Economics Assignment 2: Analysis of England and Wales Economy

VerifiedAdded on 2023/04/22

|14

|3490

|274

Report

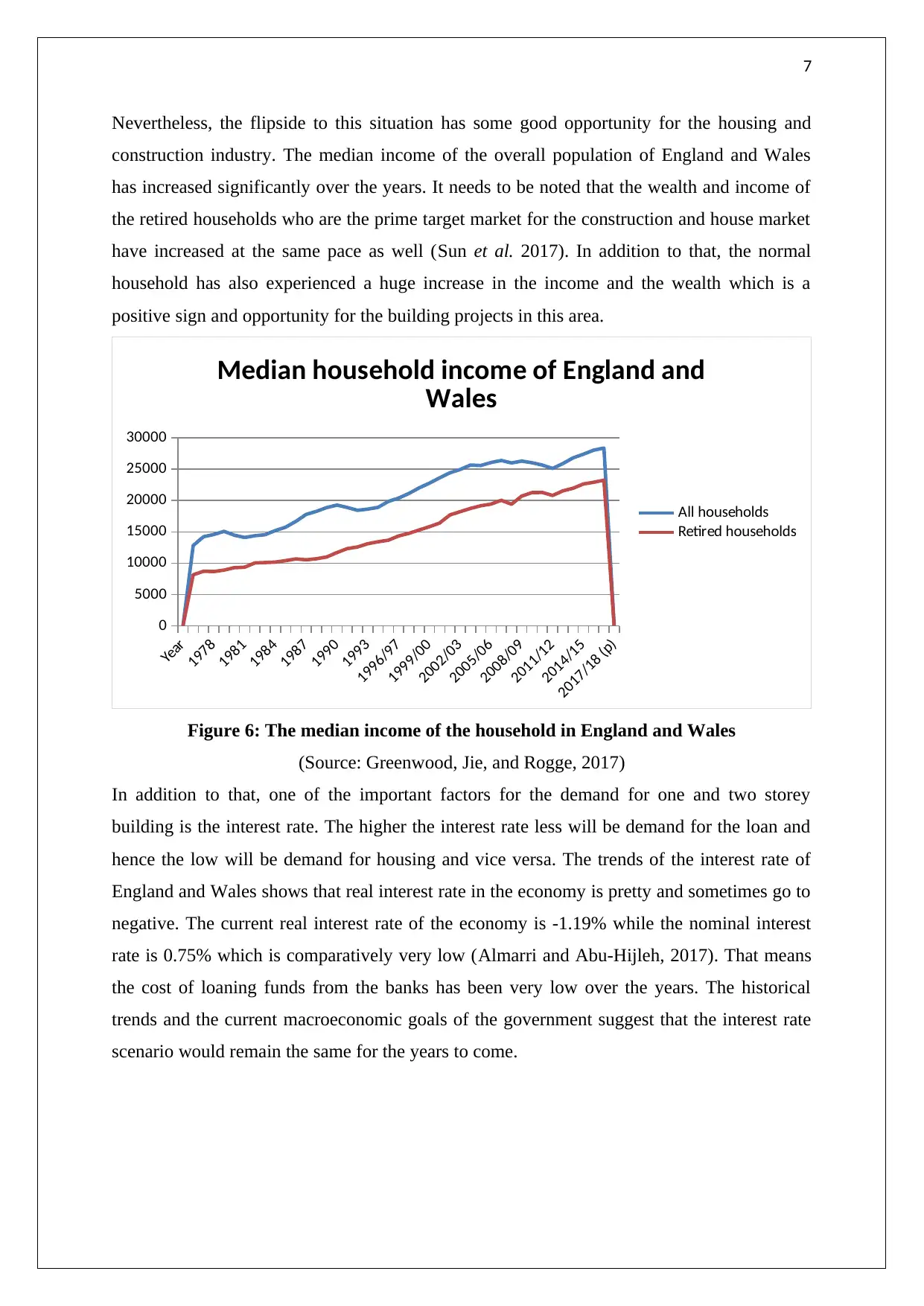

AI Summary

This economics assignment analyzes key economic indicators and trends in England and Wales, focusing on factors influencing the housing market and construction industry. The report examines birth and death statistics, homeownership rates, and the aging population's impact, presenting data visualizations to illustrate these trends. It delves into the GDP growth rate, median household income, and interest rates to assess the economic environment. The report also discusses the impact of immigration on the economy and the demand for housing. Finally, it explores funding options for local construction projects, comparing debt and equity financing methods, and concluding that bank loans are the most suitable form of debt financing for local construction projects. The assignment uses various sources to support its analysis and provide a comprehensive overview of the economic landscape of England and Wales.

1

ECONOMICS ASSIGNMENT

ECONOMICS ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Contents

Section 1.....................................................................................................................................3

Section 2.....................................................................................................................................6

Section 3...................................................................................................................................10

Section 4...................................................................................................................................11

Reference..................................................................................................................................12

Contents

Section 1.....................................................................................................................................3

Section 2.....................................................................................................................................6

Section 3...................................................................................................................................10

Section 4...................................................................................................................................11

Reference..................................................................................................................................12

