Natural Science Students: Introduction to Economics Basics Assignment

VerifiedAdded on 2021/07/28

|12

|4799

|74

Homework Assignment

AI Summary

This assignment provides a comprehensive introduction to the core concepts of economics, tailored for natural science students. It begins with a definition of economics, exploring its historical development and various perspectives. The assignment then delves into the rationales of economics, focusing on the fundamental facts of unlimited human wants and limited economic resources, emphasizing the central role of choice in addressing scarcity. It covers the scope and methods of economic analysis, differentiating between positive and normative economics, and explaining inductive and deductive reasoning. The assignment then explores scarcity, choice, and opportunity cost, including the production possibilities frontier (PPF) and its implications. It explains economic growth and its impact on the PPF. Finally, it addresses the basic economic questions of what, how, and for whom to produce, which are central to any economic system. This assignment is a valuable resource for students seeking a foundational understanding of economic principles.

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Chapter One

Basics of Economics

1.1 Definition of economics

Economics is one of the most exciting disciplines in social sciences. The word economy comes

from the Greek phrase ―one who manages a household‖. The science of economics in its current

form is about two hundred years old. Adam Smith – generally known as the father of economics

– brought out his famous book, ―An Inquiry into the Nature and Causes of Wealth of Nations‖,

in the year 1776. Though many other writers expressed important economic ideas before Adam

Smith, economics as a distinct subject started with his book. There is no universally accepted

definition of economics (its definition is controversial). This is because different economists

defined economics from different perspectives:

a. Wealth definition,

b. Welfare definition,

c. Scarcity definition, and

d. Growth definition

Hence, its definition varies as the nature and scope of the subject grow over time. But, the formal

and commonly accepted definition is as follow.

Economics is a social science which studies about efficient allocation of scarce resources so as

to attain the maximum fulfillment of unlimited human needs. As economics is a science of

choice, it studies how people choose to use scarce or limited productive resources (land, labour,

equipment, technical knowledge and the like) to produce various commodities.

1.2 The rationales of economics

There are two fundamental facts that provide the foundation for the field of economics.

1) Human (society‘s) material wants are unlimited.

2) Economic resources are limited (scarce).

The basic economic problem is about scarcity and choice since there are only limited amount

of resources available to produce the unlimited amount of goods and services we desire. Thus,

economics is the study of how human beings make choices to use scarce resources as they seek

to satisfy their unlimited wants. Therefore, choice is at the heart of all decision-making. As an

individual, family, and nation, we confront difficult choices about how to use limited resources

to meet our needs and wants. Economists study how these choices are made in various settings;

evaluate the outcomes in terms of criteria such as efficiency, equity, and stability; and search for

alternative forms of economic organization that might produce higher living standards or a more

desirable distribution of material well-being.

Scope and method of analysis in economics

1.3.1 Scope of economics

The field and scope of economics is expanding rapidly and has come to include a vast range of

topics and issues. In the recent past, many new branches of the subject have developed, including

development economics, industrial economics, transport economics, welfare economics,

environmental economics, and so on. However, the core of modern economics is

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Chapter One

Basics of Economics

1.1 Definition of economics

Economics is one of the most exciting disciplines in social sciences. The word economy comes

from the Greek phrase ―one who manages a household‖. The science of economics in its current

form is about two hundred years old. Adam Smith – generally known as the father of economics

– brought out his famous book, ―An Inquiry into the Nature and Causes of Wealth of Nations‖,

in the year 1776. Though many other writers expressed important economic ideas before Adam

Smith, economics as a distinct subject started with his book. There is no universally accepted

definition of economics (its definition is controversial). This is because different economists

defined economics from different perspectives:

a. Wealth definition,

b. Welfare definition,

c. Scarcity definition, and

d. Growth definition

Hence, its definition varies as the nature and scope of the subject grow over time. But, the formal

and commonly accepted definition is as follow.

Economics is a social science which studies about efficient allocation of scarce resources so as

to attain the maximum fulfillment of unlimited human needs. As economics is a science of

choice, it studies how people choose to use scarce or limited productive resources (land, labour,

equipment, technical knowledge and the like) to produce various commodities.

1.2 The rationales of economics

There are two fundamental facts that provide the foundation for the field of economics.

1) Human (society‘s) material wants are unlimited.

2) Economic resources are limited (scarce).

The basic economic problem is about scarcity and choice since there are only limited amount

of resources available to produce the unlimited amount of goods and services we desire. Thus,

economics is the study of how human beings make choices to use scarce resources as they seek

to satisfy their unlimited wants. Therefore, choice is at the heart of all decision-making. As an

individual, family, and nation, we confront difficult choices about how to use limited resources

to meet our needs and wants. Economists study how these choices are made in various settings;

evaluate the outcomes in terms of criteria such as efficiency, equity, and stability; and search for

alternative forms of economic organization that might produce higher living standards or a more

desirable distribution of material well-being.

Scope and method of analysis in economics

1.3.1 Scope of economics

The field and scope of economics is expanding rapidly and has come to include a vast range of

topics and issues. In the recent past, many new branches of the subject have developed, including

development economics, industrial economics, transport economics, welfare economics,

environmental economics, and so on. However, the core of modern economics is

Assosa University, college of Business and Economics, Department of Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

