Economics and Financial Management Report: Northern Rock Bank Analysis

VerifiedAdded on 2022/08/13

|20

|3850

|11

Report

AI Summary

This report provides a comprehensive analysis of Northern Rock Bank's financial performance, focusing on the impact of economic factors and accounting ratios. It begins with an executive summary highlighting key findings and recommendations. The introduction provides background information on Northern Rock's history and the reasons for its failure. The report then delves into the analysis of macroeconomic and microeconomic factors, examining their influence on the bank's operations. It includes the calculation and interpretation of key accounting ratios such as return on capital employed, net profit margin, and current ratio for the years 2017-2019. The importance of these ratios in assessing a company's financial health is also discussed. The report concludes with recommendations for the bank to improve its financial performance and overall business strategy. The analysis includes the impact of customers, suppliers, distribution channels, public, and competitors as macroeconomic factors, while demand, supply, and elasticity are considered as microeconomic factors. The report also highlights the significance of accounting ratios in evaluating profitability, efficiency, solvency, and risk.

Running head: REPORT 0

ECONOMICS AND FINANCIAL MANAGEMENT

FEBRUARY 16, 2020

STUDENT DETAILS:

ECONOMICS AND FINANCIAL MANAGEMENT

FEBRUARY 16, 2020

STUDENT DETAILS:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 1

Executive summary

The accounting ratios are effective method to measure liquidity, solvency, and efficiency along

with profitability of the company. This is a reason that the accounting ratios are relevant and

important to increase the efficiency of administration. With the help of this, the company can

make strategy to decrease expenditure as well as increase the profit margin. It can see that

Northern Rock Bank is failing to repay loan as well as generating profit. The customers have no

faith in this bank. Northern Rock Bank is required to make focus on the microeconomic factors

as well as macroeconomic factors for the development of business. By following these factors,

the company can create its image. The microeconomics analyses decision of individual as well

as business. On the other hand, the macroeconomics assesses decision made by government and

country. These macroeconomic factors are related to broad economy. The microeconomic factors

put impact on the demand along with supply. It is helpful in determining the price level. In this

report, macroeconomic factors like customer, supplier, and distribution channel, public as well as

competitor, and microeconomic factors (demand, supply and elasticity) is discussed. The below

mentioned parts also discuss definition and impact of accounting ratios. This report puts focus on

the efficiency ratio, return on capital employed, current ratio, as well as net profit margin ratio.

These below discussed parts also recommend some strategies to the bank to develop business

and get more profits.

Executive summary

The accounting ratios are effective method to measure liquidity, solvency, and efficiency along

with profitability of the company. This is a reason that the accounting ratios are relevant and

important to increase the efficiency of administration. With the help of this, the company can

make strategy to decrease expenditure as well as increase the profit margin. It can see that

Northern Rock Bank is failing to repay loan as well as generating profit. The customers have no

faith in this bank. Northern Rock Bank is required to make focus on the microeconomic factors

as well as macroeconomic factors for the development of business. By following these factors,

the company can create its image. The microeconomics analyses decision of individual as well

as business. On the other hand, the macroeconomics assesses decision made by government and

country. These macroeconomic factors are related to broad economy. The microeconomic factors

put impact on the demand along with supply. It is helpful in determining the price level. In this

report, macroeconomic factors like customer, supplier, and distribution channel, public as well as

competitor, and microeconomic factors (demand, supply and elasticity) is discussed. The below

mentioned parts also discuss definition and impact of accounting ratios. This report puts focus on

the efficiency ratio, return on capital employed, current ratio, as well as net profit margin ratio.

These below discussed parts also recommend some strategies to the bank to develop business

and get more profits.

REPORT 2

Contents

Executive summary.........................................................................................................................1

Introduction –...................................................................................................................................3

A. Analysis of economic factors and their impacts on business –................................................3

B. Calculation of ratios for each of the three years –....................................................................6

C. Accounting ratios and their importance on business –.............................................................6

D. Recommendations..................................................................................................................11

E. Conclusion..............................................................................................................................12

Contents

Executive summary.........................................................................................................................1

Introduction –...................................................................................................................................3

A. Analysis of economic factors and their impacts on business –................................................3

B. Calculation of ratios for each of the three years –....................................................................6

C. Accounting ratios and their importance on business –.............................................................6

D. Recommendations..................................................................................................................11

E. Conclusion..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 3

Introduction –

Northern Rock was founded in 1850. It was operated as building society in initial period. It

provided banking along with financial services like mortgage services. It became joint stock

Company in year 1997. It was regulated by London stock Exchange. It was regulated as publicly

traded company. It can see that the bank was performed efficiently. But, it went through the

global banking crisis of 2007. It lowered the profit margin of bank. The bank became incapable

to make money from the loans and repay the loan amount, which has been borrowed by bank for

banking functions. The main objective of this paper is to render company analysis of the

company that has failed because of several economic factors. In the following parts, the macro-

economic factors as well as micro-economic factors, and their impacts are discussed and

examined. This report also discusses the accounting ratios and their impact on the business. The

below mentioned parts also make recommendation and conclusion.