3

Section 1

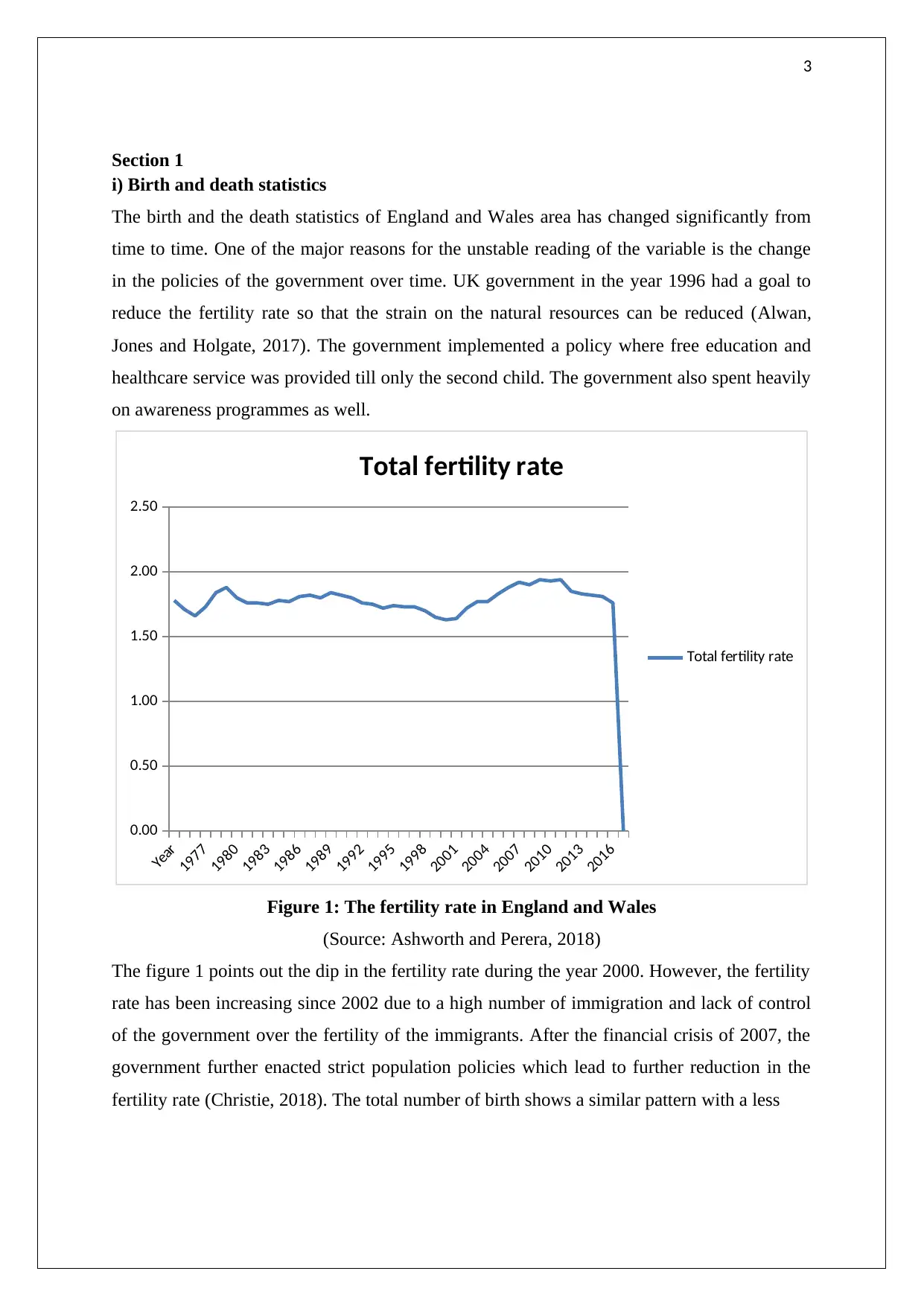

i) Birth and death statistics

The birth and the death statistics of England and Wales area has changed significantly from

time to time. One of the major reasons for the unstable reading of the variable is the change

in the policies of the government over time. UK government in the year 1996 had a goal to

reduce the fertility rate so that the strain on the natural resources can be reduced (Alwan,

Jones and Holgate, 2017). The government implemented a policy where free education and

healthcare service was provided till only the second child. The government also spent heavily

on awareness programmes as well.

Year

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

0.00

0.50

1.00

1.50

2.00

2.50

Total fertility rate

Total fertility rate

Figure 1: The fertility rate in England and Wales

(Source: Ashworth and Perera, 2018)

The figure 1 points out the dip in the fertility rate during the year 2000. However, the fertility

rate has been increasing since 2002 due to a high number of immigration and lack of control

of the government over the fertility of the immigrants. After the financial crisis of 2007, the

government further enacted strict population policies which lead to further reduction in the

fertility rate (Christie, 2018). The total number of birth shows a similar pattern with a less

Section 1

i) Birth and death statistics

The birth and the death statistics of England and Wales area has changed significantly from

time to time. One of the major reasons for the unstable reading of the variable is the change

in the policies of the government over time. UK government in the year 1996 had a goal to

reduce the fertility rate so that the strain on the natural resources can be reduced (Alwan,

Jones and Holgate, 2017). The government implemented a policy where free education and

healthcare service was provided till only the second child. The government also spent heavily

on awareness programmes as well.

Year

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

0.00

0.50

1.00

1.50

2.00

2.50

Total fertility rate

Total fertility rate

Figure 1: The fertility rate in England and Wales

(Source: Ashworth and Perera, 2018)

The figure 1 points out the dip in the fertility rate during the year 2000. However, the fertility

rate has been increasing since 2002 due to a high number of immigration and lack of control

of the government over the fertility of the immigrants. After the financial crisis of 2007, the

government further enacted strict population policies which lead to further reduction in the

fertility rate (Christie, 2018). The total number of birth shows a similar pattern with a less

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Year

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Total number of births

Total number of births

Figure 2: The total number of birth in England and Wales

(Source: Burton and Gameson, 2017)

ii) Home Ownership

The homeownership measurement can be best estimated from the study of the house price

index. The house price index is directly related to the number of houses owned by the

customers of the market. The house price has increased in England and Wales due to the

increased demand for housing and fixed supply.

Year

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

0

20

40

60

80

100

120

140

160

180

200

HPI

HPI

Year

1977

1980

1983

1986

1989

1992

1995

1998

2001

2004

2007

2010

2013

2016

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

Total number of births

Total number of births

Figure 2: The total number of birth in England and Wales

(Source: Burton and Gameson, 2017)

ii) Home Ownership

The homeownership measurement can be best estimated from the study of the house price

index. The house price index is directly related to the number of houses owned by the

customers of the market. The house price has increased in England and Wales due to the

increased demand for housing and fixed supply.

