Managerial Economics Assignment: Elasticity, Costs, and Equilibrium

VerifiedAdded on 2023/01/12

|14

|3439

|60

Homework Assignment

AI Summary

This document presents a comprehensive solution to a Managerial Economics assignment. It begins with an introduction to demand elasticity, defining various types including price, income, cross, and advertising elasticity, along with their respective formulas. The assignment then addresses specific economic scenarios, such as the impact of perfectly inelastic demand and changes in supply on equilibrium prices. It explores the determinants of supply, including climatic conditions, technology, and transportation, and how these factors affect the market. The solution further delves into cost analysis, differentiating between fixed, variable, total, marginal, and average costs, with a graphical representation of cost curves. The assignment includes elasticity calculations for specific examples, and examines how market equilibrium is affected by external factors such as environmental regulations, foreign competition, and changes in consumer preferences. The document is a valuable resource for students studying managerial economics, offering detailed explanations and practical applications of economic principles.

MANAGERIAL

ECONOMICS

ECONOMICS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................1

Introduction.................................................................................................................................1

Different types of demand elasticity...........................................................................................1

QUESTION 2...................................................................................................................................2

QUESTION 3...................................................................................................................................3

QUESTION 4...................................................................................................................................4

QUESTION 5...................................................................................................................................5

QUESTION 6...................................................................................................................................7

QUESTION 7...................................................................................................................................8

(a)................................................................................................................................................8

(B)...............................................................................................................................................9

REFERENCES..............................................................................................................................11

.......................................................................................................................................................11

QUESTION 1...................................................................................................................................1

Introduction.................................................................................................................................1

Different types of demand elasticity...........................................................................................1

QUESTION 2...................................................................................................................................2

QUESTION 3...................................................................................................................................3

QUESTION 4...................................................................................................................................4

QUESTION 5...................................................................................................................................5

QUESTION 6...................................................................................................................................7

QUESTION 7...................................................................................................................................8

(a)................................................................................................................................................8

(B)...............................................................................................................................................9

REFERENCES..............................................................................................................................11

.......................................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

Introduction

Demand of a commodity is sensitive towards the economic variables. This sensitivity and

responsiveness is calculated by elasticity. Elasticity of demand measures the change in price of a

commodity and quantity demanded of that commodity. There are various types of demand

elasticity which is associated to the economic variables of price, income and advertisement.

Different types of demand elasticity

Price elasticity of demand – In this type of elasticity, demand sensitivity against price of a

product is measured. This elasticity is measured by comparing the proportionate change in

quantity demand and price (Černohous, 2017). There total of five price elasticity of demand

which are perfectly elastic, perfectly inelastic, relatively elastic, relatively inelastic, unitary

elastic demand. The formula of calculating price elasticity is:

Ep = proportionate change in quantity demanded / proportionate change in price

Or, Ep = ΔQ / ΔP * P / Q

Income elasticity of demand – Under this situation, the effect of income change of consumer

is measured on the quantity demanded of a commodity. This elasticity represents the degree of

responsiveness of a demand over change in consumer’s income. This elasticity can be calculated

using below formula:

Ey = Percentage change in demanded quantity / percentage change in consumer’s income

Cross elasticity of demand – This concept refers to the change in quantity demanded of a

product due to the change in price of another product. This situation is result of inter related

goods which are either consumed together or have a substitutional relationship. The cross

elasticity of demand can be calculated using the following formula:

Ec = proportionate change in quantity demanded of product X / proportionate change in

price of product Y.

In order to apply this situation, it is important for the two products to be complementary or

substitutional so that one product can affect other product.

Advertising elasticity of demand – This elasticity refers to the change in quantity demanded

of a product due to the advertisement of that product. This responsiveness can be calculated

1

Introduction

Demand of a commodity is sensitive towards the economic variables. This sensitivity and

responsiveness is calculated by elasticity. Elasticity of demand measures the change in price of a

commodity and quantity demanded of that commodity. There are various types of demand

elasticity which is associated to the economic variables of price, income and advertisement.

Different types of demand elasticity

Price elasticity of demand – In this type of elasticity, demand sensitivity against price of a

product is measured. This elasticity is measured by comparing the proportionate change in

quantity demand and price (Černohous, 2017). There total of five price elasticity of demand

which are perfectly elastic, perfectly inelastic, relatively elastic, relatively inelastic, unitary

elastic demand. The formula of calculating price elasticity is:

Ep = proportionate change in quantity demanded / proportionate change in price

Or, Ep = ΔQ / ΔP * P / Q

Income elasticity of demand – Under this situation, the effect of income change of consumer

is measured on the quantity demanded of a commodity. This elasticity represents the degree of

responsiveness of a demand over change in consumer’s income. This elasticity can be calculated

using below formula:

Ey = Percentage change in demanded quantity / percentage change in consumer’s income

Cross elasticity of demand – This concept refers to the change in quantity demanded of a

product due to the change in price of another product. This situation is result of inter related

goods which are either consumed together or have a substitutional relationship. The cross

elasticity of demand can be calculated using the following formula:

Ec = proportionate change in quantity demanded of product X / proportionate change in

price of product Y.

