Holmes Institute HI5003 Economics: Banking Industry Analysis Report

VerifiedAdded on 2022/10/01

|14

|3429

|20

Report

AI Summary

This report offers a comprehensive analysis of the Australian banking industry, examining its structure, key players, and market dynamics. It delves into ethical issues within the sector, such as misconduct and consumer abuse, and explores the impact of these issues on the Australian economy. The report investigates the causes and consequences of fluctuations in interest rates, applying the concepts of market demand and supply. It also analyzes government policies designed to stabilize the market. The analysis covers the major banks, their market capitalization, and their contribution to the Australian economy. The report utilizes aggregate demand and supply models to explain the industry's economic relationships and the effects of monetary policies. Finally, it evaluates ethical issues and the impact on the financial sector.

System04099

[COMPANY NAME] [Company address]

MBA ASSIGNMENT

[COMPANY NAME] [Company address]

MBA ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction...........................................................................................................................................3

Banking industry...................................................................................................................................3

Market structure of the banking industry...............................................................................................5

Examination of issue regarding the industry on Australian economy....................................................8

Examination of ethical issue..............................................................................................................8

Evaluation of unnecessary fluctuation in interest rates of houses......................................................8

Relevant application of market demand and market supply...................................................................9

Government policies that intervene in market and finally stabilise them.............................................11

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

Introduction...........................................................................................................................................3

Banking industry...................................................................................................................................3

Market structure of the banking industry...............................................................................................5

Examination of issue regarding the industry on Australian economy....................................................8

Examination of ethical issue..............................................................................................................8

Evaluation of unnecessary fluctuation in interest rates of houses......................................................8

Relevant application of market demand and market supply...................................................................9

Government policies that intervene in market and finally stabilise them.............................................11

Conclusion...........................................................................................................................................12

References...........................................................................................................................................13

Introduction

The report brings out a discussion on recent royal commission leading to misconduct in the

banking sector, financial services industry, and superannuation. This report continues

background of Australian banking industry with elaboration of major issues as given below

with how they can be resolved through government policies and law compliance.

Misconducting and the consumer abuse is quite prominent, chronic, long standing, and

profound (Reserve Bank of Australia, 2018). The authorities of royal commission is being

heard as CBA top manager as they have the power to negotiate with issues related to media

release rather than undertaking the case under court enforceable after selling bank`s super

accounts. At last, there is an analysis of affecting issue in regards to the industry on the

economy of Australia. This discussion will carry out a discussion on aggregate demand and

aggregate supply model and its relativity with the banking industry (Reserve Bank of

Australia, 2018).

Banking industry

Banking in Australia is ruled by four main banks named as Westpac banking corporation,

New Zealand banking group, Commonwealth bank of Australia and National Australian

Bank (Reserve Bank of Australia, 2019). Although, there are several banks in the country

with the large number of financial institutional including credit unions, creating societies,

mutual banks that can finally provide banking type services as being described as the deposit

taking institutions. The central bank of Australia is named as “reserve bank of Australia.”

(Cummings, and Wright, 2016).

Several greater banks have their presence where few have retail banking presence. Banks of

Australian government has guaranteed deposits nearly to $250000 per customers against the

banking failures. Under the Banking Act, 1959, it is seen that a licence has to operate through

The report brings out a discussion on recent royal commission leading to misconduct in the

banking sector, financial services industry, and superannuation. This report continues

background of Australian banking industry with elaboration of major issues as given below

with how they can be resolved through government policies and law compliance.

Misconducting and the consumer abuse is quite prominent, chronic, long standing, and

profound (Reserve Bank of Australia, 2018). The authorities of royal commission is being

heard as CBA top manager as they have the power to negotiate with issues related to media

release rather than undertaking the case under court enforceable after selling bank`s super

accounts. At last, there is an analysis of affecting issue in regards to the industry on the

economy of Australia. This discussion will carry out a discussion on aggregate demand and

aggregate supply model and its relativity with the banking industry (Reserve Bank of

Australia, 2018).

Banking industry

Banking in Australia is ruled by four main banks named as Westpac banking corporation,

New Zealand banking group, Commonwealth bank of Australia and National Australian

Bank (Reserve Bank of Australia, 2019). Although, there are several banks in the country

with the large number of financial institutional including credit unions, creating societies,

mutual banks that can finally provide banking type services as being described as the deposit

taking institutions. The central bank of Australia is named as “reserve bank of Australia.”

(Cummings, and Wright, 2016).

Several greater banks have their presence where few have retail banking presence. Banks of

Australian government has guaranteed deposits nearly to $250000 per customers against the

banking failures. Under the Banking Act, 1959, it is seen that a licence has to operate through

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operations in Australia and the Australian foreign corporate bank (Reserve Bank of Australia,

2019). It should comply with religious charitable development banking funds that are exempt

from the requirement of licence. For the last ten years, commonwealth bank is ranked at first

in terms of Bloomberg return riskless with a risk adjustment of 18 percent. These four major

banks hold world`s largest market capitalisation with rank of 25 for the safe banks

(Cummings, and Wright, 2016). The banking sector of Australia is its largest Australian

financial system. It can comprise of 147 authorities for the deposit taking institution that can

collectively hold nearly 55 percent of the assets of the AFI (Australian financial institutions).

