ECON 2 Assignment: Price Elasticity, Market, Growth, and Inflation

VerifiedAdded on 2022/10/01

|11

|2948

|22

Homework Assignment

AI Summary

This economics assignment delves into four core economic theories: price elasticity of demand, market theory, economic growth, and the theory of inflation. The assignment begins by exploring price elasticity, advising a pharmaceutical company on pricing strategies for a new drug based on different elasticity values (1.4, 0.6, and 1). The second question analyzes market theory, focusing on the dynamics of perfect competition, the impact of economic profits and losses, and the effects of new firms entering or exiting the market in the long run. The third question examines economic growth theory, highlighting the roles of physical capital, human capital, and technology in driving economic growth, with a focus on GDP per capita and comparisons between high, middle, and low-income countries. Finally, the assignment concludes with an analysis of inflation, explaining how the consumer price index (CPI) is calculated and used to measure inflation rates over time. The student provides detailed explanations, supporting evidence, and diagrams to illustrate these economic concepts.

ECONOMICS 1

Principles of Economics

Student Name

Course

Professor’s Name

University

City

Date

Principles of Economics

Student Name

Course

Professor’s Name

University

City

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 2

Question 1: Price Elasticity of Demand theory

The question relates to the price elasticity of demand theory. The coefficient of price

elasticity of demand is computed by dividing the percentage change in the quantity of goods that

the consumers demand by the respective proportion variations in their prices as given in the

following formulae (Jawad et al. 2018 p. 693). Price elasticity of demand (Ped) = (Q2-Q1/ P2-

P1)*100. Provided that variations in the prices and quantity are inversely related, the minus sign

is ignored. Therefore, a point of interest is the co-efficient of elasticity of demand as opposed to

the resultant sign.