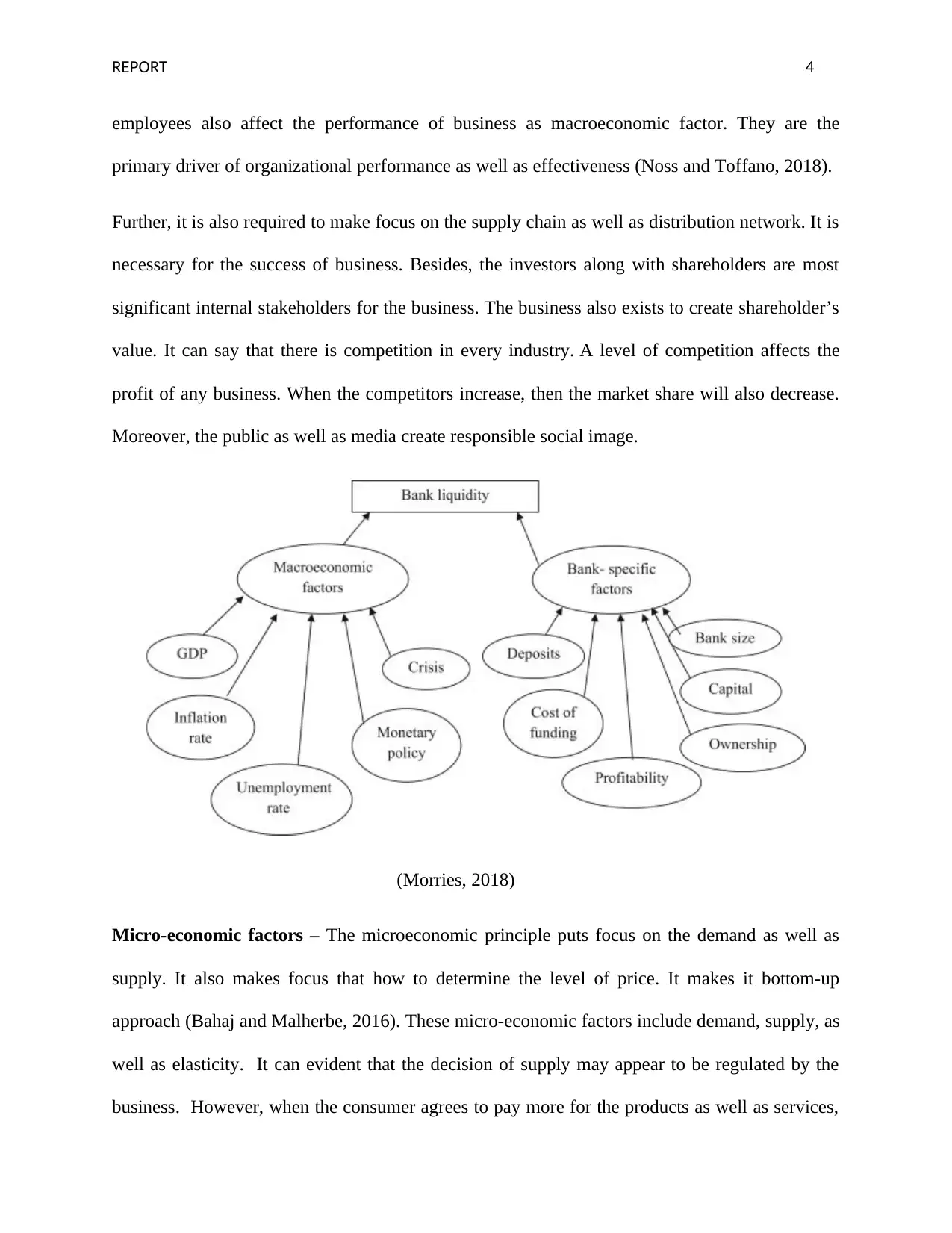

A. Analysis of economic factors and their impacts on business –

Macro-economic factors- the macroeconomic principle is helpful to understand the decisions

made by government along with nation. The macroeconomic factors are competitor, customer,

distribution channel, public, as well as supplier. It can say that these macroeconomic factors play

significant role in the business (Gandhi and Perumal, 2016). These key uncontrollable or

outer factors put impact on the powers of taking decision of the entity. The entity can make

better strategies to perform well. It can see that the customer is most significant factor in

microenvironment. The reason is that the business is centred on the customers. Additionally, the

