UGB 109 Economics Alternative Assessment 2020: Elasticity and Banks

VerifiedAdded on 2023/01/11

|11

|3157

|77

Report

AI Summary

This economics report, submitted as an alternative assessment for the UGB 109 module, delves into core economic concepts. The report addresses two key questions: the first explores three types of elasticity (price elasticity of demand, price elasticity of supply, and income elasticity of demand), providing calculations and examples to illustrate each. The second question examines how commercial banks generate money, detailing the role of deposits, reserves, and lending in the money creation process. The report aims to enhance understanding of these critical economic principles, demonstrating the relationships between economic factors and financial markets.

Project Alternative

Exam

Exam

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 1........................................................................................................................................1

1. Explain three different types of elasticity in the economy and how it should be calculated...1

Question 3........................................................................................................................................5

1. Explain that how commercial banks generate money.............................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

MAIN BODY..................................................................................................................................1

Question 1........................................................................................................................................1

1. Explain three different types of elasticity in the economy and how it should be calculated...1

Question 3........................................................................................................................................5

1. Explain that how commercial banks generate money.............................................................5

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Economic theories is the easiest and concise description of how social hierarchy the scarce

resources. It is a social science associated with products and services being generated, circulated,

and consumed. Macroeconomics is the field of sociology researching a national economy's

overall working (Ibanez And et.al., 2018). In particular, economies can be subdivided into

macroeconomics that focuses on world economy behaviour and microeconomics focuses on

individual customers and enterprises. This assessment is based on two questions which help the

students to improve their learning and knowledge. A first question is based on different type of

elasticity that is based on the change of demanded quantity over change in price. There are major

four types but this report discussed about major three such as price elasticity of demand (PES),

price elasticity of supply (PES) and at the end, income elasticity of demand (YED). In addition,

second question is based on how commercial banks generate money.

MAIN BODY

Question 1

1. Explain three different types of elasticity in the economy and how it should be calculated

Elasticity is a core economic principle and it applicable in many cases. Simple analysis of

demand and supply describes why economic factors, such as size, income and productions are

consistently related. Elasticity may provide valuable knowledge about the power of these

partnerships or their vulnerability. It refers with one sensitivity economic factor such as the

required quantity to a transition in some other variable such as price.

Economic experts use price elasticity to explain how supply or demand adjusts and

understand the complexities of the financial market, despite price changes. For example, certain

goods are rather inelastic, because their prices don't change at all with increases in supply or

demand (Liu and Yu, 2018). People want to buy fuel to get to work or fly across the world, and

even if oil prices increase, people are going to purchase exactly the same amount of petrol again.

Similarly, other commodities are very dynamic, creating significant changes in their demand or

availability due to their price fluctuations.

There are majorly four types of elasticity but this report discussed about only three type of

elasticity which helps in measuring relationship between two factors and it’s discussed below:

1

Economic theories is the easiest and concise description of how social hierarchy the scarce

resources. It is a social science associated with products and services being generated, circulated,

and consumed. Macroeconomics is the field of sociology researching a national economy's

overall working (Ibanez And et.al., 2018). In particular, economies can be subdivided into

macroeconomics that focuses on world economy behaviour and microeconomics focuses on

individual customers and enterprises. This assessment is based on two questions which help the

students to improve their learning and knowledge. A first question is based on different type of

elasticity that is based on the change of demanded quantity over change in price. There are major

four types but this report discussed about major three such as price elasticity of demand (PES),

price elasticity of supply (PES) and at the end, income elasticity of demand (YED). In addition,

second question is based on how commercial banks generate money.

MAIN BODY

Question 1

1. Explain three different types of elasticity in the economy and how it should be calculated

Elasticity is a core economic principle and it applicable in many cases. Simple analysis of

demand and supply describes why economic factors, such as size, income and productions are

consistently related. Elasticity may provide valuable knowledge about the power of these

partnerships or their vulnerability. It refers with one sensitivity economic factor such as the

required quantity to a transition in some other variable such as price.

Economic experts use price elasticity to explain how supply or demand adjusts and

understand the complexities of the financial market, despite price changes. For example, certain

goods are rather inelastic, because their prices don't change at all with increases in supply or

demand (Liu and Yu, 2018). People want to buy fuel to get to work or fly across the world, and

even if oil prices increase, people are going to purchase exactly the same amount of petrol again.

Similarly, other commodities are very dynamic, creating significant changes in their demand or

availability due to their price fluctuations.