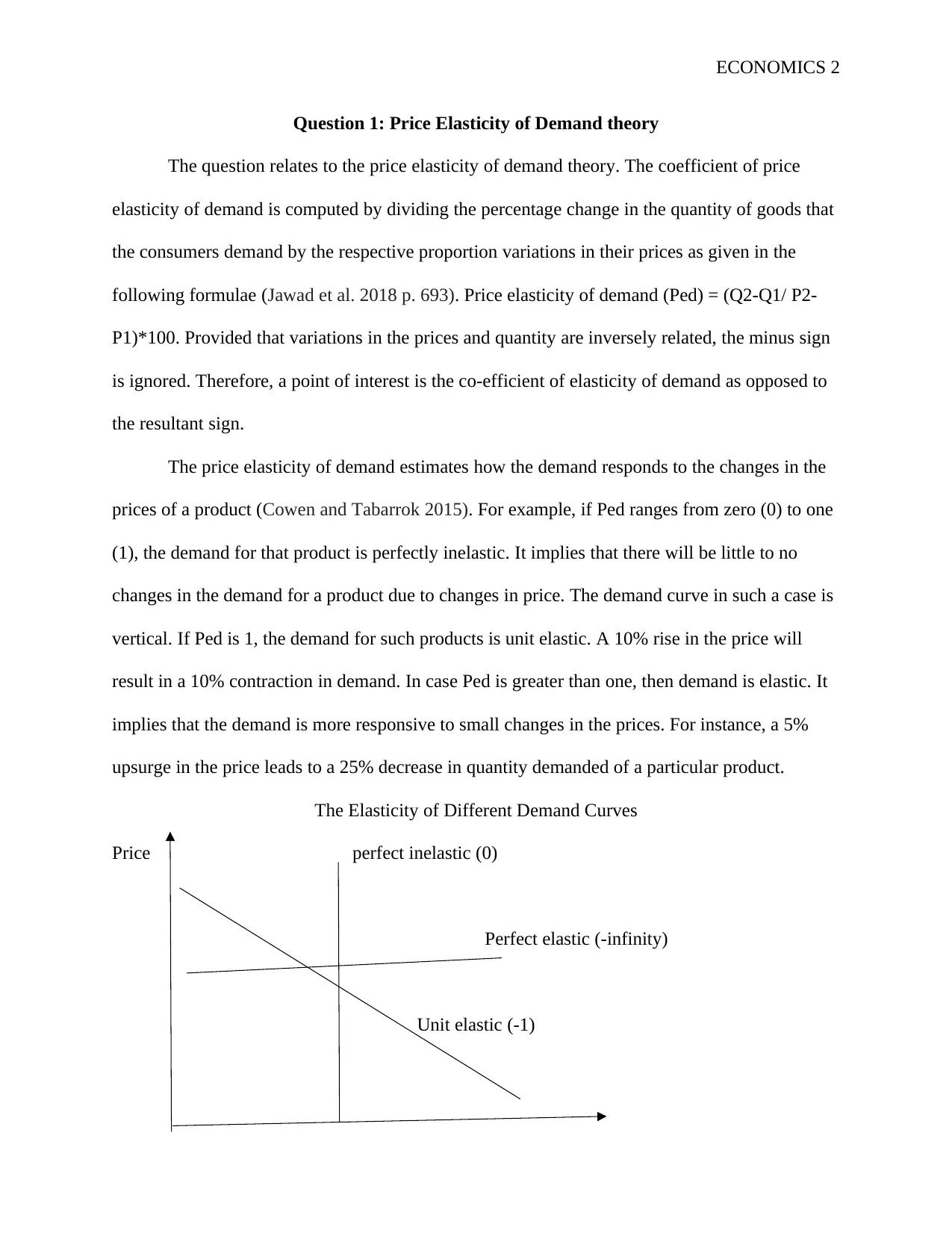

The price elasticity of demand estimates how the demand responds to the changes in the

prices of a product (Cowen and Tabarrok 2015). For example, if Ped ranges from zero (0) to one

(1), the demand for that product is perfectly inelastic. It implies that there will be little to no

changes in the demand for a product due to changes in price. The demand curve in such a case is

vertical. If Ped is 1, the demand for such products is unit elastic. A 10% rise in the price will

result in a 10% contraction in demand. In case Ped is greater than one, then demand is elastic. It

implies that the demand is more responsive to small changes in the prices. For instance, a 5%

upsurge in the price leads to a 25% decrease in quantity demanded of a particular product.

The Elasticity of Different Demand Curves

Price perfect inelastic (0)

Perfect elastic (-infinity)

Unit elastic (-1)

Question 1: Price Elasticity of Demand theory

The question relates to the price elasticity of demand theory. The coefficient of price

elasticity of demand is computed by dividing the percentage change in the quantity of goods that

the consumers demand by the respective proportion variations in their prices as given in the

following formulae (Jawad et al. 2018 p. 693). Price elasticity of demand (Ped) = (Q2-Q1/ P2-

P1)*100. Provided that variations in the prices and quantity are inversely related, the minus sign

is ignored. Therefore, a point of interest is the co-efficient of elasticity of demand as opposed to

the resultant sign.

The price elasticity of demand estimates how the demand responds to the changes in the

prices of a product (Cowen and Tabarrok 2015). For example, if Ped ranges from zero (0) to one

(1), the demand for that product is perfectly inelastic. It implies that there will be little to no

changes in the demand for a product due to changes in price. The demand curve in such a case is

vertical. If Ped is 1, the demand for such products is unit elastic. A 10% rise in the price will

result in a 10% contraction in demand. In case Ped is greater than one, then demand is elastic. It

implies that the demand is more responsive to small changes in the prices. For instance, a 5%

upsurge in the price leads to a 25% decrease in quantity demanded of a particular product.

The Elasticity of Different Demand Curves

Price perfect inelastic (0)

Perfect elastic (-infinity)

Unit elastic (-1)

ECONOMICS 3

Quantity

The price elasticity of demand theory helps to answer the question as it explains how the

changes in the various prices of the product will affect the quantity of the product that the

consumer will demand. Therefore, based on this knowledge, the producer will know when to

increase, decrease or hold the price of various goods and services at market constant. For

example, when the Ped is at 1.4 at the present price, I will advise the company to lower the price

as the demand is elastic. Small changes in the prices of this product will result in a large

contraction in the level of demand. Therefore, lowering the cost of selling that good will result in

an upsurge of the levels of demand by consumers. When the elasticity is at 0.6, I will advise the

company to raise the price of the product as there will be no changes in the quantity demanded

due to changes in prices. For example, important medical products, where people are willing to

pay any amount as long as they can afford to acquire services. When the elasticity of demand is

at 1, it implies that this is unit elasticity and the proportion changes in the level of demand are

identical to the proportion change in price. Therefore, in this case, I will advise the company to

keep the price the same as the variations in the levels of prices will have a net-zero effect on the

quantity demanded.