In order to apply this situation, it is important for the two products to be complementary or

substitutional so that one product can affect other product.

Advertising elasticity of demand – This elasticity refers to the change in quantity demanded

of a product due to the advertisement of that product. This responsiveness can be calculated

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

using change in demand of a commodity and change in promotional expenses of that commodity.

Formula of this elasticity is:

Ea = Proportional change in quantity demanded of a product / proportional change in

advertisement expenses of that product

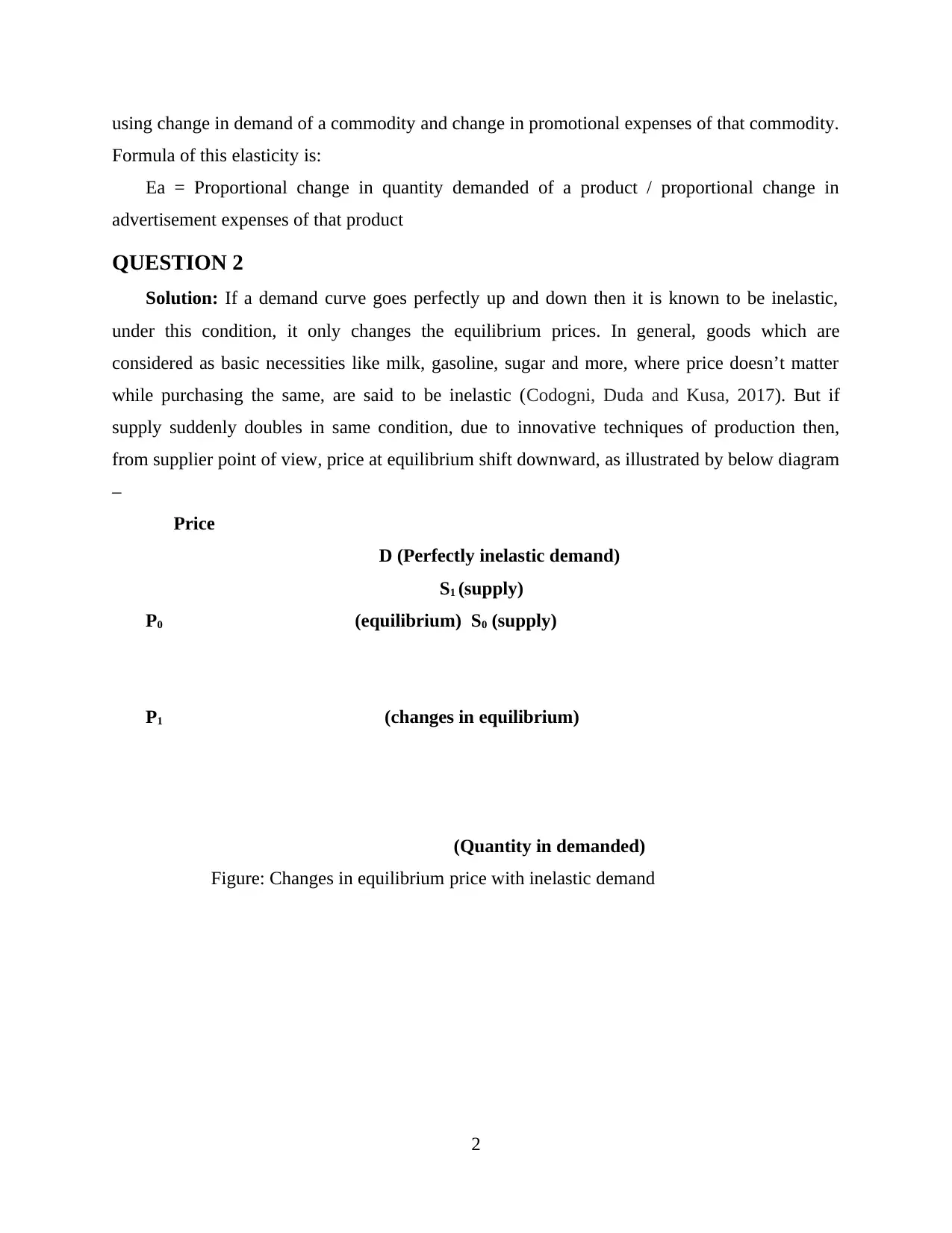

QUESTION 2

Solution: If a demand curve goes perfectly up and down then it is known to be inelastic,

under this condition, it only changes the equilibrium prices. In general, goods which are

considered as basic necessities like milk, gasoline, sugar and more, where price doesn’t matter

while purchasing the same, are said to be inelastic (Codogni, Duda and Kusa, 2017). But if

supply suddenly doubles in same condition, due to innovative techniques of production then,

from supplier point of view, price at equilibrium shift downward, as illustrated by below diagram

