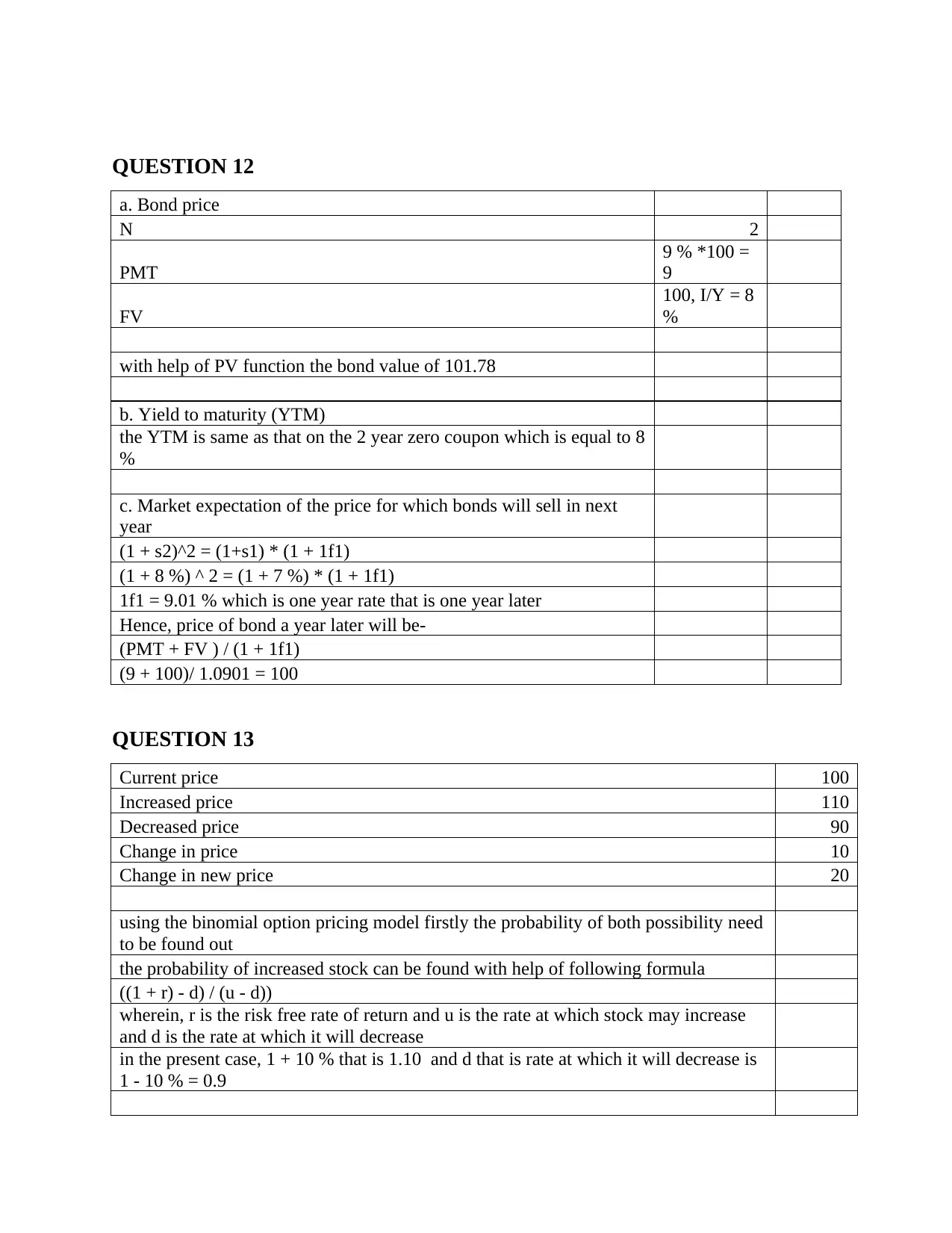

hence, the probability of moving up the stock is

((1 + 0.05) - 0.90) / (1.10 - 0.90)

0.15 / 0.2 = 0.75

this simply means that probability of moving up the stock is 0.75 that is 75 %

on the other hand, the probability of stock to decrease is

1 - 0.75 = 0.25

Thus, the probability or chances of the stock decreasing is 0.25 that is 25 %.

a. Cost of put

The cost of the put = ((probability of stock increase * intrinsic value of put if stock

increases) + (probability of stock decrease * intrinsic value of put if stock

decreases)) / (1 + risk-free rate)^n n is the duration

Cost of put = (0.75 * 0) + (0.25 * 10) / 1.05 = 2.38095

b. Cost of protective put portfolio = Cost of stock - cost of purchase

100 - 2.38095 = 97.6191

c.

QUESTION 14

A

The sharpe ratio is higher for risky portfolio of both the domestic shares in the foreign assets and

for the risky portfolio of domestic shares only. This is correct pertaining to the reason that this

ratio adjust the performance of the portfolio fast and expected against the accessories which is

taken by the investor. In addition to this a high sharpe ratio is good when compared to similar

portfolio years at the international or domestic. In addition to this the ratio is being used in order

to calculate the risk adjusted returns. Hence this will assist the investor in adding assets of

diversified portfolio with different portfolio having different types of risk.