Question 2: Market Theory

In the perfect competition market, the firms are entitled to economic profit or economic

losses. The two have major influence regarding the perfectly competitive market. The presence

of the economic profits will attract new firms to the industry over time. As a result of more new

players joining the industry, the supply curve shifts to the right, prices reduce, and also profits

reduce (Azevedo and Gottlieb 2017 p. 72). New players will continue to join the industry

provided that there is still profit being made. In case some companies in the industry incur losses,

Quantity

The price elasticity of demand theory helps to answer the question as it explains how the

changes in the various prices of the product will affect the quantity of the product that the

consumer will demand. Therefore, based on this knowledge, the producer will know when to

increase, decrease or hold the price of various goods and services at market constant. For

example, when the Ped is at 1.4 at the present price, I will advise the company to lower the price

as the demand is elastic. Small changes in the prices of this product will result in a large

contraction in the level of demand. Therefore, lowering the cost of selling that good will result in

an upsurge of the levels of demand by consumers. When the elasticity is at 0.6, I will advise the

company to raise the price of the product as there will be no changes in the quantity demanded

due to changes in prices. For example, important medical products, where people are willing to

pay any amount as long as they can afford to acquire services. When the elasticity of demand is

at 1, it implies that this is unit elasticity and the proportion changes in the level of demand are

identical to the proportion change in price. Therefore, in this case, I will advise the company to

keep the price the same as the variations in the levels of prices will have a net-zero effect on the

quantity demanded.

Question 2: Market Theory

In the perfect competition market, the firms are entitled to economic profit or economic

losses. The two have major influence regarding the perfectly competitive market. The presence

of the economic profits will attract new firms to the industry over time. As a result of more new

players joining the industry, the supply curve shifts to the right, prices reduce, and also profits

reduce (Azevedo and Gottlieb 2017 p. 72). New players will continue to join the industry

provided that there is still profit being made. In case some companies in the industry incur losses,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 4

they will be forced to exit the market. Consequently, the curve denoting supply will shift to the

left which will result in an increase in the price and reduction in the losses. When players in the

industry are making losses, more of them will continue to exit the industry until there are zero

losses.