–

Price

D (Perfectly inelastic demand)

S1 (supply)

P0 (equilibrium) S0 (supply)

P1 (changes in equilibrium)

(Quantity in demanded)

Figure: Changes in equilibrium price with inelastic demand

2

Formula of this elasticity is:

Ea = Proportional change in quantity demanded of a product / proportional change in

advertisement expenses of that product

QUESTION 2

Solution: If a demand curve goes perfectly up and down then it is known to be inelastic,

under this condition, it only changes the equilibrium prices. In general, goods which are

considered as basic necessities like milk, gasoline, sugar and more, where price doesn’t matter

while purchasing the same, are said to be inelastic (Codogni, Duda and Kusa, 2017). But if

supply suddenly doubles in same condition, due to innovative techniques of production then,

from supplier point of view, price at equilibrium shift downward, as illustrated by below diagram

–

Price

D (Perfectly inelastic demand)

S1 (supply)

P0 (equilibrium) S0 (supply)

P1 (changes in equilibrium)

(Quantity in demanded)

Figure: Changes in equilibrium price with inelastic demand

2

QUESTION 3

Solution: In economics, quantity of a good which is available on a particular price on a

specified period of time, within marketplace, refers to be supply. It defines in respect of function

of price and cost of production, but there is a number of factors present that influences supply. It

includes natural or weather conditions, technology, transport facilities, price, cost of production,

government policies and price of relatable goods, where all such factors are known as

determinants of supply. Hereby, climatic conditions like drought, flood, heavy or less rainfall

influences the production of raw materials, which affects the production of finished or semi-

finished goods. Under such condition, supply of such products either becomes limited or

available in good or high quantity (Duménil and Lévy, 2018). Similarly, technology also

influences rate of production like production of fertilisers, good quality of products and more,

that increases supply of same, at particular marketplace. Other factors like transport facilities

affect process of supply chain, where poor transportation reduces availability of goods or impact

on quality of same that decreases demand of such products and influences supply accordingly.

Therefore, to maintain supply of products, it is essential to develop good infrastructure like road

and other transport ways, so that goods can be supplied in desired manner. Along with this,

changes in price of relatable goods like in production of clothes, price of raw materials like

fabric, cotton, silk, wool, technology, wages of labour, transportation and more, influences its

prices therefore, ultimately either increases or decreases rate of supply in following way –

3

Solution: In economics, quantity of a good which is available on a particular price on a

specified period of time, within marketplace, refers to be supply. It defines in respect of function

of price and cost of production, but there is a number of factors present that influences supply. It

includes natural or weather conditions, technology, transport facilities, price, cost of production,

government policies and price of relatable goods, where all such factors are known as

determinants of supply. Hereby, climatic conditions like drought, flood, heavy or less rainfall

influences the production of raw materials, which affects the production of finished or semi-

finished goods. Under such condition, supply of such products either becomes limited or

available in good or high quantity (Duménil and Lévy, 2018). Similarly, technology also

influences rate of production like production of fertilisers, good quality of products and more,

that increases supply of same, at particular marketplace. Other factors like transport facilities

affect process of supply chain, where poor transportation reduces availability of goods or impact

on quality of same that decreases demand of such products and influences supply accordingly.

Therefore, to maintain supply of products, it is essential to develop good infrastructure like road

and other transport ways, so that goods can be supplied in desired manner. Along with this,

changes in price of relatable goods like in production of clothes, price of raw materials like

fabric, cotton, silk, wool, technology, wages of labour, transportation and more, influences its

prices therefore, ultimately either increases or decreases rate of supply in following way –

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 4

Solution: Costs can be defined as expenses which is used for manufacturing a product

which includes building the firm, labour wages, raw materials prices, machinery and more.

Therefore, it can be categorised in economics in various manner, as described below –

Types of costs in economics

Types of costs Descriptions

Fixed costs (FC) It refers to that costs, which doesn’t vary with changes in output like

costs of insurance, legal bills, building a factory etc. even if any

company experiences changes within business operations like sales

volume, production and more. In this regard, amortization,

depreciations, rent, salaries etc. are remains fixed in business.

Variable costs (VC) It refers to corporate expenses which changes as per production output,

i.e. increase or decrease in variable costs depends totally on volume of

production (Fanti, Gori and Sodini, 2017). Costs of raw materials,

packaging, sales commission, direct labour costs etc. are some few

illustrations of variable costs in business.