There are majorly four types of elasticity but this report discussed about only three type of

elasticity which helps in measuring relationship between two factors and it’s discussed below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

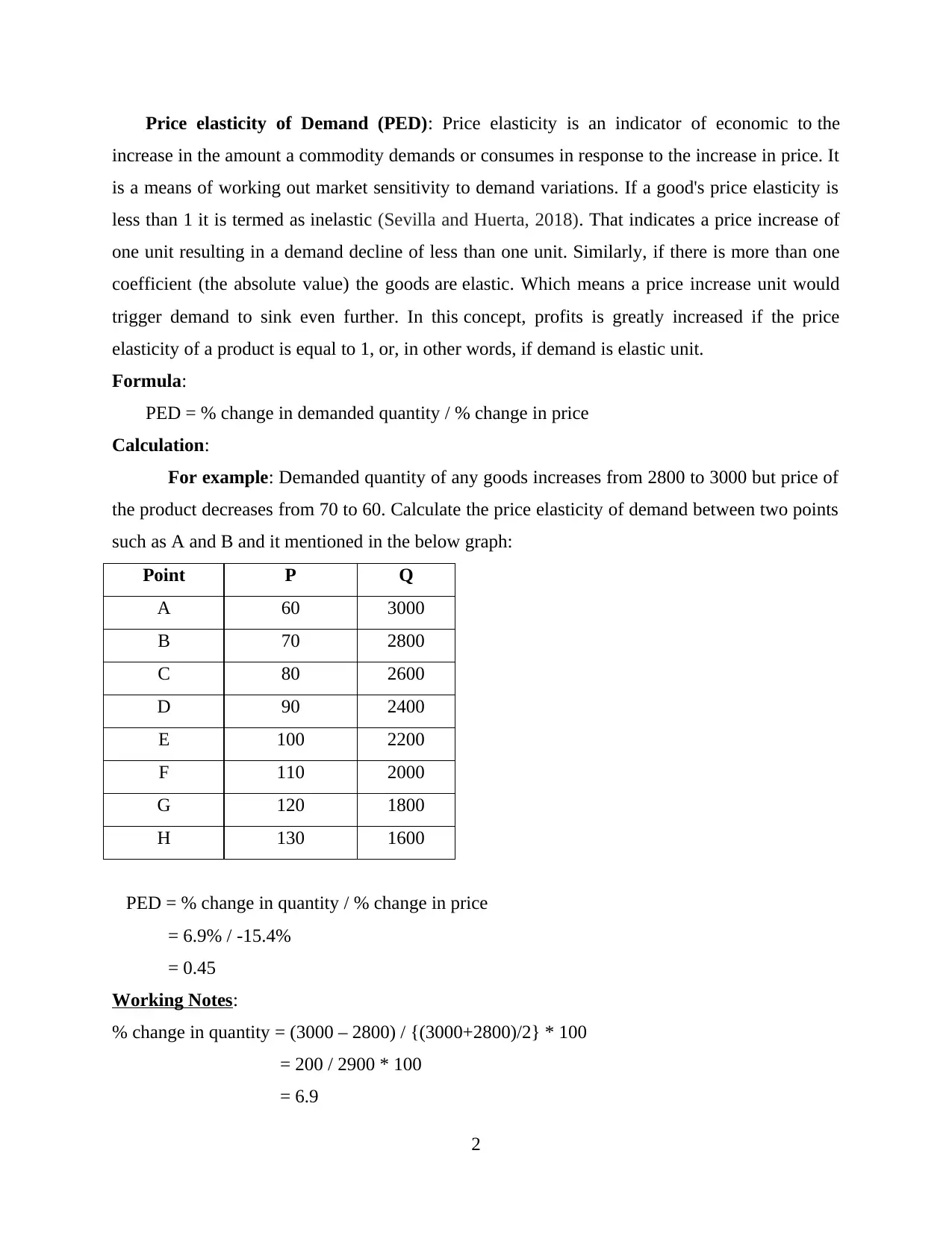

Price elasticity of Demand (PED): Price elasticity is an indicator of economic to the

increase in the amount a commodity demands or consumes in response to the increase in price. It

is a means of working out market sensitivity to demand variations. If a good's price elasticity is

less than 1 it is termed as inelastic (Sevilla and Huerta, 2018). That indicates a price increase of

one unit resulting in a demand decline of less than one unit. Similarly, if there is more than one

coefficient (the absolute value) the goods are elastic. Which means a price increase unit would

trigger demand to sink even further. In this concept, profits is greatly increased if the price

elasticity of a product is equal to 1, or, in other words, if demand is elastic unit.

Formula:

PED = % change in demanded quantity / % change in price

Calculation:

For example: Demanded quantity of any goods increases from 2800 to 3000 but price of

the product decreases from 70 to 60. Calculate the price elasticity of demand between two points

such as A and B and it mentioned in the below graph:

Point P Q

A 60 3000

B 70 2800

C 80 2600

D 90 2400

E 100 2200

F 110 2000

G 120 1800

H 130 1600

PED = % change in quantity / % change in price

= 6.9% / -15.4%

= 0.45

Working Notes:

% change in quantity = (3000 – 2800) / {(3000+2800)/2} * 100

= 200 / 2900 * 100

= 6.9

2

increase in the amount a commodity demands or consumes in response to the increase in price. It

is a means of working out market sensitivity to demand variations. If a good's price elasticity is

less than 1 it is termed as inelastic (Sevilla and Huerta, 2018). That indicates a price increase of

one unit resulting in a demand decline of less than one unit. Similarly, if there is more than one

coefficient (the absolute value) the goods are elastic. Which means a price increase unit would

trigger demand to sink even further. In this concept, profits is greatly increased if the price

elasticity of a product is equal to 1, or, in other words, if demand is elastic unit.

