Economics Assignment - Managerial Economics, Dubai 2019

VerifiedAdded on 2022/10/17

|18

|1939

|4

Homework Assignment

AI Summary

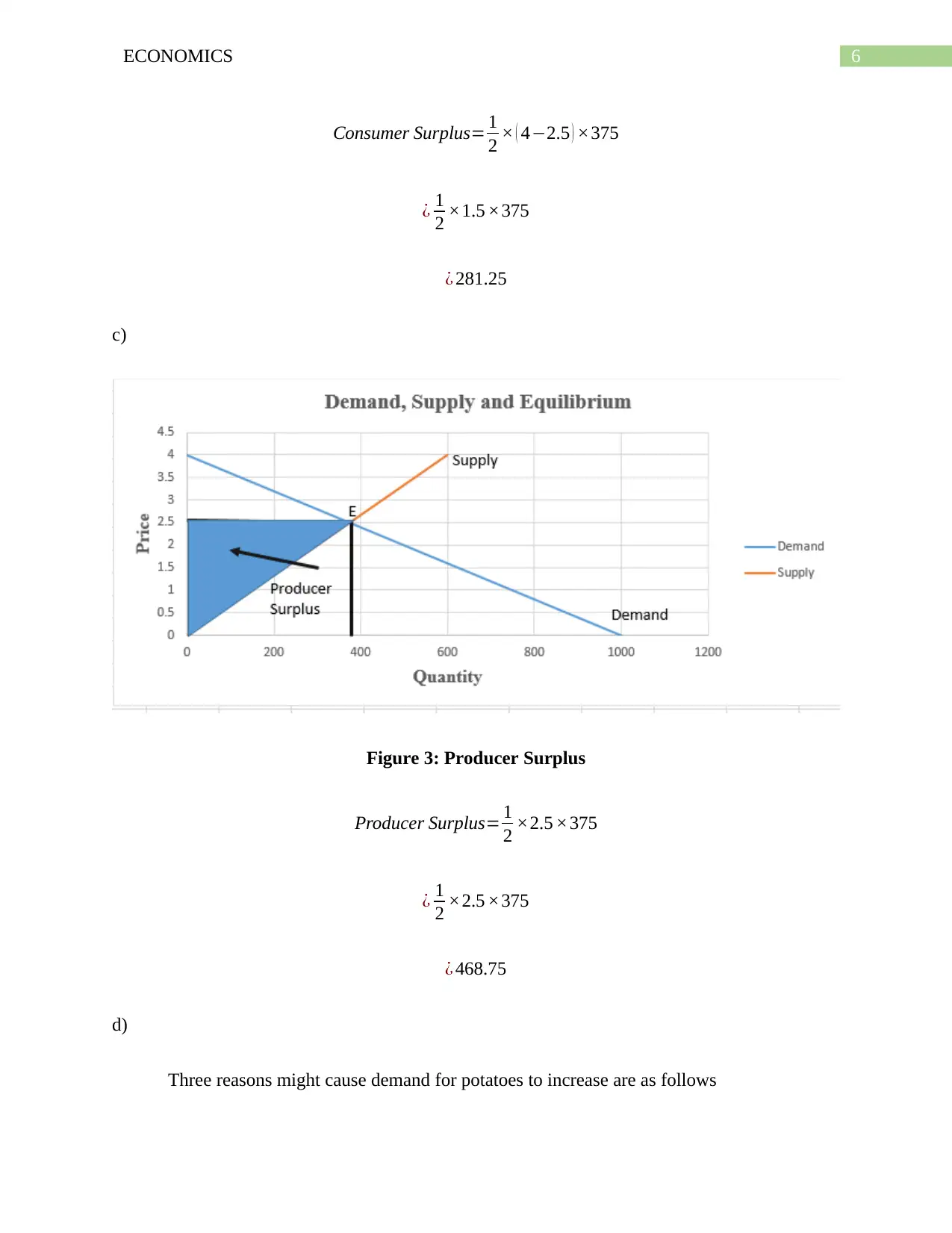

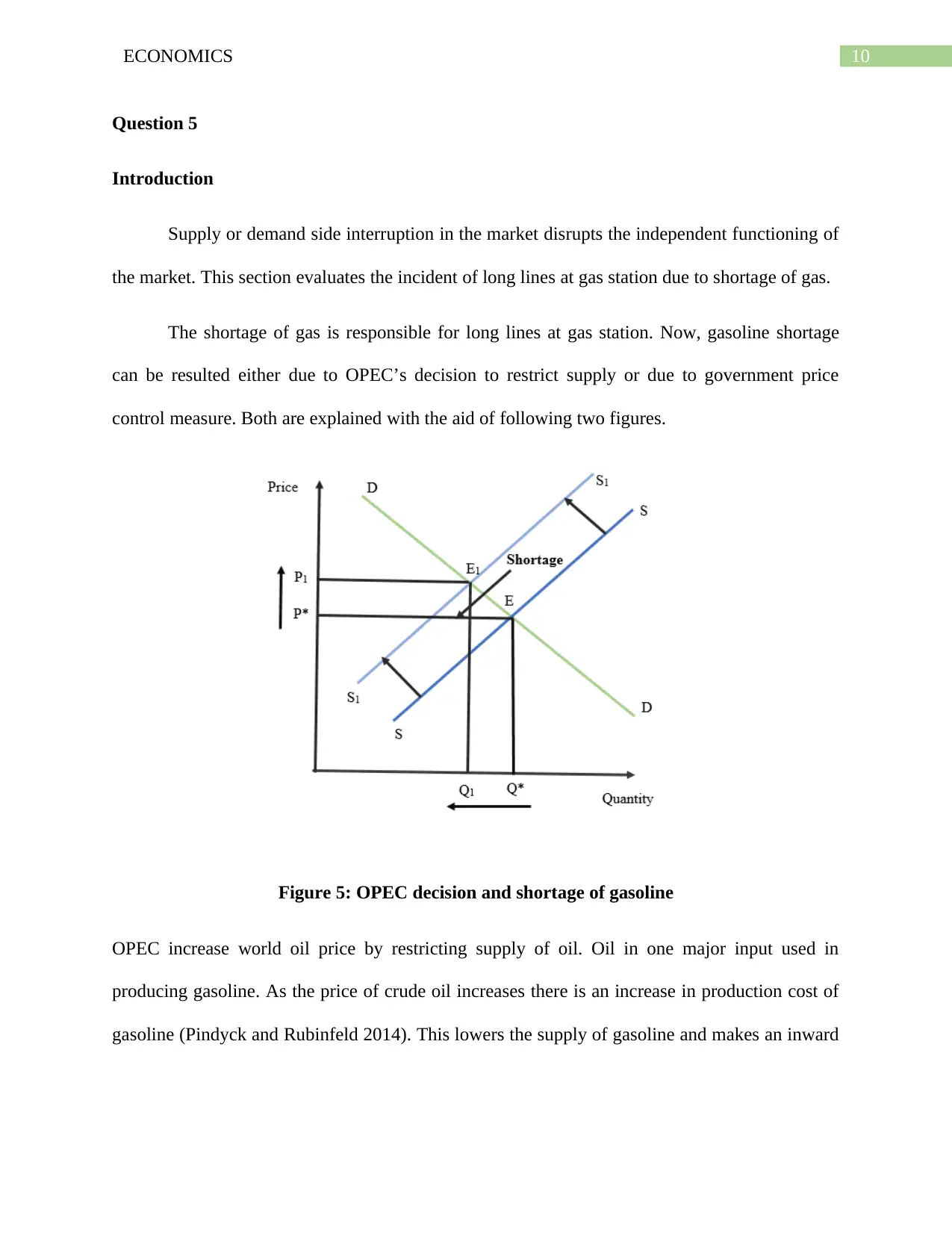

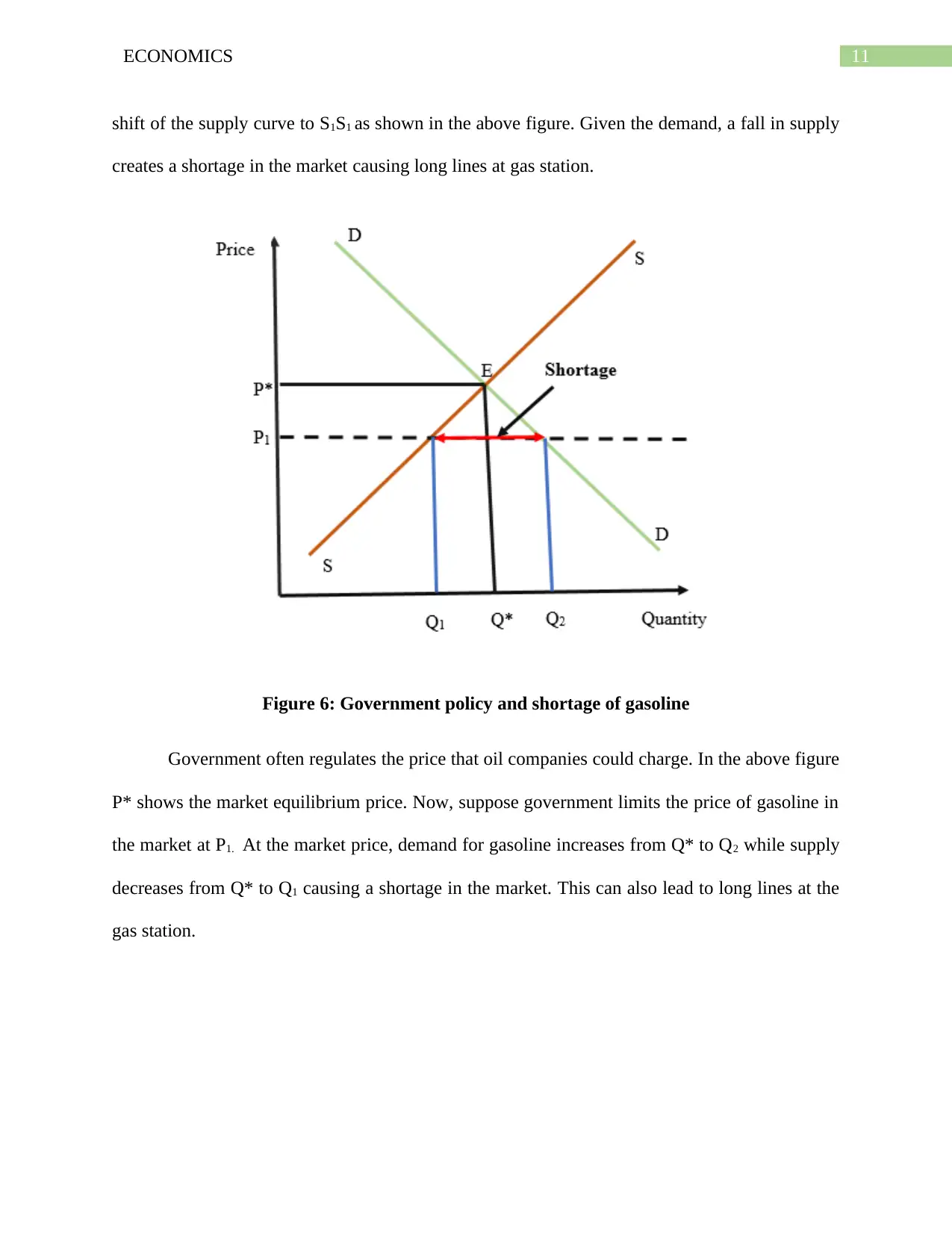

This economics assignment delves into several key concepts, including market failure, price discrimination, and monopoly. The assignment begins by defining market failure and exploring government tools to correct it, such as taxation, subsidies, regulations, and pollution permits, with a specific example of a steel plant polluting a river. The second part analyzes supply and demand dynamics in the potato market, determining equilibrium price, quantity, consumer surplus, and producer surplus. The assignment then examines the effects of a tax on cigarettes on the market for substitutes like cigars and chewing tobacco. The concept of price discrimination is discussed, focusing on how it affects consumer surplus. Finally, the assignment explores market disruptions due to supply or demand-side interruptions, using the example of gasoline shortages caused by OPEC decisions or government price controls. Section B analyzes monopoly, calculating profit-maximizing output for a bookstore and illustrating the concepts graphically. The assignment concludes by discussing the competitive firm in the long run and how market conditions affect profitability, including the impact of license fees.

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.