Introduction –

Northern Rock was founded in 1850. It was operated as building society in initial period. It

provided banking along with financial services like mortgage services. It became joint stock

Company in year 1997. It was regulated by London stock Exchange. It was regulated as publicly

traded company. It can see that the bank was performed efficiently. But, it went through the

global banking crisis of 2007. It lowered the profit margin of bank. The bank became incapable

to make money from the loans and repay the loan amount, which has been borrowed by bank for

banking functions. The main objective of this paper is to render company analysis of the

company that has failed because of several economic factors. In the following parts, the macro-

economic factors as well as micro-economic factors, and their impacts are discussed and

examined. This report also discusses the accounting ratios and their impact on the business. The

below mentioned parts also make recommendation and conclusion.

A. Analysis of economic factors and their impacts on business –

Macro-economic factors- the macroeconomic principle is helpful to understand the decisions

made by government along with nation. The macroeconomic factors are competitor, customer,

distribution channel, public, as well as supplier. It can say that these macroeconomic factors play

significant role in the business (Gandhi and Perumal, 2016). These key uncontrollable or

outer factors put impact on the powers of taking decision of the entity. The entity can make

better strategies to perform well. It can see that the customer is most significant factor in

microenvironment. The reason is that the business is centred on the customers. Additionally, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 4

employees also affect the performance of business as macroeconomic factor. They are the

primary driver of organizational performance as well as effectiveness (Noss and Toffano, 2018).

Further, it is also required to make focus on the supply chain as well as distribution network. It is

necessary for the success of business. Besides, the investors along with shareholders are most

significant internal stakeholders for the business. The business also exists to create shareholder’s

value. It can say that there is competition in every industry. A level of competition affects the

profit of any business. When the competitors increase, then the market share will also decrease.

Moreover, the public as well as media create responsible social image.

(Morries, 2018)