History of banking has begun with the prototype banks that are related to merchants of world,

which has made grain loans to the farmers and the traders that carry goods between the cities.

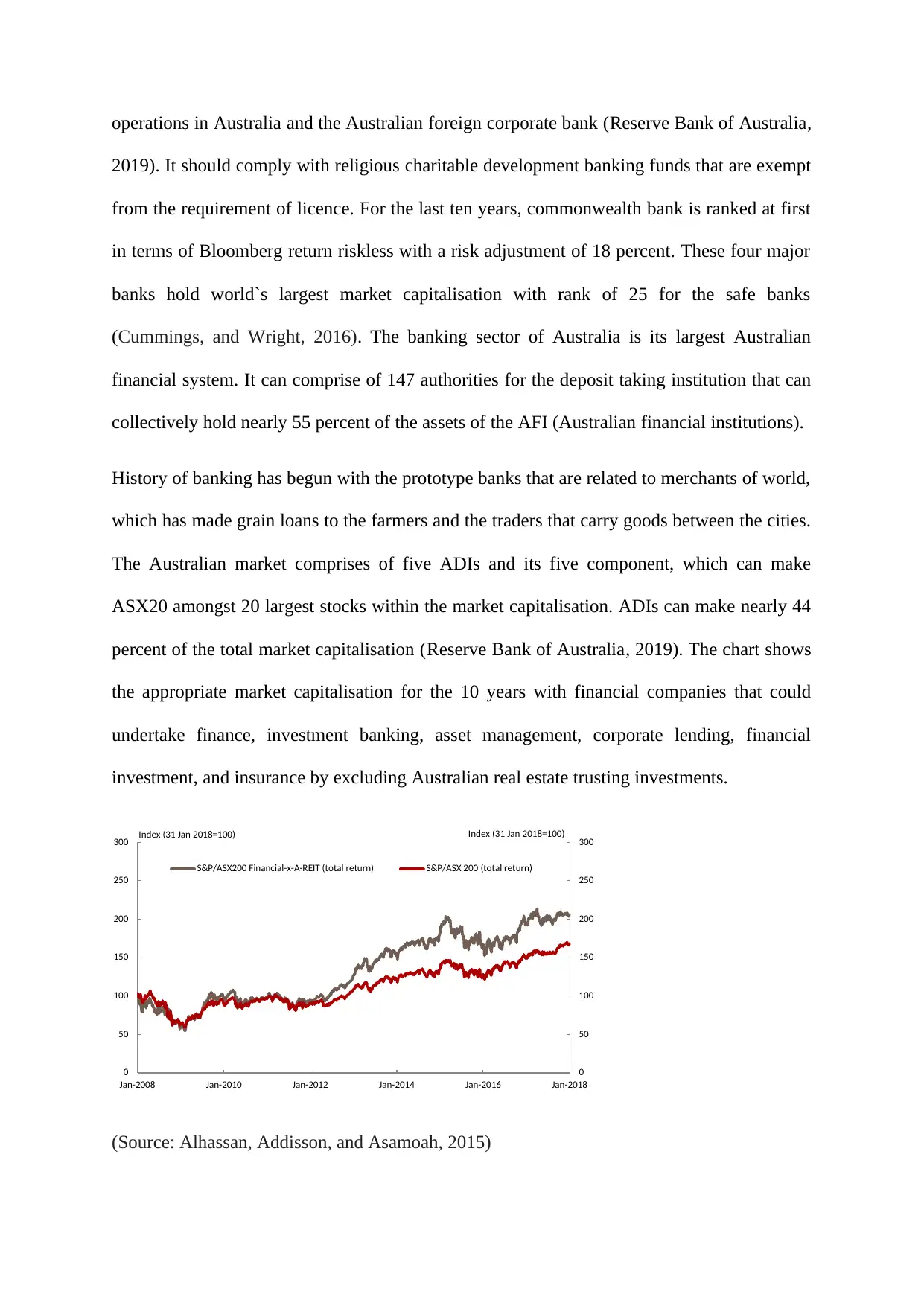

The Australian market comprises of five ADIs and its five component, which can make

ASX20 amongst 20 largest stocks within the market capitalisation. ADIs can make nearly 44

percent of the total market capitalisation (Reserve Bank of Australia, 2019). The chart shows

the appropriate market capitalisation for the 10 years with financial companies that could

undertake finance, investment banking, asset management, corporate lending, financial

investment, and insurance by excluding Australian real estate trusting investments.

0

50

100

150

200

250

300

0

50

100

150

200

250

300

Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018

S&P/ASX200 Financial-x-A-REIT (total return) S&P/ASX 200 (total return)

Index (31 Jan 2018=100) Index (31 Jan 2018=100)

(Source: Alhassan, Addisson, and Asamoah, 2015)

2019). It should comply with religious charitable development banking funds that are exempt

from the requirement of licence. For the last ten years, commonwealth bank is ranked at first

in terms of Bloomberg return riskless with a risk adjustment of 18 percent. These four major

banks hold world`s largest market capitalisation with rank of 25 for the safe banks

(Cummings, and Wright, 2016). The banking sector of Australia is its largest Australian

financial system. It can comprise of 147 authorities for the deposit taking institution that can

collectively hold nearly 55 percent of the assets of the AFI (Australian financial institutions).