Year

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

0

20

40

60

80

100

120

140

160

180

200

HPI

HPI

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

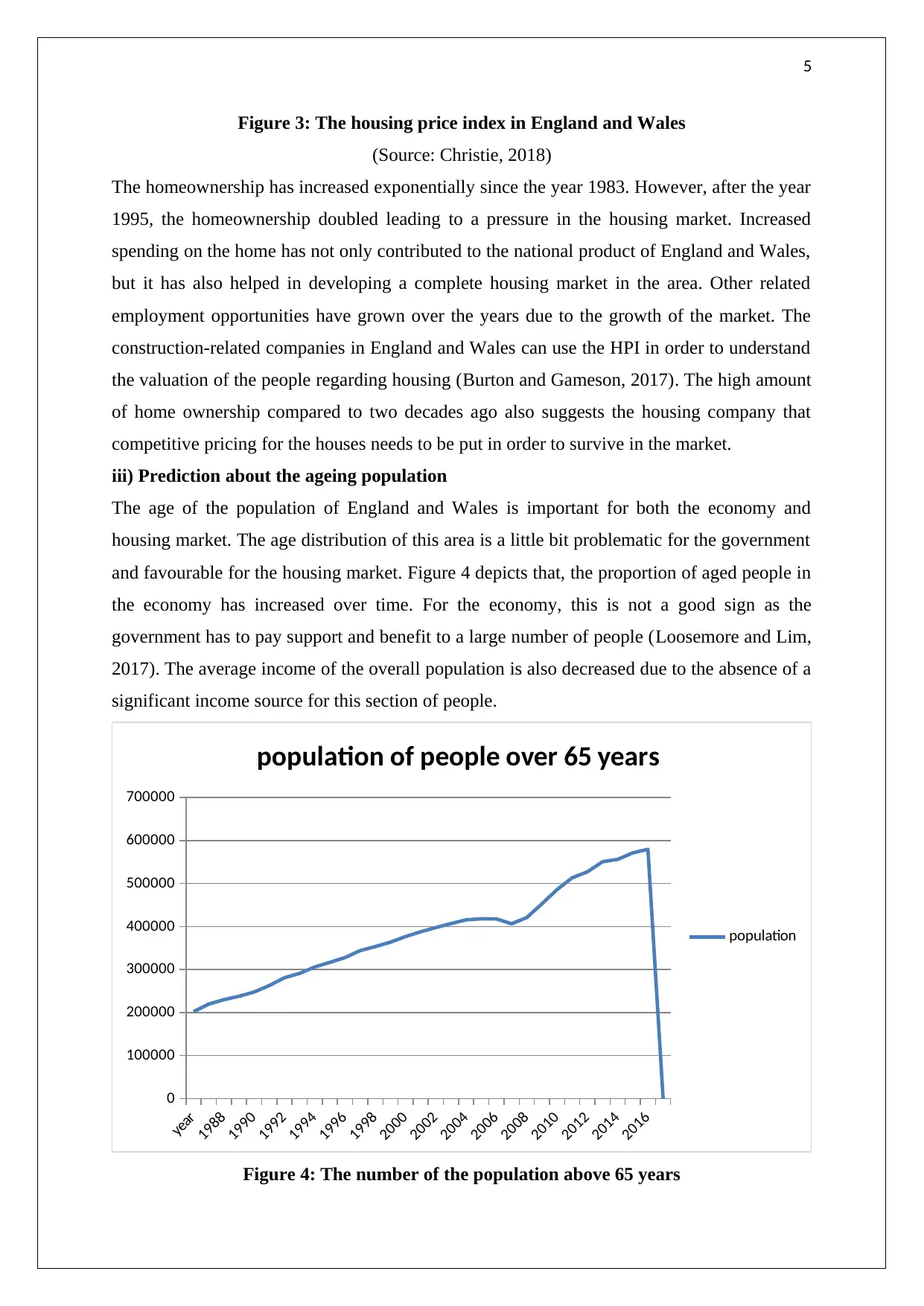

Figure 3: The housing price index in England and Wales

(Source: Christie, 2018)

The homeownership has increased exponentially since the year 1983. However, after the year

1995, the homeownership doubled leading to a pressure in the housing market. Increased

spending on the home has not only contributed to the national product of England and Wales,

but it has also helped in developing a complete housing market in the area. Other related

employment opportunities have grown over the years due to the growth of the market. The

construction-related companies in England and Wales can use the HPI in order to understand

the valuation of the people regarding housing (Burton and Gameson, 2017). The high amount

of home ownership compared to two decades ago also suggests the housing company that

competitive pricing for the houses needs to be put in order to survive in the market.

iii) Prediction about the ageing population

The age of the population of England and Wales is important for both the economy and

housing market. The age distribution of this area is a little bit problematic for the government

and favourable for the housing market. Figure 4 depicts that, the proportion of aged people in

the economy has increased over time. For the economy, this is not a good sign as the

government has to pay support and benefit to a large number of people (Loosemore and Lim,

2017). The average income of the overall population is also decreased due to the absence of a

significant income source for this section of people.

year

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0

100000

200000

300000

400000

500000

600000

700000

population of people over 65 years

population

Figure 4: The number of the population above 65 years

Figure 3: The housing price index in England and Wales

(Source: Christie, 2018)

The homeownership has increased exponentially since the year 1983. However, after the year

1995, the homeownership doubled leading to a pressure in the housing market. Increased

spending on the home has not only contributed to the national product of England and Wales,

but it has also helped in developing a complete housing market in the area. Other related

employment opportunities have grown over the years due to the growth of the market. The

construction-related companies in England and Wales can use the HPI in order to understand

the valuation of the people regarding housing (Burton and Gameson, 2017). The high amount

of home ownership compared to two decades ago also suggests the housing company that

competitive pricing for the houses needs to be put in order to survive in the market.

iii) Prediction about the ageing population

The age of the population of England and Wales is important for both the economy and

housing market. The age distribution of this area is a little bit problematic for the government

and favourable for the housing market. Figure 4 depicts that, the proportion of aged people in

the economy has increased over time. For the economy, this is not a good sign as the

government has to pay support and benefit to a large number of people (Loosemore and Lim,

2017). The average income of the overall population is also decreased due to the absence of a

significant income source for this section of people.

year

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

2012

2014

2016

0

100000

200000

300000

400000

500000

600000

700000

population of people over 65 years

population

Figure 4: The number of the population above 65 years

6

(Source: Lee and Cullen, 2018)

However, from the perspective of the housing market, the study of data can be informative.