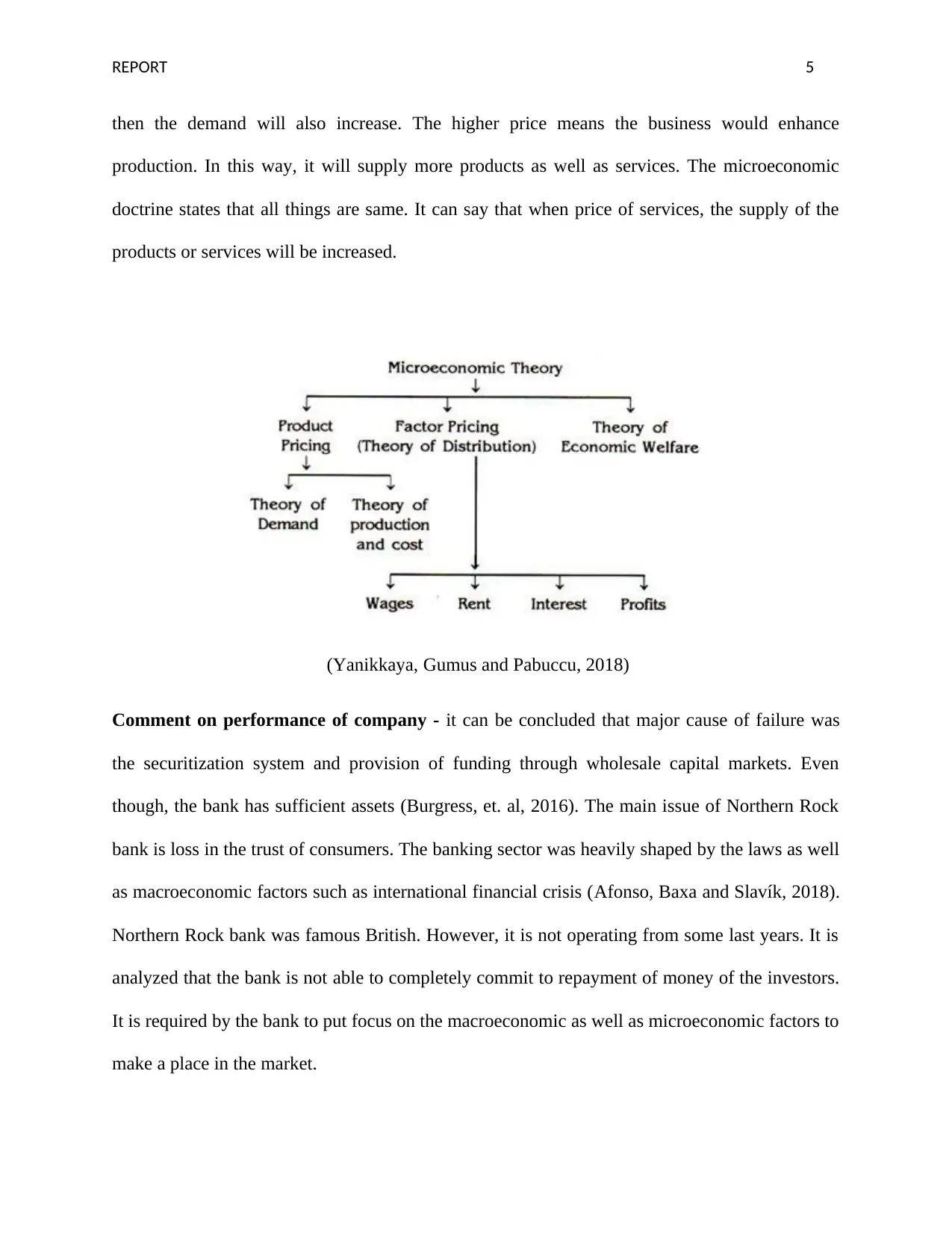

Micro-economic factors – The microeconomic principle puts focus on the demand as well as

supply. It also makes focus that how to determine the level of price. It makes it bottom-up

approach (Bahaj and Malherbe, 2016). These micro-economic factors include demand, supply, as

well as elasticity. It can evident that the decision of supply may appear to be regulated by the

business. However, when the consumer agrees to pay more for the products as well as services,

employees also affect the performance of business as macroeconomic factor. They are the

primary driver of organizational performance as well as effectiveness (Noss and Toffano, 2018).

Further, it is also required to make focus on the supply chain as well as distribution network. It is

necessary for the success of business. Besides, the investors along with shareholders are most

significant internal stakeholders for the business. The business also exists to create shareholder’s

value. It can say that there is competition in every industry. A level of competition affects the

profit of any business. When the competitors increase, then the market share will also decrease.

Moreover, the public as well as media create responsible social image.

(Morries, 2018)

Micro-economic factors – The microeconomic principle puts focus on the demand as well as

supply. It also makes focus that how to determine the level of price. It makes it bottom-up

approach (Bahaj and Malherbe, 2016). These micro-economic factors include demand, supply, as

well as elasticity. It can evident that the decision of supply may appear to be regulated by the

business. However, when the consumer agrees to pay more for the products as well as services,

REPORT 5

then the demand will also increase. The higher price means the business would enhance

production. In this way, it will supply more products as well as services. The microeconomic

doctrine states that all things are same. It can say that when price of services, the supply of the

products or services will be increased.

(Yanikkaya, Gumus and Pabuccu, 2018)

Comment on performance of company - it can be concluded that major cause of failure was

the securitization system and provision of funding through wholesale capital markets. Even

though, the bank has sufficient assets (Burgress, et. al, 2016). The main issue of Northern Rock

bank is loss in the trust of consumers. The banking sector was heavily shaped by the laws as well

as macroeconomic factors such as international financial crisis (Afonso, Baxa and Slavík, 2018).

Northern Rock bank was famous British. However, it is not operating from some last years. It is

analyzed that the bank is not able to completely commit to repayment of money of the investors.

It is required by the bank to put focus on the macroeconomic as well as microeconomic factors to

make a place in the market.

then the demand will also increase. The higher price means the business would enhance

production. In this way, it will supply more products as well as services. The microeconomic

doctrine states that all things are same. It can say that when price of services, the supply of the

products or services will be increased.

(Yanikkaya, Gumus and Pabuccu, 2018)

Comment on performance of company - it can be concluded that major cause of failure was

the securitization system and provision of funding through wholesale capital markets. Even

though, the bank has sufficient assets (Burgress, et. al, 2016). The main issue of Northern Rock

bank is loss in the trust of consumers. The banking sector was heavily shaped by the laws as well

as macroeconomic factors such as international financial crisis (Afonso, Baxa and Slavík, 2018).

Northern Rock bank was famous British. However, it is not operating from some last years. It is

analyzed that the bank is not able to completely commit to repayment of money of the investors.