History of banking has begun with the prototype banks that are related to merchants of world,

which has made grain loans to the farmers and the traders that carry goods between the cities.

The Australian market comprises of five ADIs and its five component, which can make

ASX20 amongst 20 largest stocks within the market capitalisation. ADIs can make nearly 44

percent of the total market capitalisation (Reserve Bank of Australia, 2019). The chart shows

the appropriate market capitalisation for the 10 years with financial companies that could

undertake finance, investment banking, asset management, corporate lending, financial

investment, and insurance by excluding Australian real estate trusting investments.

0

50

100

150

200

250

300

0

50

100

150

200

250

300

Jan-2008 Jan-2010 Jan-2012 Jan-2014 Jan-2016 Jan-2018

S&P/ASX200 Financial-x-A-REIT (total return) S&P/ASX 200 (total return)

Index (31 Jan 2018=100) Index (31 Jan 2018=100)

(Source: Alhassan, Addisson, and Asamoah, 2015)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is important to calculate profits and return on equity of the ADIs (American depository

investments) derived a net profit of nearly around $35.9 billion in 2017. The major banks of

Australia earn a profit margin of $831 million. International comparison of prices of Australia

bank profits and its relative returns can not undertake different accounting standards and

financial reporting. ADI has substantially contributed to Australian economy. At the end in

2017, ADIs held on $4.6 trillion in regards to assets. Financial with other insurance services

include several financial corporation that is the major contributor to the gross value added to

real industry. It is a measure for healthcare, social services, and construction with

contribution of 8 percent, manufacturing mining contributes to 6 percent to the real industry

as it is added to the real industry valuation (Alhassan, Addisson, and Asamoah, 2015).

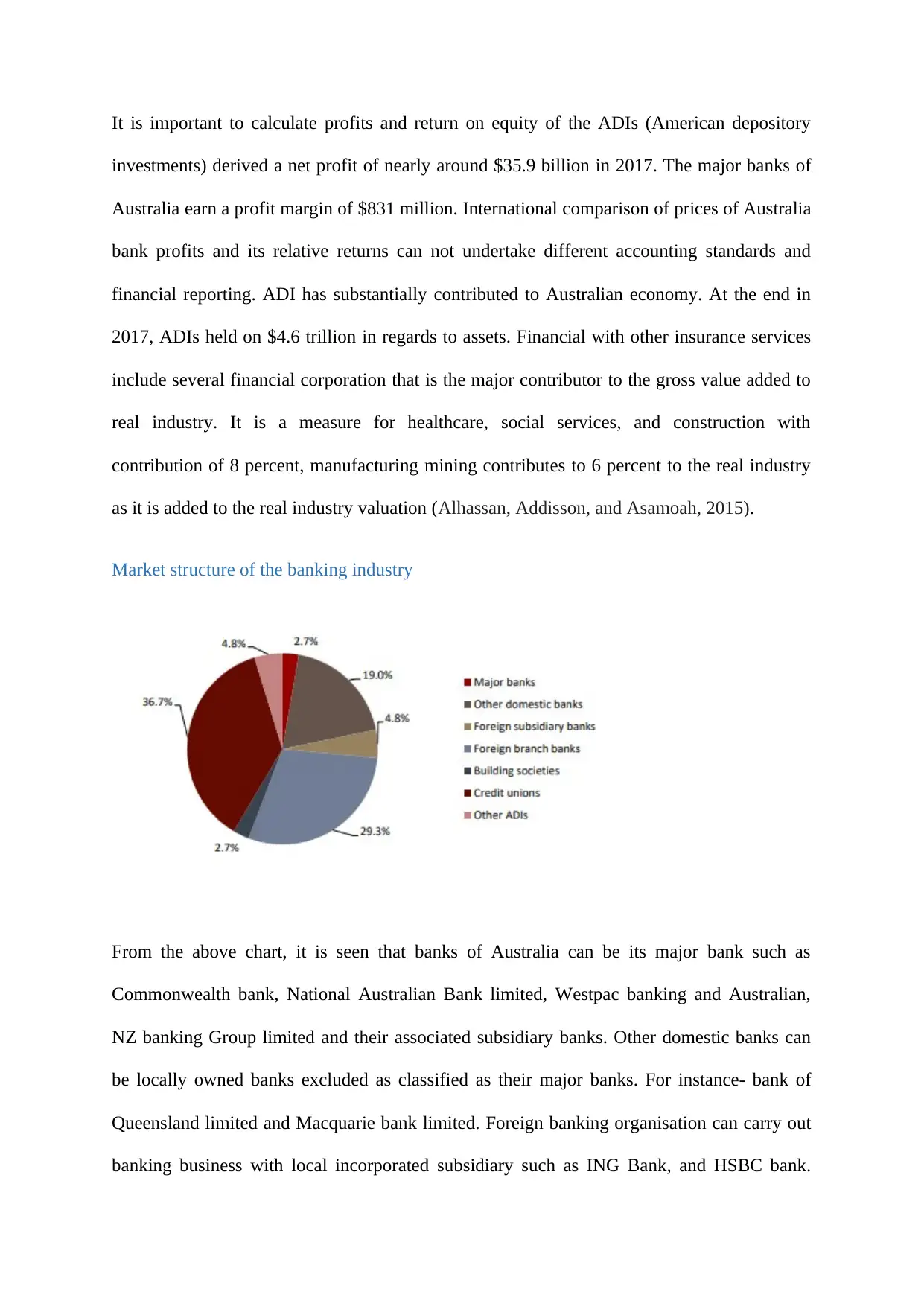

Market structure of the banking industry

From the above chart, it is seen that banks of Australia can be its major bank such as