B

It was true that a French investor with higher values of A should have purchase the domestic

shares only. the reason underlying this factors that for France the conventional wisdom was to

((1 + 0.05) - 0.90) / (1.10 - 0.90)

0.15 / 0.2 = 0.75

this simply means that probability of moving up the stock is 0.75 that is 75 %

on the other hand, the probability of stock to decrease is

1 - 0.75 = 0.25

Thus, the probability or chances of the stock decreasing is 0.25 that is 25 %.

a. Cost of put

The cost of the put = ((probability of stock increase * intrinsic value of put if stock

increases) + (probability of stock decrease * intrinsic value of put if stock

decreases)) / (1 + risk-free rate)^n n is the duration

Cost of put = (0.75 * 0) + (0.25 * 10) / 1.05 = 2.38095

b. Cost of protective put portfolio = Cost of stock - cost of purchase

100 - 2.38095 = 97.6191

c.

QUESTION 14

A

The sharpe ratio is higher for risky portfolio of both the domestic shares in the foreign assets and

for the risky portfolio of domestic shares only. This is correct pertaining to the reason that this

ratio adjust the performance of the portfolio fast and expected against the accessories which is

taken by the investor. In addition to this a high sharpe ratio is good when compared to similar

portfolio years at the international or domestic. In addition to this the ratio is being used in order

to calculate the risk adjusted returns. Hence this will assist the investor in adding assets of

diversified portfolio with different portfolio having different types of risk.

B

It was true that a French investor with higher values of A should have purchase the domestic

shares only. the reason underlying this factors that for France the conventional wisdom was to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

consider that the foreign investment were over committed to European countries only (Harvey,

2017). and because of this day over the political and diplomatic considerations and due to this

should purchase the domestic shares only and not invest within the international funds or the

investments in other countries.

C

In the present given scenario the share of a complete portfolio investors and metallurgy

sector will be almost around 20%. The remaining share of the investment will be within the risk

free friends acids and some to the optimal risky portfolio which involves domestic shares and

foreign assets. This fact is that the major share held by the French investor within the foreign

asset is between 23% to 25%. And because of this reason the investment and metallurgy sector

will be around 25%. In addition to this it also seems that with respect to the modern portfolio

theory and financial analysis statistics the French investors widely or inclined with foreign

investment. This is particularly because of the reason that the view of French investors

conservative and cautious and because of this state is not investing much within the foreign

investments. Hence the major preference of the French investor is to allocate the capital to the

risk-free French assets only and a little portion to the optimal risky portfolio which involves both

domestic and foreign assets.

Along with this it was also proved that the French investors I'm find more opportunities

available on the Paris stock exchange. The reason underlying this practice of the French

investment abroad improves the portfolio efficiency but this is more interesting that French

investors could have endured the bias against the domestic investment. Hence the structure of

French portfolio corroborates the rationality of the reference of an investor for the European

investments only and not the foreign investments. This seems that there is an existence of

domestic buyers at the time of investment and because of this the investor does not invest within

the international or other countries investment (Harvey and Liu, 2020). The reason underlying

this fact is that there is always a risk being attached and because of this the French investors does

not like to invest much more international investments. This is the only reason why the ratio of

the domestic investment compared with the foreign investment is low. The French investors like

to invest more within theme domestic investment rather than the foreign.

D

2017). and because of this day over the political and diplomatic considerations and due to this

should purchase the domestic shares only and not invest within the international funds or the

investments in other countries.

C

In the present given scenario the share of a complete portfolio investors and metallurgy

sector will be almost around 20%. The remaining share of the investment will be within the risk

free friends acids and some to the optimal risky portfolio which involves domestic shares and

foreign assets. This fact is that the major share held by the French investor within the foreign

asset is between 23% to 25%. And because of this reason the investment and metallurgy sector

will be around 25%. In addition to this it also seems that with respect to the modern portfolio

theory and financial analysis statistics the French investors widely or inclined with foreign

investment. This is particularly because of the reason that the view of French investors

conservative and cautious and because of this state is not investing much within the foreign

investments. Hence the major preference of the French investor is to allocate the capital to the

risk-free French assets only and a little portion to the optimal risky portfolio which involves both

domestic and foreign assets.

Along with this it was also proved that the French investors I'm find more opportunities

available on the Paris stock exchange. The reason underlying this practice of the French

investment abroad improves the portfolio efficiency but this is more interesting that French

investors could have endured the bias against the domestic investment. Hence the structure of

French portfolio corroborates the rationality of the reference of an investor for the European

investments only and not the foreign investments. This seems that there is an existence of

domestic buyers at the time of investment and because of this the investor does not invest within

the international or other countries investment (Harvey and Liu, 2020). The reason underlying

this fact is that there is always a risk being attached and because of this the French investors does

not like to invest much more international investments. This is the only reason why the ratio of

the domestic investment compared with the foreign investment is low. The French investors like

to invest more within theme domestic investment rather than the foreign.