It is required by the bank to put focus on the macroeconomic as well as microeconomic factors to

make a place in the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 6

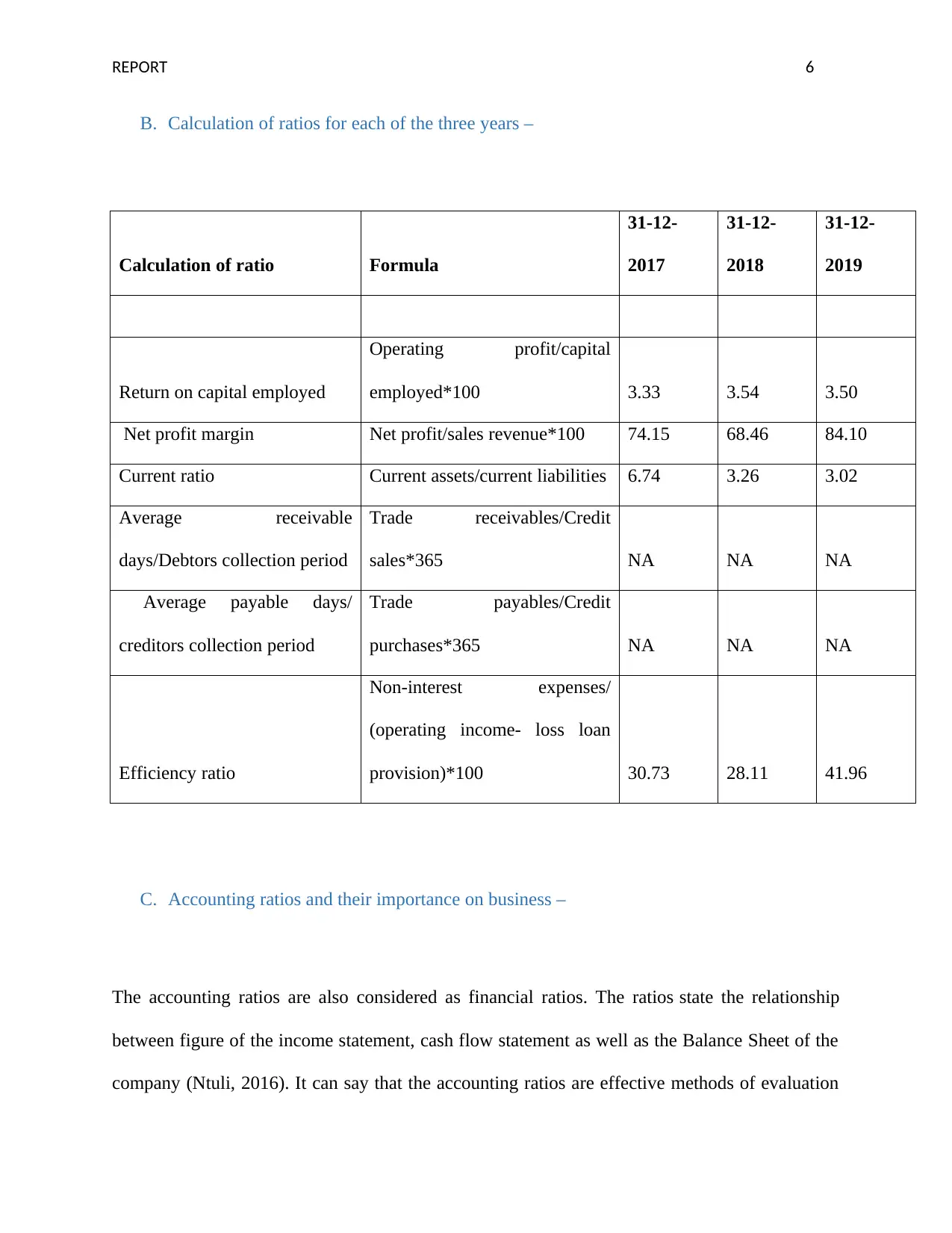

B. Calculation of ratios for each of the three years –

Calculation of ratio Formula

31-12-

2017

31-12-

2018

31-12-

2019

Return on capital employed

Operating profit/capital

employed*100 3.33 3.54 3.50

Net profit margin Net profit/sales revenue*100 74.15 68.46 84.10

Current ratio Current assets/current liabilities 6.74 3.26 3.02

Average receivable

days/Debtors collection period

Trade receivables/Credit

sales*365 NA NA NA

Average payable days/

creditors collection period

Trade payables/Credit

purchases*365 NA NA NA

Efficiency ratio

Non-interest expenses/

(operating income- loss loan

provision)*100 30.73 28.11 41.96

C. Accounting ratios and their importance on business –

The accounting ratios are also considered as financial ratios. The ratios state the relationship

between figure of the income statement, cash flow statement as well as the Balance Sheet of the

company (Ntuli, 2016). It can say that the accounting ratios are effective methods of evaluation