Total costs (TC) It is defined as sum of fixed and variable costs, i.e. entire expenses

which is used for producing a good, such as office rent, costs of raw

materials, investment on technology and other machineries etc.

Marginal costs (MC) Marginal costs of production can be defined as total production costs,

which is used for producing a single unit. So, it can be calculating by

dividing the changes in costs of manufacturing the products by changes

in quantity. This would help in determining the point at which a firm can

achieve its economies of scale, by optimising production as well as

overall operations. In such manner, if marginal costs for manufacturing a

single unit calculated as much lower than price of goods per unit, then it

shows potential of business to gain high profitability.

Average total costs

4

Solution: Costs can be defined as expenses which is used for manufacturing a product

which includes building the firm, labour wages, raw materials prices, machinery and more.

Therefore, it can be categorised in economics in various manner, as described below –

Types of costs in economics

Types of costs Descriptions

Fixed costs (FC) It refers to that costs, which doesn’t vary with changes in output like

costs of insurance, legal bills, building a factory etc. even if any

company experiences changes within business operations like sales

volume, production and more. In this regard, amortization,

depreciations, rent, salaries etc. are remains fixed in business.

Variable costs (VC) It refers to corporate expenses which changes as per production output,

i.e. increase or decrease in variable costs depends totally on volume of

production (Fanti, Gori and Sodini, 2017). Costs of raw materials,

packaging, sales commission, direct labour costs etc. are some few

illustrations of variable costs in business.

Total costs (TC) It is defined as sum of fixed and variable costs, i.e. entire expenses

which is used for producing a good, such as office rent, costs of raw

materials, investment on technology and other machineries etc.

Marginal costs (MC) Marginal costs of production can be defined as total production costs,

which is used for producing a single unit. So, it can be calculating by

dividing the changes in costs of manufacturing the products by changes

in quantity. This would help in determining the point at which a firm can

achieve its economies of scale, by optimising production as well as

overall operations. In such manner, if marginal costs for manufacturing a

single unit calculated as much lower than price of goods per unit, then it

shows potential of business to gain high profitability.