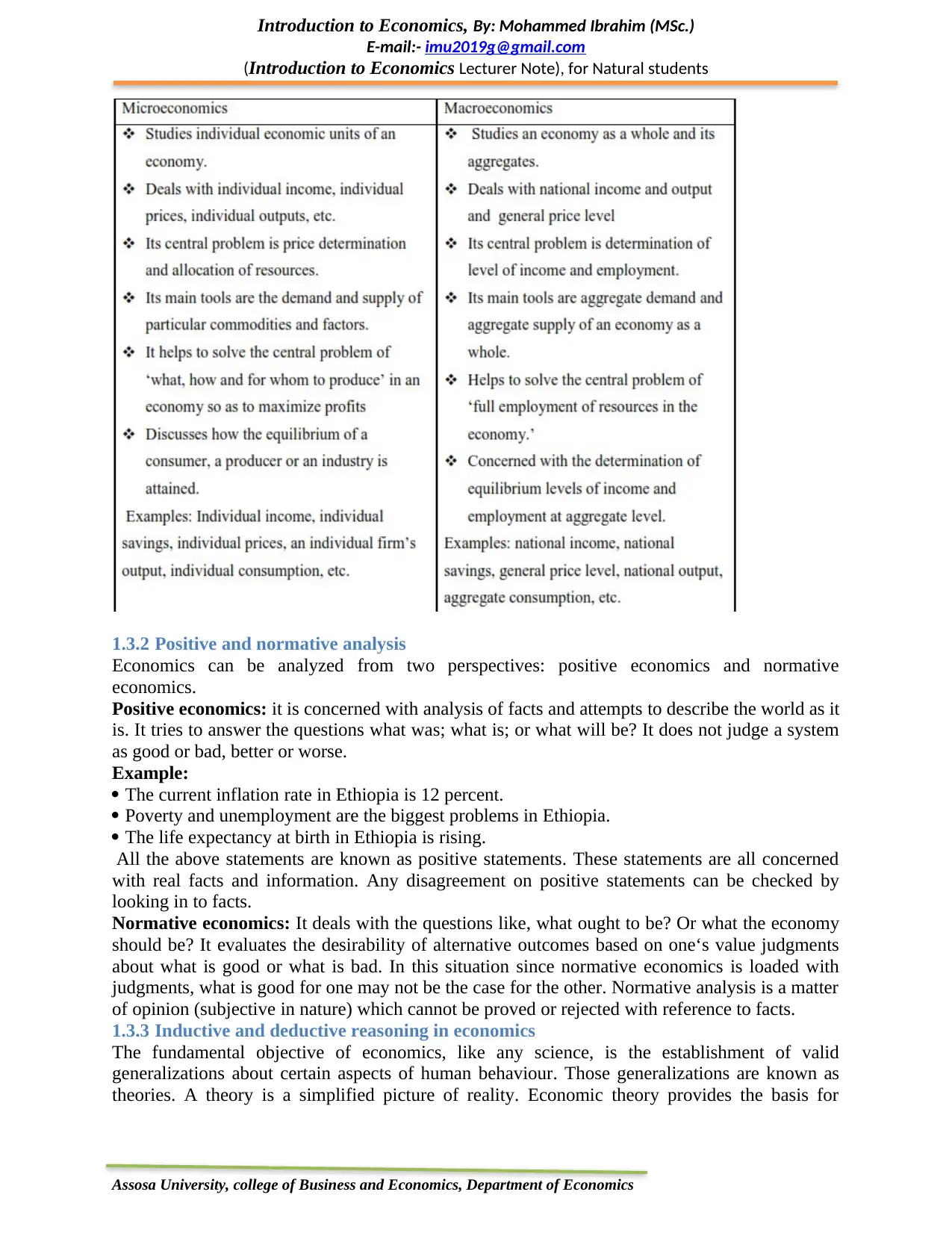

1.3.2 Positive and normative analysis

Economics can be analyzed from two perspectives: positive economics and normative

economics.

Positive economics: it is concerned with analysis of facts and attempts to describe the world as it

is. It tries to answer the questions what was; what is; or what will be? It does not judge a system

as good or bad, better or worse.

Example:

The current inflation rate in Ethiopia is 12 percent.

Poverty and unemployment are the biggest problems in Ethiopia.

The life expectancy at birth in Ethiopia is rising.

All the above statements are known as positive statements. These statements are all concerned

with real facts and information. Any disagreement on positive statements can be checked by

looking in to facts.

Normative economics: It deals with the questions like, what ought to be? Or what the economy

should be? It evaluates the desirability of alternative outcomes based on one‘s value judgments

about what is good or what is bad. In this situation since normative economics is loaded with

judgments, what is good for one may not be the case for the other. Normative analysis is a matter

of opinion (subjective in nature) which cannot be proved or rejected with reference to facts.

1.3.3 Inductive and deductive reasoning in economics

The fundamental objective of economics, like any science, is the establishment of valid

generalizations about certain aspects of human behaviour. Those generalizations are known as

theories. A theory is a simplified picture of reality. Economic theory provides the basis for

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

1.3.2 Positive and normative analysis

Economics can be analyzed from two perspectives: positive economics and normative

economics.

Positive economics: it is concerned with analysis of facts and attempts to describe the world as it

is. It tries to answer the questions what was; what is; or what will be? It does not judge a system

as good or bad, better or worse.

Example:

The current inflation rate in Ethiopia is 12 percent.

Poverty and unemployment are the biggest problems in Ethiopia.

The life expectancy at birth in Ethiopia is rising.

All the above statements are known as positive statements. These statements are all concerned

with real facts and information. Any disagreement on positive statements can be checked by

looking in to facts.

Normative economics: It deals with the questions like, what ought to be? Or what the economy

should be? It evaluates the desirability of alternative outcomes based on one‘s value judgments

about what is good or what is bad. In this situation since normative economics is loaded with

judgments, what is good for one may not be the case for the other. Normative analysis is a matter

of opinion (subjective in nature) which cannot be proved or rejected with reference to facts.

1.3.3 Inductive and deductive reasoning in economics

The fundamental objective of economics, like any science, is the establishment of valid

generalizations about certain aspects of human behaviour. Those generalizations are known as

theories. A theory is a simplified picture of reality. Economic theory provides the basis for

Assosa University, college of Business and Economics, Department of Economics

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

economic analysis which uses logical reasoning. There are two methods of logical reasoning:

inductive and deductive.

a) Inductive reasoning is a logical method of reaching at a correct general statement or theory

based on several independent and specific correct statements. In short, it is the process of

deriving a principle or theory by moving from facts to theories and from particular to general

economic analysis.

Inductive method involves the following steps.

1. Selecting problem for analysis

2. Collection, classification, and analysis of data

3. Establishing cause and effect relationship between economic phenomena.

b) Deductive reasoning is a logical way of arriving at a particular or specific correct statement

starting from a correct general statement. In short, it deals with conclusions about economic

phenomenon from certain fundamental assumptions or truths or axioms through a process of

logical arguments. The theory may agree or disagree with the real world and we should check the

validity of the theory to facts by moving from general to particular. Major steps in the deductive

approach include:

1. Problem identification

2. Specification of the assumptions

3. Formulating hypotheses

4. Testing the validity of the hypotheses

1.4 Scarcity, choice, opportunity cost and production possibilities frontier

It is often said that the central purpose of economic activity is the production of goods and

services to satisfy consumer‘s needs and wants i.e. to meet people‘s need for consumption both

as a means of survival and also to meet their ever-growing demand for an improved lifestyle or

standard of living.

1. Scarcity

The fundamental economic problem that any human society faces is the problem of scarcity.

Scarcity refers to the fact that all economic resources that a society needs to produce goods and

services are finite or limited in supply. But their being limited should be expressed in relation to

human wants. Thus, the term scarcity reflects the imbalance between our wants and the means to

satisfy those wants.

Economic resources are usually classified into four categories.

Labour: refers to the physical as well as mental efforts of human beings in the production

and distribution of goods and services. The reward for labour is called wage.

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

economic analysis which uses logical reasoning. There are two methods of logical reasoning:

inductive and deductive.

a) Inductive reasoning is a logical method of reaching at a correct general statement or theory

based on several independent and specific correct statements. In short, it is the process of

deriving a principle or theory by moving from facts to theories and from particular to general

economic analysis.

Inductive method involves the following steps.

1. Selecting problem for analysis

2. Collection, classification, and analysis of data

3. Establishing cause and effect relationship between economic phenomena.

b) Deductive reasoning is a logical way of arriving at a particular or specific correct statement

starting from a correct general statement. In short, it deals with conclusions about economic

phenomenon from certain fundamental assumptions or truths or axioms through a process of

logical arguments. The theory may agree or disagree with the real world and we should check the

validity of the theory to facts by moving from general to particular. Major steps in the deductive

approach include:

1. Problem identification

2. Specification of the assumptions

3. Formulating hypotheses

4. Testing the validity of the hypotheses

1.4 Scarcity, choice, opportunity cost and production possibilities frontier

It is often said that the central purpose of economic activity is the production of goods and

services to satisfy consumer‘s needs and wants i.e. to meet people‘s need for consumption both

as a means of survival and also to meet their ever-growing demand for an improved lifestyle or

standard of living.

1. Scarcity

The fundamental economic problem that any human society faces is the problem of scarcity.

Scarcity refers to the fact that all economic resources that a society needs to produce goods and

services are finite or limited in supply. But their being limited should be expressed in relation to

human wants. Thus, the term scarcity reflects the imbalance between our wants and the means to

satisfy those wants.

Economic resources are usually classified into four categories.

Labour: refers to the physical as well as mental efforts of human beings in the production

and distribution of goods and services. The reward for labour is called wage.

