Economic Value Added, Surplus Utilisation & Break-Even Analysis Report

VerifiedAdded on 2024/05/31

|7

|930

|203

Report

AI Summary

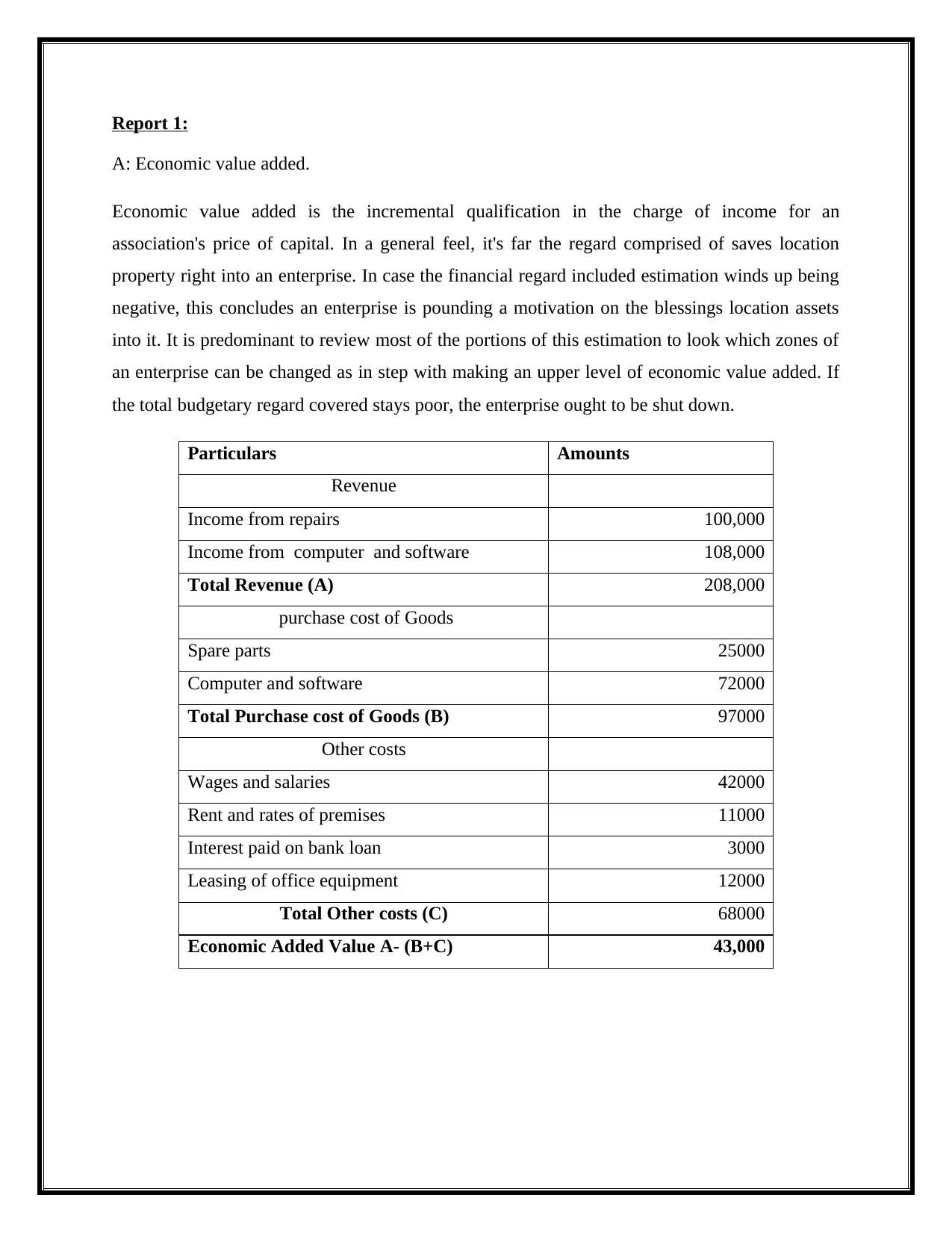

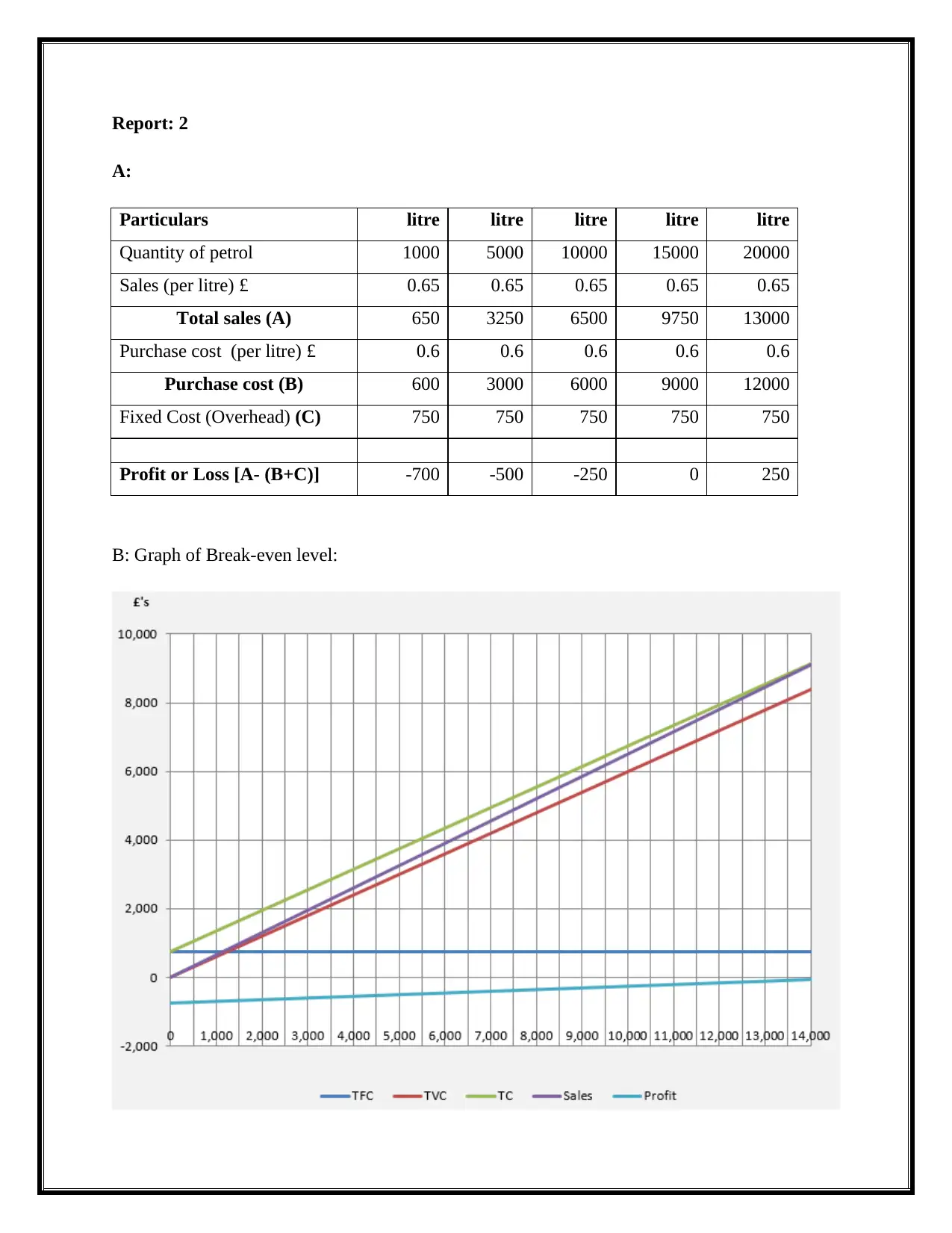

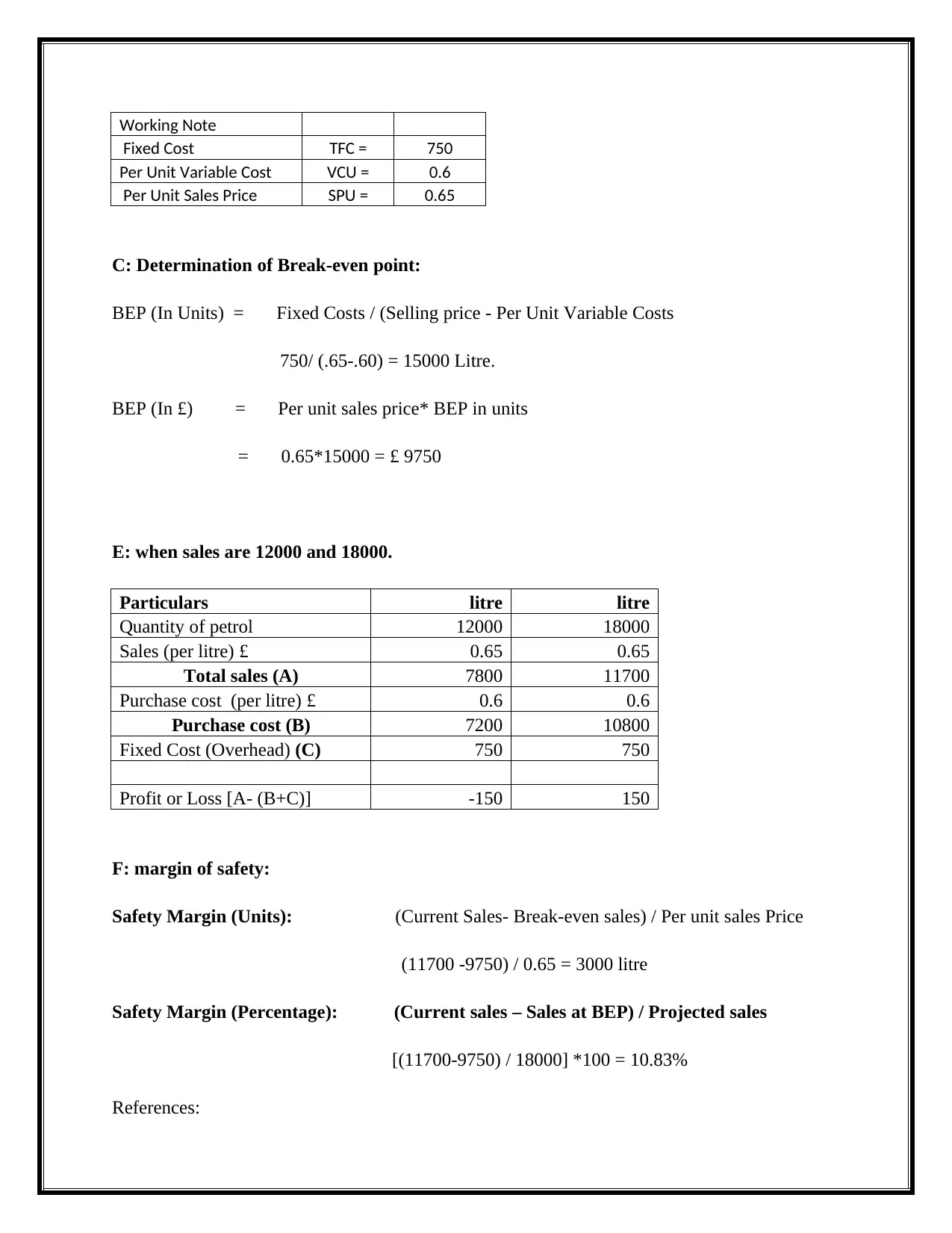

This assignment provides a comprehensive financial analysis, focusing on Economic Value Added (EVA) for CompSoft Ltd and break-even analysis for a petrol sales scenario. The EVA calculation details revenue, costs, and resulting added value, with recommendations for surplus money utilization. Percentage calculations highlight cost structures for spare parts and software sales. The break-even analysis determines the point at which total revenue equals total costs, including fixed costs, variable costs, and sales prices. The report includes calculations for break-even point in units and monetary value, profit/loss analysis at different sales volumes, and safety margin calculations. It also contains a graph illustrating the break-even level. This solved assignment is available on Desklib, along with numerous other solved assignments and study resources.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.