People of this age generally have huge savings which are mostly spent in housing. Therefore,

the housing and construction market of England and Wales can target this segment of the

population for better revenue. It is predicted, given the current scenario that the number of

people above 65 years would further increase making a great opportunity for the construction

industry of the area (Nasir et al. 2017). However, the cost of that which is higher government

spending can increase the price level in the future that in turn can be a negative impact for the

economy as a whole.

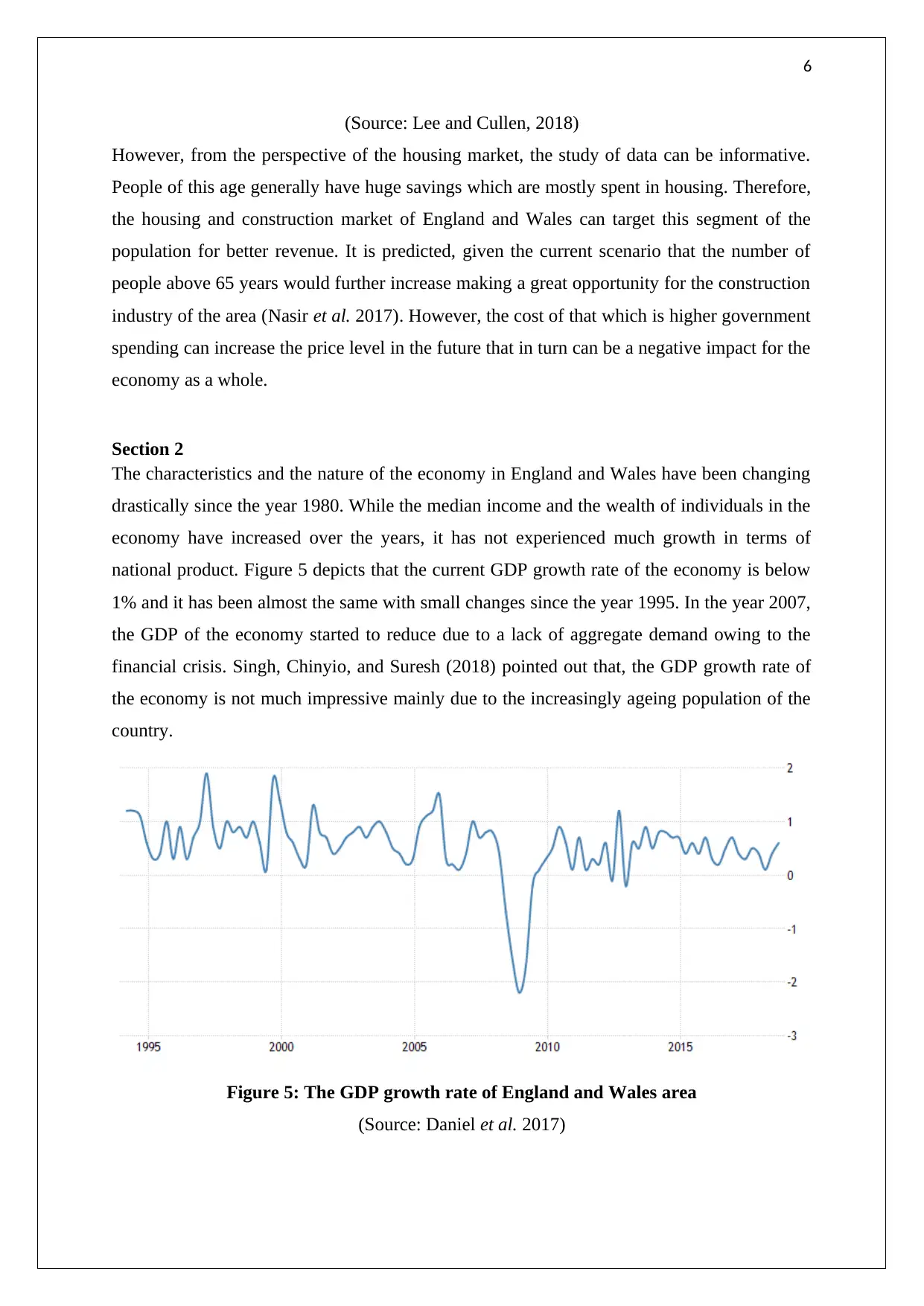

Section 2

The characteristics and the nature of the economy in England and Wales have been changing

drastically since the year 1980. While the median income and the wealth of individuals in the

economy have increased over the years, it has not experienced much growth in terms of

national product. Figure 5 depicts that the current GDP growth rate of the economy is below

1% and it has been almost the same with small changes since the year 1995. In the year 2007,

the GDP of the economy started to reduce due to a lack of aggregate demand owing to the

financial crisis. Singh, Chinyio, and Suresh (2018) pointed out that, the GDP growth rate of

the economy is not much impressive mainly due to the increasingly ageing population of the

country.

Figure 5: The GDP growth rate of England and Wales area

(Source: Daniel et al. 2017)

(Source: Lee and Cullen, 2018)

However, from the perspective of the housing market, the study of data can be informative.

People of this age generally have huge savings which are mostly spent in housing. Therefore,

the housing and construction market of England and Wales can target this segment of the

population for better revenue. It is predicted, given the current scenario that the number of

people above 65 years would further increase making a great opportunity for the construction

industry of the area (Nasir et al. 2017). However, the cost of that which is higher government

spending can increase the price level in the future that in turn can be a negative impact for the

economy as a whole.