Commonwealth bank, National Australian Bank limited, Westpac banking and Australian,

NZ banking Group limited and their associated subsidiary banks. Other domestic banks can

be locally owned banks excluded as classified as their major banks. For instance- bank of

Queensland limited and Macquarie bank limited. Foreign banking organisation can carry out

banking business with local incorporated subsidiary such as ING Bank, and HSBC bank.

investments) derived a net profit of nearly around $35.9 billion in 2017. The major banks of

Australia earn a profit margin of $831 million. International comparison of prices of Australia

bank profits and its relative returns can not undertake different accounting standards and

financial reporting. ADI has substantially contributed to Australian economy. At the end in

2017, ADIs held on $4.6 trillion in regards to assets. Financial with other insurance services

include several financial corporation that is the major contributor to the gross value added to

real industry. It is a measure for healthcare, social services, and construction with

contribution of 8 percent, manufacturing mining contributes to 6 percent to the real industry

as it is added to the real industry valuation (Alhassan, Addisson, and Asamoah, 2015).

Market structure of the banking industry

From the above chart, it is seen that banks of Australia can be its major bank such as

Commonwealth bank, National Australian Bank limited, Westpac banking and Australian,

NZ banking Group limited and their associated subsidiary banks. Other domestic banks can

be locally owned banks excluded as classified as their major banks. For instance- bank of

Queensland limited and Macquarie bank limited. Foreign banking organisation can carry out

banking business with local incorporated subsidiary such as ING Bank, and HSBC bank.

Banking industry can handle credit, financial transactions and cash that provides a safe store

to keep the extra cash and the credit. This will help to offer certificates, checking accounts,

and saving account. The structure is believed to be transparent, reliable, and also there are

some relative structural with operation difference as compared to the American system. There

are almost 149 authorised depository institutions in Australia. In the business environment,

majority of banks occupy 80 percent of market and then set models in order to measure the

risk of loan without mattering whether it is a small ADI. The financial service sector has

three main regulators such as reserve bank of India that look at the monetary policies,

responsible institutions named as building societies, banks, credit unions, Australian

securities and the investment commission that will focus on consumer protection and market

integrity.

The market structure of the banking system is related to monopoly where the market is

dominated by four major banks (ANZ bank, commonwealth bank, national Australia bank,

and Westpac). Trade finance liquidity that remains as an issue in the rest of the world.

Monopoly requires where a group of banks dominates the whole economy. Form the point of

view of regulations, monopoly exists as the 75 percent of the Australia`s economy is

dominated by these four banks.

Associated issue

Ethical issue-

Recently, the Australian banking industry has been facing severe challenges as it has been

facing reputation issues as financial industry has misshapen. These days, Australian financial

industry is ranked last in some of its surveys. The Australian banking industry has noticed

that it is expected to pick up through the back of monetary with the fiscal stimuli that is likely

to boost household income with consumer pricing. With compliance of moral standards,

principle, rules, and regulations, which give a sense of professional behaviour. The ethical

to keep the extra cash and the credit. This will help to offer certificates, checking accounts,

and saving account. The structure is believed to be transparent, reliable, and also there are

some relative structural with operation difference as compared to the American system. There

are almost 149 authorised depository institutions in Australia. In the business environment,

majority of banks occupy 80 percent of market and then set models in order to measure the

risk of loan without mattering whether it is a small ADI. The financial service sector has

three main regulators such as reserve bank of India that look at the monetary policies,

responsible institutions named as building societies, banks, credit unions, Australian

securities and the investment commission that will focus on consumer protection and market

integrity.

The market structure of the banking system is related to monopoly where the market is

dominated by four major banks (ANZ bank, commonwealth bank, national Australia bank,

and Westpac). Trade finance liquidity that remains as an issue in the rest of the world.

Monopoly requires where a group of banks dominates the whole economy. Form the point of

view of regulations, monopoly exists as the 75 percent of the Australia`s economy is

dominated by these four banks.

