ECOM2001 - Financial Asset Portfolio Analysis Project Semester 1

VerifiedAdded on 2023/04/03

|17

|1458

|198

Project

AI Summary

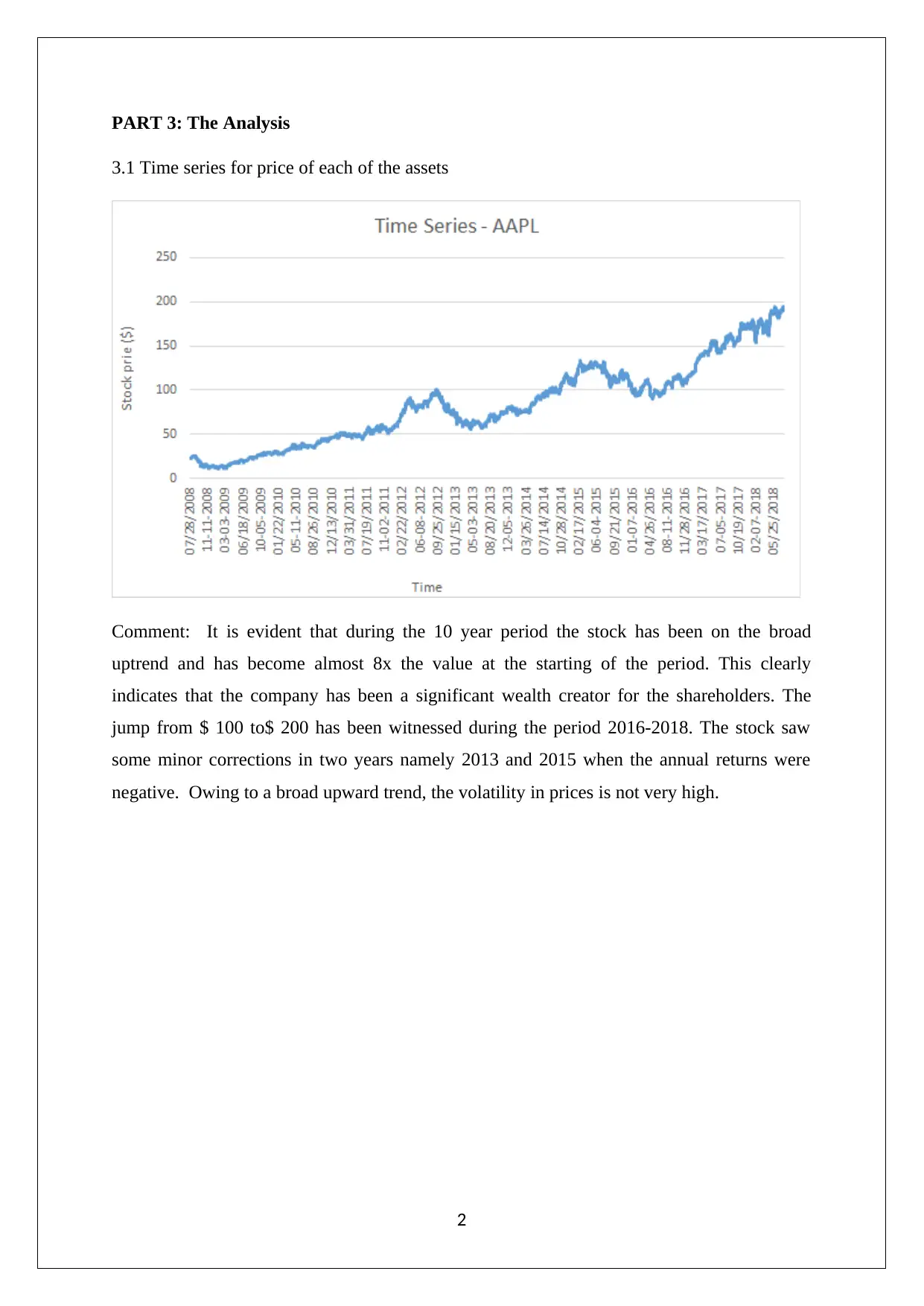

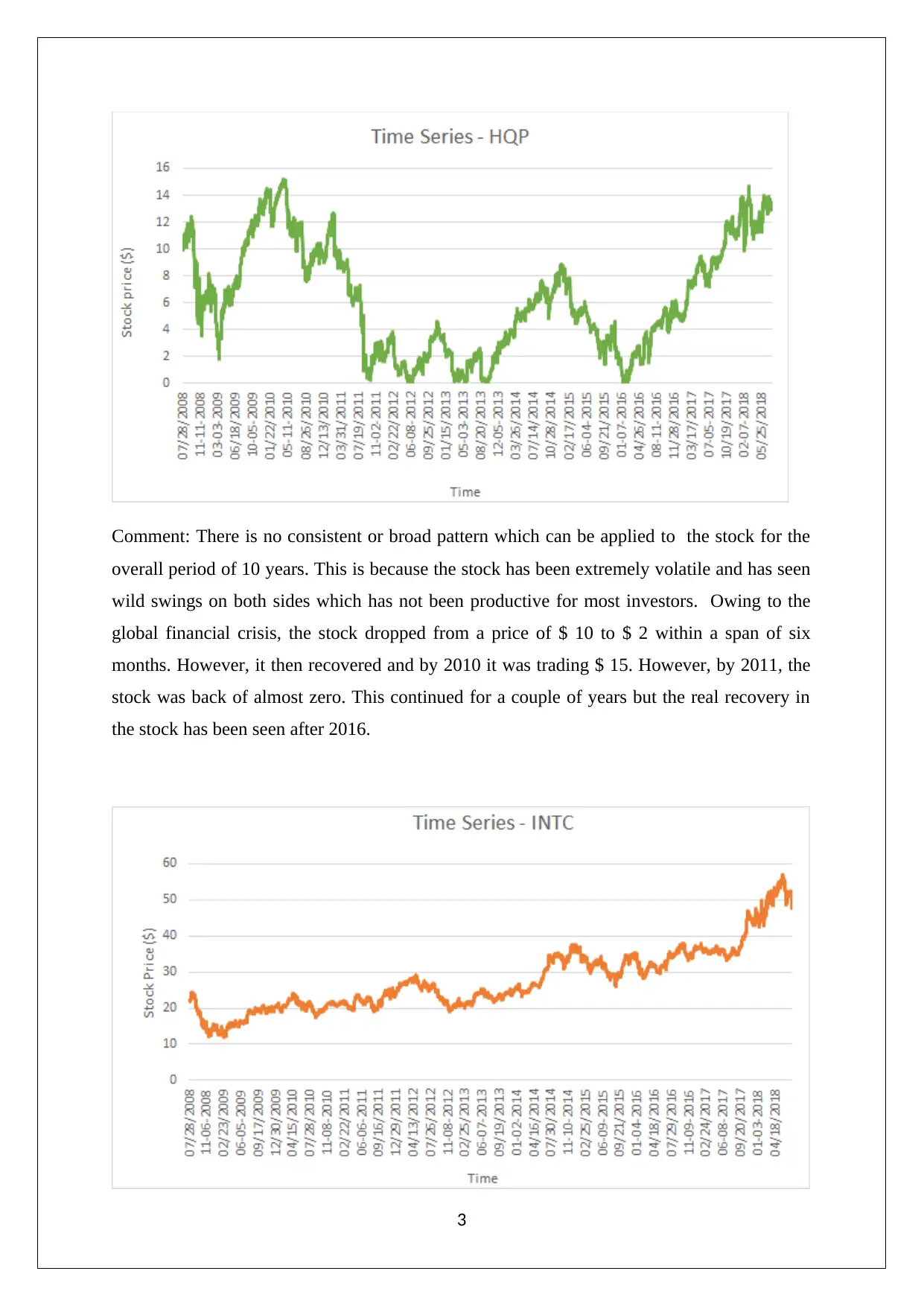