Section 2

The characteristics and the nature of the economy in England and Wales have been changing

drastically since the year 1980. While the median income and the wealth of individuals in the

economy have increased over the years, it has not experienced much growth in terms of

national product. Figure 5 depicts that the current GDP growth rate of the economy is below

1% and it has been almost the same with small changes since the year 1995. In the year 2007,

the GDP of the economy started to reduce due to a lack of aggregate demand owing to the

financial crisis. Singh, Chinyio, and Suresh (2018) pointed out that, the GDP growth rate of

the economy is not much impressive mainly due to the increasingly ageing population of the

country.

Figure 5: The GDP growth rate of England and Wales area

(Source: Daniel et al. 2017)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

Nevertheless, the flipside to this situation has some good opportunity for the housing and

construction industry. The median income of the overall population of England and Wales

has increased significantly over the years. It needs to be noted that the wealth and income of

the retired households who are the prime target market for the construction and house market

have increased at the same pace as well (Sun et al. 2017). In addition to that, the normal

household has also experienced a huge increase in the income and the wealth which is a

positive sign and opportunity for the building projects in this area.

Year

1978

1981

1984

1987

1990

1993

1996/97

1999/00

2002/03

2005/06

2008/09

2011/12

2014/15

2017/18 (p)

0

5000

10000

15000

20000

25000

30000

Median household income of England and

Wales

All households

Retired households

Figure 6: The median income of the household in England and Wales

(Source: Greenwood, Jie, and Rogge, 2017)

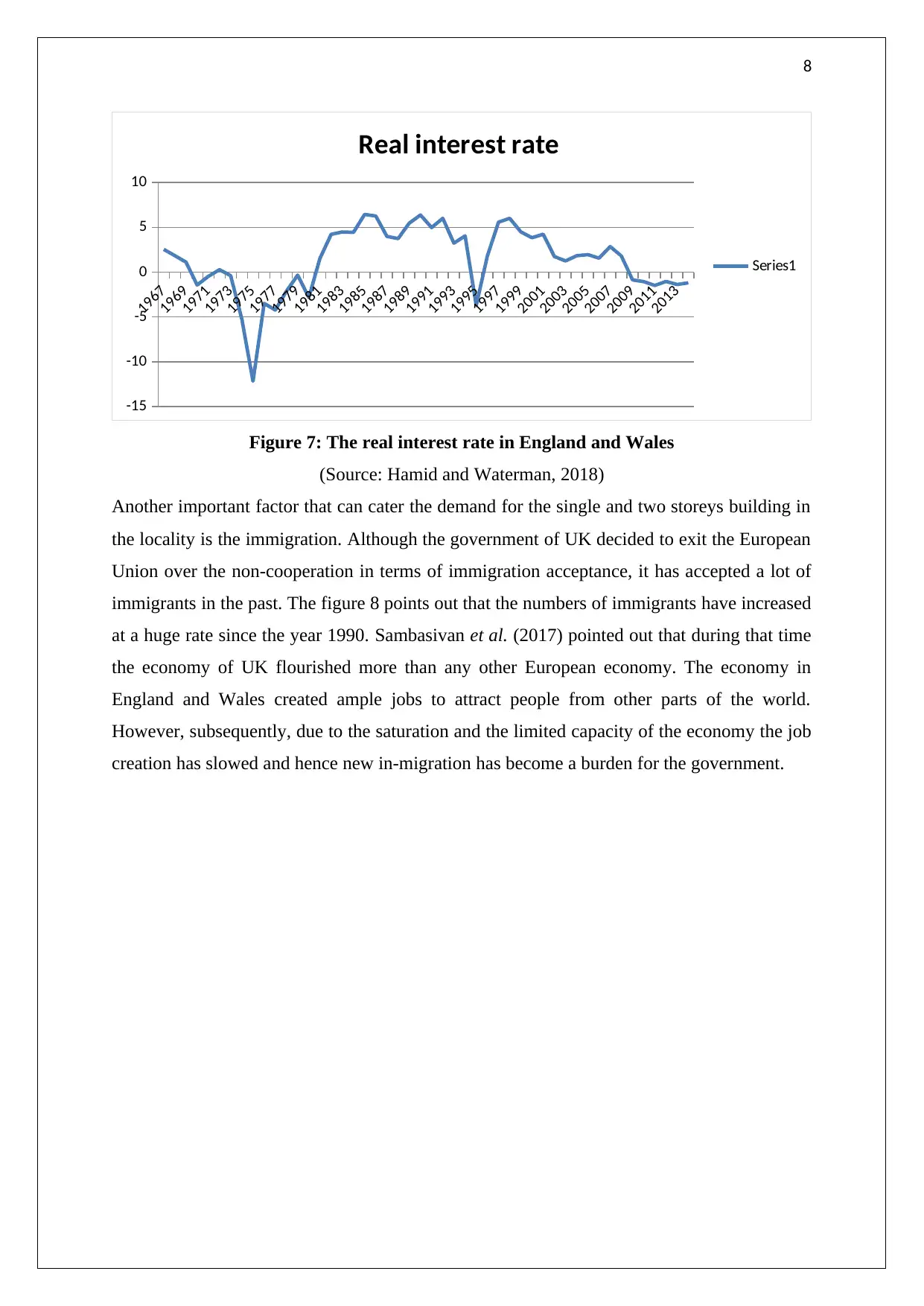

In addition to that, one of the important factors for the demand for one and two storey

building is the interest rate. The higher the interest rate less will be demand for the loan and

hence the low will be demand for housing and vice versa. The trends of the interest rate of

England and Wales shows that real interest rate in the economy is pretty and sometimes go to

negative. The current real interest rate of the economy is -1.19% while the nominal interest

rate is 0.75% which is comparatively very low (Almarri and Abu-Hijleh, 2017). That means

the cost of loaning funds from the banks has been very low over the years. The historical

trends and the current macroeconomic goals of the government suggest that the interest rate

scenario would remain the same for the years to come.

Nevertheless, the flipside to this situation has some good opportunity for the housing and

construction industry. The median income of the overall population of England and Wales

has increased significantly over the years. It needs to be noted that the wealth and income of

the retired households who are the prime target market for the construction and house market

have increased at the same pace as well (Sun et al. 2017). In addition to that, the normal

household has also experienced a huge increase in the income and the wealth which is a

positive sign and opportunity for the building projects in this area.

