University Economics 101: Assignment 1 - Microeconomic Analysis

VerifiedAdded on 2020/03/13

|10

|2590

|90

Homework Assignment

AI Summary

This economics assignment delves into fundamental microeconomic concepts, starting with an explanation of the production possibility curve and the concept of scarcity. It explores the economic system of India, analyzing its evolution from a mixed economy to a more market-oriented approach. The assignment then examines market dynamics, including supply and demand schedules for ice cream, calculating equilibrium price, consumer surplus, and producer surplus, and analyzing the impact of seasonal changes. Further questions address government interventions like price floors in the milk market and their effects on farmers' income. The assignment concludes with calculations of price elasticity of demand, using the midpoint method, and an analysis of how elasticity changes during different periods, along with a complete cost schedule for a gardening company, determining the profit-maximizing output level in a perfectly competitive market.

Assignment 1

Due: 9pmTuesday,15 August, 2017(Week 6)

Weighting: 25%

Note that when you are answering questions that require mathematical calculations, you should

provide details as to how the answers were derived.In completing your answers, you should use

graphs wherever possible. Always provide a brief explanation of each graph, including how it relates

to your overall answer/argument.

Question 1

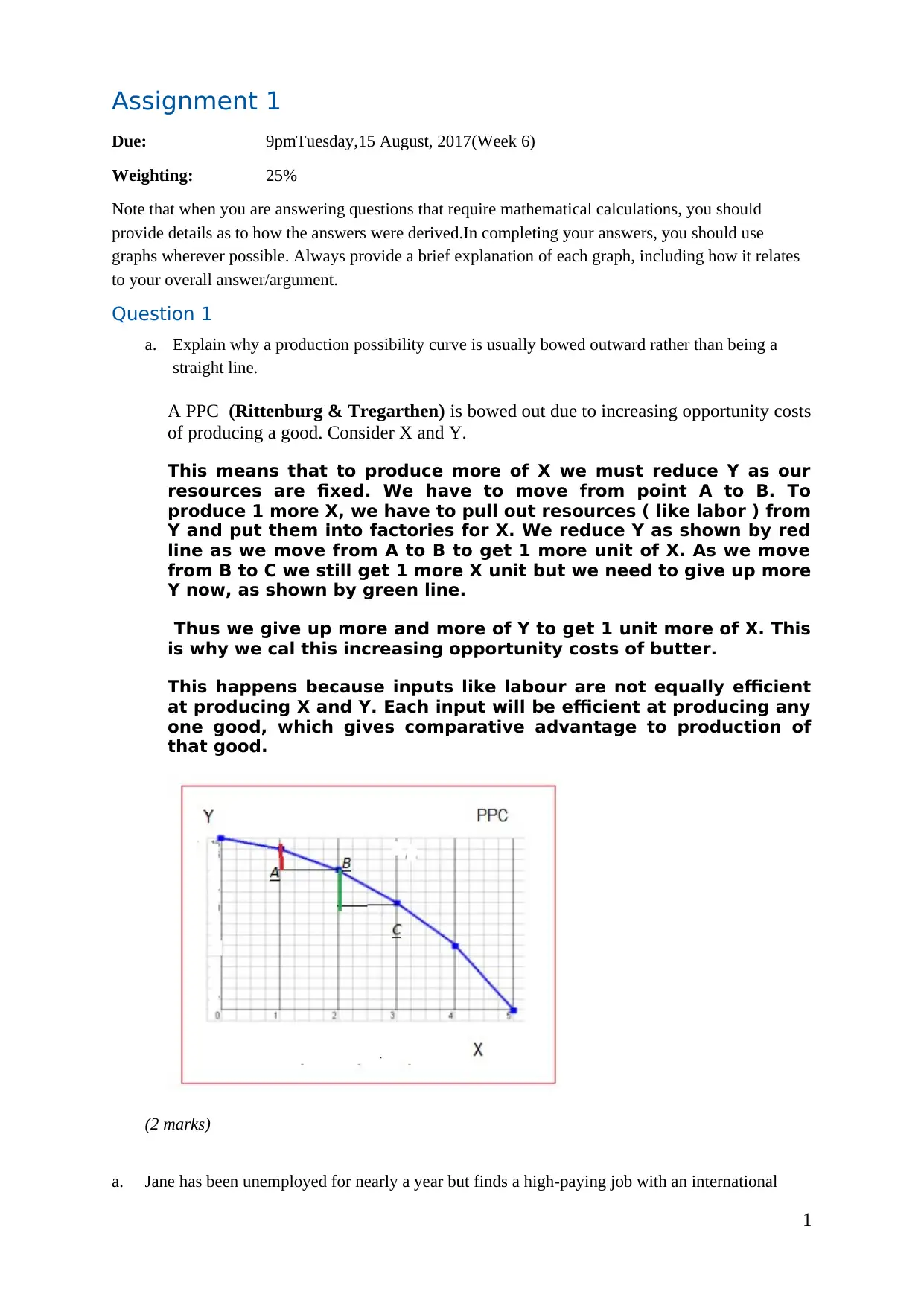

a. Explain why a production possibility curve is usually bowed outward rather than being a

straight line.

A PPC (Rittenburg & Tregarthen) is bowed out due to increasing opportunity costs

of producing a good. Consider X and Y.

This means that to produce more of X we must reduce Y as our

resources are fixed. We have to move from point A to B. To

produce 1 more X, we have to pull out resources ( like labor ) from

Y and put them into factories for X. We reduce Y as shown by red

line as we move from A to B to get 1 more unit of X. As we move

from B to C we still get 1 more X unit but we need to give up more

Y now, as shown by green line.

Thus we give up more and more of Y to get 1 unit more of X. This

is why we cal this increasing opportunity costs of butter.

This happens because inputs like labour are not equally efficient

at producing X and Y. Each input will be efficient at producing any

one good, which gives comparative advantage to production of

that good.