Formula:

PED = % change in demanded quantity / % change in price

Calculation:

For example: Demanded quantity of any goods increases from 2800 to 3000 but price of

the product decreases from 70 to 60. Calculate the price elasticity of demand between two points

such as A and B and it mentioned in the below graph:

Point P Q

A 60 3000

B 70 2800

C 80 2600

D 90 2400

E 100 2200

F 110 2000

G 120 1800

H 130 1600

PED = % change in quantity / % change in price

= 6.9% / -15.4%

= 0.45

Working Notes:

% change in quantity = (3000 – 2800) / {(3000+2800)/2} * 100

= 200 / 2900 * 100

= 6.9

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

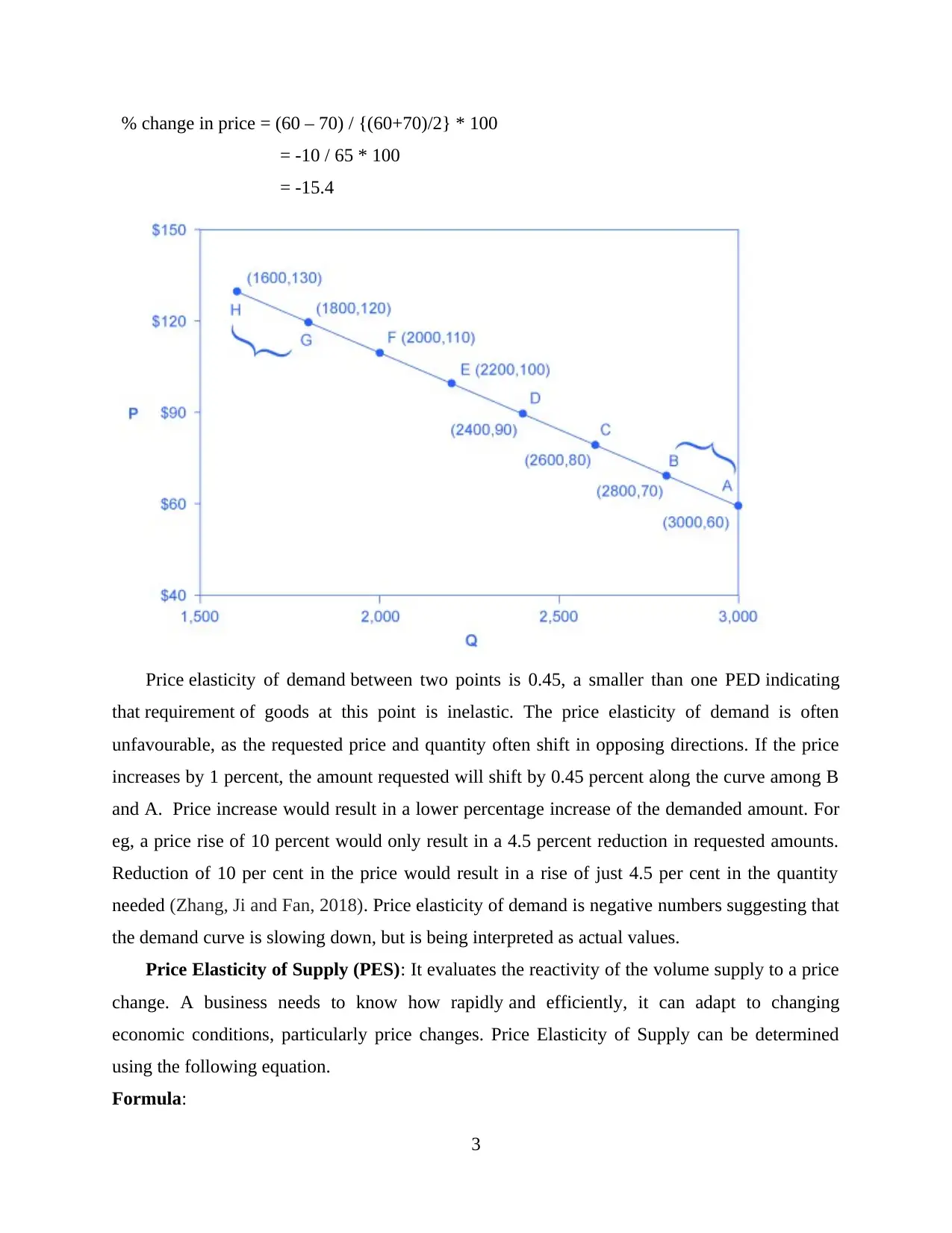

% change in price = (60 – 70) / {(60+70)/2} * 100

= -10 / 65 * 100

= -15.4

Price elasticity of demand between two points is 0.45, a smaller than one PED indicating

that requirement of goods at this point is inelastic. The price elasticity of demand is often

unfavourable, as the requested price and quantity often shift in opposing directions. If the price

increases by 1 percent, the amount requested will shift by 0.45 percent along the curve among B

and A. Price increase would result in a lower percentage increase of the demanded amount. For

eg, a price rise of 10 percent would only result in a 4.5 percent reduction in requested amounts.