Year

1978

1981

1984

1987

1990

1993

1996/97

1999/00

2002/03

2005/06

2008/09

2011/12

2014/15

2017/18 (p)

0

5000

10000

15000

20000

25000

30000

Median household income of England and

Wales

All households

Retired households

Figure 6: The median income of the household in England and Wales

(Source: Greenwood, Jie, and Rogge, 2017)

In addition to that, one of the important factors for the demand for one and two storey

building is the interest rate. The higher the interest rate less will be demand for the loan and

hence the low will be demand for housing and vice versa. The trends of the interest rate of

England and Wales shows that real interest rate in the economy is pretty and sometimes go to

negative. The current real interest rate of the economy is -1.19% while the nominal interest

rate is 0.75% which is comparatively very low (Almarri and Abu-Hijleh, 2017). That means

the cost of loaning funds from the banks has been very low over the years. The historical

trends and the current macroeconomic goals of the government suggest that the interest rate

scenario would remain the same for the years to come.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

-15

-10

-5

0

5

10

Real interest rate

Series1

Figure 7: The real interest rate in England and Wales

(Source: Hamid and Waterman, 2018)

Another important factor that can cater the demand for the single and two storeys building in

the locality is the immigration. Although the government of UK decided to exit the European

Union over the non-cooperation in terms of immigration acceptance, it has accepted a lot of

immigrants in the past. The figure 8 points out that the numbers of immigrants have increased

at a huge rate since the year 1990. Sambasivan et al. (2017) pointed out that during that time

the economy of UK flourished more than any other European economy. The economy in

England and Wales created ample jobs to attract people from other parts of the world.

However, subsequently, due to the saturation and the limited capacity of the economy the job

creation has slowed and hence new in-migration has become a burden for the government.

1967

1969

1971

1973

1975

1977

1979

1981

1983

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

2013

-15

-10

-5

0

5

10

Real interest rate

Series1

Figure 7: The real interest rate in England and Wales

(Source: Hamid and Waterman, 2018)

Another important factor that can cater the demand for the single and two storeys building in

the locality is the immigration. Although the government of UK decided to exit the European

Union over the non-cooperation in terms of immigration acceptance, it has accepted a lot of

immigrants in the past. The figure 8 points out that the numbers of immigrants have increased

at a huge rate since the year 1990. Sambasivan et al. (2017) pointed out that during that time

the economy of UK flourished more than any other European economy. The economy in

England and Wales created ample jobs to attract people from other parts of the world.

However, subsequently, due to the saturation and the limited capacity of the economy the job

creation has slowed and hence new in-migration has become a burden for the government.

9

date

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

2017

-200000

-100000

0

100000

200000

300000

400000

500000

600000

700000

Migration from and to England and Wales over

the years

Net migration

Emigration

Immigration

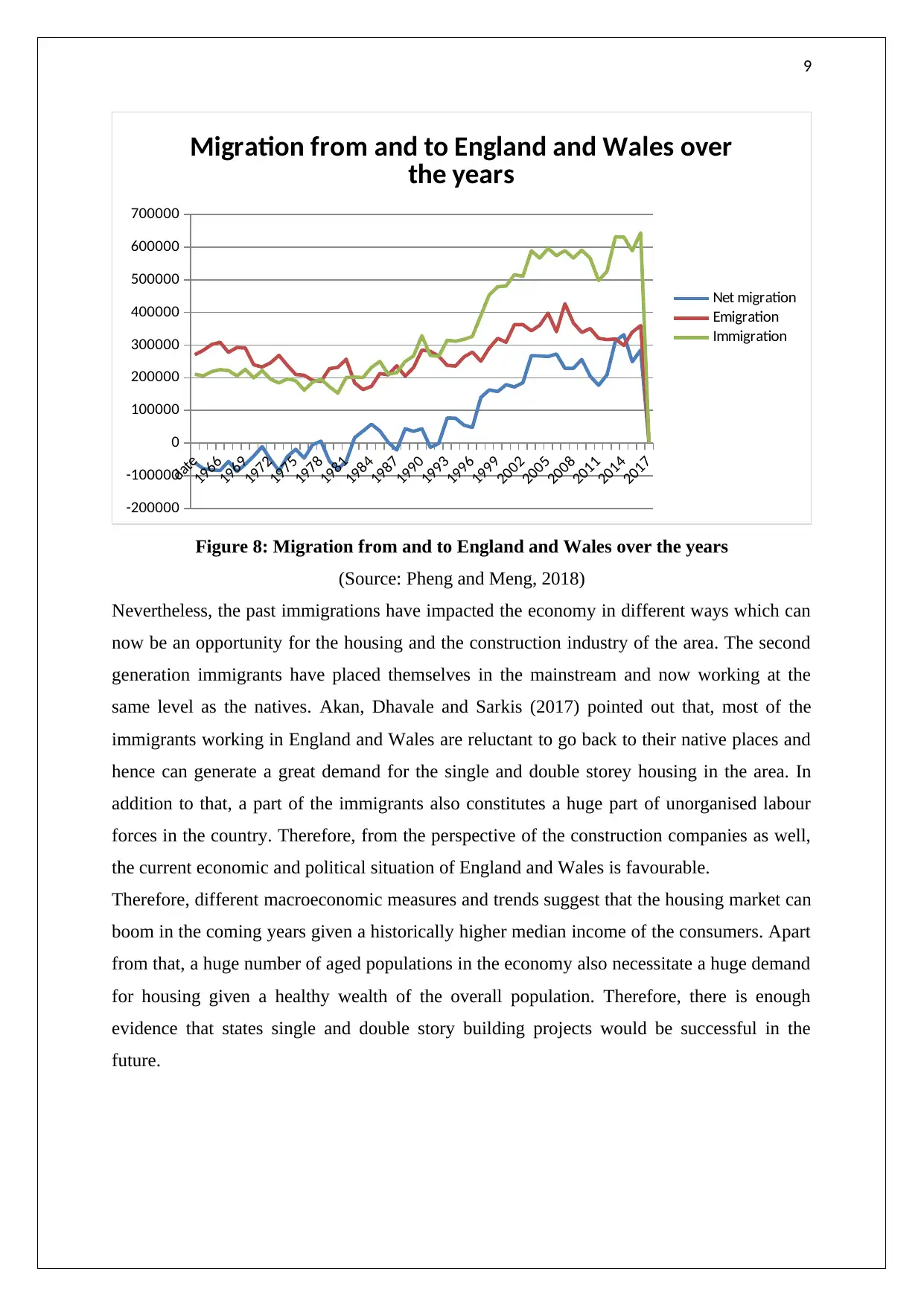

Figure 8: Migration from and to England and Wales over the years

(Source: Pheng and Meng, 2018)