(2 marks)

a. Jane has been unemployed for nearly a year but finds a high-paying job with an international

1

Due: 9pmTuesday,15 August, 2017(Week 6)

Weighting: 25%

Note that when you are answering questions that require mathematical calculations, you should

provide details as to how the answers were derived.In completing your answers, you should use

graphs wherever possible. Always provide a brief explanation of each graph, including how it relates

to your overall answer/argument.

Question 1

a. Explain why a production possibility curve is usually bowed outward rather than being a

straight line.

A PPC (Rittenburg & Tregarthen) is bowed out due to increasing opportunity costs

of producing a good. Consider X and Y.

This means that to produce more of X we must reduce Y as our

resources are fixed. We have to move from point A to B. To

produce 1 more X, we have to pull out resources ( like labor ) from

Y and put them into factories for X. We reduce Y as shown by red

line as we move from A to B to get 1 more unit of X. As we move

from B to C we still get 1 more X unit but we need to give up more

Y now, as shown by green line.

Thus we give up more and more of Y to get 1 unit more of X. This

is why we cal this increasing opportunity costs of butter.

This happens because inputs like labour are not equally efficient

at producing X and Y. Each input will be efficient at producing any

one good, which gives comparative advantage to production of

that good.

(2 marks)

a. Jane has been unemployed for nearly a year but finds a high-paying job with an international

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

hotel firm. Does this mean that Jane will no longer experience the problem of ‘scarcity’? Explain

the reasons for your answer.

Scarcity is a macro issue, from the economy level. It means that jobs available are lesser than the

no of persons who are looking for work. For each person who has a job there is no scarcity as

long as he has a job. For someone who is unemployed there is scarcity of jobs.

As long as Jane has a job she does not face scarcity. If unemployed there is scarcity of jobs for

her.,

(3 marks)

b. Every country has an economic system that has been established to address the problem of

scarcity. Describe the economic system of a country other than Australia. Justify your assessment

of the system by considering the major factors that determinean economic system within a

country (300 words maximum).

Consider India as a country. When it became free of British colonial rule in 1947 it adopted

mixed economy model of an economic system. It allowed some sectors to have private producers

but reserved many sectors for State production only- defence, heavy machines, etc. This was

done as resources were scarce and the needs of a poor nation were manifold. It was thought that

State allocation of resources is best to overcome the scarcity problem.

India first policy - Industrial Policy of 1948 was framed under the mixed

economy concept, allowing a role for private and public sector. It was

followed by Industrial Policy 1956. IT clearly came out in favour of wide

spread State involvement in industrial activities. 17 industries were made

the exclusive domain of State. No private sector was allowed in these

industries- arms and ammunition, atomic energy, iron and steel, heavy

castings and forgings of iron and steel, heavy machinery, heavy electrical

industries, coal, mineral oil, mining; iron ore and other important minerals

like, copper, lead and zinc; railway transport, aircraft, ship building,

telephone, telegraph and wireless equipment, and generation and

distribution of electricity. (Jadhav, n.d.)

This policy was later reversed in 1991, when India embarked on reforms. The cause of this

change was the difference in economic strenght of India in 1947 and 1991. In 1947 India was

poor and under developed- with scarce resources- financial and non financial. It needed to build

on its limited resources to grow. By 1991 India was better placed and had built up certain basic

industries and started deregulating many industries. The process of privatisation was made

possible due to availability of more resources that were better and more efficient than those in

1947. (Home.fau.edu, n.d.)

This is clear case of resource availability dictating the economic system adopted by a nation.

(5 marks)

2

the reasons for your answer.

Scarcity is a macro issue, from the economy level. It means that jobs available are lesser than the

no of persons who are looking for work. For each person who has a job there is no scarcity as

long as he has a job. For someone who is unemployed there is scarcity of jobs.

As long as Jane has a job she does not face scarcity. If unemployed there is scarcity of jobs for

her.,

(3 marks)

b. Every country has an economic system that has been established to address the problem of

scarcity. Describe the economic system of a country other than Australia. Justify your assessment

of the system by considering the major factors that determinean economic system within a

country (300 words maximum).

Consider India as a country. When it became free of British colonial rule in 1947 it adopted

mixed economy model of an economic system. It allowed some sectors to have private producers

but reserved many sectors for State production only- defence, heavy machines, etc. This was

done as resources were scarce and the needs of a poor nation were manifold. It was thought that

State allocation of resources is best to overcome the scarcity problem.

India first policy - Industrial Policy of 1948 was framed under the mixed

economy concept, allowing a role for private and public sector. It was

followed by Industrial Policy 1956. IT clearly came out in favour of wide

spread State involvement in industrial activities. 17 industries were made

the exclusive domain of State. No private sector was allowed in these

industries- arms and ammunition, atomic energy, iron and steel, heavy

castings and forgings of iron and steel, heavy machinery, heavy electrical

industries, coal, mineral oil, mining; iron ore and other important minerals

like, copper, lead and zinc; railway transport, aircraft, ship building,

telephone, telegraph and wireless equipment, and generation and

distribution of electricity. (Jadhav, n.d.)

This policy was later reversed in 1991, when India embarked on reforms. The cause of this

change was the difference in economic strenght of India in 1947 and 1991. In 1947 India was

poor and under developed- with scarce resources- financial and non financial. It needed to build

on its limited resources to grow. By 1991 India was better placed and had built up certain basic

industries and started deregulating many industries. The process of privatisation was made

possible due to availability of more resources that were better and more efficient than those in

1947. (Home.fau.edu, n.d.)

This is clear case of resource availability dictating the economic system adopted by a nation.

