Economic Principles Analysis: BEO1105 Assignment Solution

VerifiedAdded on 2022/08/31

|11

|1199

|22

Homework Assignment

AI Summary

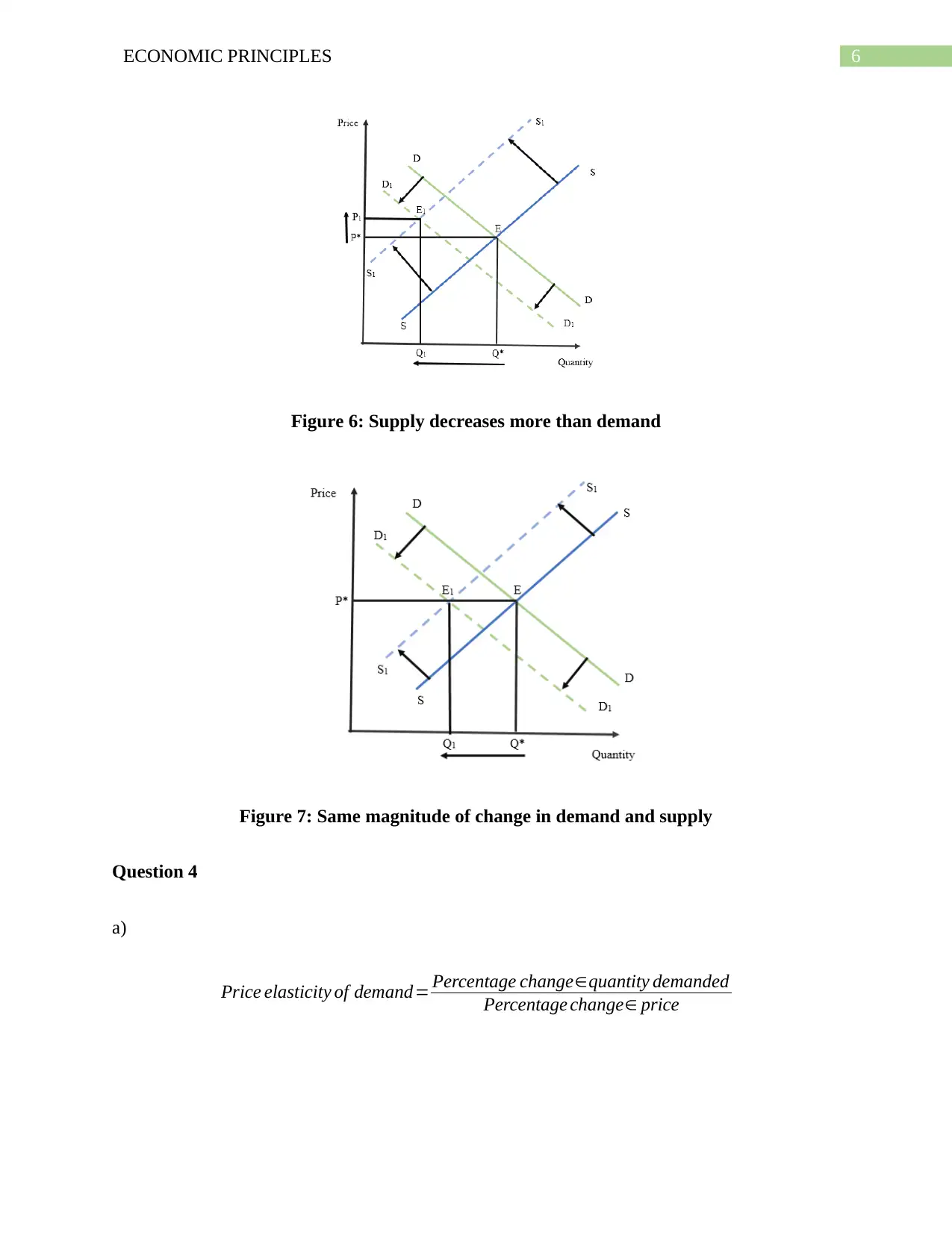

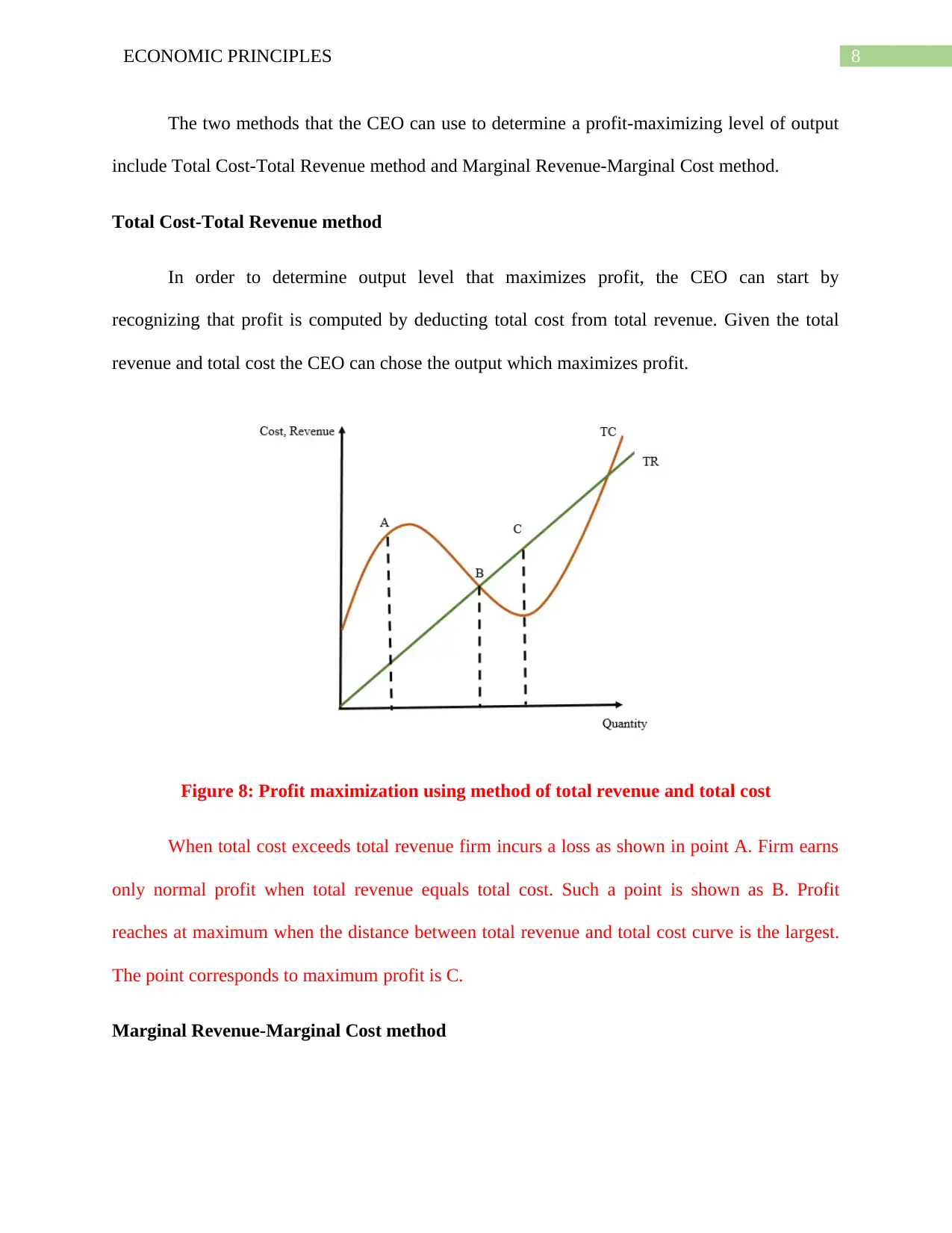

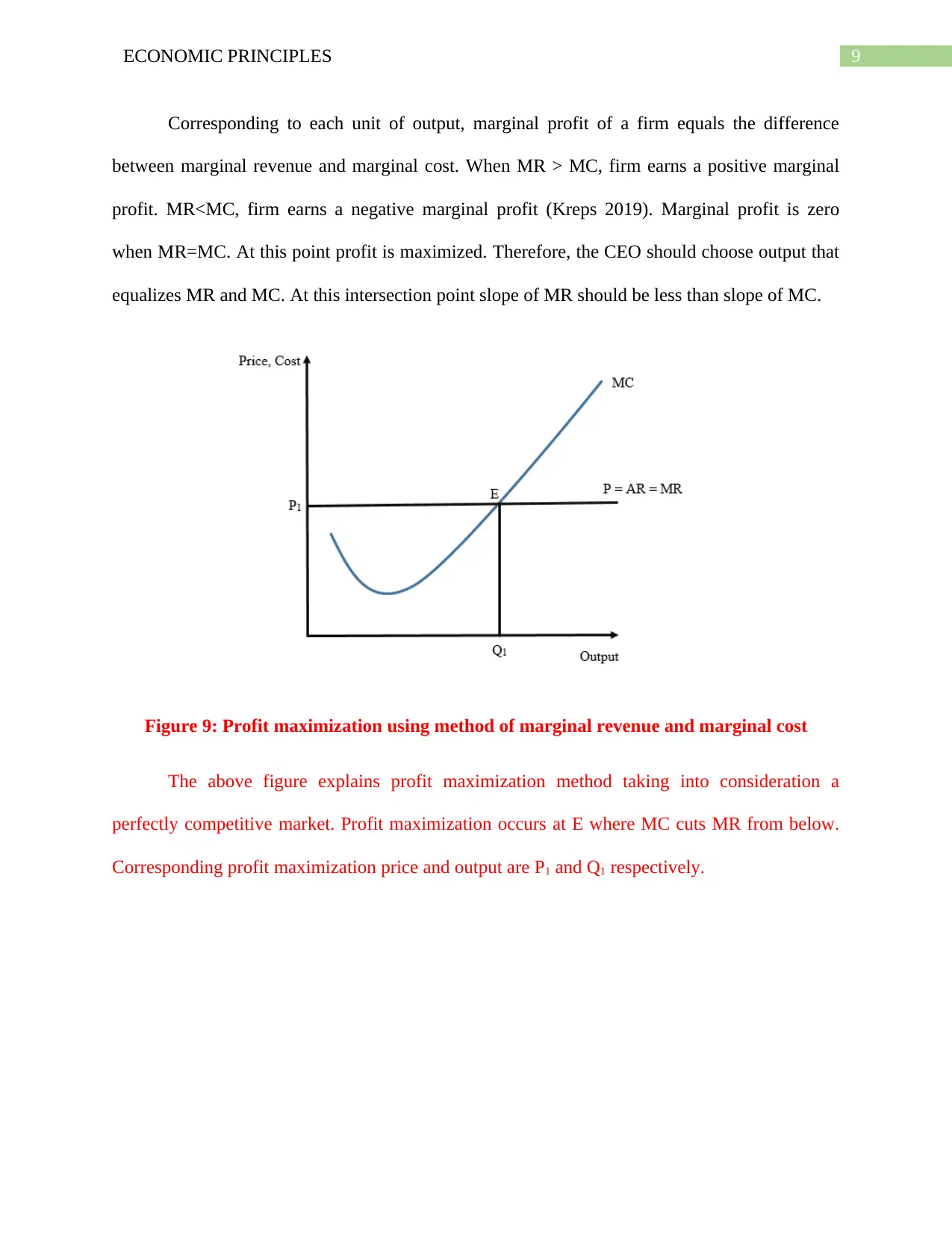

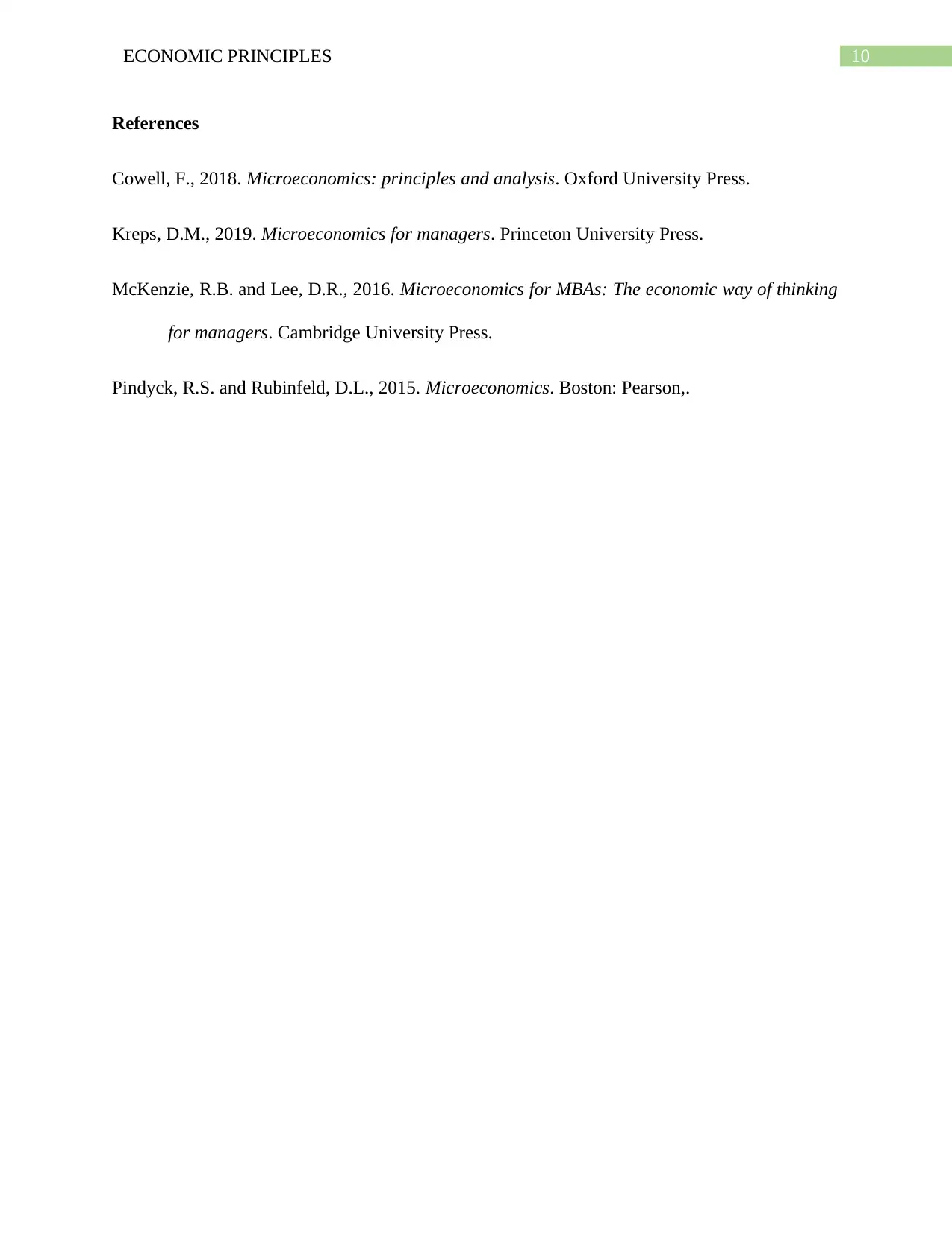

This assignment solution for an economics course (BEO1105) analyzes various economic principles and market dynamics. It addresses questions related to the impact of changes in prices of substitute goods, adoption of new technologies, and income fluctuations on the apple market, using demand and supply graphs to illustrate the market equilibrium adjustments. The solution also critiques flawed reasoning regarding demand curve shifts versus movements along the curve, specifically in the context of garlic consumption. Additionally, it examines the effects of African swine fever on the live pig market in China. The assignment further explores the concept of price elasticity of demand and its implications for revenue maximization. Finally, the solution presents and compares two methods—the total cost-total revenue method and the marginal revenue-marginal cost method—that a CEO can use to determine the profit-maximizing level of output, providing graphical representations and explanations of each method.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.