Associated issue

Ethical issue-

Recently, the Australian banking industry has been facing severe challenges as it has been

facing reputation issues as financial industry has misshapen. These days, Australian financial

industry is ranked last in some of its surveys. The Australian banking industry has noticed

that it is expected to pick up through the back of monetary with the fiscal stimuli that is likely

to boost household income with consumer pricing. With compliance of moral standards,

principle, rules, and regulations, which give a sense of professional behaviour. The ethical

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

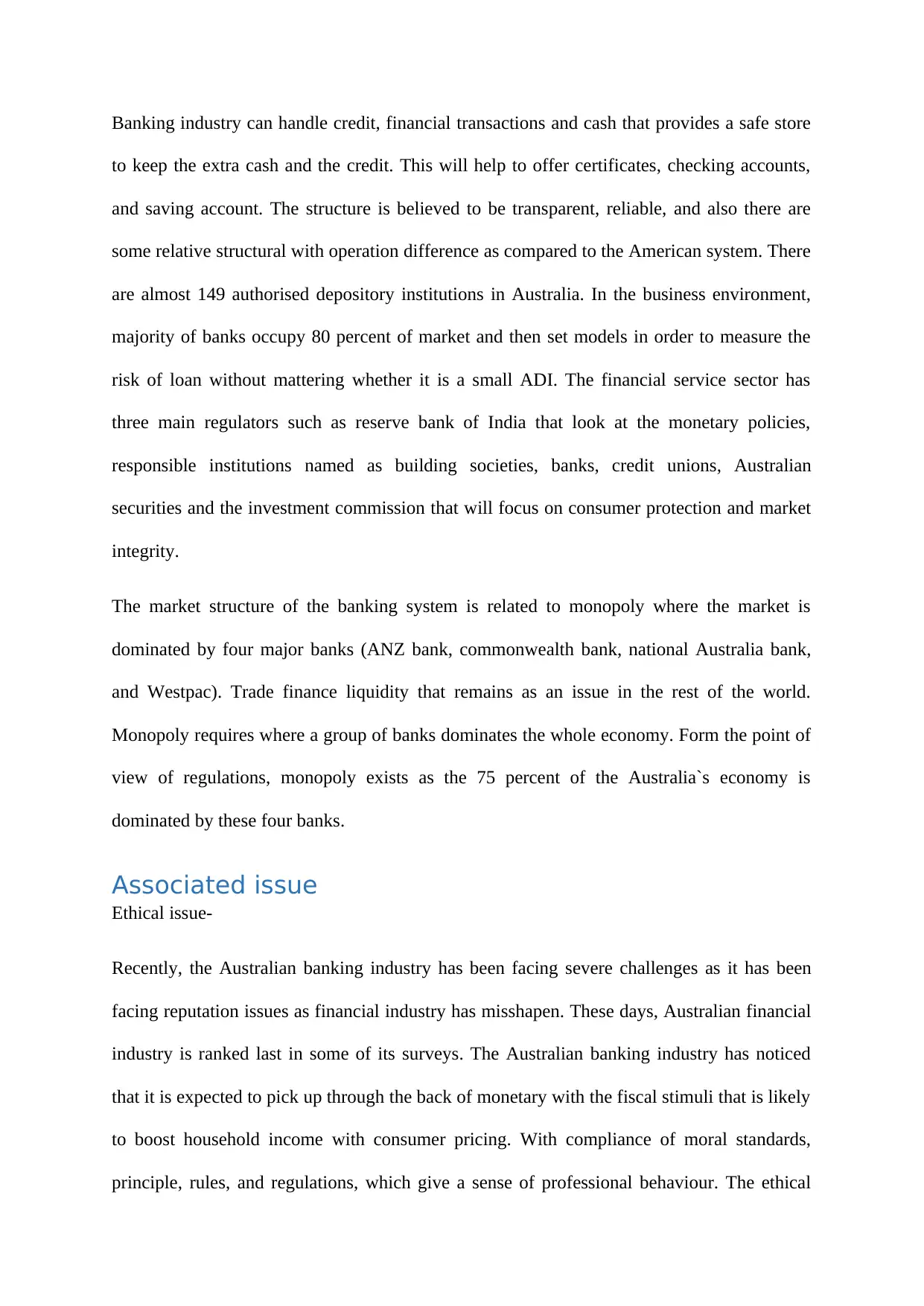

issue relates to unauthorised trading, short selling, credit rating, mis-selling, and bribery

among the top-level management. Australian Prudential regulation Authority, Australian

securities with the investment commission, and the reserve bank of Australia launch a set

banking code of conduct that is an enforceable standards which the consumer, guarantors,

and small businesses expecting from the banks of Australia.

(Source: JACOBS, 2018)

The issue is related to disruption from the innovation strategy including lack of real time

payments with the mobile banking both in terms of threat for the sector. Improvement in

efficiency ratios in regards to the Australian economy, which has certainly slow down the

growth as the curve has been falling down (JACOBS, 2018).

Examination of issue regarding the industry on Australian economy

Examination of ethical issue

RBA (Reserve bank of Australia) has examined that the Australian ethical index has fallen

majorly six points from 41 to 35. The financial and corporate sector faced significant falls.

The governance of Australia points out that index suggests several high profiling scandals

with the alarming company breaches that have undermined confidence (Cassidy, and Kosev,

2015). These big banks had huge customer trust in its operation and advice, which is being

among the top-level management. Australian Prudential regulation Authority, Australian

securities with the investment commission, and the reserve bank of Australia launch a set

banking code of conduct that is an enforceable standards which the consumer, guarantors,

and small businesses expecting from the banks of Australia.

(Source: JACOBS, 2018)

The issue is related to disruption from the innovation strategy including lack of real time

payments with the mobile banking both in terms of threat for the sector. Improvement in

efficiency ratios in regards to the Australian economy, which has certainly slow down the

growth as the curve has been falling down (JACOBS, 2018).

