Econometrics Homework: CEO Salary and Wage Equation Analysis

VerifiedAdded on 2023/01/11

|7

|995

|85

Homework Assignment

AI Summary

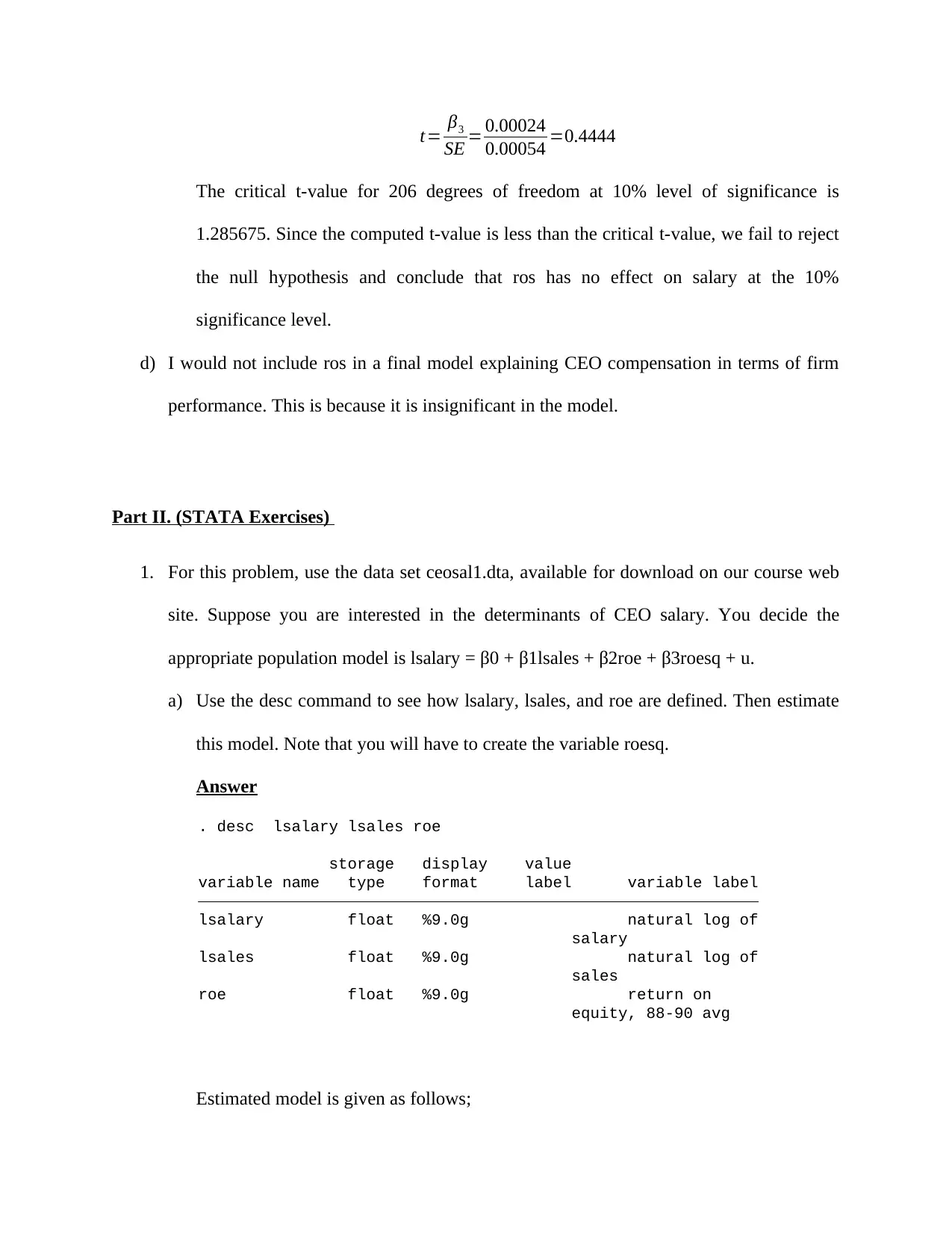

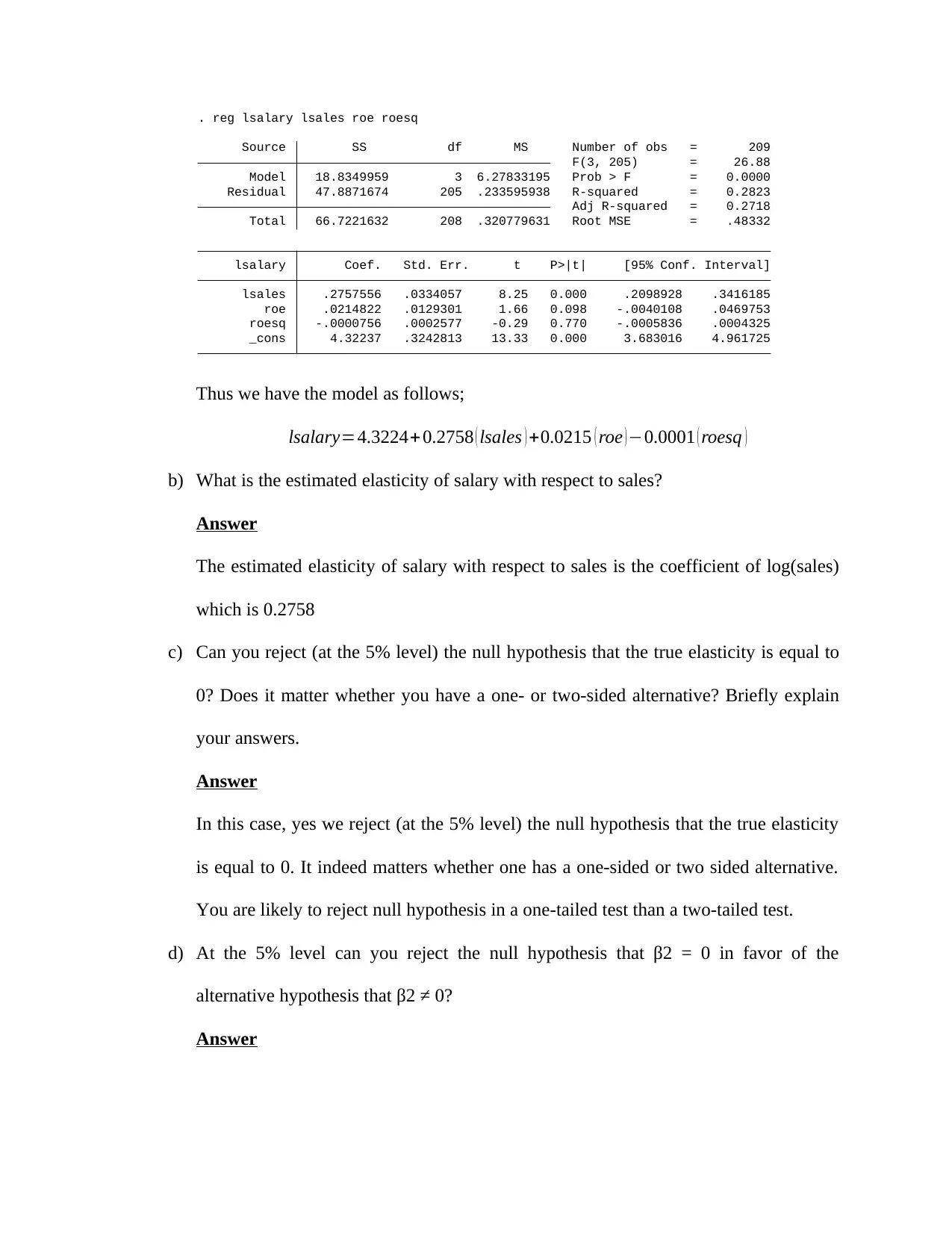

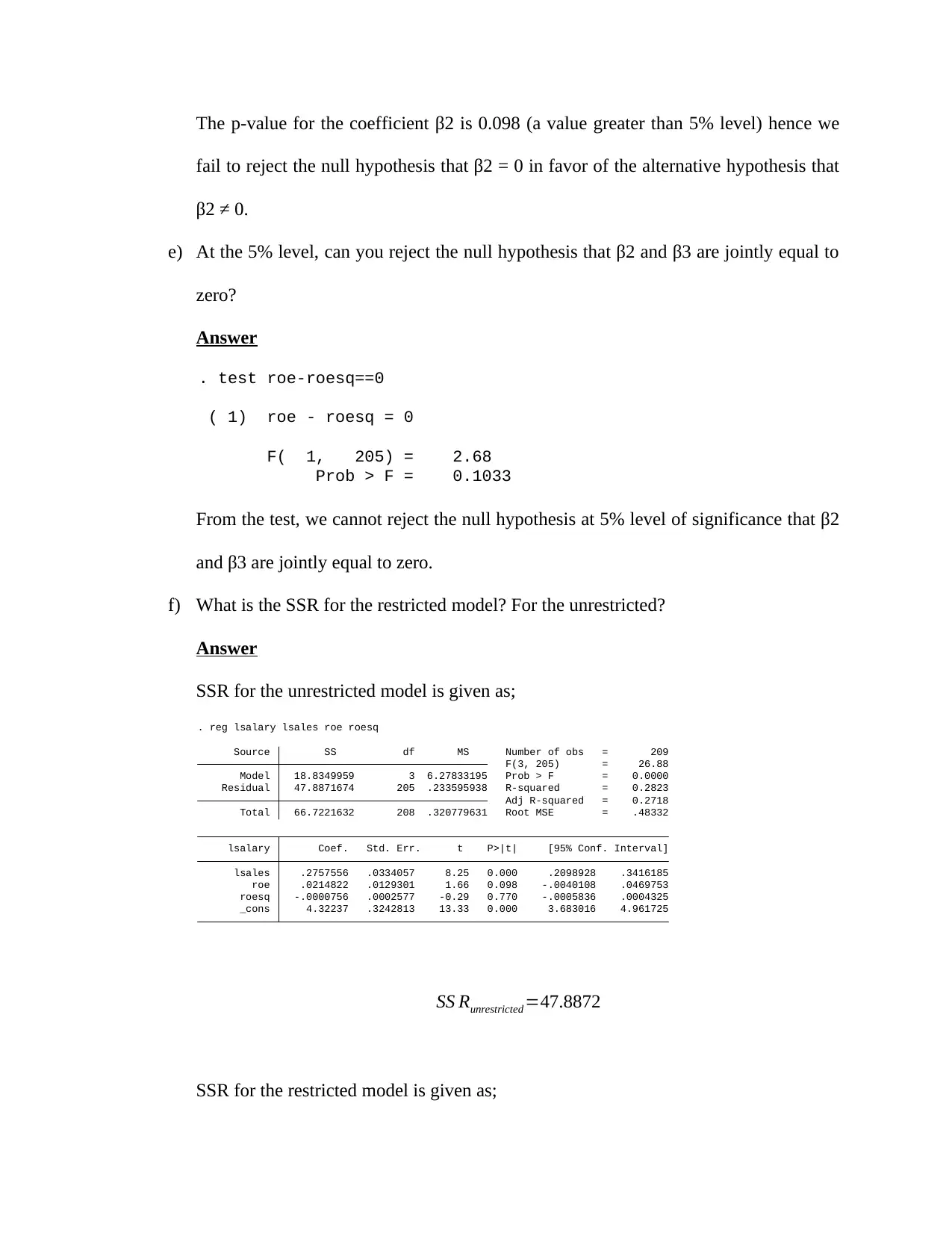

