Economics for Business 2019-20: Equilibrium, Growth, and Policy

VerifiedAdded on 2023/01/11

|8

|1324

|23

Homework Assignment

AI Summary

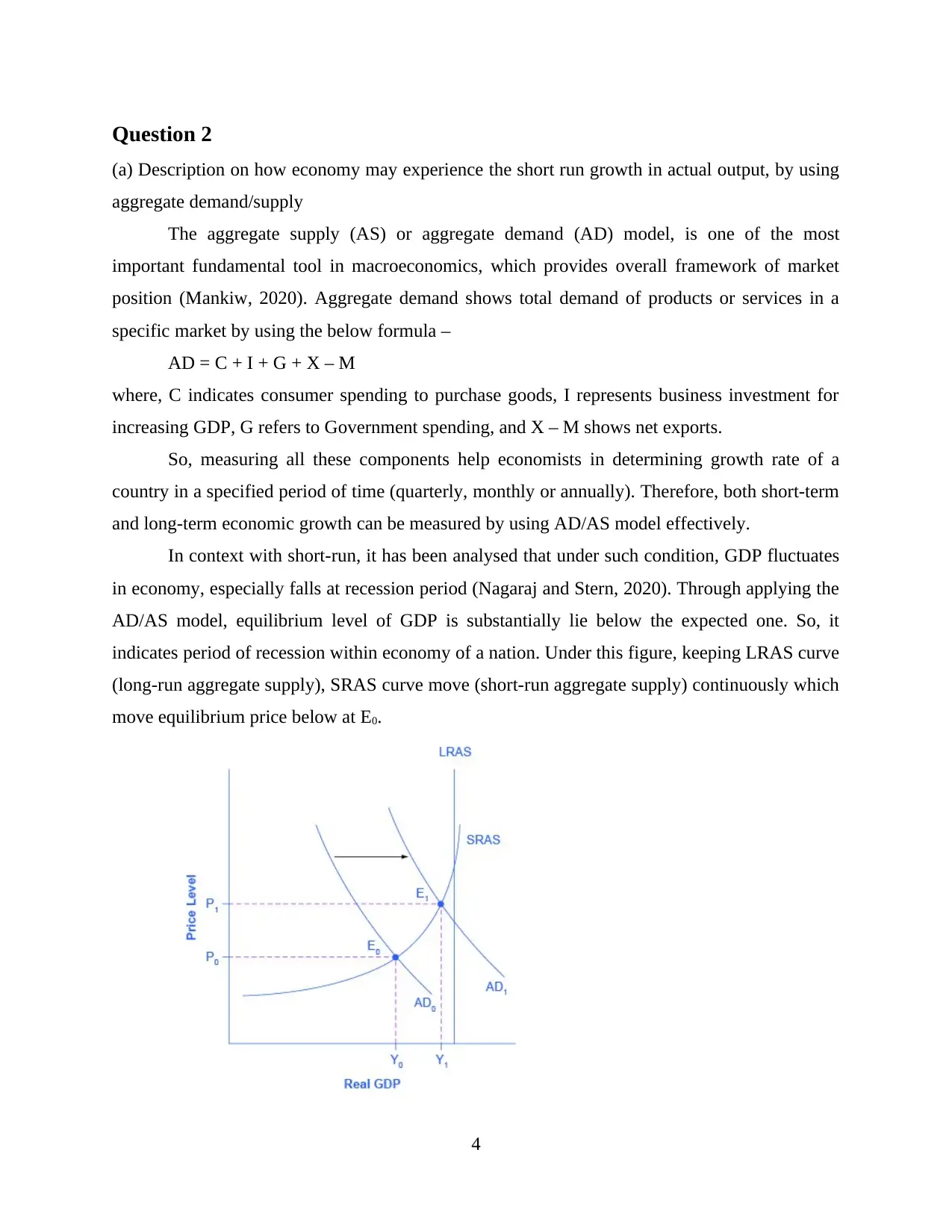

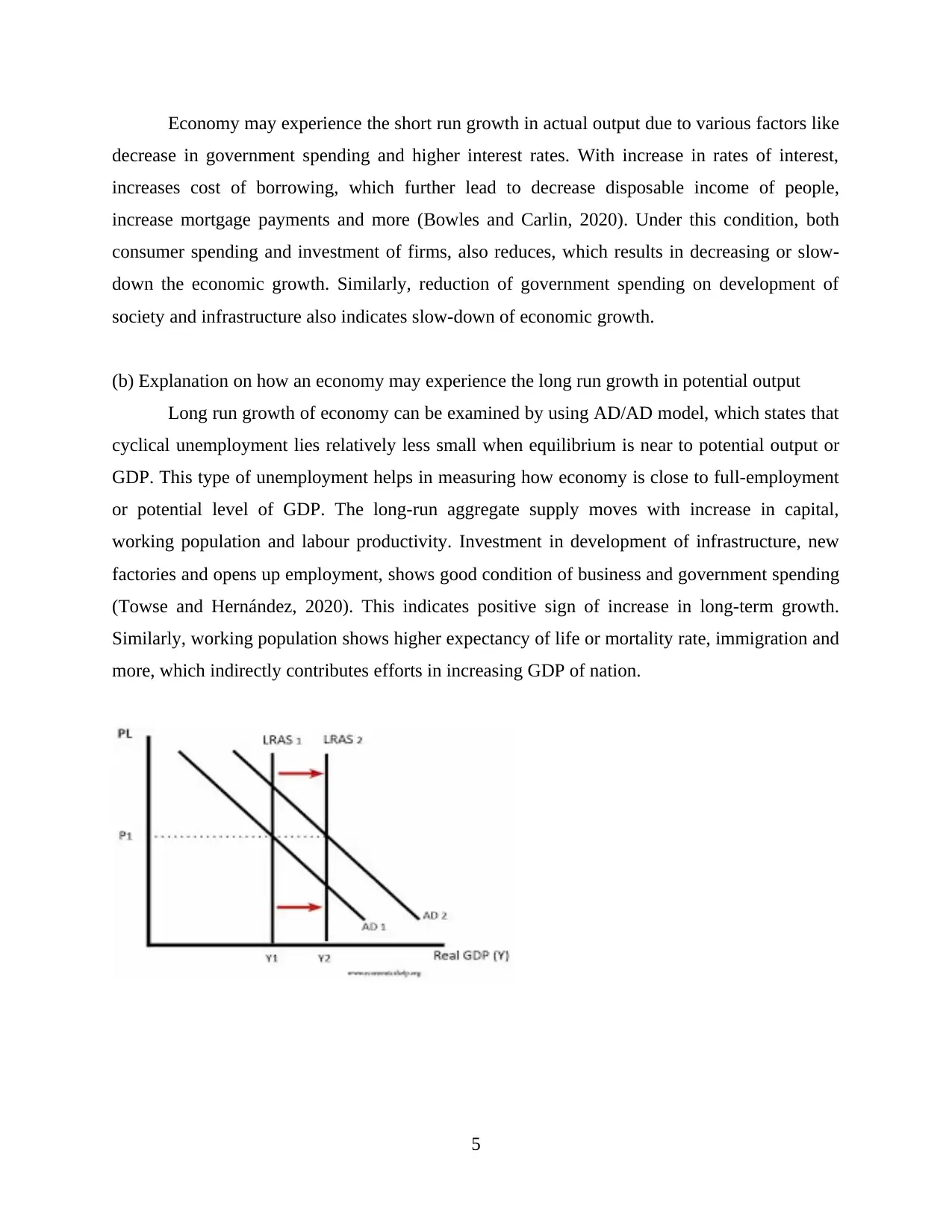

This economics assignment explores the determination of equilibrium price and quantity through the interaction of demand and supply, examining the impact of minimum price interventions and changes in raw material prices. It further analyzes short-run economic growth using the aggregate demand/supply model, considering factors like government spending and interest rates. The assignment also delves into long-run economic growth, linking it to potential output and factors such as capital investment and labor productivity. The solutions provided incorporate economic models, definitions, and examples, offering a comprehensive analysis of these key macroeconomic concepts. The assignment addresses specific questions related to equilibrium, growth, and the influence of economic policies on market dynamics and overall economic performance. Diagrams are also included to aid in explaining the concepts.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.