B. Calculation of ratios for each of the three years –

Calculation of ratio Formula

31-12-

2017

31-12-

2018

31-12-

2019

Return on capital employed

Operating profit/capital

employed*100 3.33 3.54 3.50

Net profit margin Net profit/sales revenue*100 74.15 68.46 84.10

Current ratio Current assets/current liabilities 6.74 3.26 3.02

Average receivable

days/Debtors collection period

Trade receivables/Credit

sales*365 NA NA NA

Average payable days/

creditors collection period

Trade payables/Credit

purchases*365 NA NA NA

Efficiency ratio

Non-interest expenses/

(operating income- loss loan

provision)*100 30.73 28.11 41.96

C. Accounting ratios and their importance on business –

The accounting ratios are also considered as financial ratios. The ratios state the relationship

between figure of the income statement, cash flow statement as well as the Balance Sheet of the

company (Ntuli, 2016). It can say that the accounting ratios are effective methods of evaluation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 7

utilised by the administration, shareholder, and creditor along with different stakeholders of

organisation. It is evident that the accounting ratios are considered as significant sub-set

of financial ratios. They are regarded as group of metrics that can be utilised to assess, solvency,

profitability as well as efficiency of the organisation based on the financial report. These ratios

render the manner of expressing the relationships between one accounting data point to other

point. In this way, they are base of ratio analysis (Blundell-Wignall, Atkinson and Roulet, 2018).

Further, the accounting ratios are significant to assess the financial performance of company.

They are helpful to evaluate profitability, efficiency, solvency, as well as risk. They are helpful

to make comparison between the trends of 2 or more than 2 companies over the period. In this

way, the accounting ratios can be utilised to measure the fundamentals of company.

Additionally, these ratios render data about the performance of an organisation over previous

quarter or financial year.

I. Return on capital employed – the Return on capital employed is a profitability ratio.

It can say that it is accounting ratio that can be used at the time of valuation. It has

important place in accounting. The Return on capital employed is helpful to compare

the relative profitability of the organisations after considering the amount of capital

utilised. In this way, the Return on capital employed is known as financial ratio. It is a

good measure for assessing the profitability as well as efficiency of the company. In

different terms, this ratio assesses how well the entity is making profit from the

capital. Therefore, this ratio is used as a ratio to measure the performance of company

(Rashwan and Ehab, 2017).

utilised by the administration, shareholder, and creditor along with different stakeholders of

organisation. It is evident that the accounting ratios are considered as significant sub-set

of financial ratios. They are regarded as group of metrics that can be utilised to assess, solvency,

profitability as well as efficiency of the organisation based on the financial report. These ratios

render the manner of expressing the relationships between one accounting data point to other

point. In this way, they are base of ratio analysis (Blundell-Wignall, Atkinson and Roulet, 2018).

Further, the accounting ratios are significant to assess the financial performance of company.

They are helpful to evaluate profitability, efficiency, solvency, as well as risk. They are helpful

to make comparison between the trends of 2 or more than 2 companies over the period. In this

way, the accounting ratios can be utilised to measure the fundamentals of company.

Additionally, these ratios render data about the performance of an organisation over previous

quarter or financial year.

I. Return on capital employed – the Return on capital employed is a profitability ratio.

It can say that it is accounting ratio that can be used at the time of valuation. It has

important place in accounting. The Return on capital employed is helpful to compare

the relative profitability of the organisations after considering the amount of capital

utilised. In this way, the Return on capital employed is known as financial ratio. It is a

good measure for assessing the profitability as well as efficiency of the company. In

different terms, this ratio assesses how well the entity is making profit from the

capital. Therefore, this ratio is used as a ratio to measure the performance of company

(Rashwan and Ehab, 2017).

REPORT 8

From the above calculation, it can say that the return on capital employed ratio of

Northern Rock Bank was 3.33 in year 2017. Further, this ratio was increased to 3.54

in 2018. In 2019, it was slightly decreased to 3.50. As it can see that bank has return

of 3.50 in 2018. In different terms, every dollar invested in employed capital, the

bank gets $3.50. In this way, the return may be high because it keeps lower level of

assets. This ratio states how much profits every dollar of employed capital makes. It

can see that the higher ratio will be favourable for the company for the reason that

more dollar of profit is made by each dollar of the capital employed. It is clear that

the company having small amount of asset as well as large amount of profit would

have the high return. From the above discussion, it is found that the company has

high return on capital employed but it needs to improve the return on capital

employed by reducing cost and increasing sales.

II. Net profit margin – the net profit margin is considered as percentage of revenue

excluding expenditures have been reduces from sale. The assessment states the

amount of profit that can be extracted from the total sale. The net profit margin ratio

is useful to define the capability of company to generate profits and to take different

matters in consideration, like increase in expenditures that is deemed unsuccessful. It

is very helpful in the financial model as well as valuation of company. It can say that

the net profit margin is solid display of the whole success of company. This ratio is

normally described as the percentage. However, the main thing to consider is that the

single number in the report of company is rarely adequate to consider the

performance of company. The increase in revenue may be converted into the loss if

From the above calculation, it can say that the return on capital employed ratio of

Northern Rock Bank was 3.33 in year 2017. Further, this ratio was increased to 3.54

in 2018. In 2019, it was slightly decreased to 3.50. As it can see that bank has return

of 3.50 in 2018. In different terms, every dollar invested in employed capital, the

bank gets $3.50. In this way, the return may be high because it keeps lower level of

assets. This ratio states how much profits every dollar of employed capital makes. It

can see that the higher ratio will be favourable for the company for the reason that

more dollar of profit is made by each dollar of the capital employed. It is clear that

the company having small amount of asset as well as large amount of profit would

have the high return. From the above discussion, it is found that the company has

high return on capital employed but it needs to improve the return on capital

employed by reducing cost and increasing sales.

