Economic Principles and Decision Making Assignment - ECON6000

VerifiedAdded on 2023/01/17

|8

|1169

|42

Homework Assignment

AI Summary

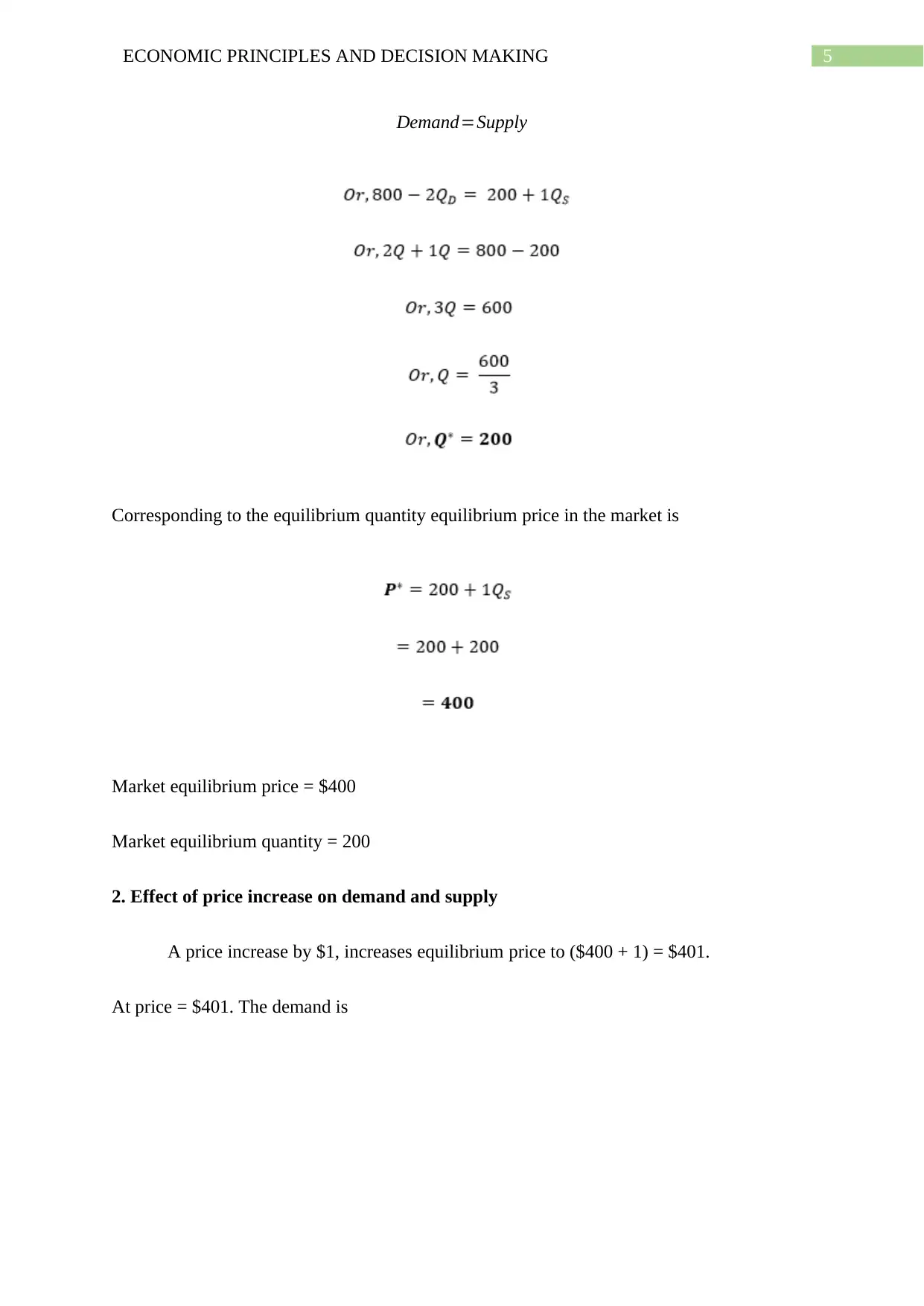

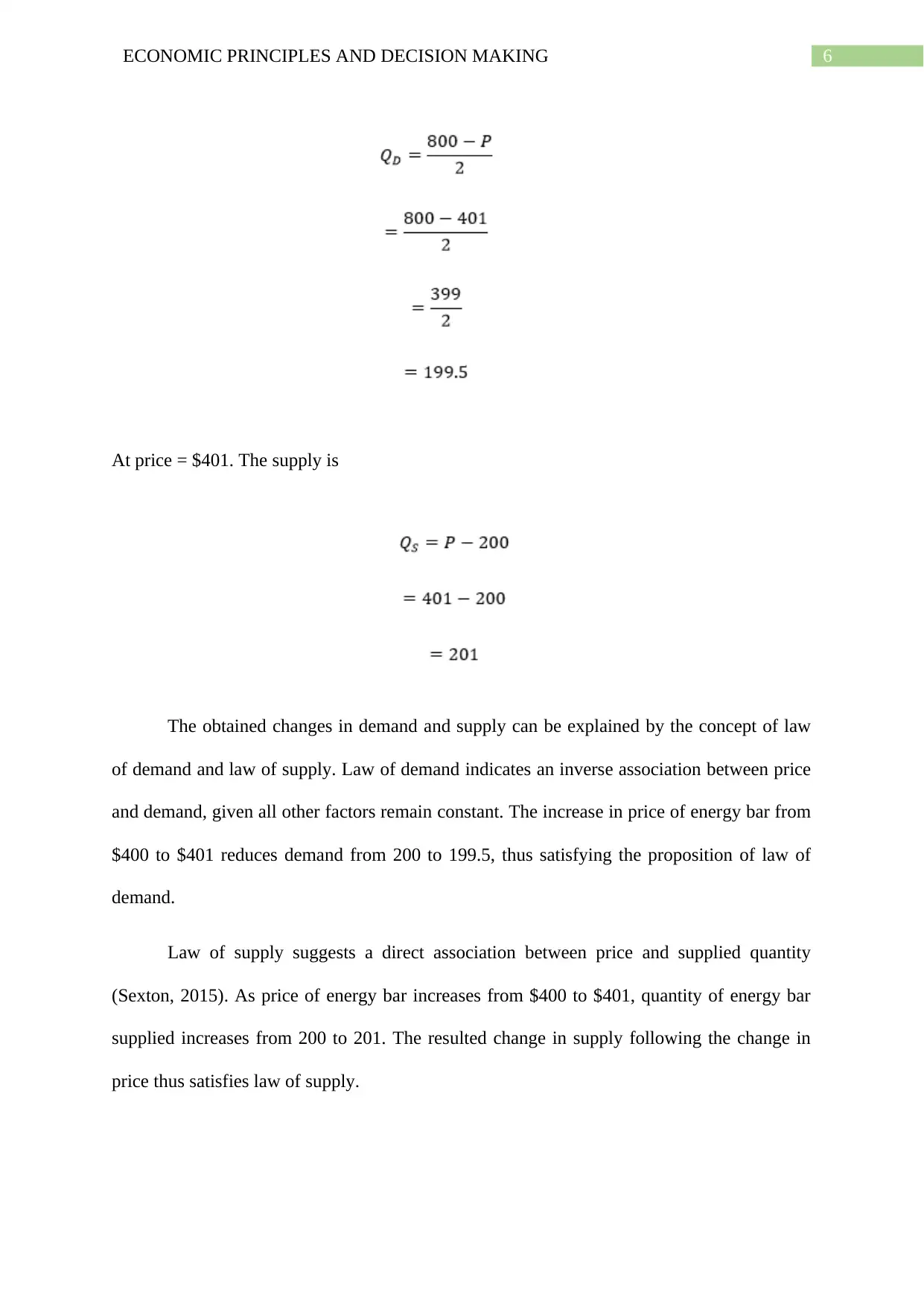

This assignment solution addresses two economic problems. Problem A explores the production possibilities frontier (PPF) in District D, analyzing the production of Schmeckt Gut energy bars and Schmeckt Gut 2.0, including the impact of increased demand and strategies to meet it. It covers the assumptions underlying the PPF, its characteristics (downward slope and concavity), and the concept of opportunity cost. Problem B focuses on determining the equilibrium price and quantity in the local market of Industria, using demand and supply functions for energy bars. It calculates the equilibrium point and examines the effects of a price increase on demand and supply, demonstrating the application of the laws of demand and supply. The solution includes graphical representations and detailed explanations of economic concepts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.