Reduction of 10 per cent in the price would result in a rise of just 4.5 per cent in the quantity

needed (Zhang, Ji and Fan, 2018). Price elasticity of demand is negative numbers suggesting that

the demand curve is slowing down, but is being interpreted as actual values.

Price Elasticity of Supply (PES): It evaluates the reactivity of the volume supply to a price

change. A business needs to know how rapidly and efficiently, it can adapt to changing

economic conditions, particularly price changes. Price Elasticity of Supply can be determined

using the following equation.

Formula:

3

= -10 / 65 * 100

= -15.4

Price elasticity of demand between two points is 0.45, a smaller than one PED indicating

that requirement of goods at this point is inelastic. The price elasticity of demand is often

unfavourable, as the requested price and quantity often shift in opposing directions. If the price

increases by 1 percent, the amount requested will shift by 0.45 percent along the curve among B

and A. Price increase would result in a lower percentage increase of the demanded amount. For

eg, a price rise of 10 percent would only result in a 4.5 percent reduction in requested amounts.

Reduction of 10 per cent in the price would result in a rise of just 4.5 per cent in the quantity

needed (Zhang, Ji and Fan, 2018). Price elasticity of demand is negative numbers suggesting that

the demand curve is slowing down, but is being interpreted as actual values.

Price Elasticity of Supply (PES): It evaluates the reactivity of the volume supply to a price

change. A business needs to know how rapidly and efficiently, it can adapt to changing

economic conditions, particularly price changes. Price Elasticity of Supply can be determined

using the following equation.

Formula:

3

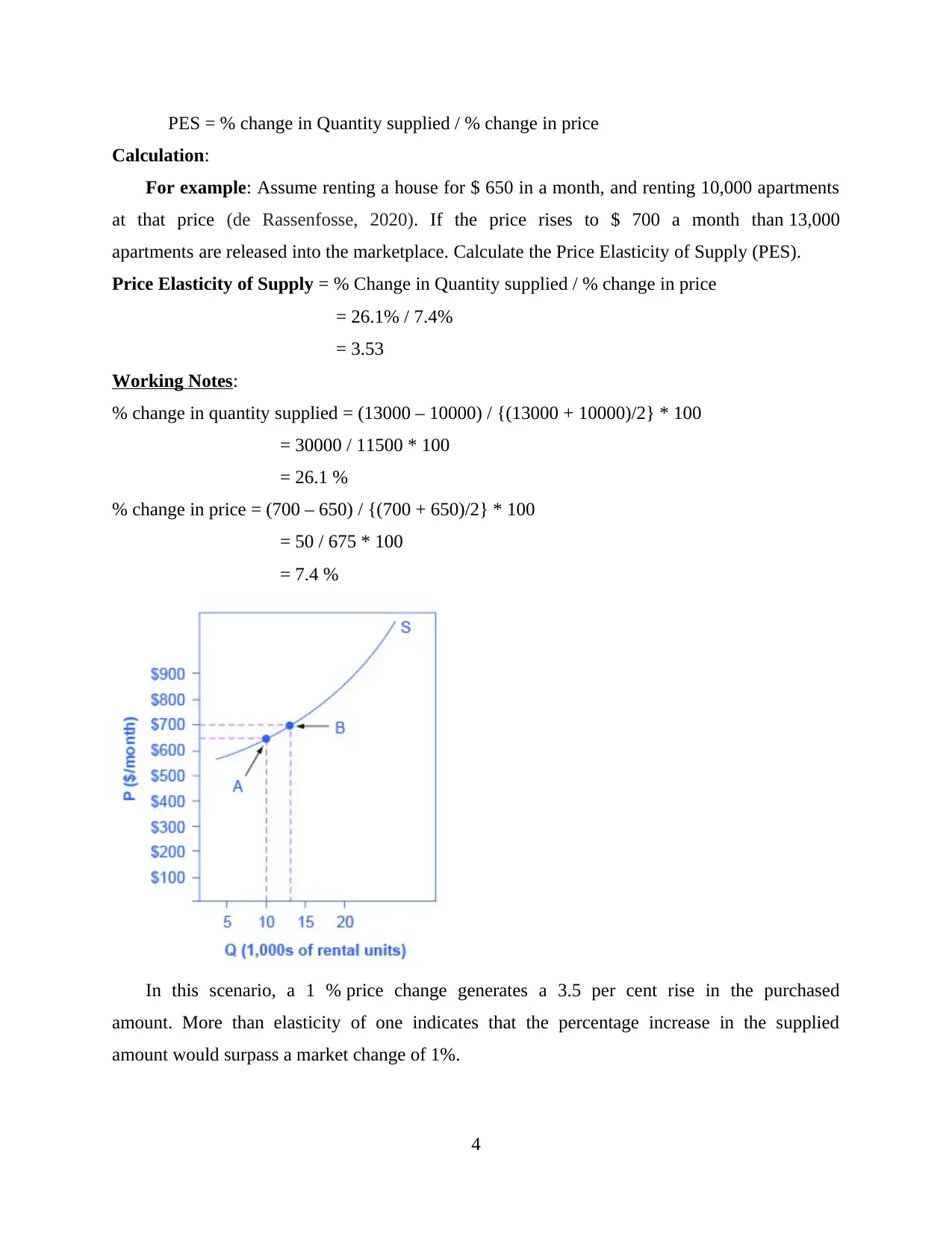

PES = % change in Quantity supplied / % change in price

Calculation:

For example: Assume renting a house for $ 650 in a month, and renting 10,000 apartments

at that price (de Rassenfosse, 2020). If the price rises to $ 700 a month than 13,000

apartments are released into the marketplace. Calculate the Price Elasticity of Supply (PES).

Price Elasticity of Supply = % Change in Quantity supplied / % change in price

= 26.1% / 7.4%

= 3.53

Working Notes:

% change in quantity supplied = (13000 – 10000) / {(13000 + 10000)/2} * 100

= 30000 / 11500 * 100

= 26.1 %

% change in price = (700 – 650) / {(700 + 650)/2} * 100

= 50 / 675 * 100

= 7.4 %

In this scenario, a 1 % price change generates a 3.5 per cent rise in the purchased

amount. More than elasticity of one indicates that the percentage increase in the supplied

amount would surpass a market change of 1%.

4

Calculation:

For example: Assume renting a house for $ 650 in a month, and renting 10,000 apartments

at that price (de Rassenfosse, 2020). If the price rises to $ 700 a month than 13,000

apartments are released into the marketplace. Calculate the Price Elasticity of Supply (PES).

Price Elasticity of Supply = % Change in Quantity supplied / % change in price

= 26.1% / 7.4%

= 3.53

Working Notes:

% change in quantity supplied = (13000 – 10000) / {(13000 + 10000)/2} * 100

= 30000 / 11500 * 100

= 26.1 %

% change in price = (700 – 650) / {(700 + 650)/2} * 100

= 50 / 675 * 100

= 7.4 %

In this scenario, a 1 % price change generates a 3.5 per cent rise in the purchased

amount. More than elasticity of one indicates that the percentage increase in the supplied

amount would surpass a market change of 1%.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Income Elasticity of Demand (YED): It is refers to the responsiveness of the quantity

required for a certain product to a adjustment in the actual income of people who purchased this

commodity while keeping all other items stable (Ghoddusi, Rafizadeh and Rahmati, 2018). The

method is estimating the total increase in demand quantity divided by the increase in sales rate.

Through demand elasticity in wages, they can say whether a particular product represents a need

or a privilege.

Formula:

YED = % Change in quantity demanded / % Change in Income

Calculation:

For example: Imagine a regional car dealer that collects statistics over a given year on shifts

in market and customer profits over their vehicles. When its consumers' annual real income

declines from £ 50,000 to £ 40,000, demand for their vehicles plunge from 10,000 to 5,000 sales

volumes, all other aspects unchanged.

YED = 66.6% / 22.2%

= 3

Working Notes:

% Change in income = (50000 – 10000) / {(50000 + 10000) / 2} * 100

= (10000 / 45000) * 100

= 22.2 %

% Change in demanded quantity = (10000 – 5000) / {(10000 + 5000) / 2} * 100

= (5000 / 7500) * 100

= 66.6 %

From the above calculation it is observed that, income elasticity of product is 3 which

indicate that local consumers are especially biased when it comes to buying cars for shifts in

their profits.

Question 3

1. Explain that how commercial banks generate money

Banks are commercial businesses that make profit, much as department shops and groceries.

Some banks, with only a few branches, are very small and they do trade in a restricted area

(Jordan, 2018). Others were one of the largest companies, with dozens of branches scattered

5

required for a certain product to a adjustment in the actual income of people who purchased this

commodity while keeping all other items stable (Ghoddusi, Rafizadeh and Rahmati, 2018). The

method is estimating the total increase in demand quantity divided by the increase in sales rate.

Through demand elasticity in wages, they can say whether a particular product represents a need

or a privilege.

Formula:

YED = % Change in quantity demanded / % Change in Income

Calculation:

For example: Imagine a regional car dealer that collects statistics over a given year on shifts

in market and customer profits over their vehicles. When its consumers' annual real income

declines from £ 50,000 to £ 40,000, demand for their vehicles plunge from 10,000 to 5,000 sales

volumes, all other aspects unchanged.