Assosa University, college of Business and Economics, Department of Economics

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Land: refers to the natural resources or all the free gifts of nature usable in the production of

goods and services. The reward for the services of land is known as rent.

Capital: refers to all the manufactured inputs that can be used to produce other goods and

services. Example: equipment, machinery, transport and communication facilities, etc. The

reward for the services of capital is called interest.

Entrepreneurship: refers to a special type of human talent that helps to organize and

manage other factors of production to produce goods and services and takes risk of making loses.

The reward for entrepreneurship is called profit.

Note: Scarcity does not mean shortage. We have already said that a good is said to be scarce if

the amount available is less than the amount people wish to have at zero price. But we say that

there is shortage of goods and services when people are unable to get the amount they want at the

prevailing or on going price. Shortage is a specific and short term problem but scarcity is a

universal and everlasting problem.

2. Choice

If resources are scarce, then output will be limited. If output is limited, then we cannot satisfy all

of our wants. Thus, choice must be made. Due to the problem of scarcity, individuals, firms and

government are forced to choose as to what output to produce, in what quantity, and what output

not to produce. In short, scarcity implies choice. Choice, in turn, implies cost. That means

whenever choice is made, an alternative opportunity is sacrificed. This cost is known as

opportunity cost.

3. Opportunity cost

In a world of scarcity, a decision to have more of one thing, at the same time, means a decision

to have less of another thing. The value of the next best alternative that must be sacrificed is,

therefore, the opportunity cost of the decision.

Definition: Opportunity cost is the amount or value of the next best alternative that must be

sacrificed (forgone) in order to obtain one more unit of a product. For example, suppose the

country spends all of its limited resources on the production of cloth or computer. If a given

amount of resources can produce either one meter of cloth or 20 units of computer, then the cost

of one meter of cloth is the 20 units of computer that must be sacrificed in order to produce a

meter of cloth.

When we say opportunity cost, we mean that:

It is measured in goods & services but not in money costs

It should be in line with the principle of substitution.

In conclusion, when opportunity cost of an activity increases people substitute other activities in

its place.

4. The Production Possibilities Frontier or Curve (PPF/ PPC)

The production possibilities frontier (PPF) is a curve that shows the various possible

combinations of goods and services that the society can produce given its resources and

technology. To draw the PPF we need the following assumptions. a. The quantity as well as

quality of economic resource available for use during the year is fixed.

b. There are two broad classes of output to be produced over the year.

c. The economy is operating at full employment and is achieving full production (efficiency).

d. Technology does not change during the year.

e. Some inputs are better adapted to the production of one good than to the production of the

other (specialization).

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Land: refers to the natural resources or all the free gifts of nature usable in the production of

goods and services. The reward for the services of land is known as rent.

Capital: refers to all the manufactured inputs that can be used to produce other goods and

services. Example: equipment, machinery, transport and communication facilities, etc. The

reward for the services of capital is called interest.

Entrepreneurship: refers to a special type of human talent that helps to organize and

manage other factors of production to produce goods and services and takes risk of making loses.

The reward for entrepreneurship is called profit.

Note: Scarcity does not mean shortage. We have already said that a good is said to be scarce if

the amount available is less than the amount people wish to have at zero price. But we say that

there is shortage of goods and services when people are unable to get the amount they want at the

prevailing or on going price. Shortage is a specific and short term problem but scarcity is a

universal and everlasting problem.

2. Choice

If resources are scarce, then output will be limited. If output is limited, then we cannot satisfy all

of our wants. Thus, choice must be made. Due to the problem of scarcity, individuals, firms and

government are forced to choose as to what output to produce, in what quantity, and what output

not to produce. In short, scarcity implies choice. Choice, in turn, implies cost. That means

whenever choice is made, an alternative opportunity is sacrificed. This cost is known as

opportunity cost.

3. Opportunity cost

In a world of scarcity, a decision to have more of one thing, at the same time, means a decision

to have less of another thing. The value of the next best alternative that must be sacrificed is,

therefore, the opportunity cost of the decision.

Definition: Opportunity cost is the amount or value of the next best alternative that must be

sacrificed (forgone) in order to obtain one more unit of a product. For example, suppose the

country spends all of its limited resources on the production of cloth or computer. If a given

amount of resources can produce either one meter of cloth or 20 units of computer, then the cost

of one meter of cloth is the 20 units of computer that must be sacrificed in order to produce a

meter of cloth.

When we say opportunity cost, we mean that:

It is measured in goods & services but not in money costs

It should be in line with the principle of substitution.

In conclusion, when opportunity cost of an activity increases people substitute other activities in

its place.

4. The Production Possibilities Frontier or Curve (PPF/ PPC)

The production possibilities frontier (PPF) is a curve that shows the various possible

combinations of goods and services that the society can produce given its resources and

technology. To draw the PPF we need the following assumptions. a. The quantity as well as

quality of economic resource available for use during the year is fixed.

b. There are two broad classes of output to be produced over the year.

c. The economy is operating at full employment and is achieving full production (efficiency).

d. Technology does not change during the year.

e. Some inputs are better adapted to the production of one good than to the production of the

other (specialization).

Assosa University, college of Business and Economics, Department of Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