Examination of issue regarding the industry on Australian economy

Examination of ethical issue

RBA (Reserve bank of Australia) has examined that the Australian ethical index has fallen

majorly six points from 41 to 35. The financial and corporate sector faced significant falls.

The governance of Australia points out that index suggests several high profiling scandals

with the alarming company breaches that have undermined confidence (Cassidy, and Kosev,

2015). These big banks had huge customer trust in its operation and advice, which is being

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

eroded by streaming the stories of scandals. The ethics index of Governance institute of

Australia has been dragged by poor perception of ethics in regards to the banking sector.

Almost half of banking, insurance, and finance are considered unethical and only 28 percent

of the cases are ethical (Liu, 2015). Ethically important issue in the banking and finance

industry continues to execute salaries, corruption and bribery issues even in the executive

bonuses (Cassidy, and Kosev, 2015). Australians often think that CEO is paid maximum so

more unethical they think it may be. Nearly three-fourth of people think that they are

unethical when the CEO is paid nearly to $3 million and 50 times higher than the average

Australian income for an year. The most trusted professionals in banking industry are

ambulance officers, fire fighters, and the nurses. The least trusted people are state politicians,

federal politicians, and real estate agent (Liu, 2015).

Evaluation of unnecessary fluctuation in interest rates of houses

The required reduction in interest rate reflect weak performance of the Australia`s economy

in 12 months. With the need of the hour, central bank has noticed that it leads to full

employment, which has shifted, with the number of Australians that started their work with

more increased working hours implying lower unemployment rate leading to get their wages

and rise in the prices. The growth has decreased due to number of reasons such as least

number of productive workforce, slow down economic growth, increased risk of business,

weighted potential recovery in terms of investments, which have resulted into US china trade

dispute. Fall in sizable housing prices in among the two Australian greatest market that

further leads to fall in the new building construction when weakened housing sentiments. It is

the sign of slowing economy evident in terms of household income growth.

Relevant application of market demand and market supply

Aggregate supply is the total quantity of the output, which the organisations will produce and

sell at a certain price level. This curve shows a certain adjusted level of income with relation

Australia has been dragged by poor perception of ethics in regards to the banking sector.

Almost half of banking, insurance, and finance are considered unethical and only 28 percent

of the cases are ethical (Liu, 2015). Ethically important issue in the banking and finance

industry continues to execute salaries, corruption and bribery issues even in the executive

bonuses (Cassidy, and Kosev, 2015). Australians often think that CEO is paid maximum so

more unethical they think it may be. Nearly three-fourth of people think that they are

unethical when the CEO is paid nearly to $3 million and 50 times higher than the average

Australian income for an year. The most trusted professionals in banking industry are

ambulance officers, fire fighters, and the nurses. The least trusted people are state politicians,

federal politicians, and real estate agent (Liu, 2015).

Evaluation of unnecessary fluctuation in interest rates of houses

The required reduction in interest rate reflect weak performance of the Australia`s economy

in 12 months. With the need of the hour, central bank has noticed that it leads to full

employment, which has shifted, with the number of Australians that started their work with

more increased working hours implying lower unemployment rate leading to get their wages

and rise in the prices. The growth has decreased due to number of reasons such as least

number of productive workforce, slow down economic growth, increased risk of business,

weighted potential recovery in terms of investments, which have resulted into US china trade

dispute. Fall in sizable housing prices in among the two Australian greatest market that

further leads to fall in the new building construction when weakened housing sentiments. It is

the sign of slowing economy evident in terms of household income growth.

Relevant application of market demand and market supply

Aggregate supply is the total quantity of the output, which the organisations will produce and

sell at a certain price level. This curve shows a certain adjusted level of income with relation

