Economics for Business: Decision Making Assignment, University Name

VerifiedAdded on 2020/03/13

|14

|1681

|47

Homework Assignment

AI Summary

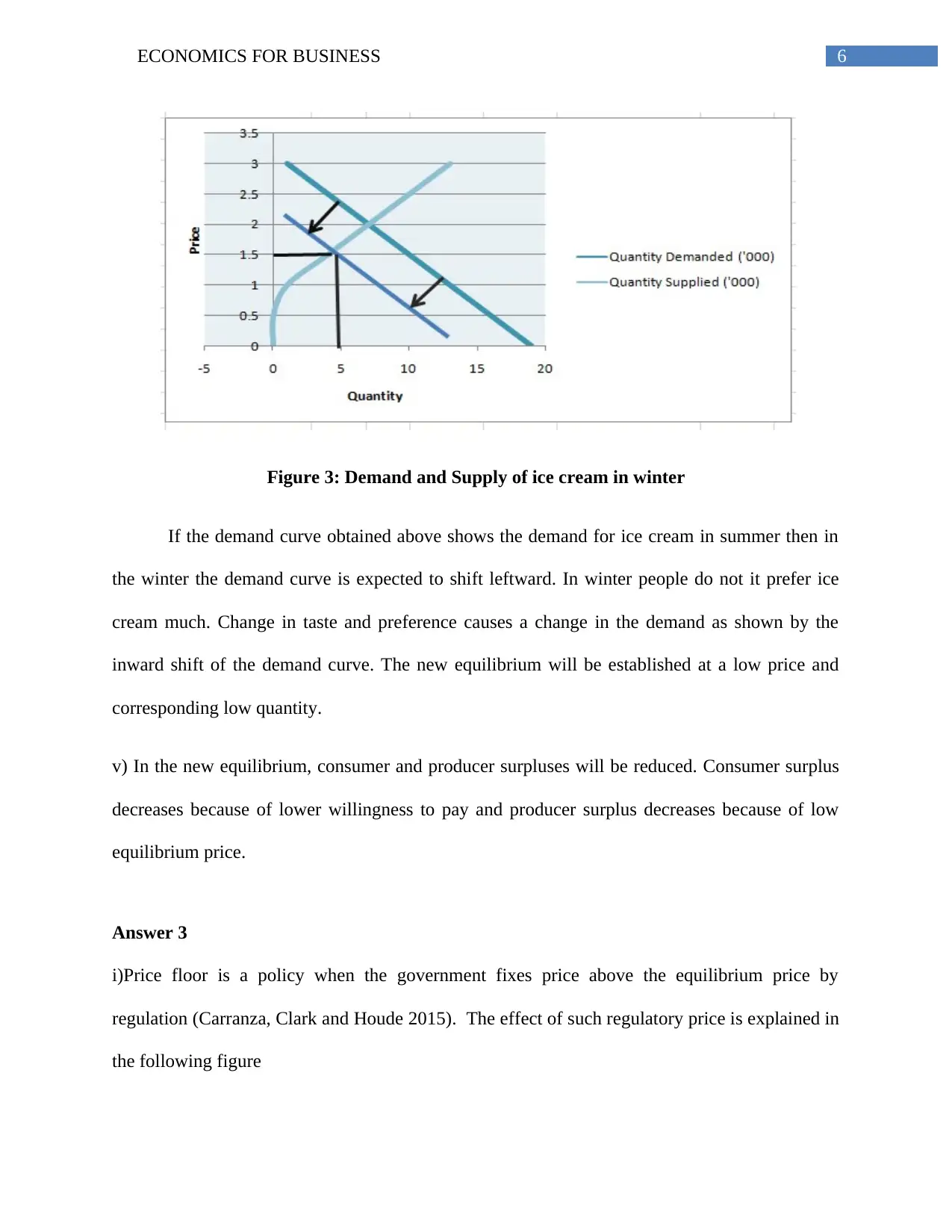

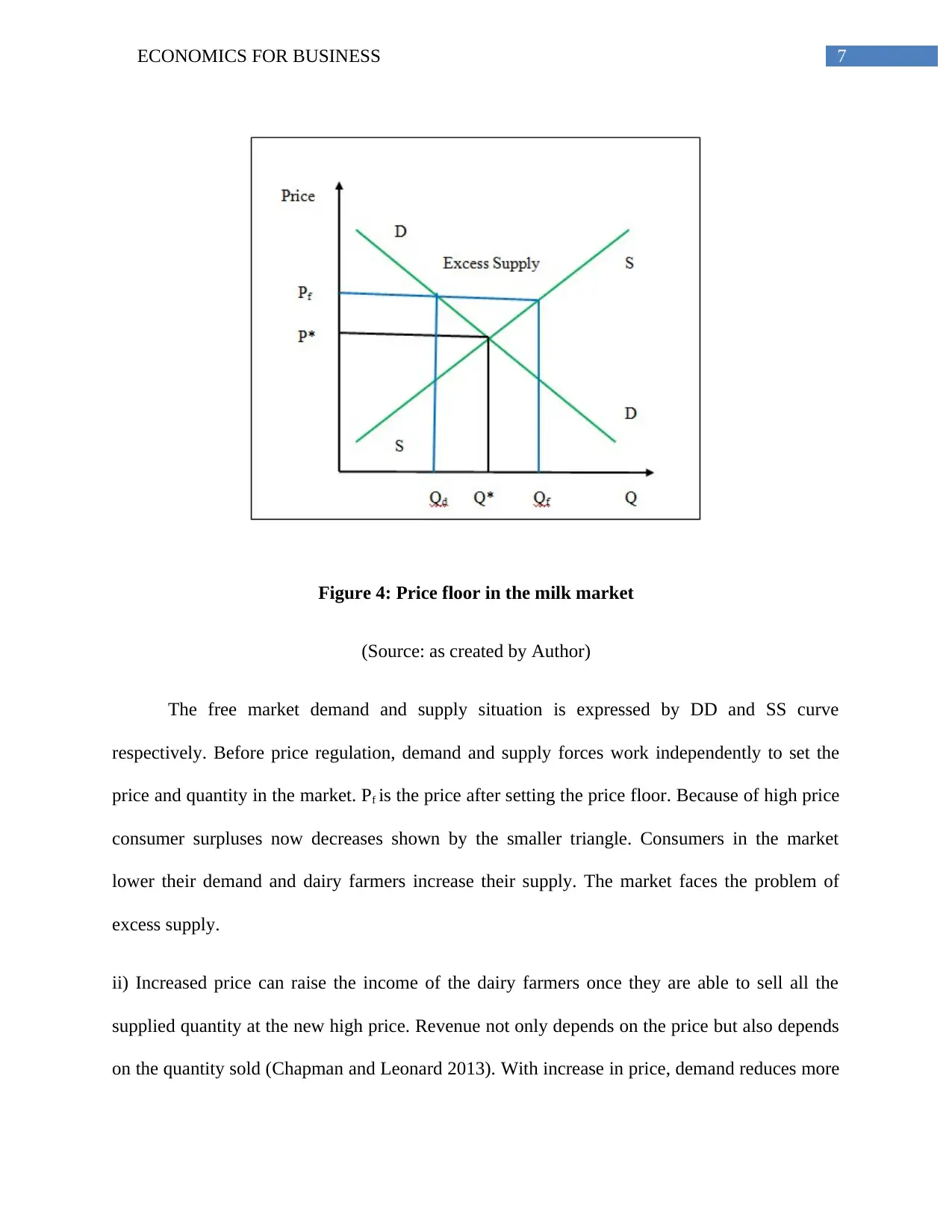