Nevertheless, the past immigrations have impacted the economy in different ways which can

now be an opportunity for the housing and the construction industry of the area. The second

generation immigrants have placed themselves in the mainstream and now working at the

same level as the natives. Akan, Dhavale and Sarkis (2017) pointed out that, most of the

immigrants working in England and Wales are reluctant to go back to their native places and

hence can generate a great demand for the single and double storey housing in the area. In

addition to that, a part of the immigrants also constitutes a huge part of unorganised labour

forces in the country. Therefore, from the perspective of the construction companies as well,

the current economic and political situation of England and Wales is favourable.

Therefore, different macroeconomic measures and trends suggest that the housing market can

boom in the coming years given a historically higher median income of the consumers. Apart

from that, a huge number of aged populations in the economy also necessitate a huge demand

for housing given a healthy wealth of the overall population. Therefore, there is enough

evidence that states single and double story building projects would be successful in the

future.

date

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

2008

2011

2014

2017

-200000

-100000

0

100000

200000

300000

400000

500000

600000

700000

Migration from and to England and Wales over

the years

Net migration

Emigration

Immigration

Figure 8: Migration from and to England and Wales over the years

(Source: Pheng and Meng, 2018)

Nevertheless, the past immigrations have impacted the economy in different ways which can

now be an opportunity for the housing and the construction industry of the area. The second

generation immigrants have placed themselves in the mainstream and now working at the

same level as the natives. Akan, Dhavale and Sarkis (2017) pointed out that, most of the

immigrants working in England and Wales are reluctant to go back to their native places and

hence can generate a great demand for the single and double storey housing in the area. In

addition to that, a part of the immigrants also constitutes a huge part of unorganised labour

forces in the country. Therefore, from the perspective of the construction companies as well,

the current economic and political situation of England and Wales is favourable.

Therefore, different macroeconomic measures and trends suggest that the housing market can

boom in the coming years given a historically higher median income of the consumers. Apart

from that, a huge number of aged populations in the economy also necessitate a huge demand

for housing given a healthy wealth of the overall population. Therefore, there is enough

evidence that states single and double story building projects would be successful in the

future.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Section 3

The local construction development projects can raise funds in two different ways, either by

debt financing or by equity financing. Under debt financing, the local construction company

loans funds from the banks or from the investors at a fixed or flexible interest rate.

Construction Company, after the completion and the sale of the project, returns the money

with interest to the investor or to the bank. For the case of the local construction project, a

bank loan would be the best form of debt financing method for raising funds. One of the

biggest advantages of debt financing over the equity financing is that it allows the

construction company to have full control over the projects. In addition to that, financing

through debt also allows the company to claim a tax deduction in the UK that in turn helps in

the profitability of the construction company. Goh et al. (2017) highlighted that, in the case

of local construction projects, the profits are proportionately smaller than bigger projects.

Therefore, debt financing is advantageous as it does not allow a third party to have a share in

the profit. Nevertheless, debt financing can also become a great burden for the project as

repayment does not depend on success or failure. Failing to repay the debt will not only cost

the company legally, but it also affects the credit rating of the company and future projects

would be at risk. Improper money management when debt financing has been chosen can

lead to bankruptcy as well (Na and Subramaniam, 2018). Therefore, while debt financing

provides a greater control it necessitates proper money management in order to be successful.

Another form of financing that can be used by the local construction project is equity

financing. In equity financing, the company transfers shares of the company to the lender.

Therefore, one of the biggest advantages of debt financing is that investors have a vested

interest in the success of the project. Fianto et al. (2018) stated that, in local construction

cases, equity financing allows the project to get additional help from the investors as their

money is at stake as well. The risk involved in equity financing is also lower compared to the

debt financing. The construction company has to share profits only when the company earns

a positive profit. The company also receives a contribution from the investors in case of

decision making which becomes very helpful for the local projects. However, despite some of

the benefits, disadvantages such as less control over the company are also there. Apart from

that, the equity financing is also considered a costlier alternative for financing as the amount

to be paid back is proportionately more than the investment compared to debt financing

(Qureshi, Ahsan, and Azid, 2017). The investors also have their say in the decision making of

the company that can make the project less flexible as well. Thus, while debt financing is less

risky it can be costlier for the local construction company.

Section 3

The local construction development projects can raise funds in two different ways, either by

debt financing or by equity financing. Under debt financing, the local construction company

loans funds from the banks or from the investors at a fixed or flexible interest rate.

Construction Company, after the completion and the sale of the project, returns the money

with interest to the investor or to the bank. For the case of the local construction project, a

bank loan would be the best form of debt financing method for raising funds. One of the

biggest advantages of debt financing over the equity financing is that it allows the

construction company to have full control over the projects. In addition to that, financing

through debt also allows the company to claim a tax deduction in the UK that in turn helps in

the profitability of the construction company. Goh et al. (2017) highlighted that, in the case

of local construction projects, the profits are proportionately smaller than bigger projects.