II. Net profit margin – the net profit margin is considered as percentage of revenue

excluding expenditures have been reduces from sale. The assessment states the

amount of profit that can be extracted from the total sale. The net profit margin ratio

is useful to define the capability of company to generate profits and to take different

matters in consideration, like increase in expenditures that is deemed unsuccessful. It

is very helpful in the financial model as well as valuation of company. It can say that

the net profit margin is solid display of the whole success of company. This ratio is

normally described as the percentage. However, the main thing to consider is that the

single number in the report of company is rarely adequate to consider the

performance of company. The increase in revenue may be converted into the loss if

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REPORT 9

followed by the increase in expenditure. Alternatively, the reduction in revenue,

followed by best regulation over expenditures, may put entity further in profits

(Ariesta, Marlina and Hidayati, 2019).

From the above calculation, it can say that the net profit margin of Northern Rock

Bank was 74.15% in year 2017. Further, this margin was decreased to 68.46% in

2018. In 2019, it was increased to 84.10%. It means that the company is doing well.

However, the company needs to increase net margin by enhancing revenue. It is

required by the bank to sell more goods as well as services. It should also increase

the price. In this way, it can say that the bank can increase the net profit margin by

decreasing the costs. The company needs to find inexpensive sources for the raw

materials. The bank should also reduce the utilities to increase net profit margin. In

addition, the bank should find new customers to develop the business. However, it

may be the most expensive approach to generate more revenue. The products or

services with the highest gross profit margin are the most important to your business.

The bank should make strategy to attract more customers by focusing productive

services. After identifying the profitable services, the banks should focus on them. It

is required for the bank to determine whether the unprofitable services should be

removed in whole. The bank should review the area of improvement to make place in

the market.

III. Current ratio – The current ratio is also known as acid-test ratio or quick ratio. This

ratio is considered as liquidity ratio. It is helpful in measuring the capability of

company to make payment of short-term obligation (obligations due within 1 year). It

followed by the increase in expenditure. Alternatively, the reduction in revenue,

followed by best regulation over expenditures, may put entity further in profits

(Ariesta, Marlina and Hidayati, 2019).

From the above calculation, it can say that the net profit margin of Northern Rock

Bank was 74.15% in year 2017. Further, this margin was decreased to 68.46% in

2018. In 2019, it was increased to 84.10%. It means that the company is doing well.

However, the company needs to increase net margin by enhancing revenue. It is

required by the bank to sell more goods as well as services. It should also increase

the price. In this way, it can say that the bank can increase the net profit margin by

decreasing the costs. The company needs to find inexpensive sources for the raw

materials. The bank should also reduce the utilities to increase net profit margin. In

addition, the bank should find new customers to develop the business. However, it

may be the most expensive approach to generate more revenue. The products or

services with the highest gross profit margin are the most important to your business.

The bank should make strategy to attract more customers by focusing productive

services. After identifying the profitable services, the banks should focus on them. It

is required for the bank to determine whether the unprofitable services should be

removed in whole. The bank should review the area of improvement to make place in

the market.

III. Current ratio – The current ratio is also known as acid-test ratio or quick ratio. This

ratio is considered as liquidity ratio. It is helpful in measuring the capability of

company to make payment of short-term obligation (obligations due within 1 year). It

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT 10

is helpful for the investor along with analyst to know how the entity can increase

the current assets on the balance sheet for satisfying the current debt as well as other

payable (Osborne, Fuertes and Milne, 2017).

From the above calculation, it can say that the current of Northern Rock Bank was

6.74 in year 2017. Further, this margin was decreased to 3.26 in 2018. In 2019, it was

again decreased to 3.02. It can say that the company is not doing well. As it can see

that, the current ratio is 3.02 in 2019. The current ratio of 3.02:1 means that the

business has $ 3.02 of current assets for every $ 1 of current liabilities. The ideal

current ratio is 2:1. It is required by the company to improve current ratio. For

reducing the current ratio, it is required by the bank to increase short-term loans. The

bank needs to spend more cash in optimal way. The company should focus on the

amortization of prepaid expenses. In addition, the company should also focus on the

leaner working capital cycle (Tüysüz and Yıldız, 2019).