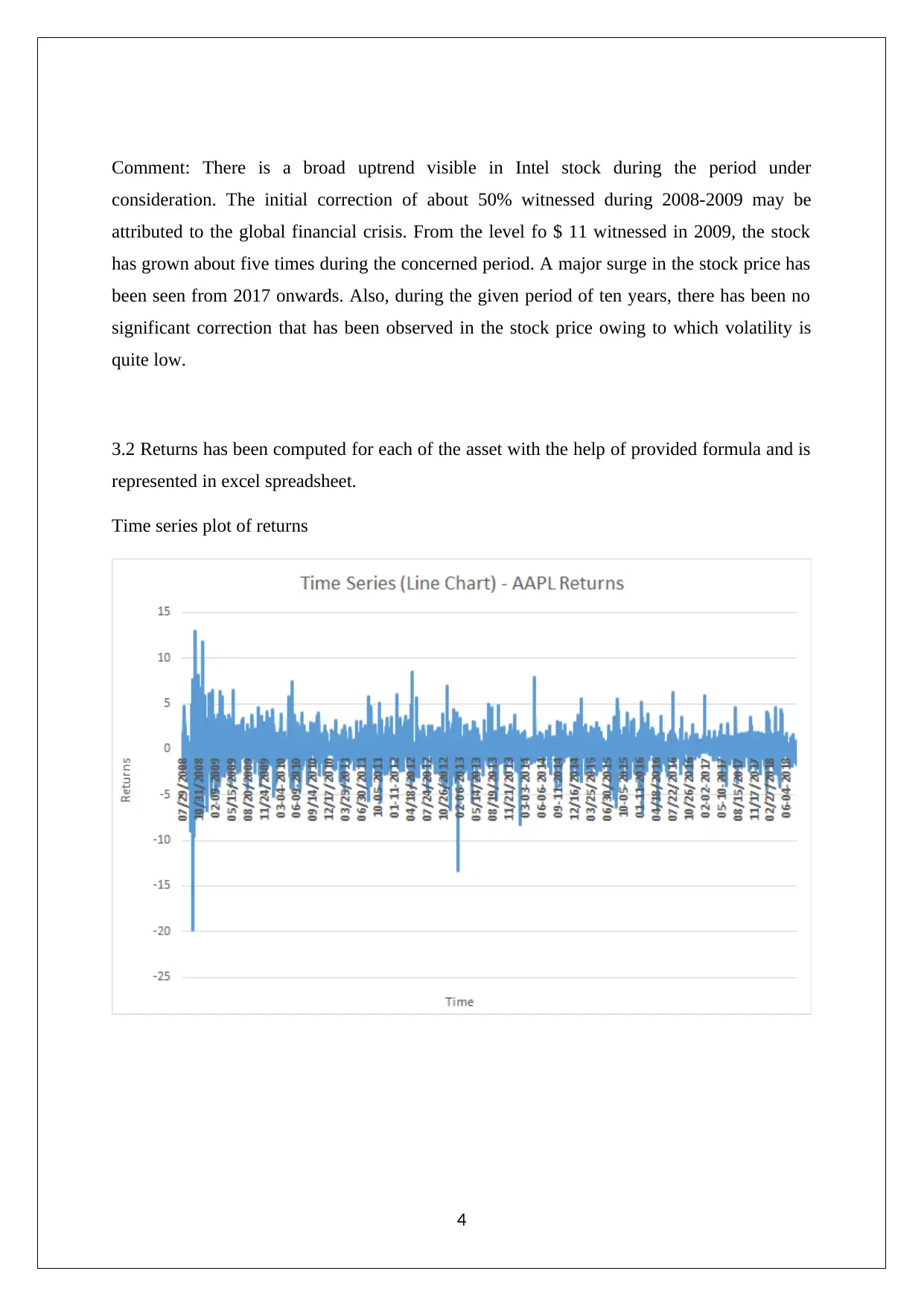

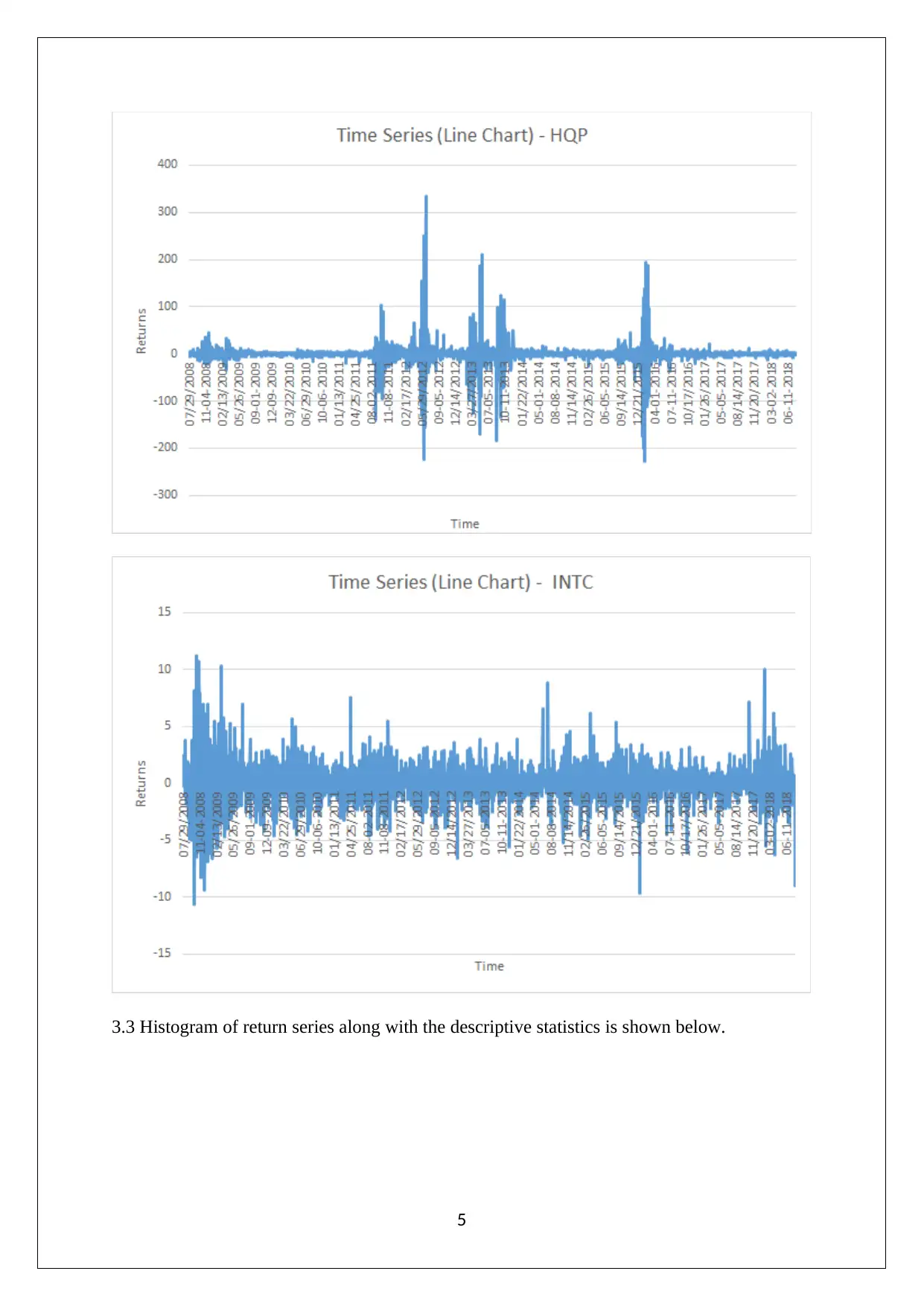

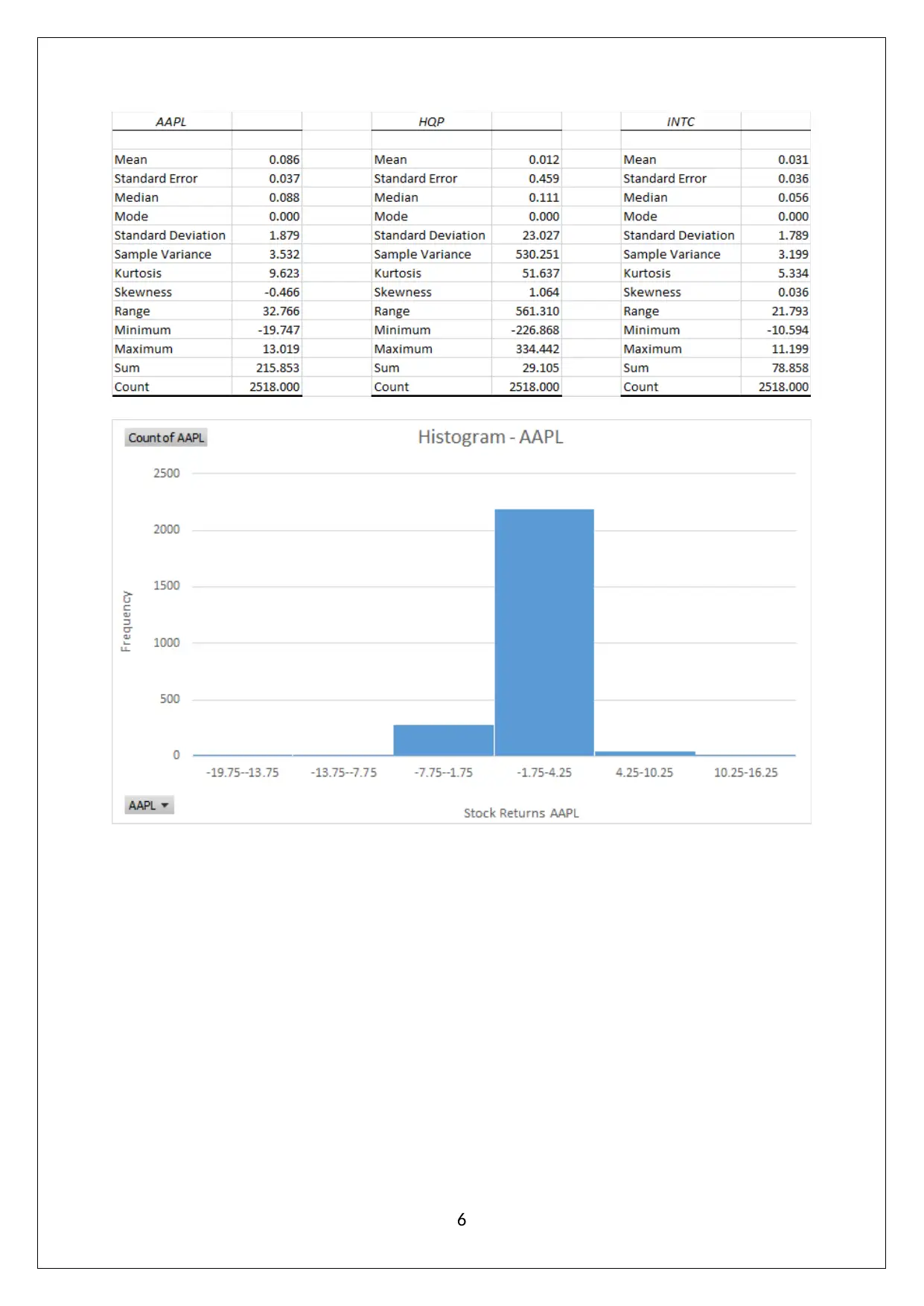

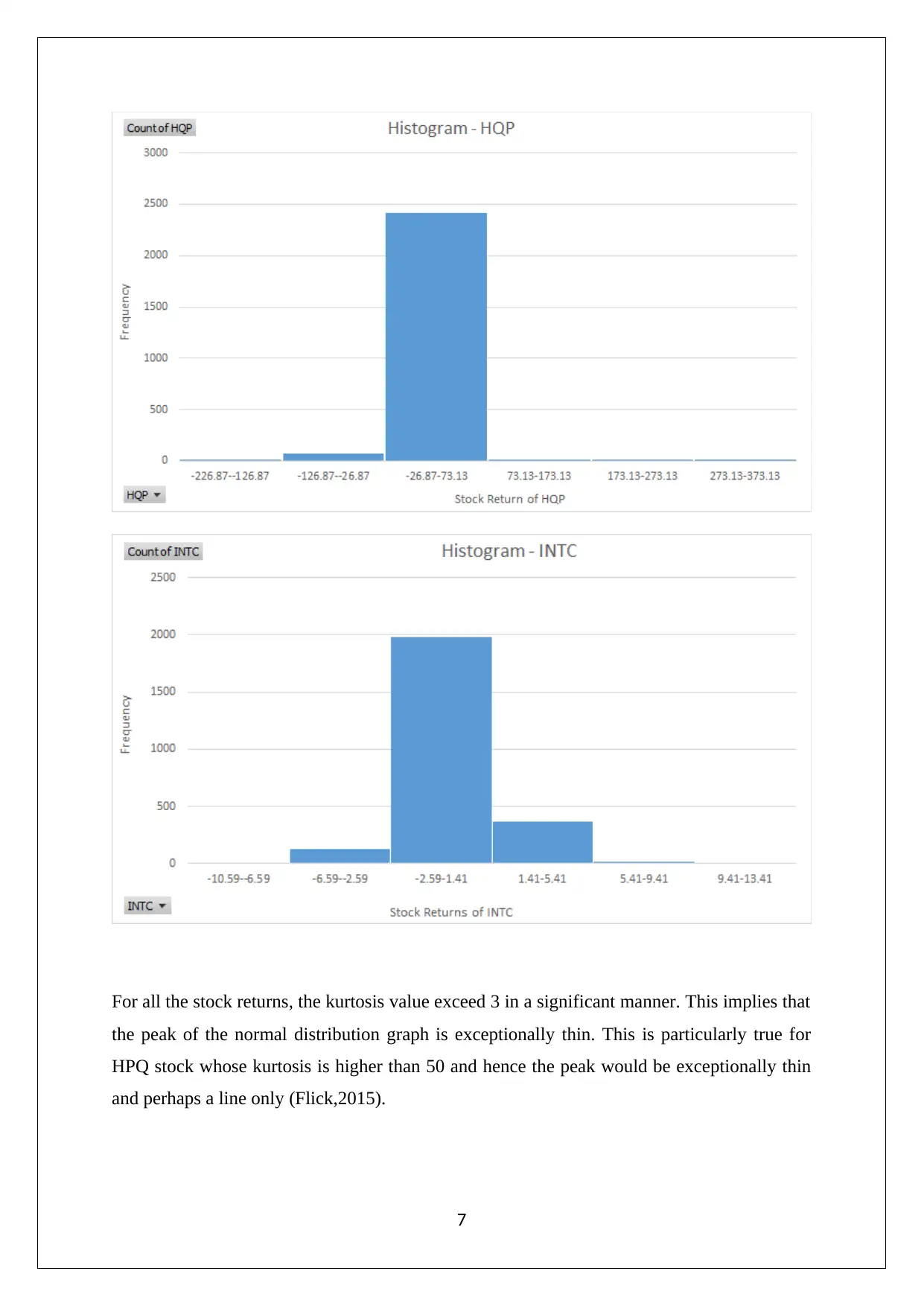