(5 marks)

2

Question 2

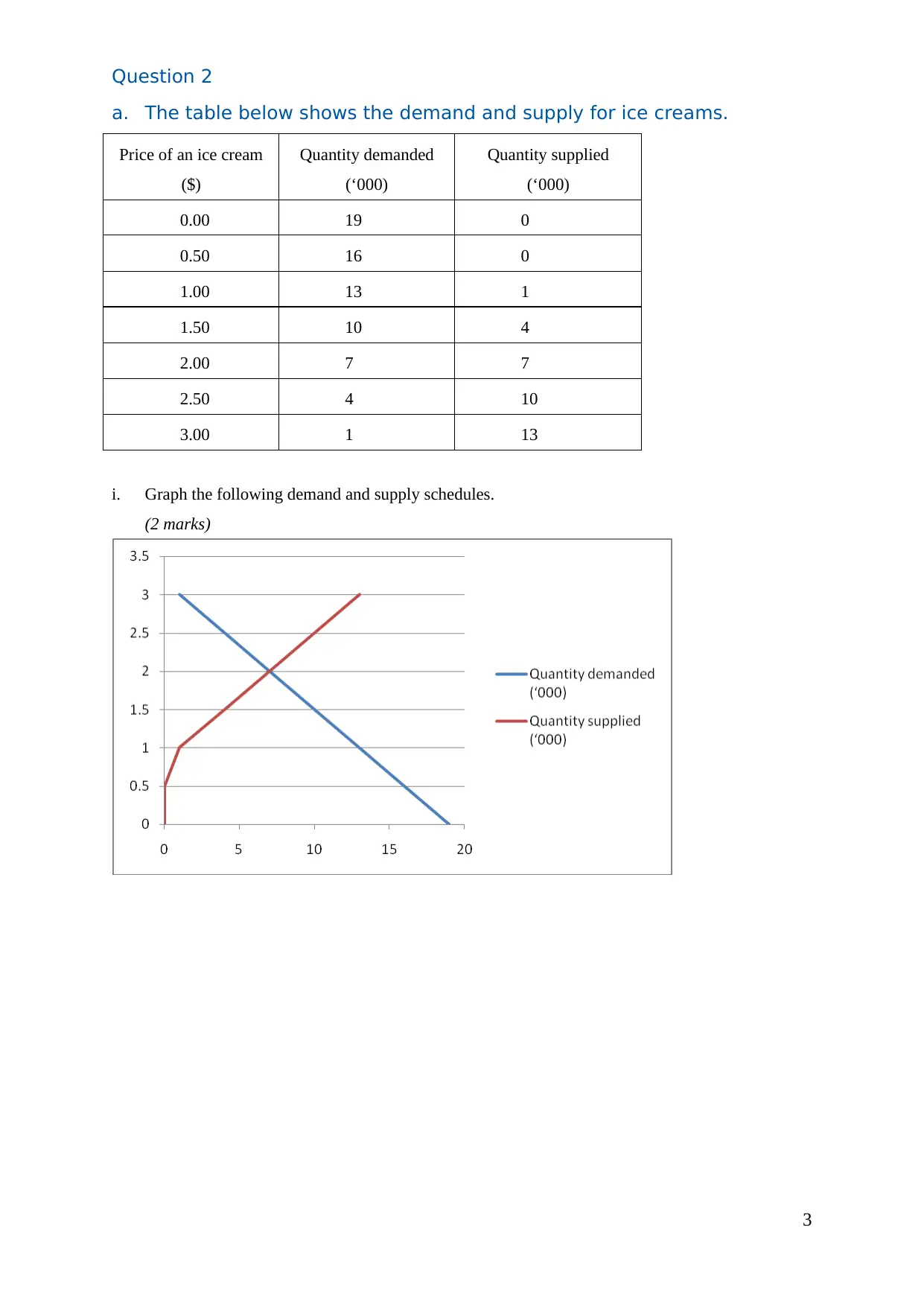

a. The table below shows the demand and supply for ice creams.

Price of an ice cream

($)

Quantity demanded

(‘000)

Quantity supplied

(‘000)

0.00 19 0

0.50 16 0

1.00 13 1

1.50 10 4

2.00 7 7

2.50 4 10

3.00 1 13

i. Graph the following demand and supply schedules.

(2 marks)

3

a. The table below shows the demand and supply for ice creams.

Price of an ice cream

($)

Quantity demanded

(‘000)

Quantity supplied

(‘000)

0.00 19 0

0.50 16 0

1.00 13 1

1.50 10 4

2.00 7 7

2.50 4 10

3.00 1 13

i. Graph the following demand and supply schedules.

(2 marks)