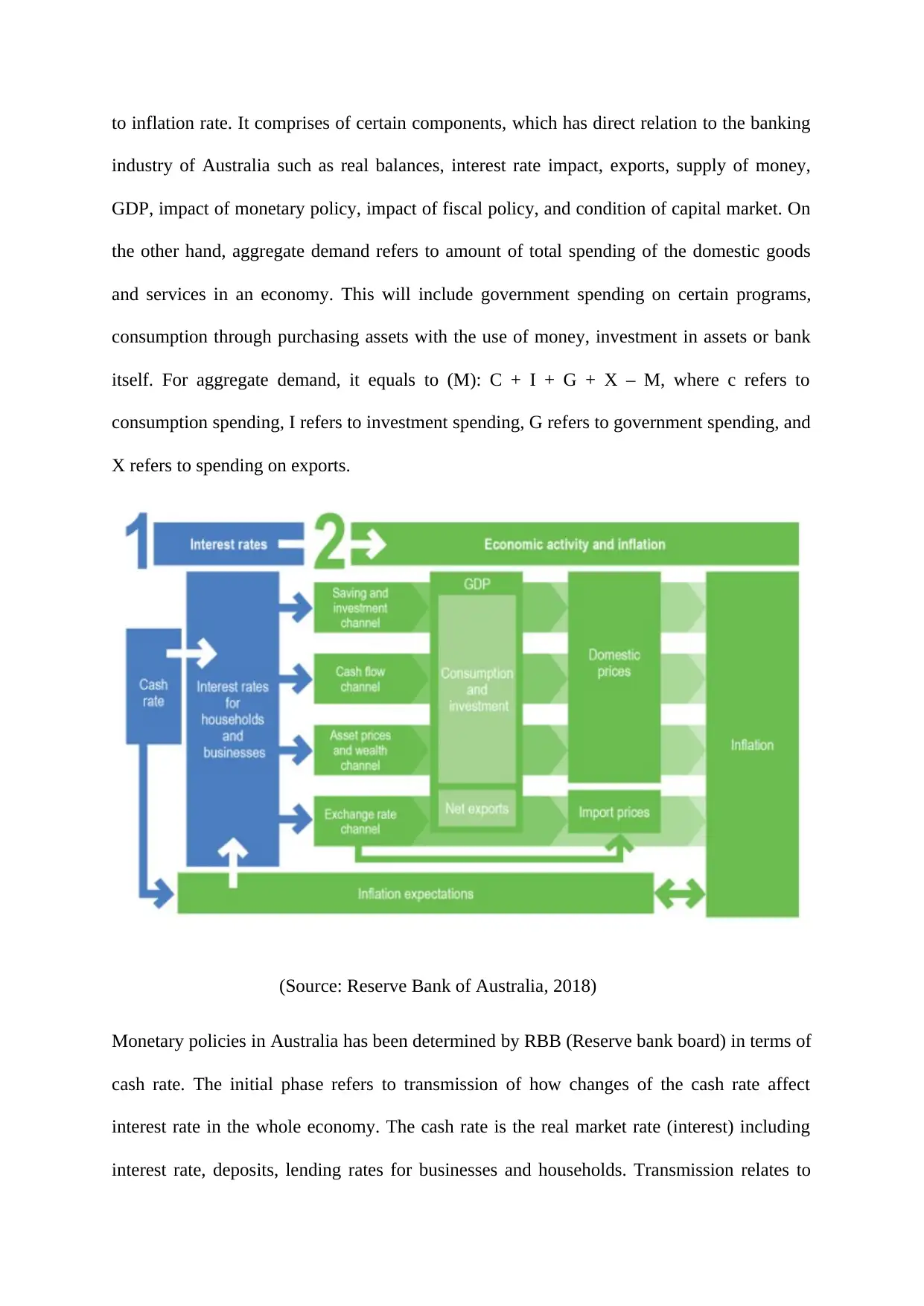

to inflation rate. It comprises of certain components, which has direct relation to the banking

industry of Australia such as real balances, interest rate impact, exports, supply of money,

GDP, impact of monetary policy, impact of fiscal policy, and condition of capital market. On

the other hand, aggregate demand refers to amount of total spending of the domestic goods

and services in an economy. This will include government spending on certain programs,

consumption through purchasing assets with the use of money, investment in assets or bank

itself. For aggregate demand, it equals to (M): C + I + G + X – M, where c refers to

consumption spending, I refers to investment spending, G refers to government spending, and

X refers to spending on exports.

(Source: Reserve Bank of Australia, 2018)

Monetary policies in Australia has been determined by RBB (Reserve bank board) in terms of

cash rate. The initial phase refers to transmission of how changes of the cash rate affect

interest rate in the whole economy. The cash rate is the real market rate (interest) including

interest rate, deposits, lending rates for businesses and households. Transmission relates to

industry of Australia such as real balances, interest rate impact, exports, supply of money,

GDP, impact of monetary policy, impact of fiscal policy, and condition of capital market. On

the other hand, aggregate demand refers to amount of total spending of the domestic goods

and services in an economy. This will include government spending on certain programs,

consumption through purchasing assets with the use of money, investment in assets or bank

itself. For aggregate demand, it equals to (M): C + I + G + X – M, where c refers to

consumption spending, I refers to investment spending, G refers to government spending, and

X refers to spending on exports.

(Source: Reserve Bank of Australia, 2018)

Monetary policies in Australia has been determined by RBB (Reserve bank board) in terms of

cash rate. The initial phase refers to transmission of how changes of the cash rate affect

interest rate in the whole economy. The cash rate is the real market rate (interest) including

interest rate, deposits, lending rates for businesses and households. Transmission relates to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

change in the interest rate affecting economic inflation and activity. The central bank can host

inflation expectation increasing the confidence of business while making decisions regarding

decision and saving the investment as uncertainty is reduced. It is important to understand

that there are several channels defined in aggregate demand and aggregate supply such as

saving and investment channel, asset pricing and wealth management, cash flow model and

the exchange rate channel (Alhassan, Addisson, and Asamoah, 2015).

Interest rate affect economic activity to change the incentive for investment and saving. This

channel affects housing investment, business investment and the consumption. A decrease in

deposit rates has reduced the incentive for our households. Lower lending rates can lead to

the encouragement to increase the borrowing, which face lower repayments as lower lending

rate can support huge demand for the housing assets. Interest rate can affect the decision of

the household by changing the amount of the cash available on services and goods

(Mortimer, Neale, Hasan, and Dunphy, 2015). Reduction in the lending rates has reduced the

interest repayment on debt, business to spend on services and goods, and raised amount of

cash available for businesses and household to spend on the goods. Asset price with the

people`s wealth impact can borrow and how will it spend in economy. The asset price with

people wealth impact with how they can borrow and how these can spend in the economy.

