Economics Assignment: Externalities, Elasticity, and Market Analysis

VerifiedAdded on 2023/04/20

|16

|2297

|441

Homework Assignment

AI Summary

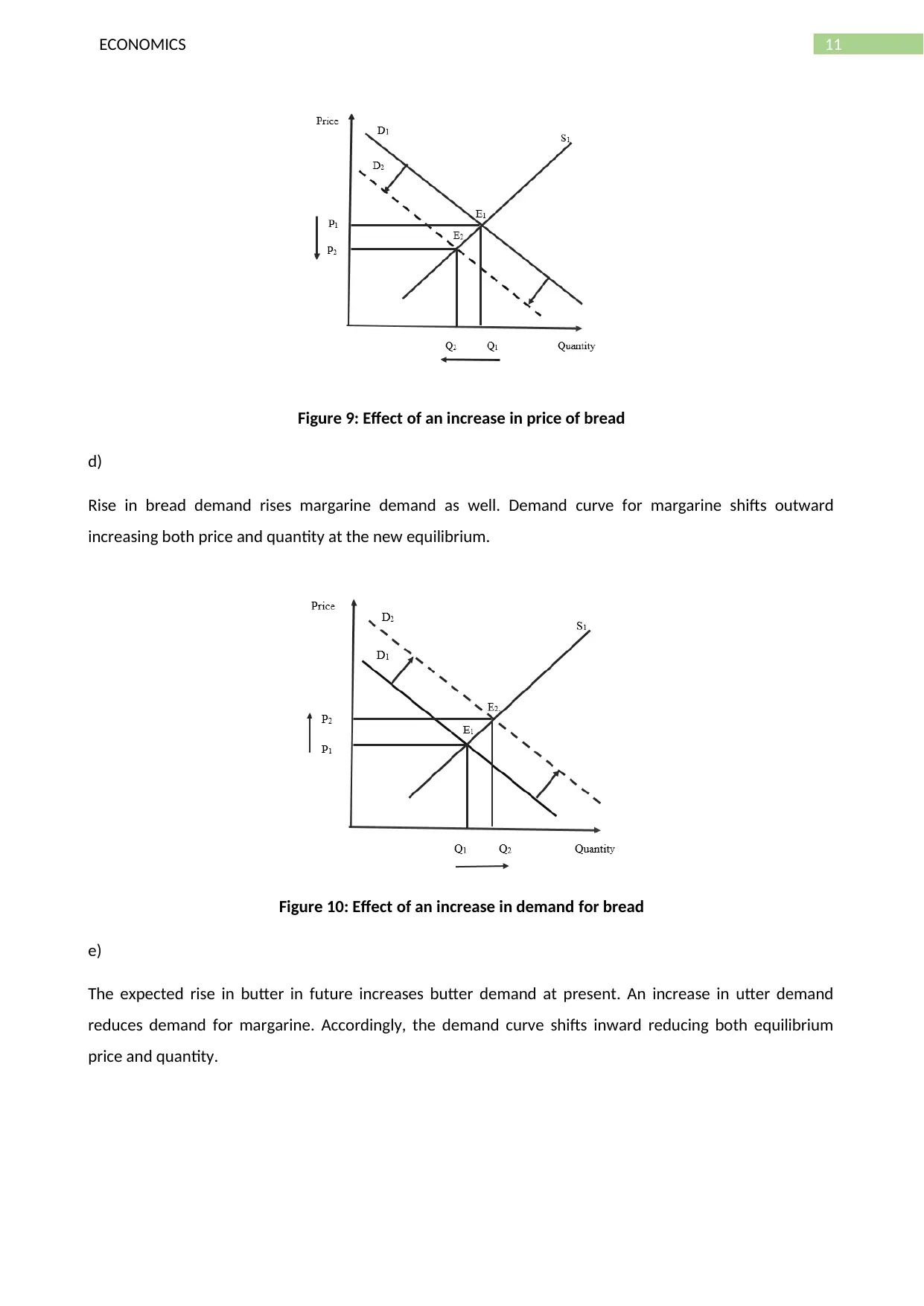

This economics assignment delves into several key concepts within the field. It begins by examining the impact of external costs and benefits on resource allocation, exploring how these externalities lead to market inefficiencies. The assignment then explores elasticity of demand, calculating price elasticity and analyzing its implications on total revenue. Further, it analyzes the characteristics of public and private goods. The assignment also covers cost analysis, differentiating between fixed and variable costs, and calculating average and marginal costs. Finally, it compares allocative efficiency in perfectly competitive markets and monopolies, and analyzes the effects of various market changes such as changes in supply and demand. The assignment provides a comprehensive analysis of these topics, offering a solid foundation in microeconomic principles. This document is contributed by a student to be published on the website Desklib, a platform which provides all the necessary AI based study tools for students.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.