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

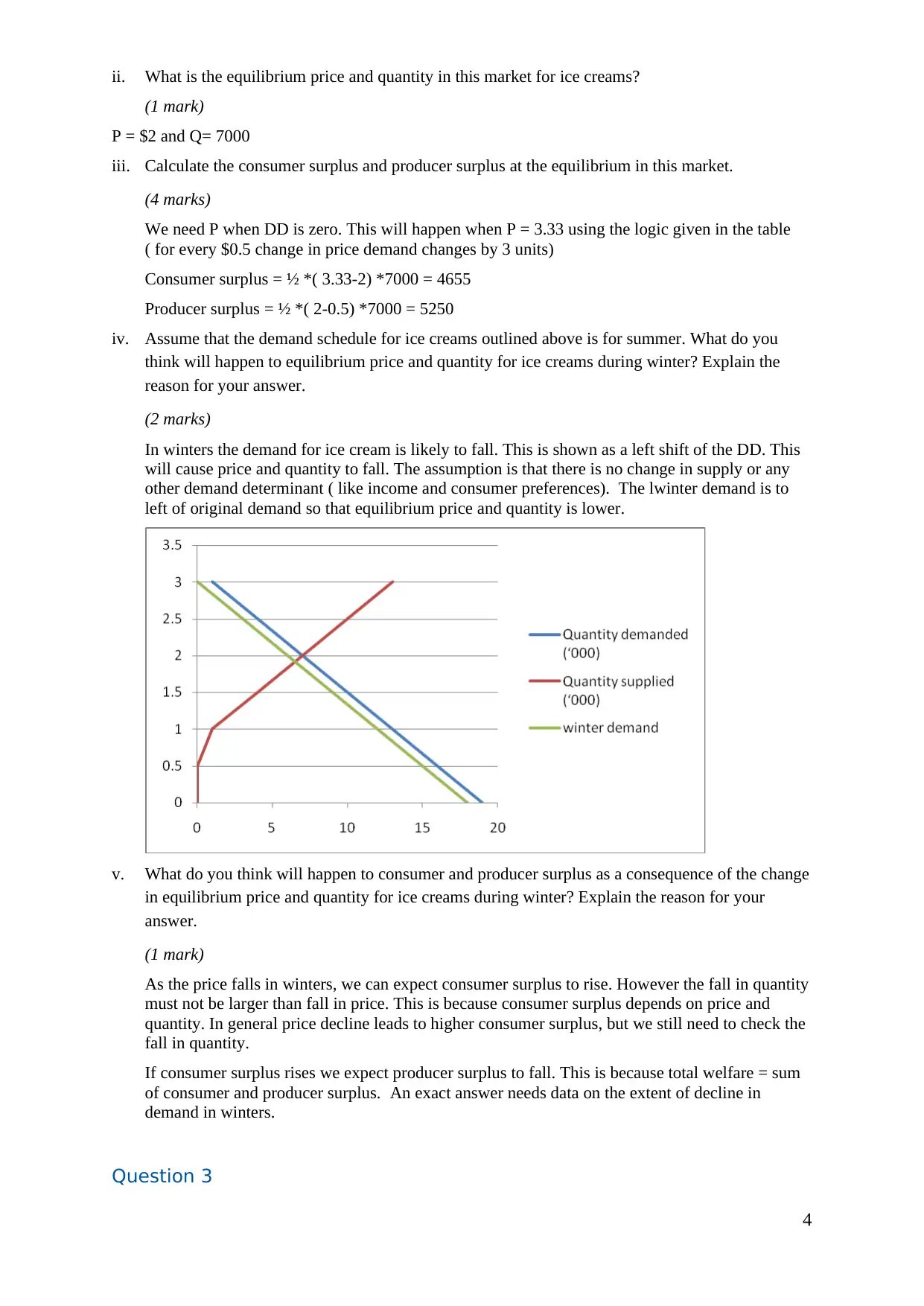

ii. What is the equilibrium price and quantity in this market for ice creams?

(1 mark)

P = $2 and Q= 7000

iii. Calculate the consumer surplus and producer surplus at the equilibrium in this market.

(4 marks)

We need P when DD is zero. This will happen when P = 3.33 using the logic given in the table

( for every $0.5 change in price demand changes by 3 units)

Consumer surplus = ½ *( 3.33-2) *7000 = 4655

Producer surplus = ½ *( 2-0.5) *7000 = 5250

iv. Assume that the demand schedule for ice creams outlined above is for summer. What do you

think will happen to equilibrium price and quantity for ice creams during winter? Explain the

reason for your answer.

(2 marks)

In winters the demand for ice cream is likely to fall. This is shown as a left shift of the DD. This

will cause price and quantity to fall. The assumption is that there is no change in supply or any

other demand determinant ( like income and consumer preferences). The lwinter demand is to

left of original demand so that equilibrium price and quantity is lower.

v. What do you think will happen to consumer and producer surplus as a consequence of the change

in equilibrium price and quantity for ice creams during winter? Explain the reason for your

answer.

(1 mark)

As the price falls in winters, we can expect consumer surplus to rise. However the fall in quantity

must not be larger than fall in price. This is because consumer surplus depends on price and

quantity. In general price decline leads to higher consumer surplus, but we still need to check the

fall in quantity.

If consumer surplus rises we expect producer surplus to fall. This is because total welfare = sum

of consumer and producer surplus. An exact answer needs data on the extent of decline in

demand in winters.

Question 3

4

(1 mark)

P = $2 and Q= 7000

iii. Calculate the consumer surplus and producer surplus at the equilibrium in this market.

(4 marks)

We need P when DD is zero. This will happen when P = 3.33 using the logic given in the table

( for every $0.5 change in price demand changes by 3 units)

Consumer surplus = ½ *( 3.33-2) *7000 = 4655

Producer surplus = ½ *( 2-0.5) *7000 = 5250

iv. Assume that the demand schedule for ice creams outlined above is for summer. What do you

think will happen to equilibrium price and quantity for ice creams during winter? Explain the

reason for your answer.

(2 marks)

In winters the demand for ice cream is likely to fall. This is shown as a left shift of the DD. This

will cause price and quantity to fall. The assumption is that there is no change in supply or any

other demand determinant ( like income and consumer preferences). The lwinter demand is to

left of original demand so that equilibrium price and quantity is lower.

v. What do you think will happen to consumer and producer surplus as a consequence of the change

in equilibrium price and quantity for ice creams during winter? Explain the reason for your

answer.

(1 mark)

As the price falls in winters, we can expect consumer surplus to rise. However the fall in quantity

must not be larger than fall in price. This is because consumer surplus depends on price and

quantity. In general price decline leads to higher consumer surplus, but we still need to check the

fall in quantity.

If consumer surplus rises we expect producer surplus to fall. This is because total welfare = sum

of consumer and producer surplus. An exact answer needs data on the extent of decline in

demand in winters.