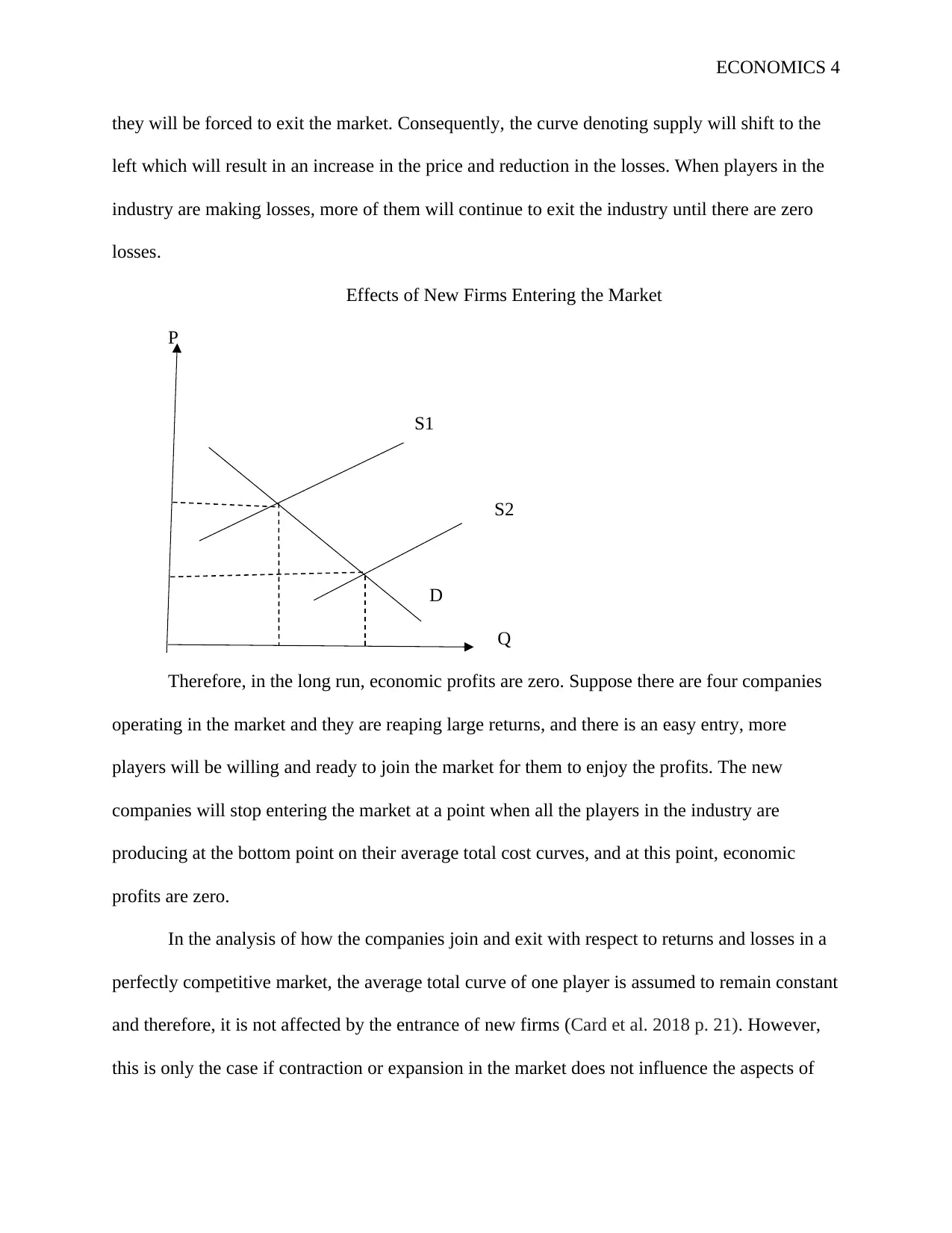

Effects of New Firms Entering the Market

P

S1

S2

D

Q

Therefore, in the long run, economic profits are zero. Suppose there are four companies

operating in the market and they are reaping large returns, and there is an easy entry, more

players will be willing and ready to join the market for them to enjoy the profits. The new

companies will stop entering the market at a point when all the players in the industry are

producing at the bottom point on their average total cost curves, and at this point, economic

profits are zero.

In the analysis of how the companies join and exit with respect to returns and losses in a

perfectly competitive market, the average total curve of one player is assumed to remain constant

and therefore, it is not affected by the entrance of new firms (Card et al. 2018 p. 21). However,

this is only the case if contraction or expansion in the market does not influence the aspects of

they will be forced to exit the market. Consequently, the curve denoting supply will shift to the

left which will result in an increase in the price and reduction in the losses. When players in the

industry are making losses, more of them will continue to exit the industry until there are zero

losses.

Effects of New Firms Entering the Market

P

S1

S2

D

Q

Therefore, in the long run, economic profits are zero. Suppose there are four companies

operating in the market and they are reaping large returns, and there is an easy entry, more

players will be willing and ready to join the market for them to enjoy the profits. The new

companies will stop entering the market at a point when all the players in the industry are

producing at the bottom point on their average total cost curves, and at this point, economic

profits are zero.

In the analysis of how the companies join and exit with respect to returns and losses in a

perfectly competitive market, the average total curve of one player is assumed to remain constant

and therefore, it is not affected by the entrance of new firms (Card et al. 2018 p. 21). However,

this is only the case if contraction or expansion in the market does not influence the aspects of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 5

manufacture which are employed by the companies in the market. For example, in the case

where the entrance of the new firms does not influence the charges of the prices of the inputs

which are used in manufacturing, then the industry is a constant cost industry. But, there are

some cases where the entry of the new firms impacts the prices of the costs of production.