Average total costs

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

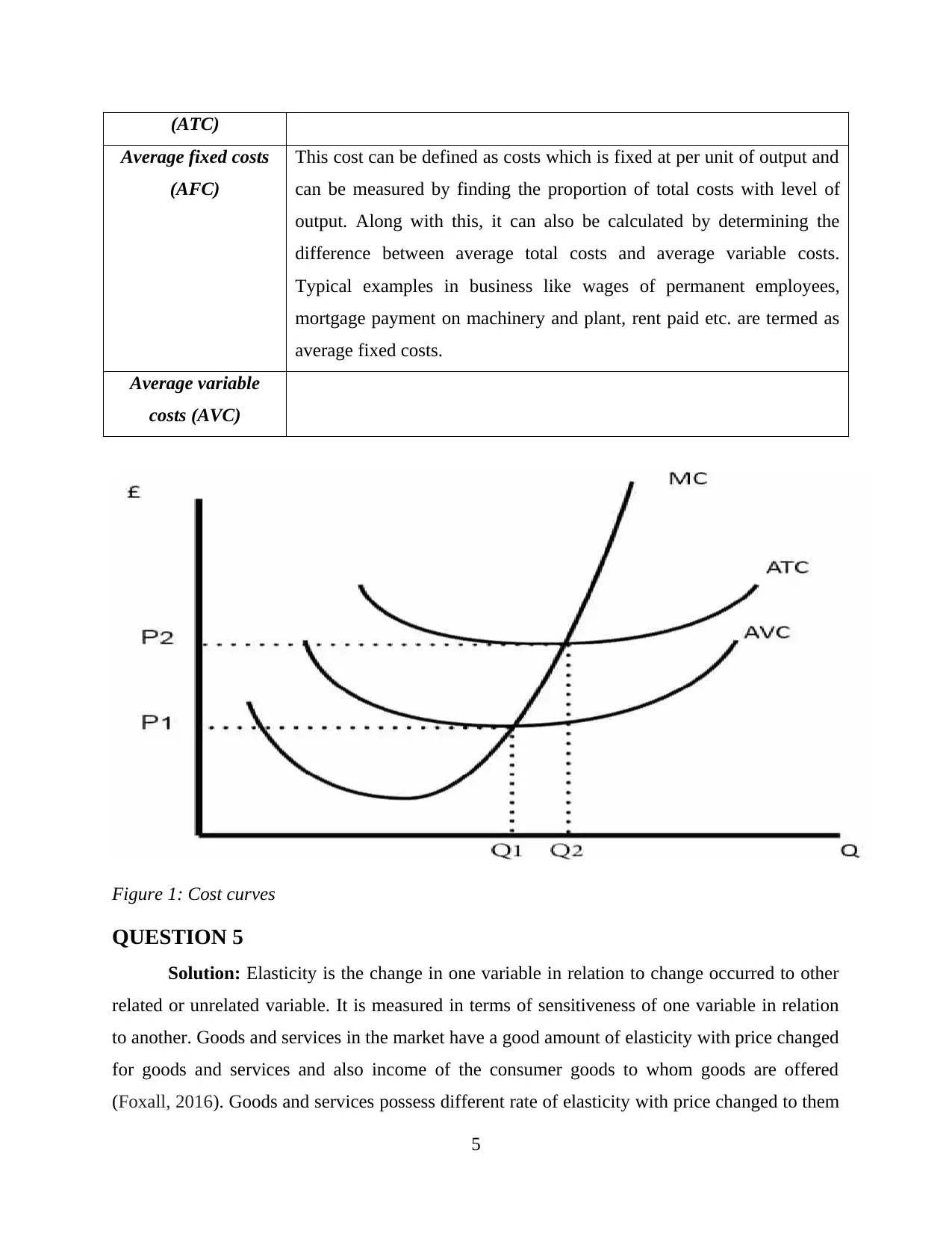

(ATC)

Average fixed costs

(AFC)

This cost can be defined as costs which is fixed at per unit of output and

can be measured by finding the proportion of total costs with level of

output. Along with this, it can also be calculated by determining the

difference between average total costs and average variable costs.

Typical examples in business like wages of permanent employees,

mortgage payment on machinery and plant, rent paid etc. are termed as

average fixed costs.

Average variable

costs (AVC)

Figure 1: Cost curves

QUESTION 5

Solution: Elasticity is the change in one variable in relation to change occurred to other

related or unrelated variable. It is measured in terms of sensitiveness of one variable in relation

to another. Goods and services in the market have a good amount of elasticity with price changed

for goods and services and also income of the consumer goods to whom goods are offered

(Foxall, 2016). Goods and services possess different rate of elasticity with price changed to them

5

Average fixed costs

(AFC)

This cost can be defined as costs which is fixed at per unit of output and

can be measured by finding the proportion of total costs with level of

output. Along with this, it can also be calculated by determining the

difference between average total costs and average variable costs.

Typical examples in business like wages of permanent employees,

mortgage payment on machinery and plant, rent paid etc. are termed as

average fixed costs.

Average variable

costs (AVC)

Figure 1: Cost curves

QUESTION 5

Solution: Elasticity is the change in one variable in relation to change occurred to other

related or unrelated variable. It is measured in terms of sensitiveness of one variable in relation

to another. Goods and services in the market have a good amount of elasticity with price changed

for goods and services and also income of the consumer goods to whom goods are offered

(Foxall, 2016). Goods and services possess different rate of elasticity with price changed to them