Question 3

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

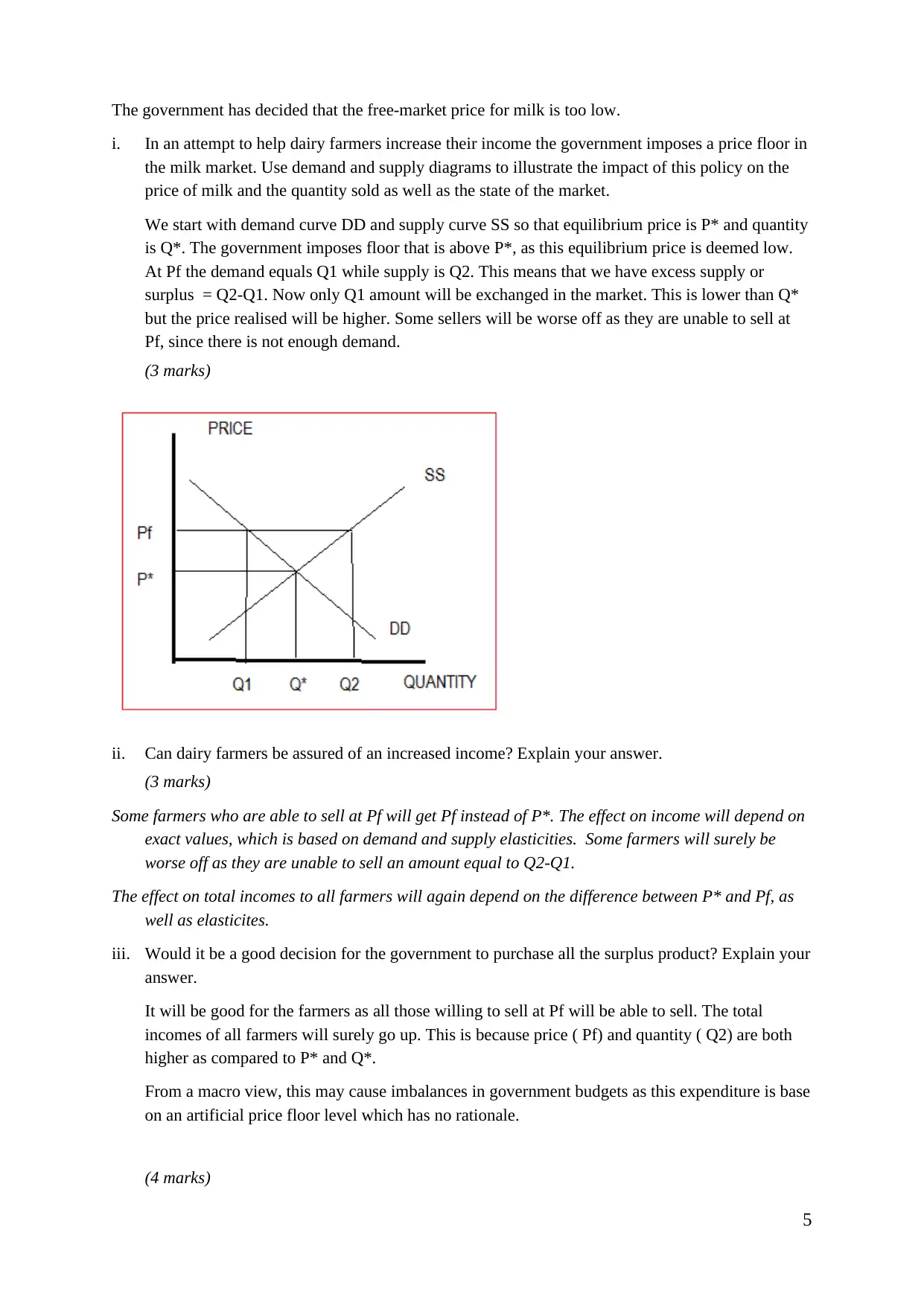

The government has decided that the free-market price for milk is too low.

i. In an attempt to help dairy farmers increase their income the government imposes a price floor in

the milk market. Use demand and supply diagrams to illustrate the impact of this policy on the

price of milk and the quantity sold as well as the state of the market.

We start with demand curve DD and supply curve SS so that equilibrium price is P* and quantity

is Q*. The government imposes floor that is above P*, as this equilibrium price is deemed low.

At Pf the demand equals Q1 while supply is Q2. This means that we have excess supply or

surplus = Q2-Q1. Now only Q1 amount will be exchanged in the market. This is lower than Q*

but the price realised will be higher. Some sellers will be worse off as they are unable to sell at

Pf, since there is not enough demand.

(3 marks)

ii. Can dairy farmers be assured of an increased income? Explain your answer.

(3 marks)

Some farmers who are able to sell at Pf will get Pf instead of P*. The effect on income will depend on

exact values, which is based on demand and supply elasticities. Some farmers will surely be

worse off as they are unable to sell an amount equal to Q2-Q1.

The effect on total incomes to all farmers will again depend on the difference between P* and Pf, as

well as elasticites.

iii. Would it be a good decision for the government to purchase all the surplus product? Explain your

answer.

It will be good for the farmers as all those willing to sell at Pf will be able to sell. The total

incomes of all farmers will surely go up. This is because price ( Pf) and quantity ( Q2) are both

higher as compared to P* and Q*.

From a macro view, this may cause imbalances in government budgets as this expenditure is base

on an artificial price floor level which has no rationale.

(4 marks)

5

i. In an attempt to help dairy farmers increase their income the government imposes a price floor in

the milk market. Use demand and supply diagrams to illustrate the impact of this policy on the

price of milk and the quantity sold as well as the state of the market.

We start with demand curve DD and supply curve SS so that equilibrium price is P* and quantity

is Q*. The government imposes floor that is above P*, as this equilibrium price is deemed low.

At Pf the demand equals Q1 while supply is Q2. This means that we have excess supply or

surplus = Q2-Q1. Now only Q1 amount will be exchanged in the market. This is lower than Q*

but the price realised will be higher. Some sellers will be worse off as they are unable to sell at

Pf, since there is not enough demand.

(3 marks)

ii. Can dairy farmers be assured of an increased income? Explain your answer.

(3 marks)

Some farmers who are able to sell at Pf will get Pf instead of P*. The effect on income will depend on

exact values, which is based on demand and supply elasticities. Some farmers will surely be

worse off as they are unable to sell an amount equal to Q2-Q1.

The effect on total incomes to all farmers will again depend on the difference between P* and Pf, as

well as elasticites.

iii. Would it be a good decision for the government to purchase all the surplus product? Explain your

answer.

It will be good for the farmers as all those willing to sell at Pf will be able to sell. The total

incomes of all farmers will surely go up. This is because price ( Pf) and quantity ( Q2) are both

higher as compared to P* and Q*.