The introduction of the new firms to the industry will result in an increase in the

competition for the inputs of production which are utilized in the industry. Then, if the industry

is significantly using those factors of production, the rise in demand could push up the price in

the market for all the firms in the industry. If this is the case, any firm that enters the industry

will improve the average costs and it will also reduce the pressure on the price. The firms will

operate at the lowest level of the average total curve and the economic profit will be zero.

However, the cost curve is higher compared before the entry of the new firms. For instance, an

increase in the number of vehicles push the prices higher and attracts new firms to the industry,

the industry will demand more workers. The demand for more workers is likely to push the

wages up.

The knowledge of economic returns and losses, in the long run, helps to answer this

question as firms which operate in perfect competition are subject to losses and profit depending

on the action of other firms. For example, when the firms that are already in the industry are

making economic profits, and there are fewer barriers to entry, the higher earnings will lure more

players to enter the market. As a result, there will be an expansion in the demand leading to an

outward shift, and the prices will fall and the quantity demanded will increase. Due to the fall in

the profits, it will reach a point where the firms in the industry are not able to cover the total

average costs, and at these points, they will suffer economic losses. Some of the firms will be

manufacture which are employed by the companies in the market. For example, in the case

where the entrance of the new firms does not influence the charges of the prices of the inputs

which are used in manufacturing, then the industry is a constant cost industry. But, there are

some cases where the entry of the new firms impacts the prices of the costs of production.

The introduction of the new firms to the industry will result in an increase in the

competition for the inputs of production which are utilized in the industry. Then, if the industry

is significantly using those factors of production, the rise in demand could push up the price in

the market for all the firms in the industry. If this is the case, any firm that enters the industry

will improve the average costs and it will also reduce the pressure on the price. The firms will

operate at the lowest level of the average total curve and the economic profit will be zero.

However, the cost curve is higher compared before the entry of the new firms. For instance, an

increase in the number of vehicles push the prices higher and attracts new firms to the industry,

the industry will demand more workers. The demand for more workers is likely to push the

wages up.

The knowledge of economic returns and losses, in the long run, helps to answer this

question as firms which operate in perfect competition are subject to losses and profit depending

on the action of other firms. For example, when the firms that are already in the industry are

making economic profits, and there are fewer barriers to entry, the higher earnings will lure more

players to enter the market. As a result, there will be an expansion in the demand leading to an

outward shift, and the prices will fall and the quantity demanded will increase. Due to the fall in

the profits, it will reach a point where the firms in the industry are not able to cover the total

average costs, and at these points, they will suffer economic losses. Some of the firms will be

ECONOMICS 6

forced to exit the market. Finally, the equilibrium will be restored in the market, and the firms

will operate at a point where economic profits are equal to zero in the long run.

Question 3: Economic Growth Theory

The aggregate production function comprises physical capital, human capital, and

technology which are responsible for the economic growth of a country. The category of

physical capital comprises of the equipment and plants which are used by firms in production.

There are two ways in which physical capital influences the productivity of the country.

Productivity will increase if there is an increase in the quantity and quality of physical capital.

Another component of the aggregate production function is the human capital (Zhang 2018).

Similar to physical capital, investment in human capital pays off in the long run.

The third component constitutes the technology that a country uses in production.

Technology, in this case, refers to the combination of the factors of production. Therefore, the

differences in these main elements which form the production function explain why growth in

various countries is different from others and takes place at different rates. The economic growth

is interested in the living standards per person; hence, there is a need to concentrate on GDP per

capita. With GDP per capita, it is possible to compare growth in countries with small populations

such as Uruguay and those with large populations such as China.