Therefore, debt financing is advantageous as it does not allow a third party to have a share in

the profit. Nevertheless, debt financing can also become a great burden for the project as

repayment does not depend on success or failure. Failing to repay the debt will not only cost

the company legally, but it also affects the credit rating of the company and future projects

would be at risk. Improper money management when debt financing has been chosen can

lead to bankruptcy as well (Na and Subramaniam, 2018). Therefore, while debt financing

provides a greater control it necessitates proper money management in order to be successful.

Another form of financing that can be used by the local construction project is equity

financing. In equity financing, the company transfers shares of the company to the lender.

Therefore, one of the biggest advantages of debt financing is that investors have a vested

interest in the success of the project. Fianto et al. (2018) stated that, in local construction

cases, equity financing allows the project to get additional help from the investors as their

money is at stake as well. The risk involved in equity financing is also lower compared to the

debt financing. The construction company has to share profits only when the company earns

a positive profit. The company also receives a contribution from the investors in case of

decision making which becomes very helpful for the local projects. However, despite some of

the benefits, disadvantages such as less control over the company are also there. Apart from

that, the equity financing is also considered a costlier alternative for financing as the amount

to be paid back is proportionately more than the investment compared to debt financing

(Qureshi, Ahsan, and Azid, 2017). The investors also have their say in the decision making of

the company that can make the project less flexible as well. Thus, while debt financing is less

risky it can be costlier for the local construction company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Section 4

The topic for the portfolio mainly concentrated on the data trends pertaining to England and

Wales that have been used to understand the relation with the construction industry of the

countries. The module has helped me to learn how to analyse data and relate it to a relevant

industry. The data has become important in recent times for the decision making of profit and

nonprofit companies. Therefore, the lessons from this module can be used in real life

situations for the decision making in general. Apart from that, financing is an integral part of

any project or company. This module has helped me to understand how financing works and

what would be the best financing strategy given the size and the environment of the business.

Section 4

The topic for the portfolio mainly concentrated on the data trends pertaining to England and

Wales that have been used to understand the relation with the construction industry of the

countries. The module has helped me to learn how to analyse data and relate it to a relevant

industry. The data has become important in recent times for the decision making of profit and

nonprofit companies. Therefore, the lessons from this module can be used in real life

situations for the decision making in general. Apart from that, financing is an integral part of

any project or company. This module has helped me to understand how financing works and

what would be the best financing strategy given the size and the environment of the business.

12

Reference

Akan, M.Ö.A., Dhavale, D.G. and Sarkis, J., 2017. Greenhouse gas emissions in the

construction industry: An analysis and evaluation of a concrete supply chain. Journal of

Cleaner Production, 167, pp.1195-1207.

Almarri, K. and Abu-Hijleh, B., 2017. Critical Success Factors for Public-Private

Partnerships in the UAE Construction Industry-A Comparative Analysis between the UAE

and the UK. Journal of Engineering, Project & Production Management, 7(1).

Alwan, Z., Jones, P. and Holgate, P., 2017. Strategic sustainable development in the UK

construction industry, through the framework for strategic sustainable development, using

Building Information Modelling. Journal of Cleaner Production, 140, pp.349-358.

Ashworth, A. and Perera, S., 2018. Contractual procedures in the construction industry.

Routledge.

Burton, M.C. and Gameson, R.N., 2017, September. An evaluation of the factors for a

successful alliance in the United Kingdom (UK) construction industry. In International

Research Conference 2017: Shaping Tomorrow's Built Environment (pp. 530-543). The

University of Salford.

Christie, D.S., 2018. 'Splendid, but what does it actually mean?'Good faith and relational

contracts in the UK construction industry.

Daniel, E.I., Pasquire, C., Dickens, G. and Ballard, H.G., 2017. The relationship between the

Last Planner® System and collaborative planning practice in UK construction. Engineering,

Construction and Architectural Management, 24(3), pp.407-425.

Fianto, B.A., Gan, C., Hu, B. and Roudaki, J., 2018. Equity financing and debt-based

financing: Evidence from Islamic microfinance institutions in Indonesia. Pacific-Basin

Finance Journal, 52, pp.163-172.

Goh, B.W., Lim, C.Y., Lobo, G.J. and Tong, Y.H., 2017. Conditional conservatism and debt

versus equity financing. Contemporary Accounting Research, 34(1), pp.216-251.

Reference

Akan, M.Ö.A., Dhavale, D.G. and Sarkis, J., 2017. Greenhouse gas emissions in the

construction industry: An analysis and evaluation of a concrete supply chain. Journal of

Cleaner Production, 167, pp.1195-1207.

Almarri, K. and Abu-Hijleh, B., 2017. Critical Success Factors for Public-Private

Partnerships in the UAE Construction Industry-A Comparative Analysis between the UAE

and the UK. Journal of Engineering, Project & Production Management, 7(1).

Alwan, Z., Jones, P. and Holgate, P., 2017. Strategic sustainable development in the UK

construction industry, through the framework for strategic sustainable development, using

Building Information Modelling. Journal of Cleaner Production, 140, pp.349-358.

Ashworth, A. and Perera, S., 2018. Contractual procedures in the construction industry.

Routledge.

Burton, M.C. and Gameson, R.N., 2017, September. An evaluation of the factors for a

successful alliance in the United Kingdom (UK) construction industry. In International

Research Conference 2017: Shaping Tomorrow's Built Environment (pp. 530-543). The

University of Salford.

Christie, D.S., 2018. 'Splendid, but what does it actually mean?'Good faith and relational

contracts in the UK construction industry.

Daniel, E.I., Pasquire, C., Dickens, G. and Ballard, H.G., 2017. The relationship between the

Last Planner® System and collaborative planning practice in UK construction. Engineering,

Construction and Architectural Management, 24(3), pp.407-425.

Fianto, B.A., Gan, C., Hu, B. and Roudaki, J., 2018. Equity financing and debt-based

financing: Evidence from Islamic microfinance institutions in Indonesia. Pacific-Basin

Finance Journal, 52, pp.163-172.

Goh, B.W., Lim, C.Y., Lobo, G.J. and Tong, Y.H., 2017. Conditional conservatism and debt

versus equity financing. Contemporary Accounting Research, 34(1), pp.216-251.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.