5

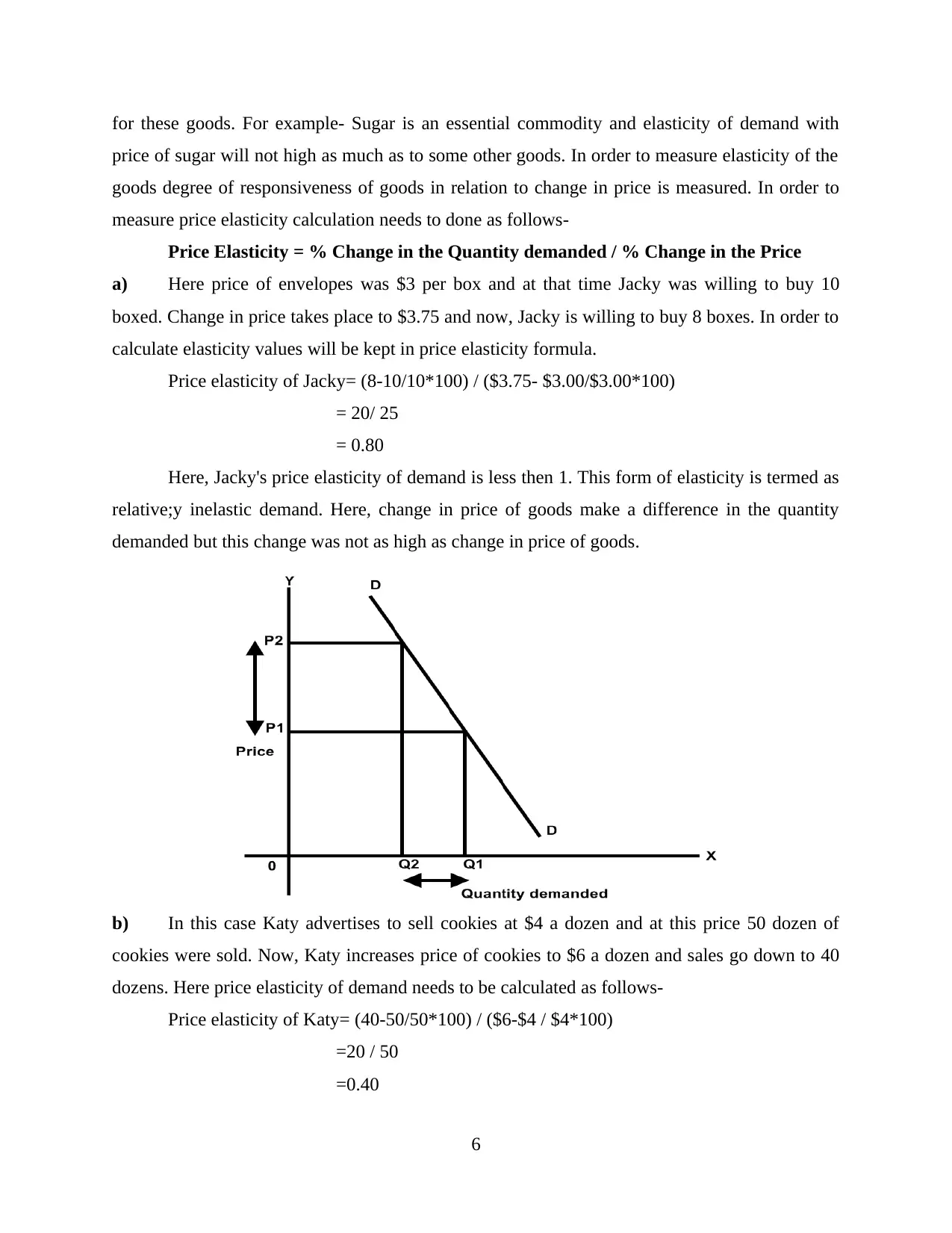

for these goods. For example- Sugar is an essential commodity and elasticity of demand with

price of sugar will not high as much as to some other goods. In order to measure elasticity of the

goods degree of responsiveness of goods in relation to change in price is measured. In order to

measure price elasticity calculation needs to done as follows-

Price Elasticity = % Change in the Quantity demanded / % Change in the Price

a) Here price of envelopes was $3 per box and at that time Jacky was willing to buy 10

boxed. Change in price takes place to $3.75 and now, Jacky is willing to buy 8 boxes. In order to

calculate elasticity values will be kept in price elasticity formula.

Price elasticity of Jacky= (8-10/10*100) / ($3.75- $3.00/$3.00*100)

= 20/ 25

= 0.80

Here, Jacky's price elasticity of demand is less then 1. This form of elasticity is termed as

relative;y inelastic demand. Here, change in price of goods make a difference in the quantity

demanded but this change was not as high as change in price of goods.

b) In this case Katy advertises to sell cookies at $4 a dozen and at this price 50 dozen of

cookies were sold. Now, Katy increases price of cookies to $6 a dozen and sales go down to 40

dozens. Here price elasticity of demand needs to be calculated as follows-

Price elasticity of Katy= (40-50/50*100) / ($6-$4 / $4*100)

=20 / 50

=0.40

6

price of sugar will not high as much as to some other goods. In order to measure elasticity of the

goods degree of responsiveness of goods in relation to change in price is measured. In order to

measure price elasticity calculation needs to done as follows-

Price Elasticity = % Change in the Quantity demanded / % Change in the Price

a) Here price of envelopes was $3 per box and at that time Jacky was willing to buy 10

boxed. Change in price takes place to $3.75 and now, Jacky is willing to buy 8 boxes. In order to

calculate elasticity values will be kept in price elasticity formula.

Price elasticity of Jacky= (8-10/10*100) / ($3.75- $3.00/$3.00*100)

= 20/ 25

= 0.80

Here, Jacky's price elasticity of demand is less then 1. This form of elasticity is termed as

relative;y inelastic demand. Here, change in price of goods make a difference in the quantity

demanded but this change was not as high as change in price of goods.

b) In this case Katy advertises to sell cookies at $4 a dozen and at this price 50 dozen of

cookies were sold. Now, Katy increases price of cookies to $6 a dozen and sales go down to 40

dozens. Here price elasticity of demand needs to be calculated as follows-

Price elasticity of Katy= (40-50/50*100) / ($6-$4 / $4*100)

=20 / 50

=0.40

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Here, Katy also possess relatively in-elasticity of demand with price as change in the

price takes place to 50% but change in quantity demanded is only of 20% and this made

elasticity of cookies with price is of 0.40 only.

