Economics Assignment: Analysis of the Oligopoly in Australian Banking

VerifiedAdded on 2020/05/28

|7

|742

|89

Report

AI Summary

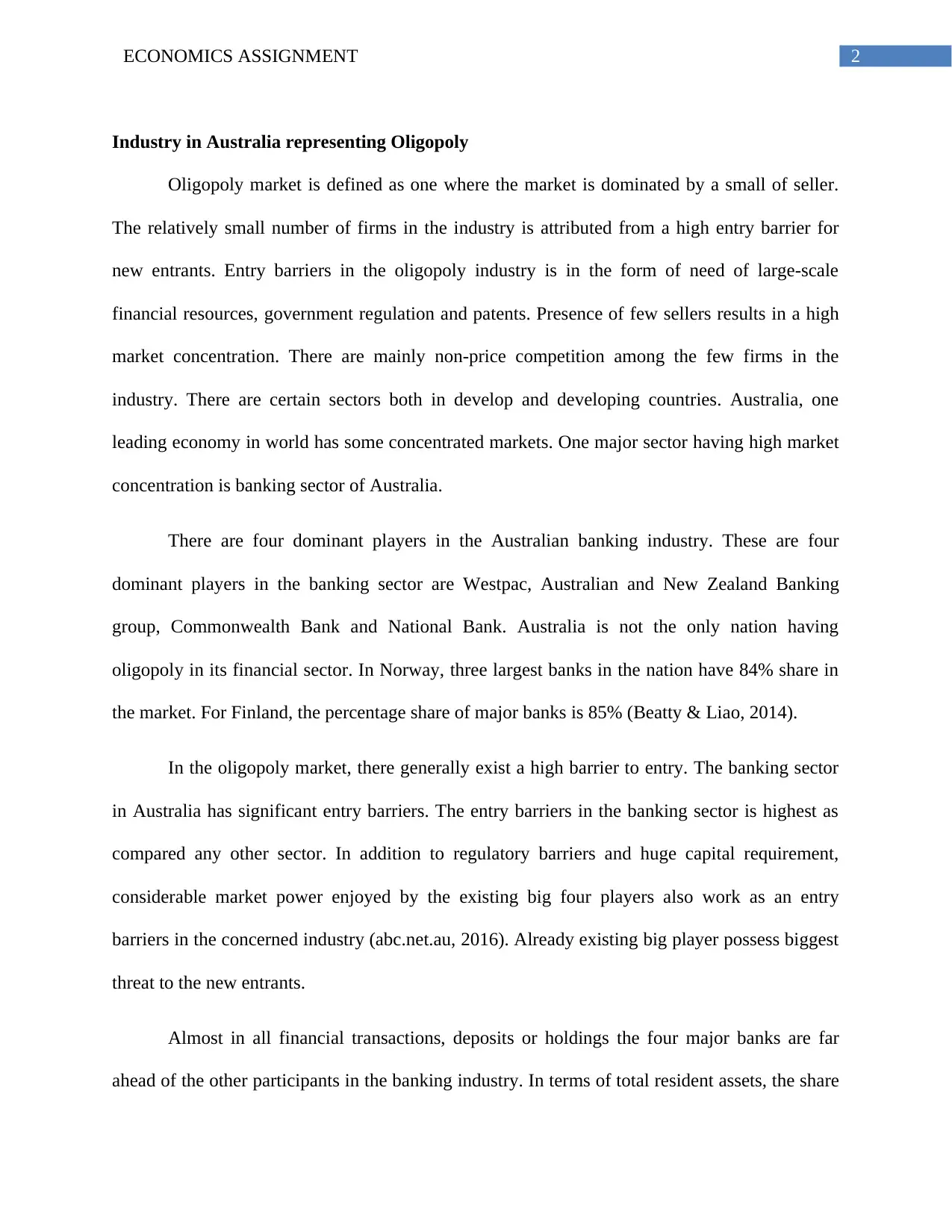

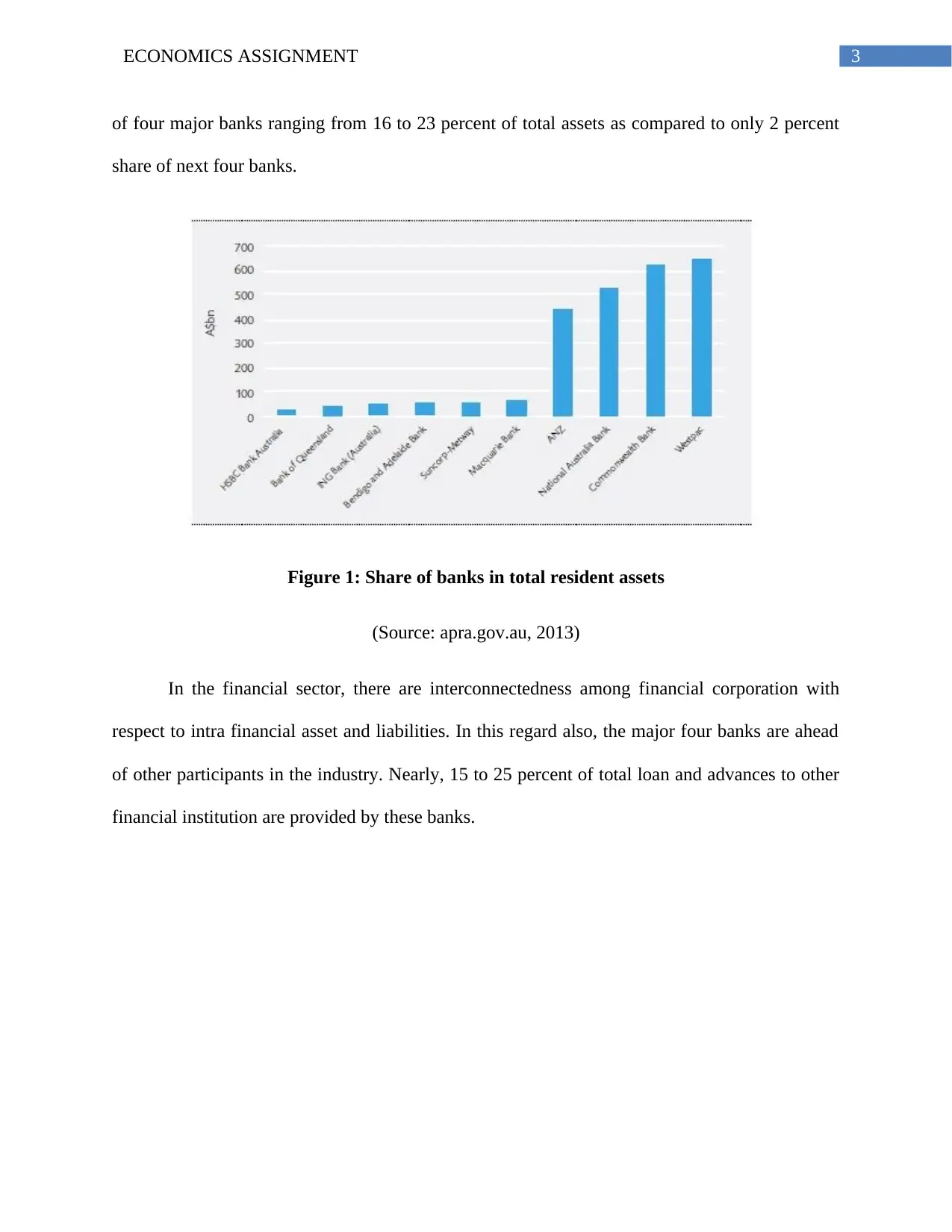

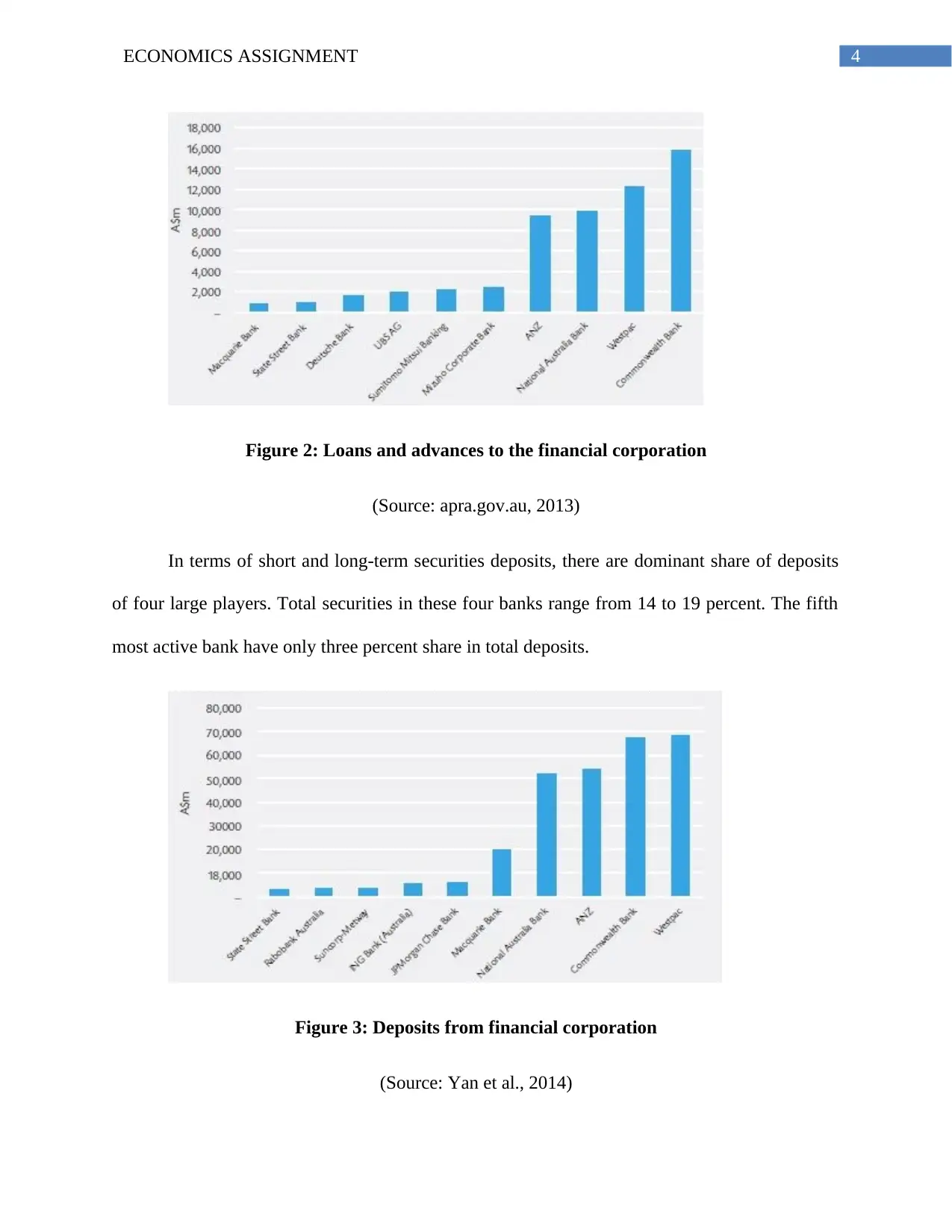

This economics assignment report analyzes the oligopoly market structure within the Australian banking sector. It defines an oligopoly and highlights its characteristics, such as a small number of sellers and high entry barriers, which are often due to factors like large-scale financial requirements, government regulations, and patents. The report identifies the Australian banking sector as a prime example of an oligopoly, dominated by four major players: Westpac, ANZ, Commonwealth Bank, and National Bank. It compares the Australian scenario with other nations like Norway and Finland. The assignment provides data on the market share of these banks, the interconnectedness of financial corporations, and the dominance of the major banks in terms of assets, loans, and deposits. The analysis also touches upon the Australian government's support for the concentration in the banking industry, which strengthens the power of the dominant players. The report uses figures to illustrate the market share of the banks in total resident assets, loans, and deposits from financial corporations, and concludes that the four major banks play a significantly dominating role in the Australian banking industry.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.