Economics Assignment 1: Analysis of Market Structures and Efficiency

VerifiedAdded on 2020/05/28

|23

|4439

|118

Report

AI Summary

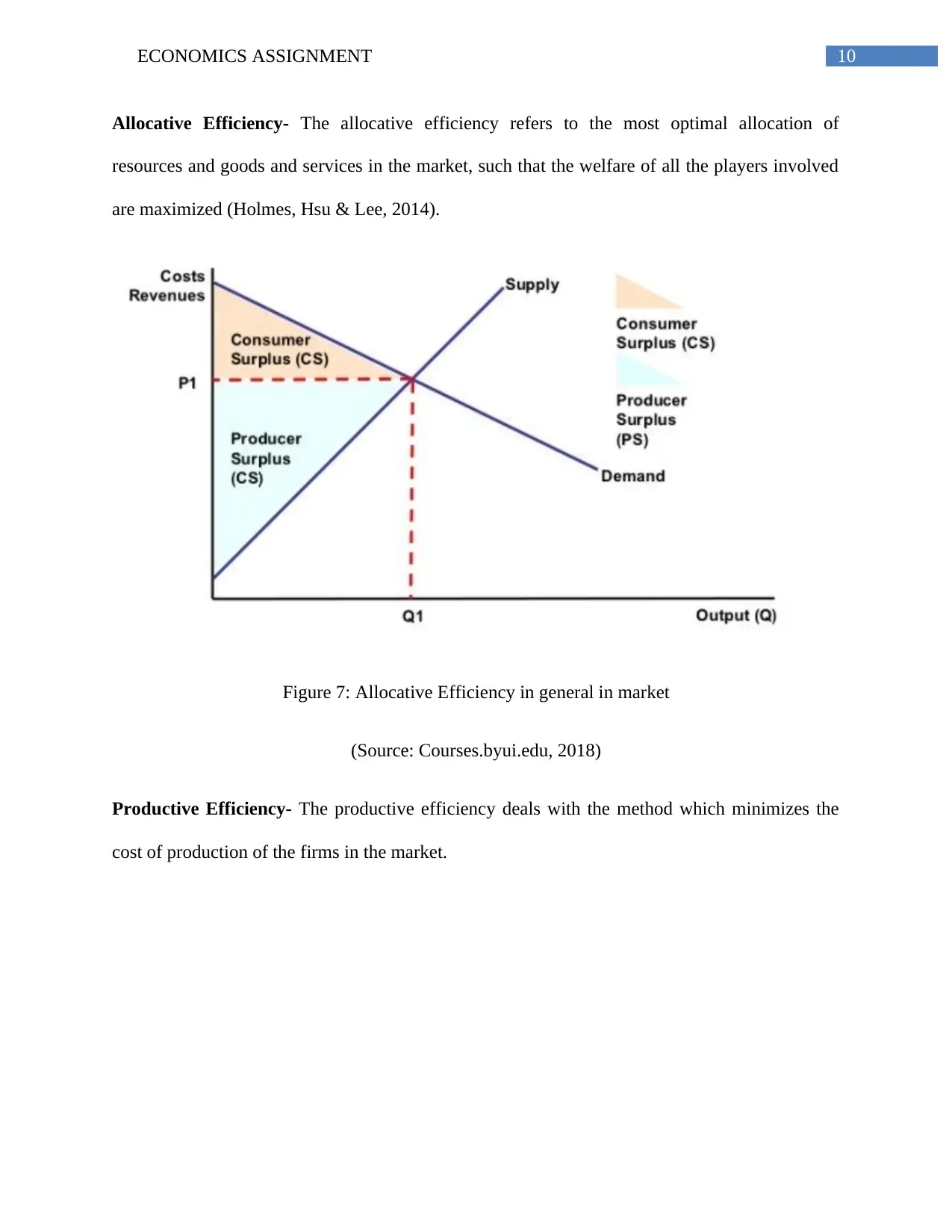

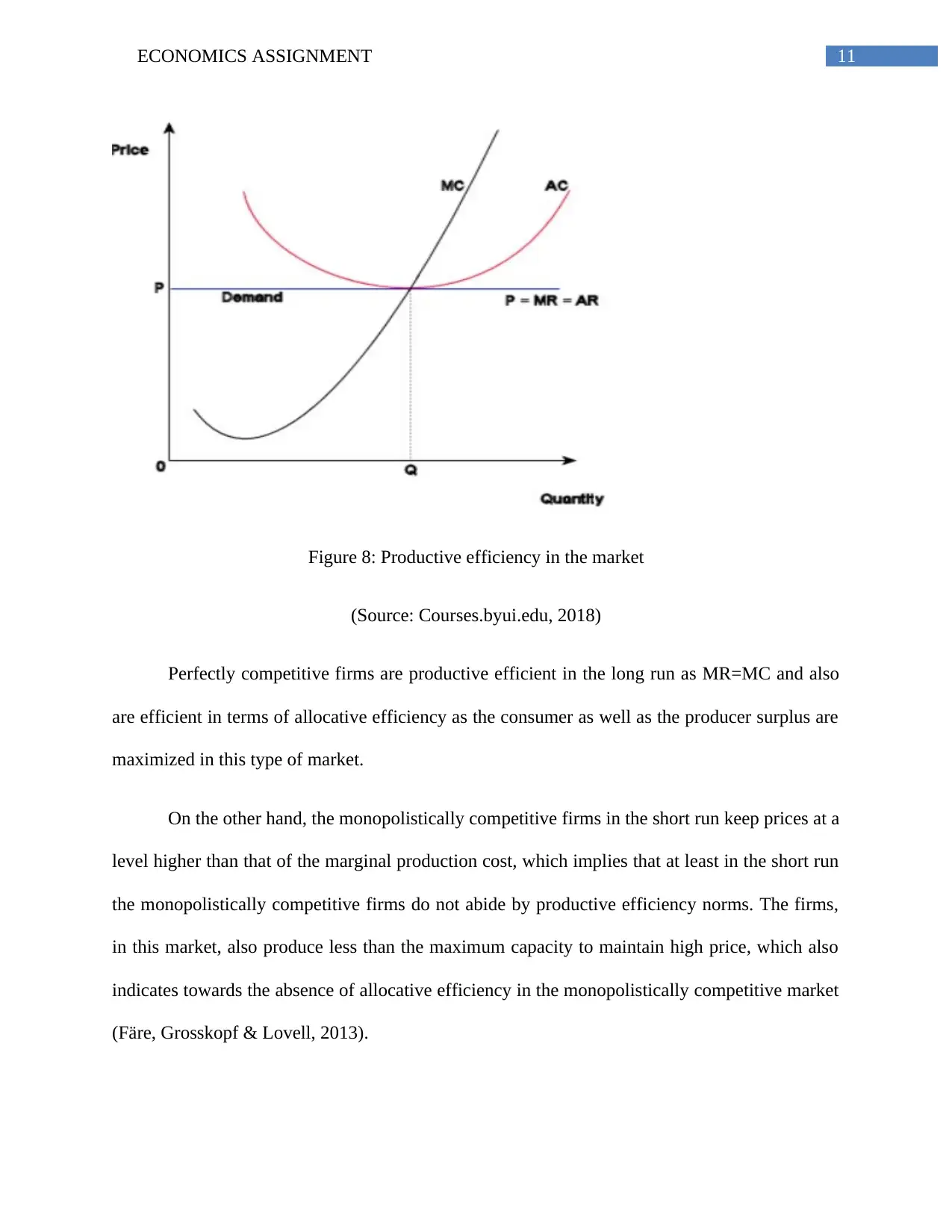

This economics assignment provides a comprehensive analysis of different market structures, focusing on perfect competition, monopolistically competitive markets, and oligopolies, with specific examples from the Australian economy. The assignment begins by differentiating between perfectly competitive and monopolistically competitive markets, highlighting key characteristics such as product type, number of players, and market power. It then delves into the equilibrium conditions in both market types, examining short-run and long-run scenarios, and illustrating these concepts with diagrams. The report further explores allocative and productive efficiencies in these markets. A significant portion of the assignment is dedicated to the oligopolistic market structure, discussing its features and providing examples of its presence in the Australian economy. The assignment concludes by examining the crisis of housing affordability in Australia, offering insights into its economic implications. Overall, the assignment offers a detailed and insightful exploration of market structures and their relevance in real-world economic scenarios.

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.