YED = 66.6% / 22.2%

= 3

Working Notes:

% Change in income = (50000 – 10000) / {(50000 + 10000) / 2} * 100

= (10000 / 45000) * 100

= 22.2 %

% Change in demanded quantity = (10000 – 5000) / {(10000 + 5000) / 2} * 100

= (5000 / 7500) * 100

= 66.6 %

From the above calculation it is observed that, income elasticity of product is 3 which

indicate that local consumers are especially biased when it comes to buying cars for shifts in

their profits.

Question 3

1. Explain that how commercial banks generate money

Banks are commercial businesses that make profit, much as department shops and groceries.

Some banks, with only a few branches, are very small and they do trade in a restricted area

(Jordan, 2018). Others were one of the largest companies, with dozens of branches scattered

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

through many nations. The key role Banks perform in the economy is to create money is

accepting deposits and lending money. By doing so they are making income.

Commercial banks in many other countries are legally obliged to keep approximately 10

% of the bank deposits as reserves above the threshold (How Commercial Banks Create Money,

2019). Such reserves are referred to as Required Reserves (RR). Indeed, banks must also carry at

least the funds rate needed to protect against the risk that multiple depositors will make

transactions from bank accounts collectively. Yet in fact, people and companies typically keep

steady the amount of funds they carry compared to the volume of checking account balances. So,

they would expect the people to really see their scanning accounts which boost the amount of

currency which they hold as balances.

Deposits are lenders' obligations as they are owing to people and companies who have

invested the money (Teresienė, 2018) (Siciliani, 2018). For examples, if they deposited 1000 to

bank account, the banks owe those 1000, and person can order it back any time. In addition,

banks do not earn interest on the "reserve requirement." for all of these reasons; banks need to

use all of their bank deposits (90%) to create money.

Banks will loan out a lot more than just the cash and assets they keep. If financial

institutions make loans, the bank account flow increase, and the supply of money extends. It will

be done by the accounting they use in making loans; commercial banks can generate new

income. Although this is always difficult to imagine at first, the staff who run the financial

industry are common aware of this. In March 2014, the Bank of England published a study

entitled "Money Production in the Global Economy," saying: Financial (i.e., high-street) banks

generate money by issuing new loans throughout the context of bank deposits.

For example, when a bank gives a loan to anyone who takes out a mortgage to purchase a

home, it usually is not doing that by sending them thousands of pounds of currency notes.

Instead, it funds their savings account with a mortgage-sized bank deposit. Fresh capital is being

generated at the moment. "In other words, financial institutions generate new capital as they lend

or generate credit, either by issuing loans or by purchasing existing properties. When making

credit, banks make deposits in our bank accounts at the same time, which is capital of all

intensive purposes (Kumhof and Wang, 2018). The opposite side of this capital development

would be the new debt arises with a new mortgage which not borrowing from either the savings

of anyone else, but capital that was generated by banks out of nowhere. The debt load will

6

accepting deposits and lending money. By doing so they are making income.

Commercial banks in many other countries are legally obliged to keep approximately 10

% of the bank deposits as reserves above the threshold (How Commercial Banks Create Money,

2019). Such reserves are referred to as Required Reserves (RR). Indeed, banks must also carry at

least the funds rate needed to protect against the risk that multiple depositors will make

transactions from bank accounts collectively. Yet in fact, people and companies typically keep

steady the amount of funds they carry compared to the volume of checking account balances. So,

they would expect the people to really see their scanning accounts which boost the amount of

currency which they hold as balances.

Deposits are lenders' obligations as they are owing to people and companies who have

invested the money (Teresienė, 2018) (Siciliani, 2018). For examples, if they deposited 1000 to

bank account, the banks owe those 1000, and person can order it back any time. In addition,

banks do not earn interest on the "reserve requirement." for all of these reasons; banks need to

use all of their bank deposits (90%) to create money.

Banks will loan out a lot more than just the cash and assets they keep. If financial

institutions make loans, the bank account flow increase, and the supply of money extends. It will

be done by the accounting they use in making loans; commercial banks can generate new

income. Although this is always difficult to imagine at first, the staff who run the financial

industry are common aware of this. In March 2014, the Bank of England published a study

entitled "Money Production in the Global Economy," saying: Financial (i.e., high-street) banks

generate money by issuing new loans throughout the context of bank deposits.

For example, when a bank gives a loan to anyone who takes out a mortgage to purchase a

home, it usually is not doing that by sending them thousands of pounds of currency notes.

Instead, it funds their savings account with a mortgage-sized bank deposit. Fresh capital is being

generated at the moment. "In other words, financial institutions generate new capital as they lend

or generate credit, either by issuing loans or by purchasing existing properties. When making

credit, banks make deposits in our bank accounts at the same time, which is capital of all

intensive purposes (Kumhof and Wang, 2018). The opposite side of this capital development

would be the new debt arises with a new mortgage which not borrowing from either the savings

of anyone else, but capital that was generated by banks out of nowhere. The debt load will

6

inevitably become really high, culminating in the surge of bankruptcy that causes a financial

crash, like in the situation of the US residential financial crisis in 2008. The biggest determinant

about how much bank can lend because they trusted that loan can be returned and the trust

against the loan sum in the value of the loan assets and the collateral.