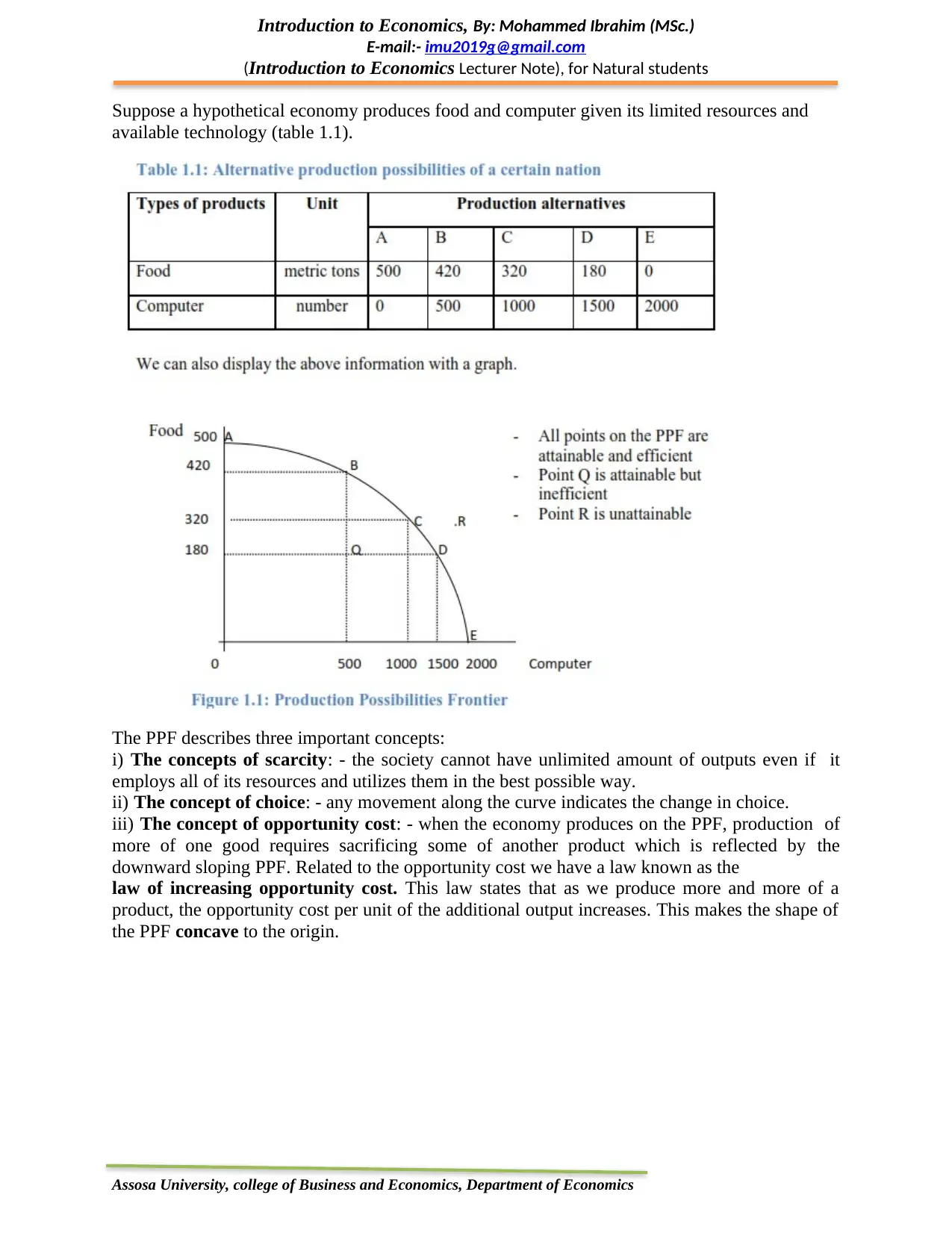

Suppose a hypothetical economy produces food and computer given its limited resources and

available technology (table 1.1).

The PPF describes three important concepts:

i) The concepts of scarcity: - the society cannot have unlimited amount of outputs even if it

employs all of its resources and utilizes them in the best possible way.

ii) The concept of choice: - any movement along the curve indicates the change in choice.

iii) The concept of opportunity cost: - when the economy produces on the PPF, production of

more of one good requires sacrificing some of another product which is reflected by the

downward sloping PPF. Related to the opportunity cost we have a law known as the

law of increasing opportunity cost. This law states that as we produce more and more of a

product, the opportunity cost per unit of the additional output increases. This makes the shape of

the PPF concave to the origin.

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Suppose a hypothetical economy produces food and computer given its limited resources and

available technology (table 1.1).

The PPF describes three important concepts:

i) The concepts of scarcity: - the society cannot have unlimited amount of outputs even if it

employs all of its resources and utilizes them in the best possible way.

ii) The concept of choice: - any movement along the curve indicates the change in choice.

iii) The concept of opportunity cost: - when the economy produces on the PPF, production of

more of one good requires sacrificing some of another product which is reflected by the

downward sloping PPF. Related to the opportunity cost we have a law known as the

law of increasing opportunity cost. This law states that as we produce more and more of a

product, the opportunity cost per unit of the additional output increases. This makes the shape of

the PPF concave to the origin.

Assosa University, college of Business and Economics, Department of Economics

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

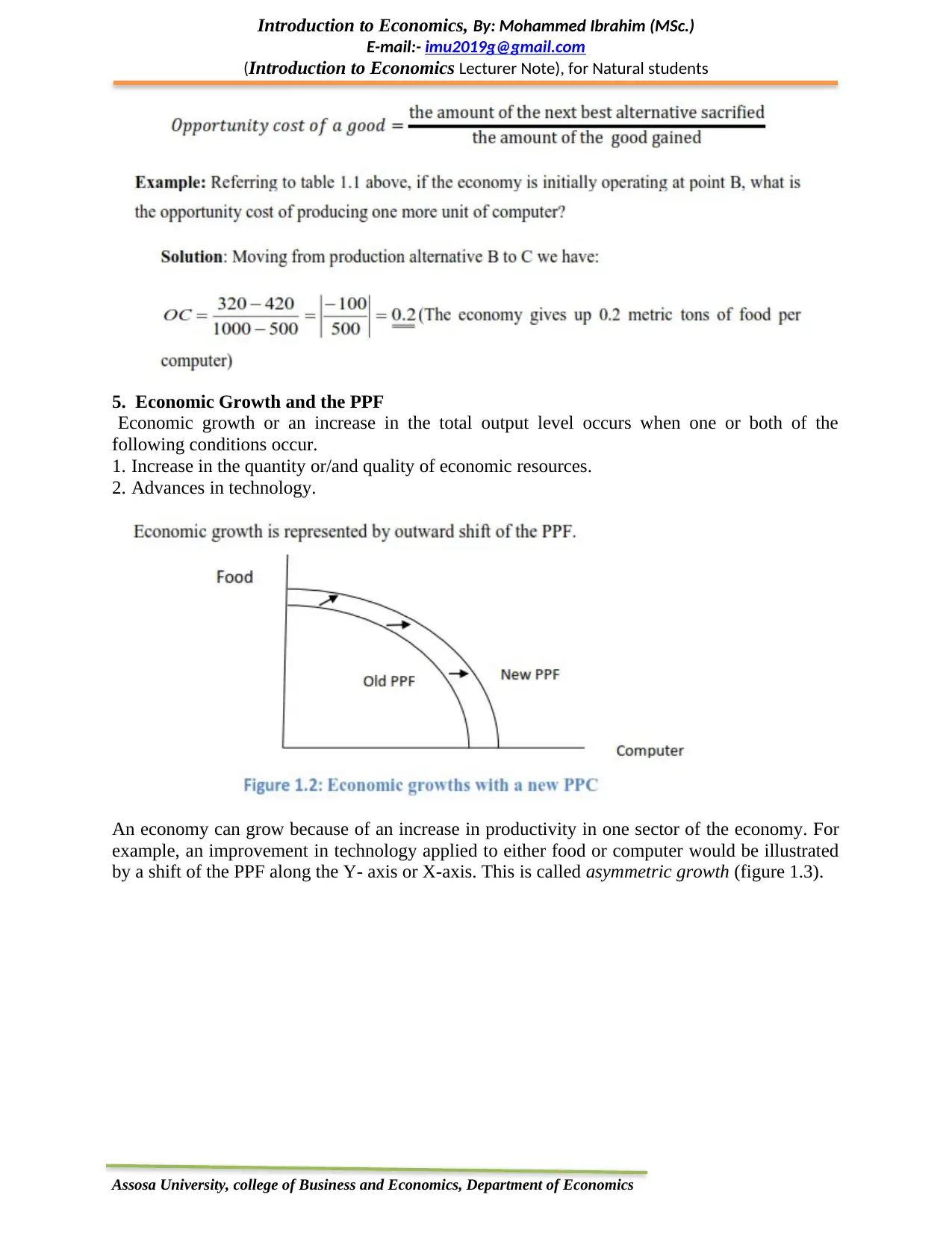

5. Economic Growth and the PPF

Economic growth or an increase in the total output level occurs when one or both of the

following conditions occur.