From a macro view, this may cause imbalances in government budgets as this expenditure is base

on an artificial price floor level which has no rationale.

(4 marks)

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

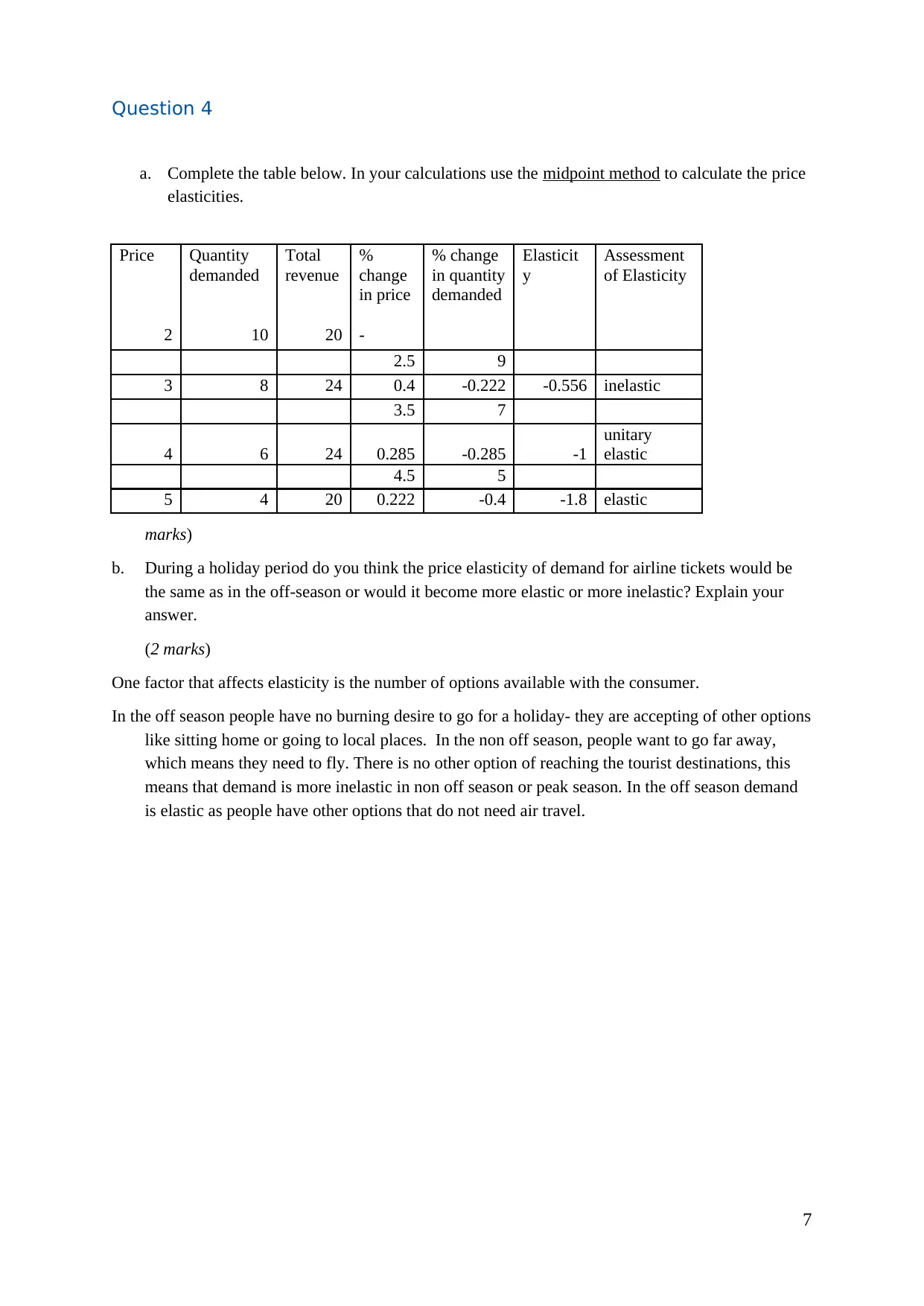

Question 4

a. Complete the table below. In your calculations use the midpoint method to calculate the price

elasticities.

Price Quantity

demanded

Total

revenue

%

change

in price

% change

in quantity

demanded

Elasticit

y

Assessment

of Elasticity

2 10 20 -

2.5 9

3 8 24 0.4 -0.222 -0.556 inelastic

3.5 7

4 6 24 0.285 -0.285 -1

unitary

elastic

4.5 5

5 4 20 0.222 -0.4 -1.8 elastic

marks)

b. During a holiday period do you think the price elasticity of demand for airline tickets would be

the same as in the off-season or would it become more elastic or more inelastic? Explain your

answer.

(2 marks)

One factor that affects elasticity is the number of options available with the consumer.

In the off season people have no burning desire to go for a holiday- they are accepting of other options

like sitting home or going to local places. In the non off season, people want to go far away,

which means they need to fly. There is no other option of reaching the tourist destinations, this

means that demand is more inelastic in non off season or peak season. In the off season demand

is elastic as people have other options that do not need air travel.

7

a. Complete the table below. In your calculations use the midpoint method to calculate the price

elasticities.

Price Quantity

demanded

Total

revenue

%

change

in price

% change

in quantity

demanded

Elasticit

y

Assessment

of Elasticity

2 10 20 -

2.5 9

3 8 24 0.4 -0.222 -0.556 inelastic

3.5 7

4 6 24 0.285 -0.285 -1

unitary

elastic

4.5 5

5 4 20 0.222 -0.4 -1.8 elastic

marks)

b. During a holiday period do you think the price elasticity of demand for airline tickets would be

the same as in the off-season or would it become more elastic or more inelastic? Explain your

answer.

(2 marks)

One factor that affects elasticity is the number of options available with the consumer.