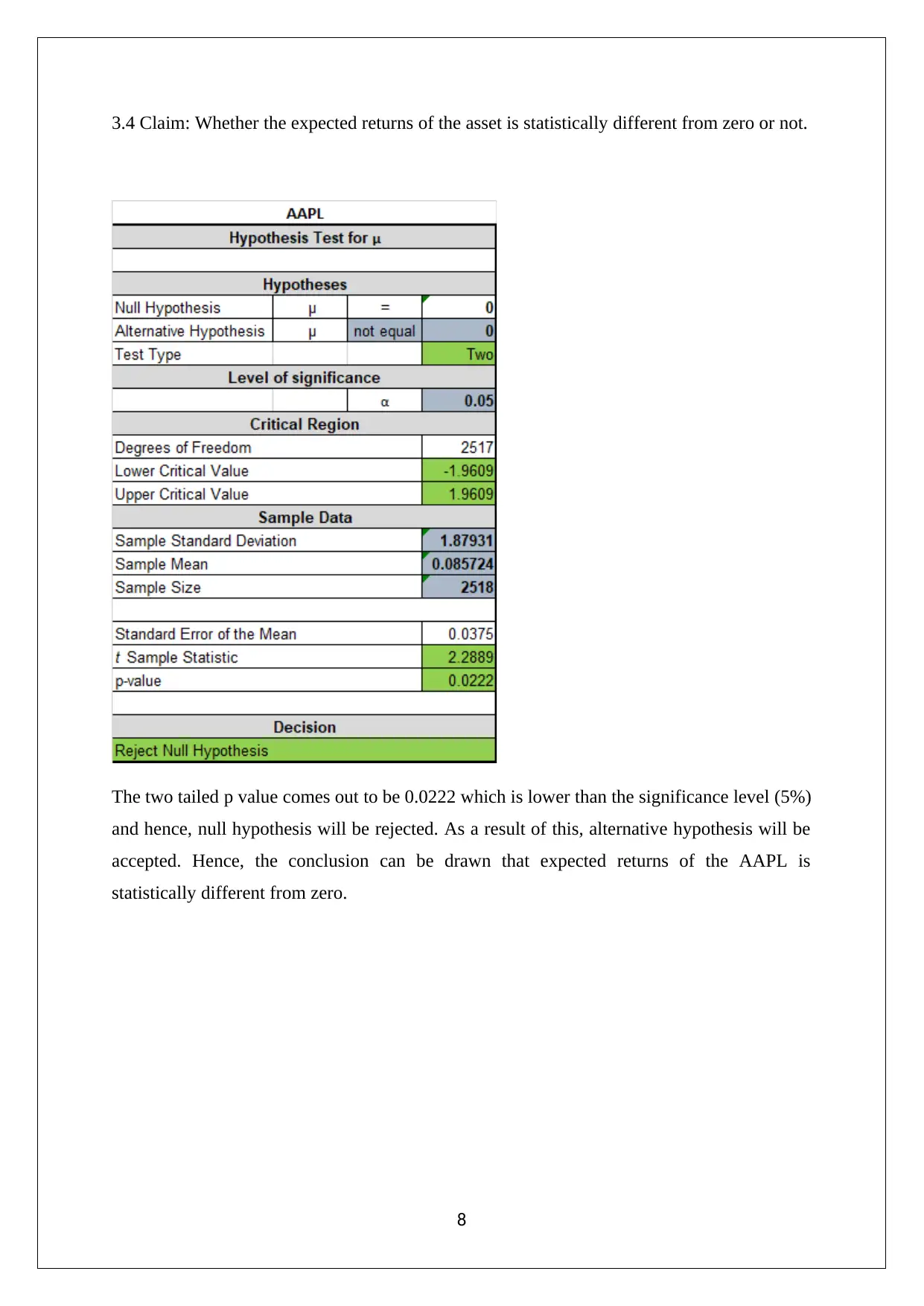

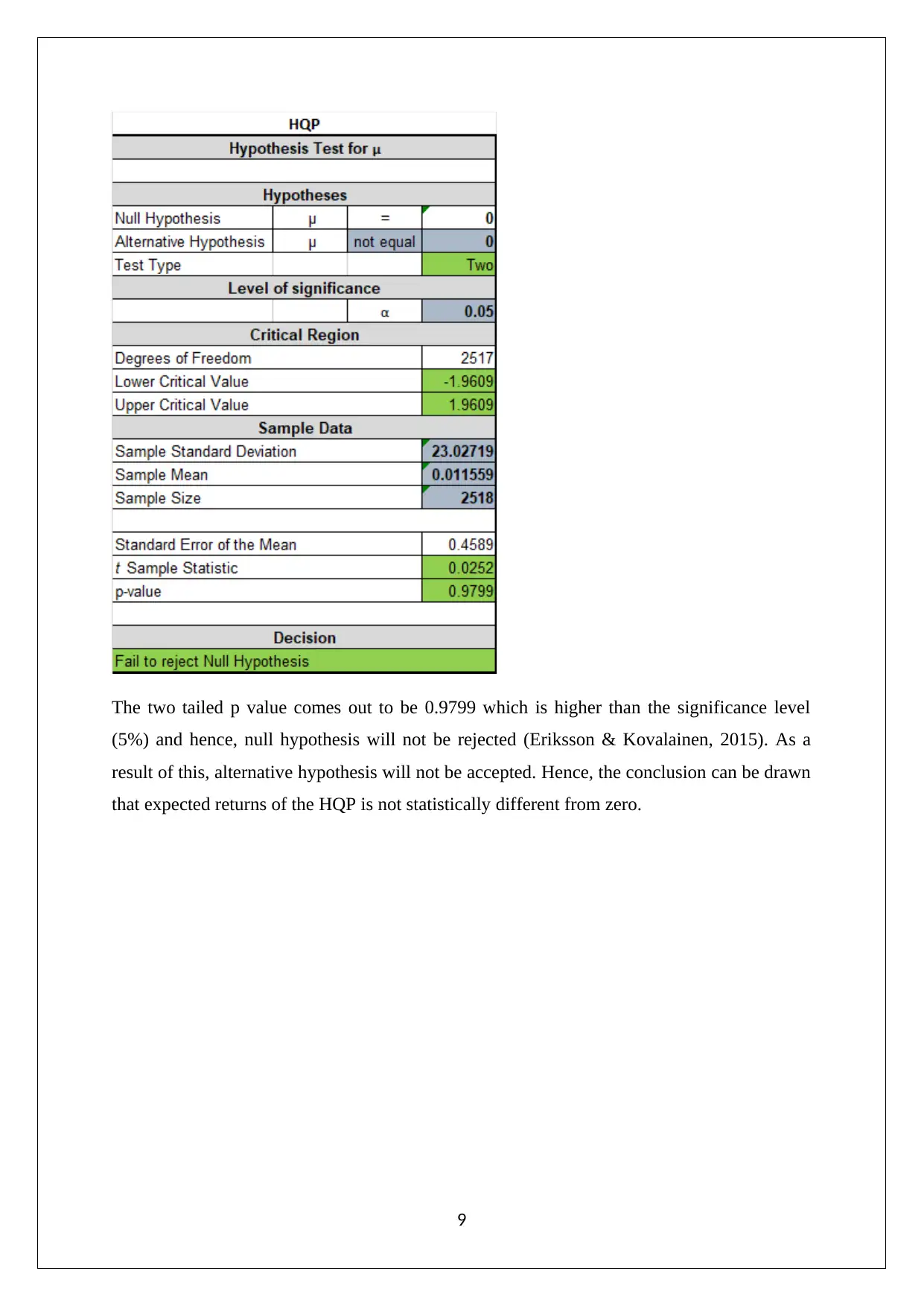

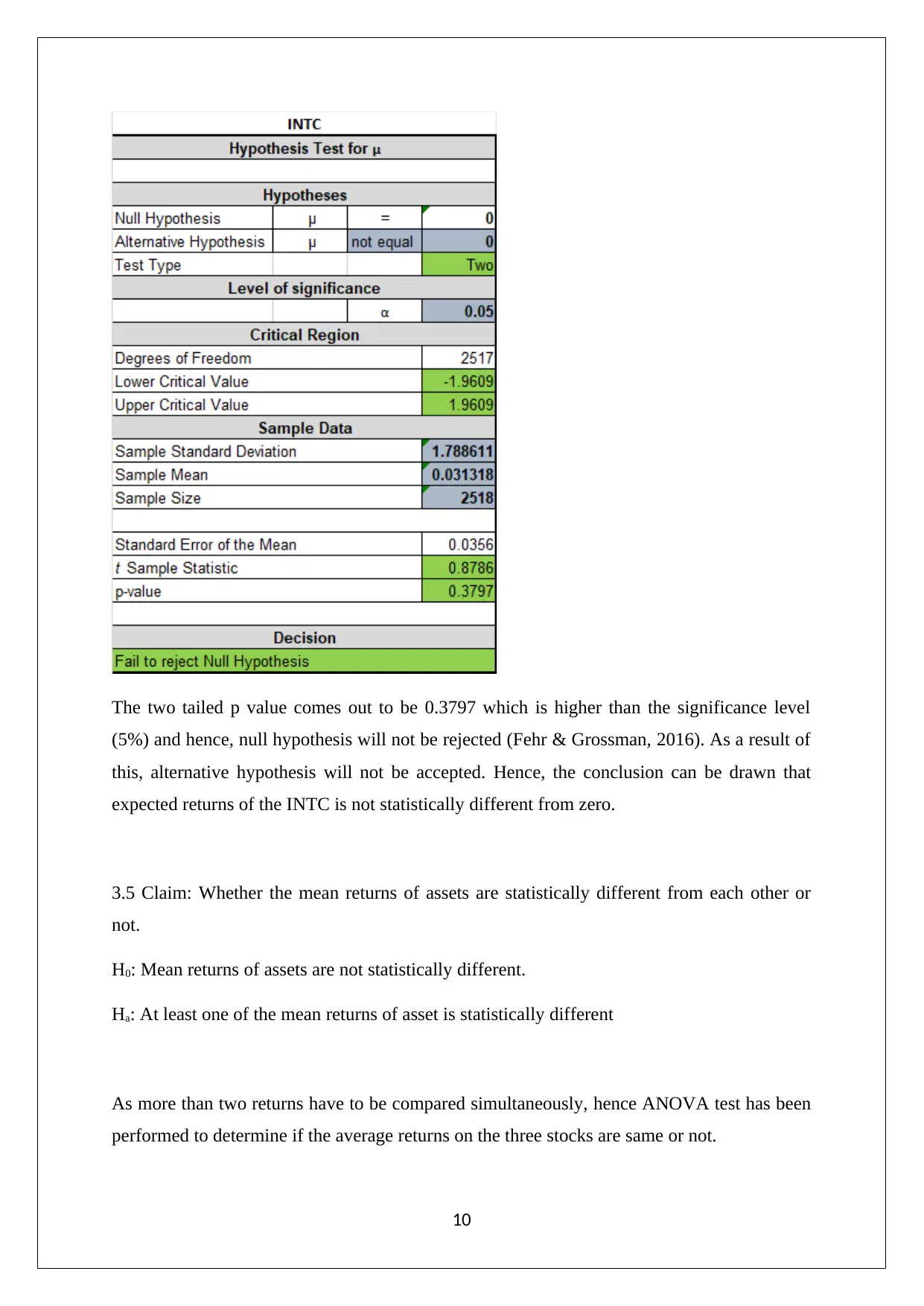

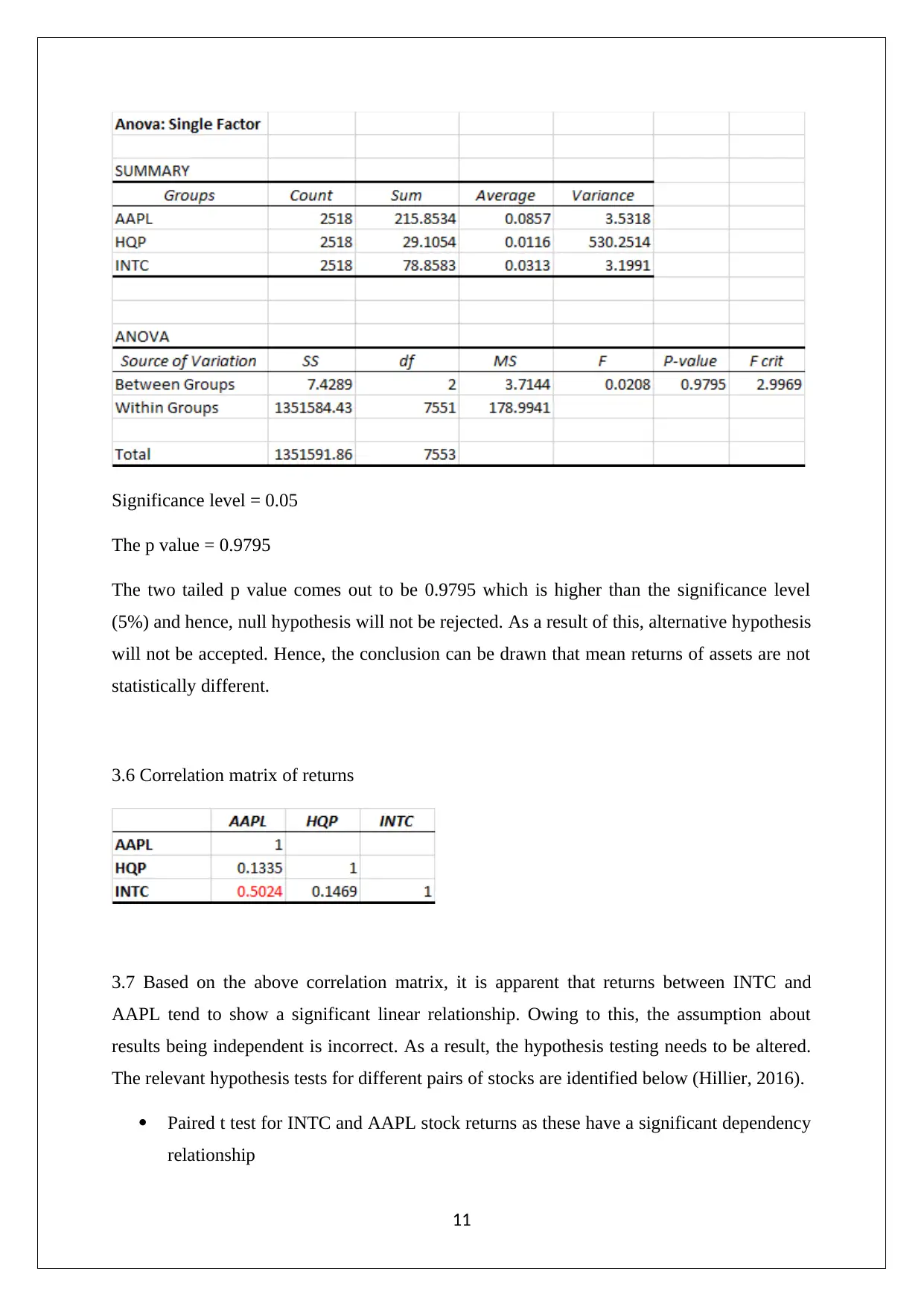

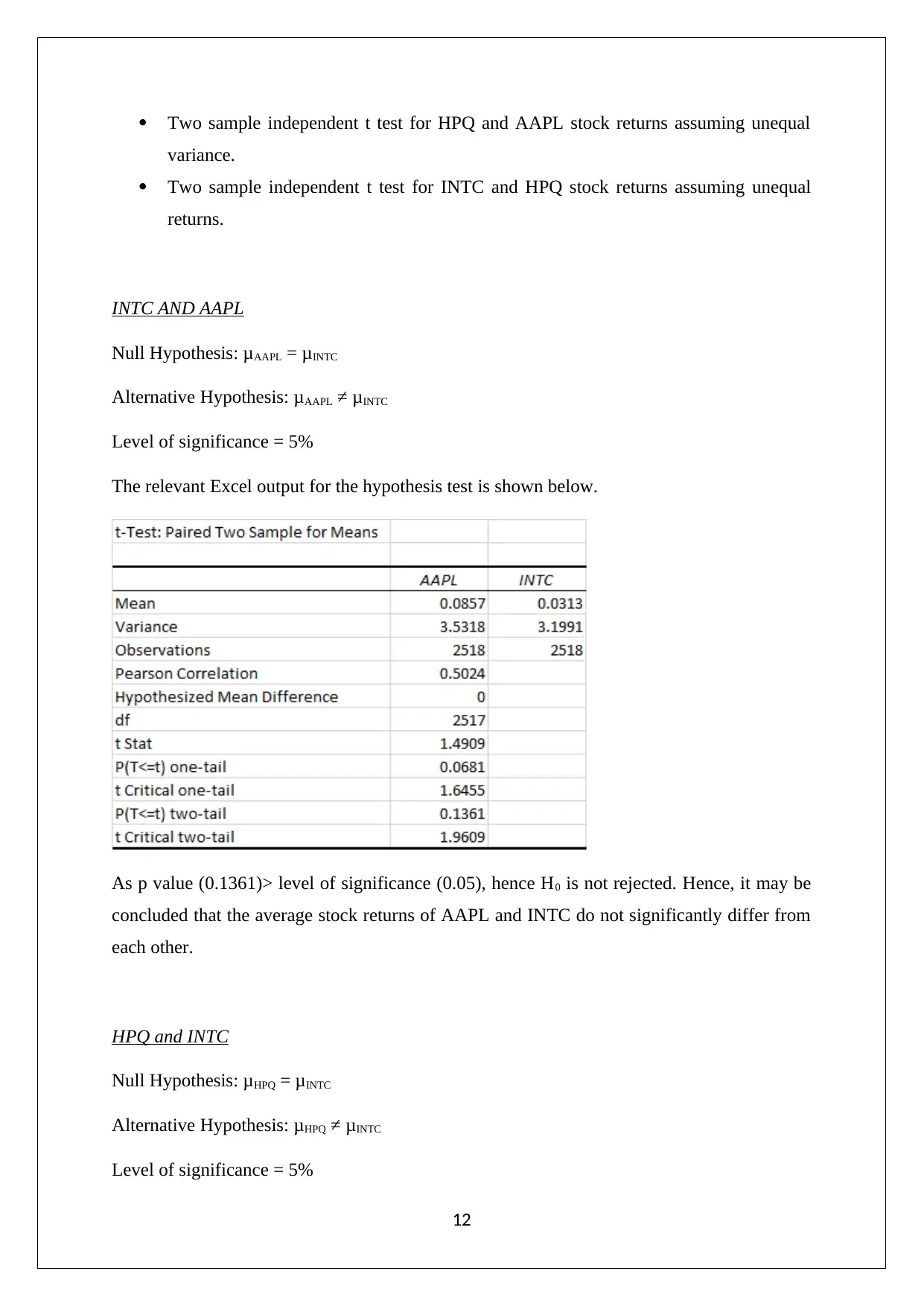

This project provides a detailed analysis of a portfolio composed of three financial assets: Apple (AAPL), Hewlett Packard (HPQ), and Intel (INTC). It includes plotting the prices of each asset over time, calculating and plotting returns, creating histograms of return series with descriptive statistics, and performing hypothesis tests to determine if the expected returns of the assets are statistically different from zero and from each other. The analysis incorporates time series plots, return calculations, kurtosis analysis, ANOVA testing, correlation matrices, and paired t-tests to assess the relationships between the assets. The project concludes with an objective function and optimal weight calculation for a two-stock portfolio consisting of AAPL and INTC, aiming to maximize returns per unit of risk, subject to constraints. The analysis also discusses the limitations of assuming a normal distribution for stock prices due to various market factors.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.