Firstly, banks make money from by offering loans and collecting interest income. It

includes the services such as consumers deposit funds, checking, savings accounts, certificates of

deposit and investment certificates (Njogu, Olweny and Njeru, 2018). They receive interest from

lenders on such deposits. The rate of interest earned by the institutions on money which they (the

banks) borrowed, however, is lower than the rate imposed on money they borrow. Commercial

banks can borrow the money from bigger banks to finance loans at a favoured interest rate. That

is how they get profit out of the loan themselves. For example, suppose a consumer buys a six-

year Certificate of Deposits from a commercial bank at an annual return of 3 per cent for

100,000. Another borrower gets a six-year auto loan from the same bank for 100,000 at an

average interest rate of 7 percent on the same day. The bank will charge the CD customer

Rs.18000 over six years, assuming simple interest, while it collects 42,000 from the auto loan

client. The difference of 24,000 is an indication of expansion or net interest income and it

reflects bank profit.

Secondly, commercial banks are making money out of residential mortgages. For example,

once customers buy a home by getting a loan from a mortgage, the bank will start paying them

multiple costs, such as a loan servicing fee, payment fee, reinsurance fee, transaction fee, etc. In

fact, the bank will receive interest rates on a 30 year, fixed-rate loan for the very first 10 or 20

years. The cumulative interest payment owed on a 30 year, fixed-rate loan may surpass the

initial monthly payment taken. Interest is the income of a bank receives to lend customers the

money to purchase a mortgage.

Thirdly, banks make money through credit card money. Of course not all banks lend credit

cards, and those who do make lots of money. For example, several credit card servicers can

charge their customers annual fees (Bogati and Vongurai, 2018). This amounts of probably vary

and wildly based on the card. For premium plastic some commercial banks charging thousands

of pounds. Penalty charges refer to overdraft charges and late payments of credit cards provided

by banks. These charges can add up to much of the average yearly profit for financial institutions

issuing credit cards.

7

crash, like in the situation of the US residential financial crisis in 2008. The biggest determinant

about how much bank can lend because they trusted that loan can be returned and the trust

against the loan sum in the value of the loan assets and the collateral.

Firstly, banks make money from by offering loans and collecting interest income. It

includes the services such as consumers deposit funds, checking, savings accounts, certificates of

deposit and investment certificates (Njogu, Olweny and Njeru, 2018). They receive interest from

lenders on such deposits. The rate of interest earned by the institutions on money which they (the

banks) borrowed, however, is lower than the rate imposed on money they borrow. Commercial

banks can borrow the money from bigger banks to finance loans at a favoured interest rate. That

is how they get profit out of the loan themselves. For example, suppose a consumer buys a six-

year Certificate of Deposits from a commercial bank at an annual return of 3 per cent for

100,000. Another borrower gets a six-year auto loan from the same bank for 100,000 at an

average interest rate of 7 percent on the same day. The bank will charge the CD customer

Rs.18000 over six years, assuming simple interest, while it collects 42,000 from the auto loan

client. The difference of 24,000 is an indication of expansion or net interest income and it

reflects bank profit.

Secondly, commercial banks are making money out of residential mortgages. For example,

once customers buy a home by getting a loan from a mortgage, the bank will start paying them

multiple costs, such as a loan servicing fee, payment fee, reinsurance fee, transaction fee, etc. In

fact, the bank will receive interest rates on a 30 year, fixed-rate loan for the very first 10 or 20

years. The cumulative interest payment owed on a 30 year, fixed-rate loan may surpass the

initial monthly payment taken. Interest is the income of a bank receives to lend customers the

money to purchase a mortgage.

Thirdly, banks make money through credit card money. Of course not all banks lend credit

cards, and those who do make lots of money. For example, several credit card servicers can

charge their customers annual fees (Bogati and Vongurai, 2018). This amounts of probably vary

and wildly based on the card. For premium plastic some commercial banks charging thousands

of pounds. Penalty charges refer to overdraft charges and late payments of credit cards provided

by banks. These charges can add up to much of the average yearly profit for financial institutions

issuing credit cards.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Overall discussion help in evaluating that, banks generate money through accepting

customer’s deposits, lending mortgage loan, several investment functions etc. These are the main

source of earning of commercial banks.

CONCLUSION

From the above discussion it has been observed that in the economy there are various factors

which required evaluating in order to understand the elasticity of demand and supply. Multiple

type of elasticity indicates the different perspective. Such as price elasticity of demand indicate

that how elastic is demand for particular product and it is similar to the price elasticity of supply

as well. On the other side, in context of financial institutions such as commercial banks, the

biggest source of income for banks is lending mortgage loan where they charge interest rate as

per the amount demanded by consumers. Customer deposits and credit card facilities also helps

in creating revenue for commercial banks.

8

customer’s deposits, lending mortgage loan, several investment functions etc. These are the main

source of earning of commercial banks.