GDP per capita is computed by taking the domestic country’s economic output divided

by its people. Hence, the GDP per capita can be expressed as (GDP = human capital per person +

physical capital per person+ technology per person). GDP per capita = GDP/ population. The

output production function indicates what goes into the production of the output for the entire

economy. Therefore, the rate of growth of GDP is closely associated with the rate of a country’s

GDP per capita. For instance, if the fraction of the people that are employed increases, GDP per

forced to exit the market. Finally, the equilibrium will be restored in the market, and the firms

will operate at a point where economic profits are equal to zero in the long run.

Question 3: Economic Growth Theory

The aggregate production function comprises physical capital, human capital, and

technology which are responsible for the economic growth of a country. The category of

physical capital comprises of the equipment and plants which are used by firms in production.

There are two ways in which physical capital influences the productivity of the country.

Productivity will increase if there is an increase in the quantity and quality of physical capital.

Another component of the aggregate production function is the human capital (Zhang 2018).

Similar to physical capital, investment in human capital pays off in the long run.

The third component constitutes the technology that a country uses in production.

Technology, in this case, refers to the combination of the factors of production. Therefore, the

differences in these main elements which form the production function explain why growth in

various countries is different from others and takes place at different rates. The economic growth

is interested in the living standards per person; hence, there is a need to concentrate on GDP per

capita. With GDP per capita, it is possible to compare growth in countries with small populations

such as Uruguay and those with large populations such as China.

GDP per capita is computed by taking the domestic country’s economic output divided

by its people. Hence, the GDP per capita can be expressed as (GDP = human capital per person +

physical capital per person+ technology per person). GDP per capita = GDP/ population. The

output production function indicates what goes into the production of the output for the entire

economy. Therefore, the rate of growth of GDP is closely associated with the rate of a country’s

GDP per capita. For instance, if the fraction of the people that are employed increases, GDP per

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 7

capita will increase. In the long run, the only way the GDP per capita can continually increase is

when the productivity of the average worker increases or if there is an increase in capital.

The theory of economic growth in different countries based on the factors that constitute

the aggregate production function helps to address this question as it explains why there are

variations in growth in different countries (Van den Berg 2016). For example, in Australia which

is a high-income economy, for it to experience growth in GDP per capita, it should consider an

increase in the productivity per average worker. One way to enhance productivity per worker is

through an increase in the levels of education. It is assumed that Australia is a developed

country, has both high levels of technology and physical capital. Therefore, it has to boost how

human and physical capital are combined to attain more growth in GDP per capita.

For India, which is a middle-income country, it has to increase its physical and human

capital. For any country to experience growth in the long run, the average productivity per

person has to increase. The person’s productivity increase if there is an investment in human

capital through means such as advancement in knowledge and skills. Additionally, India also

needs to increase its physical capital. The combination of physical and human capital in the right

ratio will result in an increase in the per capita GDP. Lastly, for a low-income country such as

Afghanistan, to attain growth in GDP per capita, it has to increase all three factors of production.

It has to invest more in physical capital, technology, and human capital. Thereafter, workers with

necessary knowledge and skills will use the available physical capital appropriately and

productivity per worker will increase; hence an overall growth in GDP per capita.

Question 4: Theory of Inflation

The inflation rate is the rate at which the prices of products and services increase over

time (Alexander, Jyoti and Magueijo 2016). The rate of inflation is measured based on a base

capita will increase. In the long run, the only way the GDP per capita can continually increase is

when the productivity of the average worker increases or if there is an increase in capital.

The theory of economic growth in different countries based on the factors that constitute

the aggregate production function helps to address this question as it explains why there are

variations in growth in different countries (Van den Berg 2016). For example, in Australia which

is a high-income economy, for it to experience growth in GDP per capita, it should consider an

increase in the productivity per average worker. One way to enhance productivity per worker is

through an increase in the levels of education. It is assumed that Australia is a developed

country, has both high levels of technology and physical capital. Therefore, it has to boost how

human and physical capital are combined to attain more growth in GDP per capita.

For India, which is a middle-income country, it has to increase its physical and human

capital. For any country to experience growth in the long run, the average productivity per

person has to increase. The person’s productivity increase if there is an investment in human

capital through means such as advancement in knowledge and skills. Additionally, India also

needs to increase its physical capital. The combination of physical and human capital in the right

ratio will result in an increase in the per capita GDP. Lastly, for a low-income country such as

Afghanistan, to attain growth in GDP per capita, it has to increase all three factors of production.

