Economics Assignment 1: Market Dynamics, Elasticity and Costs

VerifiedAdded on 2020/04/21

|12

|1153

|107

Homework Assignment

AI Summary

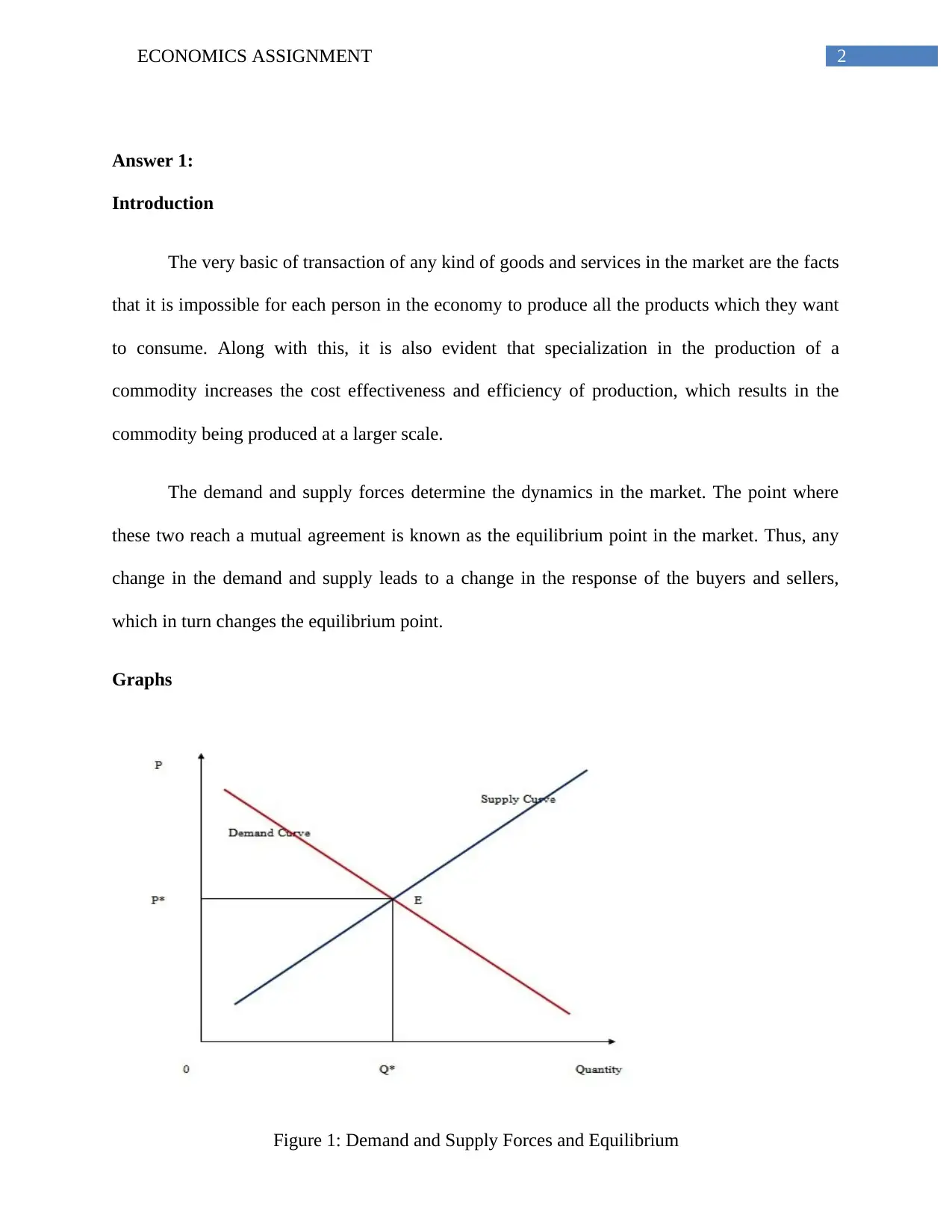

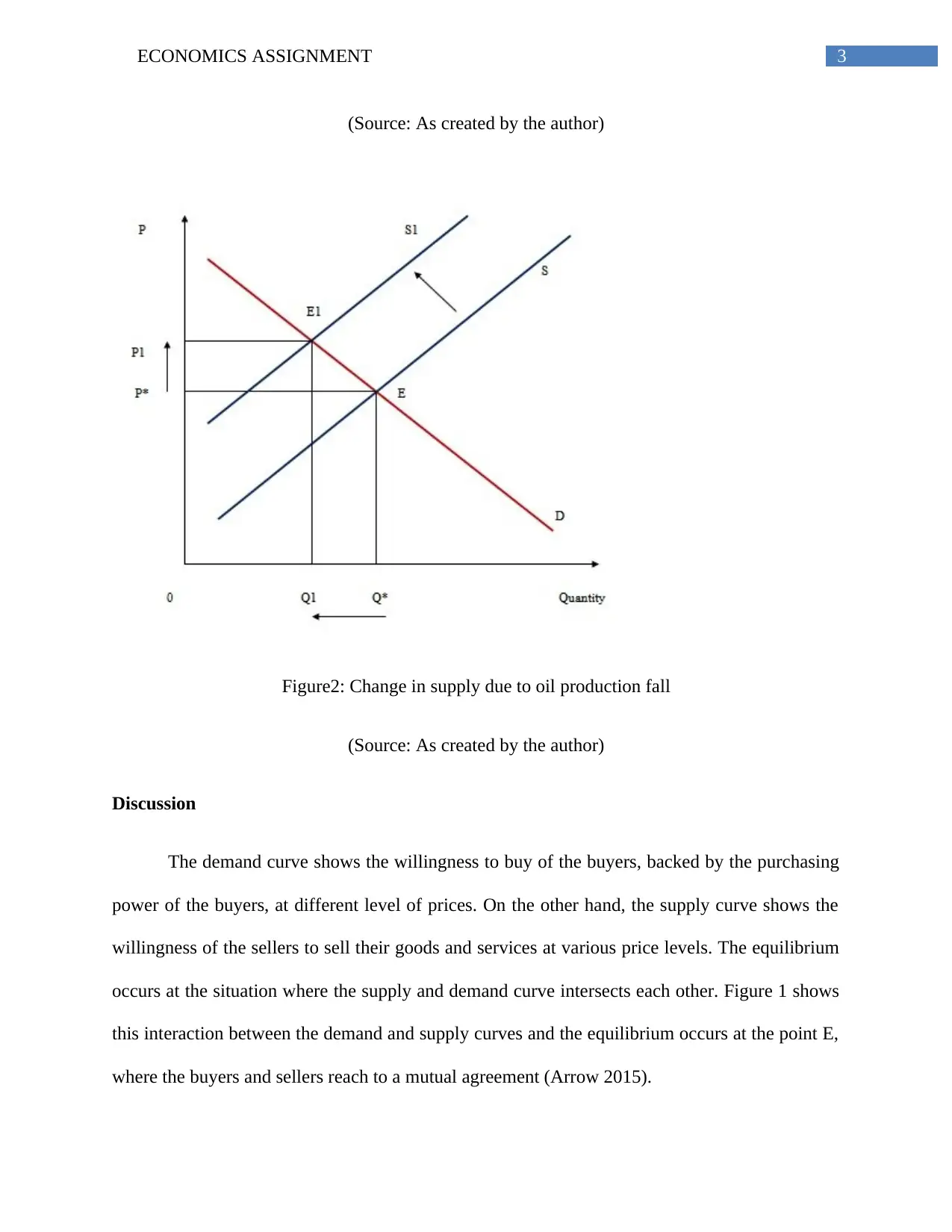

