ECON 214: Problem Set on Money, Banking, and Monetary Policy

VerifiedAdded on 2023/06/15

|9

|1586

|422

Homework Assignment

AI Summary

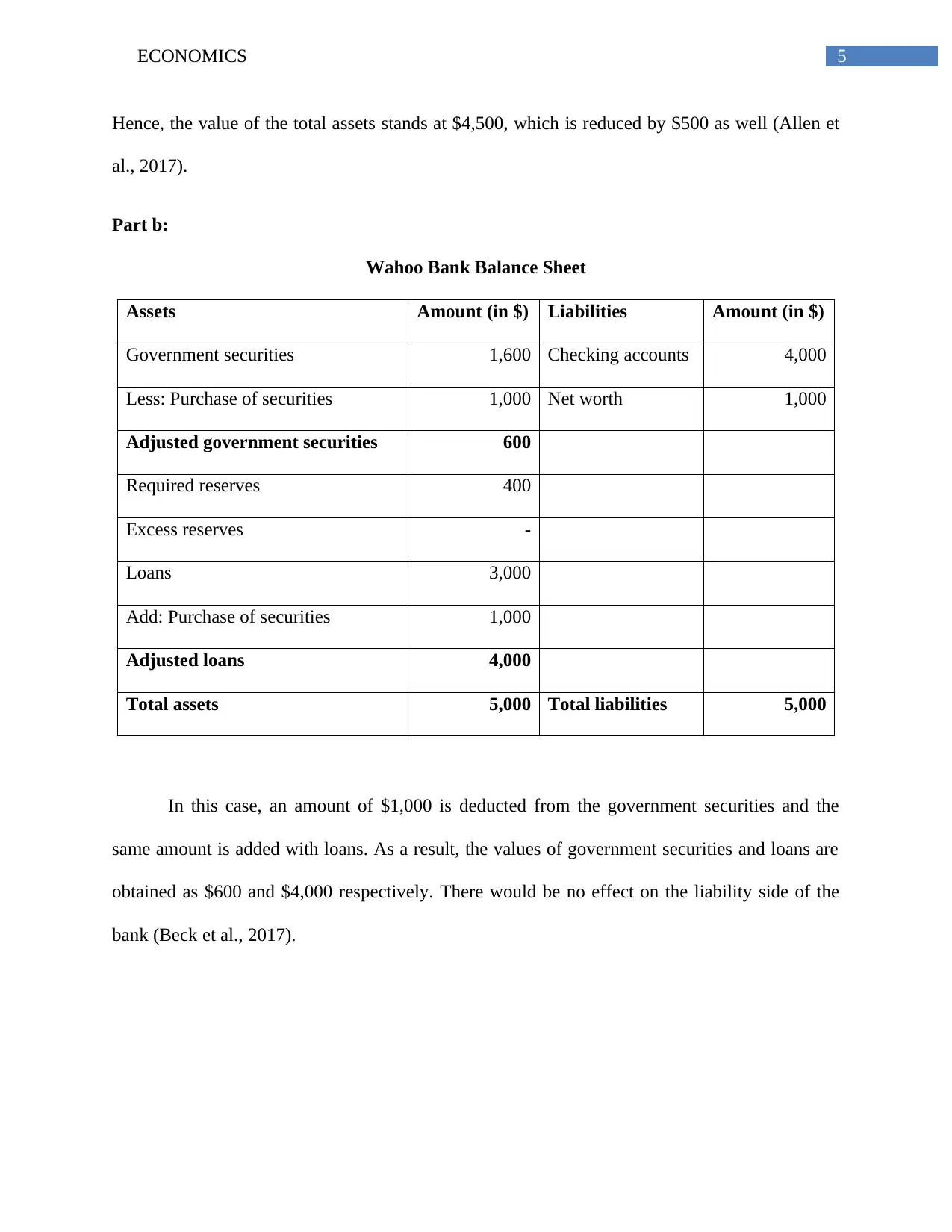

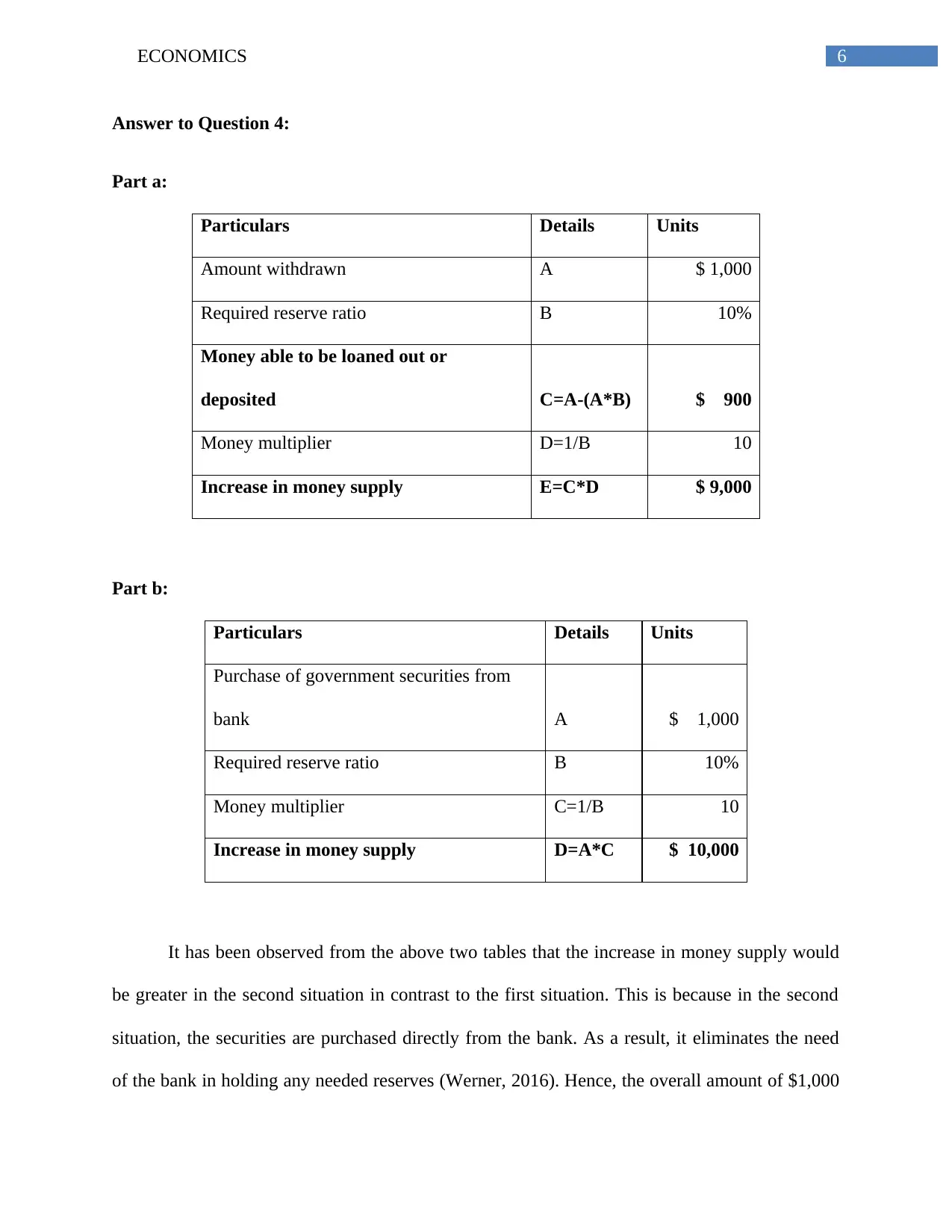

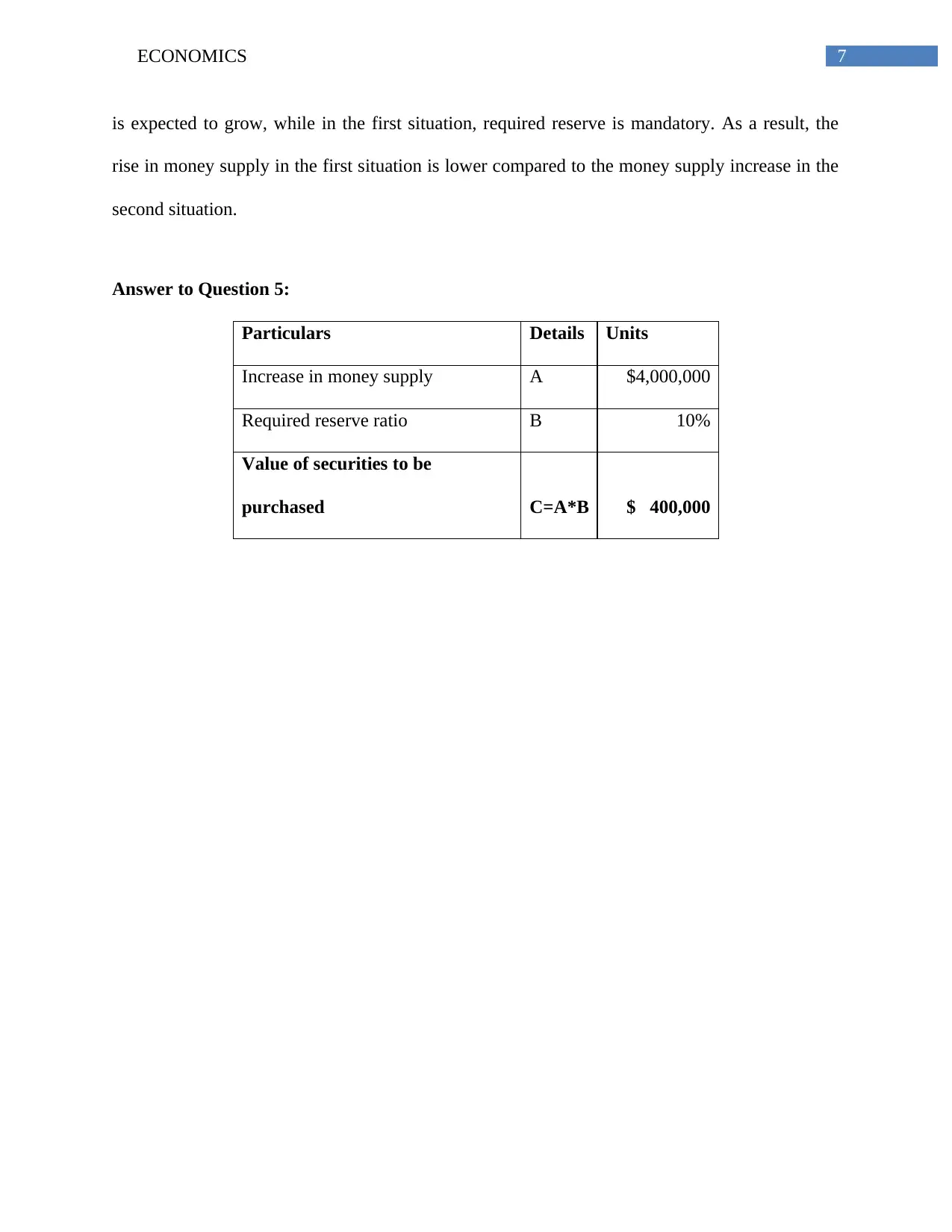

This assignment solution delves into key concepts of economics, starting with an exploration of the three primary functions of money: medium of exchange, unit of account, and store of value, emphasizing the medium of exchange as the most critical. It differentiates between the federal funds rate and the discount rate as tools used by the Federal Reserve in setting monetary policy. Through a series of balance sheet adjustments for Wahoo Bank, the assignment illustrates the impact of withdrawals and Federal Reserve actions on required reserves, excess reserves, and loan amounts. Furthermore, it analyzes scenarios involving money deposits and government securities purchases to determine their effects on the money supply, highlighting how direct purchases from banks lead to greater increases due to the elimination of required reserve holdings. The assignment concludes by calculating the value of government securities needed to be purchased to achieve a specific increase in the money supply, given a required reserve ratio. Desklib provides access to this and many other solved assignments for students.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.