IV. Average receivable days/Debtors collection period – the average collection period

is average account receivable divided by average credit sales (Nyssa, 2019).

The average collection period is helpful in informing the business owners about the

the liquidity of accounts receivable of a company. It can see that this ratio renders

data about the credit policy of company. In this way, the business owners can assess

how well the credit policy of company is working by assessing average collection

period. It can see that this ratio is not applicable in case of bank (Chowdhury, 2019).

is helpful for the investor along with analyst to know how the entity can increase

the current assets on the balance sheet for satisfying the current debt as well as other

payable (Osborne, Fuertes and Milne, 2017).

From the above calculation, it can say that the current of Northern Rock Bank was

6.74 in year 2017. Further, this margin was decreased to 3.26 in 2018. In 2019, it was

again decreased to 3.02. It can say that the company is not doing well. As it can see

that, the current ratio is 3.02 in 2019. The current ratio of 3.02:1 means that the

business has $ 3.02 of current assets for every $ 1 of current liabilities. The ideal

current ratio is 2:1. It is required by the company to improve current ratio. For

reducing the current ratio, it is required by the bank to increase short-term loans. The

bank needs to spend more cash in optimal way. The company should focus on the

amortization of prepaid expenses. In addition, the company should also focus on the

leaner working capital cycle (Tüysüz and Yıldız, 2019).

IV. Average receivable days/Debtors collection period – the average collection period

is average account receivable divided by average credit sales (Nyssa, 2019).

The average collection period is helpful in informing the business owners about the

the liquidity of accounts receivable of a company. It can see that this ratio renders

data about the credit policy of company. In this way, the business owners can assess

how well the credit policy of company is working by assessing average collection

period. It can see that this ratio is not applicable in case of bank (Chowdhury, 2019).

REPORT 11

V. Average payable days/ creditors collection period – this ratio states that Creditor

Days are enhancing beyond the general trading terms of suppliers. It shows that the

company is not making payment to dealers as efficiently as it is required. The

downward trends in the Creditor Days ratio mean that the enhancing amount of the

cash (possibly from overdrafts) is required to funding business. In this, this can be the

issue for developing the business. This ratio is not applicable in case of bank

(Degryse, Matthews and Zhao, 2018).

VI. Efficiency ratio - The efficiency ratio indicates the expenditures as the percentage of

revenues, with some variations. This is significantly how much the entity or person

spends to generate dollar; the companies are supposed to attempt reducing efficiency

ratios.

From the above calculation, it can say that the current of Northern Rock Bank was

30.73 in year 2017. Further, this margin was decreased to 28.11 in 2018. In 2019, it

was again increased to 41.96. The efficiency ratio of 50% or below 50% is optimal

ratio. When this ratio increases, then it can say that the expenditures are enhancing or

the revenues are reducing. In this way, it can say that the company is doing well.

However, the bank should decrease efficiency ratio to the great extent because lower

efficiency ratio is better (Tvaronavičienė, Masood and Javaria, 2018).

D. Recommendations

As it can see that, the Northern Rock Bank has low profit margin. The bank also lost faith of the

customers. In this situation, it is suggested that the bank should try to get support of the

commercial buyers and government. The bank should follow different approaches to make its

V. Average payable days/ creditors collection period – this ratio states that Creditor

Days are enhancing beyond the general trading terms of suppliers. It shows that the

company is not making payment to dealers as efficiently as it is required. The

downward trends in the Creditor Days ratio mean that the enhancing amount of the

cash (possibly from overdrafts) is required to funding business. In this, this can be the

issue for developing the business. This ratio is not applicable in case of bank

(Degryse, Matthews and Zhao, 2018).

VI. Efficiency ratio - The efficiency ratio indicates the expenditures as the percentage of

revenues, with some variations. This is significantly how much the entity or person

spends to generate dollar; the companies are supposed to attempt reducing efficiency

ratios.

From the above calculation, it can say that the current of Northern Rock Bank was

30.73 in year 2017. Further, this margin was decreased to 28.11 in 2018. In 2019, it

was again increased to 41.96. The efficiency ratio of 50% or below 50% is optimal

ratio. When this ratio increases, then it can say that the expenditures are enhancing or

the revenues are reducing. In this way, it can say that the company is doing well.

However, the bank should decrease efficiency ratio to the great extent because lower

efficiency ratio is better (Tvaronavičienė, Masood and Javaria, 2018).

D. Recommendations

As it can see that, the Northern Rock Bank has low profit margin. The bank also lost faith of the

customers. In this situation, it is suggested that the bank should try to get support of the

commercial buyers and government. The bank should follow different approaches to make its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.