1. Increase in the quantity or/and quality of economic resources.

2. Advances in technology.

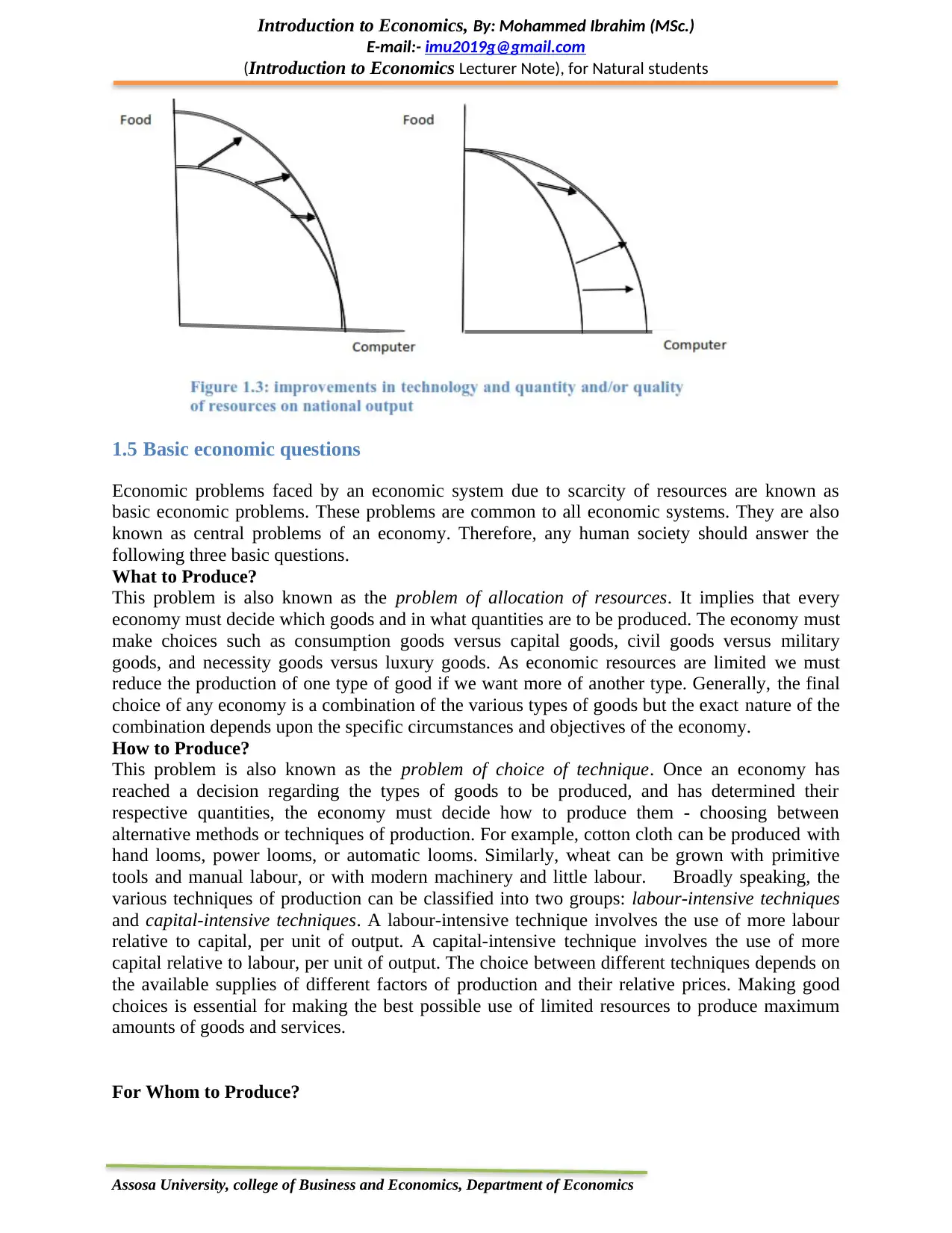

An economy can grow because of an increase in productivity in one sector of the economy. For

example, an improvement in technology applied to either food or computer would be illustrated

by a shift of the PPF along the Y- axis or X-axis. This is called asymmetric growth (figure 1.3).

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

5. Economic Growth and the PPF

Economic growth or an increase in the total output level occurs when one or both of the

following conditions occur.

1. Increase in the quantity or/and quality of economic resources.

2. Advances in technology.

An economy can grow because of an increase in productivity in one sector of the economy. For

example, an improvement in technology applied to either food or computer would be illustrated

by a shift of the PPF along the Y- axis or X-axis. This is called asymmetric growth (figure 1.3).

Assosa University, college of Business and Economics, Department of Economics

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

1.5 Basic economic questions

Economic problems faced by an economic system due to scarcity of resources are known as

basic economic problems. These problems are common to all economic systems. They are also

known as central problems of an economy. Therefore, any human society should answer the

following three basic questions.

What to Produce?

This problem is also known as the problem of allocation of resources. It implies that every

economy must decide which goods and in what quantities are to be produced. The economy must

make choices such as consumption goods versus capital goods, civil goods versus military

goods, and necessity goods versus luxury goods. As economic resources are limited we must

reduce the production of one type of good if we want more of another type. Generally, the final

choice of any economy is a combination of the various types of goods but the exact nature of the

combination depends upon the specific circumstances and objectives of the economy.

How to Produce?

This problem is also known as the problem of choice of technique. Once an economy has

reached a decision regarding the types of goods to be produced, and has determined their

respective quantities, the economy must decide how to produce them - choosing between

alternative methods or techniques of production. For example, cotton cloth can be produced with

hand looms, power looms, or automatic looms. Similarly, wheat can be grown with primitive

tools and manual labour, or with modern machinery and little labour. Broadly speaking, the

various techniques of production can be classified into two groups: labour-intensive techniques

and capital-intensive techniques. A labour-intensive technique involves the use of more labour

relative to capital, per unit of output. A capital-intensive technique involves the use of more

capital relative to labour, per unit of output. The choice between different techniques depends on

the available supplies of different factors of production and their relative prices. Making good

choices is essential for making the best possible use of limited resources to produce maximum

amounts of goods and services.

For Whom to Produce?

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

1.5 Basic economic questions

Economic problems faced by an economic system due to scarcity of resources are known as

basic economic problems. These problems are common to all economic systems. They are also

known as central problems of an economy. Therefore, any human society should answer the

following three basic questions.

What to Produce?

This problem is also known as the problem of allocation of resources. It implies that every

economy must decide which goods and in what quantities are to be produced. The economy must

make choices such as consumption goods versus capital goods, civil goods versus military

goods, and necessity goods versus luxury goods. As economic resources are limited we must

reduce the production of one type of good if we want more of another type. Generally, the final

choice of any economy is a combination of the various types of goods but the exact nature of the

combination depends upon the specific circumstances and objectives of the economy.

How to Produce?

This problem is also known as the problem of choice of technique. Once an economy has

reached a decision regarding the types of goods to be produced, and has determined their

respective quantities, the economy must decide how to produce them - choosing between

alternative methods or techniques of production. For example, cotton cloth can be produced with

hand looms, power looms, or automatic looms. Similarly, wheat can be grown with primitive

tools and manual labour, or with modern machinery and little labour. Broadly speaking, the

various techniques of production can be classified into two groups: labour-intensive techniques

and capital-intensive techniques. A labour-intensive technique involves the use of more labour

relative to capital, per unit of output. A capital-intensive technique involves the use of more

capital relative to labour, per unit of output. The choice between different techniques depends on

the available supplies of different factors of production and their relative prices. Making good

choices is essential for making the best possible use of limited resources to produce maximum

amounts of goods and services.

For Whom to Produce?

Assosa University, college of Business and Economics, Department of Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

This problem is also known as the problem of distribution of national product. It relates to how

a material product is to be distributed among the members of a society. The economy must

decide, for example, whether to produce for the benefit of the few rich people or for the large

number of poor people. An economy that wants to benefit the maximum number of persons

would first try to produce the necessities of the whole population and then to proceed to the

production of luxury goods. All these and other fundamental economic problems center around

human needs and wants. Many human efforts in society are directed towards the production of

goods and services to satisfy human needs and wants. These human efforts result in economic

activities that occur within the framework of an economic system.