Low interest rate can support asset price by motivating demand for assets. A reason can be

due to present discounted value of future income, which is higher when interest rate is lower

(Pham, Anderson, Duong, and Lajbcygier, 2018).

Government policies that intervene in market and finally stabilise them

There is an established between government and businesses in Australia as being examined

with the consideration of availing stable set of rules for organisation to act within and adapt

to the changing situations (Salim, Arjomandi, and Seufert, 2016). Government has attempted

with an achievement to step certain changes with usage of independent task forces, which has

inflation expectation increasing the confidence of business while making decisions regarding

decision and saving the investment as uncertainty is reduced. It is important to understand

that there are several channels defined in aggregate demand and aggregate supply such as

saving and investment channel, asset pricing and wealth management, cash flow model and

the exchange rate channel (Alhassan, Addisson, and Asamoah, 2015).

Interest rate affect economic activity to change the incentive for investment and saving. This

channel affects housing investment, business investment and the consumption. A decrease in

deposit rates has reduced the incentive for our households. Lower lending rates can lead to

the encouragement to increase the borrowing, which face lower repayments as lower lending

rate can support huge demand for the housing assets. Interest rate can affect the decision of

the household by changing the amount of the cash available on services and goods

(Mortimer, Neale, Hasan, and Dunphy, 2015). Reduction in the lending rates has reduced the

interest repayment on debt, business to spend on services and goods, and raised amount of

cash available for businesses and household to spend on the goods. Asset price with the

people`s wealth impact can borrow and how will it spend in economy. The asset price with

people wealth impact with how they can borrow and how these can spend in the economy.

Low interest rate can support asset price by motivating demand for assets. A reason can be

due to present discounted value of future income, which is higher when interest rate is lower

(Pham, Anderson, Duong, and Lajbcygier, 2018).

Government policies that intervene in market and finally stabilise them

There is an established between government and businesses in Australia as being examined

with the consideration of availing stable set of rules for organisation to act within and adapt

to the changing situations (Salim, Arjomandi, and Seufert, 2016). Government has attempted

with an achievement to step certain changes with usage of independent task forces, which has

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

examined technological progression (Pham, Anderson, Duong, and Lajbcygier, 2018). The

challenge is related to development of rulers and regulation, which would avail stable to

operate within the strategy. The government authorities should comply with policies relating

to code of conduct as seen by the reserve bank board members. This will recognise the role

while maintaining the reputation for integrity and the propriety in each respect to which they

will have to agree (Salim, Arjomandi, and Seufert, 2016). Payment system board will find the

role of maintaining the reputation of bank for all the respects and agreeing to the code of

conduct. Staff is responsible for conduction of code of conduct with high level of integrity to

achieve excellence, perform well, and promote interest. The reserve bank ensures that they

meet compliance related to Australia`s competition laws (Pham, Anderson, Duong, and

Lajbcygier, 2018).

Conclusion

Australia’s banking industry has been emerging from GFC as it emerged as strong position.

The reputation was enhanced but at the same time, it faces challenges in making of the

policies as being related to cost with the stability of funds, implementation of the

international reformation, and the enhancement of consumer welfare. It is important to

maintain a competitiveness as it will help the banks to gain welfare profits in any of the

market. Competition is the main cornerstone of the related to efficiency. Competition need to

become more balanced with the maintenance of stability. There is safe and stable banking

system as it is one of the important component of the economic infrastructure. From the

above discussion, it is seen that policy maker and government look forward to work with

industry to meet several challenges, where the customers are facing ethical issue and

implementation is related to government reform package as being announced. The greater fall

in the housing prices that are coincided with an extended period of weakened household

income, level that is quite weighing in terms of consumer spending.

challenge is related to development of rulers and regulation, which would avail stable to

operate within the strategy. The government authorities should comply with policies relating

to code of conduct as seen by the reserve bank board members. This will recognise the role

while maintaining the reputation for integrity and the propriety in each respect to which they

will have to agree (Salim, Arjomandi, and Seufert, 2016). Payment system board will find the

role of maintaining the reputation of bank for all the respects and agreeing to the code of

conduct. Staff is responsible for conduction of code of conduct with high level of integrity to

achieve excellence, perform well, and promote interest. The reserve bank ensures that they

meet compliance related to Australia`s competition laws (Pham, Anderson, Duong, and

Lajbcygier, 2018).

Conclusion

Australia’s banking industry has been emerging from GFC as it emerged as strong position.

The reputation was enhanced but at the same time, it faces challenges in making of the

policies as being related to cost with the stability of funds, implementation of the

international reformation, and the enhancement of consumer welfare. It is important to

maintain a competitiveness as it will help the banks to gain welfare profits in any of the

market. Competition is the main cornerstone of the related to efficiency. Competition need to

become more balanced with the maintenance of stability. There is safe and stable banking

system as it is one of the important component of the economic infrastructure. From the

above discussion, it is seen that policy maker and government look forward to work with

industry to meet several challenges, where the customers are facing ethical issue and

implementation is related to government reform package as being announced. The greater fall

in the housing prices that are coincided with an extended period of weakened household

income, level that is quite weighing in terms of consumer spending.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.