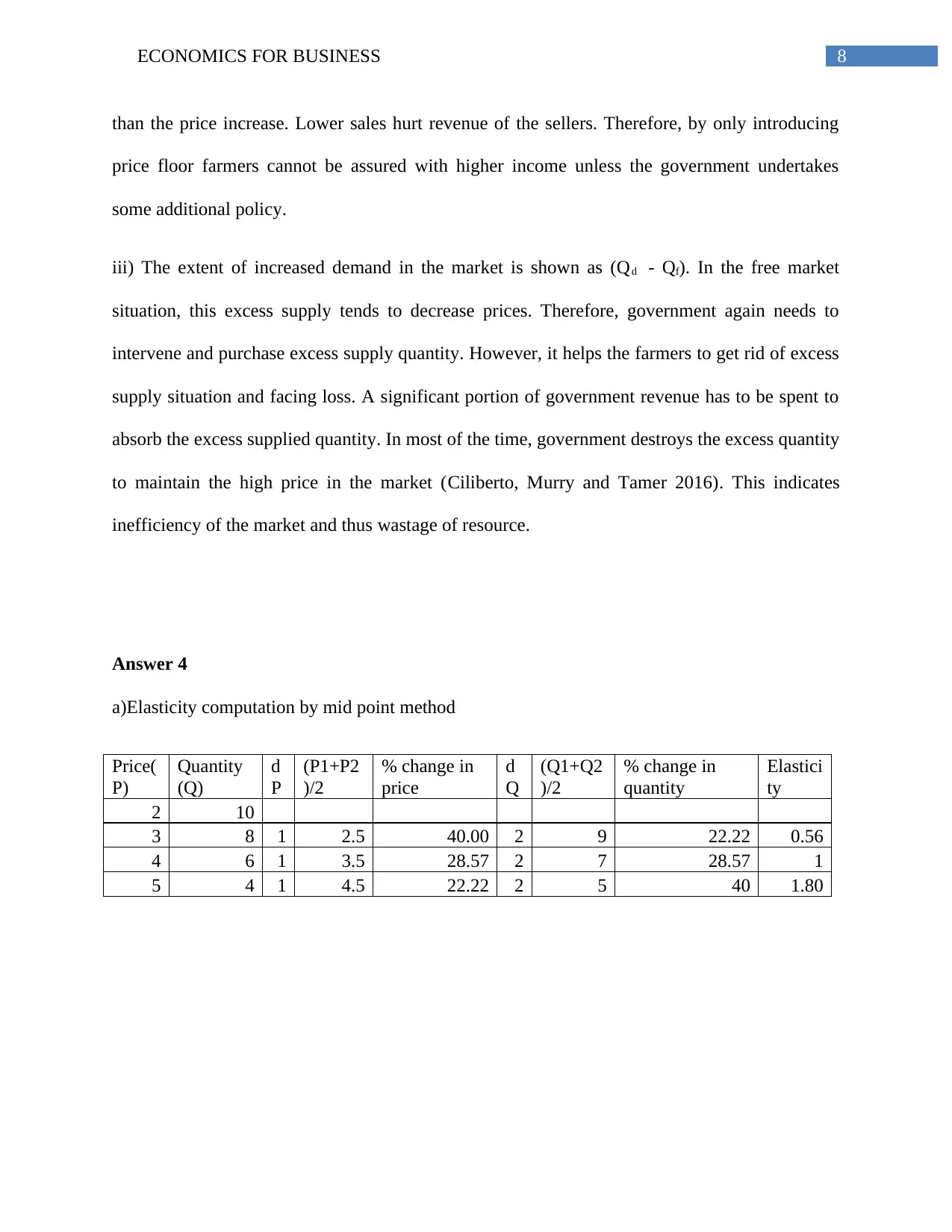

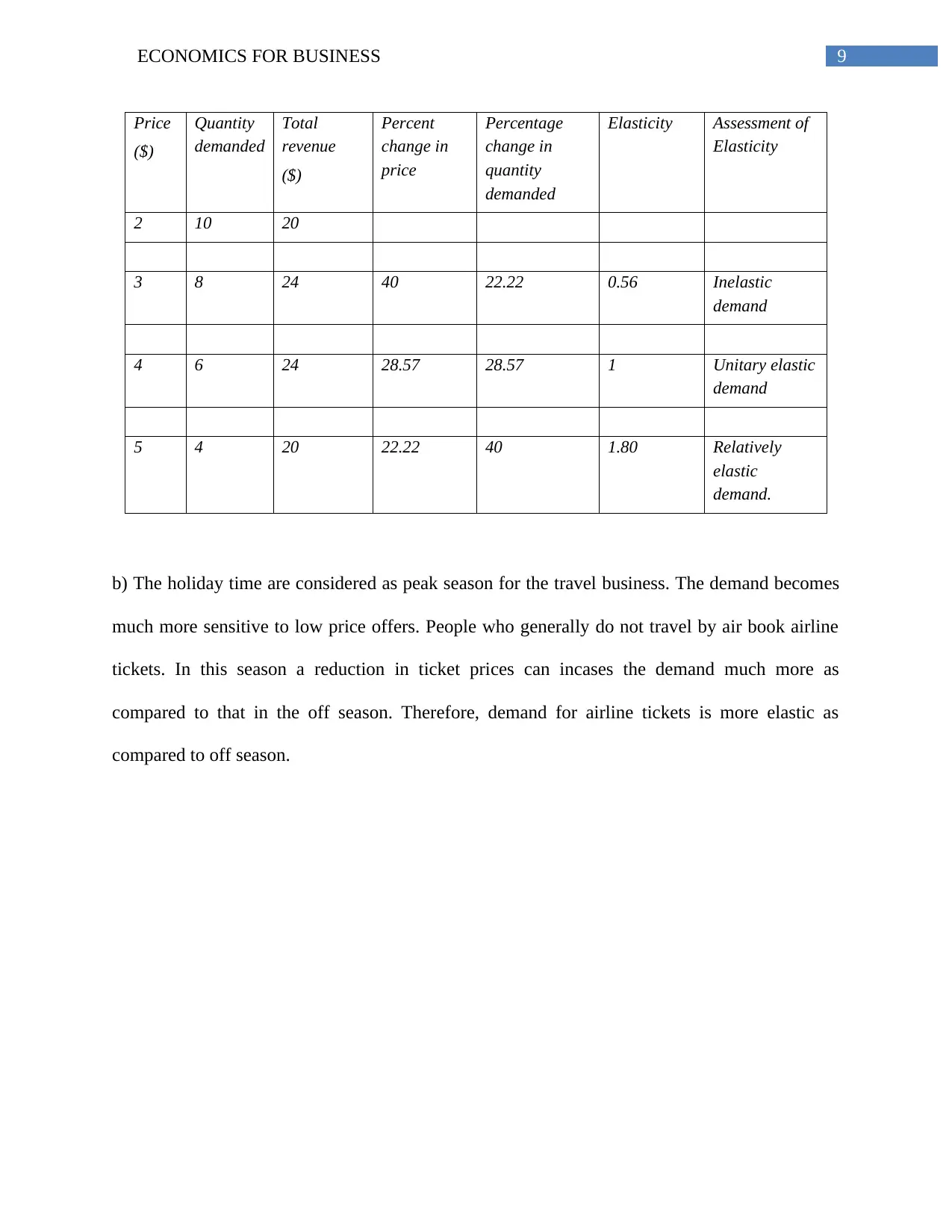

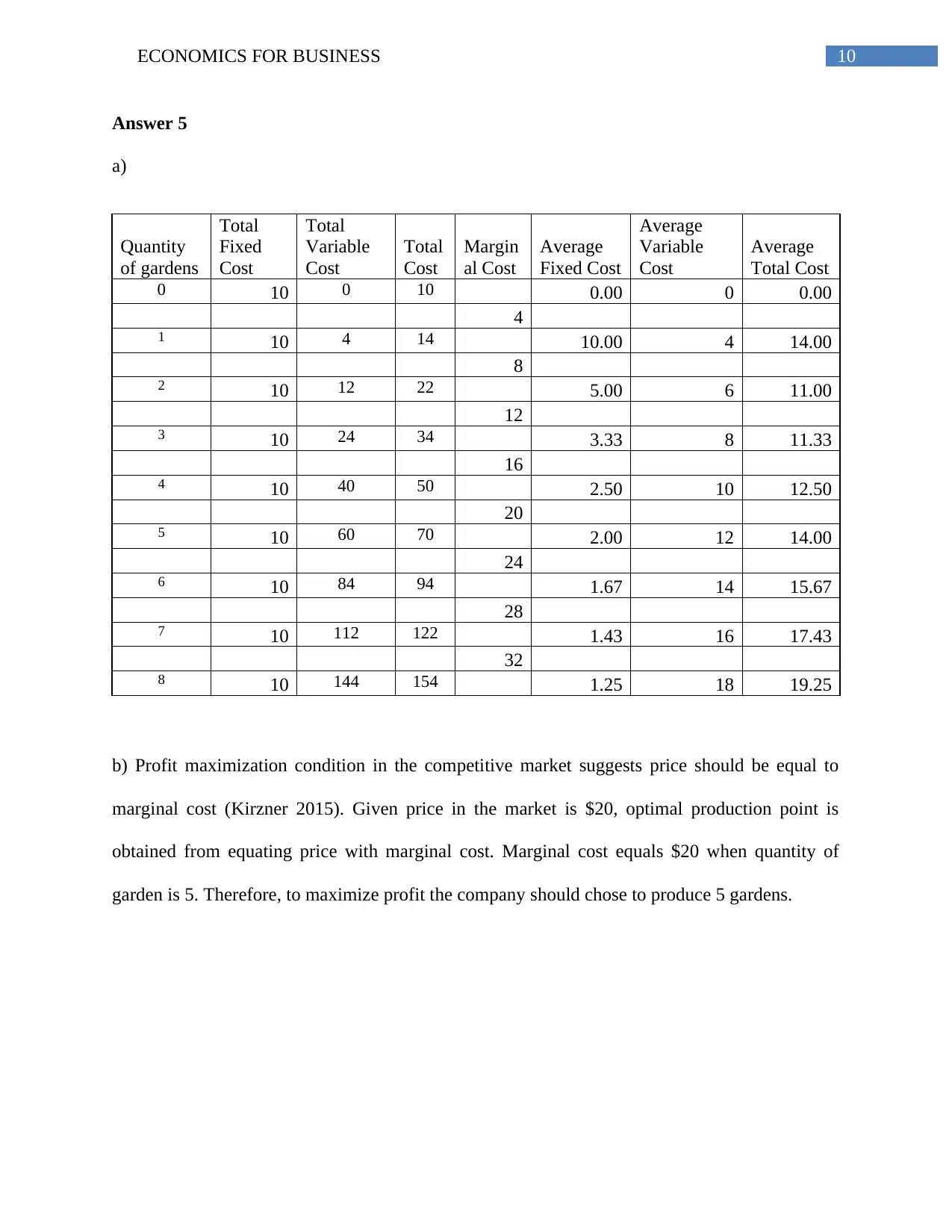

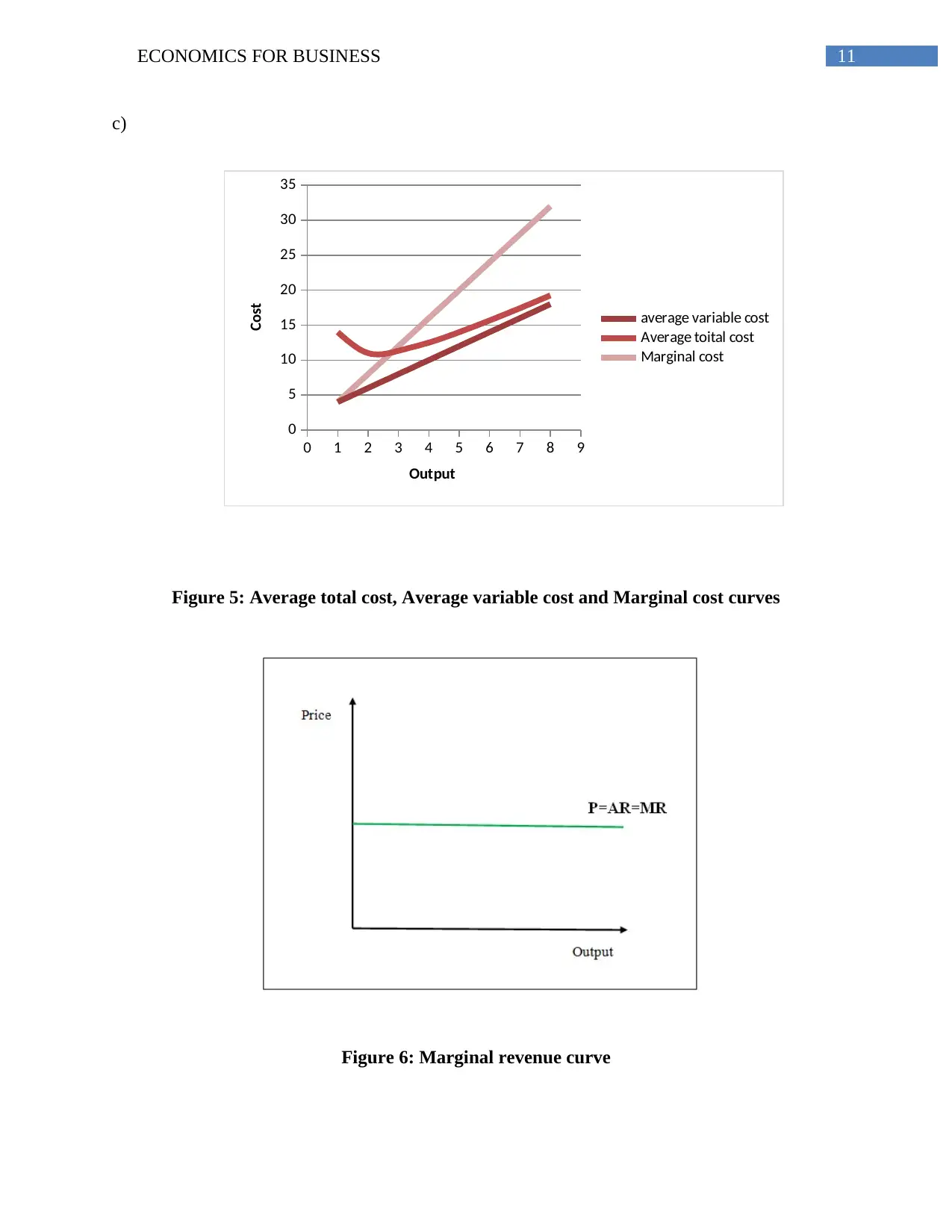

This economics assignment solution covers fundamental concepts in business economics, including the production possibility frontier and its concave shape, explaining opportunity cost. It defines scarcity in economic terms and its implications. The solution analyzes supply and demand dynamics, equilibrium price and quantity, consumer and producer surplus, and the impact of shifts in demand. It examines price floors, their effects on market equilibrium, and the potential for excess supply. Furthermore, the assignment calculates price elasticity using the midpoint method and assesses demand elasticity in different scenarios, like peak seasons. Finally, it explores cost analysis, including total, fixed, variable, and marginal costs, and determines the profit-maximizing production level in a competitive market, relating price to marginal cost. The assignment utilizes figures and tables to illustrate key concepts.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.