It has to invest more in physical capital, technology, and human capital. Thereafter, workers with

necessary knowledge and skills will use the available physical capital appropriately and

productivity per worker will increase; hence an overall growth in GDP per capita.

Question 4: Theory of Inflation

The inflation rate is the rate at which the prices of products and services increase over

time (Alexander, Jyoti and Magueijo 2016). The rate of inflation is measured based on a base

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 8

year. The base year is the first year in a sequence of years in an economic period. To

accommodate the changes in the prices of the products and services, there is a frequent update of

base years periodically. Even though any year can serve as a base year, the analyst selects the

latest years. For instance, to find the rate of inflation between 2014 and 2019, 2014 is used as a

base year.

The consumer price index (CPI) is computed by dividing the budget of the bundles of

goods in the present period by the value of the bundles of goods in the base period and multiply

by 100. CPI = (cost of the bundles of goods in the present year/ costs of the bundles of goods in

the base period. For example, if the price in periods one and two are $20 and $40 respectively,

then CPI = (40/20)*100=200. It implies that in this current year, the price is twenty percent more

than in the base year. The main use of CPI is to estimate inflation. The inflation rate is computed

as inflation = (CPI in the present year –CPI in the previous year/ CPI previous year)*100.

However, in the computation of inflation, errors can occur which leads to underestimation or

overestimation of the inflation. The three reasons why inflation may be overestimated are quality

change bias, new goods bias, and substitution bias. Hence, based on the information regarding

the computation of inflation, it helps to address the effects of changes in a base year on the

substitution bias and new good bias.

In the estimation of inflation, new goods bias occurs when goods that were not available

during the base year are more expensive than the products they replace. Then the price is biased

as it will be higher. Another form of bias is the substitution bias. The consumers can substitute

one good for another due to variations in the prices (Fox and Syed 2016 p. 401). For instance,

when the prices of mangoes rise, but the price of apples remains constant, then consumers can

opt to consumer apples instead of mangoes. The substitution bias is experienced if the price

year. The base year is the first year in a sequence of years in an economic period. To

accommodate the changes in the prices of the products and services, there is a frequent update of

base years periodically. Even though any year can serve as a base year, the analyst selects the

latest years. For instance, to find the rate of inflation between 2014 and 2019, 2014 is used as a

base year.

The consumer price index (CPI) is computed by dividing the budget of the bundles of

goods in the present period by the value of the bundles of goods in the base period and multiply

by 100. CPI = (cost of the bundles of goods in the present year/ costs of the bundles of goods in

the base period. For example, if the price in periods one and two are $20 and $40 respectively,

then CPI = (40/20)*100=200. It implies that in this current year, the price is twenty percent more

than in the base year. The main use of CPI is to estimate inflation. The inflation rate is computed

as inflation = (CPI in the present year –CPI in the previous year/ CPI previous year)*100.

However, in the computation of inflation, errors can occur which leads to underestimation or

overestimation of the inflation. The three reasons why inflation may be overestimated are quality

change bias, new goods bias, and substitution bias. Hence, based on the information regarding

the computation of inflation, it helps to address the effects of changes in a base year on the

substitution bias and new good bias.

In the estimation of inflation, new goods bias occurs when goods that were not available

during the base year are more expensive than the products they replace. Then the price is biased

as it will be higher. Another form of bias is the substitution bias. The consumers can substitute

one good for another due to variations in the prices (Fox and Syed 2016 p. 401). For instance,

when the prices of mangoes rise, but the price of apples remains constant, then consumers can

opt to consumer apples instead of mangoes. The substitution bias is experienced if the price

ECONOMICS 9

index does not consider the changing in price if the basket of the products that are being

compared is the same. In the substitution bias, the basket of the products that are used in the

computation of CPI is fixed and does not consider the consumer’s substitution effect from the

items whose price increase.