QUESTION 6

Equilibrium is a position where demand and supply curve intersect with each other

ensuring that quantity demanded and supply become similar to a point keeping all the economic

factors in consideration. In this question after several years of decline in the market of handmade

guitars a comeback is initiated (Garen, 2019). As these guitars are made in a small workshop

with few skills luithers. Here, impact on equilibrium price and quantity of handmade guitar will

be identified based on certain pre-determined situations.

a) Environmentalists succeed in having the use of Brazilian rosewood banned in the United

States, forcing luthiers to seek out alternative, more costly woods.

In order to prepare guitar usage of Brazilian rosewood had taken place from several years

but now this wood is banned in United states. This creates a situation of using some other wood

as raw material for preparation of handmade guitar's. When cost of raw material used for

preparation of guitar increases then it leads to higher the prices of handmade guitar's in the

market. A situation will rise which will make a outward shift in the equilibrium price of the

guitar. On the other hand when change in price of goods is made then it will create a direct

impact on the demand of the goods. Price and demand possess inverse relationship so demand

curve will shift inward to reflect low demand of guitar's with increased prices.

b) A foreign producer reengineers the guitar-making process and floods the market with

identical guitars.

Identical goods available in the market also serves as one of the economical factor which

leads to change in the demand of the handmade guiter's offered in the market. When a foreign

producer floods the market with identical guitars then supply of identical goods will become high

then demand and the equilibrium will shifts upwards which means at some lower price (Kaushik,

2016). In this situation equilibrium price will go down and demand will increase to certain level

so that new equilibrium can be established where demand and supply curves intersect with each

other.

c) Music featuring handmade acoustic guitars makes a comeback as audiences tire of heavy

metal and grunge music.

7

price takes place to 50% but change in quantity demanded is only of 20% and this made

elasticity of cookies with price is of 0.40 only.

QUESTION 6

Equilibrium is a position where demand and supply curve intersect with each other

ensuring that quantity demanded and supply become similar to a point keeping all the economic

factors in consideration. In this question after several years of decline in the market of handmade

guitars a comeback is initiated (Garen, 2019). As these guitars are made in a small workshop

with few skills luithers. Here, impact on equilibrium price and quantity of handmade guitar will

be identified based on certain pre-determined situations.

a) Environmentalists succeed in having the use of Brazilian rosewood banned in the United

States, forcing luthiers to seek out alternative, more costly woods.

In order to prepare guitar usage of Brazilian rosewood had taken place from several years

but now this wood is banned in United states. This creates a situation of using some other wood

as raw material for preparation of handmade guitar's. When cost of raw material used for

preparation of guitar increases then it leads to higher the prices of handmade guitar's in the

market. A situation will rise which will make a outward shift in the equilibrium price of the

guitar. On the other hand when change in price of goods is made then it will create a direct

impact on the demand of the goods. Price and demand possess inverse relationship so demand

curve will shift inward to reflect low demand of guitar's with increased prices.

b) A foreign producer reengineers the guitar-making process and floods the market with

identical guitars.

Identical goods available in the market also serves as one of the economical factor which

leads to change in the demand of the handmade guiter's offered in the market. When a foreign

producer floods the market with identical guitars then supply of identical goods will become high

then demand and the equilibrium will shifts upwards which means at some lower price (Kaushik,

2016). In this situation equilibrium price will go down and demand will increase to certain level

so that new equilibrium can be established where demand and supply curves intersect with each

other.

c) Music featuring handmade acoustic guitars makes a comeback as audiences tire of heavy

metal and grunge music.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Demand of guitar is highly influenced through trends and preferences available in the

music industry. As audiences likes music with handmade guitar then, eventually it will leads to

generate high demand for handmade guitar's in the music industry. High demand will leads to

change in the price of the guitar to some higher level and equilibrium will shift to outwards.

Demand curve will shift outward to reflect more demand and supply curve will remain same so

that new equilibrium can be established at higher prices.

d) The country goes into a deep recession and the income of the average American falls

sharply.

Income is one of the influential economic factor which have and grate impact on demand

for goods and services offered in the market. When situation of recession arises then demand for

non-essential commodities goods down. As guitar is not an essential commodity so demand

curve of guitar in this situation will move left side and this will leads to minimise price of the

guitar. Here, change in equilibrium price and quantity will be made and demand curve will

change. Leftward shift in demand curve will lower equilibrium price. Change in supply curve

takes place when supply side recession occurs (Rajasulochana and Ganesh, 2019).

QUESTION 7

(a)

Monopolistic competitive market structure is the one where large number of firms are

present and operate business activities. This depicts the presence of imperfect competition

within the market. Here, large number of producers are present that sell products which are

differentiated from each other and not considered as perfect substitutes. There are many reason

behind the difference in between the products like branding, quality and some other special

features possess by each producers. The organisations charges the price of products in

accordance to the price of rivalries products. They does not focus over analysing the impact of

own price over the price of others. The main reason behind the acceptance of all such tactics is to

ascertain the benefits of conditions present in market along with combating the power of

competitors. There are many features that are present in monopolistic competitive market

structure. These will be described below to gain the information about the conditions that are

basically present in the monopolistic competitive industry:

8

music industry. As audiences likes music with handmade guitar then, eventually it will leads to

generate high demand for handmade guitar's in the music industry. High demand will leads to

change in the price of the guitar to some higher level and equilibrium will shift to outwards.