1.6 Economic systems

The way a society tries to answer the above fundamental questions is summarized by a concept

known as economic system. An economic system is a set of organizational and institutional

arrangements established to answer the basic economic questions. Customarily, we can identify

three types of economic system. These are capitalism, command and mixed economy.

1.6.1 Capitalist economy

Capitalism is the oldest formal economic system in the world. It became widespread in the

middle of the 19th century. In this economic system, all means of production are privately owned,

and production takes place at the initiative of individual private entrepreneurs who work mainly

for private profit. Government intervention in the economy is minimal. This system is also called

free market economy or market system or laissez faire.

Features of Capitalistic Economy

The right to private property: The right to private property is a fundamental feature of a

capitalist economy. As part of that principle, economic or productive factors such as land,

factories, machinery, mines etc. are under private ownership.

Freedom of choice by consumers: Consumers can buy the goods and services that suit their

tastes and preferences. Producers produce goods in accordance with the wishes of the

consumers. This is known as the principle of consumer sovereignty.

Profit motive: Entrepreneurs, in their productive activity, are guided by the motive of profit-

making.

Competition: In a capitalist economy, competition exists among sellers or producers of

similar goods to attract customers. Among buyers, there is competition to obtain goods. Among

workers, the competition is to get jobs. Among employers, it is to get workers and investment

funds.

Price mechanism: All basic economic problems are solved through the price mechanism.

Minor role of government: The government does not interfere in day-to-day economic

activities and confines itself to defense and maintenance of law and order.

Self-interest: Each individual is guided by self-interest and motivated by the desire for

economic gain.

Inequalities of income: There is a wide economic gap between the rich and the poor.

Existence of negative externalities: A negative externality is the harm, cost, or

inconvenience suffered by a third party because of actions by others. In capitalistic economy,

decision of firms may result in negative externalities against another firm or society in general.

Advantages of Capitalistic Economy

Flexibility or adaptability: It successfully adapts itself to changing environments.

Decentralization of economic power: Market mechanisms work as a decentralizing force

against the concentration of economic power.

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

This problem is also known as the problem of distribution of national product. It relates to how

a material product is to be distributed among the members of a society. The economy must

decide, for example, whether to produce for the benefit of the few rich people or for the large

number of poor people. An economy that wants to benefit the maximum number of persons

would first try to produce the necessities of the whole population and then to proceed to the

production of luxury goods. All these and other fundamental economic problems center around

human needs and wants. Many human efforts in society are directed towards the production of

goods and services to satisfy human needs and wants. These human efforts result in economic

activities that occur within the framework of an economic system.

1.6 Economic systems

The way a society tries to answer the above fundamental questions is summarized by a concept

known as economic system. An economic system is a set of organizational and institutional

arrangements established to answer the basic economic questions. Customarily, we can identify

three types of economic system. These are capitalism, command and mixed economy.

1.6.1 Capitalist economy

Capitalism is the oldest formal economic system in the world. It became widespread in the

middle of the 19th century. In this economic system, all means of production are privately owned,

and production takes place at the initiative of individual private entrepreneurs who work mainly

for private profit. Government intervention in the economy is minimal. This system is also called

free market economy or market system or laissez faire.

Features of Capitalistic Economy

The right to private property: The right to private property is a fundamental feature of a

capitalist economy. As part of that principle, economic or productive factors such as land,

factories, machinery, mines etc. are under private ownership.

Freedom of choice by consumers: Consumers can buy the goods and services that suit their

tastes and preferences. Producers produce goods in accordance with the wishes of the

consumers. This is known as the principle of consumer sovereignty.

Profit motive: Entrepreneurs, in their productive activity, are guided by the motive of profit-

making.

Competition: In a capitalist economy, competition exists among sellers or producers of

similar goods to attract customers. Among buyers, there is competition to obtain goods. Among

workers, the competition is to get jobs. Among employers, it is to get workers and investment

funds.

Price mechanism: All basic economic problems are solved through the price mechanism.

Minor role of government: The government does not interfere in day-to-day economic

activities and confines itself to defense and maintenance of law and order.

Self-interest: Each individual is guided by self-interest and motivated by the desire for

economic gain.

Inequalities of income: There is a wide economic gap between the rich and the poor.

Existence of negative externalities: A negative externality is the harm, cost, or

inconvenience suffered by a third party because of actions by others. In capitalistic economy,

decision of firms may result in negative externalities against another firm or society in general.

Advantages of Capitalistic Economy

Flexibility or adaptability: It successfully adapts itself to changing environments.

Decentralization of economic power: Market mechanisms work as a decentralizing force

against the concentration of economic power.

Assosa University, college of Business and Economics, Department of Economics

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Increase in per-capita income and standard of living: Rapid growth in levels of production

and income leads to higher per-capita income and standards of living.

New types of consumer goods: Varieties of new consumer goods are developed and produced

at large scale.

Growth of entrepreneurship: Profit motive creates and supports new entrepreneurial skills

and approaches.

Optimum utilization of productive resources: Full utilization of productive resources is

possible due to innovations and technological progress.

High rate of capital formation: The right to private property helps in capital formation.

Disadvantages of Capitalistic Economy

Inequality of income: Capitalism promotes economic inequalities and creates social

imbalance.

Unbalanced economic activity: As there is no check on the economic system, the economy

can develop in an unbalanced way in terms of different geographic regions and different sections

of society.

Exploitation of labour: In a capitalistic economy, exploitation of labour (for example

bypaying low wages) is common.

Negative externalities: are problems in capitalistic economy where profit maximization is the

main objective of firms. If economic makes sense for a firm to force others to pay the impacts of

negative externalities such as pollution.

1.6.2 Command economy

Command economy is also known as socialistic economy. Under this economic system, the

economic institutions that are engaged in production and distribution are owned and controlled

by the state. In the recent past, socialism has lost its popularity and most of the socialist countries

are trying free market economies.

Main Features of Command Economy

Collective ownership: All means of production are owned by the society as a whole, and

there is no right to private property.

Central economic planning: Planning for resource allocation is performed by the controlling

authority according to given socio-economic goals.

Strong government role: Government has complete control over all economic activities.

Maximum social welfare: Command economy aims at maximizing social welfare and does

not allow the exploitation of labour.

Relative equality of incomes: Private property does not exist in a command economy, the

profit motive is absent, and there are no opportunities for accumulation of wealth. All these

factors lead to greater equality in income distribution, in comparison with capitalism.

Advantages of Command Economy

Absence of wasteful competition: There is no place for wasteful use of productive resources

through unhealthy competition.

Balanced economic growth: Allocation of resources through centralized planning leads to

balanced economic development. Different regions and different sectors of the economy can

develop equally.

Elimination of private monopolies and inequalities: Command economies avoid the major

evils of capitalism such as inequality of income and wealth, private monopolies, and

concentration of economic, political and social power.

Disadvantages of Command Economy

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Increase in per-capita income and standard of living: Rapid growth in levels of production

and income leads to higher per-capita income and standards of living.

New types of consumer goods: Varieties of new consumer goods are developed and produced

at large scale.

Growth of entrepreneurship: Profit motive creates and supports new entrepreneurial skills

and approaches.

Optimum utilization of productive resources: Full utilization of productive resources is

possible due to innovations and technological progress.

High rate of capital formation: The right to private property helps in capital formation.

Disadvantages of Capitalistic Economy

Inequality of income: Capitalism promotes economic inequalities and creates social

imbalance.

Unbalanced economic activity: As there is no check on the economic system, the economy

can develop in an unbalanced way in terms of different geographic regions and different sections

of society.