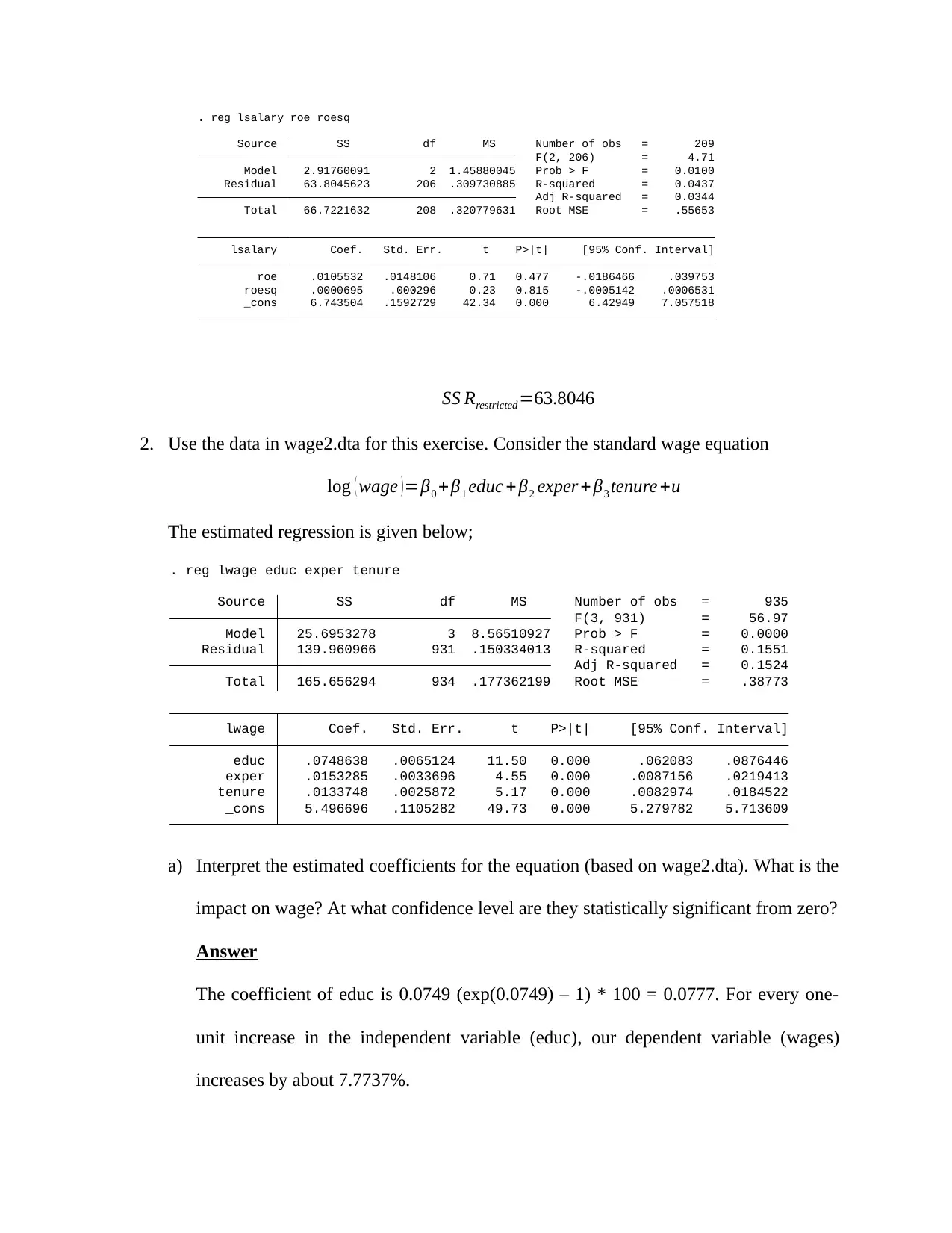

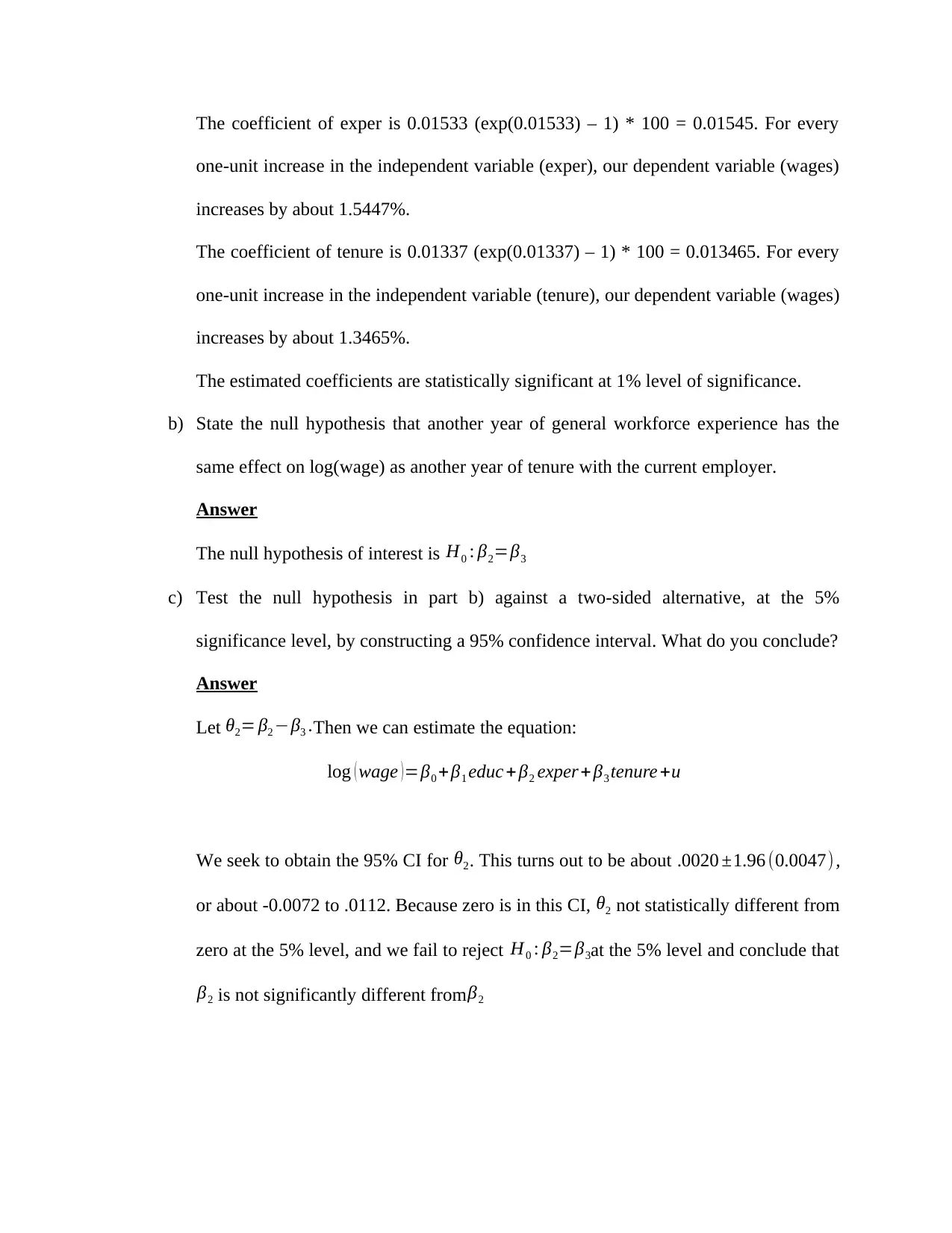

This document presents a comprehensive solution to an econometrics homework assignment. It begins with theoretical exercises focusing on causality and its measurement, specifically addressing the impact of illegal downloads on subscription growth and evaluating the effect of 'ros' on CEO salary. The solution then delves into STATA exercises using the 'ceosal1.dta' dataset to model CEO salary determinants, calculate elasticity, and test hypotheses regarding the elasticity of salary with respect to sales. Further analysis employs the 'wage2.dta' dataset to interpret wage equation coefficients, assess their statistical significance, and test hypotheses about the impact of general work experience and tenure on wages, including constructing and interpreting a 95% confidence interval. The document provides detailed interpretations and statistical tests, demonstrating a strong understanding of econometric principles.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.