Demand curve will shift outward to reflect more demand and supply curve will remain same so

that new equilibrium can be established at higher prices.

d) The country goes into a deep recession and the income of the average American falls

sharply.

Income is one of the influential economic factor which have and grate impact on demand

for goods and services offered in the market. When situation of recession arises then demand for

non-essential commodities goods down. As guitar is not an essential commodity so demand

curve of guitar in this situation will move left side and this will leads to minimise price of the

guitar. Here, change in equilibrium price and quantity will be made and demand curve will

change. Leftward shift in demand curve will lower equilibrium price. Change in supply curve

takes place when supply side recession occurs (Rajasulochana and Ganesh, 2019).

QUESTION 7

(a)

Monopolistic competitive market structure is the one where large number of firms are

present and operate business activities. This depicts the presence of imperfect competition

within the market. Here, large number of producers are present that sell products which are

differentiated from each other and not considered as perfect substitutes. There are many reason

behind the difference in between the products like branding, quality and some other special

features possess by each producers. The organisations charges the price of products in

accordance to the price of rivalries products. They does not focus over analysing the impact of

own price over the price of others. The main reason behind the acceptance of all such tactics is to

ascertain the benefits of conditions present in market along with combating the power of

competitors. There are many features that are present in monopolistic competitive market

structure. These will be described below to gain the information about the conditions that are

basically present in the monopolistic competitive industry:

8

Presence of large number of buyers and consumers in industry along with no one has

total control over the market price.

The perception of consumers that there will be no difference among the prices of all

differentiated products.

There are few barriers in entry and exist of firms.

The different producers have some control over price but the same will be work around to

the rivalries power.

The organisations under this market behave in accordance to the feeling of confidence

about the demand of their products and the cost incurred in business operation.

Normal profit will be earned by each firm in long period of time.

The substantial amount of cost is incurred towards the advertisement of their products.

Coffee industry is one of the prominent industry that operates the functions in all over the

world with the aid of large number of small and large organisations. The products and services

provided by all are kind of same but totally differentiated on the basis of the brand quality, store

designing, services capabilities etc. Starbucks and costa coffee are the big layers of this industry.

They always decide the price on the basis of the pricing policies followed by each other. All the

different characteristics of monopolistic competitive market structure is justified by the

organisations of this industry. This will clearly depicts the presence of this structure within the

coffee industry. The impact of same is ascertained by the industry in the form of creating major

characteristics which are adhered by all players (Romprasert, 2018). The different major

characteristics which are actually exists in this industry are presented below:

Prices will be fixed by organisations by considering the conditions present in market.

Same raw materials will be used that processed differently to attain competitive edge.

Growing business sector that increases with the rate of 7% due to providence of

differentiated products.

Less number of barriers are exist from the government side regarding the use of beans

and their processing in production of coffee. This promotes the new organisations to enter

easily in market.

Focus over differentiating through improvement in presentation and opening of themed

stores.

9

total control over the market price.

The perception of consumers that there will be no difference among the prices of all

differentiated products.

There are few barriers in entry and exist of firms.

The different producers have some control over price but the same will be work around to

the rivalries power.

The organisations under this market behave in accordance to the feeling of confidence

about the demand of their products and the cost incurred in business operation.

Normal profit will be earned by each firm in long period of time.

The substantial amount of cost is incurred towards the advertisement of their products.

Coffee industry is one of the prominent industry that operates the functions in all over the

world with the aid of large number of small and large organisations. The products and services

provided by all are kind of same but totally differentiated on the basis of the brand quality, store

designing, services capabilities etc. Starbucks and costa coffee are the big layers of this industry.

They always decide the price on the basis of the pricing policies followed by each other. All the

different characteristics of monopolistic competitive market structure is justified by the

organisations of this industry. This will clearly depicts the presence of this structure within the

coffee industry. The impact of same is ascertained by the industry in the form of creating major

characteristics which are adhered by all players (Romprasert, 2018). The different major

characteristics which are actually exists in this industry are presented below:

Prices will be fixed by organisations by considering the conditions present in market.

Same raw materials will be used that processed differently to attain competitive edge.

Growing business sector that increases with the rate of 7% due to providence of

differentiated products.

Less number of barriers are exist from the government side regarding the use of beans

and their processing in production of coffee. This promotes the new organisations to enter

easily in market.

Focus over differentiating through improvement in presentation and opening of themed

stores.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.