In the off season people have no burning desire to go for a holiday- they are accepting of other options

like sitting home or going to local places. In the non off season, people want to go far away,

which means they need to fly. There is no other option of reaching the tourist destinations, this

means that demand is more inelastic in non off season or peak season. In the off season demand

is elastic as people have other options that do not need air travel.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Question 5

a) Complete the cost schedule below for a gardening company:

Quantity

of

gardens

Total Fixed

Cost (TFC)

Total

Variable

Cost

(TVC)

Total

Cost (TC)

Marginal

Cost (MC)

Average

fixed cost

Average

variable cost

Average

total cost

$ (AFC) (AVC) (ATC)

$ $ $ $ $ $

0 10 10

1 10 4 14 4 10 4 14

2 10 12 22 8 5 6 11

3 10 24 34 12 3.3333 8 11.333

4 10 40 50 16 2.5 10 12.5

5 10 60 70 20 2 12 14

6 10 84 94 24 1.6667 14 15.667

7 10 112 122 28 1.428 16 17.428

8 10 144 154 32 1.25 18 19.25

(3 arks)

b. If the firm is operating in a perfect market where the price for gardening at one houseis $20

dollars, how many gardens should this companydo in order to maximise profit? Explain your

answer.

The logic used is MR= MC

As price is fixed the P= MR = 20

MC is shown in table.

At Q = 5 MR=MC = 20

This is equilibrium output level where profits are maximum .

Profits = TR-TC = 20*5 – 70 = 30

(3 marks)

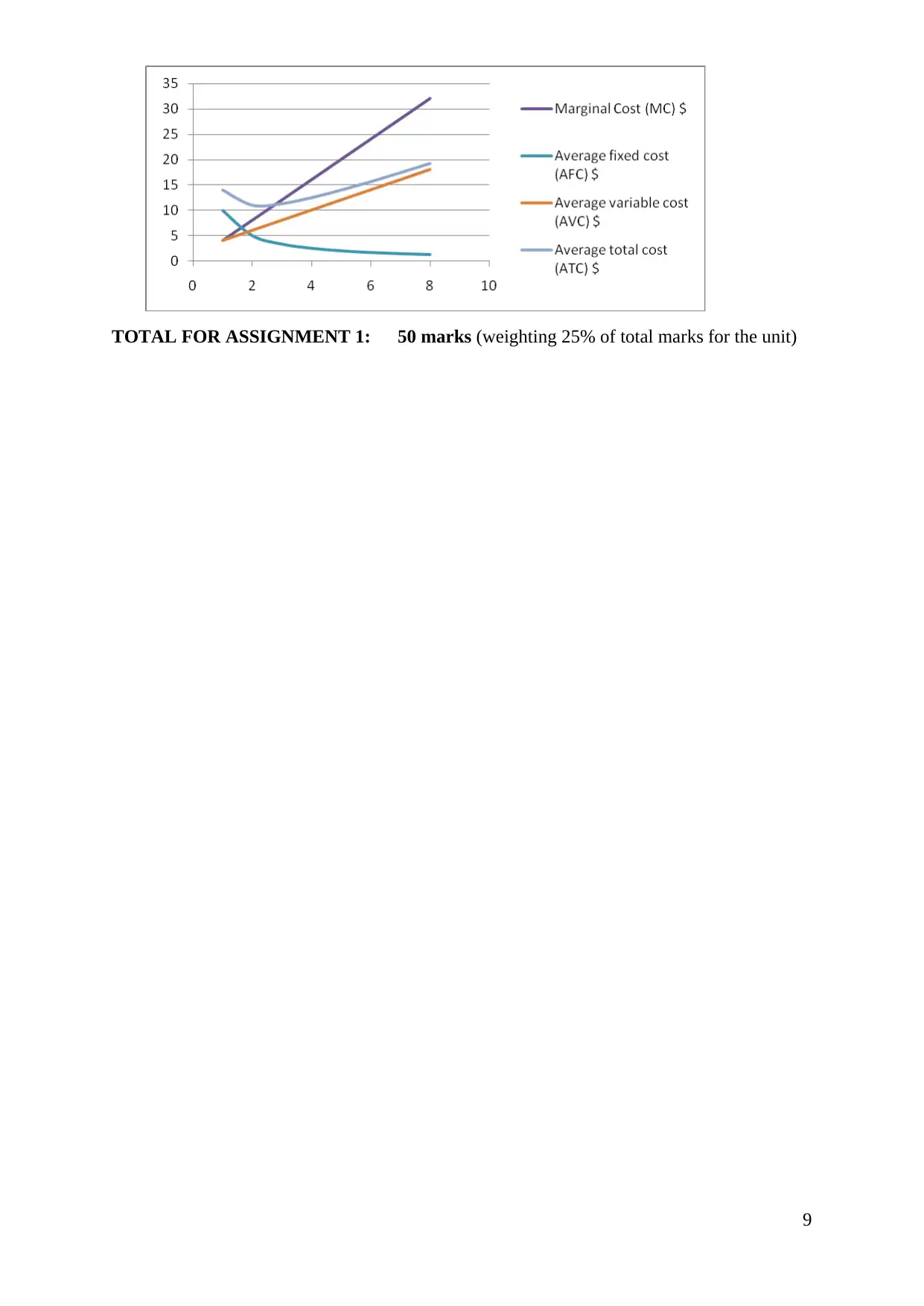

c. Graph the average variable cost, average total cost and marginal cost and marginal revenue

curves.

(4 marks)

8

a) Complete the cost schedule below for a gardening company:

Quantity

of

gardens

Total Fixed

Cost (TFC)

Total

Variable

Cost

(TVC)

Total

Cost (TC)

Marginal

Cost (MC)

Average

fixed cost

Average

variable cost

Average

total cost

$ (AFC) (AVC) (ATC)

$ $ $ $ $ $

0 10 10

1 10 4 14 4 10 4 14

2 10 12 22 8 5 6 11

3 10 24 34 12 3.3333 8 11.333

4 10 40 50 16 2.5 10 12.5

5 10 60 70 20 2 12 14

6 10 84 94 24 1.6667 14 15.667

7 10 112 122 28 1.428 16 17.428

8 10 144 154 32 1.25 18 19.25

(3 arks)

b. If the firm is operating in a perfect market where the price for gardening at one houseis $20

dollars, how many gardens should this companydo in order to maximise profit? Explain your

answer.

