Economics Assignment: Output and Costs, Perfect Competition, Monopoly

VerifiedAdded on 2021/12/28

|11

|1487

|54

Homework Assignment

AI Summary

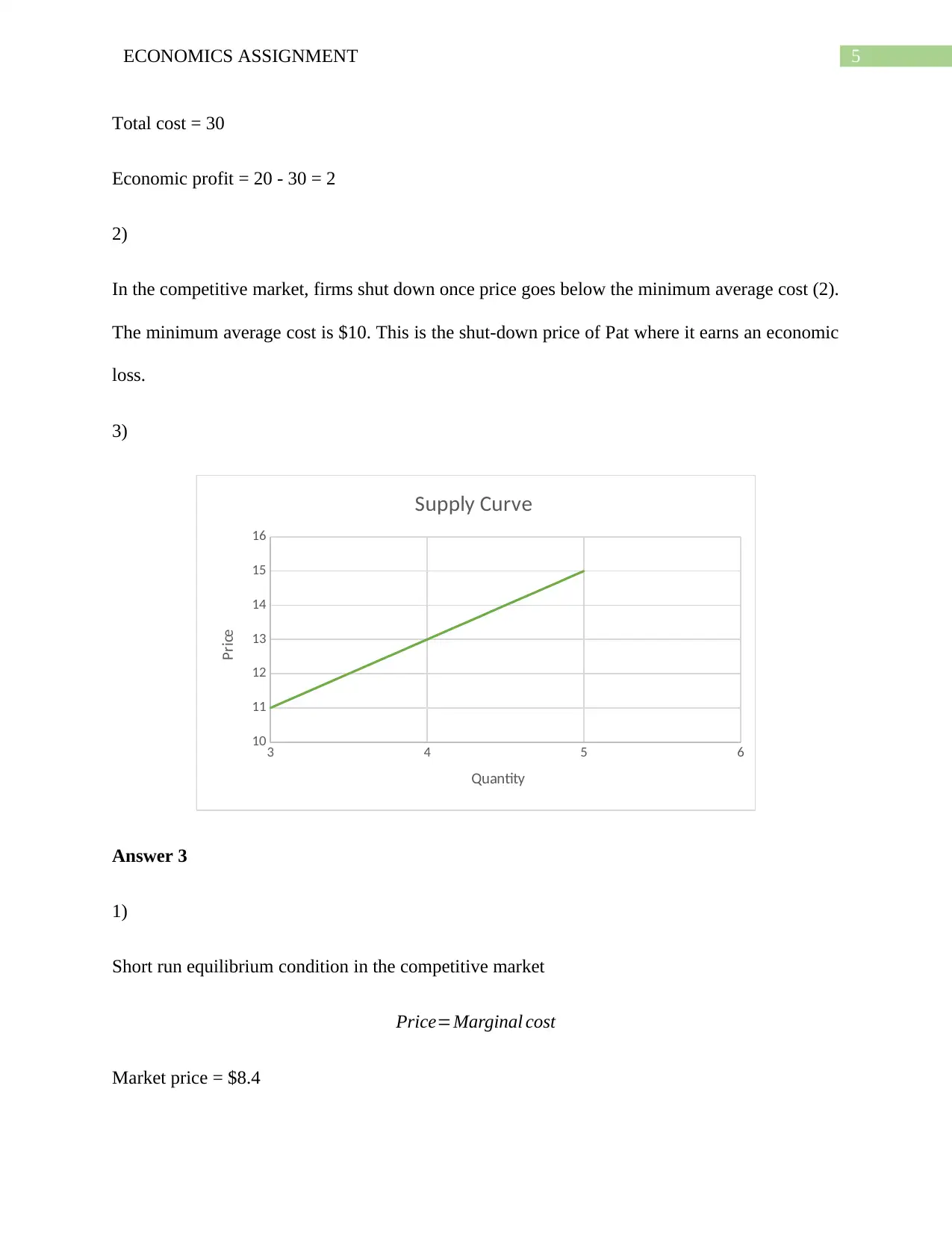

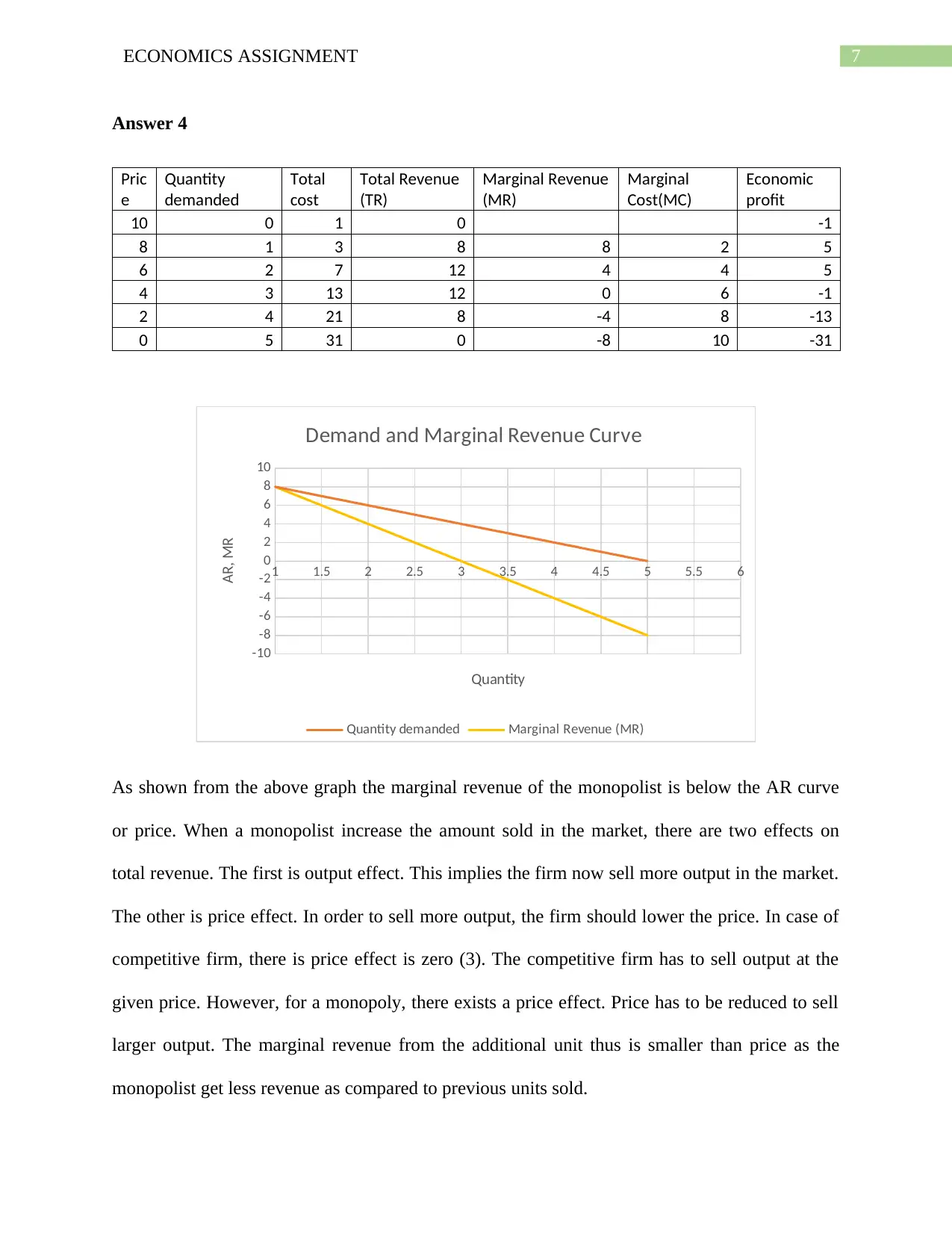

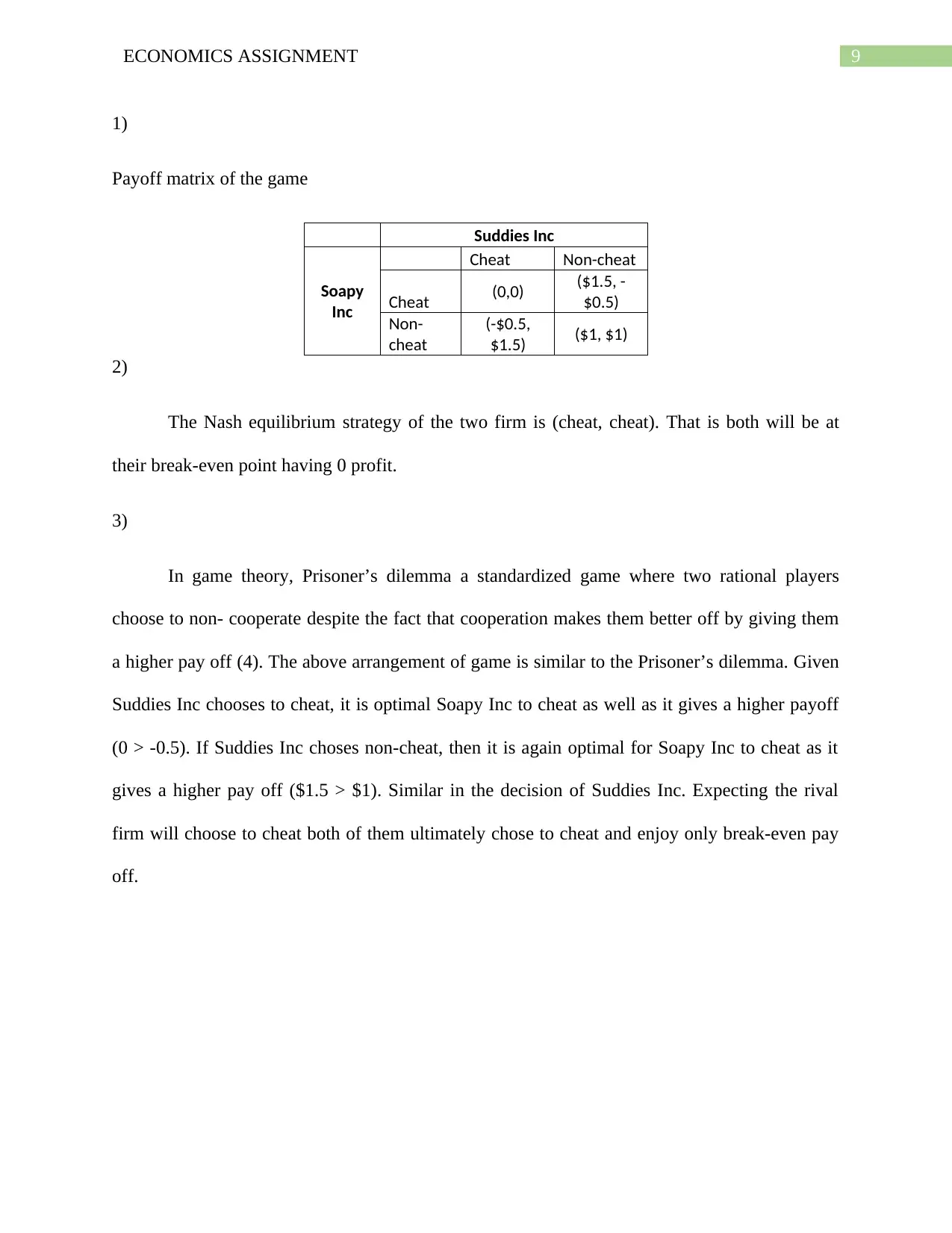

This economics assignment delves into several key microeconomic concepts. It begins by analyzing output and costs, including the calculation of total variable cost, total fixed cost, total cost, average total cost, average fixed cost, average variable cost, and marginal cost. The assignment then explores market structures, starting with perfect competition, examining profit maximization, and shutdown decisions. The analysis continues with monopoly and monopolistic competition, addressing marginal revenue, profit maximization, and the impact of new firms. Finally, the assignment investigates oligopoly, including payoff matrices, Nash equilibrium, and the application of the Prisoner's Dilemma. The assignment provides detailed calculations, graphical interpretations, and explanations of economic principles.

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.