D

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With the aznalysis of the article it was evaluated that the investors must have done the

investments with London stock exchange rather than Paris stock exchange. This is particularly

because of the reason that the London stock exchange account for 60% of the total nominal value

of all the stocks listed on the exchange. In addition to this the one third of all these topics

accounts for foreign stocks which are issued by the foreign Government and the municipalities.

On the other hand 40% of the stocks are devoted to the railways (Chang, McAleer and Wong,

2018).

In addition to this the remaining are financed through mines and plantation along with

banks and financial institutions of public utilities. This involves majorly government and all the

authentic and stable companies. Hence it is much safer for investing within the London stock

exchange. In contrast to this the foreign issues being made by the Paris stock exchange is around

50%. In comparison of both it was found that London stock exchange is having 60% of the

foreign stocks whereas Paris stock exchange is having only 50%.

In addition to this the Great Britain has a particular approach which explains that use

investment abroad helps in identifying the gap in return between the domestic and foreign asset.

The reason behind this fact is that the foreign investment provides more result as compared to the

domestic one. Hence it is advisable to the investors that they must invest through the London

stock exchange rather than the Paris stock exchange. Along with this the British foreign

investment were also allowed Victoria investors to hold the diversify portfolio used in order to

enhance their performance. Moreover a little emphasis was also put over the geographical

distribution of these foreign investments. This is considered as a methodology that European

investors were aware of all the investments at the end of the 19th century.

investments with London stock exchange rather than Paris stock exchange. This is particularly

because of the reason that the London stock exchange account for 60% of the total nominal value

of all the stocks listed on the exchange. In addition to this the one third of all these topics

accounts for foreign stocks which are issued by the foreign Government and the municipalities.

On the other hand 40% of the stocks are devoted to the railways (Chang, McAleer and Wong,

2018).

In addition to this the remaining are financed through mines and plantation along with

banks and financial institutions of public utilities. This involves majorly government and all the

authentic and stable companies. Hence it is much safer for investing within the London stock

exchange. In contrast to this the foreign issues being made by the Paris stock exchange is around

50%. In comparison of both it was found that London stock exchange is having 60% of the

foreign stocks whereas Paris stock exchange is having only 50%.

In addition to this the Great Britain has a particular approach which explains that use

investment abroad helps in identifying the gap in return between the domestic and foreign asset.

The reason behind this fact is that the foreign investment provides more result as compared to the

domestic one. Hence it is advisable to the investors that they must invest through the London

stock exchange rather than the Paris stock exchange. Along with this the British foreign

investment were also allowed Victoria investors to hold the diversify portfolio used in order to

enhance their performance. Moreover a little emphasis was also put over the geographical

distribution of these foreign investments. This is considered as a methodology that European

investors were aware of all the investments at the end of the 19th century.

REFERENCES

Books and Journals

Raza, Z., 2020. The expected values of arithmetic bond connectivity and geometric indices in

random phenylene chains. Heliyon. 6(7). p.e04479.

Caine, B. A., Dardonville, C. and Popelier, P. L., 2018. Prediction of Aqueous p K a Values for

Guanidine-Containing Compounds Using Ab Initio Gas-Phase Equilibrium Bond

Lengths. ACS omega. 3(4). pp.3835-3850.

Wu, X. And et.al., 2020. H-bond interactions between arsenite and deoxynucleotides at different

pH values: A combined computational and experimental study. Chemosphere. 251.

p.126395.

Harvey, C.R., 2017. Presidential address: The scientific outlook in financial economics. The

Journal of Finance, 72(4), pp.1399-1440.

Harvey, C.R. and Liu, Y., 2020. False (and missed) discoveries in financial economics. The

Journal of Finance, 75(5), pp.2503-2553.

Chang, C.L., McAleer, M. and Wong, W.K., 2018. Management information, decision sciences,

and financial economics: A connection (No. TI 2018-004/III). Tinbergen Institute

Discussion Paper.

Books and Journals

Raza, Z., 2020. The expected values of arithmetic bond connectivity and geometric indices in

random phenylene chains. Heliyon. 6(7). p.e04479.

Caine, B. A., Dardonville, C. and Popelier, P. L., 2018. Prediction of Aqueous p K a Values for

Guanidine-Containing Compounds Using Ab Initio Gas-Phase Equilibrium Bond

Lengths. ACS omega. 3(4). pp.3835-3850.

Wu, X. And et.al., 2020. H-bond interactions between arsenite and deoxynucleotides at different

pH values: A combined computational and experimental study. Chemosphere. 251.

p.126395.

Harvey, C.R., 2017. Presidential address: The scientific outlook in financial economics. The

Journal of Finance, 72(4), pp.1399-1440.

Harvey, C.R. and Liu, Y., 2020. False (and missed) discoveries in financial economics. The

Journal of Finance, 75(5), pp.2503-2553.

Chang, C.L., McAleer, M. and Wong, W.K., 2018. Management information, decision sciences,

and financial economics: A connection (No. TI 2018-004/III). Tinbergen Institute

Discussion Paper.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.