Economic Principles: Opportunity Cost and Budget Constraint Analysis

VerifiedAdded on 2022/08/22

|7

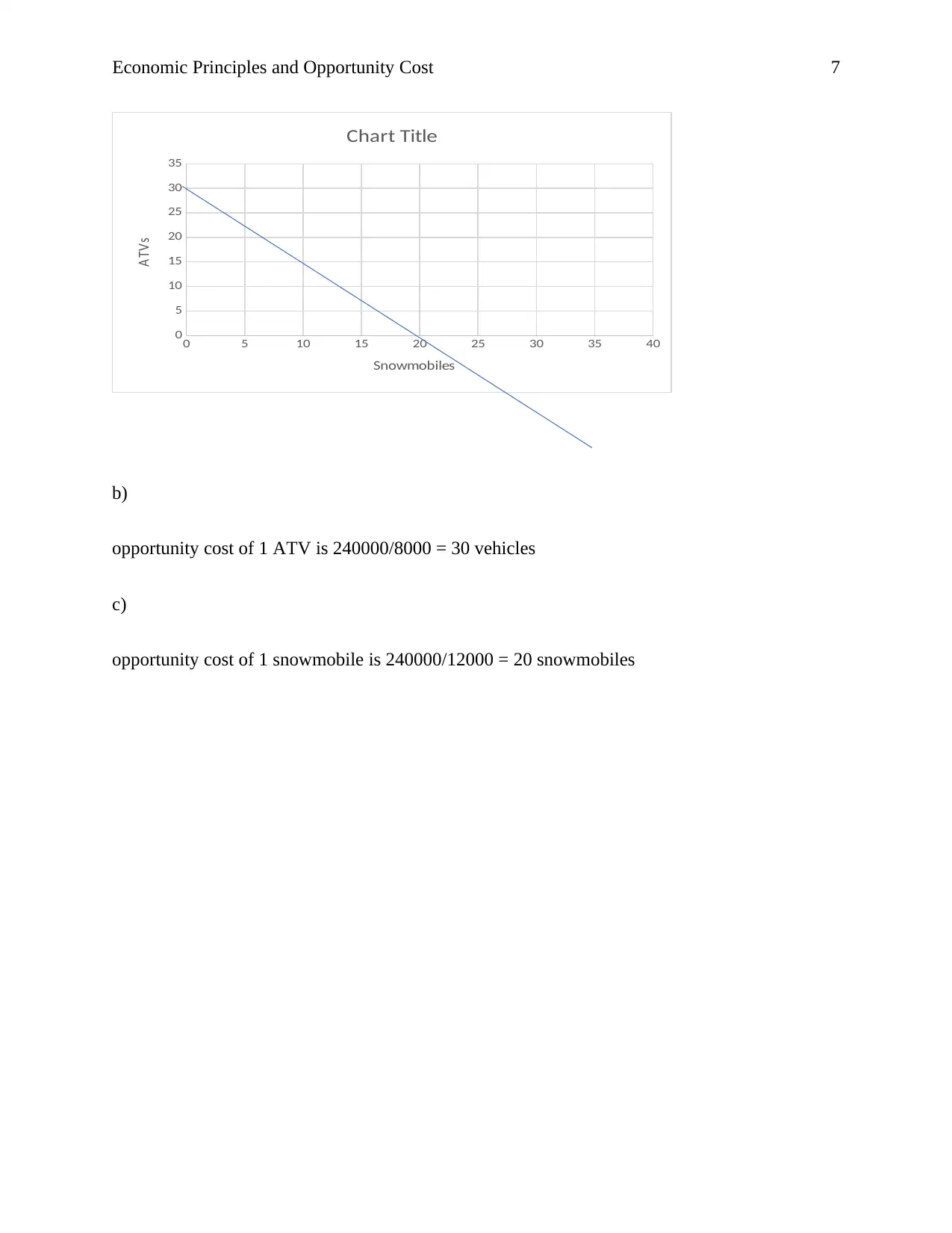

|930

|17

Homework Assignment

AI Summary

This assignment analyzes key economic principles, including trade-offs, opportunity cost, marginal thinking, and incentives. The student explores these concepts through practical examples, such as resource allocation and production decisions. The paper examines opportunity cost in production scenarios, calculating the cost of producing apples and pears. It also analyzes budget constraints, constructing a budget line and calculating opportunity costs for purchasing ATVs and snowmobiles. The assignment uses equations and graphical representations to illustrate economic concepts, providing a comprehensive understanding of how these principles apply to real-world decision-making. The document is available on Desklib, a platform offering valuable resources for students seeking assistance with their coursework.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.