Exploitation of labour: In a capitalistic economy, exploitation of labour (for example

bypaying low wages) is common.

Negative externalities: are problems in capitalistic economy where profit maximization is the

main objective of firms. If economic makes sense for a firm to force others to pay the impacts of

negative externalities such as pollution.

1.6.2 Command economy

Command economy is also known as socialistic economy. Under this economic system, the

economic institutions that are engaged in production and distribution are owned and controlled

by the state. In the recent past, socialism has lost its popularity and most of the socialist countries

are trying free market economies.

Main Features of Command Economy

Collective ownership: All means of production are owned by the society as a whole, and

there is no right to private property.

Central economic planning: Planning for resource allocation is performed by the controlling

authority according to given socio-economic goals.

Strong government role: Government has complete control over all economic activities.

Maximum social welfare: Command economy aims at maximizing social welfare and does

not allow the exploitation of labour.

Relative equality of incomes: Private property does not exist in a command economy, the

profit motive is absent, and there are no opportunities for accumulation of wealth. All these

factors lead to greater equality in income distribution, in comparison with capitalism.

Advantages of Command Economy

Absence of wasteful competition: There is no place for wasteful use of productive resources

through unhealthy competition.

Balanced economic growth: Allocation of resources through centralized planning leads to

balanced economic development. Different regions and different sectors of the economy can

develop equally.

Elimination of private monopolies and inequalities: Command economies avoid the major

evils of capitalism such as inequality of income and wealth, private monopolies, and

concentration of economic, political and social power.

Disadvantages of Command Economy

Assosa University, college of Business and Economics, Department of Economics

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Absence of automatic price determination: Since all economic activities are controlled by

the government, there is no automatic price mechanism.

Absence of incentives for hard work and efficiency: The entire system depends on

bureaucrats who are considered inefficient in running businesses. There is no financial incentive

for hard work and efficiency. The economy grows at a relatively slow rate.

Lack of economic freedom: Economic freedom for consumers, producers, investors, and

employers is totally absent, and all economic powers are concentrated in the hands of the

government.

Red-tapism: it is widely prevalent in a command economy because all decisions are made by

government officials.

1.6.3 Mixed economy

A mixed economy is an attempt to combine the advantages of both the capitalistic economy and

the command economy. It incorporates some of the features of both and allows private and

public sectors to co-exist.

Main Features of Mixed Economy

Co-existence of public and private sectors: Public and private sectors co-exist in this

system. Their respective roles and aims are well-defined. Industries of national and strategic

importance, such as heavy and basic industry, defense production, power generation, etc. are set

up in the public sector, whereas consumer-goods industry and small-scale industry are developed

through the private sector.

Economic welfare: Economic welfare is the most important criterion of the success of a

mixed economy. The public sector tries to remove regional imbalances, provides large

employment opportunities and seeks economic welfare through its price policy. Government

control over the private sector leads to economic welfare of society at large.

Economic planning: The government uses instruments of economic planning to achieve co-

ordinated rapid economic development, making use of both the private and the public sector.

Price mechanism: The price mechanism operates for goods produced in the private sector, but

not for essential commodities and goods produced in the public sector. Those prices are defined

and regulated by the government.

Economic equality: Private property is allowed, but rules exist to prevent concentration of

wealth. Limits are fixed for owning land and property. Progressive taxation, concessions and

subsides are implemented to achieve economic equality.

Advantages of Mixed Economy

Private property, profit motive and price mechanism: All the advantages of a capitalistic

economy, such as the right to private property, motivation through the profit motive, and control

of economic activity through the price mechanism, are available in a mixed economy. At the

same time, government control ensures that they do not lead to exploitation.

Adequate freedom: Mixed economies allow adequate freedom to different economic units

such as consumers, employees, producers, and investors.

Rapid and planned economic development: Planned economic growth takes place, resources

are properly and efficiently utilized, and fast economic development takes place because the

private and public sector complement each other.

Social welfare and fewer economic inequalities: The government‘s restricted control over

economic activities helps in achieving social welfare and economic equality.

Disadvantages of Mixed Economy

Ineffectiveness and inefficiency: A mixed economy might not actually have the usual

advantages of either the public sector or the private sector. The public sector might be inefficient

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Absence of automatic price determination: Since all economic activities are controlled by

the government, there is no automatic price mechanism.

Absence of incentives for hard work and efficiency: The entire system depends on

bureaucrats who are considered inefficient in running businesses. There is no financial incentive

for hard work and efficiency. The economy grows at a relatively slow rate.

Lack of economic freedom: Economic freedom for consumers, producers, investors, and

employers is totally absent, and all economic powers are concentrated in the hands of the

government.

Red-tapism: it is widely prevalent in a command economy because all decisions are made by

government officials.

1.6.3 Mixed economy

A mixed economy is an attempt to combine the advantages of both the capitalistic economy and

the command economy. It incorporates some of the features of both and allows private and

public sectors to co-exist.

Main Features of Mixed Economy

Co-existence of public and private sectors: Public and private sectors co-exist in this

system. Their respective roles and aims are well-defined. Industries of national and strategic

importance, such as heavy and basic industry, defense production, power generation, etc. are set

up in the public sector, whereas consumer-goods industry and small-scale industry are developed

through the private sector.

Economic welfare: Economic welfare is the most important criterion of the success of a

mixed economy. The public sector tries to remove regional imbalances, provides large

employment opportunities and seeks economic welfare through its price policy. Government

control over the private sector leads to economic welfare of society at large.

Economic planning: The government uses instruments of economic planning to achieve co-

ordinated rapid economic development, making use of both the private and the public sector.

Price mechanism: The price mechanism operates for goods produced in the private sector, but

not for essential commodities and goods produced in the public sector. Those prices are defined

and regulated by the government.

Economic equality: Private property is allowed, but rules exist to prevent concentration of

wealth. Limits are fixed for owning land and property. Progressive taxation, concessions and

subsides are implemented to achieve economic equality.

Advantages of Mixed Economy

Private property, profit motive and price mechanism: All the advantages of a capitalistic

economy, such as the right to private property, motivation through the profit motive, and control

of economic activity through the price mechanism, are available in a mixed economy. At the

same time, government control ensures that they do not lead to exploitation.

Adequate freedom: Mixed economies allow adequate freedom to different economic units

such as consumers, employees, producers, and investors.

Rapid and planned economic development: Planned economic growth takes place, resources

are properly and efficiently utilized, and fast economic development takes place because the

private and public sector complement each other.

Social welfare and fewer economic inequalities: The government‘s restricted control over

economic activities helps in achieving social welfare and economic equality.

Disadvantages of Mixed Economy

Ineffectiveness and inefficiency: A mixed economy might not actually have the usual

advantages of either the public sector or the private sector. The public sector might be inefficient

Assosa University, college of Business and Economics, Department of Economics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

due to lack of incentive and responsibility, and the private sector might be made ineffective by

government regulation and control.

Economic fluctuations: If the private sector is not properly controlled by the government,

economic fluctuations and unemployment can occur.

Corruption and black markets: if government policies, rules and directives are not

effectively implemented, the economy can be vulnerable to increased corruption and black

market activities.