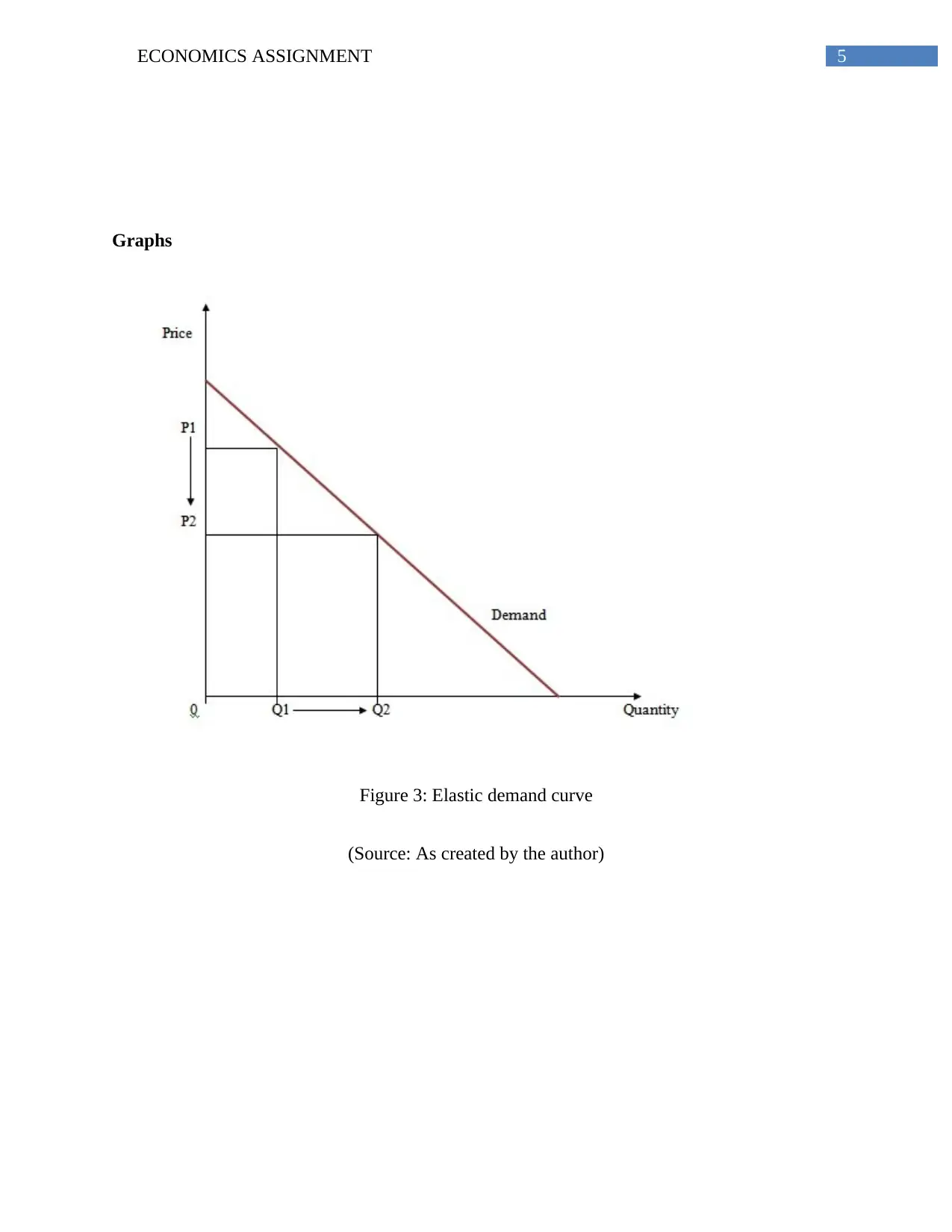

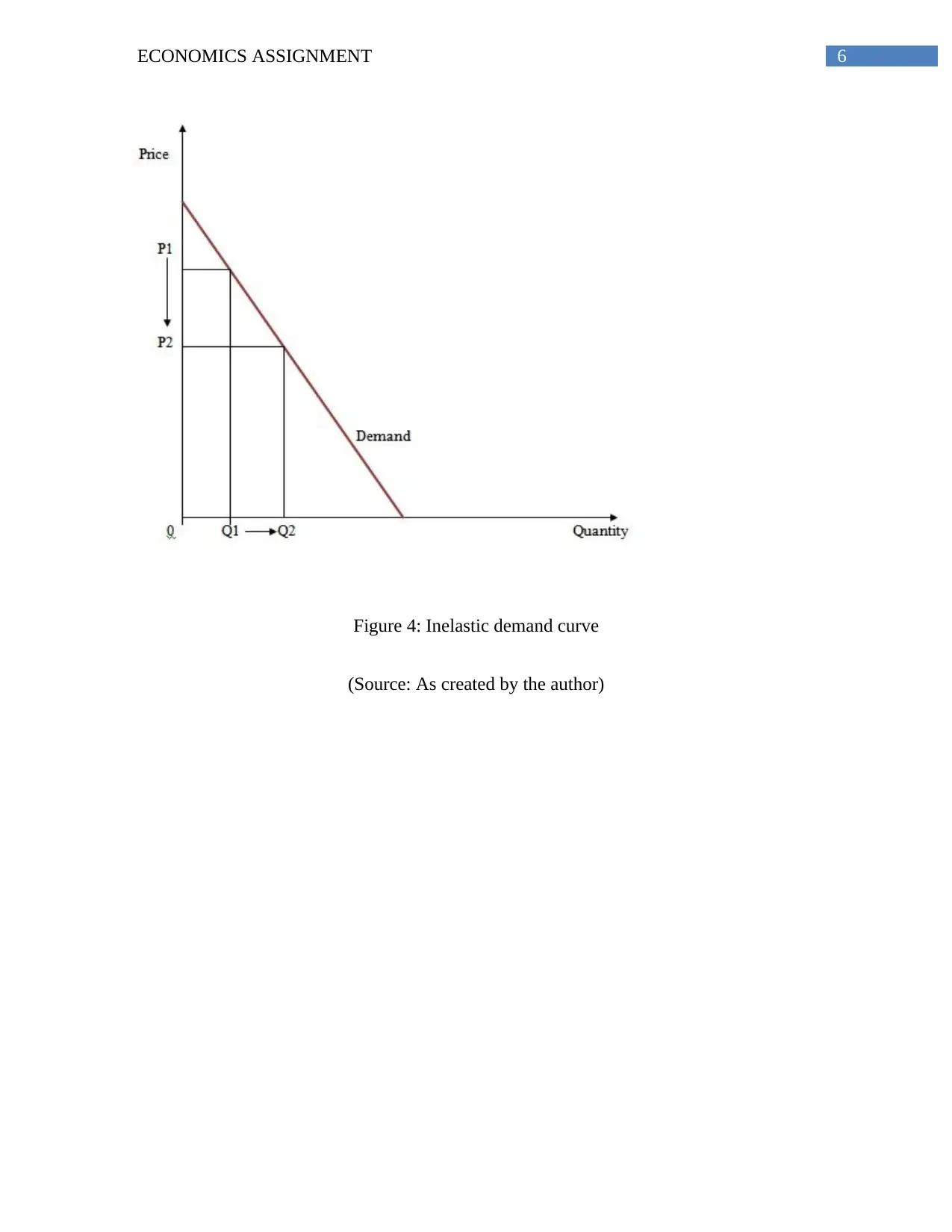

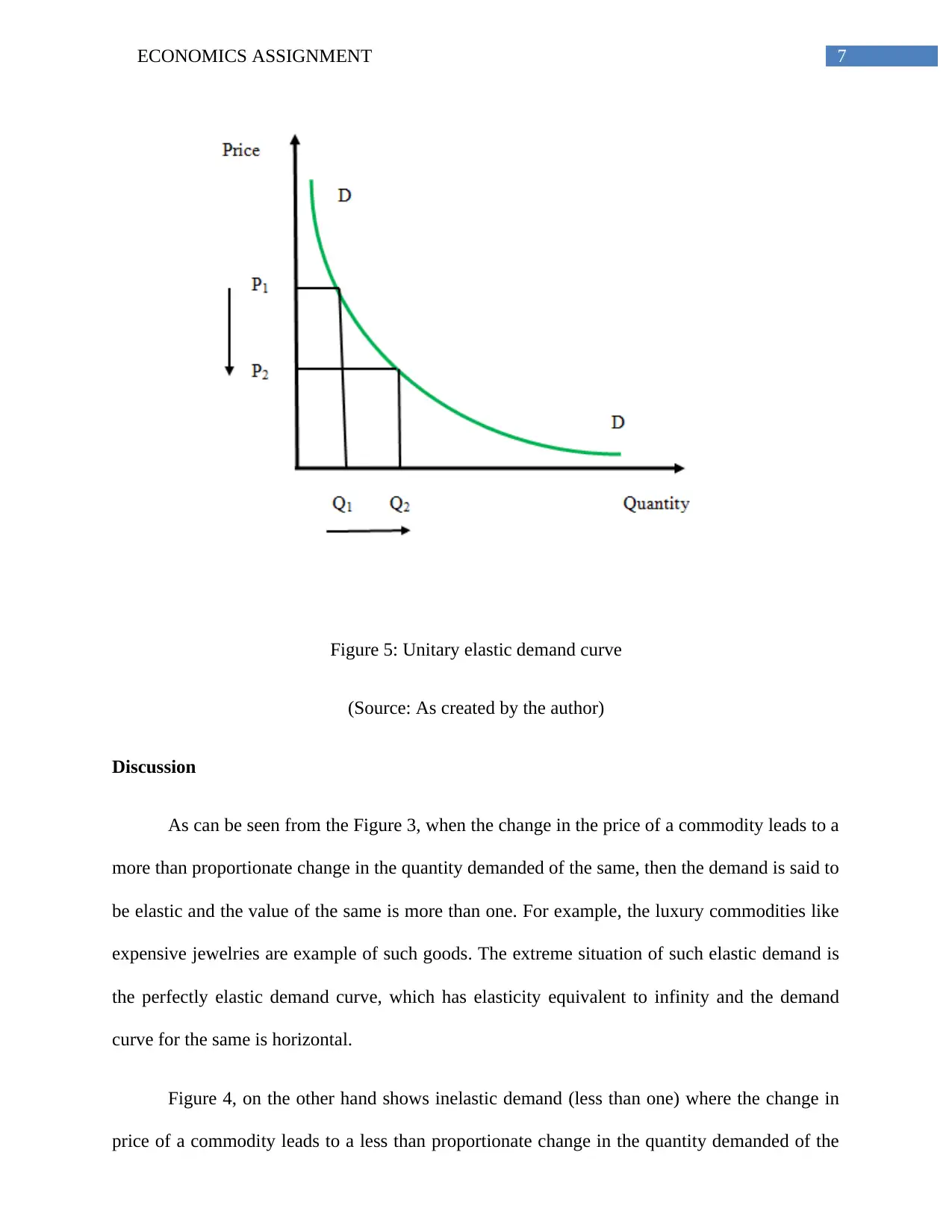

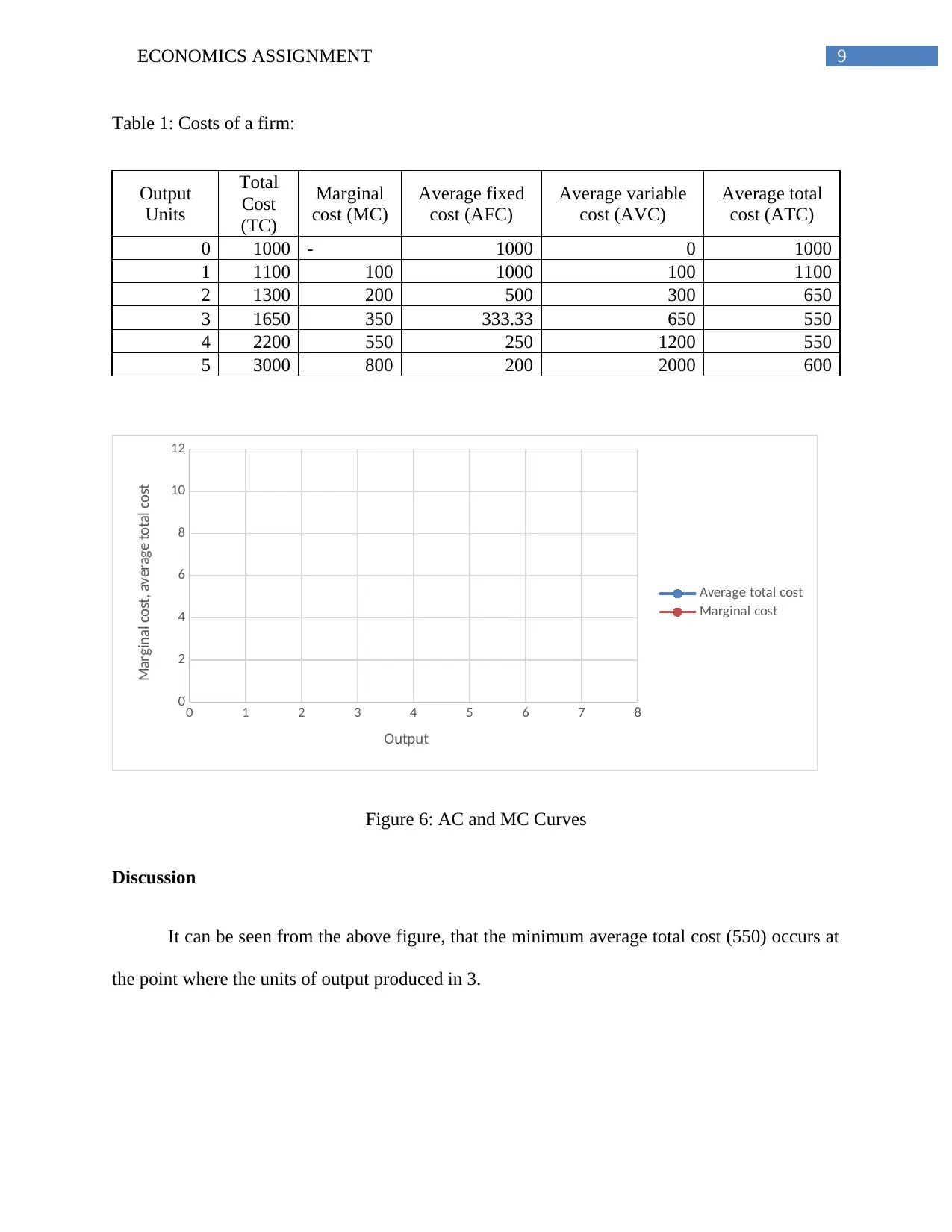

This economics assignment delves into fundamental economic concepts, starting with the interaction of demand and supply forces to determine market equilibrium. It explores how shifts in supply, such as those caused by changes in oil production, impact equilibrium prices and quantities. The assignment then focuses on the concept of price elasticity of demand, differentiating between elastic, inelastic, and unitary elastic demand curves and providing real-world examples. Finally, the assignment examines cost structures within a firm, including average fixed cost, average variable cost, and marginal cost, demonstrating how a firm aims to maximize profit or minimize costs by analyzing these cost components and determining the optimal output level. The assignment uses graphs and tables to illustrate these concepts, providing a comprehensive overview of market dynamics and cost analysis.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.