CONCLUSION

From the above discussion it has been observed that in the economy there are various factors

which required evaluating in order to understand the elasticity of demand and supply. Multiple

type of elasticity indicates the different perspective. Such as price elasticity of demand indicate

that how elastic is demand for particular product and it is similar to the price elasticity of supply

as well. On the other side, in context of financial institutions such as commercial banks, the

biggest source of income for banks is lending mortgage loan where they charge interest rate as

per the amount demanded by consumers. Customer deposits and credit card facilities also helps

in creating revenue for commercial banks.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books & Journals

Ibanez, R. And et.al., 2018. A manifold learning approach to data-driven computational elasticity

and inelasticity. Archives of Computational Methods in Engineering. 25(1). pp.47-57.

Sevilla, R., Giacomini, M., Karkoulias, A. and Huerta, A., 2018. A superconvergent hybridisable

discontinuous Galerkin method for linear elasticity. International Journal for Numerical

Methods in Engineering. 116(2). pp.91-116.

Zhang, Y., Ji, Q. and Fan, Y., 2018. The price and income elasticity of China's natural gas

demand: A multi-sectoral perspective. Energy Policy. 113. pp.332-341.

de Rassenfosse, G., 2020. On the price elasticity of demand for trademarks. Industry and

Innovation. 27(1-2), pp.11-24.

Ghoddusi, H., Rafizadeh, N. and Rahmati, M. H., 2018. Price elasticity of gasoline smuggling: A

semi-structural estimation approach. Energy Economics. 71. pp.171-185.

Kumhof, M. and Wang, X., 2018. Banks, Money and the Zero Lower Bound. Saïd Business

School WP, 16.

Jordan, T. J., 2018. How money is created by the central bank and the banking system. Zurich:

Swiss National Bank, 16.

Teresienė, D., 2018. Performance measurement issues in central banks.

Siciliani, P., 2018. Competition for retail deposits between commercial banks and non-bank

operators: a two-sided platform analysis.

Njogu, G. K., Olweny, T. and Njeru, A., 2018. Relationship between farm production capacity

and agricultural credit access from commercial banks.

Bogati, D. and Vongurai, R., 2018. Determinants Of Customer Satisfaction And Customer

Loyalty In E-Banking: A Case Study of Thailand’s Selected Commercial Banks in

Bangkok’s Central Business Area. International Research E-Journal on Business and

Economics. 2(2). p.32.

Liu, Q. and Yu, Z., 2018, October. The elasticity and plasticity in semi-containerized co-locating

cloud workload: A view from Alibaba trace. In Proceedings of the ACM Symposium on

Cloud Computing (pp. 347-360).

Online

How Commercial Banks Create Money. 2019. [Online]. Available Through:

<https://morungexpress.com/how-do-commercial-banks-create-money>

9

Books & Journals

Ibanez, R. And et.al., 2018. A manifold learning approach to data-driven computational elasticity

and inelasticity. Archives of Computational Methods in Engineering. 25(1). pp.47-57.

Sevilla, R., Giacomini, M., Karkoulias, A. and Huerta, A., 2018. A superconvergent hybridisable

discontinuous Galerkin method for linear elasticity. International Journal for Numerical

Methods in Engineering. 116(2). pp.91-116.

Zhang, Y., Ji, Q. and Fan, Y., 2018. The price and income elasticity of China's natural gas

demand: A multi-sectoral perspective. Energy Policy. 113. pp.332-341.

de Rassenfosse, G., 2020. On the price elasticity of demand for trademarks. Industry and

Innovation. 27(1-2), pp.11-24.

Ghoddusi, H., Rafizadeh, N. and Rahmati, M. H., 2018. Price elasticity of gasoline smuggling: A

semi-structural estimation approach. Energy Economics. 71. pp.171-185.

Kumhof, M. and Wang, X., 2018. Banks, Money and the Zero Lower Bound. Saïd Business

School WP, 16.

Jordan, T. J., 2018. How money is created by the central bank and the banking system. Zurich:

Swiss National Bank, 16.

Teresienė, D., 2018. Performance measurement issues in central banks.

Siciliani, P., 2018. Competition for retail deposits between commercial banks and non-bank

operators: a two-sided platform analysis.

Njogu, G. K., Olweny, T. and Njeru, A., 2018. Relationship between farm production capacity

and agricultural credit access from commercial banks.

Bogati, D. and Vongurai, R., 2018. Determinants Of Customer Satisfaction And Customer

Loyalty In E-Banking: A Case Study of Thailand’s Selected Commercial Banks in

Bangkok’s Central Business Area. International Research E-Journal on Business and

Economics. 2(2). p.32.

Liu, Q. and Yu, Z., 2018, October. The elasticity and plasticity in semi-containerized co-locating

cloud workload: A view from Alibaba trace. In Proceedings of the ACM Symposium on

Cloud Computing (pp. 347-360).

Online

How Commercial Banks Create Money. 2019. [Online]. Available Through:

<https://morungexpress.com/how-do-commercial-banks-create-money>

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.