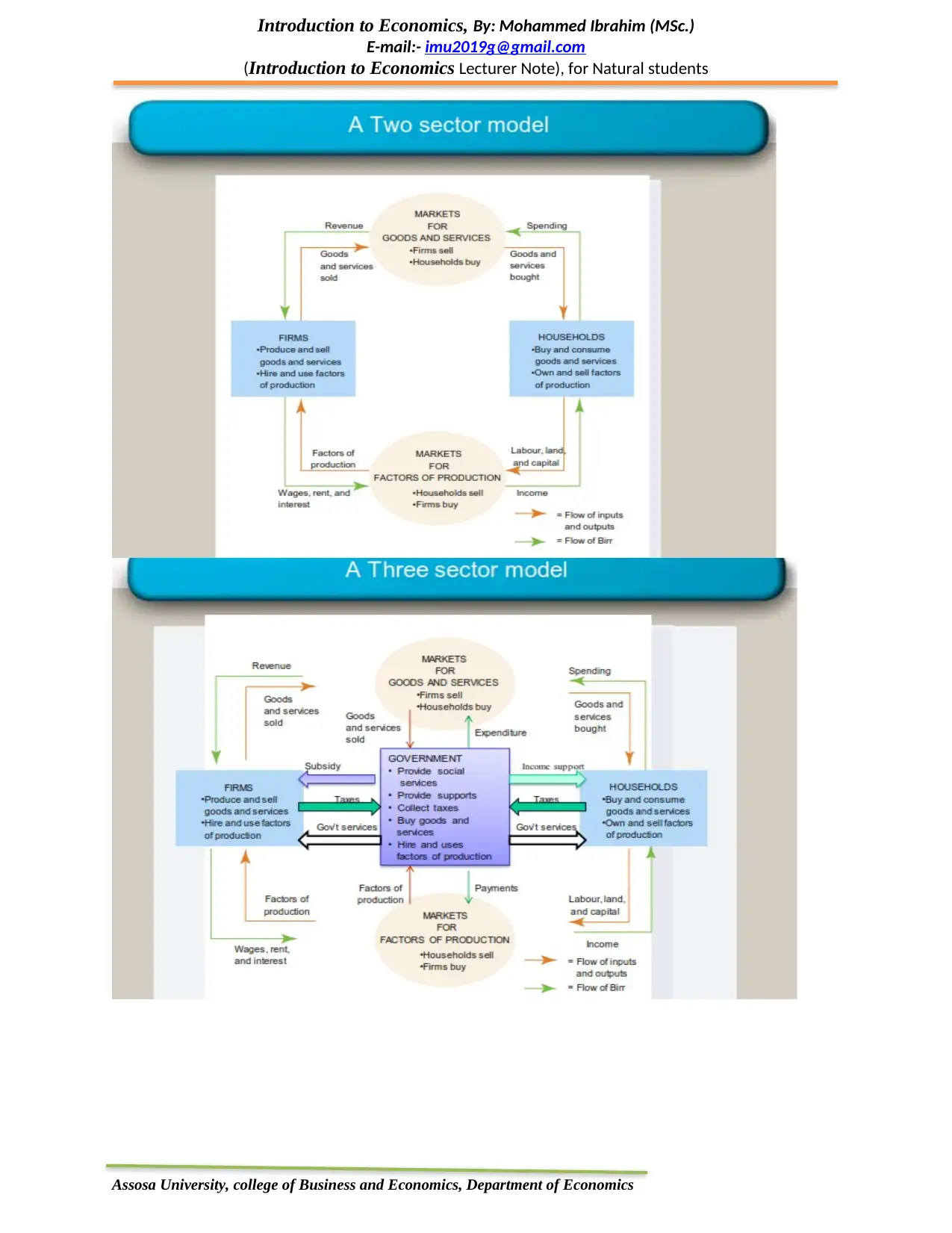

1.7 Decision making units and the circular flow model

There are three decision making units in a closed economy. These are households, firms and the

government.

i) Household: A household can be one person or more who live under one roof and make joint

financial decisions. Households make two decisions.

a) Selling of their resources, and

b) Buying of goods and services.

ii) Firm: A firm is a production unit that uses economic resources to produce goods and

services. Firms also make two decisions:

a) Buying of economic resources

b) Selling of their products.

iii) Government: A government is an organization that has legal and political power to control

or influence households, firms and markets. Government also provides some types of goods and

services known as public goods and services for the society. The three economic agents

interact in two markets:

o Product market: it is a market where goods and services are transacted/ exchanged. That is, a

market where households and governments buy goods and services from business firms.

o Factor market (input market): it is a market where economic units transact/exchange factors

of production (inputs). In this market, owners of resources (households) sell their resources to

business firms and governments. The circular-flow diagram is a visual model of the economy

that shows how money (Birr), economic resources and goods and services flows through markets

among the decision making units. For simplicity, let‘s first see a two sector model where we

have only households and business firms. In this case, therefore, we see the flow of goods and

services from producers to households and a flow of resources from households to business

firms. In the following diagram, the clock – wise direction shows the flow of economic

resources and final goods and services. Business firms sell goods and services to households in

product markets (upper part of the diagram). On the other hand, the lower part shows, where

households sell factors of production to business firms through factor market. The anti – clock

wise direction indicates the flow of birr (in the form of revenue, income and spending on

consumption). Firms, by selling goods and services to households, receive money in the form of

revenue which is consumption expenditure for households in the product market. On the other

hand, households by supplying their resources to firms receive income. This represents

expenditure by firms to purchase factors of production which is used as an input to produce

goods and services.

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

due to lack of incentive and responsibility, and the private sector might be made ineffective by

government regulation and control.

Economic fluctuations: If the private sector is not properly controlled by the government,

economic fluctuations and unemployment can occur.

Corruption and black markets: if government policies, rules and directives are not

effectively implemented, the economy can be vulnerable to increased corruption and black

market activities.

1.7 Decision making units and the circular flow model

There are three decision making units in a closed economy. These are households, firms and the

government.

i) Household: A household can be one person or more who live under one roof and make joint

financial decisions. Households make two decisions.

a) Selling of their resources, and

b) Buying of goods and services.

ii) Firm: A firm is a production unit that uses economic resources to produce goods and

services. Firms also make two decisions:

a) Buying of economic resources

b) Selling of their products.

iii) Government: A government is an organization that has legal and political power to control

or influence households, firms and markets. Government also provides some types of goods and

services known as public goods and services for the society. The three economic agents

interact in two markets:

o Product market: it is a market where goods and services are transacted/ exchanged. That is, a

market where households and governments buy goods and services from business firms.

o Factor market (input market): it is a market where economic units transact/exchange factors

of production (inputs). In this market, owners of resources (households) sell their resources to

business firms and governments. The circular-flow diagram is a visual model of the economy

that shows how money (Birr), economic resources and goods and services flows through markets

among the decision making units. For simplicity, let‘s first see a two sector model where we

have only households and business firms. In this case, therefore, we see the flow of goods and

services from producers to households and a flow of resources from households to business

firms. In the following diagram, the clock – wise direction shows the flow of economic

resources and final goods and services. Business firms sell goods and services to households in

product markets (upper part of the diagram). On the other hand, the lower part shows, where

households sell factors of production to business firms through factor market. The anti – clock

wise direction indicates the flow of birr (in the form of revenue, income and spending on

consumption). Firms, by selling goods and services to households, receive money in the form of

revenue which is consumption expenditure for households in the product market. On the other

hand, households by supplying their resources to firms receive income. This represents

expenditure by firms to purchase factors of production which is used as an input to produce

goods and services.

Assosa University, college of Business and Economics, Department of Economics

Introduction to Economics, By: Mohammed Ibrahim (MSc.)

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Assosa University, college of Business and Economics, Department of Economics

E-mail:- imu2019g@gmail.com

(Introduction to Economics Lecturer Note), for Natural students

Assosa University, college of Business and Economics, Department of Economics

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.