The logic used is MR= MC

As price is fixed the P= MR = 20

MC is shown in table.

At Q = 5 MR=MC = 20

This is equilibrium output level where profits are maximum .

Profits = TR-TC = 20*5 – 70 = 30

(3 marks)

c. Graph the average variable cost, average total cost and marginal cost and marginal revenue

curves.

(4 marks)

8

TOTAL FOR ASSIGNMENT 1: 50 marks (weighting 25% of total marks for the unit)

9

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Bibliography

Courseera.org, n.d. MR=MC rule. [Online] Available at: HYPERLINK

"https://www.coursera.org/learn/principles-of-microeconomics/lecture/zKD8R/pricing-and-

production-rules-p-mr-mc-the-shutdown-rule" https://www.coursera.org/learn/principles-of-

microeconomics/lecture/zKD8R/pricing-and-production-rules-p-mr-mc-the-shutdown-rule

[Accessed 2 August 2017].

CSun.edu, n.d. Microeconomics. [Online] Available at: HYPERLINK

"http://www.csun.edu/sites/default/files/micro3.pdf"

http://www.csun.edu/sites/default/files/micro3.pdf [Accessed 2 June 2017].

Econ.ohio-state.edu, n.d. Elasticity. [Online] Available at: HYPERLINK

"http://www.econ.ohio-state.edu/jpeck/H200/EconH200L5.pdf" http://www.econ.ohio-

state.edu/jpeck/H200/EconH200L5.pdf [Accessed 30 May 2017].

Econport.org, n.d. Impact of Shifts in demand and supply. [Online] Available at:

HYPERLINK "http://www.econport.org/content/handbook/Equilibrium/Impact-.html"

http://www.econport.org/content/handbook/Equilibrium/Impact-.html [Accessed 3 June

2017].

Gallo, A., n.d. A refresher on price elasticity. [Online] Available at: HYPERLINK

"https://hbr.org/2015/08/a-refresher-on-price-elasticity" https://hbr.org/2015/08/a-refresher-

on-price-elasticity [Accessed 15 August 2017].

Home.fau.edu, n.d. Indian Economy since Independence. [Online] Available at:

HYPERLINK "http://home.fau.edu/sghosh/web/images/India%20talk.pdf"

http://home.fau.edu/sghosh/web/images/India%20talk.pdf [Accessed 15 Aug 2017].

Jadhav, N., n.d. Industrial Policy since 1956. [Online] Available at: HYPERLINK

"http://www.drnarendrajadhav.info/drjadhav-data_files/Published%20papers/Indian

%20Industrial%20Policy%20Since%201956.pdf"

http://www.drnarendrajadhav.info/drjadhav-data_files/Published%20papers/Indian

%20Industrial%20Policy%20Since%201956.pdf [Accessed 15 Aug 2017].

Rittenburg, L. & Tregarthen, T., n.d. Principles of Economics V 1.0. [Online] Available at:

HYPERLINK "https://catalog.flatworldknowledge.com/bookhub/22?e=rittenecon-ch02_s03"

https://catalog.flatworldknowledge.com/bookhub/22?e=rittenecon-ch02_s03 [Accessed 14

August 2017].

10

Courseera.org, n.d. MR=MC rule. [Online] Available at: HYPERLINK

"https://www.coursera.org/learn/principles-of-microeconomics/lecture/zKD8R/pricing-and-

production-rules-p-mr-mc-the-shutdown-rule" https://www.coursera.org/learn/principles-of-

microeconomics/lecture/zKD8R/pricing-and-production-rules-p-mr-mc-the-shutdown-rule

[Accessed 2 August 2017].

CSun.edu, n.d. Microeconomics. [Online] Available at: HYPERLINK

"http://www.csun.edu/sites/default/files/micro3.pdf"

http://www.csun.edu/sites/default/files/micro3.pdf [Accessed 2 June 2017].

Econ.ohio-state.edu, n.d. Elasticity. [Online] Available at: HYPERLINK

"http://www.econ.ohio-state.edu/jpeck/H200/EconH200L5.pdf" http://www.econ.ohio-

state.edu/jpeck/H200/EconH200L5.pdf [Accessed 30 May 2017].

Econport.org, n.d. Impact of Shifts in demand and supply. [Online] Available at:

HYPERLINK "http://www.econport.org/content/handbook/Equilibrium/Impact-.html"

http://www.econport.org/content/handbook/Equilibrium/Impact-.html [Accessed 3 June

2017].

Gallo, A., n.d. A refresher on price elasticity. [Online] Available at: HYPERLINK

"https://hbr.org/2015/08/a-refresher-on-price-elasticity" https://hbr.org/2015/08/a-refresher-

on-price-elasticity [Accessed 15 August 2017].

Home.fau.edu, n.d. Indian Economy since Independence. [Online] Available at:

HYPERLINK "http://home.fau.edu/sghosh/web/images/India%20talk.pdf"

http://home.fau.edu/sghosh/web/images/India%20talk.pdf [Accessed 15 Aug 2017].

Jadhav, N., n.d. Industrial Policy since 1956. [Online] Available at: HYPERLINK

"http://www.drnarendrajadhav.info/drjadhav-data_files/Published%20papers/Indian

%20Industrial%20Policy%20Since%201956.pdf"

http://www.drnarendrajadhav.info/drjadhav-data_files/Published%20papers/Indian

%20Industrial%20Policy%20Since%201956.pdf [Accessed 15 Aug 2017].

Rittenburg, L. & Tregarthen, T., n.d. Principles of Economics V 1.0. [Online] Available at:

HYPERLINK "https://catalog.flatworldknowledge.com/bookhub/22?e=rittenecon-ch02_s03"

https://catalog.flatworldknowledge.com/bookhub/22?e=rittenecon-ch02_s03 [Accessed 14

August 2017].

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.