Economic Assignment on Rationality, Incentives, and Income Elasticity

VerifiedAdded on 2021/04/16

|9

|1401

|21

Homework Assignment

AI Summary

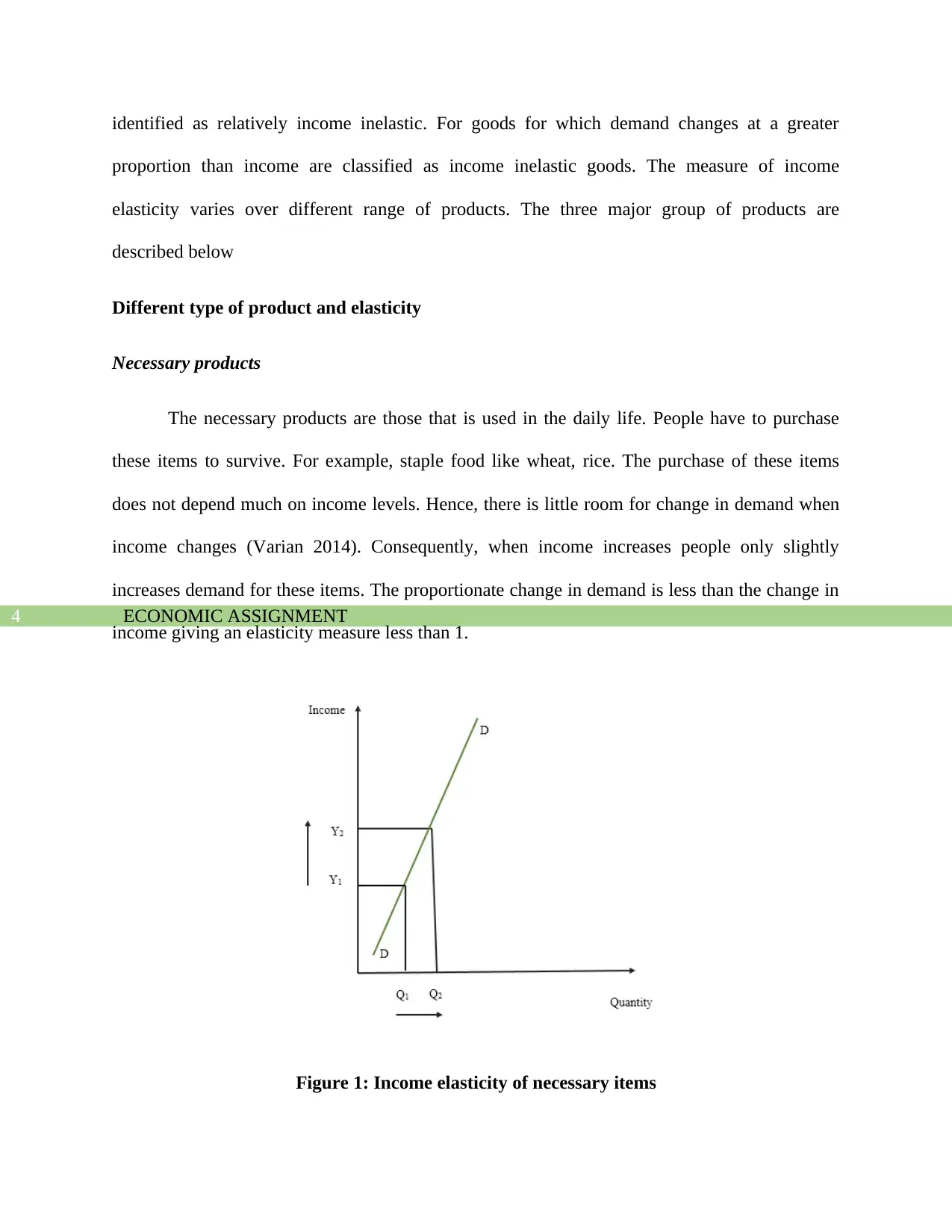

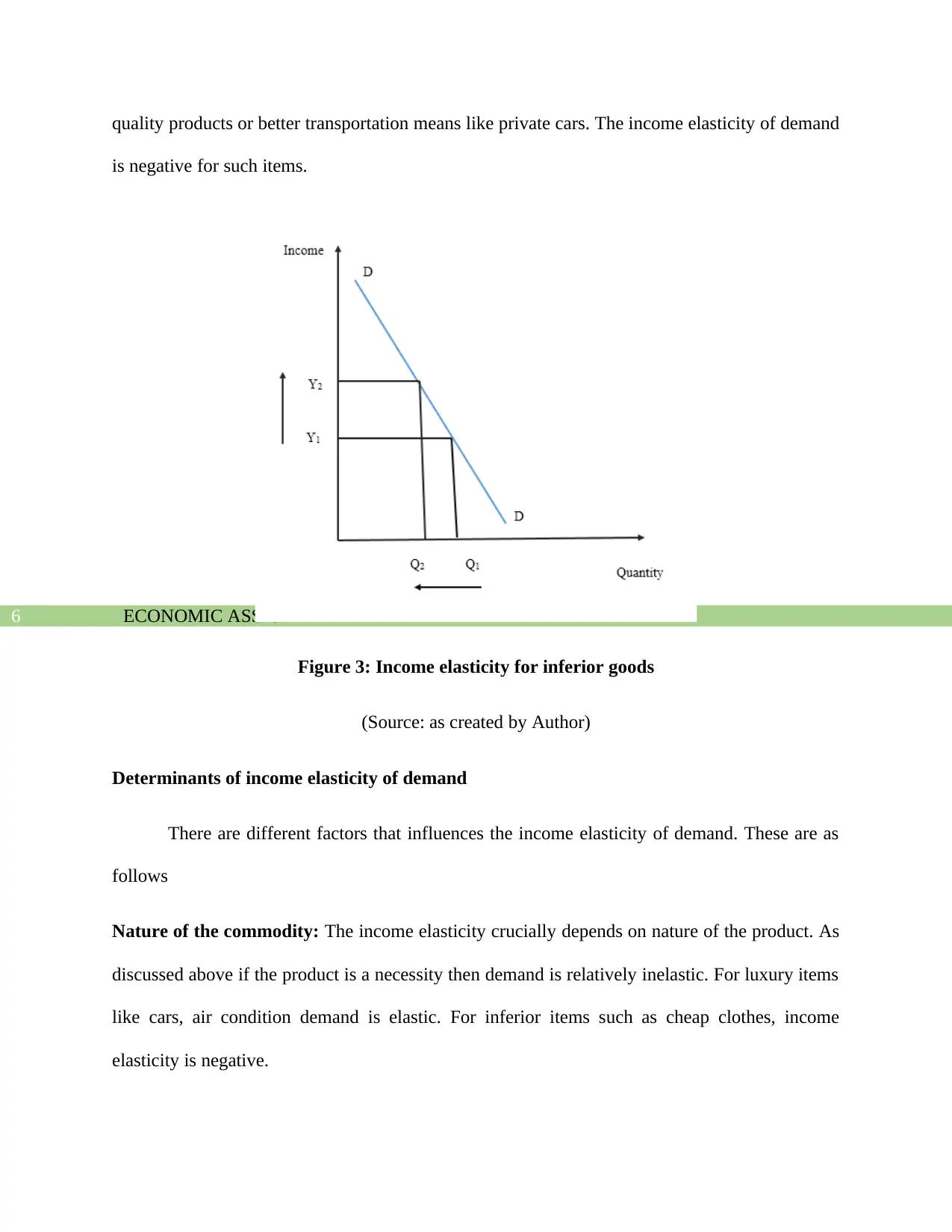

This economics assignment explores fundamental economic principles, beginning with the assumption of rationality in decision-making. It examines how individuals make optimal choices by conducting cost-benefit analyses and responding to economic incentives. The assignment then delves into the concept of income elasticity of demand, defining it as the percentage change in quantity demanded in response to a percentage change in income. It categorizes products based on their income elasticity, including necessary goods (income inelastic), luxury goods (income elastic), and inferior goods (negative income elasticity). The assignment also discusses the determinants of income elasticity, such as the nature of the commodity, time, variety of use, and distribution of wealth. These factors influence how demand changes in response to income fluctuations, providing a comprehensive overview of consumer behavior and market dynamics.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.