The overestimation or underestimation has a negative influence on the overall economy

(Wolters and Tillmann 2015 p.1671). Therefore, the government statisticians always strive to

reduce it. To reduce the bias in the estimation of inflation, the consumer expenditures are

conducted more frequently and update information on CPI basket in a short period such as two

years. Therefore, if the government statisticians who have been computing the rate of inflation

have been updating the basket of goods after every ten years, then they change to five years, this

will reduce both the substitution bias and new goods bias. Hence, the accuracy rate in the

estimation of inflation will increase.

index does not consider the changing in price if the basket of the products that are being

compared is the same. In the substitution bias, the basket of the products that are used in the

computation of CPI is fixed and does not consider the consumer’s substitution effect from the

items whose price increase.

The overestimation or underestimation has a negative influence on the overall economy

(Wolters and Tillmann 2015 p.1671). Therefore, the government statisticians always strive to

reduce it. To reduce the bias in the estimation of inflation, the consumer expenditures are

conducted more frequently and update information on CPI basket in a short period such as two

years. Therefore, if the government statisticians who have been computing the rate of inflation

have been updating the basket of goods after every ten years, then they change to five years, this

will reduce both the substitution bias and new goods bias. Hence, the accuracy rate in the

estimation of inflation will increase.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ECONOMICS 10

List of References

Alexander, S., Jyoti, D. and Magueijo, J., 2016. Inflation and the Measurement Problem. arXiv

preprint arXiv:1602.01216.

Azevedo, E.M. and Gottlieb, D., 2017. Perfect competition in markets with adverse

selection. Econometrica, 85(1), pp.67-105.

Card, D., Cardoso, A.R., Heining, J. and Kline, P., 2018. Firms and labor market inequality:

Evidence and some theory. Journal of Labor Economics, 36(S1), pp.S13-S70.

Cowen, T. and Tabarrok, A., 2015. Modern principles of economics. Macmillan International

Higher Education.

Fox, K.J. and Syed, I.A., 2016. Price discounts and the measurement of inflation. Journal of

econometrics, 191(2), pp.398-406.

Jawad, M., Lee, J.T., Glantz, S. and Millett, C., 2018. Price elasticity of demand of non-cigarette

tobacco products: a systematic review and meta-analysis. Tobacco control, 27(6), pp.689-

695.

Van den Berg, H., 2016. Economic growth and development. World Scientific Publishing

Company.

Wolters, M.H. and Tillmann, P., 2015. The changing dynamics of US inflation persistence: A

quantile regression approach. Studies in Nonlinear Dynamics & Econometrics, 19(2),

pp.161-182.

Zhang, W.B., 2018. Economic Growth Theory: Capital, Knowledge, and Economic Structures.

Routledge.

List of References

Alexander, S., Jyoti, D. and Magueijo, J., 2016. Inflation and the Measurement Problem. arXiv

preprint arXiv:1602.01216.

Azevedo, E.M. and Gottlieb, D., 2017. Perfect competition in markets with adverse

selection. Econometrica, 85(1), pp.67-105.

Card, D., Cardoso, A.R., Heining, J. and Kline, P., 2018. Firms and labor market inequality:

Evidence and some theory. Journal of Labor Economics, 36(S1), pp.S13-S70.

Cowen, T. and Tabarrok, A., 2015. Modern principles of economics. Macmillan International

Higher Education.

Fox, K.J. and Syed, I.A., 2016. Price discounts and the measurement of inflation. Journal of

econometrics, 191(2), pp.398-406.

Jawad, M., Lee, J.T., Glantz, S. and Millett, C., 2018. Price elasticity of demand of non-cigarette

tobacco products: a systematic review and meta-analysis. Tobacco control, 27(6), pp.689-

695.

Van den Berg, H., 2016. Economic growth and development. World Scientific Publishing

Company.

Wolters, M.H. and Tillmann, P., 2015. The changing dynamics of US inflation persistence: A

quantile regression approach. Studies in Nonlinear Dynamics & Econometrics, 19(2),

pp.161-182.

Zhang, W.B., 2018. Economic Growth Theory: Capital, Knowledge, and Economic Structures.

Routledge.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ECONOMICS 11

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.